Where to Go with Corporate Sustainability? Opening Paths for Sustainable Businesses through the Collaboration between Universities, Governments, and Organizations

,

,  ,

,  and

and

Abstract

1. Introduction

2. Research Method

3. Scientific–Technical Scenario

3.1. Scientific Scenario

3.1.1. Maturity Level of Scientific Development

3.1.2. Major Authors

3.1.3. Scientific Government Efforts

3.1.4. Major Scientific Journals

3.1.5. Hot Topics and Timeline Overview

3.2. Technical Scenario

3.2.1. World Economic Forum

3.2.2. Global Compact and SDGs

3.2.3. Global Reporting Initiative

3.2.4. Dow Jones Sustainability Index

3.2.5. Technical Government Efforts

3.2.6. Patents and Innovations for CS Development

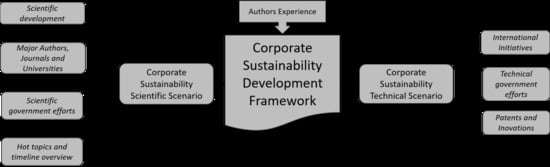

4. Corporate Sustainability Framework

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Whiteman, G.; Walker, B.; Perego, P. Planetary Boundaries: Ecological Foundations for Corporate Sustainability. J. Manag. Stud. 2013, 50, 307–336. [Google Scholar] [CrossRef]

- Keeble, B.R. The Brundtland Report: “Our Common Future”. Med. War 1988, 4, 17–25. [Google Scholar] [CrossRef]

- Kuhlman, T.; Farrington, J. What is sustainability? Sustainability 2010, 2, 3436–3448. [Google Scholar] [CrossRef]

- Aras, G.; Crowther, D. Governance and sustainability: An investigation into the relationship between corporate governance and corporate sustainability. Manag. Decis. 2008, 46, 433–448. [Google Scholar] [CrossRef]

- Hahn, T.; Figge, F. Beyond the Bounded Instrumentality in Current Corporate Sustainability Research: Toward an Inclusive Notion of Profitability. J. Bus. Ethics 2011, 104, 325–345. [Google Scholar] [CrossRef]

- Currie, G.; Knights, D.; Starkey, K. Introduction: A post-crisis critical reflection on business schools. Br. J. Manag. 2010, 21, s1–s5. [Google Scholar] [CrossRef]

- Cullen, J.G. Educating Business Students About Sustainability: A Bibliometric Review of Current Trends and Research Needs. J. Bus. Ethics 2017, 145, 429–439. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Earth Overshoot Day. Available online: https://www.overshootday.org/ (accessed on 18 December 2020).

- Milne, M.J.; Gray, R. W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Lo, S.F.; Sheu, H.J. Is corporate sustainability a value-increasing strategy for business? Corp. Gov. Int. Rev. 2007, 15, 345–358. [Google Scholar] [CrossRef]

- Elkington, J. Accounting for the Triple Bottom Line. Meas. Bus. Excell. 1997, 2, 18–22. [Google Scholar] [CrossRef]

- Lee, D.D.; Faff, R.W. Corporate sustainability performance and idiosyncratic risk: A global perspective. Financ. Rev. 2009, 44, 213–237. [Google Scholar] [CrossRef]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Bos-brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strateg. Environ. 2009, 19, 417–435. [Google Scholar] [CrossRef]

- UN Global Compact. United Nations Global Compact Progress Report 2018; United Nations: New York, NY, USA, 2018. [Google Scholar]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management. Account. Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Lee, K.H.; Farzipoor Saen, R.; Farzipoor, R. Measuring corporate sustainability management: A data envelopment analysis approach. Int. J. Prod. Econ. 2012, 140, 219–226. [Google Scholar] [CrossRef]

- Talbot, D.; Boiral, O. GHG reporting and impression management: An assessment of sustainability reports from the energy sector. J. Bus. Ethics 2018, 147, 367–383. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef]

- Feil, A.A.; de Quevedo, D.M.; Schreiber, D. An analysis of the sustainability index of micro- and small-sized furniture industries. Clean Technol. Environ. Policy 2017, 19, 1883–1896. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business cases for sustainability: The role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Formentini, M.; Taticchi, P. Corporate sustainability approaches and governance mechanisms in sustainable supply chain management. J. Clean. Prod. 2016, 112, 1920–1933. [Google Scholar] [CrossRef]

- Broman, G.I.; Robèrt, K.H. A framework for strategic sustainable development. J. Clean. Prod. 2017, 140, 17–31. [Google Scholar] [CrossRef]

- Nawaz, W.; Koç, M. Development of a systematic framework for sustainability management of organizations. J. Clean. Prod. 2018, 171, 1255–1274. [Google Scholar] [CrossRef]

- Ferreira, J.J.M.; Fernandes, C.I.; Ratten, V. A co-citation bibliometric analysis of strategic management research. Scientometrics 2016, 109, 1–32. [Google Scholar] [CrossRef]

- Kimatu, J.N. Evolution of strategic interactions from the triple to quad helix innovation models for sustainable development in the era of globalization. J. Innov. Entrep. 2016, 5, 1–7. [Google Scholar] [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef]

- Batista, A.A.S.; de Francisco, A.C. Organizational sustainability practices: A study of the firms listed by the Corporate Sustainability Index. Sustainability 2018, 10, 226. [Google Scholar] [CrossRef]

- Kourula, A.; Pisani, N.; Kolk, A. Corporate sustainability and inclusive development: Highlights from international business and management research. Curr. Opin. Environ. Sustain. 2017, 24, 14–18. [Google Scholar] [CrossRef]

- Desore, A.; Narula, S.A. An overview on corporate response towards sustainability issues in textile industry. Environ. Dev. Sustain. 2018, 20, 1439–1459. [Google Scholar] [CrossRef]

