Modelling Sustainability Risk in the Brazilian Cosmetics Industry

Abstract

1. Introduction

2. Literature Review

2.1. Sustainability Risks in Supply Chain

2.1.1. Economic Risks

2.1.2. Social Risks

2.1.3. Environmental Risks

2.2. Risk Responses

- i

- Insure (IN)—General insurance, protection of employees’ health against natural catastrophes and disasters, and in operation, protect employees against pandemics, and develop a system to inform managers in a timely manner on litigation;

- ii

- Retain (RT)—Accept risk if penalties are low and adapt to a new reality;

- iii

- Prevent (PR)—Monitor CO2 footprint across the supply chain;

- iv

- Reduce (RE)—Sustainable waste management, relationship with local communities, establish crisis team to deal with attacks, reduction in flexible hours, respond quickly to media or government reports, safety instructions and contingency plans, train employees and adopt new technology;

- v

- Mitigate (MI)—Have health procedures to protect staff, emergency plans for potential accidents, system to act swiftly in response to allegations, improve environmental audits, insure against infringements from customers/suppliers, invest in renewable energy sources, locate facility away from urban areas, respond swiftly to adverse reports, water recycling.

- vi

- Cooperate (CP)—Build a flexible supply chain, work with suppliers to quickly determine potential consequences, close industry collaboration, continuously assess the water footprint, design products requiring less packaging, work with potential suppliers to interpret the law to identify risk sources;

- vii

- Avoid (AV)—Locate facility away from urban areas, use clean energy, avoid polluting suppliers, avoid countries with poor transparency record, avoid investment in regions with a poor record for child labor, avoid investment in unstable regions;

- viii

- Share (SH)—Conduct sustainability audit with critical suppliers; work closely with suppliers to limit child labor;

- ix

- Transfer (TR)—Employ legal services to deal with equal opportunities, engage governments and financial institutions to support liquidity, hedge against volatility jointly;

- x

- Control (CO)—Acquire ISO14001 and ISO26000 certificate.

