Integrated Management Solution for a Sustainable SME—Selection Proposal Using AHP

Abstract

1. Introduction

2. Literature Review

2.1. SME’s Sustainable Development

- The optimal allocation of resources, which should consider not just economic efficiency but ecological and social efficiency at the same time. Economic efficiency has its important role for the well–being of each person, determining a social efficiency, while ecological efficiency has the role of preserving present resources for future generations.

- The optimal distribution of resources, which brings into question the need to address intra–generational inequity caused by the global situation, with billions of dollars spent on armaments and over billions of people living in developing countries.

- The optimal ratio between the place occupied by humans and the place of other life forms on the planet.

- Sustainability, sufficiency, equity, and efficiency should be the basis of sustainable development strategies, in this order of priority and importance.

2.2. The Relationship between ERP and Sustainability

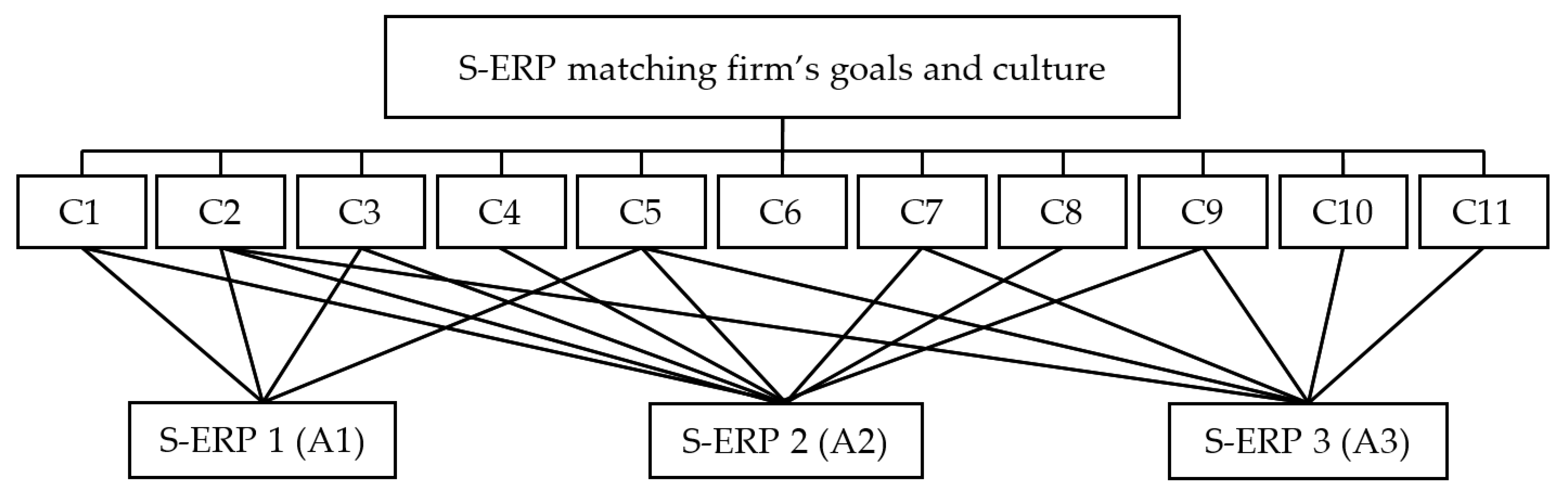

2.3. Criteria for S–ERP Selection

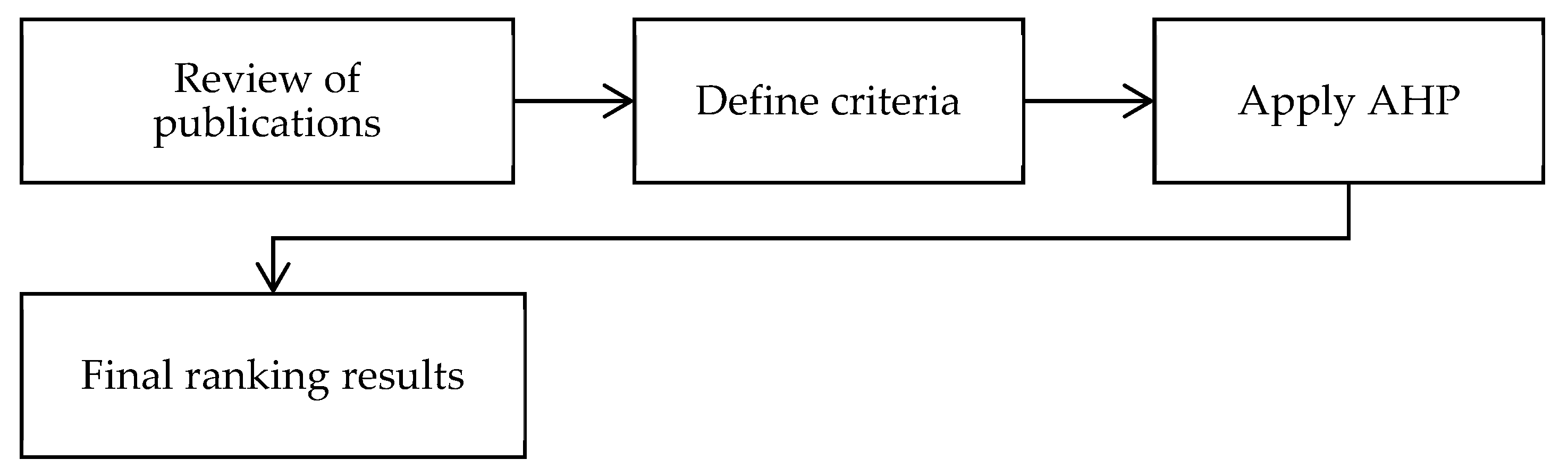

3. Research Methodology

3.1. Collecting Data

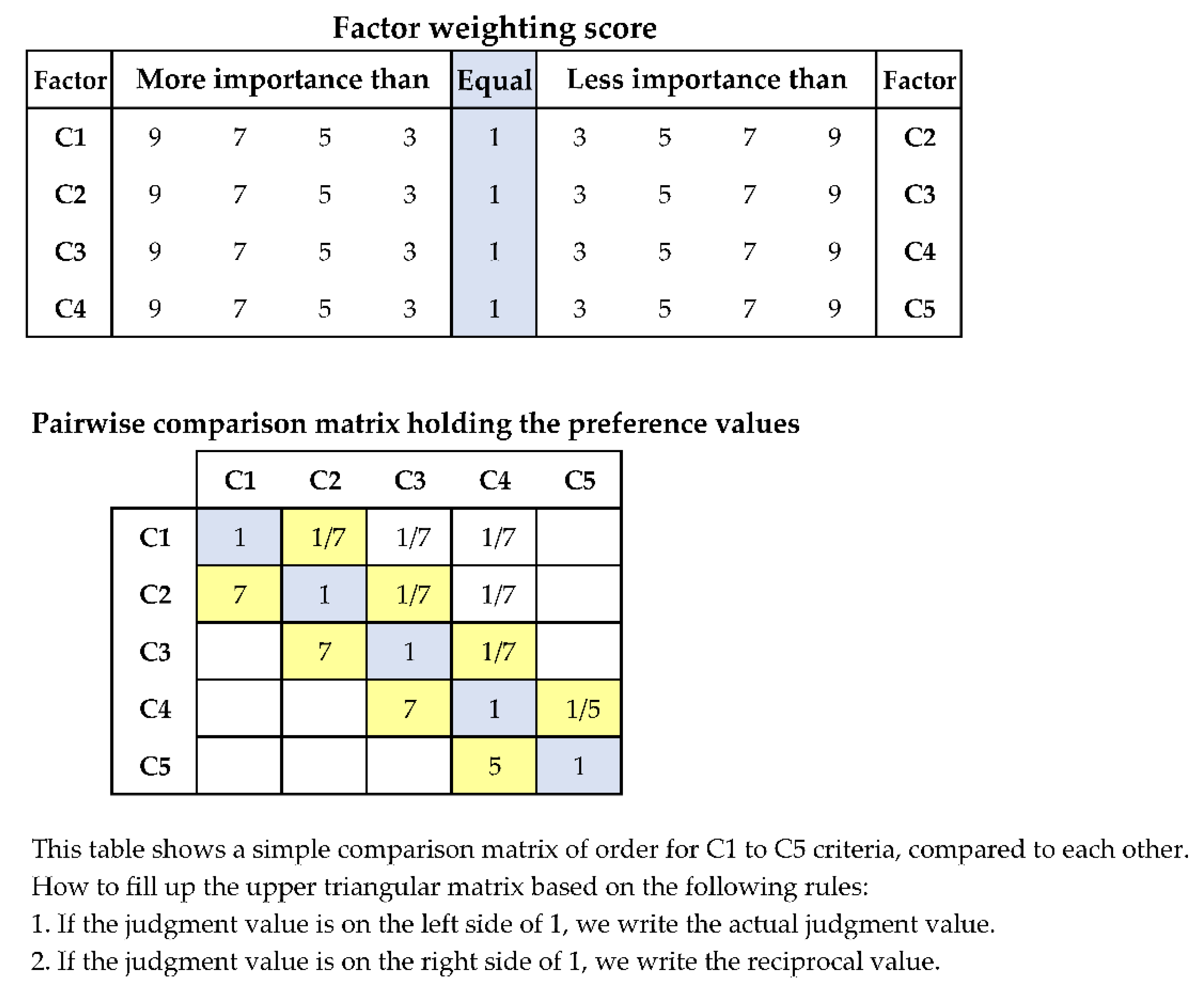

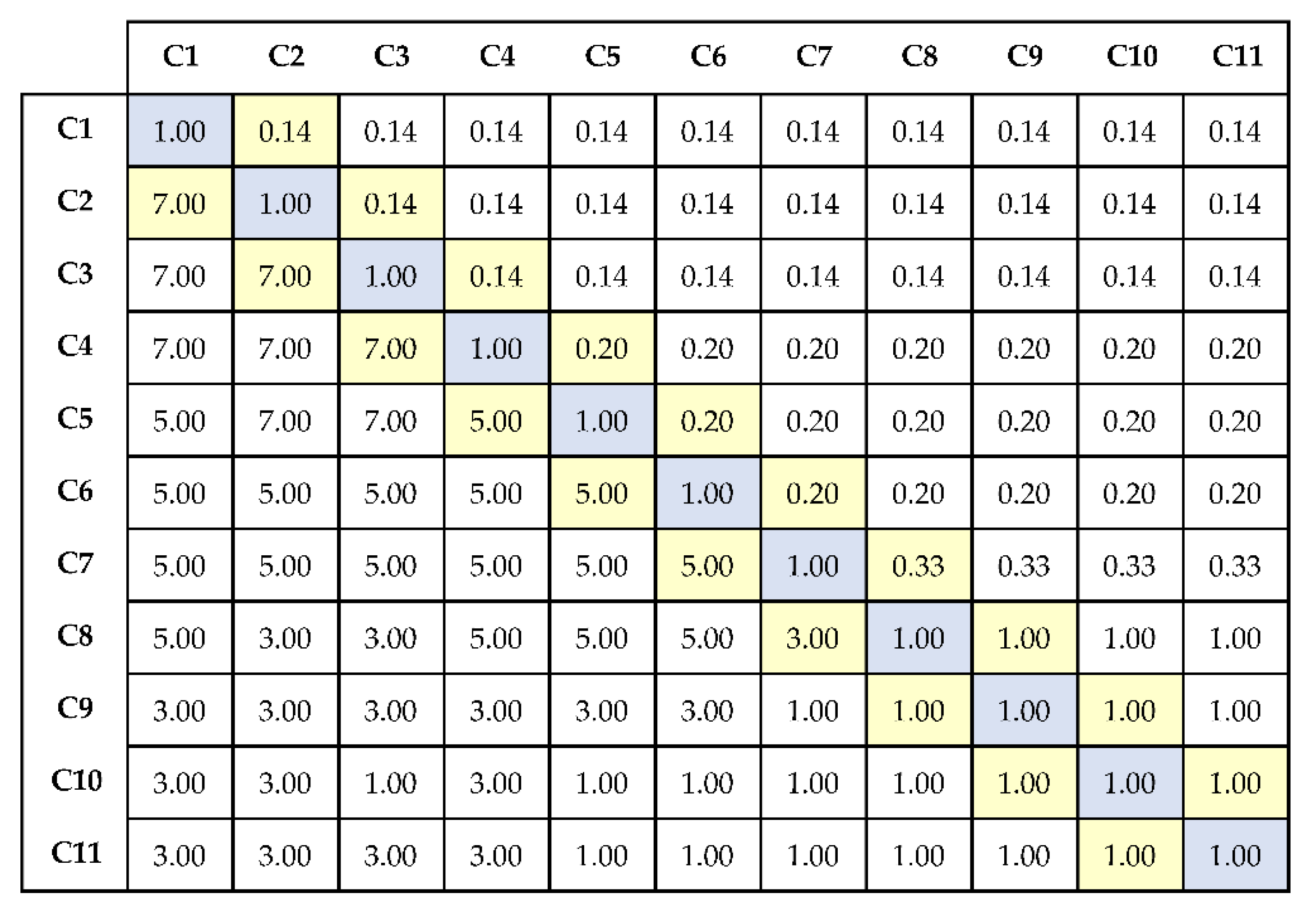

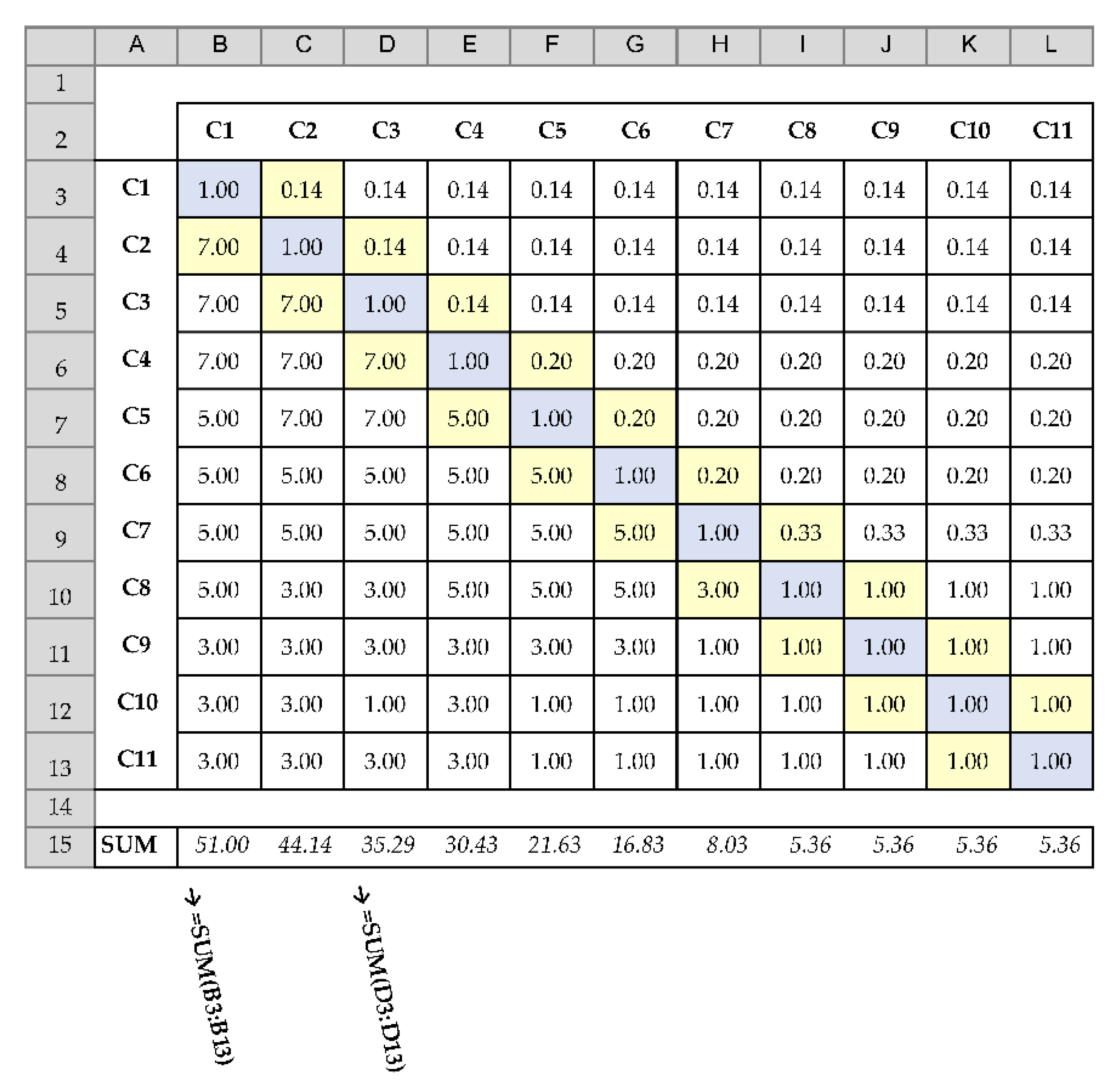

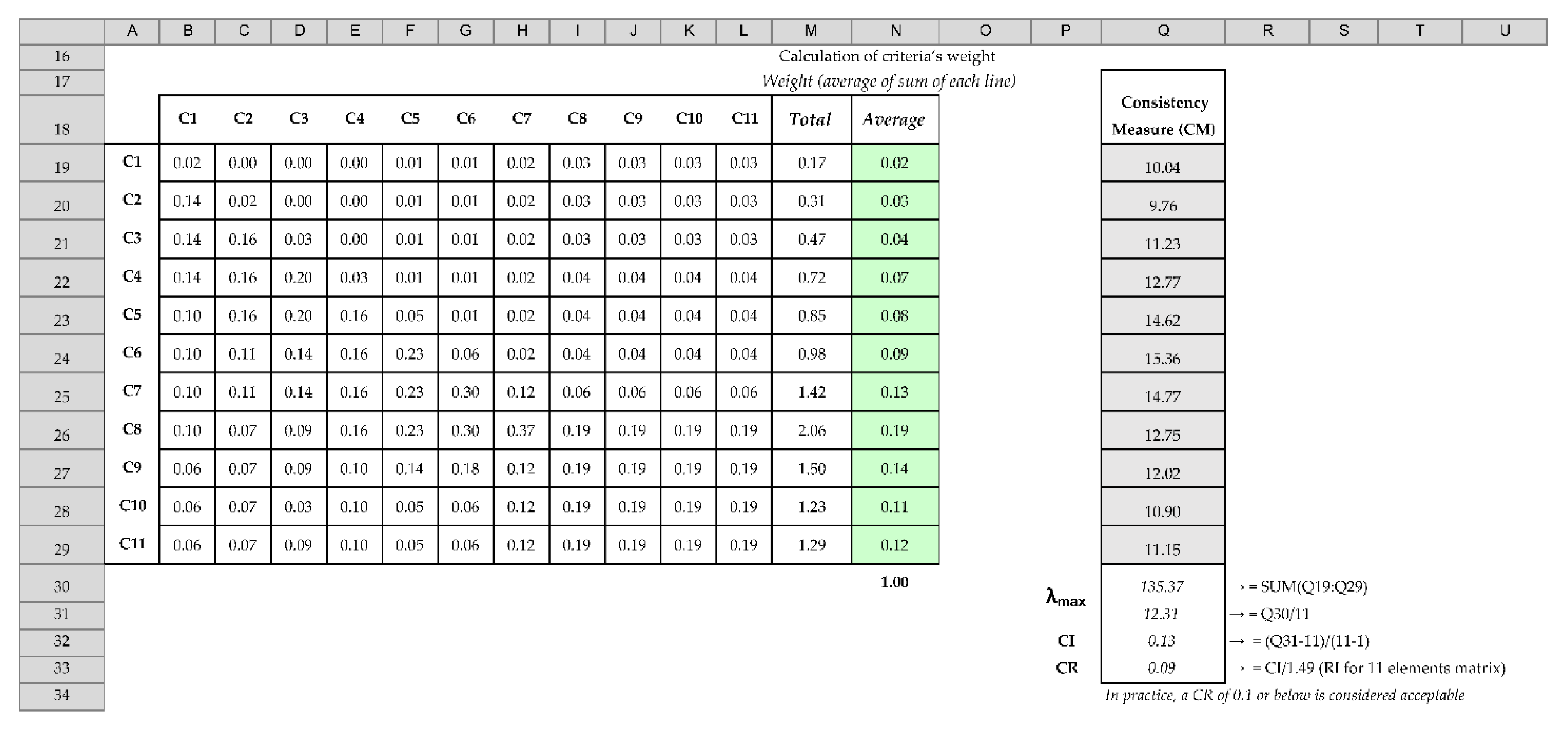

