Resilience in Vulnerable Small and New Social Enterprises

Abstract

:1. Introduction

2. Predicting Vulnerability with Financial Ratios

3. Financial Ratio Analysis in Social Enterprises

4. Hypotheses Development

5. Materials and Methods

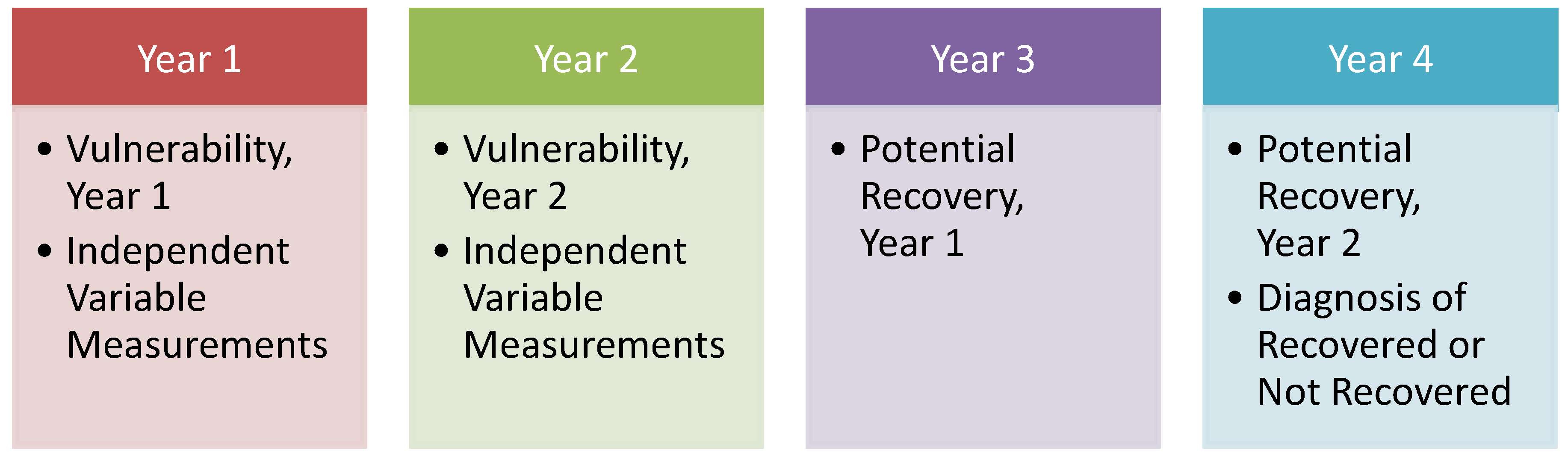

5.1. Data Source

5.2. Sample Selection

5.3. Dependent Variables

5.4. Independent Variables

5.5. Model Specification

6. Results

6.1. Equity Ratio

6.2. Surplus Ratio

6.3. Revenue Diversification

6.4. Size

6.5. Age

6.6. Control Variables

7. Robustness Tests

7.1. Robustness 1: Age Quadratic

7.2. Robustness Test 2: Standardization by Total Assets

8. Discussion and Practical Applications

8.1. Equity Ratio

8.2. Surplus Ratio

8.3. Revenue Concentration

8.4. Size

8.5. Age

9. Limitations

10. Conclusions and Policy Implications

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Harrison, T.D.; Laincz, C.A. Entry and exit in the nonprofit sector. BE J. Econ. Anal. Policy 2008, 8, 1–42. [Google Scholar] [CrossRef]

- Calabrese, T.D. Do Donors Penalize Nonprofit Organizations with Accumulated Wealth? Public Adm. Rev. 2011, 71, 859–869. [Google Scholar] [CrossRef]

- Calabrese, T.D. Testing Competing Capital Structure Theories of Nonprofit Organizations. Public Budg. Financ. 2011, 31, 119–143. [Google Scholar] [CrossRef]

- Ashley, S.; Faulk, L. Nonprofit competition in the grants marketplace. Nonprofit Manag. Leadersh. 2010, 21, 43–57. [Google Scholar] [CrossRef]

- Bowman, W.; Tuckman, H.P.; Young, D.R. Issues in Nonprofit Finance Research: Surplus, Endowment, and Endowment Portfolios. Nonprofit Volunt. Sect. Q. 2011, 41, 560–579. [Google Scholar] [CrossRef]

- Kearns, K. Income portfolios. In Financing Nonprofits: Putting Theory into Practice; Young, D.R., Ed.; Edward Elgar: Cheltenham, UK, 2007; pp. 291–314. [Google Scholar]