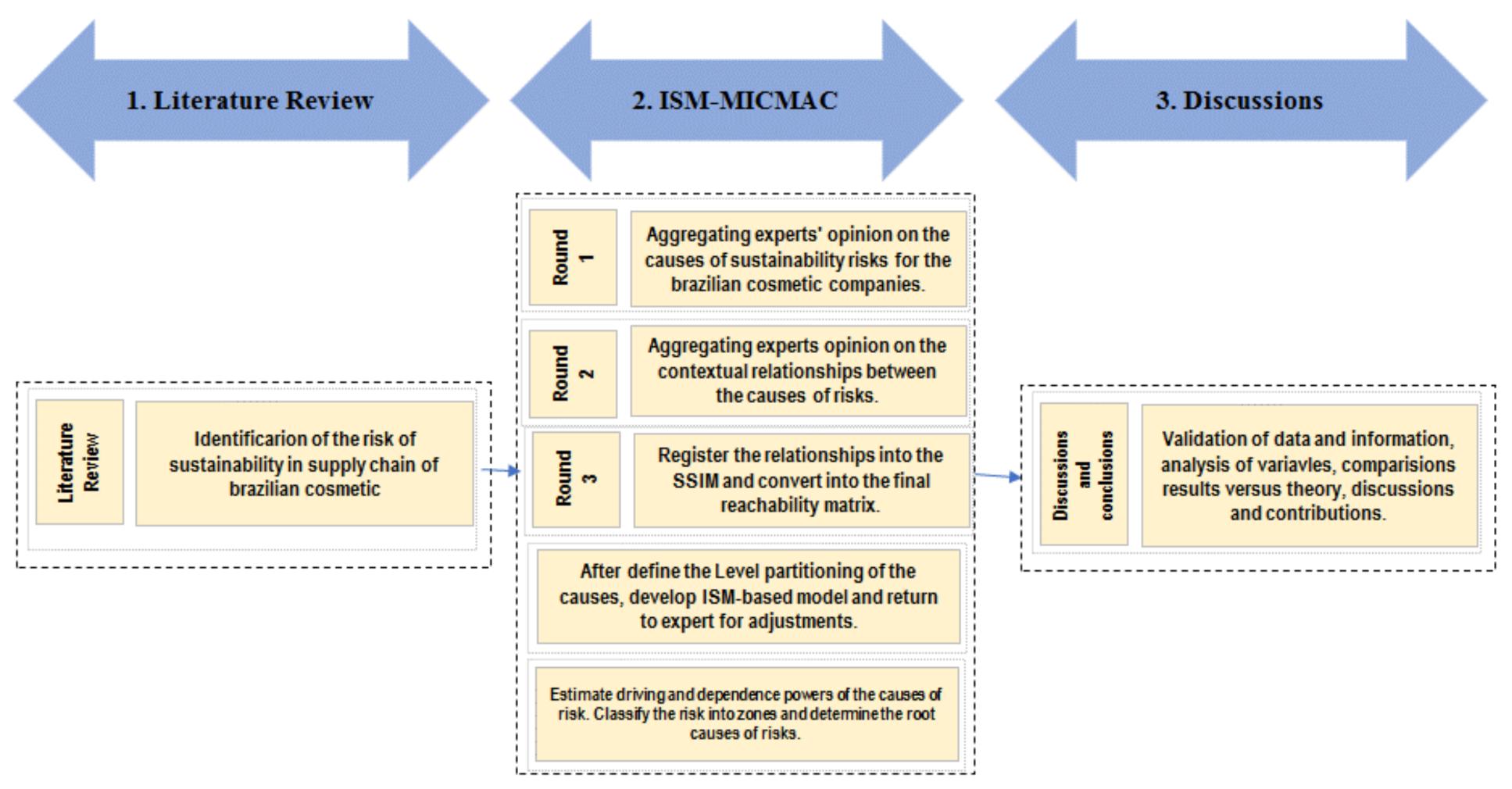

3. Methods

3.1. General Context

3.2. Focus Group

3.3. Interpretive Structural Modeling

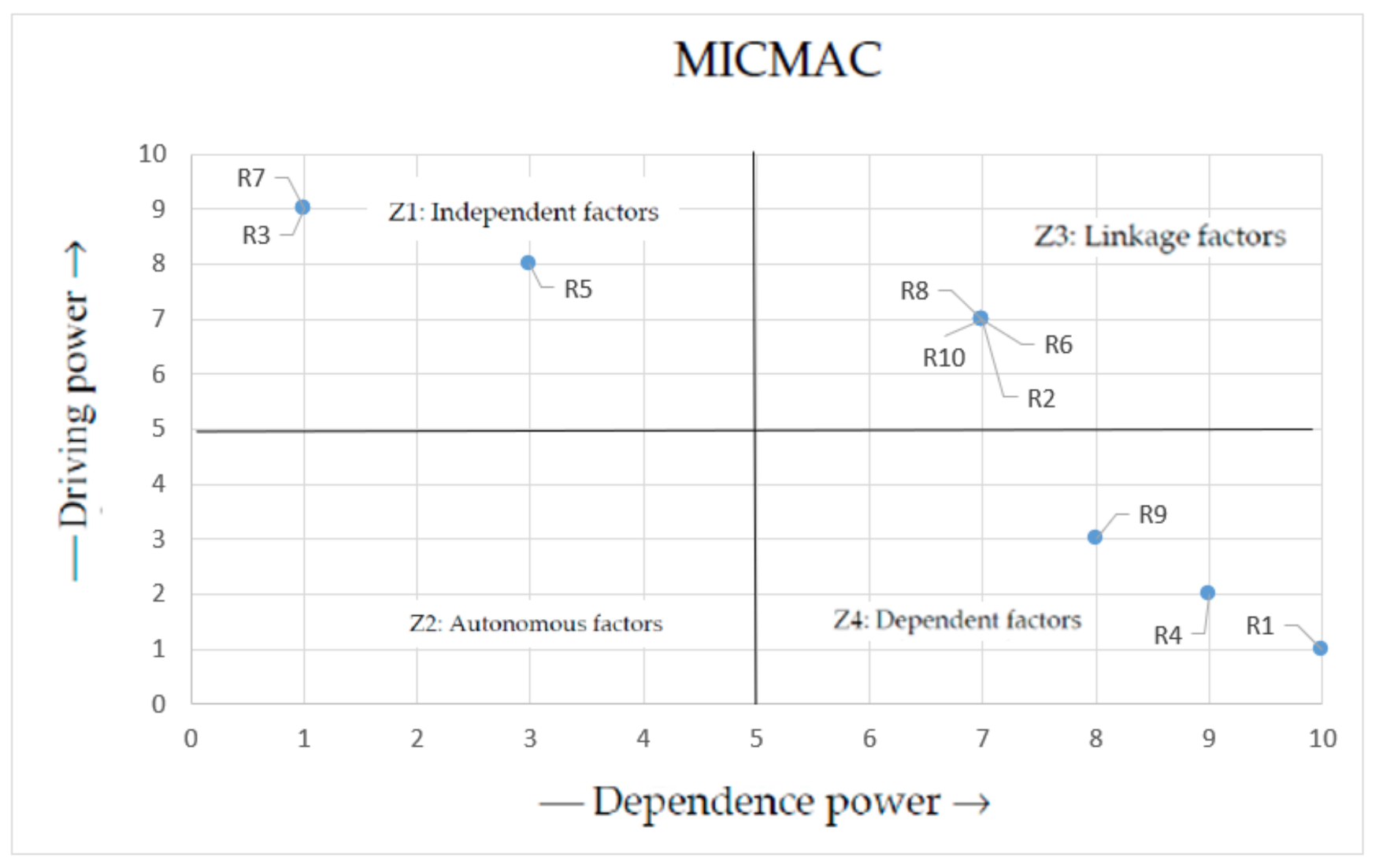

3.4. Classification of Risks: MICMAC Analysis

4. Results

4.1. Identification of the Risks Factors

4.2. Structural Self-Interaction Matrix

- i

- If the (i, j) input in SSIM is V, then the (i, j) input in IRM becomes 1 and the (j, i) input becomes 0;

- ii

- If the (i, j) input in SSIM is A, then the (i, j) input in IRM becomes 0 and the (j, i) input becomes 1;

- iii

- If the (i, j) input in SSIM is X, then the (i, j) and (j, i) inputs in IRM become 1;

- iv

- If the (i, j) input in SSIM is O, then the (i, j) and (j, i) inputs in IRM become 0.