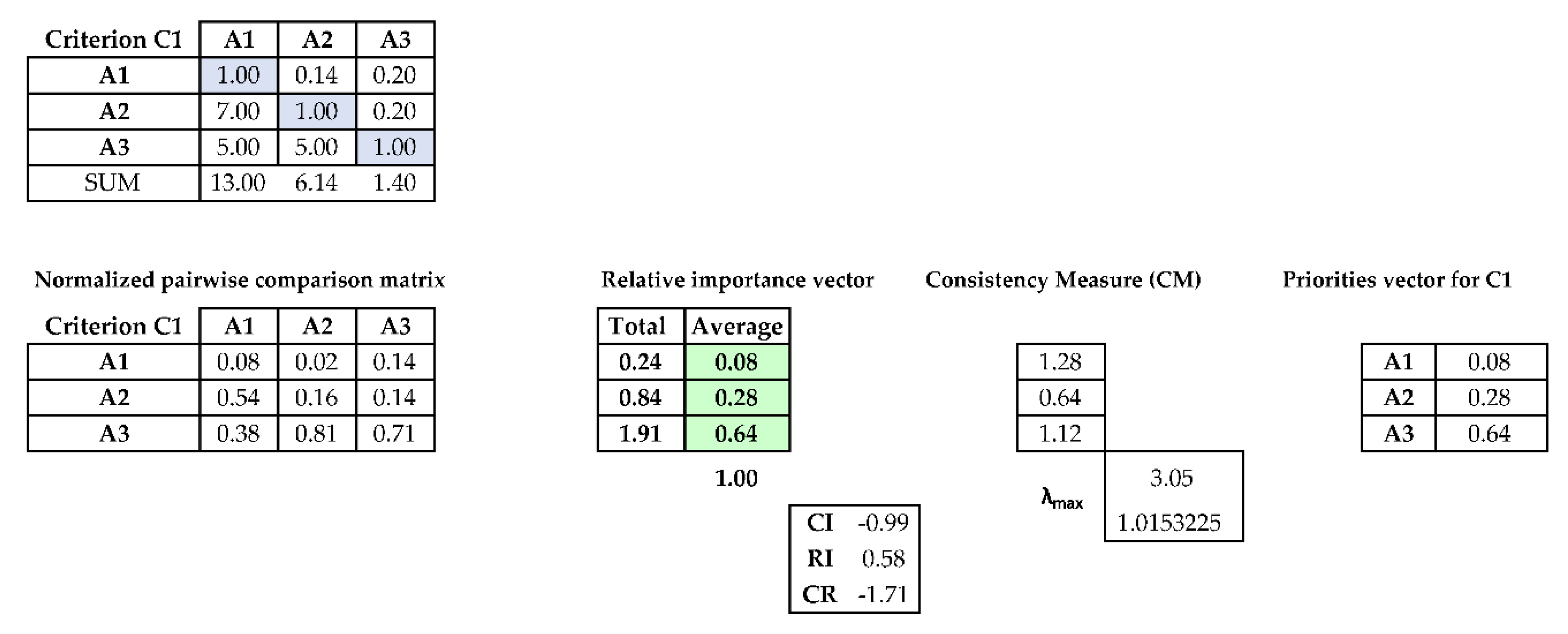

3.2. Analytic Hierarchy Process

4. Results and Discussion of the Applied AHP Model

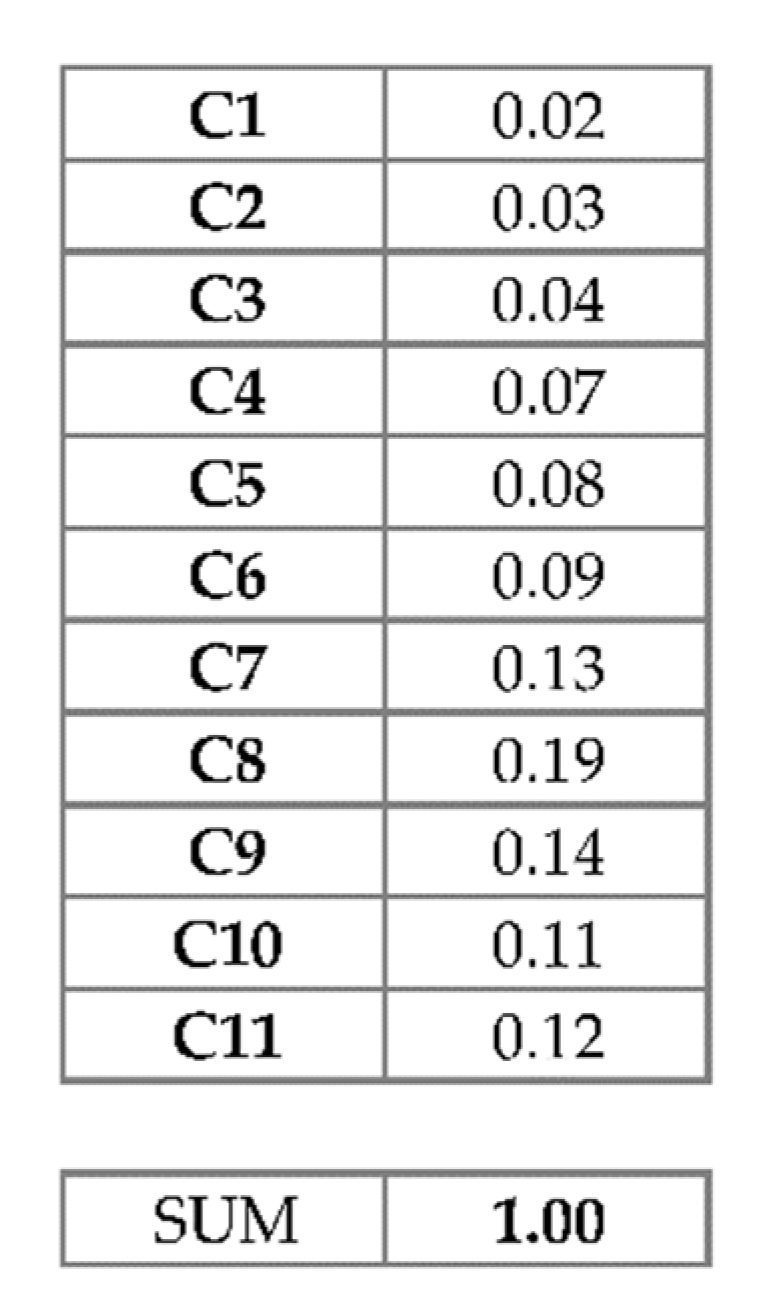

4.1. Results

4.2. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ursacescu, M.; Popescu, D.; State, C.; Smeureanu, I. Assessing the greenness of enterprise resource planning systems through green IT solutions: A Romanian perspective. Sustainability 2019, 11, 4472. [Google Scholar] [CrossRef]

