1. Introduction

The sudden breakthrough of the coronavirus pandemic significantly disrupted the global economy. Companies have suffered a multifaceted shock. On the one hand, a significant number of firms had to lockdown, thus undergoing a supply shock because of their inability to produce and sell their products on the markets. On the other hand, businesses that could continue to operate were facing less demand than usual. Indeed, the cessation of activity in some sectors reduced orders and, therefore, the activity of suppliers [

1].

In addition, workers in the stalled sectors were laid off for economic reasons or simply dismissed, with the main consequence to be the loss of income for both employees and the self-employed, exacerbating the weakness of demand [

2,

3].

To mitigate liquidity shortages and avoid bankruptcies that might follow from the COVID-19 pandemic, it was necessary to support the afflicted companies. Closed businesses no longer received payments and those operating did so in slow motion. Cash flow problems arose acutely and the risk that they would turn into solvency problems increased as time passed. Indeed, many of the fixed costs, such as rents and interest payments, remain due, while the cash flow destined to meet these obligations vanished [

4]. The objective was then to design measures with a basic principle that could be stated as “No cash in, no cash out” for self-employed workers and companies.

The effect of the crisis had been particularly considered by academics via the number of companies and self-employed workers who had to stop their activities. The demographic characteristics of halting companies and those resisting were the first elements highlighted in studies. As an example, Fairlie [

5] observes a significant decline in the number of businesses operating in the USA between February and May 2020. Looking at the demographics of owners, he notes that women and immigrants were the most affected populations.

Particular attention was also devoted to the dynamics of the main indicators of business activity. Thus, turnover, employment, cash flow, and the length of time a firm was able to continue paying its bills was examined by industry, by gender of the owner, and by other business characteristics [

6]. Much research still remains in terms of understanding the internal and external determinants of companies’ resistance and resilience to negative shocks, and allowing resources to recover, more or less quickly, after large-scale adverse events is critical [

7,

8]. Researchers may also question of which policies are best, from an economic viewpoint, to curb the crisis. In this regard, the tools of monetary and fiscal policy and their relative adequacy fueled debates among academic economists [

9,

10,

11].

The originality of the present contribution comes from the fact that, despite the huge interest of economists in the economic impact of the COVID-19 pandemic, very little attention has been given to the perception and rating of the supportive measures by SME owners and the self-employed. Our approach puts SMEs, more specifically their owners and self-employed people, at the center of the discussion.

The opinion of the self-employed and heads of SMEs can be seen as an assessment of economic policy measures from the point of view of the “stakeholders”. In May 2020, the date to which our data correspond, the rapid initial response policies in question were already in effect. Thus, contextually, we are neither in an ex ante evaluation, nor in an ex post evaluation. We consider our study as a rating evaluation, by the targeted recipients, of an ongoing economic policy in its early phase [

12]. To serve this purpose, we use their rating of the various policy measures designed and implemented to support them in limiting the damage of the crisis to their businesses.

Although we were in a difficult period, we can see that some business leaders remained optimistic and/or ambitious about the possibilities of growing their business in the short term. Their rating of the various policy measures is analyzed jointly with their business expectations, i.e., how they foresee the short-term development of their activities. We were in a context of an early-stage crisis, when everything stopped abruptly. No one knew when activity would return to its early 2020 level and the short-term expectations of the majority of firm owners were pessimistic.

Thus, our questions of interest are formulated as follows. How do SME owners and self-employed people rate policy measures taken to respond to the COVID-19 crisis? Are their business expectations associated with their rating of policy measures? Which policy measures to support companies have the most positive prospects?

To answer our research questions and substantiate the above arguments, we exploit an original and rich dataset derived from a survey conducted in May 2020 among a representative sample of more than 2100 Belgian (Walloon) SMEs. The time at which the information was collected is an asset of the survey. Indeed, in May 2020, the effects of the shock were already tangible in Belgium [

13]; from a medical viewpoint, COVID-19 itself was a little better known; macroeconomic forecasts, integrating the shock, were made available, and agents were able to project themselves a bit more on what the image of the future [

14]. The dependent variable in our econometric regressions corresponds to the measurement, through a Likert scale, of small firm owner opinions about the various implemented policy measures. The Belgian experience is interesting because the wide variety of undertaken measures echo many of the measures taken within the OECD countries.

