Abstract

The property income growth of urban and rural residents is an important part of the continuous increase in the disposable income of these residents, which is also inseparable from the deepening development of the financial market. After sorting out the various sources of income that affect residents’ property in the existing research and controlling regional fixed effects, based on data from 31 provinces in China, this article considers important financial factors and the process of urbanization as explanatory variables to perform panel regression on the property income of provincial residents under fixed effects and random effects. In the context of large differences in the investment environment between urban and rural areas, we further examine the effects of financial factors on the property income of urban and rural residents. Only by expanding the investment opportunities and enhancing the investment ability of the residents, can the property income of the residents, especially the rural residents, be guaranteed to grow steadily and sustainably.

1. Introduction

For the first time in October 2007, China clearly proposed the implementation goal of “creating conditions for more people to have property income”, making “property income” an important indicator of the sustainable growth of Chinese residents’ income. Property income refers to the return obtained through the provision of financial assets or tangible non-productive assets. In 2012, the 18th National People’s Congress of China proposed “to double the GDP and per capita income of urban and rural residents by 2020” as a strategic goal for future economic development. This is the so-called “Income Doubling Plan for Chinese Residents”, which is explicitly included in the Congress Report for the first time. The key targets of income doubling in the plan are the lower and middle income groups, especially rural residents.

Based on the general consensus on the importance and influencing factors of property income in various countries, combined with the characteristics of the regional gap and the large urban–rural gap in developing countries, this paper uses Chinese data to conduct a preliminary study.

According to Aldieri et al. [1,2], an abundant amount of works in the literature corroborate that good governance has a significant and positive impact on technical (for example, energy) efficiency, so government management and fiscal expenditure are essential to the sustainable development of benefits and income effect. Many countries have reached an agreement on the impact of property income in research: In the process of rapid industrialization in many European and American countries, the proportion of property income in disposable income continues to rise, which plays an important role in economic growth and income equity. It can not only stimulate innovation and investment through capital income, but also have great significance for the fairness of overall income distribution [3]. Therefore, the gap in property income and its formation mechanism should be paid attention to.

Specifically, transnational research on property income shows that the proportion of property income in residents’ disposable income has risen, but its contribution to the unfairness of disposable income is huge, several times greater than this proportion [3,4,5,6]. According to the data of Jäntti [4], although only 3% of the UK’s income was property income in 1986, it caused 10% inequality; a 6% property income share could even explain 18% of the American income gap. Becker’s [5] study of Germany also reached a consistent conclusion.

The research on wealth distribution and income distribution in Western countries is quite mature, and the macro-level and micro-individual data are so complete that they can even be compared across countries. However, on the one hand, they mostly analyze the behavioral choices of financial assets, and whether their conclusions are applicable to developing countries with large regional policy differences like China is still doubtful; on the other hand, the restricted mobility of population is not considered as a macro factor. As a result, the availability of financial markets is severely fragmented, and the location is very important.

Ensuring inclusive and sustainable growth counts a great deal for developing countries, and it is vital to highlight urban and rural perspectives. This article uses authentic data, which can be applied to analyze the overall property income. Therefore, the contribution of this article is to use reliable data to quantitatively analyze the different effects of the development of the financial market on urban and rural areas under the circumstances of restricted mobility of population and severe urban–rural segmentation. The goal is to find the bottleneck for the increase in property income of rural residents and the increase in investment participation rate.

Ning Guangjie et al. [7] reviewed the existing literature on the property income of Chinese people and observed a consistent conclusion in China: A general increase in property income may widen the total income gap.

In addition, the level of financial market development, education level, and policy systems have an impact on household financial asset selection and investment returns, which is the consensus of existing research. Based on these conclusions and consensus, this article combines the characteristics of developing countries’ regional gaps, large urban–rural gaps, especially financial market development gaps, and uses Chinese data to analyze the sources of income differences. Taking into account the economic volume of China’s provinces, the provincial panel analysis is likely to be of reference significance for the balanced income growth of developing countries in the process of industrialization.

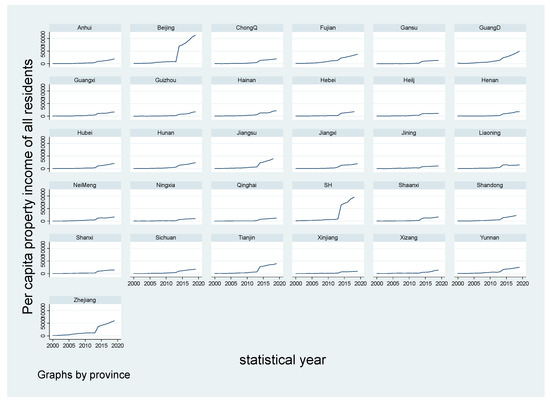

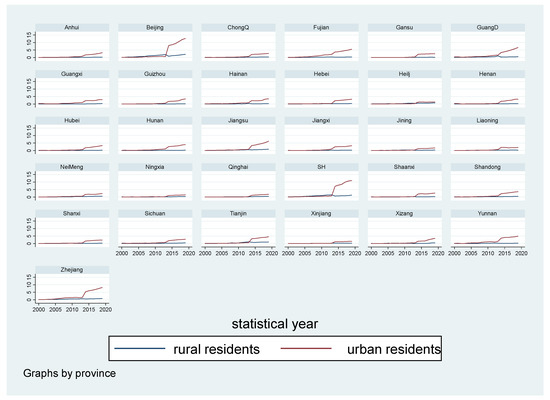

Undoubtedly, the property income of rural residents is a critical issue which the economic development and income enhancement policies should focus on. Considering its pulling effect in the sources of residents’ disposable income in recent years, we focus on analyzing the determinants and mechanism of Chinese residents’ property income, as well as the reasons for the slow growth of rural residents’ income. The per capita property income data of all residents in China’s provinces, municipalities, and autonomous regions (hereinafter referred to as “provinces” for short), from 2000 to 2019, according to the “China Statistical Yearbook”, are shown in Figure 1, and the unit is yuan RMB. For comparison, the per capita property income data of urban and rural residents in each province are shown in Figure 2, and the unit is one thousand yuan RMB. The various resident income data used in this article are actual values, that is, the value after adjusting the spatial price difference through the annual consumer price index of each province.