- Naidoo, M.; Gasparatos, A. Corporate environmental sustainability in the retail sector: Drivers, strategies and performance measurement. J. Clean. Prod. 2018, 203, 125–142. [Google Scholar] [CrossRef]

- Chatha, K.A.; Butt, I.; Tariq, A. Research Methodologies and Publication Trends in Manufacturing Strategy. Int. J. Oper. Prod. Manag. 2015, 35, 487–546. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Oliveira, O.J. Analysis of Integrated Management Systems research: Identifying core themes and trends for future studies. Total Qual. Manag. Bus. Excell. 2018, 31, 1–23. [Google Scholar] [CrossRef]

- José, S.; Reis, M.; Costa, A.C.F.; Espuny, M.; Batista, W.J.; Francisco, F.E.; Gonçalves, G.S.; Tasinaffo, P.M.; Dias, L.A.V.; Cunha, A.M.; et al. Education 4.0: Gaps Research Between School Formation and Technological Development. In Proceedings of the 17th International Conference on Information Technology–New Generations (ITNG 2020), Las Vegas, NV, USA, 5–8 April 2020; Springer: Cham, Switzerland, 2020; pp. 415–420. [Google Scholar]

- Tietze, A.; Hofmann, P. The h-index and multi-author h m -index for individual researchers in condensed matter physics. Scientometrics 2019, 119, 171–185. [Google Scholar] [CrossRef]

- Santos, G.; Salvador, J.; Reis, M.; De Oliveira, F.; Maximilian, S.; Larah, E.; Lescura, G.; Luís, A.; Ferreira, C.; Barbosa, M.; et al. The Rapid Escalation of Publications on Covid-19: A Snapshot of Trends in the Early Months to Overcome the Pandemic and to Improve Life Quality. Int. J. Qual. Res. 2020, 14, 951–968. [Google Scholar]

- Cristino, T.M.; Faria Neto, A.; Costa, A.F.B. Energy efficiency in buildings: Analysis of scientific literature and identification of data analysis techniques from a bibliometric study. Scientometrics 2018, 114, 1275–1326. [Google Scholar] [CrossRef]

- Dabi, Y.; Darrigues, L.; Katsahian, S.; Azoulay, D.; Antonio, D.; Lazzati, A.; Dabi, Y.; Darrigues, L.; Katsahian, S.; Azoulay, D.; et al. Publication Trends in Bariatric Surgery: A Bibliometric Study To cite this version: HAL Id: Hal-01301990. Obes. Surg. 2016, 26, 2691–2699. [Google Scholar] [CrossRef]

- EMAN. Stefan Schaltegger. Available online: http://eman-eu.org/steering-committee/stefan-schaltegger-chair (accessed on 18 October 2020).

- Leuphana Universität Lüneburg: Stefan Schaltegger. Available online: https://www.leuphana.de/en/institutes/centre-for-sustainability-management-csm/persons/stefan-schaltegger.html (accessed on 18 October 2020).

- Ryerson University Cory Searcy Ryerson University Faculty Experts. Available online: https://experts.ryerson.ca/cory-searcy (accessed on 18 October 2020).

- Ryerson University Cory Searcy—Mechanical and Industrial Engineering—Ryerson University. Available online: https://www.ryerson.ca/mechanical-industrial (accessed on 18 October 2020).

- Graz University Baumgartner Rupert—Profile—Research Portal—Karl Franzens University Graz. Available online: https://sis.uni-graz.at/en (accessed on 18 October 2020).

- Hahn, T.; Pinkse, J.; Preuss, L.; Figge, F. Tensions in Corporate Sustainability: Towards an Integrative Framework. J. Bus. Ethics 2015, 127, 297–316. [Google Scholar] [CrossRef]

- Atkinson, G. Measuring corporate sustainability. J. Environ. Plan. Manag. 2000, 43, 235–252. [Google Scholar] [CrossRef]

- Leuphana University of Lüneburg: Study. Leuphana University of Lüneburg, Lüneburg, Germany. Available online: https://www.leuphana.de/en/study.html (accessed on 18 October 2020).

- University of Lüneburg: Sustainability Research. Leuphana University of Lüneburg Leuphana, Lüneburg, Germany. Available online: https://www.leuphana.de/en/research/research-initiatives/sustainability-research.html (accessed on 18 October 2020).

- Ryerson University Sustainability Management and Enterprise Process Excellence. The Chang School of Continuing Education—Ryerson University. Available online: https://continuing.ryerson.ca/public/category/courseCategoryCertificateProfile.do?method=load&certificateId=199149 (accessed on 18 October 2020).

- Ryerson University Clean Energy Zone—Centre for Urban Energy—Ryerson University. Available online: https://www.ryerson.ca/cue/clean-energy-zone/ (accessed on 18 October 2020).

- Times Higher Education (THE). Times Higher Education Impact Rankings Impact Rankings. 2020. Available online: https://www.timeshighereducation.com/rankings/impact/2020/overall#!/page/0/length/25/sort_by/rank/sort_order/asc/cols/undefined (accessed on 18 October 2020).

- University of Leeds. Leeds is Top Three in UK for Sustainable Impact. Available online: http://www.leeds.ac.uk/news/article/4578/leeds_is_top_three_in_uk_for_sustainable_impact (accessed on 18 October 2020).

- University of Leeds Sustainability Service. Available online: https://sustainability.leeds.ac.uk/ (accessed on 18 October 2020).