Our results suggest that the respondents have an overall positive evaluation of the various economic and social policy measures implemented by the Belgian authorities. More importantly, the assessment of SME owners with the most favorable short-term expectations is significantly different (higher or lower). Measures helping the firm to maintain the workforce under contract were particularly highly rated by firms with the highest prospects. It also appears that those firms did not want some measures to be maintained for too long. Additionally, policy measures to provide more loans and higher guarantees from public financial institutions were appreciated, although less clearly. Ultimately, we believe that our article contributes to informing policymakers about the type of entrepreneurial policies likely to help more resilient and ambitious firms, which are likely to contribute the most to economic recovery, in comparison with laggard and zombie firms [

15,

16].

In the next section, we present the policy measures active at the time of the survey to support business activities during the COVID-19 crisis. Although this study can be regarded as largely exploratory,

Section 3 highlights some arguments for an a priori, or theoretical, treatment of the question raised. In

Section 4, we introduce how we conducted our empirical analysis and report the obtained results.

Section 5 is devoted to the conclusion, where we draw some lessons from the results of our study.

2. Policy Measures Taken to Support Business Activities during the COVID-19 Crisis

All countries, including Belgium, designed and implemented packages of economic and social policy measures to meet the huge challenge of the COVID-19 crisis. In an environment where everything stopped abruptly, Belgian authorities reacted quickly and vigorously to support both households and businesses, with a view to softening the harmful effects of the COVID-19 pandemic on the country’s economy.

2.1. Employment and Social Policy Measures

One of the main expenditures for businesses, especially SMEs, which represent the bulk of the Belgian economic landscape, is the overall cost associated with labor. Therefore, special attention is devoted to the contributions of businesses to social security, and relief from the amounts payable to workers. In Belgium, some companies were obliged to lockdown, thus facing an abrupt stop to their sales. They were allowed to grant temporary unemployment to their employees for economic reasons, also called

force majeure. The usual benefits were raised from 65% to 70% of gross wages, supplemented by a lump-sum benefit of EUR 5.63 per day [

17].

The social measures taken in Belgium and in the majority of OECD countries in response to the COVID-19 crisis are inspired by the

job retention schemes previously used during the financial crisis of 2008 [

18,

19]. Depending on its environment, each country adapted these mechanisms to help employees keep their contracts with their employers, even if their work was suspended. Named

Kurzarbeit in Germany and

partial activity in France, these can take the form of short-time work (STW) schemes that directly subsidize hours not worked. Another variant of this scheme was used in the Netherlands, under the name

Emergency Bridging Measure, with the payment of a wage subsidy, making it possible to maintain the workers’ income even during periods when they are not working (see also [

20]).

Unlike employees, the self-employed are generally not insured against the loss of their job. Whether they work alone or have salaried workers, SME owners in Belgium are considered self-employed with respect to social security matters. Starting in March 2020, self-employed workers forced to interrupt their activity because of the COVID-19 crisis were allowed to defer the payment of their social security contributions. They could also benefit from a monthly replacement income of 1291.69 euros or, if a family depended on them, of 1614.10 euros. This measure known as

bridging right was first implemented in March 2020 for three months. It was subsequently prolonged until 31 August 2020; for individuals working in industries in difficulty or remaining closed, it was prolonged through 31 December 2020 [

16]. In other OECD countries, support measures for self-employed workers range “from providing sick leave payments and unemployment benefits, to lump sum subsidies. (…) France set up a solidarity fund for the self-employed of EUR 2 billion, and provides EUR 1500 monthly compensation for self-employed (and small companies), when their turnover is less than EUR 1 million and they experience a drop in their turnover of 70% or more. (…) In the United Kingdom, self-employed and gig economy workers, who are not entitled to sick pay, receive assistance worth GBP 500 million as part of the 2020 Budget” (pp. 28–29, [

21]).

2.2. Financial Policy Measures

The emergency measures implemented to tackle the COVID-19 health crisis led to severe difficulties for companies trying to meet their financial obligations [

22]. With the drying up of their treasury owing to the cessation of their activities, they needed financial support to stay afloat. There is evidence that, even in normal conditions, SMEs generally have fewer of their own resources and confront difficulties in accessing external finance, except through their banks [

23,

24]. Here, we present financial support to SMEs in Belgium and similar measures in some OECD countries. These include regional allowances, credit repayment facilities, and guarantees provided by public financial institutions to commercial banks in order to keep lending money to entrepreneurs and SMEs.

On 18 March 2020, the National Security Council of Belgium strengthened its measures to fight the coronavirus. In order to support businesses and self-employed people directly impacted by these measures, the Walloon Government (Wallonia is one of the three regions of Federal Belgium; the other two regions are Brussels and Flanders) set up an extraordinary fund of EUR 573.8 million. Under defined conditions, Walloon businesses and self-employed persons could benefit from an indemnity of 5000 EUR or assistance of 2500 EUR subject to acceptance after verification of the application file by officials of the Public Service of Wallonia. The single lump-sum amount of 5000 EUR was given to each company and self-employed person strongly affected by the measures of the National Security Council in the fight against the coronavirus.