Figure 1.

Per capita property income of all residents in China’s provinces, from 2000 to 2019.

Figure 2.

Per capita property income of urban and rural residents in China’s provinces, from 2000 to 2019.

The growth trends of per capita property income in various provinces are completely different, reflecting the great provincial heterogeneity in economic and social development opportunities between urban and rural areas: The property incomes of urban residents in most provinces increased rapidly after 2013, while the property incomes of rural residents have grown slowly in the past 20 years. It is a common phenomenon that the asset resources and investment channels owned by rural areas confront constraints, and this phenomenon greatly hinders the narrowing of the income distribution gap and is not conducive to the overall increase of the property income of all residents in each province.

When the economy develops to a certain stage, residents’ property income is crucial to residents’ income growth. Property income sources are prone to produce a “Matthew effect” on the gap between the rich and the poor, and it is easy to breed profiteering classes and solidify the social structure; the consumer demand of the entire society is not fully realized, which is not conducive to sustained economic growth.

As the development of financial market is closely related to and mutually reinforcing the investment opportunities of residents’ property, based on the panel data of 31 provinces in mainland China, after sorting out the various sources of income that affect residents’ property in the existing research and controlling regional fixed effects, this article considers important financial factors and the process of urbanization as explanatory variables to perform panel regression on the property income of provincial residents under fixed effects and random effects, clarifying the mechanism of investment environment, financial development and various macroeconomic factors on property income. As mentioned above, China’s financial development has not achieved the original intention of policy making of “creating conditions for more people to have property income”. In order to further analyze this phenomenon mathematically, this paper uses empirical analysis to analyze the impact of financial development on Chinese residents’ property income, hoping to clarify the main factors that influence the sustainable growth of Chinese residents’ income at the present stage.

2. Literature Review: Determining Factors

Data on income and expenditure of urban and rural residents nationwide are separately derived from the Household Income and Living Conditions Survey organized and conducted by the National Bureau of Statistics and released on a quarterly basis. Residents’ disposable income refers to the sum of residents’ final consumption expenditure and savings, including both cash income and physical income. The disposable income of urban and rural residents can be divided into four categories according to the source of income: wage income, net operational income, net property income, and net transfer income. Correspondingly, based on the urban and rural population in each province, the per capita disposable income, property income, wage income, household operational income, and transfer income of all residents in each province can be obtained by calculating the weighted averages of those income indicators mentioned above.

China has been in the middle and late stage of industrialization and urbanization development for a long time, and the disposable income and wealth accumulation of residents are increasingly abundant. Therefore, in the study of income distribution in recent years, the investment opportunity and income gap between urban and rural areas are indispensable topics. Theoretical scholars have carried out relevant studies and reflections from different perspectives. We have combed through the two major influencing factors of financial investment market development and other macroeconomic structures.

2.1. The Effects of Urbanization

In the process of urbanization in China in recent decades, with economic resources and preferential policies tilted towards cities, and their software and hardware conditions continue to improve, urban residents have more property, investment opportunities, and appreciation of space. At the same time, rural residents are restricted by the “dual” economic and social structure of urban and rural areas. However, Research conclusions on the relationship between urbanization and urban–rural income gap (URIG) are divided. Therefore, Yuan Yuan et al. (2020) [8] conducted a systematic meta-regression analysis of 29 empirical studies and found that the conclusions were related to the heterogeneity indicators selected by URIG. URIG as measured by urban and rural income or consumption is positively associated with urbanization, and URIG as measured by the inequality index is negatively associated with urbanization. Wang Min et al. [9] conducted a regression analysis on the panel data of 30 provinces and regions in China, from 2005 to 2012, proving that the urbanization process did aggravate the inequality level of property income gap between urban and rural residents. The main reason lies in the difference in the degree of marketization of assets and the development of investment opportunities: The degree of marketization of rural residents’ property is not high, and the investment opportunities they are faced with are insufficient. The land-use right and homestead owned by rural residents are facing the situation of long-term idleness, lack of trading opportunities, or being traded cheaply, so their property income sources and investment channels are still narrow.

2.2. The Effects of Financial Deepening

Does financial development promote sustainable income growth? Is the function mechanism of financial deepening on the property income of residents and the gap between urban and rural areas expanded or compressed? The answers to these questions remain controversial. Finance is an important core competitiveness of the country. Financial development and economic operation are accelerating the integration at an unprecedented speed. The government’s coordination of fiscal and monetary policies to achieve the goal of national governance has become the consensus of theoretical circles and global politicians. However, academic circles have different opinions on whether the financial development promotes the sustainable growth of residents’ income.