- University of Leeds. Annual Sustainability Report 2017/18; University of Leeds: Leeds, UK, 2018. [Google Scholar]

- Dandurand, Y.; Boghen, A.D.; Clews, R.A.; Schugurensky, D.; Parazelli, M.; Sabourin, P.S. ProActive Disclosure for SSHRC’s Grants and Contributions/Divulgation Proactive des Subventions et des Contributions du CRSH. Connections 2008, 3, 2009. [Google Scholar]

- Canada NSERC—Research Grants Competition—Results by Institution—2018. Available online: http://www.nserc-crsng.gc.ca/NSERC-CRSNG/FundingDecisions-DecisionsFinancement/ResearchGrants-SubventionsDeRecherche/ResultsInsDetail-ResultatsEtabDetails_eng.asp?Year=2018&Institution=85 (accessed on 18 October 2020).

- Brasil. Chamadas públicas—Portal CNPq. Available online: http://www.cnpq.br/web/guest/chamadas-publicas?p_p_id=resultadosportlet_WAR_resultadoscnpqportlet_INSTANCE_0ZaM&cache=clear (accessed on 18 October 2020).

- Brasil. Prêmio Jovem Cientista. Available online: http://estatico.cnpq.br/portal/premios/2018/pjc/index.html (accessed on 18 October 2020).

- Pinto, A.C.; de Andrade, J.B. Fator de impacto de revistas científicas: Qual o significado deste parâmetro? Quim. Nova 1999, 22, 448–453. [Google Scholar] [CrossRef]

- Phillips, J.F.; Sheff, M.; Boyer, C.B. The astronomy of Africa’s health systems literature during the mdg era: Where are the systems clusters? Glob. Heal. Sci. Pract. 2015, 3, 482–502. [Google Scholar]

- Cobo, M.J.; López-Herrera, A.G.; Herrera-Viedma, E.; Herrera, F. SciMAT: A new science mapping analysis software tool. J. Am. Soc. Inf. Sci. Technol. 2012, 63, 1609–1630. [Google Scholar] [CrossRef]

- de Oliveira, O.J.; da Silva, F.F.; Juliani, F.; Barbosa, L.C.F.M.; Nunhes, T.V. Bibliometric Method for Mapping the State-of-the-Art and Identifying Research Gaps and Trends in Literature: An Essential Instrument to Support the Development of Scientific Projects. In Intech; IntechOpen Limited: London, UK, 2019; p. 21. [Google Scholar]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Grimm, J.H.; Hofstetter, J.S.; Sarkis, J. Critical factors for sub-supplier management: A sustainable food supply chains perspective. Int. J. Prod. Econ. 2014, 152, 159–173. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: A literature review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar]

- Amui, L.B.L.; Jabbour, C.J.C.; de Sousa Jabbour, A.B.L.; Kannan, D. Sustainability as a dynamic organizational capability: A systematic review and a future agenda toward a sustainable transition. J. Clean. Prod. 2017, 142, 308–322. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 32–44. [Google Scholar] [CrossRef]

- Wolf, J. The Relationship Between Sustainable Supply Chain Management, Stakeholder Pressure and Corporate Sustainability Performance. J. Bus. Ethics 2014, 119, 317–328. [Google Scholar] [CrossRef]

- Ortiz-de-Mandojana, N.; Bansal, P. The Effect of Firm Compensation Structures on the Mobility and Entrepreneurship of Extreme Performers. Strateg. Manag. J. 2016, 37, 1615–1631. [Google Scholar] [CrossRef]

- Zhou, H.; Yang, Y.; Chen, Y.; Zhu, J. Data envelopment analysis application in sustainability: The origins, development and future directions. Eur. J. Oper. Res. 2018, 264, 1–16. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability: Are We There Yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Van der Byl, C.A.; Slawinski, N. Embracing Tensions in Corporate Sustainability: A Review of Research from Win-Wins and Trade-Offs to Paradoxes and Beyond. Organ. Environ. 2015, 28, 54–79. [Google Scholar] [CrossRef]

- Hahn, R.; Lülfs, R. Legitimizing Negative Aspects in GRI-Oriented Sustainability Reporting: A Qualitative Analysis of Corporate Disclosure Strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar]

- Cho, C.H.; Laine, M.; Roberts, R.W.; Rodrigue, M. Organized hypocrisy, organizational façades, and sustainability reporting. Account. Organ. Soc. 2015, 40, 78–94. [Google Scholar] [CrossRef]

- World Economic Forum. Davos Manifesto 2020: The Universal Purpose of a Company in the Fourth Industrial Revolution; World Economic Forum: Colony, Switzerland, 2019. [Google Scholar]

- UN Global Compact. Guide to Corporate Sustainability; UN Global Compact: New York, NY, USA, 2014. [Google Scholar]

- Cetindamar, D.; Husoy, K. Corporate social responsibility practices and environmentally responsible behavior: The case of the United Nations global compact. J. Bus. Ethics 2007, 76, 163–176. [Google Scholar] [CrossRef]

- Rasche, A. “A Necessary Supplement” What the United Nations Global Compact Is and Is Not. Bus. Soc. 2009, 48, 511–537. [Google Scholar] [CrossRef]

- United Nations. United Nations Sustainable Development—17 Goals to Transform Our World. Available online: https://www.un.org/sustainabledevelopment (accessed on 10 July 2018).

- UN Global Compact. Sustainable Development; UN Global Compact: New York, NY, USA, 1987. [Google Scholar]

- UN Global Compact. Uniting Business in the Decade Building on 20 Years of Progress; UN Global Compact: New York, NY, USA, 2020. [Google Scholar]

- Global Reporting Initiative; UN Global Compact; World Business Council for Sustainable Development. Inventory of Business Tools—SDG Compass. Available online: https://www.wbcsd.org/Programs/People/Sustainable-Development-Goals/Resources/SDG-Compass#:~:text=One%20key%20component%20of%20the%20SDG%20Compass%20is,impact%20of%20their%20organization%20on%20the%20SDG%20agenda (accessed on 10 July 2018).