- Ranjan, S.; Vijay, K.J.; Pralay, P. A strategic and sustainable multi–criteria decision making framework for ERP selection in OEM. Int. J. Appl. Eng. 2016, 11, 1916–1926. [Google Scholar]

- Hockerts, K.; Wüstenhagen, R. Greening Goliaths versus emerging Davids—Theorizing about the role of incumbents and new entrants in sustainable entrepreneurship. J. Bus. Ventur. 2010, 25, 481–492. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Muscatello, J.R.; Small, M.H.; Chen, I.J. Implementing enterprise resource planning (ERP) systems in small and midsize manufacturing firms. Int. J. Op. Prod. Manag. 2003, 23, 850–871. [Google Scholar] [CrossRef]

- Carnerud, D.; Mårtensson, A.; Karin Ahlin, K.; Persson, T.S. On the inclusion of sustainability and digitalisation in quality management—An overview from past to present. Total Qual. Manag. Bus. Excell. 2020. [Google Scholar] [CrossRef]

- ERP Software Consulting Services—Business Management Consulting. Available online: https://www.panorama–consulting.com/erp–software–selection–guide/ (accessed on 27 January 2021).

- Chang, Y.W.; Hsu, P.Y. An empirical Investigation of Organizations’ Switching Intention to Cloud enterprise resource planning: A Cost–Benefit Perspective. 2021. Available online: https://searcherp.techtarget.com/feature/ERP (accessed on 17 February 2021).

- Bharathi, S.V.; Mandal, T. Prioritising and ranking critical factors for sustainable cloud ERP adoption in SMEs. Int. J. Autom. Logist. 2015, 1, 294–316. [Google Scholar] [CrossRef]

- Bos-Brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strategy Environ. 2009, 19, 417–435. [Google Scholar] [CrossRef]

- Graafland, J.; Smid, H. Environmental impacts of SMEs and the effects of formal management tools: Evidence from EU′s largest survey. Corp. Soc. Responsib. Environ. Manag. 2015, 23, 297–307. [Google Scholar] [CrossRef]

- Eikelenboom, M.; de Jong, G. The impact of dynamic capabilities on the sustainability performance of SMEs. J. Clean. Prod. 2019, 235, 1360–1370. [Google Scholar] [CrossRef]

- Venkatraman, S.; Fahd, K. Challenges and success factors of ERP systems in Australian SMEs. Systems 2016, 4, 20. [Google Scholar] [CrossRef]

- Alansari, S.T.; Ziadat, A.H. Modelling a sustainable approach toward logistical functions at PAL aerospace services aircraft maintenance in the UAE. In Proceedings of the 2020 Advances in Science and Engineering Technology International Conferences (ASET), Dubai, United Arab Emirats, 4–6 February 2020; IEEE: Piscataway, NJ, USA, 2020. Available online: https://www.gradientconsulting.co.uk/erp–systems–and–sustainability (accessed on 20 February 2021).

- Rowland, M. Decarbonization: Don’t forget the customer. Climate Energy 2021, 37, 9–13. Available online: https://www.westmonroe.com/perspectives/in-brief/how-sustainable-is-your-enterprise-resource-planning-erp-system (accessed on 15 May 2021). [CrossRef]

- Haddara, M.; Elragal, A. ERP lifecycle: A retirement case study. Inf. Res. Manag. J. IRMJ 2021, 26, 1–11. [Google Scholar] [CrossRef]

- Haddara, M. ERP selection: The smart way. Procedia Technol. J. 2014, 16, 394–403. [Google Scholar] [CrossRef]

- Vargas, R.V. Using the analytic hierarchy process (ahp) to select and prioritize projects in a portfolio. In Proceedings of the PMI® Global Congress 2010, Washington, DC, USA, 9–12 October 2010; Project Management Institute: Newtown Square, PA, USA, 2010. [Google Scholar]

- Saaty, T.L.; Vargas, L.G. Model, methods, concepts and application of the analytical hierarchy process. Int. Ser. Oper. Res. Manag. Sci. 2012, 28, 175. [Google Scholar]

- Gupta, S.; Meissonier, R.; Drave, V.A.; Roubaud, D. Examining the impact of Cloud ERP on sustainable performance: A dynamic capability view. Int. J. Inf. Manag. 2020, 51, 102028. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Klemeš, J.J. Sustainable enterprise resource planning systems implementation: A framework development. J. Clean. Prod. 2018, 198, 1345–1354. [Google Scholar] [CrossRef]

- Tsai, W.H.; Lan, S.H.; Lee, H.L. Applying ERP and MES to implement the IFRS 8 operating segments: A steel group’s activity—Based standard costing production decision model. Sustainability 2020, 12, 4303. [Google Scholar] [CrossRef]

- Tasnawijitwong, S.; Samanchuen, T. Open source ERP selection for small and medium enterprises by using analytic hierarchy process. In Proceedings of the 2018 5th International Conference on Business and Industrial Research: Smart Technology for Next Generation of Information, Engineering, Business and Social Science, ICBIR, Bangkok, Thailand, 17–18 May 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 382–386. [Google Scholar] [CrossRef]

- Wei, C.C.; Chien, C.F.; Wang, M.J.J. An AHP–based approach to ERP system selection. Int. J. Prod. Econ. 2005, 96, 47–62. [Google Scholar] [CrossRef]

- Armand, M.T.; Roger, A.E. An AHP algorithm for an effective ERP type selection based on the african context. Electron. J. Inf. Syst. Dev. Ctries 2017, 83, 1–17. [Google Scholar] [CrossRef]

- Goepel, K.D. Implementing the Analytic Hierarchy Process as a standard method for multi–criteria decision making in corporate enterprises—A new ahp excel template with multiple inputs. In Proceedings of the International Symposium on the Analytic Hierarchy Process, Kuala Lumpur, Malaysia, 23–26 June 2013. [Google Scholar] [CrossRef]

- Simon, J.; Adamu, A.; Abdulkadir, A.; Henry, A.H. Analytical hierarchy process (AHP) model for prioritizing alternative strategies for malaria control. Asian J. Probab. Stat. 2019, 5, 1–8. [Google Scholar] [CrossRef][Green Version]