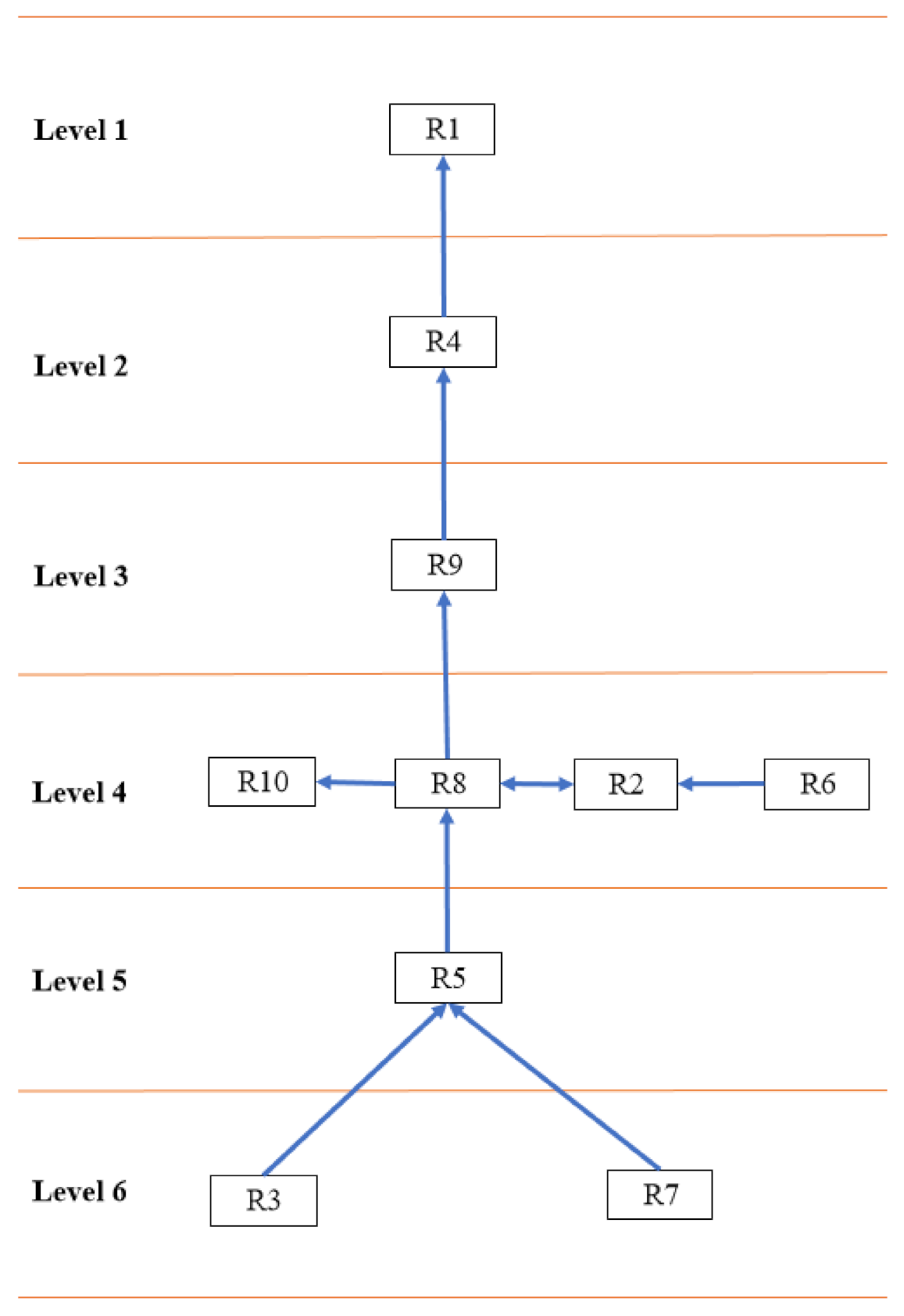

4.3. ISM-Based Model

4.4. MICMAC Analysis

4.5. Risk Responses

5. Discussion

“Sustainability is a necessary evil. The company’s priority is to expand, as much as possible, our market share. We adopt transparency in our relations along the supply chain to identify and eliminate potentially harmful internal practices or suppliers for the environment and society. However, there are blind spots in our chain, which are suppliers’ layers beyond our control. The increase in expenses with auditing processes and companies’ certifications in our chain would lead to an increase in costs that perhaps compromise our profitability and for which management is not willing to incur.”

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- United Nations. Take Action for the Sustainable Development Goals. Common indicators. Available online: https://www.un.org/sustainabledevelopment/sustainable-development-goals/ (accessed on 2 September 2020).

- Hofmann, H.; Busse, C.; Bode, C.; Henke, M. Sustainability-Related Supply Chain Risks: Conceptualization & Management. Bus. Strategy Environ. 2014, 23, 160–172. [Google Scholar]

- Busse, C.; Kach, A.; Bode, C. Sustainability & the False Sense of Legitimacy: How Institutional Distance Augments Risk in Global Supply Chains. J. Bus. Logist. 2016, 37, 312–328. [Google Scholar]

- Reinerth, D.; Busse, C.; Wagner, S.M. Using country sustainability risk to inform sustainable supply chain management: A design science study. J. Bus. Logist. 2019, 40, 241–264. [Google Scholar] [CrossRef]

- Bregman, R.; Peng, D.X.; Chin, W. The effect of controversial global sourcing practices on the ethical judgments and intentions of US consumers. J. Oper. Manag. 2015, 36, 229–243. [Google Scholar] [CrossRef]

- Bui, T.D.; Tsai, F.M.; Tseng, M.L.; Tan, R.R.; Yu, K.D.; Lim, M.K. Sustainable supply chain management towards disruption and organizational ambidexterity: A data driven bibliometric analysis. Sustain. Prod. Consum. 2021, 26, 373–410. [Google Scholar] [CrossRef]

- Ehrgott, M.; Reimann, F.; Kaufmann, L.; Carter, C. Environmental development of emerging economy suppliers: Antecedents & outcomes. J. Bus. Logist. 2013, 34, 131–147. [Google Scholar]

- Busse, C. Doing Well by Doing Good? The Self-interest of Buying Firms & Sustainable Supply Chain Management. J. Supply Chain. Manag. 2016, 52, 28–47. [Google Scholar]

- Syed, M.W.; Li, J.Z.; Junaid, M.; Ye, X.; Ziaullah, M. An Empirical Examination of Sustainable Supply Chain Risk and Integration Practices: A Performance-Based Evidence from Pakistan. Sustainability 2019, 11, 5334. [Google Scholar] [CrossRef]

- Kim, S.; Wagner, S.M.; Colicchia, C. The impact of supplier sustainability risk on shareholder value. J. Supply Chain. Manag. 2019, 55, 71–87. [Google Scholar] [CrossRef]

- Kim, S.; Wagner, S.M. Examining the stock price effect of corruption risk in the supply chain. Decis. Sci. 2021, 52, 833–865. [Google Scholar] [CrossRef]

- Tseng, M.L.; Tran, T.P.T.; Ha, M.H.; Bui, T.D.; Lim, M.L. Sustainable industrial and operation engineering trends and challenges Toward Industry 4.0: A data driven analysis. J. Ind. Prod. Engineering. 2021, 38, 1–18. [Google Scholar] [CrossRef]

- Giannakis, M.; Papadopoulos, T. Supply chain sustainability: A risk management approach. Int. J. Prod. Econ. 2016, 171, 455–470. [Google Scholar] [CrossRef]

- Awasthi, A.; Govindan, K.; Gold, S. Multi-tier sustainable global supplier selection using a fuzzy AHP-VIKOR based approach. Int. J. Prod. Econ. 2018, 195, 106–117. [Google Scholar] [CrossRef]

- Ahmadi, H.; Petrudi, S.; Wang, X. Integrating sustainability into supplier selection with analytical hierarchy process & improved grey relational analysis: A case of telecom industry. Int. J. Adv. Manuf. Technol. 2017, 90, 2413–2427. [Google Scholar]

- Bartley, T.; Child, C. Movements, markets and fields: The effects of anti-sweatshop campaigns on U.S. firms, 1993–2000. Soc. Forces 2011, 90, 425–451. [Google Scholar] [CrossRef]

- Jiang, B. The effects of interorganizational governance on supplier’s compliance with SCC: An empirical examination of compliant and non-compliant suppliers. J. Oper. Manag. 2009, 27, 267–280. [Google Scholar] [CrossRef]

- Pullman, M.E.; Maloni, M.J.; Carter, C.R. Alimentos para o pensamento: Práticas de sustentabilidade socioambiental e resultados de desempenho. J. Supply Chain Manag. 2009, 45, 38–54. [Google Scholar] [CrossRef]

- Foerstl, K.; Reuter, C.; Hartmann, E.; Blome, C. Managing supplier sustainability risks in a dynamically changing environment-sustainable supplier management in the chemical industry. J. Purch. Supply Manag. 2010, 16, 118–130. [Google Scholar] [CrossRef]

- Xu, M.; Cui, Y.; Hu, M.; Xu, X.; Zhang, Z.; Liang, S.; Qu, S. Supply chain sustainability risk & assessment. J. Clean. Prod. 2019, 225, 857–867. [Google Scholar]

- Elkington, J. Enter the Triple Bottom Line. In The Triple Bottom Line: Does It All Add Up? Henriques, A., Richardson, J., Eds.; Earthscan: London, UK, 2004; pp. 1–16. [Google Scholar]

- Schleper, M.; Busse, C. Toward a standardized supplier code of ethics: Development of a design concept based on diffusion of innovation theory. Logist. Res. 2013, 6, 187–216. [Google Scholar] [CrossRef]

- Bom, S.; Jorge, J.; Ribeiro, H.M.; Marto, J. A Step Forward on Sustainability in the Cosmetics Industry: A review. J. Clean. Prod. 2019, 225, 270–290. [Google Scholar] [CrossRef]

- Bom, S.; Ribeiro, H.M.; Marto, J. Sustainability Calculator: A Tool to Assess Sustainability in Cosmetic Products. Sustainability 2020, 12, 1437. [Google Scholar] [CrossRef]

- Lee, Y.-H.; Chen, S.-L. Effect of Green Attributes Transparency on WTA for Green Cosmetics: Mediating Effects of CSR and Green Brand Concepts. Sustainability 2019, 11, 5258. [Google Scholar] [CrossRef]

- Euromonitor Beauty & Personal Care in Brazil. 2019. Available online: https://www.euromonitor.com/beauty-and-personal-care-in-brazil/report (accessed on 12 December 2019).

