1. Introduction

The need of reducing the use of fossil fuels in shipping as means to substantially lessen the emissions of carbon dioxide (CO

2) and generally of green-house gases (GHG), as well as the related policies and instruments of the International Maritime Organization (IMO) are widely discussed in the literature and the relevant press [

1,

2,

3]. The policy goal is to achieve a 50% reduction of carbon emissions against the 2008 levels; this target is also quantified as reduction of CO

2 emissions per transport work, as an average across all segments of international shipping, by at least 40% by 2030. However, both the regulatory framework as well as the technical solutions are not fully determined yet; for example, technologies and fuels promoted as technical solutions are not considered in the current set of applicable rules and regulations [

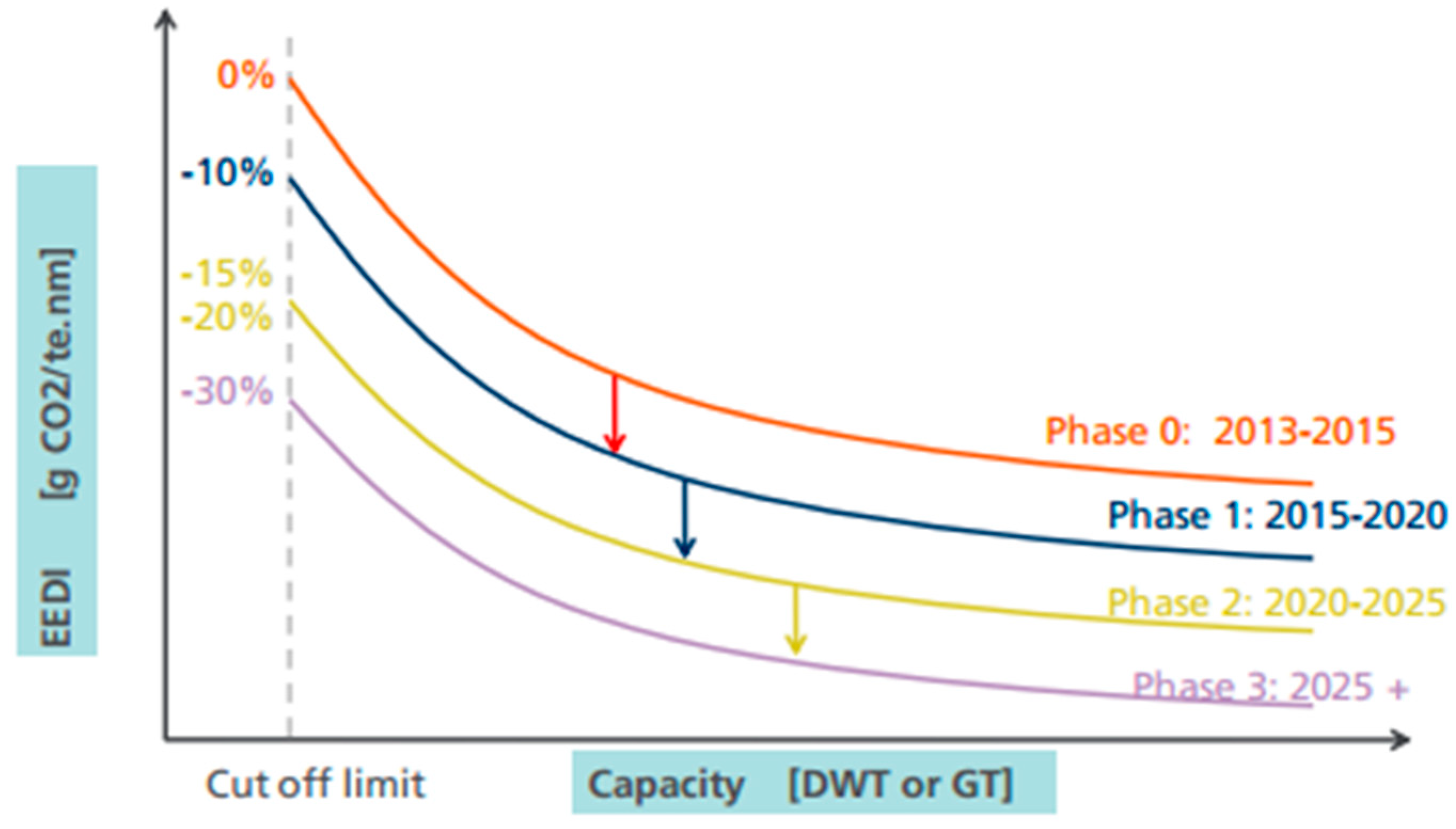

4]. In the 76th session of the Marine Environment Protection Committee (MEPC) of the IMO, new regulations, such as the Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) were adopted, while in future sessions they will be finalized.

The above policy goals also dictate the need to renew parts of the fleet that are not expected to comply with the new regulations; new ships, emitting less GHG per transport work, will replace ships that are close to the end of their economic life or the retrofit investment is not justified. In addition, a substantial number of existing ships should install new technologies or retrofit parts of their propulsion plants in order to comply with the stricter set of environmental rules and limits. Therefore, owners and financiers should schedule investments of substantial amounts within the next years in order to meet the policy goals. Considering that UNCTAD estimates the commercial value of the fleet at USD 952 billion [

5] and also considering the retreat of banking exposure [

6], the total sum will amount to billion of US dollars. In this regard, Hoffmann et al. estimated an excess capital expenditure for new-build ships of up to USD 761 billion in order to achieve maritime carbon targets [

7]. Recently, Stopford estimated an amount of USD 3.4 trillions to be necessary as maritime investments [

8], i.e., circa four times the value of the existing fleet. Bearing the above in mind, the objective of this work was to estimate the total amount required for the renewal and retrofit of the assets by 2026, as the midpoint to 2030. The analysis period of five years, from 2021 until 2026, was chosen deliberately for two main reasons. First, the time horizon can be adequately anticipated through the 2020 orderbook and is simultaneously long enough for sufficient fleet renewal to occur. Secondly, a period of 5 years appears feasible to practically understand the short- to mid-term financial impact, as opposed to more long-term considerations spanning several decades, as these involve multiple uncertain predictions to be made (such as, e.g., shifts in the fleet composition or fuel mix). Therefore, by deriving the analysis results from the current fleet structure as is, and by providing timely financial implications, the results are regarded as a valuable and practical contribution to the ongoing discourse on maritime decarbonization.