- Saaty, T.L. The Analytic Hierarchy Process; McGrawHill: New York, NY, USA, 1980. [Google Scholar]

- Lacurezeanu, R.; Bresfelean, V.P. Making a Multi-criteria analysis model for choosing an ERP for SMEs in a KM world. In Intelligent Methods in Computing, Communications and Control—ICCCC 2020; Advances in Intelligent Systems and Computing; Dzitac, I., Dzitac, S., Filip, F.G., Kacprzyk, J., Manolescu, M.J., Oros, H., Eds.; Springer: Cham, Switzerland, 2021; Volume 1243, pp. 257–273. [Google Scholar]

- Avram, C.D.; Zota, R.D.; Ciovica, L. Developing an ERP strategy based on the IT solution life cycle. Econ. Inf. 2012, 12, 26. [Google Scholar]

- Deloitte. ERP Vendor Selection for Core Financials. Available online: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/process-and-operations/us-erp-vendor-selection-for-core-financials.pdf (accessed on 18 March 2021).

- Ghosh, I.; Biswas, S. A comparative analysis of multi–criteria decision models for ERP package selection for improving supply chain performance. Asia Pac. J. Manag. Res. Innov. 2016, 12, 250–270. [Google Scholar] [CrossRef]

- Kłos, S.; Trebuna, P. Using the AHP method to select an ERP system for an SME manufacturing company. Manag. Prod. Eng. Rev. 2014, 5, 14–22. [Google Scholar] [CrossRef]

- Kilic, H.S.; Zaim, S.; Delen, D. Selecting “the best” ERP system for SMEs using a combination of ANP and PROMETHEE methods. Expert Syst. Appl. 2015, 42, 2343–2352. [Google Scholar] [CrossRef]

- Alpers, S.; Becker, C.; Eryilmaz, E.; Schuster, T. A systematic approach for evaluation and selection of ERP systems. Lect. Notes Bus. Inf. Process. 2014, 193, 36–48. [Google Scholar]

- Zeng, Y.R.; Wang, L.; Xu, X.H. An integrated model to select an ERP system for Chinese small– and medium-sized enterprise under uncertainty. Technol. Econ. Dev. Econ. 2017, 23, 38–58. [Google Scholar] [CrossRef]

- Isachi, S.E. Importance of smes in the economic development of Romania. J. Financ. Monet. Econ. 2015, 2, 191–198. [Google Scholar]

- Bodislav, A.D.; Radulescu, C.V.; Moise, D.; Burlacu, S. Environmental policy in the Romanian public sector. J. Emerg. Trends Mark. Manag. 2019, 1, 312–317. [Google Scholar]

- Pana, V.; Pana, I. Sustainable development and demography, scientific bulletin—Economic sciences. Econ. Eur. Econ. Policies 2006, 9, 51–58. [Google Scholar]

- Costache, C.; Dumitrascu, D.-D.; Maniu, I. Facilitators of and barriers to sustainable development in small and medium–sized enterprises: A descriptive exploratory study in Romania. Sustainability 2021, 13, 3213. [Google Scholar] [CrossRef]

- Gillespie, A. The Illusion of Progress—Unsustainable Development in International Law and Policy; Earthscan: London, UK, 2001; p. 256. ISBN 9781853837579. [Google Scholar]

- Aragon-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; Garcia-Morales, V.J. Environmental strategy and performance in small firms: A resource-based perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef]

- Heledd Jenkins, H. A business opportunity model of corporate social responsibility for small– and medium–sized enterprises. Bus. Eth. Eur. Rev. 2009, 18, 21–36. [Google Scholar] [CrossRef]

- European Commission. Report of the European Commission for Romania 2019. Available online: https://ec.europa.eu/info/sites/info/files/file_import/2019-european-semester-country-report-romania_en.pdf (accessed on 27 February 2021).

- OIR POSDRU. 2021. Available online: https://www.agerpres.ro/economic-intern/2021/01/20/ (accessed on 25 February 2021).

- Journeault, M.; Perron, A.; Vallières, L. The collaborative roles of stakeholders in supporting the adoption of sustainability in SMEs. J. Environ. Manag. 2021, 287, 112349. [Google Scholar] [CrossRef] [PubMed]

- Johnson, M.P.; Schaltegger, S. Two decades of sustainability management tools for SMEs: How far have we come? J. Small Bus. Manag. 2017, 54, 481–505. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Klemeš, J.J. A master plan for the implementation of sustainable enterprise resource planning systems (part II): Development of a roadmap. Chem. Eng. Trans. 2016, 52, 1099–1104. [Google Scholar] [CrossRef]

- Lotfy, M.A.M.B. Sustainability of enterprise resource planning (ERP) Benefits Postimplementation: An Individual User Perspective; Walden University: Minneapolis, MN, USA, 2015. [Google Scholar]

- Hewavitharana, F.S.T.; Perera, A. Gap analysis between ERP procedures and construction procedures. MATEC Web Conf. 2019, 266, 03011. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Ismail, S.; Mohamed Shaharoun, A.; Klemeš, J.J.; Zeinalnezhad, M. A master plan for the implementation of sustainable enterprise resource planning systems (part I): Concept and methodology. J. Clean. Prod. 2016, 136, 176–182. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Gonib, F.A.; Klemeš, J.J. Steps towards the implementation of sustainable enterprise resource planning systems. Chem. Eng. Trans. 2018, 70, 283–288. [Google Scholar]

- Zvezdov, D.; Hack, S. Carbon footprinting of large product portfolios. Extending the use of enterprise resource planning systems to carbon information management. J. Clean. Prod. 2016, 135, 1267–1275. [Google Scholar] [CrossRef]

- Anwara, S.; Ghaffarb, M.; Razzaqc, F.; Bibid, B. E-waste reduction via virtualization in green computing. Am. Sci. Res. J. Eng. Technol. Sci. 2018, 41, 1–11. [Google Scholar]

- Kewat, P.; Narain, B.; Kumar, S. Green computing and environment: A review. In Proceedings of the National Conference on Knowledge, Innovation in Technology and Engineering (NCKITE), Chhattisgarh, India, 10–11 April 2015; pp. 242–246. [Google Scholar]

- Mukta, T.A.; Ahmed, I. Review on E-waste management strategies for implementing green computing. Int. J. Comput. Appl. 2020, 177, 45–52. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Klemeš, J.J. Evaluation of a framework for sustainable enterprise resource planning systems implementation. J. Clean. Prod. 2018, 190, 778–786. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Malik, M.N.; Khan, H.H.; Klemeš, J.J. Evaluation of the sustainable enterprise resource planning implementation steps. Chem. Eng. Trans. 2019, 72, 445–450. [Google Scholar]