- Pitman, S. Brazilian Cosmetic Manufacturing Booms. Available online: https://www.cosmeticsdesign-europe.com/Article/2006/02/10/Brazilian-cosmetic-manufacturing-booms (accessed on 26 July 2021).

- Dube, A.; Gawande, R. Analysis of green supply chain barriers using integrated ISM-fuzzy MICMAC approach. Benchmarking Int. J. 2016, 23, 1558–1578. [Google Scholar] [CrossRef]

- Romano, A.L.; Teixeira, I.T.; Alves Filho, A.G.; Helleno, A.L. Avaliação da sustentabilidade corporativa e da cultura organizacional–survey no setor brasileiro de cosméticos. Rev. De Adm. Da UFSM 2018, 11, 1305–1323. [Google Scholar] [CrossRef][Green Version]

- Attri, R.; Grover, S. Modelling the quality enabled factors in initiation stage of production system life cycle. Benchmarking Int. J. 2017, 24, 163–183. [Google Scholar] [CrossRef]

- Kwak, D.; Rodrigues, V.; Mason, R.; Pettit, S.; Beresford, A. Risk interaction identification in international supply chain logistics: Developing a holistic model. Int. J. Oper. Prod. Manag. 2018, 38, 372–389. [Google Scholar] [CrossRef]

- Magalhães, V.S.; Ferreira, L.M.; Silva, C. Using a Methodological Approach to Model Causes of Food Loss and Waste in Fruit and Vegetable Supply Chains. J. Clean. Prod. 2021, 283, 124574. [Google Scholar] [CrossRef]

- Troche-Escobar, J.; Lepikson, H.; Mendonça Freires, F. A Study of Supply Chain Risk in the Brazilian Wind Power Projects by Interpretive Structural Modeling and MICMAC Analysis. Sustainability 2018, 10, 3442. [Google Scholar] [CrossRef]

- Kumar, A.; Mangla, S.; Kumar, P.; Karamperidis, S. Challenges in perishable food supply chains for sustainability management: A developing economy perspective. Bus. Strat. Environ. 2020, 29, 1809–1831. [Google Scholar] [CrossRef]

- Magalhães, V.S.; Ferreira, L.M.; César, A.S.; Bonfim, R.M.; Silva, C. Food loss and waste in the Brazilian beef supply chain: An empirical analysis. Int. J. Logist. Manag. 2021, 32, 214–236. [Google Scholar] [CrossRef]

- Romano, A.L.; Teixeira, I.T.; Alves Filho, A.G.; Helleno, A.L. A study on organizational culture in the brazilian cosmetics sector. Rev. Pensam. Contemp. Em Adm. 2014, 9, 142–158. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Freeman, R.E.; Moutchnik, A. Stakeholder management and Corporate Social Responsibility: Questions and answers. Umwelt. Wirtsch. Forum. 2013, 21, 5–9. [Google Scholar] [CrossRef]

- Okuyama, Y.; Santos, J. Disaster impact and input-output analysis. Econ. Syst. Res. 2014, 26, 1–12. [Google Scholar] [CrossRef]

- Altay, N.; Ramirez, A. Impact of disasters on firms in different sectors: Implications for supply chains. Supply Chain Manag. 2010, 46, 59–80. [Google Scholar] [CrossRef]

- Fiksel, J. Evaluating supply chain sustainability. Chem. Eng. Prog. 2010, 106, 28–38. [Google Scholar]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Acquaye, A.; Feng, K.; Oppon, E.; Salhi, S.; Ibn-Mohammed, T.; Genovese, A.; Hubacek, K. Measuring the environmental sustainability performance of global supply chains: A multi-regional input-output analysis for carbon, sulphur oxide & water footprints. J. Environ. Manag. 2017, 187, 571–585. [Google Scholar]

- Dubey, R.; Gunasekaran, A.; Childe, S.J.; Papadopoulos, T.; Hazen, B.; Giannakis, M.; Roubaud, D. Examining the effect of external pressures and organizational culture on shaping performance measurement systems for sustainability benchmarking. Int. J. Prod. Econ. 2017, 193, 63–76. [Google Scholar] [CrossRef]

- Chan, F. Performance measurement in a supply chain. Int. J. Adv. Manuf. Technol. 2003, 21, 534–548. [Google Scholar] [CrossRef]

- Cunha, L.; Ceryno, P.; Leiras, A. Social Supply Chain Risk Management: A taxonomy, a framework & a research agenda. J. Clean. Prod. 2019, 20, 1101–1110. [Google Scholar]

- Kabat, M.; Desalvo, A.; Egan, J. The tip of the iceberg: Media coverage of ‘slave labor’ in Argentina. Lat. Am. Perspect. 2017, 44, 50–62. [Google Scholar] [CrossRef]

- Blackburn, W.R. The Sustainability Handbook: The Complete Management Guide to Achieving Social, Economic & Environmental Responsibility; Earth-Scan: London, UK, 2007. [Google Scholar]

- Torres-Ruiz, A.; Ravindran, A.R. Multiple criteria framework for the sustainability risk assessment of a supplier portfolio. J. Clean. Prod. 2018, 172, 4478–4493. [Google Scholar] [CrossRef]

- Carter, C.; Jennings, M. The role of purchasing in corporate social responsibility: A structural equation analysis. J. Bus. Logist. 2004, 25, 145–186. [Google Scholar] [CrossRef]

- Govindan, K.; Azevedo, S.G.; Carvalho, H.; Machado, V. Impact of supply chain management practices on Sustainability. J. Clean. Prod. 2014, 85, 212–225. [Google Scholar] [CrossRef]

- Grimm, J.H.; Hofstetter, J.S.; Sarkis, J. Exploring sub-suppliers’ compliance with corporate sustainability standards. J. Clean. Prod. 2016, 112, 1971–1984. [Google Scholar] [CrossRef]

- Mulhall, R.; Bryson, J. Energy price risk & the sustainability of demand side supply chains. Appl. Energy 2014, 123, 327–334. [Google Scholar]