- Kingma, B.R. Portfolio theory and nonprofit financial stability. Nonprofit Volunt. Sect. Q. 1993, 22, 105–119. [Google Scholar] [CrossRef]

- Mayer, W.J.; Wang, H.-c.; Egginton, J.F.; Flint, H.S. The Impact of Revenue Diversification on Expected Revenue and Volatility for Nonprofit Organizations. Nonprofit Volunt. Sect. Q. 2014, 43, 374–392. [Google Scholar] [CrossRef]

- Young, D.R.; Wilsker, A.L.; Grinsfelder, M.C. Understanding the determinants of nonprofit income portfolios. Volunt. Sect. Rev. 2010, 1, 161–173. [Google Scholar] [CrossRef]

- Sparviero, S. The case for a socially oriented business model canvas: The social enterprise model canvas. J. Soc. Entrep. 2019, 10, 232–251. [Google Scholar] [CrossRef] [Green Version]

- Osorio-Novela, G.; Mungaray-Lagarda, A.; Ramírez-Angulo, N. Social Enterprise in Mexico, a New Business Classification. Sustainability 2021, 13, 9264. [Google Scholar] [CrossRef]

- Bardach, E.; Lesser, C. Accountability in Human Services Collaboratives—For What? and to Whom? J. Public Adm. Res. Theory 1996, 6, 197–224. [Google Scholar] [CrossRef]

- Finkler, S.; Purtell, R.; Calabrese, T.D.; Smith, D. Financial Management for Public, Health, and Not-for-Profit Organizations; Pearson: New York, NY, USA, 2013. [Google Scholar]

- Barman, E.A. Asserting Difference: The Strategic Response of Nonprofit Organizations to Competition. Soc. Forces 2002, 80, 1191–1222. [Google Scholar] [CrossRef]

- Gertler, P.; Kuan, J. Does It Matter Who Your Buyer Is? The Role of Nonprofit Mission in the Market for Corporate Control of Hospitals. J. Law Econ. 2009, 52, 295–306. [Google Scholar] [CrossRef]

- Kalleberg, A.L.; Marsden, P.V.; Reynolds, J.; Knoke, D. Beyond Profit? Sectoral Differences in High-Performance Work Practices. Work Occup. 2006, 33, 271–302. [Google Scholar] [CrossRef]

- Ruvio, A.; Rosenblatt, Z.; Hertz-Lazarowitz, R. Entrepreneurial leadership vision in nonprofit vs. for-profit organizations. Leadersh. Q. 2010, 21, 144–158. [Google Scholar] [CrossRef]

- Wolff, N.; Schlesinger, M. Access, Hospital Ownership, and Competition between For-Profit and Nonprofit Institutions. Nonprofit Volunt. Sect. Q. 1998, 27, 203–236. [Google Scholar] [CrossRef]

- Accounts receivable management in nonprofit organizations. Zesz. Teor. Rachun. 2012, 68, 83–96.

- Chapelle, K. Non-profit and for-profit entrepreneurship: A trade-off under liquidity constraint. Int. Entrep. Manag. J. 2010, 6, 55–80. [Google Scholar] [CrossRef]

- Tracey, P.; Phillips, N. The distinctive challenge of educating social entrepreneurs: A postscript and rejoinder to the special issue on entrepreneurship education. Acad. Manag. Learn. Educ. 2007, 6, 264–271. [Google Scholar] [CrossRef]

- Costa, E.; Andreaus, M. Social impact and performance measurement systems in an Italian social enterprise: A participatory action research project. J. Public Budg. Account. Financ. Manag. 2021, 33, 289–313. [Google Scholar] [CrossRef]

- Rawhouser, H.; Cummings, M.; Newbert, S.L. Social impact measurement: Current approaches and future directions for social entrepreneurship research. Entrep. Theory Pract. 2019, 43, 82–115. [Google Scholar] [CrossRef] [Green Version]

- Hudon, M.; Labie, M.; Reichert, P. What is a fair level of profit for social enterprise? Insights from microfinance. J. Bus. Ethics 2020, 162, 627–644. [Google Scholar] [CrossRef]

- Kruse, P.; Wach, D.; Wegge, J. What motivates social entrepreneurs? A meta-analysis on predictors of the intention to found a social enterprise. J. Small Bus. Manag. 2021, 59, 477–508. [Google Scholar] [CrossRef]

- Cohen, H.; Kaspi-Baruch, O.; Katz, H. The social entrepreneur puzzle: The background, personality and motivation of Israeli social entrepreneurs. J. Soc. Entrep. 2019, 10, 211–231. [Google Scholar] [CrossRef]

- Barton, M.; Schaefer, R.; Canavati, S. To be or not to be a social entrepreneur: Motivational drivers amongst American business students. Entrep. Bus. Econ. Rev. 2018, 6, 9–35. [Google Scholar] [CrossRef]