Some studies believe that there is a Kuznets effect (inverted U-shaped relation) in financial development. Greenwood Jeremy et al. [10] established a dynamic model (the GJ model) among economic growth, financial development and income distribution, and found that wealth level was similar to the “inverted U-shaped” relationship threshold effect proposed by Simon Kuznets(1955, 1963), that is, financial development could not bring sustainable growth of resident income. Subsequently, a considerable number of scholars demonstrated the conclusion through different empirical methods, including foreign scholars such as Xu Lixin et al. [11], Beck T. et al. [12], and domestic scholars such as Zhang Qi et al. [13], Fang Wenquan et al. [14], Lin Suxu et al. [15], etc.

Some researchers believe that financial development has led to widening income gaps. Scholars holding this view believe that due to credit constraints, the poor cannot participate in financial activities, and the income distribution gap has gradually expanded and solidified into different social classes [16], financial development and income inequality have a negative linear relationship. In consideration of risk and return, financial sectors, such as banks, often give loans to the poor with a small amount and a much higher interest rate than the rich, making the poor almost unable to benefit from financial development [17]. Due to credit constraints and other limitations, the poor cannot get credit support from formal banks, but can only rely on informal network loans. Therefore, financial development only benefits the rich and disadvantages the poor, further exacerbating income inequality [18]. For developing countries, due to the absence of strong political or economic institutional guarantee, it is difficult to ensure that the financial regulatory system in place. The financial leverage effect promotes the super-rapid economic growth and accelerates the process of financial liberalization, while the poor and even the middle class have weaker anti-risk ability than the rich. Therefore, financial instability will reduce or even completely offset the positive effect of financial development on poverty alleviation [12,19].

Studies have also shown that financial development may be able to reduce the income gap. This view originated from the trickle-down effect of capital accumulation proposed by Aghion et al. [13,14,15,16,20], that is, in the long run, the wealth of the rich will benefit the poor through consumption, employment, and other aspects, thereby driving their prosperity.

In recent years, empirical research results based on cross-country data or data from a certain country or region are very abundant. The past decade has witnessed the fastest financial development in China. Will China’s financial development also affect the sustainable growth of resident income in China, just as Joseph E. Stiglitz [21] asserted that “the bigger the financial sector is in a country, the more inequality there is in that country, and the relationship between them is not accidental”.

In addition, some scholars study the effect of the hidden economy on the widening of the property income gap between urban and rural residents in China. According to the calculation by Yang Canming et al. [22], the size of China’s hidden economy was between 10.61% and 26.52% from 1978 to 2010, and it had a significant positive effect on the income gap. Due to the lack of a sound and effective income monitoring system, a large number of property income in the form of hidden economy, such as taking it into account, the situation will be more serious.

2.3. Other Influencing Factors

Financial development, urbanization process and macro environment are the major determinants of property income. The various resident income data used in this article are actual values, that is, the value after adjusting the spatial price difference through the annual consumer price index of each province.

The four sources of disposable income in urban and rural areas and related proportional indicators are the main explanatory variables of this article. The core explanatory variables are financial market development and real estate construction investment. The control variables are the level of economic development, education level of population, economic openness, urbanization level and regional fiscal factors in each province.

The mechanism of each explanatory variable and control variable: Financial market is an important channel for urban and rural residents to obtain property income. The more financial assets they have, the more property income they will obtain, such as income generated through stock, bond, insurance and fund transactions. Real estate is an extremely significant part of family property. On the one hand, in the process of urbanization, housing asset is a main way for urban and rural residents to obtain property income. On the other hand, real estate will affect the willingness of households to participate in the securities market and the pattern of asset selection. Cocco et al. [23] studied the relationship between housing price risk and asset portfolio selection and pointed out that as young investors have to invest in housing, their wealth in stocks is bound to decrease. Housing price risk has a crowding-out effect on stock investment, which explains to a certain extent the phenomenon of non-market participation in the securities market. The education level of population determines the ability endowment of residents to obtain income. The higher the education level, the stronger their ability to obtain income. Higher education is essential for residents to obtain knowledge and investment capabilities [24]. High-income, highly educated, and high-age families have a higher tendency to participate in the stock market. Li Tao [25] used the survey data of households in Guangdong Province and found that such families had higher social interactions and greater willingness to make venture capital. Due to differences in social systems, regional differences, family population composition, consumer psychology and habits, religious beliefs, etc. between urban and rural areas, the development of the capital market has significant heterogeneity in the impact of urban and rural property income. Based on country-level data, Fu Minjie [26] found that the lack of real economy scale represented by GDP had a negative effect on property income per capita. In addition, the development of the capital market represented by the per capita value of the stock market had less impact on property income per capita in rural areas than it had on urban residents. Therefore, he suggested promoting urbanization.

Since the cultural traditions and investment environment of each province are quite different and the geographical location of permanent residence has a macro-level impact on investment decisions. Therefore, this article uses dummy variables to capture the fixed effects of economic regions.