- Mulyati, H.; Geldermann, J. Managing risks in the Indonesian seaweed supply chain. Clean Technol. Environ. Policy 2017, 19, 175–189. [Google Scholar] [CrossRef]

- Sodhi, M.; Son, B.; Tang, C. Researchers’ perspectives on supply chain risk management. Prod. Oper. Manag. 2012, 21, 1–13. [Google Scholar] [CrossRef]

- Zakeri, A.; Dehghanian, F.; Fahimnia, B.; Sarkis, J. Carbon pricing versus emissions trading: A supply chain planning perspective. Int. J. Prod. Econ. 2015, 164, 197–205. [Google Scholar] [CrossRef]

- Pongrácz, E. The environmental impacts of packaging. In Environmentally Conscious Materials & Chemicals Processing; Kutz, M., Ed.; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2007; pp. 237–278. [Google Scholar]

- Hsieh, C. Disaster risk assessment of ports based on the perspective of vulnerability. Nat. Hazards 2014, 74, 851–864. [Google Scholar] [CrossRef]

- International Monetary Fund—IMF Small States’ Resilience to Natural Disasters & Climate Change: Role for the IMF, IMF Policy Paper; International Monetary Fund: Washington, DC, USA, 2016.

- Smith, J.; Schellnhuber, H.; Mirza, M. Vulnerability to Climate Change & Reasons for Concern: A Synthesis. In Climate Change 2001: Impacts, Adaptation & Vulnerability. Contribution of Working Group II to the Third Assessment Report of the Intergovernmental Panel on Climate Change; McCarthy, J., Canziani, O.F., Leary, N.A., Dokken, D.J., White, K.S., Eds.; Cambridge University Press: Cambridge, UK, 2001; pp. 914–967. [Google Scholar]

- Halldórsson, Á.; Kotzab, H.; Skjott-Larsen, T. Supply chain management on the crossroad to sustainability: A blessing or a curse? Logist Res. 2009, 1, 83–94. [Google Scholar] [CrossRef]

- Cosgrove, W.; Loucks, D. Water management: Current & future challenges & research directions. Water Resour. Res. 2015, 51, 4823–4839. [Google Scholar]

- Huq, F.; Stevenson, M.; Zorzini, M. Social sustainability in developing country suppliers: An exploratory study in the ready-made garments industry of Bangladesh. Intern. J. Oper. Prod. Manag. 2014, 34, 610–638. [Google Scholar]

- Pagell, M.; Wu, Z.; Wasserman, M.E. Thinking differently about purchasing portfolios: An assessment of sustainable sourcing. J. Supply Chain. Manag. 2010, 46, 57–73. [Google Scholar] [CrossRef]

- Godar, J.; Suavet, C.; Gardner, T.; Dawkins, E.; Meyfroidt, P. Balancing detail & scale in assessing transparency to improve the governance of agricultural commodity supply chains. Environ. Res. Lett. 2016, 11, 035015. [Google Scholar] [CrossRef]

- Valinejad, F.; Rahmani, D. Sustainability risk management in the supply chain of telecommunication companies: A case study. J. Clean. Prod. 2018, 203, 53–67. [Google Scholar] [CrossRef]

- Clift, R. Metrics for supply chain sustainability. Clean Technol. Environ. Policy 2003, 5, 240–247. [Google Scholar] [CrossRef]

- Simas, M.; Pacca, S. Assessing employment in renewable energy technologies: A case study for wind power in Brazil. Renew. Sustain. Energy Rev. 2014, 31, 83–90. [Google Scholar] [CrossRef]

- Diaz, K.; O’Hanlon, N. IssueWeb: A Guide & Sourcebook for Researching Controversial Issues on the Web; Libraries Unlimited: Westport, CT, USA, 2004. [Google Scholar]

- People for the Ethical Treatment of Animals—PETA. 2014. Available online: www.peta.org (accessed on 10 December 2020).

- Hartman, L.; DesJardins, J.; MacDonald, C. Business Ethics: Decision Making for Personal Integrity & Social Responsibility, 4th ed.; Mcgraw-Hill: New York, NY, USA, 2018. [Google Scholar]

- Carter, C.; Rogers, D. A framework of sustainable supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

- Madhav, N.; Oppenheim, B.; Gallivan, M.; Mulembakani, P.; Rubin, E.; Wolfe, E. Chapter 17—Pandemics: Risks, Impacts, & Mitigation. In The International Bank for Reconstruction & Development; Jamison, D., Gelband, H., Horton, S., Jha, P., Laxminarayan, R., Mock, C., Nugent., R., Eds.; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- International Labour Organisation—ILO. 2014. Available online: http://www.ilo.org/ipec/facts/lang–en/index.htm (accessed on 20 December 2020).

- Smith-Bingham, R. The Emerging Risks Quandary. Anticipating Threats Hidden in Plain Sight; Marsh & McLennan: New York, NY, USA, 2016. [Google Scholar]

- Connor, J. The competition Law Review, Anti-Cartel Enforcement by the DOJ: An Appraisal. Compet. Law Rev. 2008, 5, 89–121. [Google Scholar]

- Sójka, J.; Wempe, J. (Eds.) Business Challenging Business Ethics: New Instruments for Coping with Diversity in International Business: The 12th Annual EBEN Conference; Springer: Dordrecht, The Netherlands, 2000; pp. 193–203. [Google Scholar]

- Humphreys, K. What Every Engineer Should Know about Ethics; Marcel Dekker, Inc.: New York, NY, USA, 1999. [Google Scholar]

- Prostean, G.; Badea, A.; Vasar, C.; Octavian, P. Risk variables in wind power supply chain. Procedia Soc. Behav. Sci. 2014, 124, 124–132. [Google Scholar] [CrossRef]

- AbdelWarith, K.; Anastasopoulos, P.; Richardson, W. Design of local roadway infrastructure to service sustainable energy facilities. Energy Sustain. Soc. 2014, 4, 14. [Google Scholar] [CrossRef]

- González, R.; Gascó, J.; Llopis, J. Information Systems Outsourcing Reasons & Risks: Review & Evolution. J. Glob. Inf. Technol. Manag. 2016, 19, 223–249. [Google Scholar] [CrossRef]

- Yusuf, Y.; Menhat, M.; Abubakar, T.; Ogbuke, N. Agile capabilities as necessary conditions for maximising sustainable supply chain performance: An em-pirical investigation. Int. J. Prod. Econ. 2019, 222, 107501. [Google Scholar]

- Madavar, M.; Nezhad, M.; Aslani, A.; Naaranoja, M. Analysis of Generations of Wind Power Technologies Based on Technology Life Cycle Approach. Distrib. Gener. Altern. Energy J. 2017, 32, 52–79. [Google Scholar] [CrossRef]