- Tuckman, H.P.; Chang, C.F. A methodology for measuring the financial vulnerability of charitable nonprofit organizations. Nonprofit Volunt. Sect. Q. 1991, 20, 445–460. [Google Scholar] [CrossRef]

- Cordery, C.J.; Sim, D.; Baskerville, R.F. Three models, one goal: Assessing financial vulnerability in New Zealand amateur sports clubs. Sport Manag. Rev. 2013, 16, 186–199. [Google Scholar] [CrossRef]

- Dayson, C. Understanding financial vulnerability in UK third sector organisations: Methodological considerations and applications for policy, practice and research. Volunt. Sect. Rev. 2013, 4, 19–38. [Google Scholar] [CrossRef]

- Greenlee, J.S.; Trussel, J.M. Predicting the Financial Vulnerability of Charitable Organizations. Nonprofit Manag. Leadersh. 2000, 11, 199–210. [Google Scholar] [CrossRef]

- Hager, M.A. Financial Vulnerability among Arts Organizations: A Test of the Tuckman-Chang Measures. Nonprofit Volunt. Sect. Q. 2001, 30, 376–392. [Google Scholar] [CrossRef] [Green Version]

- Hodge, M.M.; Piccolo, R.F. Funding source, board involvement techniques, and financial vulnerability in nonprofit organizations: A test of resource dependence. Nonprofit Manag. Leadersh. 2005, 16, 171–190. [Google Scholar] [CrossRef]

- Keating, E.; Fischer, M.; Gordon, T.; Greenlee, J. Assessing Financial Vulnerability in the Nonprofit Sector; KSG Working Paper No. RWP05-002; Hauser Center for Nonprofit Organizations: Cambridge, MA, USA, 2005. [Google Scholar]

- Lecy, J.; Van Slyke, D.; Yoon, N. What Do We Know About Nonprofit Entrepreneurs?: Results from a Large-Scale Survey. 2016. Available online: http://dx.doi.org/10.2139/ssrn.2890231 (accessed on 6 December 2021).

- Matthiesen, J.A. Searching For Organizational Effectiveness by Examining Financial Vulnerability and Nonprofit Failure. 2009. Available online: http://scholarsbank.uoregon.edu/xmlui/handle/1794/9837 (accessed on 6 December 2021).

- Trussel, J.M. Revisiting the Prediction of Financial Vulnerability. Nonprofit Manag. Leadersh. 2002, 13, 17–31. [Google Scholar] [CrossRef]

- Tevel, E.; Katz, H.; Brock, D.M. Nonprofit Financial Vulnerability: Testing Competing Models, Recommended Improvements, and Implications. Volunt. Int. J. Volunt. Nonprofit Organ. 2014, 26, 1–17. [Google Scholar] [CrossRef]

- Searing, E.A.M. Determinants of the Recovery of Distressed Nonprofits. In Proceedings of the ARNOVA Annual Conference, Indianapolis, IN, USA, 12 November 2012. [Google Scholar]

- Ohlson, J.A. Financial Ratios and the Probabilistic Prediction of Bankruptcy. J. Account. Res. 1980, 18, 109–131. [Google Scholar] [CrossRef] [Green Version]

- Beaver, W.H. Financial ratios as predictors of failure. J. Account. Res. 1966, 4, 71–111. [Google Scholar] [CrossRef]

- Searing, E.A.M. Determinants of the recovery of financially distressed nonprofits. Nonprofit Manag. Leadersh. 2018, 28, 313–328. [Google Scholar] [CrossRef]

- Tinkelman, D.; Donabedian, B. Street lamps, alleys, ratio analysis, and nonprofit organizations. Nonprofit Manag. Leadersh. 2007, 18, 5–18. [Google Scholar] [CrossRef]

- Ashley, S.R.; Van Slyke, D.M. The Influence of Administrative Cost Ratios on State Government Grant Allocations to Nonprofits. Public Adm. Rev. 2012, 72, 47–56. [Google Scholar] [CrossRef]

- Frumkin, P.; Kim, M.T. Strategic Positioning and the Financing of Nonprofit Organizations: Is Efficiency Rewarded in the Contributions Marketplace? Public Adm. Rev. 2001, 61, 266–275. [Google Scholar] [CrossRef] [Green Version]

- Lecy, J.D.; Searing, E.A.M. Anatomy of the Nonprofit Starvation Cycle: An Analysis of Falling Overhead Ratios in the Nonprofit Sector. Nonprofit Volunt. Sect. Q. 2014, 44, 539–563. [Google Scholar] [CrossRef]