2.4. Summary

Based on the actual characteristics and existing studies, the study of property income has gradually become the focus of the research field of income distribution. The existing literature not only studies the influencing factors and mechanism of property income and its gap, but also analyzes its influence on the overall income distribution as an important driving force. However, the existing results are mainly analyzed from the perspective of the impact of property income on the income gap of the class and the property income gap between urban and rural residents. Most of these papers are based on the analysis of macro-factors such as industrial structure and financial development, and some indicators with relatively coarse statistical caliber will greatly interfere with the empirical estimation and conclusion judgment. Unlike the article written by Wang Min and Cao Runlin, which focuses on including several indicators of the financial market, to explain property income. Since the construction of financial markets is of great significance for residents to obtain information and services, it is likely to improve the interpretation of regression analysis. In addition, they only regressed the difference between the average property income of urban and rural residents, and macro factors such as GDP were only considered once. In comparison, we have analyzed the determinants of urban and rural income separately and taken into account the nonlinear effects of economic development and industrial structure changes. Combined with the indicators of multiple financial markets, this paper is able to better understand the intricate relationship between various dimensions or fields of financial development on property income distribution of urban and rural residents in a more detailed way, and it also takes into account the U-shaped, inverted U-shaped and other nonlinear effects.

3. Materials and Methods

The deepening development of financial market helps residents to make full use of assets to participate in investment by broadening income sources and investment channels, so it directly affects residents’ property income. On the premise of controlling macro factors, we should focus on studying the channels and mechanisms of financial development on residents’ property income and the urban–rural gap. Therefore, the explanatory variables considered in this paper revolve around asset investment and financial markets.

3.1. Variables

At present, the theoretical circle has not formed a unified concept of the category of property income, and there may be some differences in the statistical caliber of various data sources. According to the main statistical indicators of the “China Statistical Yearbook”, “Property income refers to the income obtained by the owners of financial assets or tangible unproductive assets in return for providing funds to other institutions or using tangible unproductive assets for their disposal”. In the “Yearbook on Urban Life and Price in China”, the Urban Social and Economic Survey Department of the National Bureau of Statistics further extends property income to “income obtained from household movable property such as bank deposits and securities, and real estate such as houses, vehicles, land and collectibles”. Its specific connotation includes the following: (1) interest income, that is, the portion of income that is higher than the principal of the deposit that the owner of the asset obtains at the pre-agreed interest rate; (2) dividend and bonus income refers to the dividend and year-end bonus distributed by the stock issuing company according to the number of shares invested; (3) insurance income refers to the net insurance income obtained by a family after deducting the insurance principal paid; and (4) rental income refers to the part of income that exceeds the original purchase price after deducting various taxes and fees paid in the rental, maintenance expenses, and other costs incurred in the rental.

The various variables at the provincial level are introduced as follows, and we convert the international trade value into RMB based on the exchange rate of the Chinese and American currencies in each year. Among them, the variable units for measuring the scale of the economy and the number of people are unified as 100 million yuan and 10,000 persons. Generally, the logarithm of the scale indexes is taken; or their absolute values are compared with GDP to generate ratios and put into the regression.

3.1.1. Explained Variables

The four types of urban and rural disposable income sources and related proportional indicators are the main explained variables. Per capita disposable income of urban residents is equal to the sum of per capita wage income/per capita operating income/per capita property income and per capita transfer income of urban residents. The same goes for per capita disposable income of rural residents.

3.1.2. Core Explanatory Variables

- Development of Financial Markets

Based on the above definition, this article uses three aspects of data, namely interest rate market, stock market, and insurance market, to fully reflect the scale of the financial investment market as much as possible. The financial asset market is an important channel for urban and rural residents to obtain property income. The more financial assets they own, the more property income they can obtain, such as income generated through stocks, bonds, insurance and fund transactions. Due to the unbalanced allocation of resources in the financial market between urban and rural areas and the gap in financial awareness among urban and rural residents, urban residents have far greater opportunities and ability to obtain property income from the financial market than rural residents, and their marginal saving propensity is lower than rural residents; while rural residents are restricted by investment channels in the financial market, interest income mainly depends on savings and is affected by factors such as social security; its marginal saving propensity is greater than that of urban residents. Therefore, this article expects that savings will narrow the property income gap between urban and rural residents, while stocks and insurance will significantly promote urban property income.

The units of other per-capita and ratio indicators are different. For example, the units of insurance density and insurance depth in each province extracted by the “China Financial Statistics Yearbook” are yuan per person and percentage, respectively. Insurance density refers to the amount of average insurance premiums for permanent residents in a defined statistical area. It marks the degree of development of insurance business in the region, and also reflects the economic development of the region and the strength of people’s insurance awareness. Insurance depth refers to the ratio of premium income to the gross domestic product (GDP) of a place and reflects the position of the insurance industry in that place in the entire national economy. The depth of insurance depends on the overall economic development of a country and the speed of the insurance industry.

- 2.

- Real estate construction investment

In the process of urbanization, housing assets are an important way for urban and rural residents to obtain property income, especially for urban residents. The more housing assets they own, the more property income they obtain. Since there are no authoritative data to count the real situation of the housing assets of urban and rural residents in China, this paper chooses real estate development investment as a substitute variable and measures the relative scale of real estate development, according to its ratio to GDP. Considering that there is a construction cycle in the real estate development as an asset entering the transaction or leasing market, so the use of lag items reflects the lag effect. Theoretically, the greater the investment demand of urban and rural residents for real estate, the larger the area of commercial housing sold will be, and the stronger the protection of getting property income from the real estate market will be. At present, the main group of China’s commercial housing investment demand is mainly urban residents and college graduates with urban household registration. Therefore, urban residents are expected to be the main income beneficiaries.

3.1.3. Control Variables

The property incomes of urban and rural residents are also affected by related macroeconomic characteristics. In order to obtain a more robust estimation result, this paper also introduces a set of economic characteristic variables as control variables, mainly including the following categories.