- SGD Compass: The Guide for Business Action on the SDGs. Available online: https://sdgcompass.org/wp-content/uploads/2015/12/019104_SDG_Compass_Guide_2015.pdf (accessed on 10 July 2018).

- Muff, K.; Kapalka, A.; Dyllick, T. The Gap Frame—Translating the SDGs into relevant national grand challenges for strategic business opportunities. Int. J. Manag. Educ. 2017, 15, 363–383. [Google Scholar]

- Maas, K.; Schaltegger, S.; Crutzen, N. Integrating corporate sustainability assessment, management accounting, control, and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Chen, S.; Bouvain, P. Is corporate responsibility converging? A comparison of corporate responsibility reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

- Christofi, A.; Christofi, P.; Sisaye, S. Corporate sustainability: Historical development and reporting practices. Manag. Res. Rev. 2012, 35, 157–172. [Google Scholar]

- Landrum, N.E.; Ohsowski, B. Identifying Worldviews on Corporate Sustainability: A Content Analysis of Corporate Sustainability Reports. Bus. Strateg. Environ. 2018, 27, 128–151. [Google Scholar] [CrossRef]

- Global Reporting Initiative. GRI Works with IIRC and Leading Companies to Eliminate Reporting Confusion. Available online: https://blog.aiag.org/gri-works-with-iirc-and-leading-companies-to-eliminate-reporting-confusion (accessed on 10 July 2018).

- International Integrated Reporting Council. The International <IR> Framework. Available online: https://integratedreporting.org/?s=The+International+%3CIR%3E+Framework&x=7&y=10 (accessed on 10 July 2018).

- Taliento, M.; Favino, C.; Netti, A. Impact of environmental, social, and governance information on economic performance: Evidence of a corporate “sustainability advantage” from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef]

- Zsóka, Á.; Vajkai, É. Corporate sustainability reporting: Scrutinising the requirements of comparability, transparency and reflection of sustainability performance. Soc. Econ. 2018, 40, 19–44. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Global Reporting Initiative. About GRI. Available online: https://www.globalreporting.org/about-gri/#:~:text=%E2%80%8BGRI%20helps%20businesses%20and,and%20economic%20benefits%20for%20everyone (accessed on 10 July 2018).

- Siew, R.Y.J. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar]

- RobecoSAM Dow Jones Sustainability Index Family. Available online: https://www.robeco.com/en/key-strengths/sustainable-investing/sustainable-investing-research (accessed on 18 October 2020).

- United Nations Development Programme. Human Development Report 2020; The World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Beare, D.; Buslovich, R.; Searcy, C. Linkages between corporate sustainability reporting and public policy. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 336–350. [Google Scholar] [CrossRef]

- Bonilla, S.H.; Almeida, C.M.V.B.; Giannetti, B.F.; Huisingh, D. The roles of cleaner production in the sustainable development of modern societies: An introduction to this special issue. J. Clean. Prod. 2010, 18, 1–5. [Google Scholar] [CrossRef]

- Adams, R.J.; Smart, P.; Huff, A.S. Shades of Grey: Guidelines for Working with the Grey Literature in Systematic Reviews for Management and Organizational Studies. Int. J. Manag. Rev. 2017, 19, 432–454. [Google Scholar] [CrossRef]

- Lyon, T.P.; Delmas, M.A.; Maxwell, J.W.; Tima Bansal, P.; Chiroleu-Assouline, M.; Crifo, P.; Durand, R.; Gond, J.P.; King, A.; Lenox, M.; et al. CSR needs CPR: Corporate sustainability and politics. Calif. Manag. Rev. 2018, 60, 5–24. [Google Scholar] [CrossRef]

- Moffat, A.; Auer, A. Corporate Environmental Innovatin (CEI): A government initiative to support corporate sustainability leadership. J. Clean. Prod. 2006, 14, 589–600. [Google Scholar] [CrossRef]

- KPMG; Global Reporting Initiative; UN Environment Programme; University of Stellenbosch Business Scool. Carrots & Sticks: Global Trends in Sustainability Reporting Regulation and Policy; KPMG: Amstelveen, The Ntetherlands, 2016. [Google Scholar]

- United States of America. Secretary of State’s Award for Corporate Excellence. In Shaping International Public Opinion: A Model for Nation Branding and Public Diplomacy; U.S. Department of State: Washington, DC, USA, 2016; pp. 221–239. [Google Scholar]

- JAPAN. Japan’s Leading Companies in Climate Change Measures 1; Ministry of Foreign Affairs of Japan: Tokyo, Japan, 2019.

- Study Group on Approaches to Making More Substantial the Dialogues for Creation of Sustainable Corporate Value Compiles Interim Report. Available online: https://www.meti.go.jp/english/press/2020/0828_004.html (accessed on 24 December 2020).

- SME-focused SDG Management Plan Support. Available online: https://sustainabledevelopment.un.org/partnership/?p=31775 (accessed on 24 December 2020).

- France La Responsabilité Sociétale des Entreprises. Ministère de la Transition Écologique. Available online: https://www.ecologie.gouv.fr/responsabilite-societale-des-entreprises (accessed on 18 October 2020).

- Hall, B.H.; Helmers, C. Innovation and diffusion of clean/green technology: Can patent commons help? J. Environ. Econ. Manag. 2013, 66, 33–51. [Google Scholar] [CrossRef]

- Daim, T.U.; Rueda, G.; Martin, H.; Gerdsri, P. Forecasting emerging technologies: Use of bibliometrics and patent analysis. Technol. Forecast. Soc. Change 2006, 73, 981–1012. [Google Scholar] [CrossRef]

- Shin-Etsu Group Key Management. Shin-Etsu Group Key Management. In Sustainability; Shin-Etsu Chemical Co., Ltd.: Chiyoda, Japan; Available online: https://www.shinetsu.co.jp/en/sustainability/esg_management/ (accessed on 26 November 2020).