- Ritchie, W.J.; Kolodinsky, R.W. Nonprofit organization financial performance measurement: An evaluation of new and existing financial performance measures. Nonprofit Manag. Leadersh. 2003, 13, 367–381. [Google Scholar] [CrossRef]

- Tinkelman, D. Unintended consequences of expense ratio guidelines: The Avon breast cancer walks. J. Account. Public Policy 2009, 28, 485–494. [Google Scholar] [CrossRef]

- Abraham, A. Financial management in the nonprofit sector: A mission-based approach to ratio analysis in membership organizations. J. Am. Acad. Bus. 2006, 9, 212–217. [Google Scholar]

- Chabotar, K.J. Financial Ratio Analysis Comes to Nonprofits. J. High. Educ. 1989, 60, 188–208. [Google Scholar] [CrossRef]

- Searing, E.A.; Wiley, K.K.; Young, S.L. Resiliency tactics during financial crisis: The nonprofit resiliency framework. Nonprofit Manag. Leadersh. 2021, 32, 179–196. [Google Scholar] [CrossRef]

- Deakin, E.B. A discriminant analysis of predictors of business failure. J. Account. Res. 1972, 10, 167–179. [Google Scholar] [CrossRef]

- Altman, E.I. Predicting Financial Distress of Companies: Revisiting the Z-Score and Zeta Models; Stern School of Business, New York University: New York, NY, USA, 2000. [Google Scholar]

- Cleverley, W.O.; Nilsen, K. Assessing financial position with 29 key ratios. Hosp. Financ. Manag. 1980, 34, 30. [Google Scholar]

- Kennedy, L.; Dumas, M.B. Hospital closures and survivals: An analysis of operating characteristics and regulatory mechanisms in three states. Health Serv. Res. 1983, 18, 489. [Google Scholar]

- Beck, T.E.; Lengnick-Hall, C.A.; Lengnick-Hall, M.L. Solutions out of context: Examining the transfer of business concepts to nonprofit organizations. Nonprofit Manag. Leadersh. 2008, 19, 153–171. [Google Scholar] [CrossRef]

- Fahad, N.; Scott, T. The Effect of Capitalising Operating Leases On Charities. Aust. Account. Rev. 2021. [Google Scholar] [CrossRef]

- Moody, L.A. Who, What, and How of the Revised Model Nonprofit Corporation Act. N. Ky. L. Rev. 1988, 16, 251. [Google Scholar]

- Norris-Tirrell, D. Organization termination in the nonprofit setting: The dissolution of children’s rehabilitation services. Int. J. Public Adm. 1997, 20, 2177–21794. [Google Scholar] [CrossRef]

- Fernández-Laviada, A.; López-Gutiérrez, C.; Pérez, A. How does the development of the social enterprise sector affect entrepreneurial behavior? An empirical analysis. Sustainability 2020, 12, 826. [Google Scholar] [CrossRef] [Green Version]

- Siegner, M.; Pinkse, J.; Panwar, R. Managing tensions in a social enterprise: The complex balancing act to deliver a multi-faceted but coherent social mission. J. Clean. Prod. 2018, 174, 1314–1324. [Google Scholar] [CrossRef]

- Battilana, J. Cracking the organizational challenge of pursuing joint social and financial goals: Social enterprise as a laboratory to understand hybrid organizing. M@N@Gement 2018, 21, 1278–1305. [Google Scholar] [CrossRef] [Green Version]

- Naseem, M.A.; Lin, J.; Rehman, R.U.; Ahmad, M.I.; Ali, R. Moderating role of financial ratios in corporate social responsibility disclosure and firm value. PLoS ONE 2019, 14, e0215430. [Google Scholar] [CrossRef] [PubMed]

- Powell, M.; Gillett, A.; Doherty, B. Sustainability in social enterprise: Hybrid organizing in public services. Public Manag. Rev. 2019, 21, 159–186. [Google Scholar] [CrossRef]

- Hager, M.A. Expaining Demise among Nonprofit Organizations; University of Minnesota: Minneapolis, MN, USA, 1999. [Google Scholar]

- Calabrese, T.D. The Accumulation of Nonprofit Profits: A Dynamic Analysis. Nonprofit Volunt. Sect. Q. 2012, 41, 300–324. [Google Scholar] [CrossRef]

- de Andrés-Alonso, P.; Garcia-Rodriguez, I.; Romero-Merino, M.E. The Dangers of Assessing the Financial Vulnerability of Nonprofits Using Traditional Measures. Nonprofit Manag. Leadersh. 2015, 25, 371–382. [Google Scholar] [CrossRef]

- Coupet, J.; Berrett, J.L. Toward a valid approach to nonprofit efficiency measurement. Nonprofit Manag. Leadersh. 2019, 29, 299–320. [Google Scholar] [CrossRef] [Green Version]