(1) One is the level of economic development of each province. The higher the level of economic development, the more active the economic factors in the province, and the more property income residents will obtain [1]. This is because the degree of a place’s wealth and the development of the tertiary industry will have a direct impact on the income of residents, and indirectly affect the opportunities to obtain property income. Therefore, we use the polynomial of per capita GDP (lnpcGDP) and the ratio of tertiary industry to GDP (Rtertiary) to estimate the nonlinear effect of this factor on residents’ property income.

(2) The second is the education level of the population, which determines the investment endowment. Higher education is essential for residents to acquire knowledge and investment capabilities, especially in emerging economies like China. The overall education level of the population, especially high-quality talents, is an important source of heterogeneity for provincial development. This article selects the proportion of people with college degree or above in the total population (Rcollege) to measure the education level of residents in each province.

(3) In addition, when analyzing the income determination mechanism under the framework of an open economy, the higher the degree of economic openness, the more opportunities for residents to obtain property income. Therefore, this article incorporates the proportion of import and export trade volume of local enterprises operating in various provinces to GDP (Rtrade_GDP), that is, the degree of dependence on foreign trade as a measure of the degree of openness of foreign trade into the analysis. A local enterprise refers to an enterprise whose main business activities and business activities of a corporate legal person are located in the local office. It is different from the source of purchase and the geographical scope of business operations, namely the destination.

(4) Population urbanization rate (Rurban) is the ratio between urban population and total population. In the interpretation of statistical indicators in the “China Statistical Yearbook”, urban population refers to all permanent residents living in urban areas. The higher the urbanization, the higher the level of property income expected for all residents [27]. The permanent population refers to the permanent population who often lives at home for more than 6 months throughout the year, and also includes the floating population living in the city where they are located. The economy and life of the permanent population are integrated with the household. Although the employees who work outside the home for more than 6 months, their income is mainly taken home, the economy is connected to the household, and these people are still regarded as permanent residents of the family.

(5) Fiscal factors reveal the influence of the government. We use the percentage of general fiscal budget revenue and expenditure to GDP (Rgov_GDP) to control the influence of government participation in economic activities. The general fiscal budget revenue refers to the fiscal revenue obtained by a certain level of government through collection (excluding transfer payments) and included in the public budget management. It is also called local disposable fiscal revenue, which can be divided into tax and non-tax revenue: It is a small-caliber fiscal revenue, which is the fiscal funds that the local government can use at will, within a certain period of time.

The higher the value of this indicator, the more economic resources and newly created value the government participates in the allocation, and the higher the government’s intervention in the economic system [19,28].

3.2. Model Construction

Based on the previous theoretical analysis and variable selection instructions, this article builds a panel data regression model for empirical analysis and a set model form in Formula (1):

where i is for region, and t is for time; PropertyIncit represents the annual property income of total residents or urban and rural residents in each province; indicates the level of population urbanization, that is, the proportion of urban permanent residents in the total population; represents financial development; β is the core explanatory variable coefficient; the vector is a set of control variables; γ is the coefficient vector of the control explanatory variable; and αi means that there is an individual effect in the assumed model. As for whether the model has a bidirectional fixed effect, it can be verified by a correlation test. Moreover, εit is the disturbance term. The empirical model is as follows.

In the above equation, the explained variable PropertyIncit includes per capita property income. In the following regression, three property income variables are considered: per capita property income of residents, per capita property income of urban residents, and per capita property income of rural residents.

The data sources of the above variables are as follows: For financial indicators related to interest rate markets, stock markets, and insurance, the data come from the “China Finance Yearbook”, which is an annual publication supervised by the People’s Bank of China, compiled by the China Institute of Finance and the People’s Bank of China Institute of Finance. The content is based on the daily operation data of China’s financial industry—banking, securities, insurance, and other commercial financial institutions in the previous year—which are open, authoritative, and comparable across regions.

The income data of various provinces and urban and rural residents come from the Household Income and Living Conditions Survey organized and conducted by the National Bureau of Statistics. According to the basic data of the nationwide sample survey of over 100,000 households, the National Bureau of Statistics calculates the income level of each region weighted according to the number of households represented by each sample household and releases the income level quarterly.

The macro explanatory variables come from the “China Statistical Yearbook” compiled by the National Bureau of Statistics. The data are summarized from the daily statistical surveys of the provinces’ and cities’ statistical bureaus, in the areas under their jurisdiction. The statistical calibers are consistent, so they are comparable across the country. The “China Statistical Yearbook” is consistent with the provincial statistical yearbooks issued by various provinces.

Household financial investment and income based on sample surveys are indeed an important direction for countries to study household finance. For developing countries, survey data are emerging but need to be accumulated and improved. The overall formation mechanism and impact effect are still very essential. Taking China as an example, the commonly used survey data limit empirical analysis due to missing factors. Subject to the investigation and disclosure of micro data on Chinese residents’ income, it is extremely difficult to quantitatively analyze the influencing factors of property income in general. The widely used and credible survey data include the China Household Finance Survey (CHFS) by the Southwestern University of Finance and Economics, the Survey of Consumer Finance by Tsinghua University, but the CHFS data, in recent years, have not been made public. The Chinese General Social Survey (CGSS) data of Renmin University of China keeps geographic information confidential and thus cannot control the important factor of geographic location.