- Shin-Etsu Group Key. Shin-Etsu Group Key ESG Issues. In Sustainability; Shin-Etsu Chemical Co., Ltd.: Chiyoda, Japan; Available online: https://www.shinetsu.co.jp/en/sustainability/esg_issue/ (accessed on 26 November 2020).

- Shin-Etsu Group Key Top Message. In Sustainability; Shin-Etsu Chemical Co., Ltd.: Chiyoda, Japan; Available online: https://www.shinetsu.co.jp/en/sustainability/esg_greeting/ (accessed on 26 November 2020).

- Shin-Etsu Group Key Shin-Etsu Group. Products and Technologies that Contribute to Environmental Conservation. In Sustainability; Shin-Etsu Chemical Co., Ltd.: Chiyoda, Japan; Available online: https://www.shinetsu.co.jp/en/sustainability/product_technology/ (accessed on 26 November 2020).

- Shin-Etsu Group Key. Sustainability Report; Shin-Etsu Group Key: Tokyo, Japan, 2020. [Google Scholar]

- Shin-Etsu Group Key Respect for Human Rights. Respect for Human Rights, the Development of Human Resources and the Promotion of Diversity; Key ESG Issues; Sustainability; Shin-Etsu Chemical Co., Ltd.: Chiyoda, Japan; Available online: https://www.shinetsu.co.jp/en/sustainability/esg_employ/human-rights/ (accessed on 26 November 2020).

- Shin-Etsu Group Key. GRI Standards; Shin-Etsu Group Key: Tokyo, Japan, 2020. [Google Scholar]

- Procter & Gamble. Relatório de Cidadania 2019; Procter and Gamble: São Paulo, Brasil, 2019. [Google Scholar]

- Procter & Gamble. Environmental Sustainability; Procter and Gamble: Cincinnati, OH, USA, 2019. [Google Scholar]

- Amorepacific Group. Sustainability. Available online: https://www.apgroup.com/int/en/sustainability/sustainability.html (accessed on 26 November 2020).

- Amorepacific Group. Sustainability Report; Amorepacific Group: Seoul, Korea, 2019. [Google Scholar]

- Amorepacific Group. Sustainability Report; Amorepacific Group: Seoul, Korea, 2018. [Google Scholar]

- Birkel, H.; Veile, J.; Müller, J.; Hartmann, E.; Voigt, K.-I. Development of a Risk Framework for Industry 4.0 in the Context of Sustainability for Established Manufacturers. Sustainability 2019, 11, 1–27. [Google Scholar]

- Liao, L.; Warner, M.E.; Homsy, G.C. When Do Plans Matter? Tracking Changes in Local Government Sustainability Actions From 2010 to 2015. J. Am. Plan. Assoc. 2020, 86, 60–74. [Google Scholar] [CrossRef]

- Pechancová, V.; Hrbáčková, L.; Dvorský, J.; Chromjaková, F.; Stojanović, A. Environmental management systems: An effective tool of corporate sustainability. Entrep. Sustain. Issues 2019, 7, 825–841. [Google Scholar] [CrossRef]

- Pauer, S.U.; Pilon, A.; Badelt, B. Strengthening city-university partnerships to advance sustainability solutions: A study of research collaborations between the University of British Columbia and City of Vancouver. Int. J. Sustain. High. Educ. 2020, 21, 1189–1208. [Google Scholar] [CrossRef]

- Ridhosari, B.; Rahman, A. Carbon footprint assessment at Universitas Pertamina from the scope of electricity, transportation, and waste generation: Toward a green campus and promotion of environmental sustainability. J. Clean. Prod. 2020, 246, 119172. [Google Scholar]

- Brozzi, R.; Forti, D.; Rauch, E.; Matt, D.T. The-advantages-of-industry-40-applications-for-sustainability-Results-from-a-sample-of-manufacturing-companies. Sustainability 2020, 12, 3647. [Google Scholar] [CrossRef]

- Amaral, A.R.; Rodrigues, E.; Gaspar, A.R.; Gomes, Á. A review of empirical data of sustainability initiatives in university campus operations. J. Clean. Prod. 2020, 250, 119558. [Google Scholar] [CrossRef]

- Barros, M.V.; Puglieri, F.N.; Tesser, D.P.; Kuczynski, O.; Piekarski, C.M. Sustainability at a Brazilian university: Developing environmentally sustainable practices and a life cycle assessment case study. Int. J. Sustain. High. Educ. 2020, 21, 841–859. [Google Scholar] [CrossRef]

- Kamble, S.S.; Gunasekaran, A.; Gawankar, S.A. Sustainable Industry 4.0 framework: A systematic literature review identifying the current trends and future perspectives. Process Saf. Environ. Prot. 2018, 117, 408–425. [Google Scholar] [CrossRef]

- Cardillo, E.; Longo, M.C. Managerial reporting tools for social sustainability: Insights from a local government experience. Sustainability 2020, 12, 3675. [Google Scholar] [CrossRef]

- Hopkinson, P.; De Angelis, R.; Zils, M. Systemic building blocks for creating and capturing value from circular economy. Resour. Conserv. Recycl. 2020, 155, 104672. [Google Scholar] [CrossRef]

- Ramos, D.; Afonso, P.; Rodrigues, M.A. Integrated management systems as a key facilitator of occupational health and safety risk management: A case study in a medium sized waste management firm. J. Clean. Prod. 2020, 262, 121346. [Google Scholar] [CrossRef]