- Hu, Q.; Kapucu, N. Can management practices make a difference? Nonprofit organization financial performance during times of economic stress. J. Econ. Financ. Anal. 2017, 1, 71–88. [Google Scholar]

- Arceneaux, S.J. The Relationship Between Government Grants and Nonprofit Revenue Diversification; The University of Alabama at Birmingham: Birmingham, AL, USA, 2020. [Google Scholar]

- Wing, K.; Hager, M.A. Getting What We Pay For: Low Overhead Limits Nonprofit Effectiveness. 2004. Available online: http://webarchive.urban.org/UploadedPDF/311044_NOCP_3.pdf (accessed on 6 December 2021).

- Bowman, W. Should donors care about overhead costs? Do they care? Nonprofit Volunt. Sect. Q. 2006, 35, 288–310. [Google Scholar] [CrossRef]

- Qu, H.; Daniel, J.L. Is “Overhead” A Tainted Word? A Survey Experiment Exploring Framing Effects of Nonprofit Overhead on Donor Decision. Nonprofit Volunt. Sect. Q. 2021, 50, 397–419. [Google Scholar] [CrossRef]

- Chikoto, G.L.; Neely, D.G. Building Nonprofit Financial Capacity: The Impact of Revenue Concentration and Overhead Costs. Nonprofit Volunt. Sect. Q. 2013, 43, 570–588. [Google Scholar] [CrossRef]

- Frumkin, P.; Keating, E.K. Diversification Reconsidered: The Risks and Rewards of Revenue Concentration. J. Soc. Entrep. 2011, 2, 151–164. [Google Scholar] [CrossRef]

- Gunnerson, A.L. Strategies to Diversify Funding Sources in Nonprofit Organizations; Walden University: Minneapolis, MN, USA, 2019. [Google Scholar]

- Lu, J.; Lin, W.; Wang, Q. Does a more diversified revenue structure lead to greater financial capacity and less vulnerability in nonprofit organizations? A bibliometric and meta-analysis. Int. J. Volunt. Nonprofit Organ. 2019, 30, 593–609. [Google Scholar] [CrossRef]

- Fernandez, J.J. Causes of Dissolution among Spanish Nonprofit Associations. Nonprofit Volunt. Sect. Q. 2008, 37, 113–137. [Google Scholar] [CrossRef]

- Montrone, A.; Poledrini, S.; Searing, E. La previsione delle crisi aziendali nelle cooperative sociali italiane. Impresa Soc. 2020, 4, 20–36. [Google Scholar]

- Kruse, P. Exploring International and Inter-Sector Differences of Social Enterprises in the UK and India. Sustainability 2021, 13, 5870. [Google Scholar] [CrossRef]

- Bowman, W. Financial capacity and sustainability of ordinary nonprofits. Nonprofit Manag. Leadersh. 2011, 22, 37–51. [Google Scholar] [CrossRef]

- Core, J.E.; Guay, W.R.; Verdi, R.S. Agency problems of excess endowment holdings in not-for-profit firms. J. Account. Econ. 2006, 41, 307–333. [Google Scholar] [CrossRef] [Green Version]

- Stinchcombe, A.L. Social Structure and Organization. In Handbook of Organizations; March, J.G., Ed.; Rand McNally: Chicago, IL, USA, 1965; pp. 142–193. [Google Scholar]

- Froelich, K.A.; Knoepfle, T.W.; Pollak, T.H. Financial measures in nonprofit organization research: Comparing IRS 990 return and audited financial statement data. Nonprofit Volunt. Sect. Q. 2000, 29, 232–254. [Google Scholar] [CrossRef]

- Trussel, J.M.; Greenlee, J.S. A financial rating system for charitable nonprofit organizations. Res. Gov. Nonprofit Account. 2004, 11, 105–127. [Google Scholar]

- Tuckman, H.P.; Chang, C.F. Nonprofit equity: A behavioral model and its policy implications. J. Policy Anal. Manag. 1992, 11, 76–87. [Google Scholar] [CrossRef]

- Chikoto, G.L. Adoption And Use Of The Hirshman-Herfindahl Index in Nonprofit Research: Does Revenue Diversification Measurement Matter? In Proceedings of the 11th International Conference of the International Society for Third-Sector Research, Muenster, Germany, 22–25 July 2014. [Google Scholar]

- Flannery, M.J.; Hankins, K.W. Estimating dynamic panel models in corporate finance. J. Corp. Financ. 2013, 19, 1–19. [Google Scholar] [CrossRef]

- Palepu, K.G. Predicting takeover targets: A methodological and empirical analysis. J. Account. Econ. 1986, 8, 3–35. [Google Scholar] [CrossRef]