- Hajmohammad, S.; Vachon, S. Mitigation, Avoidance, or Acceptance? Managing Supplier Sustainability Risk. J. Supply Chain. Manag. 2016, 52, 48–65. [Google Scholar] [CrossRef]

- Dixon, M.; Martin, A.W.; Nau, M. Social Protest & Corporate Change: Brand Visibility, Third-Party Influence, & the Responsiveness of Corporations to Activist Campaigns. Mobilization Int. Q. 2016, 21, 65–82. [Google Scholar]

- Zimmer, K.; Fröhling, M.; Schultmann, F. Sustainable supplier management—A review of models supporting sustainable supplier selection, monitoring & development. Int. J. Prod. Res. 2016, 54, 1412–1442. [Google Scholar]

- Bacon, R.; Kojima, M. Coping with Oil Price Volatility. Energy Sector Management Assistance Program (ESMAP) Energy Security Special Report; No. 005/08; World Bank: Washington, DC, USA, 2008. [Google Scholar]

- Li, W.; Choi, T.-M.; Chow, P.-S. Risk & benefits brought by formal sustainability programs on fashin enterprises under market disruption. Resour. Conserv. Recycl. 2015, 104, 348–353. [Google Scholar]

- Wewege, L.; Thomsett, M. The Digital Banking Revolution—How Fintech Companies are Transforming the Retail. Banking Industry Through Disruptive Financial Innovation, 3rd ed.; Walter de Gruyter Inc.: Boston, MA, USA; Berlin, Germany, 2019. [Google Scholar] [CrossRef]

- Ganguly, G.; Setzer, J.; Heyvaert, V. If at First You Don’t Succeed: Suing Corporations for Climate Change. Oxf. J. Leg. Stud. 2018, 38, 841–868. [Google Scholar] [CrossRef]

- Roehrich, J.; Grosvold, J.; Hoejmose, S. Reputational risks and sustainable supply chain management: Decision making under bounded rationality. Int. J. Oper. Prod. Manag. 2014, 34, 695–719. [Google Scholar] [CrossRef]

- Bowen, F. Does size matter? Organizational slack and visibility as alternative explanations for environmental responsiveness. Bus. Soc. 2002, 41, 118–124. [Google Scholar] [CrossRef]

- Reuter, C.; Foerstl, K.; Hartmann, E.; Blome, C. Sustainable global supplier management: The role of dynamic capabilities in achieving competitive advantage. J. Supply Chain. Manag. 2010, 46, 45–63. [Google Scholar] [CrossRef]

- Kleindorfer, P.; Saad, G. Managing disruption risks in supply chains. Prod. Oper. Manag. 2005, 14, 53–68. [Google Scholar] [CrossRef]

- Blome, C.; Schoenherr, T. Supply chain risk management in financial crises—A multiple case-study approach. Int. J. Prod. Econ. 2011, 134, 43–57. [Google Scholar] [CrossRef]

- Klassen, R.D.; Vereecke, A. Social issues in supply chains: Capabilities link responsibility, risk (opportunity), and performance. Int. J. Prod. Econ. 2012, 140, 103–115. [Google Scholar] [CrossRef]

- Yavari, M.; Ajalli, P. Suppliers’ coalition strategy for green-Resilient supply chain network design. J. Ind. Prod. Eng. 2021, 38, 197–212. [Google Scholar] [CrossRef]

- Ritchie, B.; Brindley, C. Supply chain risk management and performance: A guiding framework for future development. Int. J. Oper. Prod. Manag. 2007, 27, 303–322. [Google Scholar] [CrossRef]

- Jüttner, U.; Peck, H.; Christopher, M. Supply chain risk management: Outlining an agenda for future research. Int. J. Logist. Res. Appl. 2003, 6, 197–210. [Google Scholar] [CrossRef]

- Miller, K. A framework for integrated risk management in international business. J. Int. Bus. Stud. 1992, 23, 311–331. [Google Scholar] [CrossRef]

- Vose, D. Risk Analysis: A Quantitative Guide, 3rd ed.; Wiley: Hoboken, NJ, USA, 2008. [Google Scholar]

- Bai, C.; Sarkis, J. Green supplier development: Analytical evaluation using rough set theory. J. Clean. Prod. 2010, 18, 1200–1210. [Google Scholar] [CrossRef]

- Zhao, X.; Flynn, B.B.; Roth, A.V. Decision sciences research in China: Current status, opportunities, and propositions for research in supply chain management, logistics, and quality management. Decis. Sci. 2007, 38, 39–80. [Google Scholar] [CrossRef]

- Jiang, X.; Lu, K.; Xia, B.; Liu, Y.; Cui, C. Identifying Significant Risks and Analyzing Risk Relationship for Construction PPP Projects in China Using Integrated FISM-MICMAC Approach. Sustainability 2019, 11, 5206. [Google Scholar] [CrossRef]

- Seuring, S.; Muller, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Wang, Z.; Sarkis, J. Investigating the relationship of sustainable supply chain management with corporate financial performance. Int. J. Prod. Perform. Manag. 2013, 63, 871–888. [Google Scholar] [CrossRef]

- Krysiak, F. Risk management as a tool for sustainability. J. Bus. Ethics 2009, 85, 483–492. [Google Scholar] [CrossRef]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students, 8th ed.; Financial Times Prentice Hall: Harlow, UK, 2019. [Google Scholar]

- Greenbaum, T. The Handbook for Focus Group Research; Sage: Thousand Oaks, CA, USA, 1998. [Google Scholar]

- Sushil. Interpreting the Interpretive Structural Model. Glob. J. Flex. Syst. Manag. 2012, 13, 87–106. [Google Scholar] [CrossRef]

- Singh, M.; Shankar, R.; Narain, R.; Agarwal, A. An interpretive structural modeling of knowledge management in engineering industries. J. Adv. Manag. Res. 2003, 1, 28–40. [Google Scholar] [CrossRef]

- Charan, P.; Shankar, R.; Baisya, R. Analysis of interactions among the variables of supply chain performance measurement system implementation. Bus. Process. Manag. J. 2008, 14, 512–529. [Google Scholar] [CrossRef]

- Jharkharia, S.; Shankar, R. IT enablement of supply chains: Modeling the enablers. Int. J. Product. Perform. Manag. 2004, 53, 700–712. [Google Scholar] [CrossRef]

- Kumar, P.; Shankar, R.; Yadav, S. Flexibility in global supply chain: Modeling the enablers. J. Model. Manag. 2008, 3, 277–297. [Google Scholar] [CrossRef]

- Bravo, A.; Carvalho, J. Challenging times to pharmaceutical supply chains towards sustainability: A case study application. Int. J. Procure. Manag. 2014, 8, 126. [Google Scholar] [CrossRef]