- Fonseca, L.; Carvalho, F. The reporting of SDGs by quality, environmental, and occupational health and safety-certified organizations. Sustainability 2019, 11, 5797. [Google Scholar] [CrossRef]

- Wolff, S.; Brönner, M.; Held, M.; Lienkamp, M. Transforming automotive companies into sustainability leaders: A concept for managing current challenges. J. Clean. Prod. 2020, 276, 124179. [Google Scholar]

- Zahid, M.; Rahman, H.U.; Muneer, S.; Butt, B.Z.; Isah-Chikaji, A.; Memon, M.A. Nexus between government initiatives, integrated strategies, internal factors and corporate sustainability practices in Malaysia. J. Clean. Prod. 2019, 241, 118329. [Google Scholar] [CrossRef]

- Pham, H.T.T.; Jung, S.C.; Lee, S.Y. Governmental ownership of voluntary sustainability information disclosure in an emerging economy: Evidence from Vietnam. Sustainability 2020, 12, 6686. [Google Scholar] [CrossRef]

- Ghalehkhondabi, I.; Ardjmand, E. Sustainable E-waste supply chain management with price/sustainability-sensitive demand and government intervention. J. Mater. Cycles Waste Manag. 2020, 22, 556–577. [Google Scholar] [CrossRef]

- Samy, G.M.; Samy, C.P.; Ammasaiappan, M. Integrated Management Systems for Better Environmental Performance and Sustainable Development—A Review Integrated Management Systems for Better Environmental Performance and Sustainable Development—A Review. Environ. Eng. Manag. J. 2015, 14. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Bernardo, M.; José de Oliveira, O. Rethinking the way of doing business: A reframe of management structures for developing corporate sustainability. Sustainability 2020, 12, 1177. [Google Scholar] [CrossRef]

- Perchinunno, P.; Cazzolle, M. A clustering approach for classifying universities in a world sustainability ranking. Environ. Impact Assess. Rev. 2020, 85, 106471. [Google Scholar] [CrossRef]

- Aksoy, M.; Yilmaz, M.K.; Tatoglu, E.; Basar, M. Antecedents of corporate sustainability performance in Turkey: The effects of ownership structure and board attributes on non-financial companies. J. Clean. Prod. 2020, 276, 124284. [Google Scholar] [CrossRef]

- Papoutsi, A.; Sodhi, M.M.S. Does disclosure in sustainability reports indicate actual sustainability performance? J. Clean. Prod. 2020, 260, 121049. [Google Scholar] [CrossRef]

- Bag, S.; Telukdarie, A.; Pretorius, J.H.C.; Gupta, S. Industry 4.0 and supply chain sustainability: Framework and future research directions. Benchmark. Int. J. 2018. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Search Criteria | Parameters |

|---|---|

| Databases | Orbit Intelligence, ProQuest, UN Global Compact |

| Time Period | 2000–2020 |

| Research Fields | Title and Invention Objective |

| Keywords | “sustainability”, “environmental pollution”, “environmental sustainability”, “sustainable development”, “economic sustainability”, “social sustainability”, “eco efficiency”, “cleaner production”, “corporate sustainability” OR “life cycle assessment”, “industrial ecology”, “circular economy” |

| Author | H-Index | Average Citations by Publication | Number of Publications (1998–2018) | Citations (1998–2018) | Annual Publications (1999–2018) | Annual Citations (1999–2018) |

|---|---|---|---|---|---|---|

| Schaltegger, S. (Germany) | 15 | 38.7 | 26 | 1006 |  |  |

| Searcy, C. (Canada) | 14 | 51.8 | 20 | 1035 |  |  |

| Baumgartner, R. J.(Áustria) | 10 | 46.5 | 11 | 512 |  |  |

| Countries | H-Index | Average Citations by Publication | Number of Publications (1998–2018) | Citations (1998–2018) | Annual Publications (1999–2018) | Annual Citations (1999–2018) |

|---|---|---|---|---|---|---|

| United States | 37 | 19.8 | 238 | 4708 |  |  |

| United Kingdom | 34 | 24.6 | 159 | 3909 |  |  |

| Germany | 33 | 30.1 | 109 | 3284 |  |  |

| Journals/JCR | Open Access | H-Index | Average Citations by Publication | Number of Publications (1998–2018) | Citations (1998–2018) | Annual PUBLICATIONS (1999–2018) | Annual Citations (1999–2018) |

|---|---|---|---|---|---|---|---|

| Jounal of Cleaner Production/7246 | No | 49 | 44.6 | 157 | 7009 |  |  |

| Business Strategy And The Environment/5483 | No | 34 | 71.1 | 72 | 5118 |  |  |

| Journal of Business Ethics/2917 | No | 34 | 57.3 | 71 | 4113 |  |  |

| Plos One/2.740 | Yes | 21 | 39.1 | 65 | 2539 |  |  |

| Sustainability Swizerland/2.576 | Yes | 19 | 10.9 | 157 | 1704 |  |  |

| Ecology and Society/3.890 | Yes | 19 | 28.3 | 32 | 905 |  |  |

| Research Theme | Words of the Theme |

|---|---|

| (a) Business Characterization | Automotive-industry, Business, business-case, Business-model, Construction-industry, Entrepreneurship, Family-business, Materiality, Small-and-medium-sized-enterprises, Small-to-medium-sized-enterprises, SMEs, Sustainable-business, Sustainable-entrepreneurship |

| (b) TBL-Environmental | Carbon-footprint, Cleaner-production, Climate-change, Corporate-environmental-performance, Eco-efficiency, Ecology, Ecosystems, Efficiency, Energy, Environment, Environmental, Environmental-management, Environmental-management-systems, Environmental-reporting, Environmental-sustainability, ISO 14001, Sustainable-consumption |