The Walloon Government also granted a one-off flat-rate aid of EUR 2500 to each self-employed worker and small business owner who operates in Wallonia and who has benefited from full temporary replacement revenue in March and April 2020. The grant was also awarded if the manager of the business was not a self-employed worker and/or if most workers were placed on temporary economic unemployment for force majeure in March and April 2020. An additional compensation of EUR 3500 was announced on 10 July 2020. This additional compensation was granted to companies that are still fully affected by the impact of the COVID-19 crisis and/or are obliged to remain closed.

The general schemes for direct lump sum subsidies are mainly targeted at SMEs and/or the self-employed. The amount granted and the required conditions vary significantly across countries [

21]. “In France, small companies and self-employed can be granted a EUR 1500 monthly compensation, when their turnover is less than EUR 1 million and they experience a drop in their turnover of 70% or more. Germany has made EUR 10 billion available in direct subsidies to one-person businesses and micro-enterprises. Bavaria offers a scheme of immediate and easily accessible aid from EUR 5000 to 30,000 for affected companies. (…) The United Kingdom is increasing grants to small businesses eligible for Small Business Rate Relief from GBP 3000 to 10,000. Furthermore, GBP 25,000 in grants is provided to retail, hospitality and leisure businesses operating from smaller premises, with a ratable value over GBP 15,000 and below GBP 51,000. Small businesses in England that already pay little or no business rates will be eligible for a one-off coronavirus grant of up to GBP 3000. Scotland is to provide grants of at least GBP 3000 to small businesses in sectors facing the worst economic impact of COVID-19” (p. 38, [

21]).

The payment of mortgages/credits and premiums for fire insurance and outstanding balance for families, viable firms, and the self-employed could be deferred until the end of September 2020 without being charged a fee. In May 2020, the payment of consumer credit was also allowed to be deferred for three months, which could be renewed for another three months.

A moratorium on the repayment of debt was also introduced, whereby SMEs could defer the repayment of debt [

21]. In Belgium, the federal government and the financial sector issued a message to the self-employed, the heads of SMEs, and the market, guaranteeing EUR 50 billion in new credits and credit lines with a maximum term of 12 months (excluding refinancing credits) provided until 30 September 2020.

Action in Wallonia/Belgium mirrors action in other OECD countries. “Australian banks announced support for SMEs through a six-month break in loan repayments” (p. 59, [

21]). “Backed by the Government, the Italian Banking Association announced an agreement with various business associations to set in place a large-scale moratorium on debt repayments, including mortgages and repayments of small loans and revolving credit lines. It would concern loans subscribed by companies until 31 January 2020” (p. 107, [

21]).

To encourage commercial banks to continue to provide loans to SMEs, many countries designed and implemented public guarantee schemes. The Walloon region, through its financial organization called Sowalfin, also set up financial products on advantageous terms for companies needing liquidity. The so-called ricochet loan should allow entrepreneurs to obtain a mixed credit composed of a guarantee of 75% on the desired bank credit and a subordinated loan of maximum 50% of the bank loan. However, the combined value must not exceed EUR 45,000.

In the United Kingdom, following a similar scheme, the government created emergency loans to SMEs known as ‘Bounce back Loans’ (BBLs), which were 100% guaranteed by the government, and thus were not considered as possible non-performing loans, even if the lenders could not repay them [

9]. Similar guarantees schemes were also implemented in many other European and Asian countries.

2.3. Tax and Fiscal Policy Measures

Additional difficulties that companies often face are related to fiscal and administrative burdens. These are among the most important obstacles to business development mentioned by the heads of SMEs. The easing and delaying of not just formalities and documents to be filed, but also payments, were implemented to support companies and the self-employed during this harsh period. Most OECD countries introduced such deferrals and relief with respect to corporate and income tax payments, albeit with varying scope, duration, and intensity [

22].

In Belgium, three main fiscal measures were taken in response to the Coronavirus crisis. Additional flexibility in the payment of tax arrears was granted to businesses in distress, including new postponement and repayment plans. The deadlines of fiscal declarations were postponed for at least two months in March 2020. This measure was prolonged for sectors remaining distressed after the first lockdown. Social security contributions were also postponed for incorporated firms regarding their employees. The self-employed also obtained a reduction in their social security contributions. The emergency measures implemented by the Federal Government, Regions, and Communities, to protect Belgian businesses and households from the crisis caused by the Coronavirus pandemic, were expected to cost 14.3 billion euros in 2020, based on figures from the National Bank of Belgium [

25].