The meanings, names and descriptive statistics of various variables in the full sample are shown in Table 1. The actual variables used are not limited to these, the specific content can be seen in the regression results. The value of per capita property income of rural residents (rpcProInc) is obviously smaller than that of urban residents (upcProInc), and its proportion in the disposable income of rural residents is also smaller than that of the latter in the disposable income of urban residents. The provincial finance development levels are very different, especially the relative sizes of the stock market (Rstock_GDP); they have a large standard deviation; and the differences in the scale or depth of financial investment reflected by other deposit, insurance, and real estate investment indicators are slightly smaller. Huge differences in import or export dependence (Rimport and Rexport) reflect the degree of foreign trade openness of each province; meanwhile, the difference in the industrial structure is not large, and the tertiary industry accounts for an average of 43.39% of GDP.

Table 1.

Descriptive statistics of variables at the provincial level.

Based on the benchmark regression equation, we first perform a preliminary panel regression on the income level of residents’ property. To avoid the problem of heteroscedasticity, this paper has carried out logarithmic processing on the absolute value of each index. In terms of the standard deviation of the variables, the cross-sectional difference is very large, so the regional fixed effects are controlled in the regression. The specific selection of the fixed effect model(FE model)or random effect model (RE model) is based on the results of the Hausman test, and these results are indicated in the third row of Table 2.

Table 2.

The influential factor of property income of all residents, at the provincial level.

As shown in Table 2, Column (1) shows the regression results of per capita property income of all residents in each province, while Column (2) and Column (3) show the regression results of upcProInc and rpcProInc, respectively. In Column (1), the result of the Hausman test is chi2(12) = 45.29, and the probability of being greater than chi2 is 0, so we choose the FE model. From the perspective of R-squared within the group, the goodness of fit is relatively high. The economic level represented by lnpcGDP presents a “U-shaped” effect on the per capita property income of all residents. According to the regression coefficient, with other conditions fixed, when lnpcGDP exceeds the inflection point 8.8524, that is, when pcGDP exceeds 6991.2 yuan (the actual value based on 2000), it will have an increasing effect on the per capita property income of all residents. Most provinces surpassed this inflection point in 2002 or earlier, while the southwest region (ecozone = 5) was a few years later, for example, Guizhou Province surpassed in 2007.

Since the quadratic term of the ratio of deposits of all financial institutions to GDP (Rdep_GDP) is significantly positive, the relative scale of deposits in each province has a positive effect. For every increase in Rdep_GDP by one unit (i.e., one percentage point), lnpcProInc increases by 0.1279. The financial and service industries are very essential to increase revenue. For every 1% increase in Rtertiary, lnpcProInc increases by 6.7130%. In addition, with the development of urbanization, the real estate market is booming, and the rental and sale of housing are conducive to the improvement of property income of owners, while the investment options of buyers and renters are squeezed out, as a result of which, the rate of return on investment declines. China’s population urbanization process has an inverted U-shaped effect on pcProInc. When Rurban continues to grow and exceeds the percentage point of 67.14, the negative effect turns out to be greater than the positive, resulting in a total negative effect on residents’ property income. At present, highly developed regions, such as Beijing, Tianjin, Shanghai, Jiangsu, and Zhejiang, have exceeded the critical value in recent years. Of course, the specific mechanism of population urbanization on income still needs to be verified by the data of individual financial investment behavior.

The regression results of Column (2) on lnupcProInc are similar to those in Column (1) and have a greater impact: The larger coefficients of Rurban and Rtertiary indicate that population migration and the development of financial and service industries mainly affect the income of urban residents. In addition, insurance depth (InsureDepth), stock market value (Rstock_GDP) and public fiscal expenditure (Rgovexp) have more obvious effects on urban residents. In contrast, in the regression of Column (3) to lnrpcProInc, these main explanatory variables are not significant except for the urbanization level of the population and the proportion of the tertiary industry, which shows that rural residents have limited benefit from the current financial market development. The R-squared within the group is only about 0.6, so in order to clarify the decision mechanism of urban and rural property income, we will add other indicators for detailed analysis.

When analyzing the property income of urban and rural residents separately, in order to consider the possible nonlinear effects of the financial market and macro control variables, the quadratic terms of various proportions and logarithmic values are included in the panel regression. To further examine the robustness of the results, this article uses the lagged terms of the main variables to reflect the lagged effect on investment returns, which is also conducive to alleviating possible endogenous problems.

The regression results of upcProInc are shown in Table 3. Columns (1)–(3) takes into account the role of the economic region and adopts the RE model according to the results of the Hausman test, and Columns (4) and (5) use the FE model to control the fixed effects of each province. While the goodness of fit is greatly improved after adjusting the variable form, the conclusions drawn by Table 2 are still very robust. In addition, the level of education Rcollege has a significant positive effect. Moreover, lnInsureDens has a U-shaped effect. In the short term, although insurance investment squeezes disposable funds, it is conducive to protecting property and asset returns in the long run. Interestingly, real estate construction has an inverted U-shaped effect on urban residents’ property income. According to the estimated coefficient in Column (4), when the ratio of real estate construction investment to GDP in the previous year is higher than 0.2614, it is not conducive to upcProInc.

Table 3.

The influential factors of property income of urban residents.

From the perspective of economic region, the property income of urban residents in the northwest region (ecozone = 6) is obviously lower than that in other regions, and lnupcProInc is 1 unit lower on average than that in North China (ecozone = 1).