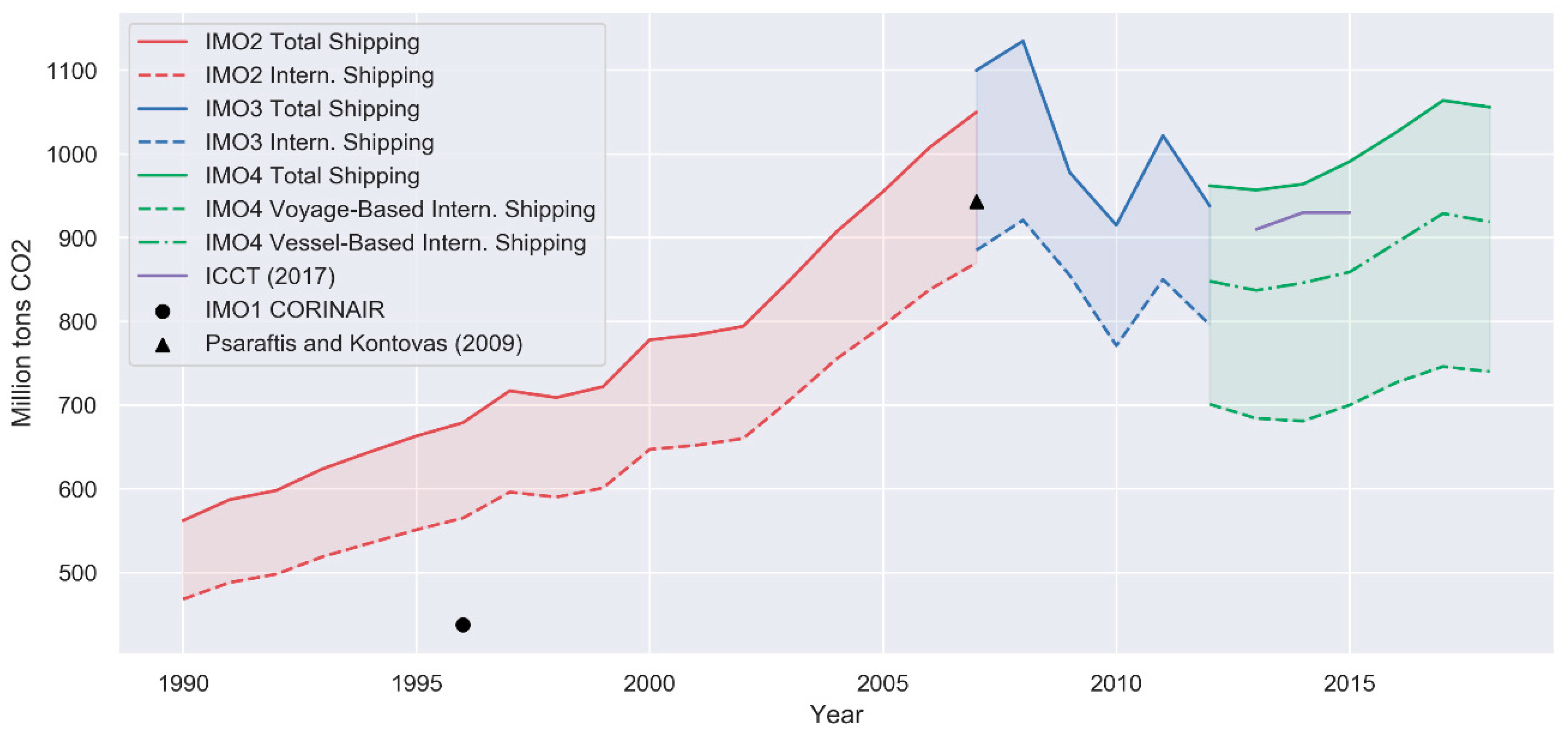

Methodologically, a bottom-to-top approach was followed, similar to the approach of Psaraftis and Kontovas [

9]. Amongst other findings, they delivered a specific breakdown of maritime emissions by vessel types and size brackets, which provides guidance for our analysis, too. Similarly, we intended to break down the financial implications of greening the fleet by vessel types and sizes and, therefore, provide results relevant to the industry, while also specifying the impacts on certain sub-segments.

The paper is structured as follows: the next section briefly outlines the recent policy developments. It should be noted that critical examination of the regulation is beyond the scope of this work, as many researchers are contributing on this aspect [

10,

11,

12,

13,

14]. Nevertheless, a section reviewing related works and literature is offered with the aim to illustrate the gap in the literature, which this work aimed to bridge. In

Section 3, the underlying methodology and model assumptions are introduced. The dataset as well as model input parameters are analyzed in

Section 4, before the results are discussed in

Section 5. The last section concludes and summarizes this work and highlights the paper’s key findings and potential implications.

