Towards Sustainable Finance: Conceptualizing Future Generations as Stakeholders

Abstract

1. Introduction

2. Materials and Methods

2.1. Research Design

- Literature review and content analysis,

- Critical analysis of the stakeholder theory,

- Analysis of the connection between the stakeholder theory and sustainable finance, and

- Substantiation of the proposal to conceptualize future generations as stakeholders.

2.2. Theoretical Background

- If this decision is implemented, whom does it create value for and whom does it destroy?

- Who benefits or suffers from the respective decision?

- Whose rights are activated, and who makes value following the decision implementation, but also in whose case these things do not apply?

3. Results and Discussion

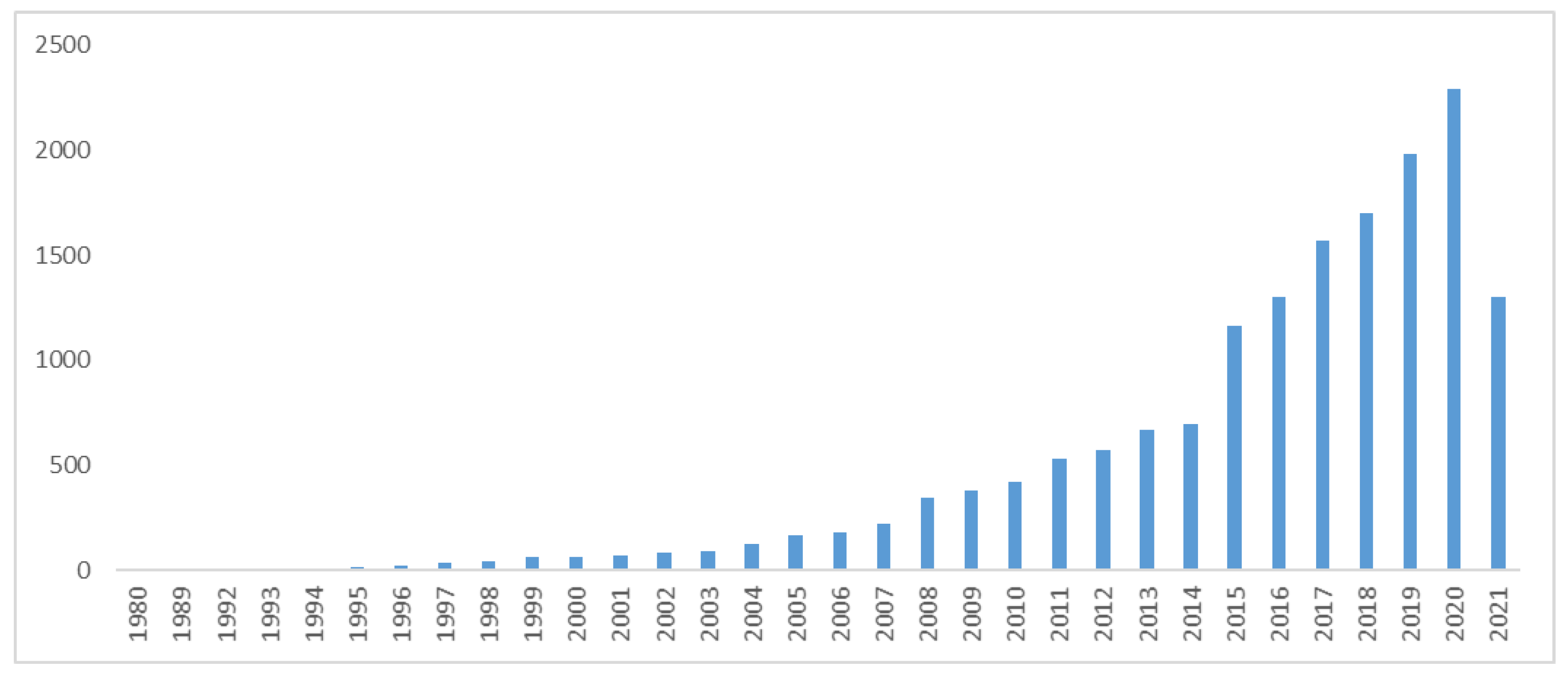

3.1. Current Developments in the Field of Sustainable Finance

3.2. Best vs. Good in the Short, Medium, and Long Term

3.3. Legal vs. Moral

- SDG financing, that is, directing a part of the financial resources in the direction of programs and projects that fall within SDGs, and

- Reconsideration of the investment methods and styles, redirecting them towards a vision focused on the future and on the diminishing of inequalities. The orientation towards the future should imply a decrease in casino capitalism practices. In addition, investments should consider the impact they have on the environment (future generations).