| (c) TBL-Social | Corporate-social-performance, Corporate-social-responsibility-(CSR), Dynamic-capabilities, Education, ISO 26000, Organizational-change, Social, Socially-responsible-investment, Social-responsibility, Stakeholder-engagement, Sustainable-leadership |

| (d) TBL-Finance | Accountability, Corporate-financial-performance, Economic, Economic-growth, Economic-sustainability, Environmental-management-accounting, Investment, Socially-responsible-investment, Sustainability-accounting, Value-creation |

| (e) Governance | Business-ethics, Communication, Corporate-governance, Corporate-responsibility, Decision-making, Disclosure, Ethics, Governance, Leadership, Legitimacy, Organizational-culture, Reputation, Responsibility, Stakeholder, Stakeholders, Standards |

| (f) CS Strategy | Benchmarking, Business-strategy, Competitive-advantage, Competitiveness, Corporate-reputation, Corporate-strategy, Environmental-strategy, Stakeholder-analysis, Stakeholder-theory, Strategic-management, Strategic-planning, Strategy, Sustainability-strategy, Sustainable-business-models, Sustainable-competitive-advantage, Sustainable-development-goals, Trade-offs |

| (g) Innovation and Globalization | Business-model-innovation, Developing-countries, Emerging-economies, External-assurance, Globalization, Global-reporting-initiative, Innovation, Planetary-boundaries, Sustainability-oriented-innovation, Sustainable-development-goals, Transformation, UN-Global-Compact |

| (h) CS Development and Management | Analytic-Network-Process, Balanced-Scorecard, Change-management, Corporate-environmental-management, Corporate-sustainability-management, Data-envelopment-analysis, DEA, Human-resource-management, Implementation, Impression-management, Innovation-management, Integration, Knowledge-management, Management, Management-systems, Resource-based-view, Risk-management, Stakeholder-management, Supply-chain, Supply-chain-management, Supply-chains, Sustainability-management, Sustainability-practices, Sustainable-supply-chain-management |

| (i) CS Performance | Assessment, Corporate-sustainability-performance, Environmental-performance, Financial-performance, Firm-performance, Global-reporting-initiative, Indicator, Indicators, Key-performance-indicators, Life-cycle-assessment, Organizational-performance, Panel-data, Performance, Performance-assessment, Performance-evaluation, Performance-indicators, Performance-measurement, Sustainability-assessment, Sustainability-index, Sustainability-indicators, Sustainability-performance, Sustainable-value, Values |

| (j) CS Disclosure | Corporate-sustainability-reporting, GRI, Integrated-reporting, Reporting, Sustainability-disclosure, Sustainability-report, Sustainability-reporting |

| Research Theme | 1999–2003 (A) | % | 2004–2008 (B) | % | 2009–2013 (C) | % | 2014–2018 (D) | % | D–B (E) |

|---|---|---|---|---|---|---|---|---|---|

| Business Characterization | 87 | 11.76% | 169 | 8.93% | 441 | 10.89% | 798 | 12.66% | 3.73% |

| TBL-environmental | 87 | 11.76% | 253 | 13.39% | 481 | 11.88% | 600 | 9.52% | −3.87% |

| TBL-social | 44 | 5.88% | 118 | 6.25% | 421 | 10.40% | 435 | 6.90% | 0.65% |

| TBL-finance | 44 | 5.88% | 68 | 3.57% | 201 | 4.95% | 257 | 4.08% | 0.51% |

| Governance | 87 | 11.76% | 203 | 10.71% | 462 | 11.39% | 673 | 10.67% | −0.04% |

| CS Strategy | 87 | 11.76% | 270 | 14.29% | 381 | 9.41% | 600 | 9.52% | −4.77% |

| Innovation and Globalization | 0 | 0.00% | 84 | 4.46% | 190 | 4.70% | 415 | 6.59% | 2.13% |

| CS Development and Management | 131 | 17.65% | 304 | 16.07% | 451 | 11.14% | 844 | 13.39% | −2.68% |

| CS Performance | 131 | 17.65% | 287 | 15.18% | 612 | 15.10% | 963 | 15.27% | 0.09% |

| CS Disclosure | 44 | 5.88% | 135 | 7.14% | 411 | 10.15% | 719 | 11.40% | 4.26% |

| TOTAL | 741 | 100.00% | 1891 | 100.00% | 4052 | 100.00% | 6304 | 100.00% |

| Ranking | Country | Number of Companies |

|---|---|---|

| 1 | United States | 59 |

| 2 | Japan | 33 |

| 3 | France | 25 |

| 4 | United Kingdom | 23 |

| 5 | South Korea | 19 |

| 6 | Australia | 18 |

| 7 | Spain | 16 |

| 8 | Taiwan | 15 |

| 9 | Germany | 14 |

| 10 | Italy | 14 |

| Company/Country | Sector | Domain | Number of Patents |

|---|---|---|---|

| Shin Etsu Chemical (SEC)/Japan | Chemical | Handling | 6 |

| Macromolecular Chemistry, Polymers | 5 | ||

| Basic Materials Chemistry | 2 | ||

| Chemical Engineering | 1 | ||

| Other Special Machines | 1 | ||

| Protector & Gamble (P&G)/USA | Consumer goods | Handling | 9 |

| Organic Fine Chemistry | 6 | ||

| Chemical Engineering | 5 | ||

| Macromolecular Chemistry, Polymers | 1 | ||

| Basic Materials Chemistry | 1 | ||

| Amorepacific/South Korea | Cosmetics and Aesthetics | Organic Fine Chemistry | 9 |

| Sector | Domain | Proposal | Triple-Helix Connection | Scientific and Technical References |

|---|---|---|---|---|

Universities | Education | Create CS-training courses at all levels (undergraduate/postgraduate/extension) | Government and Organizations | Leuphana University (2020); Ryerson University (2020); Birkel et al.(2019) |