3. Methodology

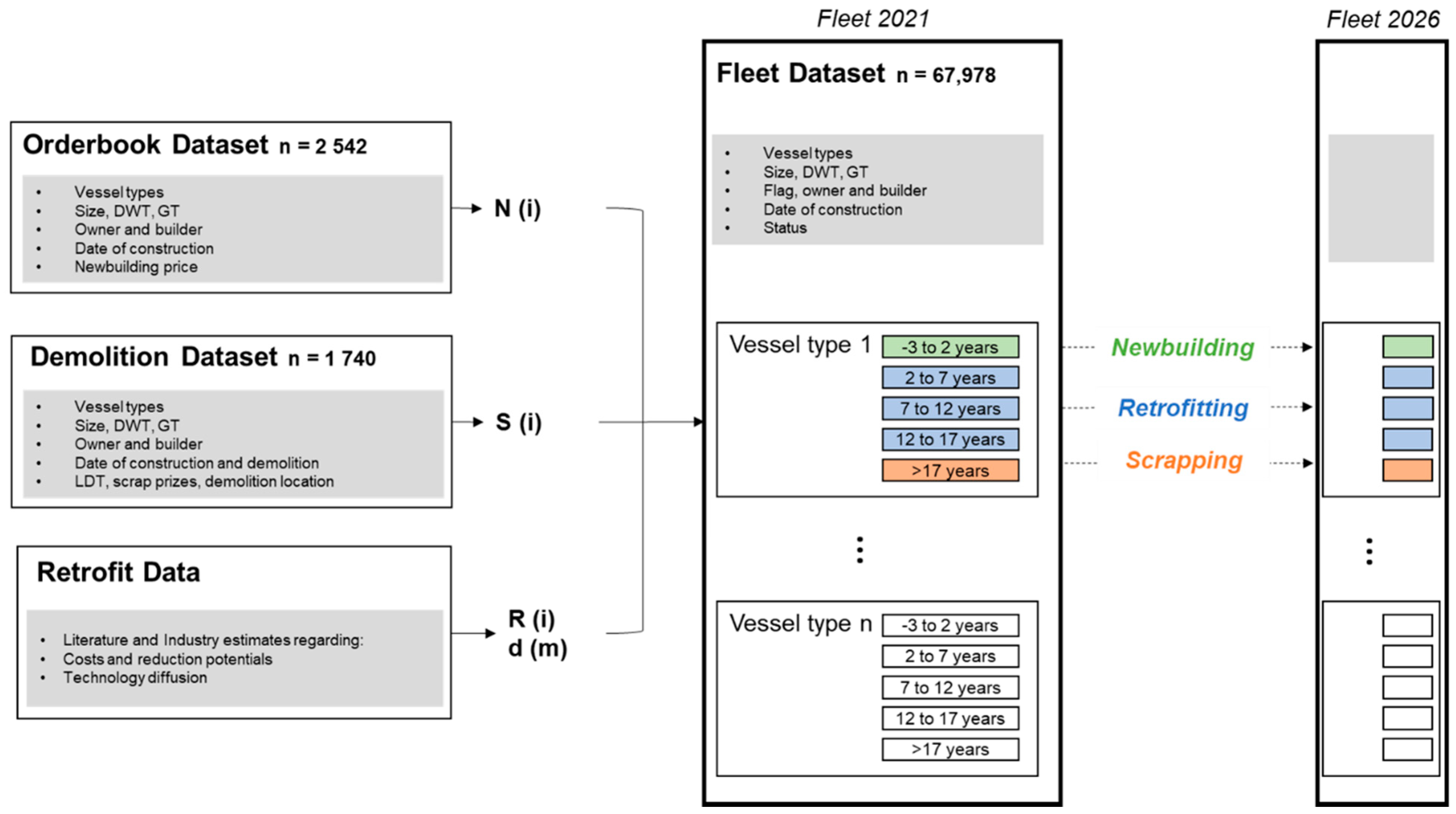

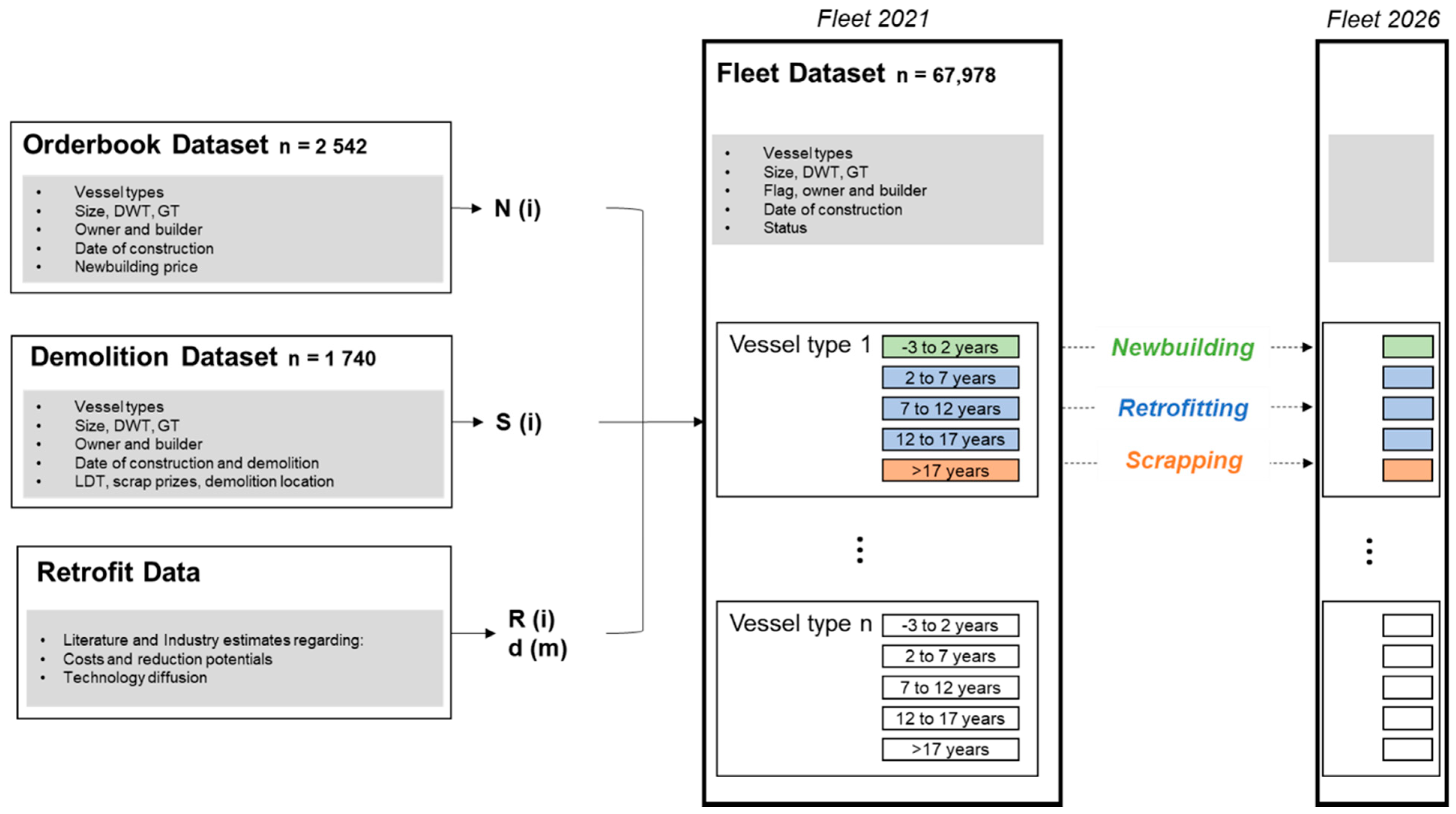

Overall, the paper developed a vessel-based model that builds up on the classification and age breakdown of the global fleet.

Figure 5 provides a brief overview of the methodological framework and indicates the relationship between the various datasets employed in the model.

Based on the 2020 fleet structure as documented in the databases of Clarksons’ Shipping Intelligence Network, the model approximated the financial need on the level of each segment, considering their respective age and size profiles. Opposing to, e.g., [

7,

59], who focus on capital expenditure for building new ships, the analysis explicitly included the expenditure associated with retrofitting the current fleet as well as the revenue generated through demolition sales that usually fuel renewal policies. Notably, the terms scrapping and demolition were used synonymously within the analysis to describe the process of recycling key resources at the end of a vessel’s useful lifetime, in line with prevalent maritime terminology [

63,

64].

Overall, the model considered a discrete time period of the next five years, i.e., from 2021 to 2026. Thus, the analysis focused on the short- to midterm financial dimension of decarbonizing the fleet. The model differentiated vessels by their age and assigned them to five age groups which determine whether the vessels are eligible for retrofitting, scrapping, or are part of the newbuilding age bin (see

Figure 5).

As a direct consequence of the age bin set-up, the average useful economic life of a vessel is defined. It is acknowledged that the analysis of empirical vessel demolition dynamics is itself highly complex and subject to many variables [

34,

37,

64]. Within the model, a uniform age threshold of 22 years was employed, which will be further elaborated on in

Section 4. In general, shorter as well longer expected vessel lifetime scenarios can be implemented in the model by iteratively adjusting the age bin structure presented in

Figure 5.

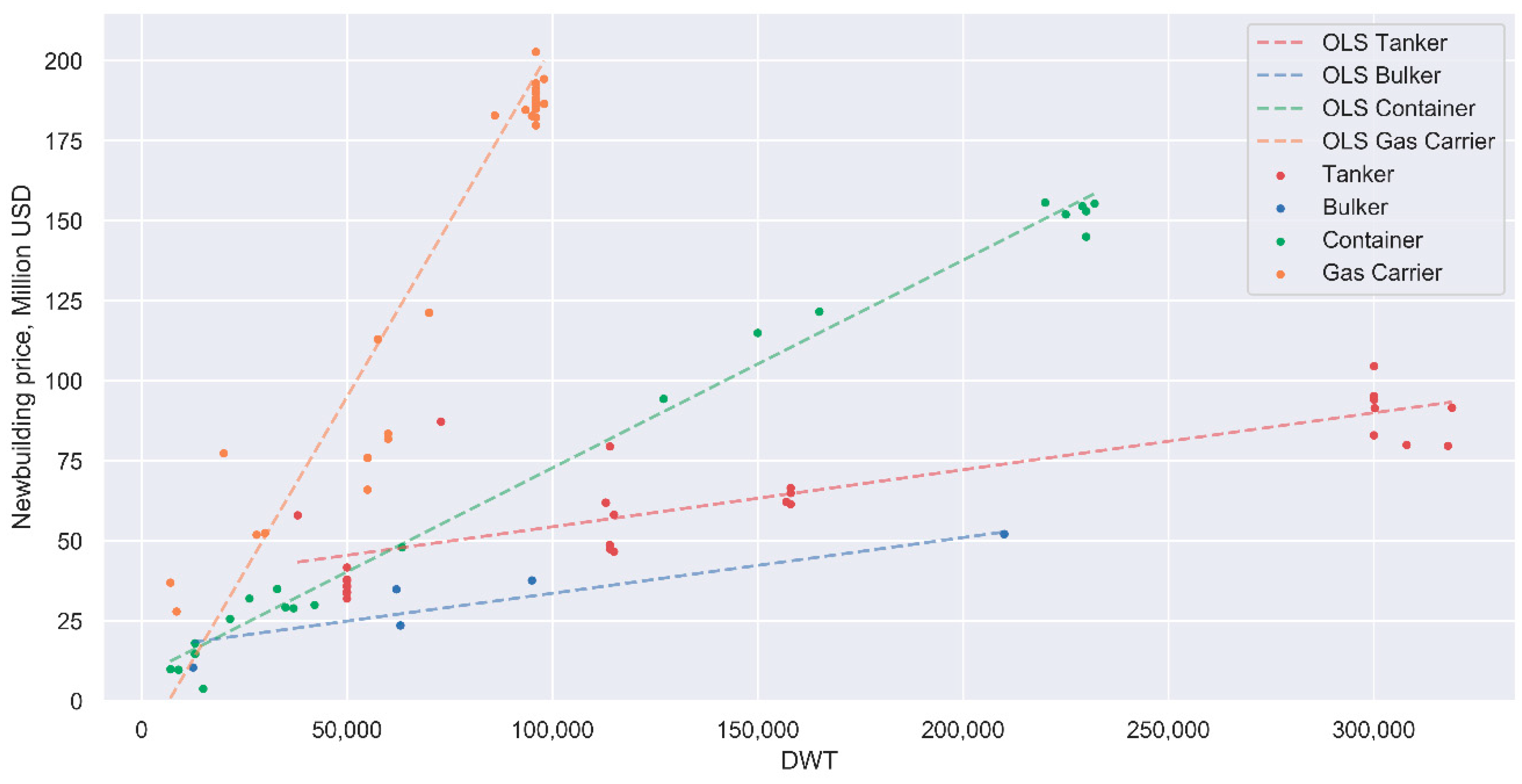

On the level of each vessel type, the total costs of decarbonizing the respective fleet segment are divided into the costs of new-build ships

, the costs for retrofit installations

, and the income generated through demolition sales

(see Equations (1) and (2)).