The U.S. Treasury Department deferred tax payments without interest or penalties with the aim of shoring up liquidity. Canada introduced deferral of income tax until 31 August 2020. Many countries are not charging interest on delayed payments, while also offering payment in instalments after the deferral period; these countries include Canada, Ireland, Lithuania, and the United Kingdom [

22].

3. Theoretical Insights and Perspectives

As a reminder, in this study, we are interested in the rating by SMEs owners of various economic policy measures in response to the COVID-19 crisis, their rating being connected to their business prospects. Linking the business prospects of the firm with the policy measures implemented can be done with the help of some theoretical insights and, furthermore, opens up some theoretical perspectives.

The resource-based view suggests [

26,

27,

28] that a company anticipating its forthcoming activity will also consider its capabilities, the resources it currently has, and those it is likely to need. Moreover, it will identify whether these capabilities and resources are internal or external. The temporality of these anticipations, whether short-, medium-, or long-term, would also play a role [

29]. An additional issue for the firm will be to be able to recombine its capabilities and resources, in particular to face uncertainty, as suggested by the dynamic capabilities theory [

30,

31].

In a fast-growing body of literature in entrepreneurship, the concept of the ambitious entrepreneur is gaining weight as an important predictor of firms’ performance outcome. Entrepreneurs qualified as ambitious want, intend, or expect to extensively grow their firms. Growth expectations are considered to be a tool to operationalize the concept of the ambitious entrepreneur. It combines what the entrepreneur wants to achieve with the opportunities and constraints s/he perceives [

15,

32].

In a period of great uncertainty, like that of the COVID-19 crisis, having growth expectations for the company is a signal of resilience. Indeed, in their expectations, entrepreneurs integrate the adverse environment, evaluating their resources and capabilities to find entrepreneurial ways to create as much value as possible despite surrounding constraints [

12,

33,

34].

A priori, or from a theoretical viewpoint, we expect self-employed people and business-owners with employees with the most promising prospects/expectations to have a different opinion about policy measures than the others. Those measures transforming, or helping them to transform, these promising prospects into concrete activity and business results might be the most appreciated. (Growing) economic activity, measured by (increasing) turnover, entails (increasing) cash flow requirements. Any measure making it possible to alleviate cash flow requirements will be, a fortiori, welcome because, by freeing up financial resources, it makes it easier to be able to seize business opportunities that arise, even during this cloudy and uncertain period. In contrast, business owners with little or no favorable prospects would be inclined to consider policy measures allowing them to survive to be positive, waiting for better days.

In addition, a company that sees forthcoming business opportunities anticipates that it will need all possible resources, including its employees, to turn these opportunities into actual activities and profit. If the downturn in activity is perceived to be temporary, the company will tend to want to retain its staff. Thus, those policy measures that allow temporary unemployment while maintaining the contractual relationship between the employee and the company will be positively considered. Contrastingly, those policy measures are such that companies with little or no favorable prospects are less likely to appreciate them.

5. Conclusions

Several policy measures, of different types, were designed and rapidly implemented to limit the damages caused by the adverse sanitary and economic shocks provoked by the COVID-19 pandemic. Among these, a set of measures were defined and implemented to support the self-employed and firms along with their business activity. In this article, we examine these measures through the eyes of business owners, both self-employed and SME owners/employers. We try to do this by crossing their opinion with their short-term development prospects. In so doing, we obtain information about the policy measures, allowing us to distinguish which are aligned with self-declared organizational positive orientation. In a complementary way, we also obtain information about the policy measures that were most appreciated by small firms with less favorable prospects.

The study was made possible by the provision of an original and rich dataset derived from a survey conducted in May 2020 of a representative sample of more than 2100 Belgian (Walloon) SMEs. The Belgian situation is interesting because of the wide variety of measures taken by Belgian public authorities that were analogous to several measures taken by other OECD countries. This is likely to increase the relevance of the results.