3.4. Investors as Actors of Sustainable Finance

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Smith, A. Wealth of Nations (Avuția Națiunilor); Publica: Bucharest, Romania, 2011; p. 45. [Google Scholar]

- Coase, R.H. The Nature of the Firm. Economica 1937, 4, 386–405. [Google Scholar] [CrossRef]

- Demsetz, A.; Alchian, H. Production, Information Costs, and Economic Organization. Am. Econ. Rev. 1972, 62, 777–795. [Google Scholar]

- Meckling, M.C.; Jensen, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman Publishing: London, UK, 1984. [Google Scholar]

- VOSviewer. Available online: https://www.vosviewer.com/ (accessed on 11 September 2021).

- Schonberger, R.J. MIS Design: A Contingency Approach. MIS Q. 1980, 4, 13. [Google Scholar] [CrossRef]

- Cornell, B.; Shapiro, A. Corporate Stakeholders and Corporate Finance. Financ. Manag. 1987, 16, 5–14. [Google Scholar] [CrossRef]

- Barton, S.L.; Hill, N.C.; Sundaram, S. An Empirical Test of Stakeholder Theory Predictions of Capital Structure. Financ. Manag. 1989, 18, 36–44. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Perkin, H. The Third Revolution and Stakeholder Capitalism: Convergence or Collapse? Political Q. 1996, 67, 198–208. [Google Scholar] [CrossRef]

- Wijnberg, N.M. Normative stakeholder theory and Aristotle: The link between Ethics and Politics. J. Bus. Ethics 2000, 25, 329–342. [Google Scholar] [CrossRef]

- Hendry, J. Economic contracts versus social relationships as a foundation for normative stakeholder theory. Bus. Ethics A Eur. Rev. 2001, 10, 223–232. [Google Scholar] [CrossRef]

- Kaller, J. Differentiating Stakeholder Theories. J. Bus. Ethics 2003, 46, 71–83. [Google Scholar] [CrossRef]

- Freeman, R.; Martin, K.; Parmar, B. Stakeholder Capitalism. J. Bus. Ethics 2007, 74, 303–314. [Google Scholar] [CrossRef]

- Stieb, J.A. Assessing Freeman’s Stakeholder Theory. J. Bus. Ethics 2009, 87, 401–414. [Google Scholar] [CrossRef]

- Bonnafous-Boucher, M.; Porcher, S. Towards a stakeholder society: Stakeholder theory vs theory of civil society. Eur. Manag. Rev. 2010, 7, 205–216. [Google Scholar] [CrossRef]

- Freeman, R.E.; Wicks, A.C.; Parmar, B. Stakeholder Theory as a Basis for Capitalism. Corp. Soc. Responsib. Corp. Gov. 2011, 149, 52–72. [Google Scholar] [CrossRef]

- Hasnas, J. Whither Stakeholder Theory? A Guide for the Perplexed Revisited. J. Bus. Ethics 2012, 112, 47–57. [Google Scholar] [CrossRef]

- Freeman, R.E.; Phillips, R.; Sisodia, R. Tensions in Stakeholder Theory. Bus. Soc. 2018, 59, 1–19. [Google Scholar] [CrossRef]

- Barney, J.; Harrison, J. Stakeholder Theory at the Crossroads. Bus. Soc. 2020, 59, 1–10. [Google Scholar] [CrossRef]

- Valentinov, V.; Roth, S.; Will, M. Stakeholder Theory: A Luhmannian Perspective. Adm. Soc. 2018, 51, 826–849. [Google Scholar] [CrossRef]

- Freeman, R.; Harrison, J.; Wicks, A. Managing for Stakeholders: Survival, Reputation and Success; Yale University Press: New Haven, CT, USA; London, UK, 2007. [Google Scholar]

- Phillips, R. Stakeholder Theory and Organizational Ethics; Berrett-Koehler Publishers: Oakland, CA, USA, 2003. [Google Scholar]

- Clark, I. Another third way? VW and the trials of stakeholder capitalism. Ind. Relat. J. 2006, 37, 593–606. [Google Scholar] [CrossRef]

- Brennan, D.M. “Fiduciary Capitalism,” the ‘Political Model of Corporate Governance’ and the Prospect of Stakeholder Capitalism in the United States. Rev. Radic. Political Econ. 2005, 37, 39–62. [Google Scholar] [CrossRef]

- Dragneva, R.; Simons, W. Corporate governance revisited: Can the stakeholder paradigm provide a way out of ‘Vulture’ capitalism in Eastern Europe? Rev. Cent. East Eur. Law 2001, 27, 93–111. [Google Scholar] [CrossRef]

- Allen, F.; Carletti, E.; Marquez, R.S. Stakeholder Capitalism, Corporate Governance and Firm Value. In EFA 2007 Ljubljana Meetings Paper, European Corporate Governance Institute (ECGI)—Finance Working Paper No. 190/2007; 2009; Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=968141 (accessed on 15 July 2021). [CrossRef]