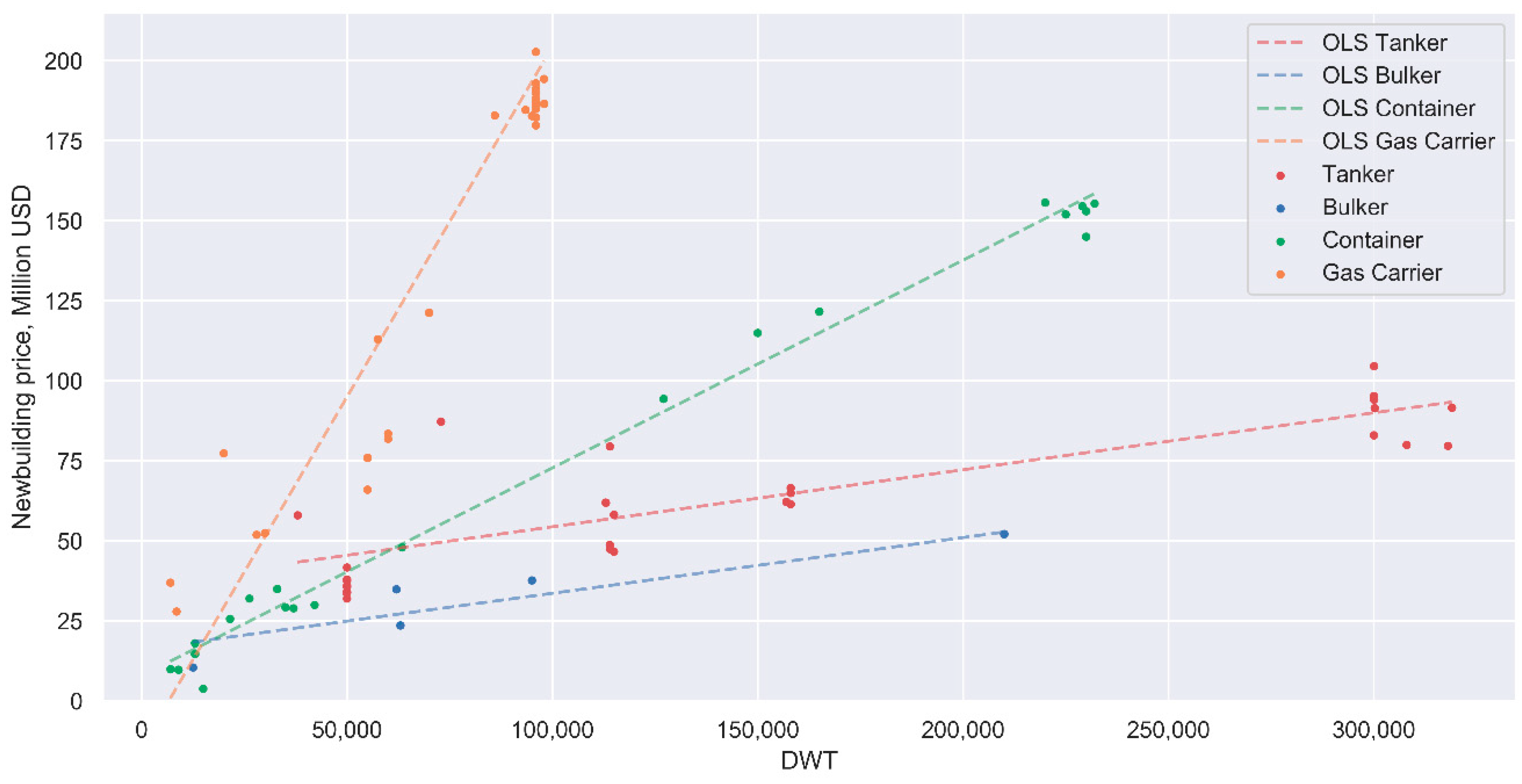

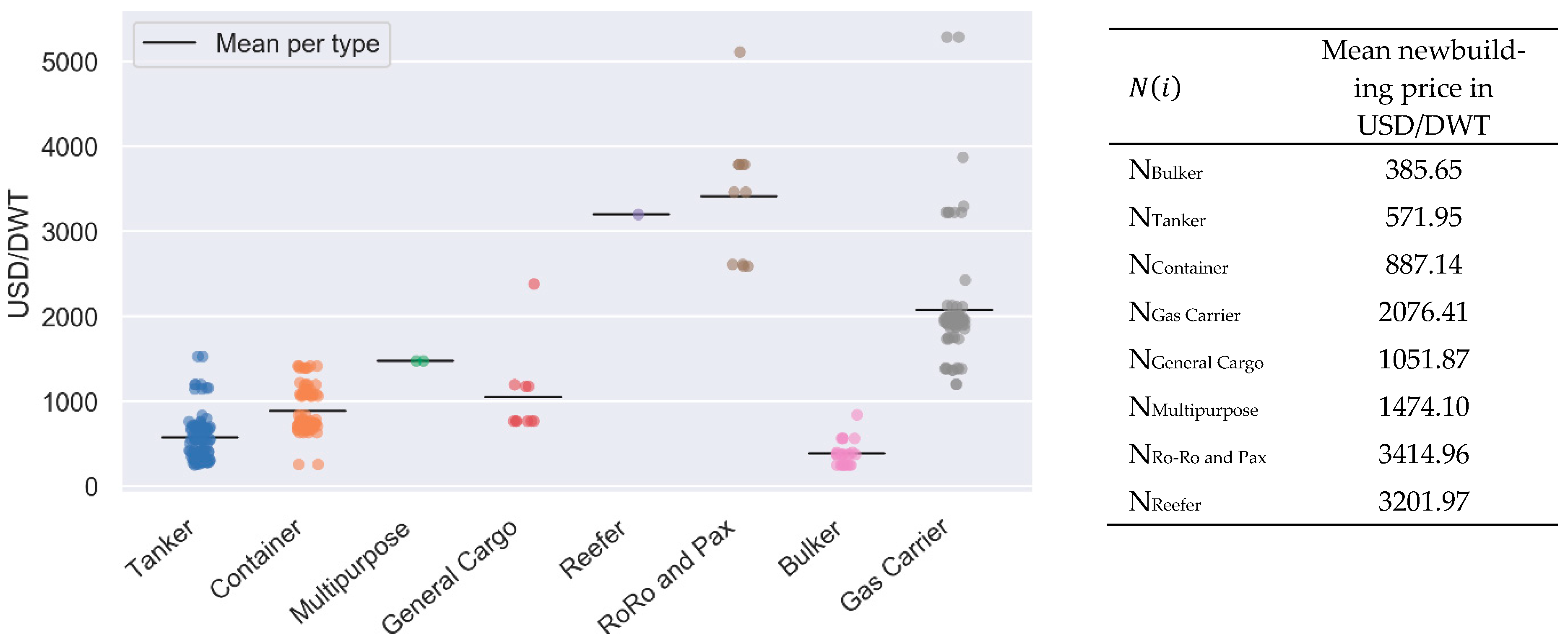

The costs associated with newbuilding (Equation (3)) are subject to the number of ordered ships

, the observed price level

, the average vessel deadweight

, and segment growth expectations

.

where

i = vessel type;

m = age bin;

n (i, m) = number of vessels per type and age bin (−3 to 2y);

N (i) = costs of new-build vessels per type in USD/DWT;

= mean deadweight per vessel type and age bin;

g (i) = growth factor per vessel type.

The estimated retrofit costs (Equation (4)) are represented by the sum of the three age bins eligible for retrofitting. For each bin, the retrofit costs are subject to the price level

, a degressive retrofit diffusion factor between 0 and 1

, the average vessel deadweight, and the number of vessels per type and age bin.

where

n (i, m) = number of vessels per type and age bin (2 to 7 years; 7 to 12 years; 12 to 17 years);

d (m) = retrofit diffusion factor per age bin [0; 1];

R (i) = costs of retrofit installation per vessel type in USD/DWT.