- Fichman, M.; Levinthal, D.A. Honeymoons and the liability of adolescence: A new perspective on duration dependence in social and organizational relationships. Acad. Manag. Rev. 1991, 16, 442–468. [Google Scholar] [CrossRef]

- Bruderl, J.; Schussler, R. Organizational mortality: The liabilities of newness and adolescence. Adm. Sci. Q. 1990, 35, 530–547. [Google Scholar] [CrossRef]

- Cameron, A.C.; Trivedi, P.K. Microeconometrics Using Stata; Stata Press: College Station, TX, USA, 2009; Volume 5. [Google Scholar]

- Foster, W.; Fine, G. How nonprofits get really big. Stanf. Soc. Innov. Rev. 2007, 5, 46–55. [Google Scholar]

- Scott, S.; Stuart, T. Organizational endowments and the performance of university start-ups. Manag. Sci. 2002, 48, 154–170. [Google Scholar]

{kind=link}

| Beginning Sample of Nonprofit Observations | 5,500,342 | (% of Original) |

|---|---|---|

| less nonprofit observations with fiscal years prior to 1987 | −5 | ~ |

| less nonprofit observations with missing rule dates | −39,867 | 0.72% |

| less nonprofit observations with incorrect rule dates | −62,333 | 1.13% |

| less nonprofit observations with ages less than −1 1 | −26,575 | 0.48% |

| less nonprofit observations that were exact duplicates | −767,966 | 13.96% |

| on employer identification number (EIN), fiscal | ||

| year, and total revenues | ||

| less nonprofit observations that were exact duplicates | −21,109 | 0.38% |

| on EIN and fiscal year 2 | ||

| less organizations with negative values for | −3170 | 0.06% |

| contributions, program revenues, or dues | ||

| less nonprofits which did not report a sector | −2 | ~ |

| Potential sample size after cleaning | 4,579,315 | 83.26% |

| Nonprofits from final potential sample with two years | 91,226 | 1.66% 3 |

| of insolvency followed by two years of filing a 990 | ||

| Nonprofits from final potential sample with two years | ||

| of 25% decrease in total net assets followed by two | 146,446 | 2.66% |

| years of filing a 990 |

| Nonprofits from final potential sample with two years of insolvency followed by two years of filing a 990 form | 91,226 |

| Less observations from nonprofits older than 10 in their diagnosis year | 59,495 |

| Less observations from nonprofits whose total revenues were consistently >$150,000 during the observation period | 21,519 |

| Final sample for Solvency | |

| Total Observations | 10,212 |

| Number of Unique Nonprofits | 5386 |

| Nonprofits from final potential sample with two years of insolvency followed by two years of filing a 990 form | 146,446 |

| Less observations from nonprofits older than 10 in their diagnosis year | 87,241 |

| Less observations from nonprofits whose total revenues were consistently >$150,000 during the observation period | 30,459 |

| Final sample for Financial Stability | |

| Total Observations | 28,746 |

| Number of Unique Nonprofits | 21,175 |

| Name | Formula | NCCS Core Data Fields |

|---|---|---|

| Equity 1 | ||

| Surplus | ||

| HHI 2 | ||

| Size 3 | Natural log of total revenues | log (TOTREV) |

| Age 4 | Years since receipt of tax-exempt status |

| Year 1 | Year 2 | ||||

|---|---|---|---|---|---|

| Variable | Mean | Std. Dev. | Mean | Std. Dev. | |

| Achieved Solvency 1 (N = 1659) | Equity | −0.326 | (0.946) | −0.247 | (1.129) |

| Surplus | −0.249 | (0.660) | −0.048 | (0.470) | |

| HHI | 0.806 | (0.210) | 0.800 | (0.214) | |

| Size | 11.355 | (1.479) | 11.603 | (1.239) | |

| Age | 2.700 | (2.319) | 3.700 | (2.319) | |

| Did Not Achieve Solvency (N = 8553) | Equity | −0.628 | (0.573) | −0.681 | (0.577) |

| Surplus | −0.317 | (0.794) | −0.210 | (0.671) | |

| HHI | 0.823 | (0.203) | 0.819 | (0.204) | |

| Size | 10.992 | (2.497) | 11.128 | (2.464) | |

| Age | 3.528 | (2.342) | 4.528 | (2.342) | |

| Year 1 | Year 2 | ||||

|---|---|---|---|---|---|

| Variable | Mean | Std. Dev. | Mean | Std. Dev. | |

| Achieved Stability 1 (N = 11,929) | Equity | 0.772 | (3.578) | 0.753 | (4.609) |