The regression results of rpcProInc are shown in Table 4. Columns (1) and (2) take into account the role of the economic region and adopts the RE model according to the results of the Hausman test, and Columns (3) and (4) use the FE model to control the fixed effects of each province. After adjusting the variable form and using rural per capita income as the control variable, the overall significance of the variable is greatly improved. Like urban areas, lnrpcInc and Rgov_GDP have produced U-shaped and positive effects, respectively. Deposits are still very important for rural investment, while the overall stock and insurance markets in the provinces play no significant role in the development. As long as the ratio of real estate construction investment to GDP in the previous year is higher than 0.26, it will help to raise the rpcProInc. Moreover, according to the estimated coefficient of Rtertiary, the effect of tertiary industry development will be positive all the time. In terms of the fixed effects of economic regions, the property income of rural residents in South China (ecozone = 4) and Northwest China (ecozone = 6) is significantly lower than that in North China (ecozone = 1).

Table 4.

The influential factors of property income of rural residents.

4. Conclusions

Based on the results of rich empirical analysis, we can get the source of residents’ property income growth. The national production level represented by per capita GDP has a U-shaped effect on residents’ income. As the per capita GDP of various provinces and cities exceeds the inflection point of 6991.2 yuan, economic growth will promote the growth of residents’ property income. Therefore, the most fundamental way for residents to increase income is development, which is conducive to residents’ income and asset accumulation.

The development of financial markets requires attention to rural areas. Compared with urban residents, rural residents have not yet benefited significantly from the development of the stock and insurance markets. They still rely mainly on savings investments and benefit from real estate construction investments. Therefore, it is necessary to improve the accessibility, investment information, and investment willingness of various financial markets in rural areas. At the same time, the urgent task is to build and perfect the leasing market of rural land and real estate, accelerating the flow efficiency and improving the utilization rate.

Pay attention to the long-term impact of different investments on the disposable income of residents. Stocks and insurance investments have a U-shaped effect on property income. Although these investments squeeze disposable funds in the short-term, they can help ensure property and increase returns in the long run. The overheated real estate market, by contrast, has benefited those with high wealth, but high housing price and excessive speculative trading in China’s urban areas are detrimental to ensuring overall income and quality of life for urban residents.

As mentioned above, reducing the property income gap is conducive to reducing the disposable income gap. Various policies are needed to increase the property income of residents, especially rural residents.

According to the results of this article’s analysis of urban and rural areas, the most fundamental solution to increase residents’ property income is to increase their total income. Bank deposits, insurance funds, and stocks are the three major financial assets of households, and the selection rate of Chinese households for bank deposits remains high. This is mainly because the overall level of disposable income is not high enough. Families tend to choose very low-risk investment methods out of the motivation of providing for the elderly, preventing major diseases and children’s education.

The second is the development of financial markets. The gap in the development of urban and rural financial markets urgently calls for breaking the urban–rural division system and removing barriers to the flow of population, capital, and information. Relevant departments need to speed up financial reforms, establish a multi-level capital market, launch more low- and medium-risk investment products, and strengthen review and supervision. The approval and supervision should be stricter to prevent the recurrence of such incidents as the successive closure of P2P lending platforms. At present, financial products with good matching of security, liquidity, and profitability in my country’s financial market are still insufficient, and there is a lack of relatively suitable investment products. We should encourage the design of various financial instruments and financial products in line with China’s national conditions, so that different families can obtain financial instruments suitable for themselves through the financial market.

The third is to increase investment in education and widely popularize financial knowledge. Cultivating financial market participants with diversified financial market participation is conducive to the improvement of financial market efficiency. Therefore, by strengthening financial education and cultivating financial awareness, we can change the traditional financial concepts of Chinese residents, especially to help rural residents understand risk assets correctly and reasonably and choose household financial assets reasonably. We need to encourage families to participate extensively in various possible investment projects, to enhance their welfare. Moreover, at the micro level, demand guidance, investor education, and social norms should be provided to families, so as to actively guide the orderly distribution of household savings to other investment channels.

Author Contributions

Conceptualization, X.P.; methodology, X.P. and Z.L.; software, H.L.; validation, H.L. and Z.L.; formal analysis, X.P.; investigation, X.P. and J.F.; resources, H.L. and J.F.; data curation, J.F.; writing—original draft preparation, X.P.; writing—review and editing, X.P. and Z.L.; visualization, H.L.; supervision, H.L. and X.P.; project administration, X.P.; funding acquisition, X.P. and Z.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by the General Program of National Natural Science Foundation of China, “Research on Measurement and Correction Mechanisms of Distribution Effect of Fiscal Policies on Residents’ Income”, with grant number 71573194, and the Youth Project of the Humanities and Social Sciences Fund of the Ministry of Education of China, “Research on the Impact of Technological Innovation on Employment Inequality in China and Countermeasures--Based on the perspective of labor market segmentation” with grant number 19YJC790108, and the National Science Foundation of Hunan Province of China, “Research on the Impact of Agricultural Technology on Agricultural Productivity Volatility under the Background of Climate Change with project number 2020JJ5263, and Educational Commission of Hunan Province of China, “Research on the Impact and Mechanism of the Structural Change of Manufacturing Employment Skills on Human Capital Investment in Rural Areas” with project number 20B305.

Institutional Review Board Statement

No applicable.

Informed Consent Statement

No applicable.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: http://www.pbc.gov.cn/rmyh/105223/105413/index.html (accessed on 1 March 2021), https://www.yearbookchina.com/navipage-n2006100046000029.html (accessed on 1 March 2021).