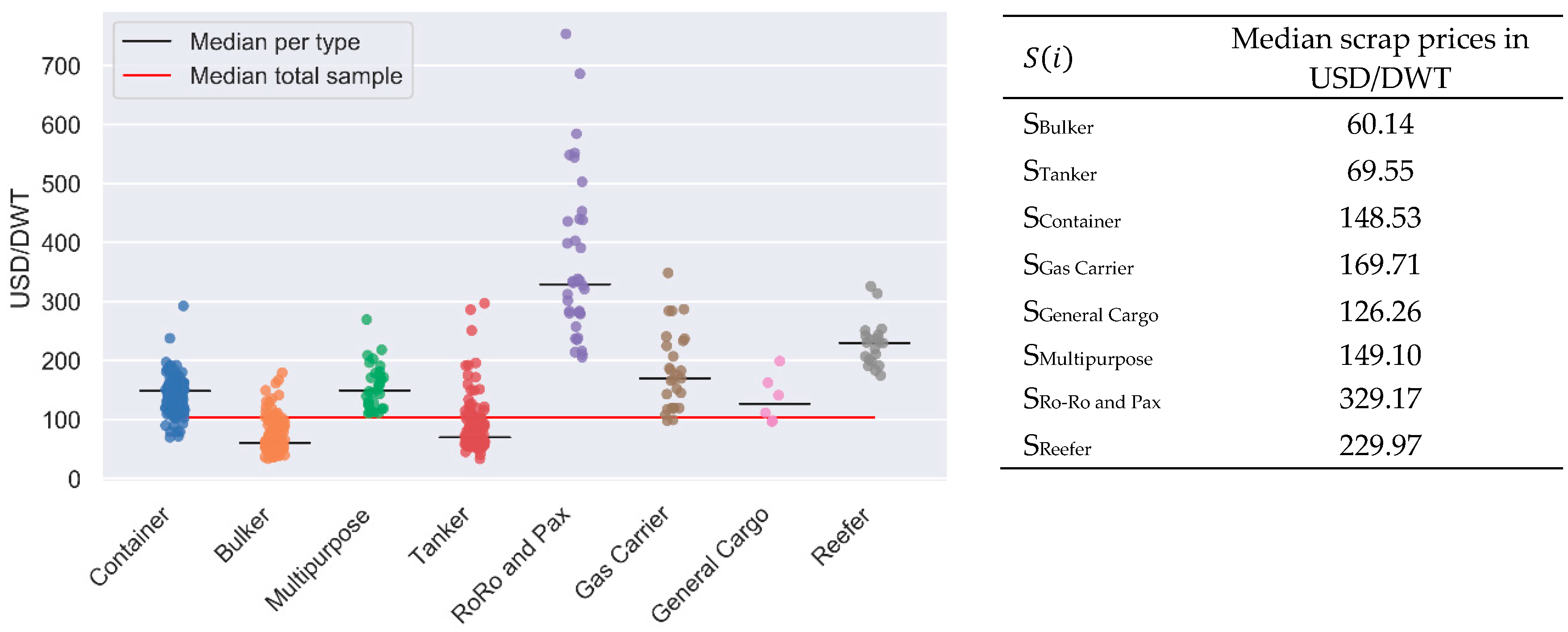

The income generated through demolition sales (Equation (5)) is derived from the number of ships older than 17 years as of 2020 (i.e., whose lifetime exceeds 22 years towards 2026) and is subject to the scrap price level

as well as the average vessel deadweight.

where

n (i, m) = number of vessels per type and age bin (>17 years);

S (i) = revenue through demolition sales per vessel type in USD/DWT.

5. Analysis of Results

5.1. Estimated Financial Need of Short-Term Decarbonization

The previous sections have documented the search for appropriate model inputs in detail, resulting in the specified base case estimates. These will be applied and extended through modelling further scenarios. To reduce the number of potential variable combinations, clusters of variables (e.g., retrofit price levels across different vessel types) were altered simultaneously as relative deviations from the base case parameters (see

Table 9). These scenarios served as an indication of the different model outcomes for variable combinations which deviate from the base case settings (as specified in previous sections). As shown in

Table 9, the scenarios represent uni- and multivariate modifications of the original model, which are intended to account for various sources of fluctuation in the relevant markets, affecting the respective model variables.

Notably, particular attention is drawn to the base case model output as well as lower and upper bound implications. The further scenarios will not be discussed individually but are represented by means of the total value ranges.

Using bulk carriers as an example, the model application shall briefly be demonstrated. The Equations (2)–(5) introduced in

Section 3 and the base case parameters for bulk carriers imply the following calculations:

By replicating this logic for all vessel types and iterating over the introduced scenarios, the final modelling results can be derived. The results are presented in