| Surplus | −0.020 | (0.606) | −0.301 | (0.652) | |

| HHI | 0.800 | (0.214) | 0.794 | (0.216) | |

| Size | 11.291 | (1.182) | 11.171 | (1.481) | |

| Age | 2.554 | (2.410) | 3.554 | (2.406) | |

| Did Not Achieve Stability (N = 16,817) | Equity | 0.306 | (3.535) | 0.099 | (3.489) |

| Surplus | −0.163 | (0.728) | −0.315 | (0.693) | |

| HHI | 0.823 | (0.205) | 0.819 | (0.205) | |

| Size | 11.192 | (1.982) | 11.172 | (2.055) | |

| Age | 3.006 | (2.422) | 4.006 | (2.422) | |

| Variable | Equity | Surplus | HHI | Size | Age | |

|---|---|---|---|---|---|---|

| Solvency | 0.169 * | 0.033 * | −0.030 * | 0.057 * | −0.130 * | |

| Solvency Year 1 | Equity | 1 | ||||

| Surplus | 0.310 * | 1 | ||||

| HHI | −0.039 * | −0.027 * | 1 | |||

| Size | 0.318 * | 0.066 * | −0.056 * | 1 | ||

| Age | −0.099 * | 0.091 * | −0.028 * | −0.011 | 1 | |

| Solvency Year 2 | Solvency | 0.224 * | 0.093 * | −0.033 * | 0.076 * | −0.130 * |

| Equity | 1 | |||||

| Surplus | 0.262 * | 1 | ||||

| HHI | −0.031 * | -0.013 | 1 | |||

| Size | 0.251 * | 0.017 | −0.037 * | 1 | ||

| Age | −0.140 * | −0.003 | −0.017 | −0.079 * | 1 |

| Variable | Equity | Surplus | HHI | Size | Age | |

|---|---|---|---|---|---|---|

| Stability | 0.064 * | 0.103 * | −0.054 * | 0.029 * | 0.092 * | |

| Stability Year 1 | Equity | 1 | ||||

| Surplus | −0.225 * | 1 | ||||

| HHI | −0.007 | 0.031 * | 1 | |||

| Size | −0.362 * | 0.186 * | −0.002 | 1 | ||

| Age | −0.002 | −0.129 * | −0.047 * | −0.039 * | 1 | |

| Stability Year 2 | Stability | 0.080 * | 0.010 | −0.59 * | −0.001 | −0.092 * |

| Equity | 1 | |||||

| Surplus | −0.395 * | 1 | ||||

| HHI | 0.000 | 0.024 * | 1 | |||

| Size | −0.450 * | 0.247 * | −0.003 | 1 | ||

| Age | −0.024 * | 0.012 | −0.014 * | −0.060 * | 1 |

| Variable | Insolvency Recovery Year 1 | Insolvency Recovery Year 2 | Disruption Recovery Year 1 | Disruption Recovery Year 2 |

|---|---|---|---|---|

| Equity Ratio | 0.138 *** | 0.202 *** | 0.014 *** | 0.014 *** |

| (0.015) | (0.019) | (0.001) | (0.001) | |

| Surplus Ratio | −0.018 ** | 0.004 | 0.087 *** | 0.045 *** |

| (0.007) | (0.013) | (0.006) | (0.006) | |

| Revenue Concentration (HHI) | −0.037 ** | −0.045 ** | −0.136 *** | −0.139 *** |

| (0.018) | (0.018) | (0.015) | (0.015) | |

| Size | −0.003 | −0.005 | 0.012 *** | 0.007 *** |

| (0.002) | (0.003) | (0.002) | (0.002) | |

| Age | −0.015 *** | −0.012 *** | −0.014 *** | −0.016 *** |

| (0.002) | (0.002) | (0.001) | (0.001) | |

| Observations | 10,212 | 10,212 | 28,746 | 28,746 |

| Log Pseudolikelihood | −4195 | −4008 | −18,849 | −18,962 |

| McFadden’s R-squared | 0.074 | 0.115 | 0.034 | 0.028 |

| Adj. Count R-squared | 0.001 | 0.001 | 0.037 | 0.031 |

| Sensitivity | 0.60% | 1.51% | 25.64% | 22.50% |

| Specificity | 99.89% | 99.72% | 84.41% | 86.25% |

| % Correctly Classified | 83.76% | 83.76% | 60.02% | 59.79% |

| VARIABLES | Insolvency Recovery Year 1 | Insolvency Recovery Year 2 | Disruption Recovery Year 1 | Disruption Recovery Year 2 |