Acknowledgments

We gratefully acknowledge the support of the Department of Public Finance and Taxation, Department of International Economics and Trade, and the Centre of Finance Research, School of Economics and Management, Wuhan University.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Aldieri, L.; Makkonen, T.; Vinci, C.P. Environmental knowledge spillovers and productivity: A patent analysis for large international firms in the energy, water and land resources fields. Resour. Policy 2020, 69, 7. [Google Scholar] [CrossRef]

- Aldieri, L.; Kotsemir, M.; Vinci, C.P. The role of environmental innovation through the technological proximity in the implementation of the sustainable development. Bus. Strategy Env. 2020, 29, 493–502. [Google Scholar] [CrossRef]

- Frassdorf, A.; Grabka, M.M.; Schwarze, J. The impact of household capital income on income inequality-a factor decomposition analysis for the UK, Germany and the USA. J. Econ. Inequal. 2011, 9, 35–56. [Google Scholar] [CrossRef]

- Jantti, M. Inequality in five countries in the 1980s: The role of demographic shifts, markets and government policies. Economica 1997, 64, 415–440. [Google Scholar] [CrossRef]

- Becker, I. The personal distribution of income in Germany—A decomposition analysis of income sources. Jahrb. Fur Natl. Und Stat. 2000, 220, 400–418. [Google Scholar]

- Gustafsson, B.; Li, S.; Wei, Z. The distribution of wealth in urban China and in China as a whole in 1995. Rev. Income Wealth 2006, 52, 173–188. [Google Scholar] [CrossRef]

- Ning, G.; Jiang, Y. Review of research on property income in China. Econ. Political Stud. Eps 2018, 6, 221–235. [Google Scholar] [CrossRef]

- Yuan, Y.; Wang, M.; Zhu, Y.; Huang, X.; Xiong, X. Urbanization’s effects on the urban-rural income gap in China: A meta-regression analysis. Land Use Policy 2020, 99. [Google Scholar] [CrossRef]

- Wang, M.; Cao, R. Research on tax distribution reform, Urbanization process and Local Tax System Improvement. Public Financ. Res. 2015, 8, 78–83. [Google Scholar] [CrossRef]

- Jeremy, G.; Boyan, J. Financial development, growth and the distribution of income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar]

- Xu, L.; Clarke, G.; Zou, H.F. Finance and Income Inequality: Test of Alternative Theories; The World Bank: Washington, DC, USA, 2003. [Google Scholar]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, Inequality, and Poverty: Cross-Country Evidence; National Bureau of Economic Research: Cambridge, MA, USA, 2004. [Google Scholar]

- Zhang, Q.; Liu, M.; Tao, R. Growth of financial intermediation and urban-rural income gap in China. China J. Financ. 2003. Available online: http://www.cngdsz.net/d/img/upfiles_1/20044321832.doc (accessed on 1 March 2021).

- Fang, W. An empirical analysis of the relationship between Income gap and financial development in China. Jianghuai Trib. 2006, 1, 30–35. [Google Scholar]

- Lin, S. Research on the Relationship between Financial Development and Income inequality in China. Financ. Account. Mon. 2015, 11, 25–28. [Google Scholar] [CrossRef]

- Galor, O.; Zeira, J. Income Distribution and Macroeconomics. Rev. Econ. Stud. 1993, 60, 35–52. [Google Scholar] [CrossRef]

- Javier, C.B.G.; Korman, R.F. Financial Development and the Distribution of Income in Latin America and the Caribbean. IZA Discussion Paper No. 3796 2008. Well Being Soc. Policy 2009, 5, 1–18. [Google Scholar]

- Bourguignon, F.; Verdier, T. Is financial openness bad for education? A political economy perspective on development. Eur. Econ. Rev. 2000, 44, 891–903. [Google Scholar] [CrossRef]

- Jeanneney, S.G.; Kpodar, K. Financial Development and Poverty Reduction: Can There be a Benefit without a Cost? J. Dev. Stud. 2011, 47, 143–163. [Google Scholar] [CrossRef]

- Aghion, P.; Bolton, P. A Theory of Trickle-Down Growth and Development. Rev. Econ. Stud. 1997, 64, 151–172. [Google Scholar] [CrossRef]

- Stiglitz, J.E. The Price of Inequality; Penguin Book: London, UK, 2012; pp. 20–22. [Google Scholar]

- Canming, Y.; Qunli, S. The Decomposition of Income Gap and Inequality in Chinese Residents—Based on the data of 2010 questionnaire survey. Financ. Trade Econ. 2011, 11, 51–56. [Google Scholar] [CrossRef]

- Cocco, J.F.; Gomes, F.J.; Maenhout, P.J. Consumption and portfolio choice over the life cycle. Rev. Financ. Stud. 2005, 18, 491–533. [Google Scholar] [CrossRef]

- Wang, M.; Cao, R.L. An empirical Study on the impact of Urbanization on the Property income gap between Urban and rural residents in China. Macroeconomics 2015, 3, 76–84. [Google Scholar] [CrossRef]

- Li, T. Social Interaction, Trust and Stock Market Participation. Econ. Res. J. 2006, 1, 34–45. [Google Scholar]

- Fu, M.J. What affects residents’ property income? On the primary function of urbanization. Res. Econ. Manag. 2010, 10, 18–23. [Google Scholar] [CrossRef]

- Zhou, A.H.; Yan, Z.H.; Cao, H.J. Analysis of the mechanism of action of public education expenditure on residents’ property income. Hunan Soc. Sci. 2018, 4, 135–145. [Google Scholar]

- Huang, S.M. A comparative study of Chinese-style local tax sharing system. J. Jiangxi Norm. Univ. Philos. Soc. Sci. Ed. 2017, 50, 65–73. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).