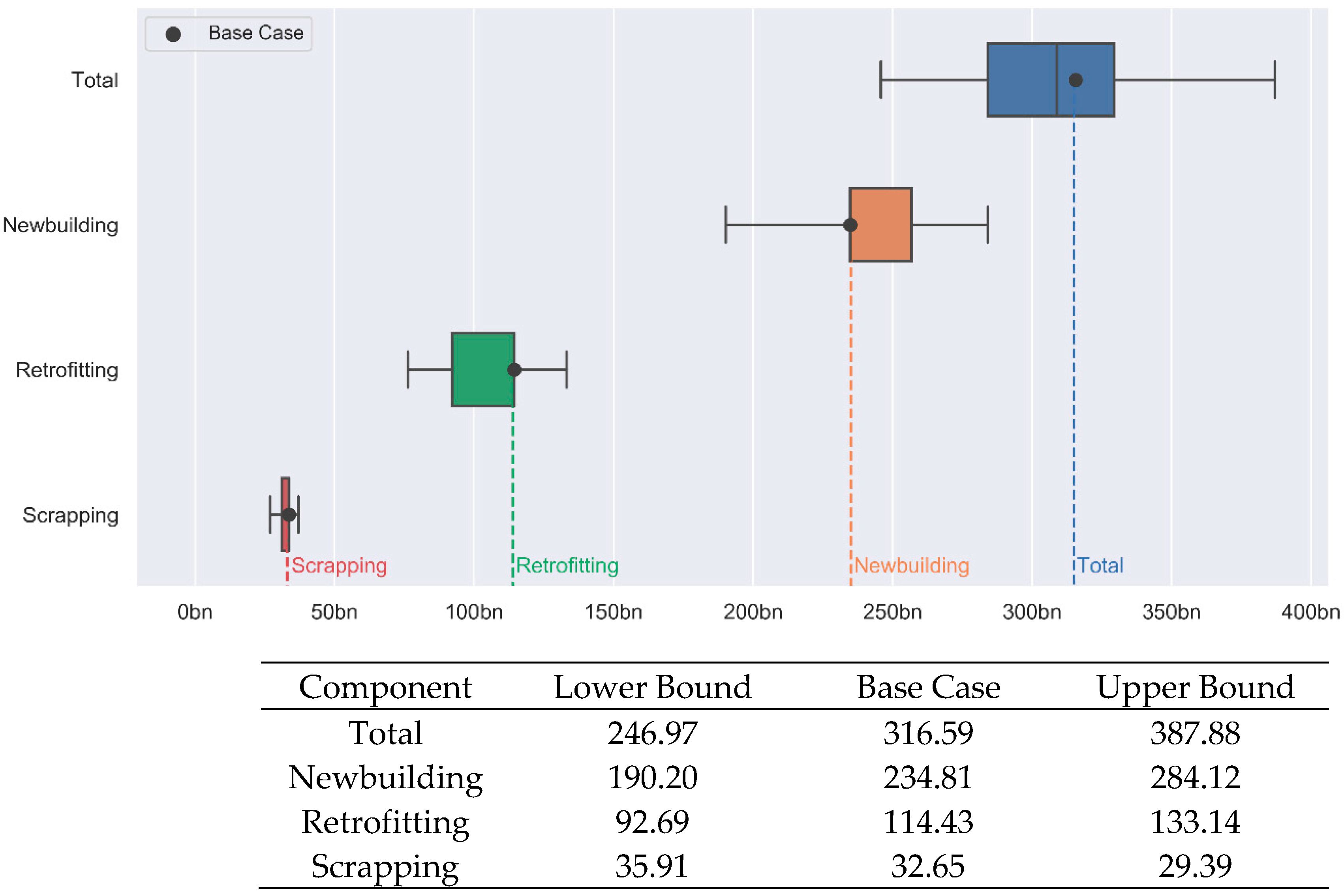

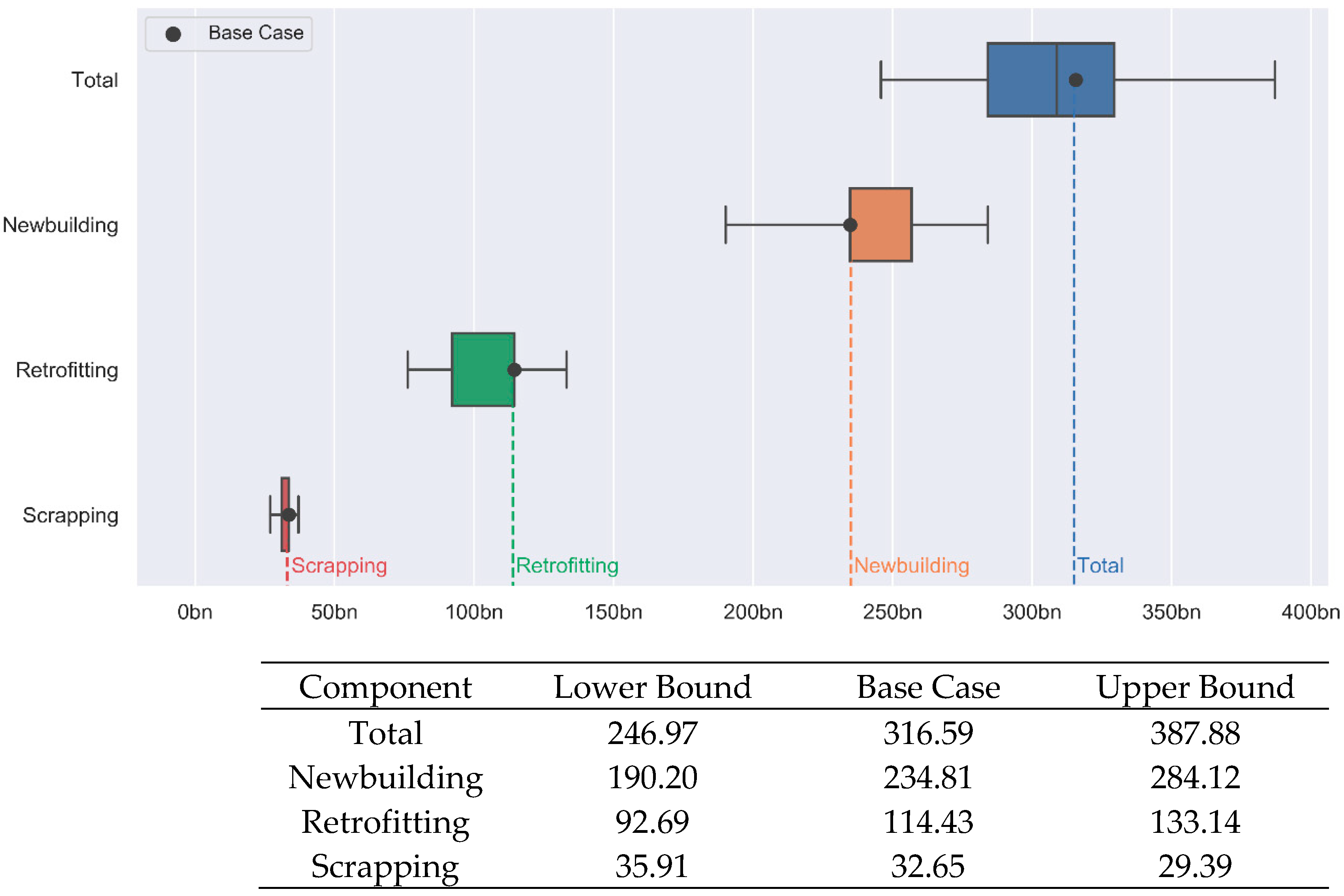

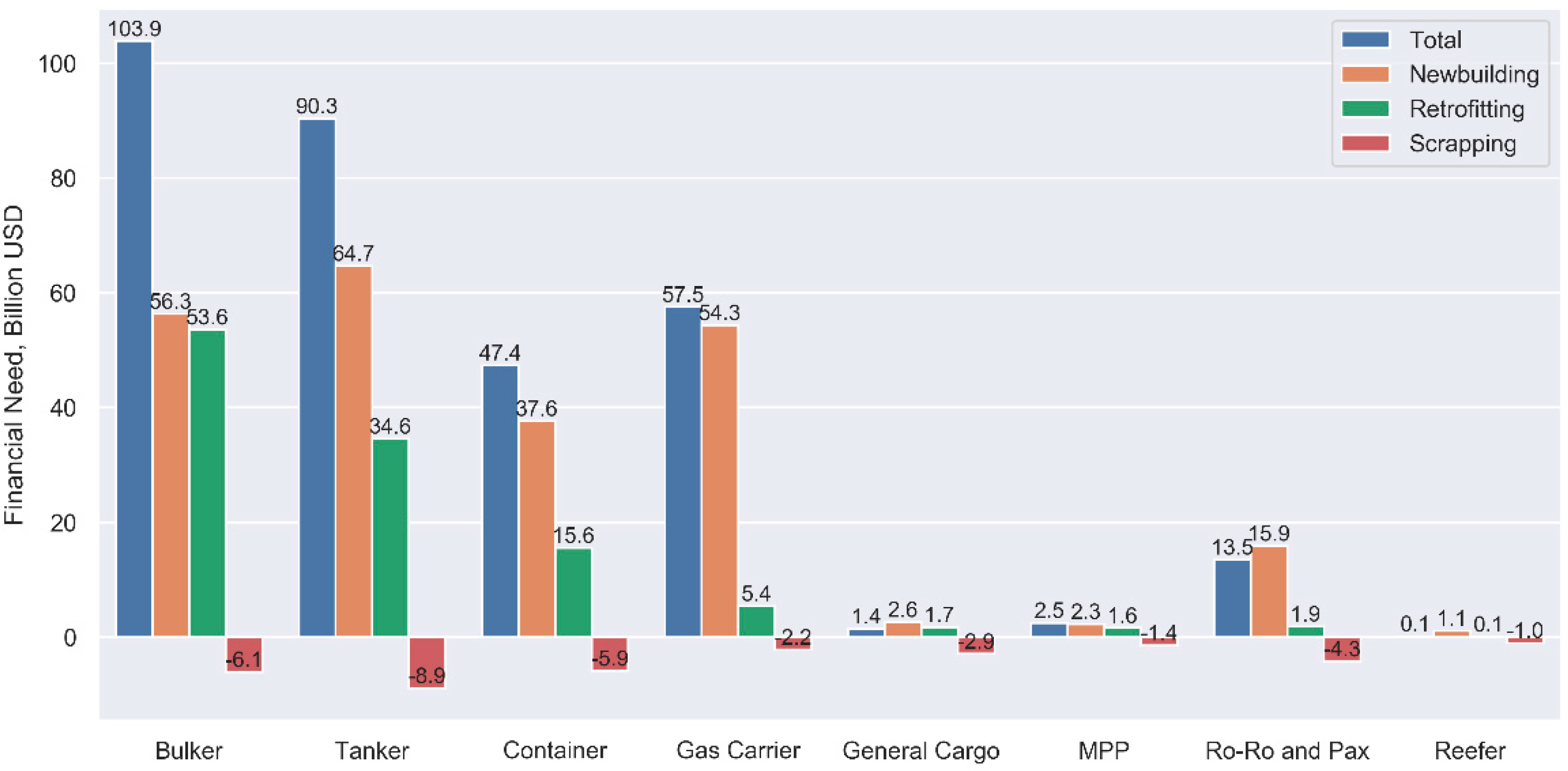

Figure 13, breaking down the total model estimate of the financial need into its subcomponents.

Until 2026, the aggregate financial need is estimated at USD 317 billion, which arises from building new ships and retrofitting existing vessels minus the income generated through demolition. Thereof, the largest share of USD 235 billion is allocated to building new ships, while the estimated costs of retrofitting amount to USD 114 billion. The income generated through vessel demolition sales is estimated at USD 33 billion.

Given the base case parameters, the need for capital per year therefore equals USD 63 billion until 2026. In total, the upper as well as lower bound estimates imply a financial need of USD 247 billion and USD 388 billion, respectively. To put these figures into a maritime business context, one may consider the total commercial value of the world fleet, estimated at USD 952 billion in 2020 [

5]. Thus, the projected aggregate financial need for capital (USD 317 billion) represents roughly 33% of the respective world fleet value.

Figure 14 disaggregates the total financial need by newbuilding, retrofitting, and scrapping for each vessel type.

Accordingly, the largest share of the financial burden relates to bulk carriers, tankers, and container ships, as well as gas carriers. For the gas carrier segment, the capital need is primarily attributed to newbuilding, driven by full orderbooks and high segment growth expectations as well as high overall asset values. The same holds true for the Ro-Ro and passenger segment.

As defined, the income generated through vessel demolition reduces the overall financial burden. Yet, the magnitude of this effect is relatively insignificant compared to the overall financial dimensions. On the level of single vessel types, though, the respective impact can be proportionally bigger. This includes clusters with higher relative age profiles such as general cargo ships, which are scrapped more frequently according to the model definition.

Moreover, the modelling results can be further broken down up to the level of single age brackets per vessel type (see

Appendix A). Additionally, the full breakdown provided in

Appendix A differentiates vessels below and above 30 k deadweight as a proxy for short-sea shipping. Given the most recent policy dynamics in regulating maritime emissions, this perspective may be of political interest, as predominantly short-sea shipping may be affected by the EU ETS in the future. Unsatisfied with the regulatory progress within the IMO, the European Parliament envisions an extension of the EU ETS scope to include shipping in the carbon trading scheme [

80].

5.2. Analysis Results Versus the Supply of Capital

Finally, the absolute estimates provided above do not yet answer the question of whether the maritime financial markets can satisfy the inherent need for capital. Thus, the following section discusses the results in relation to the current international ship finance environment.