- Hansen, M.B.; Vedung, E. Theory-Based Stakeholder Evaluation. Am. J. Eval. 2010, 31, 295–313. [Google Scholar] [CrossRef]

- Petrick, J.A. Sustainable Stakeholder Capitalism and Redesigning Management Education. J. Corp. Citizsh. 2010, 101–126. Available online: https://ur.booksc.eu/dl/54990873/456df7 (accessed on 27 June 2021). [CrossRef]

- Petrick, J.A. Sustainable Stakeholder Capitalism: A Moral Vision of Responsible Global Financial Risk Management. J. Bus. Ethics 2011, 99, 93–109. [Google Scholar] [CrossRef]

- Wu, J.; Wokutch, R. Confucian Stakeholder Theory: An Exploration. Bus. Soc. Rev. 2015, 120, 1–21. [Google Scholar] [CrossRef]

- Willmott, H.; Parker, M.; Perrow, C.; Bos, R.; Beverungen, A.; Calas, M.; Thompson, G.; Morgan, G.; Clegg, S.; Ahonen, P.; et al. The Modern Corporation Statement on Management. SSRN Electron. J. 2016. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2863077 (accessed on 26 June 2021). [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L. Sustainable Finance and the 2030 Agenda: Investing to Transform the World. Sustainability 2021, 13, 10505. [Google Scholar] [CrossRef]

- Bruntland, G.H. Our common future—Call for action. Environ. Conserv. 1987, 14, 291–294. [Google Scholar] [CrossRef]

- Matakanye, R.M.; van der Poll, H.M.; Muchara, B. Do Companies in Different Industries Respond Differently to Stakeholders’ Pressures When Prioritising Environmental, Social and Governance Sustainability Performance? Sustainability 2021, 13, 12022. [Google Scholar] [CrossRef]

- Lambrechts, W.; Son-Turan, S.; Reis, L.; Semeijn, J. Lean, Green and Clean? Sustainability Reporting in the Logistics Sector. Logistics 2019, 3, 3. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research Progress and Future Prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Montenegro, T.M. Tax Evasion, Corporate Social Responsibility and National Governance: A Country-Level Study. Sustainability 2021, 13, 11166. [Google Scholar] [CrossRef]

- Amon, J.; Rammerstorfer, M.; Weinmayer, K. Passive ESG Portfolio Management—The Benchmark Strategy for Socially Responsible Investors. Sustainability 2021, 13, 9388. [Google Scholar] [CrossRef]

- Orts, E.; Strudler, A. The Ethical and Environmental Limits of Stakeholder Theory. Bus. Ethics Q. 2002, 12, 215–233. [Google Scholar] [CrossRef]

- Buchanan, J.; Tullok, G. The Calculus of Consent. The Logical Foundations of Constitutional Democracy; University of Michigan Press: Ann Arbor, MI, USA, 1965. [Google Scholar]

- Sober, E. Philosophical problems for environmentalism. In the Preservation of Species; Princeton University Press: Princeton, NJ, USA, 1988; pp. 173–194. [Google Scholar] [CrossRef]

- Micklethwait, J.; Wooldridge, A. The Company. A Short History of a Revolutionary Idea; Modern Library: New York, NY, USA, 2003. [Google Scholar]

- United Nations. Division for Sustainable Development Goals. Available online: https://sdgs.un.org/goals (accessed on 11 September 2021).

- Abrudan, L.C.; Matei, M.C.; Abrudan, M.M. Possibilities and Limitations of the SDG and ESG Implementation in Romania. A Financial and Managerial Approach. In Proceedings of the 17th International Conference on European Integration—New Challenges-EINCO, Oradea, Romania, 27–28 May 2021; University of Oradea Publishing: Oradea, Romania, 2021. [Google Scholar]

- Mazzullo, A. Rethinking taxation of impact investments. In Contemporary Issues in Sustainable Finance; Springer: Berlin/Heidelberg, Germany, 2020; pp. 37–59. [Google Scholar] [CrossRef]

- Rutkauskas, A.V.; Miečinskiene, A.; Stasytyte, V. Investment decisions modelling along sustainable development concept on financial markets. Technol. Econ. Dev. Econ. 2008, 14, 417–427. [Google Scholar] [CrossRef]

- Kiernan, M.J. Universal Owners and ESG: Leaving money on the table? Corp. Gov. Int. Rev. 2007, 15, 478–485. [Google Scholar] [CrossRef]

- MacLean, R. ESG comes of age. Environ. Qual. Manag. 2012, 22, 99–108. [Google Scholar] [CrossRef]

- Equator Principles. Available online: https://equator-principles.com/about/ (accessed on 15 September 2021).