|---|---|---|---|---|

| Equity Ratio | 1.084 *** | 1.644 *** | 0.062 *** | 0.059 *** |

| (0.122) | (0.158) | (0.006) | (0.006) | |

| Surplus Ratio | −0.142 ** | 0.029 | 0.374 *** | 0.191 *** |

| (0.056) | (0.106) | (0.027) | (0.026) | |

| Revenue Concentration | −0.293 ** | −0.366 ** | −0.588 *** | −0.595 *** |

| (0.142) | (0.143) | (0.063) | (0.064) | |

| Size | −0.022 | −0.037 | 0.052 *** | 0.029 *** |

| (0.018) | (0.023) | (0.010) | (0.009) | |

| Age | −0.142 *** | −0.116 ** | −0.079 *** | −0.115 *** |

| (0.036) | (0.047) | (0.015) | (0.019) | |

| Age2 | 0.004 | 0.002 | 0.003 | 0.006 ** |

| (0.005) | (0.005) | (0.002) | (0.002) | |

| Constant | 0.057 (1.054) | 0.970 (1.048) | −0.187 (0.410) | 0.398 (0.412) |

| Observations | 10,212 | 10,212 | 28,746 | 28,746 |

| log likelihood | −4194 | −4008 | −18,848 | −18,959 |

| McFadden’s R-squared | 0.0743 | 0.115 | 0.0338 | 0.0281 |

| Adj. Count R-squared | −0.001 | 0.000 | 0.038 | 0.030 |

| Sensitivity | 0.60% | 1.57% | 25.79% | 22.58% |

| Specificity | 99.87% | 99.70% | 84.37% | 86.13% |

| % Correctly Classified | 83.74% | 83.75% | 60.06% | 59.75% |

| Insolvency Recovery Year 1 | Insolvency Recovery Year 2 | Disruption Recovery Year 1 | Disruption Recovery Year 2 | |

|---|---|---|---|---|

| Difference in BIC’ | 8.780 | 9.085 | 8.318 | 4.363 |

| Best Fit Model | Original | Original | Original | Original |

| Variables | Insolvency Recovery Year 1 | Insolvency Recovery Year 2 | Disruption Recovery Year 1 | Disruption Recovery Year 2 |

|---|---|---|---|---|

| Equity Ratio | 0.820 *** | 1.463 *** | 0.067 *** | 0.053 *** |

| (0.115) | (0.158) | (0.007) | (0.005) | |

| Surplus Ratio | −0.166 *** | 0.095 | 0.359 *** | 0.032 |

| (0.060) | (0.122) | (0.029) | (0.025) | |

| Revenue Concentration | −0.332 ** | −0.313 ** | −0.582 *** | −0.621 *** |

| (0.145) | (0.146) | (0.064) | (0.065) | |

| Size | −0.156 *** | −0.073 *** | −0.191 *** | −0.216 *** |

| (0.014) | (0.016) | (0.008) | (0.007) | |

| Age | −0.102 *** | −0.101 *** | −0.043 *** | −0.050 *** |

| (0.013) | (0.013) | (0.006) | (0.006) | |

| Observations | 9847 | 9850 | 28,122 | 27,543 |

| log likelihood | −3937 | −3795 | −18,068 | −17,558 |

| McFadden’s R-squared | 0.092 | 0.123 | 0.054 | 0.061 |

| Adj. Count R-squared | 0.001 | −0.001 | 0.025 | 0.041 |

| Sensitivity | 1.08% | 1.65% | 32.76% | 33.85% |

| Specificity | 99.82% | 99.66% | 78.30% | 78.91% |

| % Correctly Classified | 83.97% | 83.99% | 59.30% | 60.20% |

| Variables | Expected Sign | Insolvency Recovery Year 1 | Insolvency Recovery Year 2 | Disruption Recovery Year 1 | Disruption Recovery Year 2 |

|---|---|---|---|---|---|

| Equity Ratio | + | + | + | + | + |

| Surplus Ratio | + | - | + | + | |

| Revenue Concentration | - | - | - | - | - |

| Size | + | + | + | ||

| Age | + | - | - | - | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Searing, E.A.M. Resilience in Vulnerable Small and New Social Enterprises. Sustainability 2021, 13, 13546. https://doi.org/10.3390/su132413546

Searing EAM. Resilience in Vulnerable Small and New Social Enterprises. Sustainability. 2021; 13(24):13546. https://doi.org/10.3390/su132413546

Chicago/Turabian StyleSearing, Elizabeth A. M. 2021. "Resilience in Vulnerable Small and New Social Enterprises" Sustainability 13, no. 24: 13546. https://doi.org/10.3390/su132413546

APA StyleSearing, E. A. M. (2021). Resilience in Vulnerable Small and New Social Enterprises. Sustainability, 13(24), 13546. https://doi.org/10.3390/su132413546