Considering the central role of debt financing and especially syndicated loans for ship finance, the absolute need for capital may further be translated into the required contributions of lenders. Based on the loan-to-value (LTV) conditions prevalent in the market, the implied debt requirements can be derived [

81]. Commonly, newbuilding projects are financed with higher LTV ratios than observable for retrofit initiatives. On aggregate, a large portion of shipping loans is provided at LTV ratios between 60% and 80% [

82].

Of the total projected need for capital (USD 317 billion), USD 235 billion have been associated with newbuilding projects and USD 114 billion with retrofit investments. Given that the proceeds from scrapping vessels (USD 33 billion) are split proportionately to finance respective newbuilding or retrofit projects across the fleet, this results in the reduced financial need for debt capital, shown in

Table 10 below.

The absolute amounts and value ranges shown in

Table 10 imply debt requirements per year between USD 36 billion and 45 billion until 2026. As a reference point for the total industry credit exposure, the top 40 shipping lenders accumulated a total exposure of USD 294 billion towards shipping in 2019 [

6]. Thus, the total predicted financial need until 2026 under base case assumptions (USD 317 billion) exceeds the aggregate loan portfolio of these banks by roughly USD 22 billion, whereas the specific requirements for debt shown in

Table 10 fall below this indicative benchmark. Overall, this illustrates the magnitude of the financial challenge. Yet, a more meaningful conclusion can be drawn from analyzing dynamic flows of capital.

Kavussanos and Visvikis [

83] as well as Schinas [

52] provide an overview of the fresh capital provided to shipping annually over time. Since 2010, the total capital inflow (incl. private equity, bank debt, public equity, and bonds but excl. bilateral loans) per year can be observed at approximately USD 80 billion on average. More recent data regarding the volume of syndicated loans towards maritime industries further specifies the allocation of debt towards shipping companies (see

Table 11).

Leaving aside additional sources of funding, two preliminary conclusions can be drawn by comparing the analysis results with the high-level indicators regarding the availability of maritime capital. First, the results indicated that the underlying financial burden of decarbonizing the fleet is substantial. While this finding alone appears trivial, quantifying these efforts has proven more complex. Secondly, despite the substantial financial burden, it can be concluded that the estimated financial need is within reach of historically observable levels of capital endowment.

Therefore, this supports the overall notion that decarbonizing the fleet bears significant financial challenges which in turn do not appear irresolvable, given its estimated financial dimension. In this regard, any potential financial gap apparently widens once predictions closer to the upper bound modelling results materialize. Likewise, the results are subject to the short-term development of the supply of capital towards shipping.