- Luthra, S.; Mangla, S.K.; Xu, L.; Diabat, A. Using AHP to evaluate barriers in adopting sustainable consumption and production initiatives in a supply chain. Int. J. Prod. Econ. 2016, 181, 342–349. [Google Scholar] [CrossRef]

- Sandarbh Shukla, P.K.; Mishra, R.J.; Yadav, H.C. An integrated decision making approach for ERP system selection using SWARA and PROMETHEE method. Int. J. Intell. Enterpr. 2016, 3, 120–147. [Google Scholar] [CrossRef]

- Tam, E.K. Challenges in using environmental indicators for measuring sustainability practices. J. Environ. Eng. Sci. 2002, 1, 417–425. [Google Scholar] [CrossRef]

- Chengcheng, F.; Carrell, J.D.; Hong-Chao, Z. An investigation of indicators for measuring sustainable manufacturing. In Proceedings of the 2010 IEEE International Symposium on Sustainable Systems and Technology, Arlington, VA, USA, 17–19 May 2010; pp. 1–5. [Google Scholar] [CrossRef]

- Staniškis, J.K.; Arbačiauskas, V. Sustainability performance indicators for industrial enterprise management. Environ. Res. Eng. Manag. 2009, 48, 42–50. [Google Scholar] [CrossRef]

- Joung, C.B.; Carrell, J.; Sarkar, P.; Feng, S.C. Categorization of indicators for sustainable manufacturing. Ecol. Indic. 2013, 24, 148–157. [Google Scholar] [CrossRef]

- Hasan, M.S.; Ebrahim, Z.; Wan Mahmud, W.H.; Ab Rahman, M.N. Sustainable-ERP system: A preliminary study on sustainability indicators. J. Adv. Manuf. Technol. JAMT 2017, 11, 61–74. [Google Scholar]

- Patalas–Maliszewska, J.; Klos, S. The methodology of the S–ERP system employment for small and medium manufacturing companies. IFAC PapersOnLine 2019, 52, 10, 85–90. [Google Scholar] [CrossRef]

- Alsharari, N.M.; Al–Shboul, M.; Alteneiji, S. Implementation of cloud ERP in the SME: Evidence from UAE. J. Small Bus. Enterpr. Devel. 2020, 27, 299–327. [Google Scholar] [CrossRef]

- Eldrandaly, K. GIS software selection: A multi-criteria decision making approach. Appl. GIS 2007, 3, 1–17. [Google Scholar]

- Motaki, N. ERP Selection: A Step-by-Step Application of AHP Method. Available online: https://www.researchgate.net/publication/320477208 (accessed on 24 April 2021).

- Gupta, S.; Dangayach, G.S.; Singh, A.K.; Rao, P.N. Analytic hierarchy process (ahp) model for evaluating sustainable manufacturing practices in indian electrical panel industries. Procedia Soc. Behav. Sci. 2015, 189, 208–216. [Google Scholar] [CrossRef]

- Lizarralde, R.; Ganzarain, J.; Zubizarreta, M. Assessment and selection of technologies for the sustainable development of an R&D center. Sustainability 2020, 12, 10087. [Google Scholar] [CrossRef]

- Dey, P.K.; Cheffi, W. Green supply chain performance measurement using the analytic hierarchy process: A comparative analysis of manufacturing organizations. Prod. Planing Control 2013, 24, 702–720. [Google Scholar] [CrossRef]

- Sultan, A.; Alarfaj, K.A.; Alkutbi, G.A. Analytic hierarchy process for the success of e-government. Bus. Strategy Rev. 2012, 6, 295–306. [Google Scholar] [CrossRef]

- Subramanian, N.; Ramanathan, R. A review of applications of analytic hierarchy process in operations management. Int. J. Prod. Econ. 2012, 138, 215–241. [Google Scholar] [CrossRef]

- Harputlugil, T.; Prins, M.; Gültekin, A.T.; Topçu, İ. Conceptual framework for potential implementations of multi criteria decision making (MCDM) methods for design quality assessment. In Proceedings of the MISBE Conference, Amsterdam, The Netherlands, 19–23 June 2011. [Google Scholar]

- Meghana, H.L.; Asish, O.M.; Lewlyn, L.R. Prioritizing the factors affecting cloud ERP adoption—An analytic hierarchy process approach. Int. J. Emerg. Markets 2018, 13, 1559–1577. [Google Scholar]

- Saaty, T.L. Decision making with the analytic hierarchy process. Int. J. Serv. Sci. 2008, 1, 83–98. [Google Scholar] [CrossRef]

- Pantelidis, P.; Pazarskis, M.; Karakitsiou, A.; Dolka, V. Modeling an analytic hierarchy process (AHP) assessment system for municipalities in Greece with public accounting of austerity. J. Acc. Tax. 2018, 10, 48–60. [Google Scholar] [CrossRef][Green Version]

- Bunruamkaew, K. How to Do AHP Analysis in Excel. 2012. Available online: http://giswin.geo.tsukuba.ac.jp/sis/tutorial/How%20to%20do%20AHP%20analysis%20in%20Excel.pdf (accessed on 17 January 2021).

- Huang, S.Y.; Chiu, A.A.; Chao, P.C.; Arniati, A. Critical success factors in implementing enterprise resource planning systems for sustainable corporations. Sustainability 2020, 11, 6785. [Google Scholar] [CrossRef]

- Han, S. A practical approaches to decrease the consistency index in AHP. In Proceedings of the 2014 Joint 7th International Conference on Soft Computing and Intelligent Systems (SCIS) and 15th International Symposium on Advanced Intelligent Systems (ISIS), Kitakyushu, Japan, 3–6 December 2014; pp. 867–872. [Google Scholar] [CrossRef]

- Lai, V.S.; Wong, B.K.; Cheung, W. Group decision making in a multiple criteria environment: A case using the AHP in software selection. Eur. J. Opt. Res. 2002, 137, 134–144. [Google Scholar] [CrossRef]