- Gao, T.; Erokhin, V.; Arskiy, A. Dynamic Optimization of Fuel and Logistics Costs as a Tool in Pursuing Economic Sustainability of a Farm. Sustainability 2019, 11, 5463. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Risk (Sources and Consequences) | Description | Dimension | Origins | Response | References |

|---|---|---|---|---|---|

| Energy consumption | Inefficient energy use for the operations | EN | IN | MI, PR | [53,54] |

| Environmental accidents | Accidents in operations that affect the environment. | EN | IN | MI, PR, RE, CO, IN | [48,55] |

| Greenhouse gases | Emission of gases that contribute to the greenhouse effect | EN | IN | PR, AV, SH | [56] |

| Legal and responsibility | Failure of regulations. Liability to 3rd party companies. Unfair wages. Complexity in legislation. Delays in the process. | EN, SO, EC | IN/ EX | MI, PR, CO, IN, CT, AV | [52] |

| Ecological damage/Pollution | Air, water or soil contamination due operations or products. Interruptions in operations caused by ecological issues. Interference in habitats of endangered species. | EN | IN | RE, AV, SH | [43,48] |

| Excessive product waste | Unwanted material produced during or as a result of a process. | EN | IN | MI | [51] |

| Packaging | Failure to meet packaging standards or excessive packaging. | EN | IN | MI, RE | [48,57] |

| Natural disasters | Disruptions caused by natural disasters (hurricanes, flood, storms, severe weather conditions). | EN | EX | MI, RE, CO, IN, | [58,59] |

| Heatwaves, droughts | Increase in temperature due to climatic change. | EN | EX | MI, RE, CO, IN, | [60,61] |

| Water scarcity | Lack of water to meet the demands of operation. | EN | EX | MI, PR, IN | [62] |

| Child/forced labor | Depriving children of their childhood, harmful to develop. | SO | IN | MI, PR, AV, SH | [63,64] |

| Discrimination | Prejudicial treatment based on difference. | SO | IN | MI, PR, TR | [65] |

| Dangerous working environment | Working under unhealthy or untrusting conditions. | SO | IN | MI, PR, RE, CO | [61,66] |

| Inhumane treatment | Violating an individual’s dignity. | SO | IN | MI, PR | [67] |

| Labor force unavailability risk | Lack of trained HR. Delays due to lack of management expertise. Including unavailability due to occupational risk exposure. | SO | IN | MI, PR, RE, IN | [68] |

| Unethical treatment of animals | Treat animals cruelly, cause suffering or pain. | SO | IN | MI, PR, RE | [69,70] |

| Excessive working time | Heavy workloads and job demand beyond legal requirements. | SO | IN | MI, PR, RE, CO | [71] |

| Demographic challenges | Employment—related to immigration, ageing and population growth. | SO | EX | MI | [72] |

| Pandemic | An epidemic over a wide area, crossing boundaries. | SO | EX | PR, RT | [73] |

| Security risk/Social Instability/unrest | Strikes, work stoppages, street protests, demonstrations, terrorism. Attacks on installations. Equipment theft. Vandalism. | SO | EX | MI, RE, CO | [74,75] |

| Antitrust claims/Price fixing | Claims arising against a company that violate competition laws (cartels, predatory pricing). | EC | IN | MI, PR, RE, IN, AV | [76,77] |

| Bribery/Corruption | Offer (accept) a potential partner in exchange for business benefit. | EC | IN | PR, IN | [77,78] |

| Transport risk | Breaks during transportation. Accidents. Thefts. Damages. Natural disasters affecting the transportation stage. | EC | IN | MI, PR, AV | [79,80] |

| Third-party service | Non-compliance of outsourced services. A breach or lack of financing of contracted and subcontracted suppliers. | EN, SO, EC | IN | MI, PR, RE, IN, CO | [81] |

| Technology and innovation risk | Inaccuracies in incapacity definition. Technological obsolescence. Damage and breakage attributable to design or project sizing. | EC | IN | MI, PR, RE, IN, CO | [6,82,83] |

| Tax avoidance/ evasion | Illegal attempt to reduce the tax amount payable by fraudulent means. | EC | IN | MI, PR | [84] |

| Boycotts/Public opposition risk | Not buying from, or dealing with, an organization as a protest. Potential changes in public opinion. Conflicts over land-use restrictions. Changes in public policies affecting nearby communities. | EC | EX | PR, RE, RT | [85,86] |

| Energy prices volatility | Unpredictable, continuous energy and fuel price variation. | EC | EX | MI, IN, RT | [53,87] |

| Financial Risk | Sudden loss of a large part of the nominal value of financial assets, lack and/or loss of capital. Exchange rate variation. Cost volatility. | EC | EX | MI, RT, | [88,89] |

| Litigations | Lawsuits against a company for sustainability-related issues. | EC | EX | PR, CO, AV | [90] |

| Original Item | Example |

|---|---|

| Insure (IN) | Insurance and develop an internal information system. |

| Retain (RT) | Accept risk if penalties are low, adapt to a new reality. |

| Prevent (PR) | Monitor CO2 footprint across the supply chain. |

| Reduce (RE) | Sustainable waste management by adoption of new technology. |

| Mitigate (MI) | Plans for potential accidents, improve environmental audits. |

| Cooperate (CP) | Build flexible supply chain; close industry collaboration. |

| Avoid (AV) | Avoid countries with poor transparency records, and with child labor. |

| Share (SH) | Sustainability audit with critical suppliers. |

| Transfer (TR) | Employ legal services to deal with equal opportunities. |

| Control (CO) | Acquire environmental and social certification. |

| Expert | Type of Activity | Designation | Years of Working Experience |

|---|---|---|---|

| 1 | Cosmetic Producer | Senior Operations Manager | 15 |

| 2 | Cosmetic Producer | Operations Manager | 12 |

| 3 | Logistics Operator | Logistics Manager | 9 |

| 4 | Retailer | Procurement Manager | 11 |

| 5 | Cosmetic Supply Chain Consulting | SC Consulting | 17 |

| 6 | Cosmetic Producer | Financial Director | 11 |

| 7 | Cosmetic Producer | Operations Manager | 8 |

| 8 | Cosmetic Producer | Logistics Analyst | 13 |

| 9 | Retailer | Procurement Manager | 19 |

| 10 | Cosmetic Supply Chain Consulting | Operational Director | 27 |

| C[i/j] | R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 |

|---|---|---|---|---|---|---|---|---|---|---|

| R1 | - | A | A | A | A | A | A | A | A | A |

| R2 | - | O | V | O | A | A | X | O | X | |

| R3 | - | O | V | O | O | O | O | O | ||

| R4 | - | A | O | A | A | A | A | |||

| R5 | - | O | A | V | V | O | ||||

| R6 | - | A | A | V | A | |||||

| R7 | - | O | O | O | ||||||

| R8 | - | V | V | |||||||

| R9 | - | O | ||||||||

| R10 | - |

| C[i/j] | R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 |

|---|---|---|---|---|---|---|---|---|---|---|

| R1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| R2 | 1 | 1 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 1 |