| Integration of SDG into curricula covering as many of the “goals” as possible in order to systemically foster sustainability | Government | Birkel et al. (2020); University of Leeds (2020); Barros et al. (2020) | ||

| Research | Develop research that promotes a better understanding of the concept of sustainability in companies | Organizations | Pechancová et al. (2019); Canada (2015); Brazil (2020) | |

| Identify research opportunities that meet the interests of society and promote the development of CS | Government and Organizations | Brozzi et al. (2020); Canada (2018) | ||

| Develop studies to reduce the carbon footprint by developing green products and green processes, and using renewable energy, such as solar panels and wind turbines | Government and Organizations | Pechancová et al. (2019); Ryerson University (2020) | ||

| Conduct research on the relationship between Industry 4.0 and sustainability | Government and Organizations | Brozzi et al. (2020); Amui et al. (2017) | ||

| Management | Engage university leaders in obtaining funding and establishing partnerships for CS research | Organizations | Brasil (2020); Canada (2018); Pauer et al. (2020) | |

| Implement a solid waste management program, giving priority, respectively, to the reduction, reuse and recycling of solid waste | Government | Ridhosari and Rahman (2020); University of Leeds (2020); Amaral et al. (2020) | ||

Government | Politics and Legislation | Align national public policies with SDGs to facilitate the implementation of SDGs by companies | Organizations | Cardillo and Longo (2020); Japan (2020); Fonseca et al. (2019) |

| Include sustainability in government plans for Industry 4.0 | Organizations and Universities | Bonilla et al. (2018) | ||

| Draft laws to foster corporate sustainability, for example, regulating the publish reports on socio-environmental actions | Organizations | France (2020); Landrum and Ohsowski (2018) | ||

| Create policies and plans to foster the use of renewable energy | Organizations and Universities | Wolff et al. (2020); Japan (2020) | ||

| Create legislation to reduce the emission of gases and generation of polluting waste in industry | Organizations | USA (2017); Ghalehkhondabi (2020) | ||

| Create legislation to guarantee workers’ rights and adequate working conditions | Industry | USA (2017); Ramos et al. (2020) | ||

| Public Management | To monitor and disclose annually the evolution of the implementation of SDGs in the business sector | Organizations | Pham (2020); France (2020) | |

| Promote awards and recognitions for public and private companies with outstanding sustainable performance | Organizations | USA (2017) | ||

| Create projects for society participation in the suggestion of initiatives for developing CS | Organizations and Universities | Japan (2020) | ||

| Economy | Establish fees, tariffs, or fines on excess emissions of pollutant gases | Organizations | Taliento (2019) | |

| Financing research projects in universities and companies in the CS area | Universities | Brasil (2020); Canada (2018) | ||

| Enable loans to SMEs that present management plans strategically integrated with SDGs | Organizations | Lyon (2018); Ammasaiappan (2017) | ||

Organizations | Planning and Management | Integrate SDGs into organizations’ strategic plans | Government and Universities | Perchinunno and Cazzolle (2020); Nunhes et al. (2020) |

| Create governance processes that help integrate CS into the company’s strategy according to the reality of the countries in which they operate | Universities | Roca and Searcy (2012); GRI UNGC WBCSD (2020) | ||

| Establish partnerships with universities and research centers for developing sustainable technologies and processes | Universities | Shin Etsu Chemical (2020); Pauer et al. (2020) | ||

| Foster the suggestion of ideas and support the development of socio-environmental projects | Government and Universities | Protector & Gamble (2019); Amorepacific (2020) | ||

| Operations | Measuring sustainability performance from sustainability indices | Universities | Lozano (2015) | |

| Develop programs to promote worker health and safety and identify risks to employees’ rights | Government and Universities | Amorepacific (2020); Shin Etsu Chemica (2020) | ||

| Prepare and publish sustainability reports | Government and Universities | Papoutsi (2020) | ||

| Include sustainability criteria in product development processes | Universities | Pechancová (2019); Shin Etsu Chemica (2020) | ||

| Use Industry 4.0 technologies to improve business performance on sustainability pillars | Government and Universities | Bag et al. (2018) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vieira Nunhes, T.; Viviani Garcia, E.; Espuny, M.; Homem de Mello Santos, V.; Isaksson, R.; José de Oliveira, O. Where to Go with Corporate Sustainability? Opening Paths for Sustainable Businesses through the Collaboration between Universities, Governments, and Organizations. Sustainability 2021, 13, 1429. https://doi.org/10.3390/su13031429

Vieira Nunhes T, Viviani Garcia E, Espuny M, Homem de Mello Santos V, Isaksson R, José de Oliveira O. Where to Go with Corporate Sustainability? Opening Paths for Sustainable Businesses through the Collaboration between Universities, Governments, and Organizations. Sustainability. 2021; 13(3):1429. https://doi.org/10.3390/su13031429

Chicago/Turabian StyleVieira Nunhes, Thaís, Enzo Viviani Garcia, Maximilian Espuny, Vitor Homem de Mello Santos, Raine Isaksson, and Otávio José de Oliveira. 2021. "Where to Go with Corporate Sustainability? Opening Paths for Sustainable Businesses through the Collaboration between Universities, Governments, and Organizations" Sustainability 13, no. 3: 1429. https://doi.org/10.3390/su13031429

APA StyleVieira Nunhes, T., Viviani Garcia, E., Espuny, M., Homem de Mello Santos, V., Isaksson, R., & José de Oliveira, O. (2021). Where to Go with Corporate Sustainability? Opening Paths for Sustainable Businesses through the Collaboration between Universities, Governments, and Organizations. Sustainability, 13(3), 1429. https://doi.org/10.3390/su13031429