5.3. Sensitivity Analysis

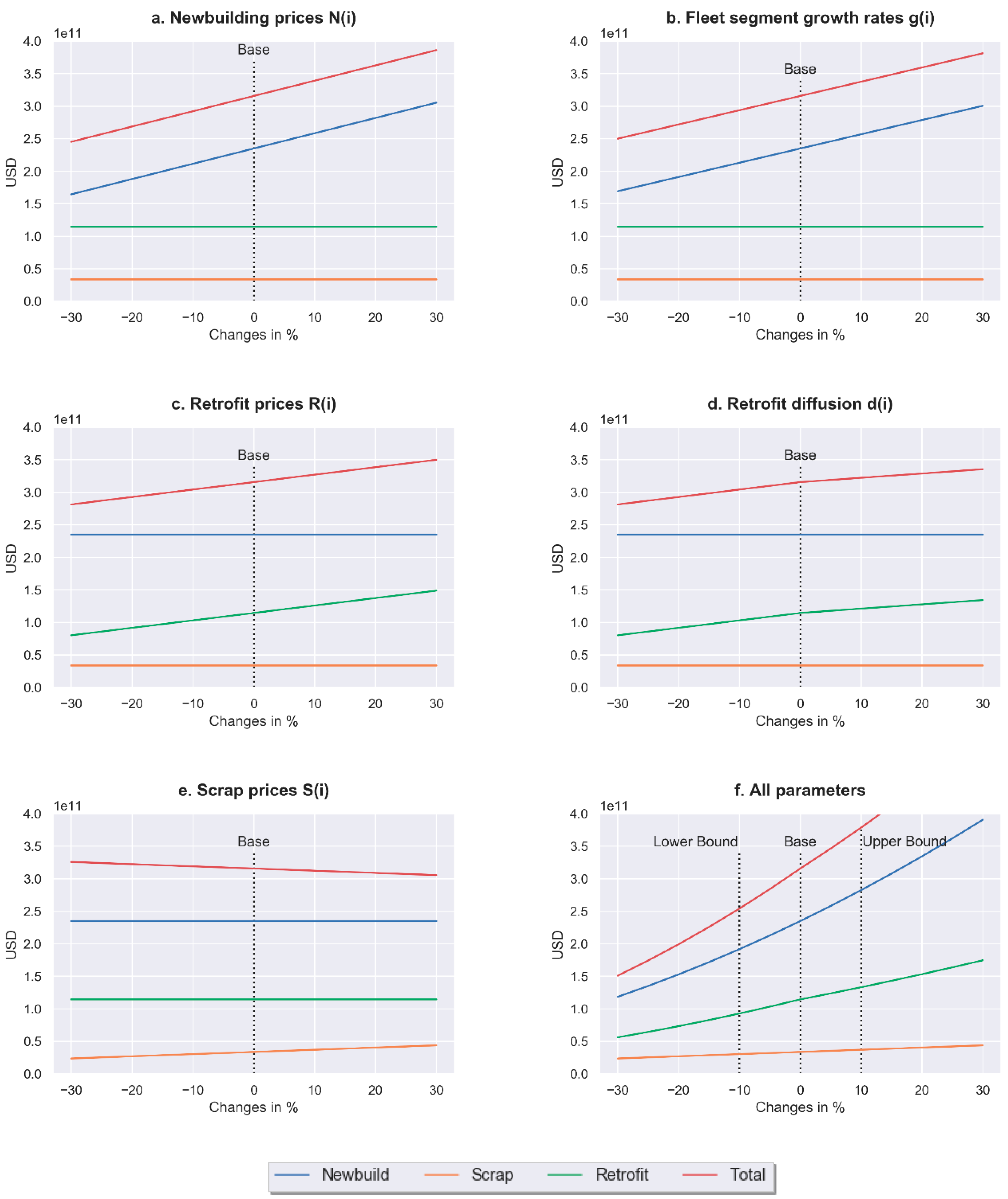

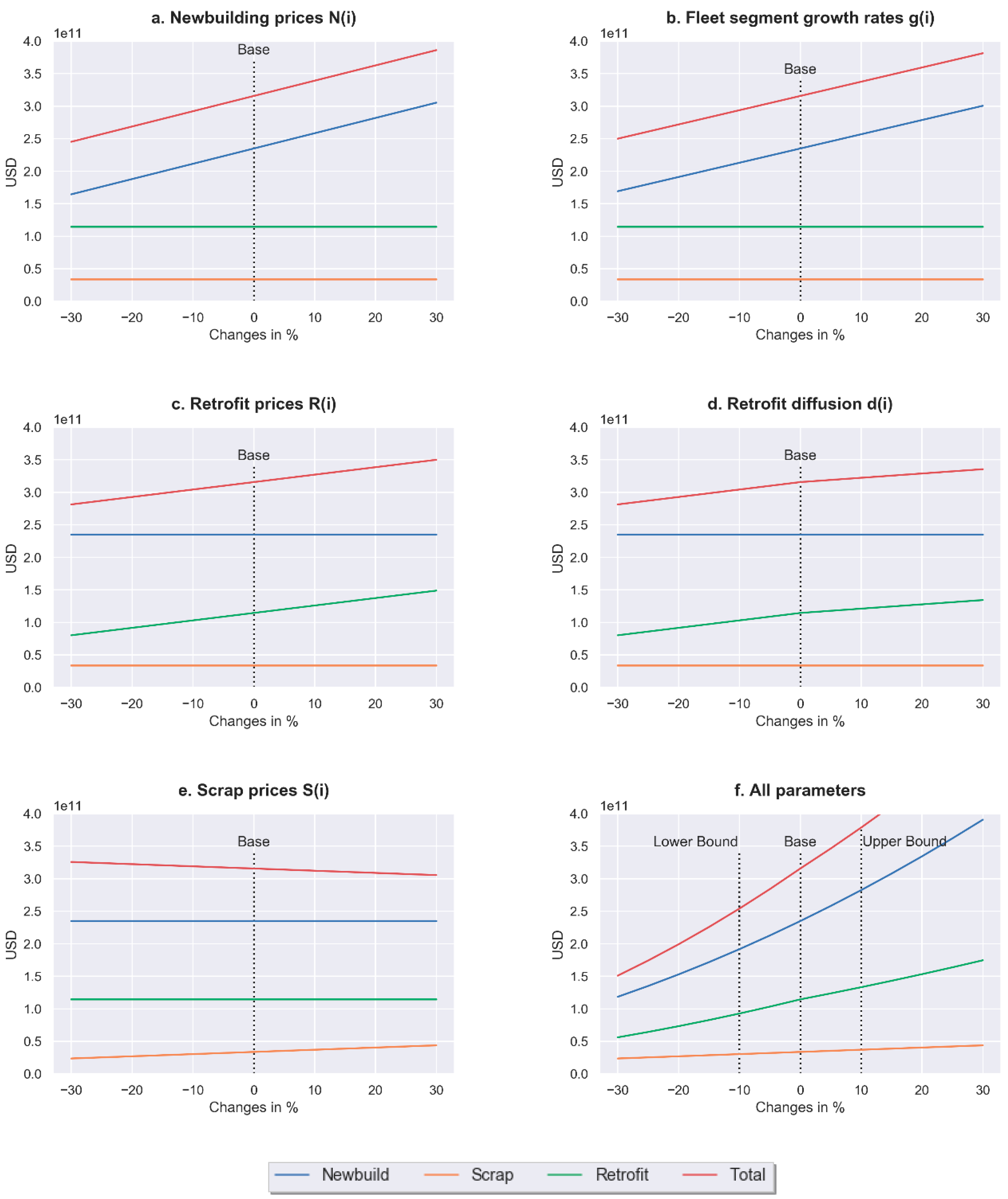

While the range of the different scenario model results already provides an overview of the fundamental model dynamics (see

Figure 13), the sensitivity towards changing parameters shall be reviewed more systematically. The subplots provided in

Figure 15 below document the impact of symmetric deviations from the base case settings.

More precisely, clusters of variables (e.g., newbuilding prices in ) were modified simultaneously as relative variations from the base case, while the other variables remained constant.

On aggregate, the sensitivity towards changes was highest for variations in the newbuilding components, i.e., price levels and fleet segment growth. Apparently, changes in both clusters of variables have the same impact on the model outcome, since they affect the same model equations (

Figure 15a,b). Given the fact that newbuilding initially accounts for a larger share of the total output compared with retrofitting, the respective leverage is naturally higher. However, the relative impact of increasing newbuilding price levels is also higher compared with equivalent changes in the retrofit price levels (

Figure 15a,c). This is further documented in

Table 12 below, providing numerical evidence of the sensitivity towards changes by ten percent for each of the variable clusters.

6. Conclusions, Limitations and Policy Implications

Decarbonizing maritime transport constitutes a key priority to international shipping. The corresponding emission targets are set by the IMO, and policy instruments designed to achieve these targets are continuously evolving, as described. At the same time, the financial implications of the implied decarbonization pathways are rarely analyzed in the literature. Among the very limited available estimates which quantify costs of compliance, methodologies and outcomes diverge significantly.

In order to address this gap in the literature, this paper approximated the short-term cost implications of maritime decarbonization. Methodologically, we follow a bottom-to-top approach considered in the literature for similar estimation problems. More precisely, we developed a vessel-based model which distinguishes financial effects caused by vessel newbuilding, retrofit investments, and vessel demolition sales for the years 2021 to 2026. Further, the model computes relevant financial implications on the level of vessel types and age brackets, up to the level of single vessels. Therefore, besides the absolute financial dimension, the paper contributed towards understanding the distribution of the financial burden towards different segments of the world fleet.

The results indicated a total financial need of USD 317 billion for decarbonizing the global fleet until 2026, given the specified base case conditions. Per year, these figures imply a need for capital of USD 63 billion to build new ships and retrofit existing vessels, less the income generated through demolition sales. Based on prevalent loan-to-value conditions, this translates to yearly debt requirements between USD 36 billion and USD 45 billion.

Based on a brief review of the current ship finance market environment and the available funding opportunities, two partial conclusions were derived. First, in absolute terms, the estimated financial need is substantial, representing a material challenge for maritime businesses. This notion is further reinforced by the ongoing contraction of shipping loan portfolios overall. At the same time, the financial burden may be regarded as moderate on an industry-level for two main reasons. On the one hand, the estimated financial need is within reach of historically observable levels of capital financing, as explored especially for debt capital. On the other hand, the provided estimates appear as moderate in comparison with other available projections.

The provided results contribute to the literature as they add another methodological perspective, since especially retrofit considerations have been underrepresented in the very few similar analyses available. Among other methodological differences, the results can be regarded as of high practical value for the ongoing discourse on maritime decarbonization, considering the short-term analysis period as well as the model design which builds upon the currently observable world fleet structures and newbuilding orderbook.

Several limitations of the study should be considered. One core challenge of the analysis relies on the heterogeneity of the fleet itself. The methodological approach intended to capture the heterogeneous nature of the fleet via the distinction of vessel types, age brackets, and size profiles. In this regard, deadweight was employed as the central variable throughout the full analysis. Notably, certain dynamics are not directly addressed by the deadweight-based modelling. For instance, these include the finding of Ross and Schinas, who documented that superior energy performance is more frequent in vessels of higher commercial value relative to its market share in deadweight [

22]. This may be regarded as a proxy for similar phenomena which are not directly embodied in the deadweight-based approach.

In general, the validity of the input parameters was closely monitored and further validated with complimentary panel data for both newbuilding and vessel demolition components. Thus, the risk of biased model input parameters was reduced to a minimum, but can hardly be eliminated entirely, especially for vessel types which exhibit stronger intra-class heterogeneity.

Among the limitations which result from the methodological set-up, time plays an important role. This relates to both the time horizon of the analysis as well as the end-of-life assumption for all vessels in the modelling. The analysis period of five years from 2021 until 2026 was chosen deliberately for two main reasons. First, the time horizon can be adequately anticipated through the 2020 orderbook and is simultaneously long enough for sufficient fleet renewal to occur. Secondly, a period of 5 years appears feasible to practically understand the short- to mid-term financial impact, as opposed to more long-term considerations spanning several decades.

The second time-related question evolves around the age bin structure, which directly implies the presumed end of life for all vessels. While the notion behind the end of life for vessels at 22 years was introduced in prior sections, it must be acknowledged that this results in potential upward bias for certain parts of the fleet. This is true for vessel types which do not fully adhere to competitive renewal cycles observable for other segments and thus exhibit comparably old age distributions, as for instance the General Cargo segment.

However, this effect can be regarded as insignificant for the total model outcome. While a considerable number of 15,910 vessels are reported to be older than 30 years in our dataset, they only makes up 1.77% of the world fleet’s deadweight. Therefore, the deadweight-based modelling places little emphasis on this fraction of the fleet. Moreover, even when factoring in the risk of upward bias for this distinct model component, the financial equivalent of vessel demolition only accounts for roughly one tenth of the total model estimate, thereby having a negligible effect on the overall results.

Furthermore, this work offered necessary insights for further policy considerations. As per the findings of

Table 10, the total sum required for a smooth transition, circa USD 300–350 billion, equals the total available lending capacity reported. More aggressive decarbonization policies will result in higher scarcity of capital. Therefore, the demand and supply of ship finance capital will be distorted, and the higher cost of capital should be expected. Should this be the case, then only some projects, mainly the riskier ones that yield higher returns, will be selected. Consequently, a lack of funding for segments with relatively lower yields such as of coastal shipping will occur, despite their critical importance in decarbonizing transportation networks. This aspect is critical when considering the European effort to shift cargoes from land to sea, a policy with an inherent green objective and other benefits to society. Other regional policies might also be affected, such as the swift change of the fuel mix used by ships or the air quality at ports. Regardless of the fuel or technology selected, current and new ships will demand higher investment vis-a-vis ships of current conventional technology or financial benefits when calling ports that eventually impact the financial performance of the ports. Therefore, policy makers should also acknowledge the limitations of the financial markets, otherwise carbon leakage might take place.

Finally, the findings of this work support further research and contributed to addressing relevant gaps. Indicatively and not exhaustively, one can estimate the size of the market of retrofit, so technology providers and investors can support estimations and decisions. Moreover, the statistical analysis and findings, such as the average price in USD/DWT for demolition, etc., can provide input in relevant estimations and models. In this regard, the use of a fleet breakdown previously considered in the literature enables comparisons and projections among studies and reports, and benchmarks are provided for further research and analysis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}