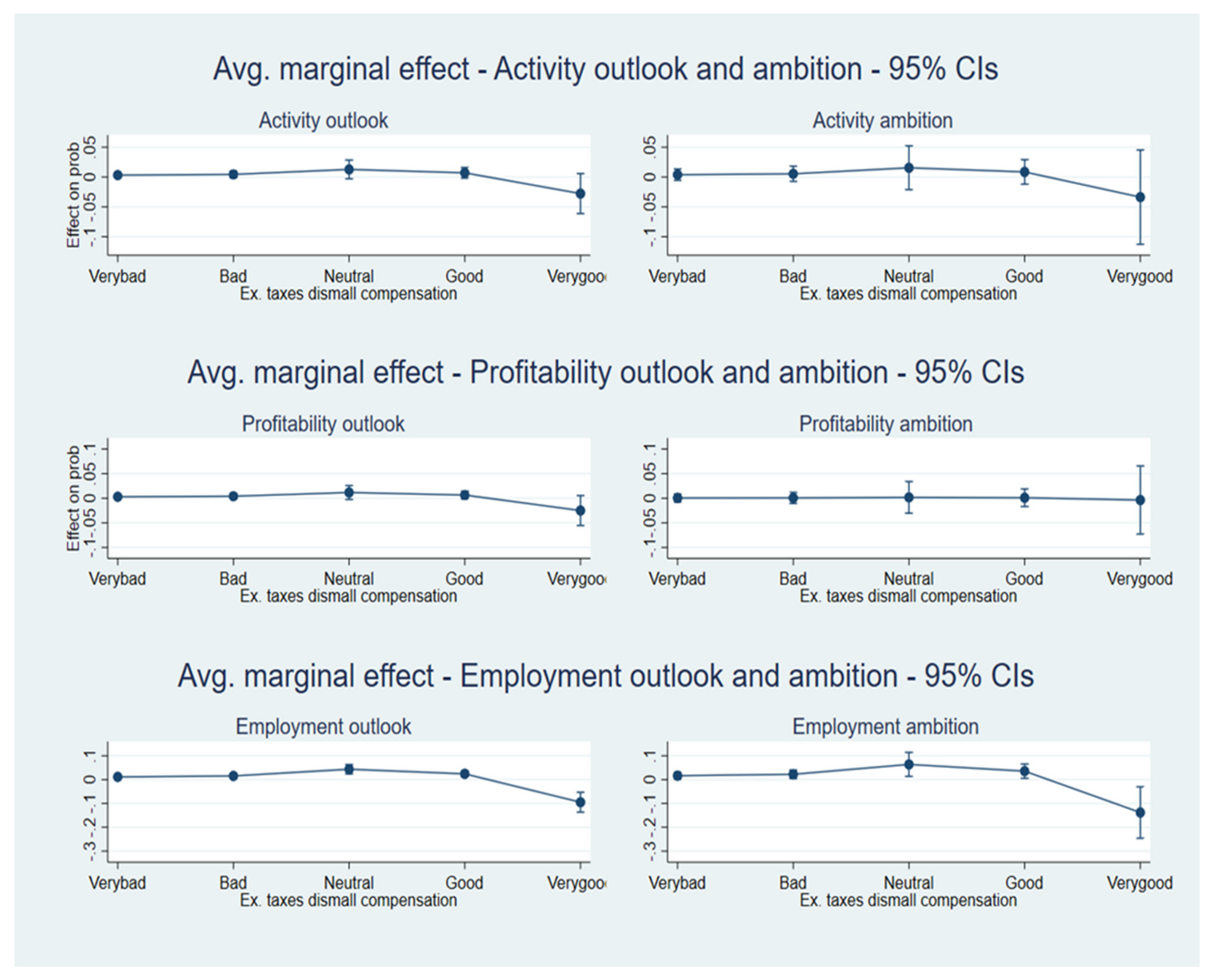

The main independent variables are the expected short-run evolution of business activity, profits, and employment, each included separately. The business owners with the most favorable expectations, at that time, are also subject to specific analysis. Control variables include size, age, and legal form of the firm; level of education of the business owner; industry; as well as whether the firm was active, partially shut down, or totally locked down.

Our results suggest that the respondents had an overall positive evaluation of the various economic and social policy measures implemented by the Belgian authorities. Additionally, the assessment of SME owners with the most favorable short-term expectations were significantly different (higher or lower). In particular, respondents with the most positive prospects in terms of activity/turnover and profit were also those who most appreciated the financial and fiscal support measures. Measures helping the firm to maintain its workforce under contract were particularly highly rated. It also appears that the firms with the best prospects did not want some measures to be maintained for too long. To transform quickly favorable expectations into results, the firm must be able to quickly rely on its workforce. Additionally, policy measures to provide more loans and higher guarantees from public financial institutions were also appreciated, although less clearly.

Our contribution modestly sheds some light on those political measures, appearing best able to safeguard entrepreneurial activities during the early stage of a sudden economic and financial collapse. Moreover, the support of entrepreneurs who expect their activities to be resilient may have a higher collective return. However, the question is far from being fully answered, with further research needed to assess the quality of self-declared expectations in highly uncertain time and to identify the set of elements inside the firm and those related to entrepreneurial ecosystems [

51], promoting resilience and ambition.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}