| R3 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| R4 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| R5 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | 1 | 0 |

| R6 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 0 |

| R7 | 1 | 1 | 0 | 1 | 1 | 1 | 1 | 0 | 0 | 0 |

| R8 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 1 | 1 |

| R9 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 |

| R10 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 1 |

| C[i/j] | R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 | DVP |

|---|---|---|---|---|---|---|---|---|---|---|---|

| R1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| R2 | 1 | 1 | 0 | 1 | 0 | 1* | 0 | 1 | 1* | 1 | 7 |

| R3 | 1 | 1* | 1 | 1* | 1 | 1* | 0 | 1* | 1* | 1* | 9 |

| R4 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 2 |

| R5 | 1 | 1* | 0 | 1 | 1 | 1* | 0 | 1 | 1 | 1* | 8 |

| R6 | 1 | 1 | 0 | 1* | 0 | 1 | 0 | 1* | 1 | 1* | 7 |

| R7 | 1 | 1 | 0 | 1 | 1 | 1 | 1 | 1* | 1* | 1* | 9 |

| R8 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 7 |

| R9 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 3 |

| R10 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 1* | 1* | 1 | 7 |

| DPP | 10 | 7 | 1 | 9 | 3 | 7 | 1 | 7 | 8 | 7 |

| Risks | Reachability Set | Antecedent Set | Intersection 1 | Level |

| Risks | Reachability Set | Antecedent Set | Intersection 1 | Level |

| R1 | {1} | {1,2,3,4,5,6,7,8,9,10} | {1} | I |

| R2 | {1,2,4,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R3 | {1,2,3,4,5,6,8,9,10} | {3} | {3} | |

| R4 | {1,4} | {2,3,4,5,6,7,8,10} | {4} | |

| R5 | {1,2,4,5,6,8,9,10} | {3,5,7} | {5} | |

| R6 | {1,2,4,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R7 | {1,2,4,5,6,7,8,9,10} | {7} | {7} | |

| R8 | {1,2,4,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| R9 | {1,4,9} | {2,3,5,6,7,8,9,10} | {9} | |

| R10 | {1,2,4,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| Risks | Reachability Set | Antecedent Set | Intersection 2 | Level |

| R2 | {2,4,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R3 | {2,3,4,5,6,8,9,10} | {3} | {3} | |

| R4 | {4} | {2,3,4,5,6,7,8,10} | {4} | II |

| R5 | {2,4,5,6,8,9,10} | {3,5,7} | {5} | |

| R6 | {2,4,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R7 | {2,4,5,6,7,8,9,10} | {7} | {7} | |

| R8 | {2,4,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| R9 | {4,9} | {2,3,5,6,7,8,9,10} | {9} | |

| R10 | {2,4,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| Risks | Reachability Set | Antecedent Set | Intersection 3 | Level |

| R2 | {2,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R3 | {2,3,5,6,8,9,10} | {3} | {3} | |

| R5 | {2,5,6,8,9,10} | {3,5,7} | {5} | |

| R6 | {2,6,8,9,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | |

| R7 | {2,5,6,7,8,9,10} | {7} | {7} | |

| R8 | {2,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| R9 | {9} | {2,3,5,6,7,8,9,10} | {9} | III |

| R10 | {2,6,8,9,10} | {2,3,5,6,7,8,9,10} | {2,6,8,9,10} | |

| Risks | Reachability Set | Antecedent Set | Intersection 4 | Level |

| R2 | {2,6,8,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | IV |

| R3 | {2,3,5,6,8,10} | {3} | {3} | |

| R5 | {2,5,6,8,10} | {3,5,7} | {5} | |

| R6 | {2,6,8,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | IV |

| R7 | {2,5,6,7,8,10} | {7} | {7} | |

| R8 | {2,6,8,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | IV |

| R10 | {2,6,8,10} | {2,3,5,6,7,8,10} | {2,6,8,10} | IV |

| Risks | Reachability Set | Antecedent Set | Intersection 5 | Level |

| R3 | {3,5} | {3} | {3} | |

| R5 | {5} | {3,5,7} | {5} | V |

| R7 | {5,7} | {7} | {7} | |

| Risks | Reachability Set | Antecedent Set | Intersection 6 | Level |

| R3 | {3} | {3} | {3} | VI |

| R7 | {7} | {7} | {7} | VI |

| Item | Risk factors | Level | Zones | Risk Response and Practices |

|---|---|---|---|---|

| R1 | Financial | L1 | Z4 | TR—Engage financial institutions to support liquidity |

| R2 | Labor Force | L4 | Z3 | CP—Engage with suppliers, industry bodies, NGOs to monitor wages |

| R3 | Technology and Innovation | L6 | Z1 | PR—Apply management practices in integrated systems RT—Accept risk if penalties are low |

| R4 | Boycotts | L2 | Z4 | RE—Collaborate with tax collection authorities RT—Accept risk if penalties are low |

| R5 | Transportation | L5 | Z1 | IN—Insure against accidents |

| R6 | Natural Hazard | L4 | Z3 | MI—Contingency plan for SC resilience IN—Insure against disaster |

| R7 | Legal and Responsibility | L6 | Z1 | PR—Collect and disseminate regulatory information to ensure compliance SH—Conduct sustainability audit with key suppliers |

| R8 | Third-Party Service | L4 | Z3 | SH—Conduct sustainability audit with key suppliers RT—Accept risk if penalties are low |

| R9 | Ecological Damage | L3 | Z4 | AV—Locate facility away from urban areas IN—Insure against accidents RT—Accept risk if penalties are low |

| R10 | Security | L4 | Z3 | RE—Contingency plans for remote work to ensure resilience in operation IN—Ensure staff against pandemic |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Romano, A.L.; Ferreira, L.M.D.F.; Caeiro, S.S.F.S. Modelling Sustainability Risk in the Brazilian Cosmetics Industry. Sustainability 2021, 13, 13771. https://doi.org/10.3390/su132413771

Romano AL, Ferreira LMDF, Caeiro SSFS. Modelling Sustainability Risk in the Brazilian Cosmetics Industry. Sustainability. 2021; 13(24):13771. https://doi.org/10.3390/su132413771

Chicago/Turabian StyleRomano, André Luiz, Luís Miguel D. F. Ferreira, and Sandra Sofia F. S. Caeiro. 2021. "Modelling Sustainability Risk in the Brazilian Cosmetics Industry" Sustainability 13, no. 24: 13771. https://doi.org/10.3390/su132413771

APA StyleRomano, A. L., Ferreira, L. M. D. F., & Caeiro, S. S. F. S. (2021). Modelling Sustainability Risk in the Brazilian Cosmetics Industry. Sustainability, 13(24), 13771. https://doi.org/10.3390/su132413771