- Eisenbach, S.; Schiereck, D.; Trillig, J.; von Flotow, P. Sustainable Project Finance, the Adoption of the Equator Principles and Shareholder Value Effects. Bus. Strategy Environ. 2013, 23, 375–394. [Google Scholar] [CrossRef]

- Badulescu, D.; Simut, R.; Badulescu, A.; Badulescu, A.V. The Relative Effects of Economic Growth, Environmental Pollution and Non-Communicable Diseases on Health Expenditures in European Union Countries. Int. J. Environ. Res. Public Health 2019, 16, 5115. [Google Scholar] [CrossRef]

- The IUCN Red List of Threatened Species. Available online: https://www.iucnredlist.org/ (accessed on 21 January 2021).

- Top 10 Most Endangered Animals. One Kind Planet 2020. Available online: https://onekindplanet.org/top-10/top-10-worlds-most-endangered-animals/ (accessed on 21 January 2021).

- Morris, S. Rich soup of life’ in Gwent wetlands at risk from motorway. The Guardian 2018. Available online: https://www.theguardian.com/uk-news/2018/nov/18/gwent-levels-wetlands-biodiversity-risk-wales-motorway (accessed on 15 January 2021).

- Balch, O. Meet the world’s first ’minister for future generations’. The Guardian 2019. Available online: https://www.theguardian.com/world/2019/mar/02/meet-the-worlds-first-future-generations-commissioner (accessed on 15 January 2021).

- Gessner, L. Knesset Commission for Future Generations. 2017. Available online: http://www.fdsd.org/ideas/knesset-commission-future-generations/ (accessed on 15 January 2021).

- About the OAG. Who we are. Office of the Auditor General of Canada. Available online: https://www.oag-bvg.gc.ca/internet/English/au_fs_e_370.html#Commissioner (accessed on 15 January 2021).

- Merriam-Webster. 2021. Available online: https://www.merriam-webster.com/dictionary/autopoiesis (accessed on 10 September 2021).

- Shutterstock. Available online: https://www.shutterstock.com/ro/image-photo/child-hands-holding-crystal-earth-globe-1919469722 (accessed on 17 September 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Critical Distortions | Friendly Misinterpretations |

|---|---|

| The stakeholder theory is an excuse for managerial opportunism (Jensen, 2000; Marcoux, 2000; Sternberg, 2000). | The stakeholder theory requires changes to the current law (Hendry, 2001a, 2001b; Van Buren, 2001). |

| The stakeholder theory cannot provide a sufficiently specific objective for the corporation (Jensen, 2000). | The stakeholder theory is socialism and refers to the entire economy (Barnett, 1997; Hutton, 1995; Rustin, 1997). |

| The stakeholder theory is primarily concerned with distribution of financial outputs (Marcoux, 2000). | The stakeholder theory is a comprehensive moral doctrine (Orts & Strudler, 2002). |

| All stakeholders must be treated equally (Gioia, 1999; Marcoux, 2000; Sternberg, 2000). | The stakeholder theory applies only to corporations (Donaldson & Preston, 1995). |

| Investors’ MSV-based approach | |

| Pros | Cons |

| A traditional way of investing with significant knowledge in the background | Ethical issues (conflicts or misdemeanors) that may conclude in boycotts from different stakeholders |

| Easy measurable outcomes | A lack of consideration regarding future generations and other stakeholders |

| More control over the entire process | A defining selfish approach |

| Investors’ ESG-based approach | |

| Pros | Cons |

| A more environmentally friendly investment method | A relatively new way of conducting the business process with insufficient grounded knowledge in the background |

| Momentarily social and governance issues are considered | Difficulties in the measuring of outcomes |

| Future generations’ interests are regarded; impact investments can produce beneficial effects in the future | A relative lack of control over some parts of the process |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abrudan, L.-C.; Matei, M.-C.; Abrudan, M.-M. Towards Sustainable Finance: Conceptualizing Future Generations as Stakeholders. Sustainability 2021, 13, 13717. https://doi.org/10.3390/su132413717

Abrudan L-C, Matei M-C, Abrudan M-M. Towards Sustainable Finance: Conceptualizing Future Generations as Stakeholders. Sustainability. 2021; 13(24):13717. https://doi.org/10.3390/su132413717

Chicago/Turabian StyleAbrudan, Leonard-Călin, Mirabela-Constanța Matei, and Maria-Madela Abrudan. 2021. "Towards Sustainable Finance: Conceptualizing Future Generations as Stakeholders" Sustainability 13, no. 24: 13717. https://doi.org/10.3390/su132413717

APA StyleAbrudan, L.-C., Matei, M.-C., & Abrudan, M.-M. (2021). Towards Sustainable Finance: Conceptualizing Future Generations as Stakeholders. Sustainability, 13(24), 13717. https://doi.org/10.3390/su132413717