- A Practical Guide for Consensus-Based Decision Making. Available online: https://www.tamarackcommunity.ca/hubfs/Resources/Tools/Practical%20Guide%20for%20Consensus–Based%20Decision%20Making.pdf (accessed on 17 March 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No | Criteria | Short Description | Articles |

|---|---|---|---|

| 1 | Functionality | Sufficient functions to fulfill all the requirements of an SME, (feature requirements, technical features, capability) | [1,20,23,29,30,31,32,33,34,35,36] |

| 2 | Ease of Use/usability | Ease of navigation, operability, comprehensibility, and learnability of the ERP to be user–friendly and to attain effectiveness and satisfaction in a specific use background | [1,21,23,29,30,31,32,35,36] |

| 3 | Feasibility | Assesses the outcomes of the ERP system advancement and implementation on sustainable development, integration, and performance | [1,36] |

| 4 | Portability | Efforts to transfer ERP from between different hardware platforms or software environments, mobility | [1,21,31,33,36] |

| 5 | Cloud ERP options and Energy Efficiency | ERP system runs on a vendor’s cloud platform; optimization of ERP system’s energy consumption in relation to resources used in the data center. | [1,21,30,31,33] |

| 6 | Ease of Implementation | Implementation time, pace, and difficulties of integrating business modules in the ERP system | [23,29,30,32,33,36] |

| 7 | Price of Software | ERP cost, affordability, detailed costs, total cost of ownerships (TCO) | [1,21,23,29,30,31,32,33,34,35,36] |

| 8 | Quality of Documentation | Quality manuals, plans and procedures, work instructions | [29,36] |

| 9 | Level of Vendor support | Technical support, consulting, education, maintenance, training, reseller support | [1,21,23,29,30,31,32,33,36] |

| 10 | Developer’s Track Record of Performance | Vendor ecosystem, vendor’s technical capability and credentials, vendor reputation and experience, credibility of the system, community of customers and case studies | [1,23,29,31,32,33,34,36] |

| 11 | Ability to fit to Business | Business strategic fits, compatibility, customization/parametrization | [21,23,29,31,32,33,34,35,36] |

| Importance Intensity | Definition | Explanation |

|---|---|---|

| 1 | Equal | Two activities have equal contribution to the objective |

| 2 | Weak/slight | |

| 3 | Moderate | One activity is faintly preferred over another, established on judgment and experience |

| 4 | Moderate+plus | |

| 5 | Strong | One activity is strongly preferred over another, established on judgment, experience |

| 6 | Strong+plus | |

| 7 | Very strong (proved importance) | One activity is very strongly preferred over another, established on judgment, experience; its dominance is proved by practice |

| 8 | Very–very strong | |

| 9 | Extreme | The substantiation when one activity is preferred over another is at the topmost possible order of affirmation |

| Reciprocals of abovementioned | If activity i is attributed one of the abovementioned non–zero values when compared to activity j, then activity j when compared to activity i has the reciprocal value | A reasonable statement |

| 1.1–1.9 | When activities are very close to each other | Although it might be complicated to allocate the best value, but in comparison to other dissimilar activities the size of small numbers wouldn’t be too perceptible, however they are able to denote the activities’ relative importance. |

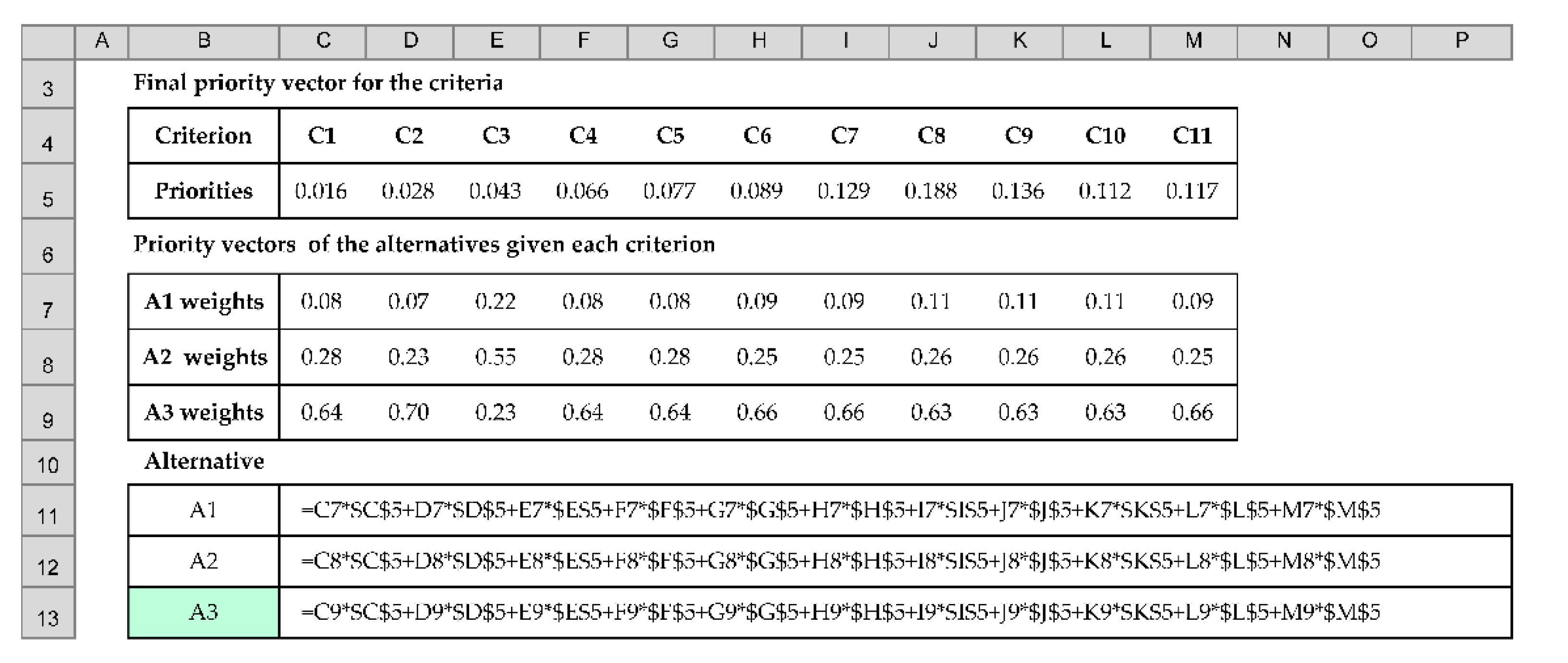

| Alternative | Weight | Rank |

|---|---|---|

| A1 | 0.102 | 3 |

| A2 | 0.271 | 2 |

| A3 | 0.627 | 1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lacurezeanu, R.; Chis, A.; Bresfelean, V.P. Integrated Management Solution for a Sustainable SME—Selection Proposal Using AHP. Sustainability 2021, 13, 10616. https://doi.org/10.3390/su131910616

Lacurezeanu R, Chis A, Bresfelean VP. Integrated Management Solution for a Sustainable SME—Selection Proposal Using AHP. Sustainability. 2021; 13(19):10616. https://doi.org/10.3390/su131910616

Chicago/Turabian StyleLacurezeanu, Ramona, Alexandru Chis, and Vasile Paul Bresfelean. 2021. "Integrated Management Solution for a Sustainable SME—Selection Proposal Using AHP" Sustainability 13, no. 19: 10616. https://doi.org/10.3390/su131910616

APA StyleLacurezeanu, R., Chis, A., & Bresfelean, V. P. (2021). Integrated Management Solution for a Sustainable SME—Selection Proposal Using AHP. Sustainability, 13(19), 10616. https://doi.org/10.3390/su131910616