Sustainable Construction and Financing—Asset-Backed Securitization of Expressway’s Usufruct with Redeemable Rights

Abstract

:1. Introduction

2. Literature Review of Asset-Backed Securitization Product Pricing

3. Issuance Scale and Coupon Rate Pricing of Redeemable ABN

3.1. The Issuance Steps of a Redeemable ABN

3.2. NS Model and SV Model

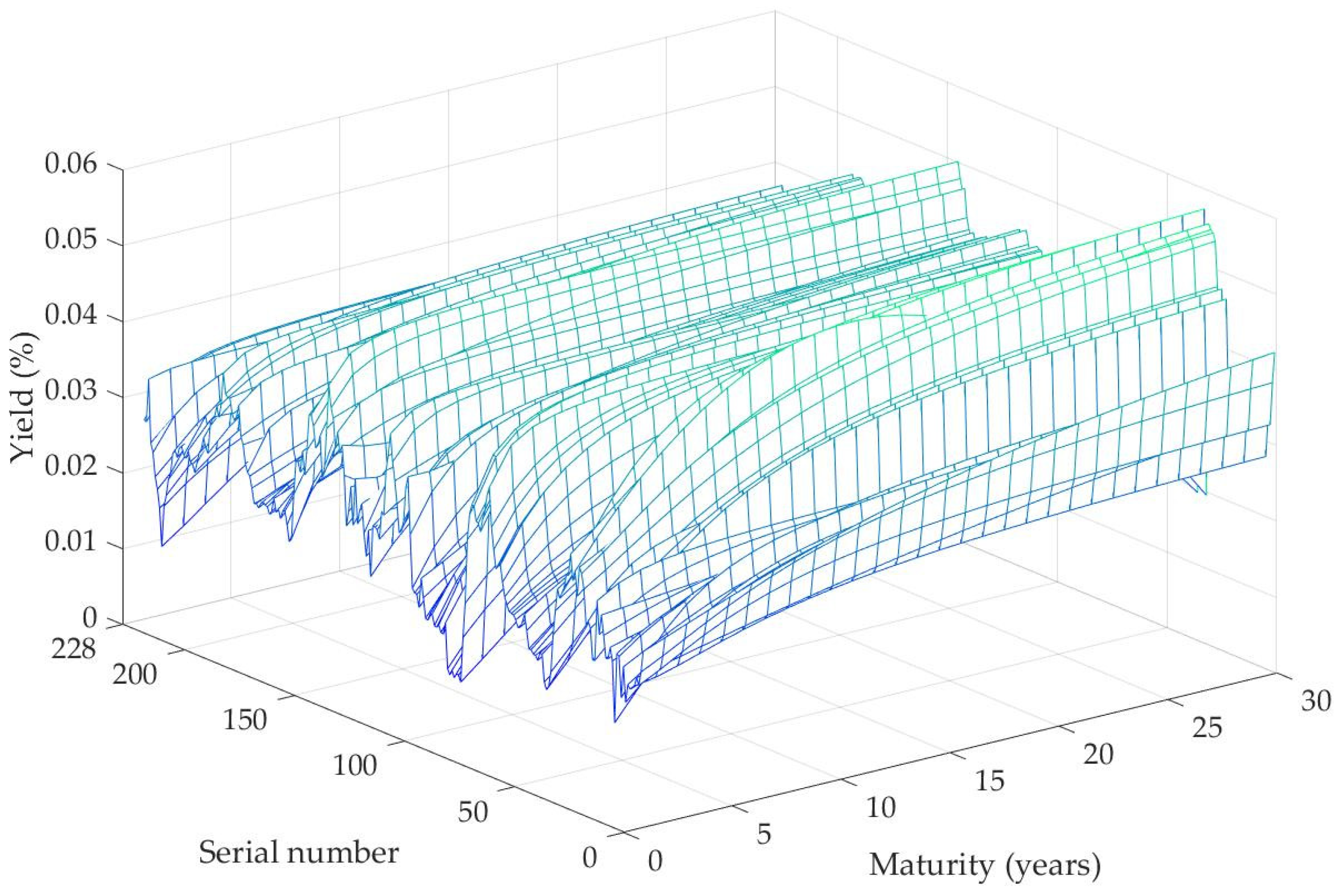

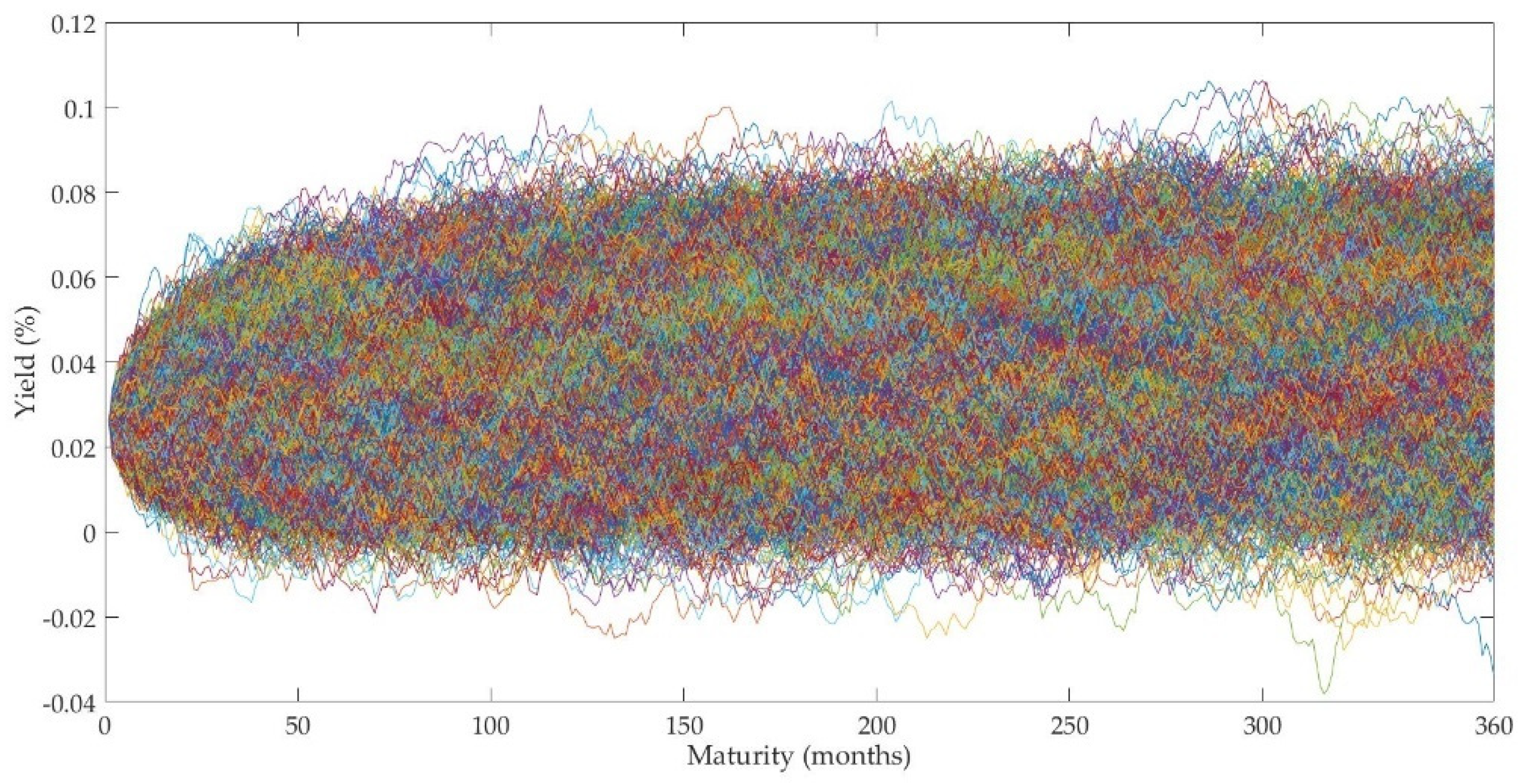

3.3. Two-Factor Vasicek Model and Kalman Filter Method

4. Empirical Simulation Analysis

4.1. Basic Conditions and Assumptions of the Project

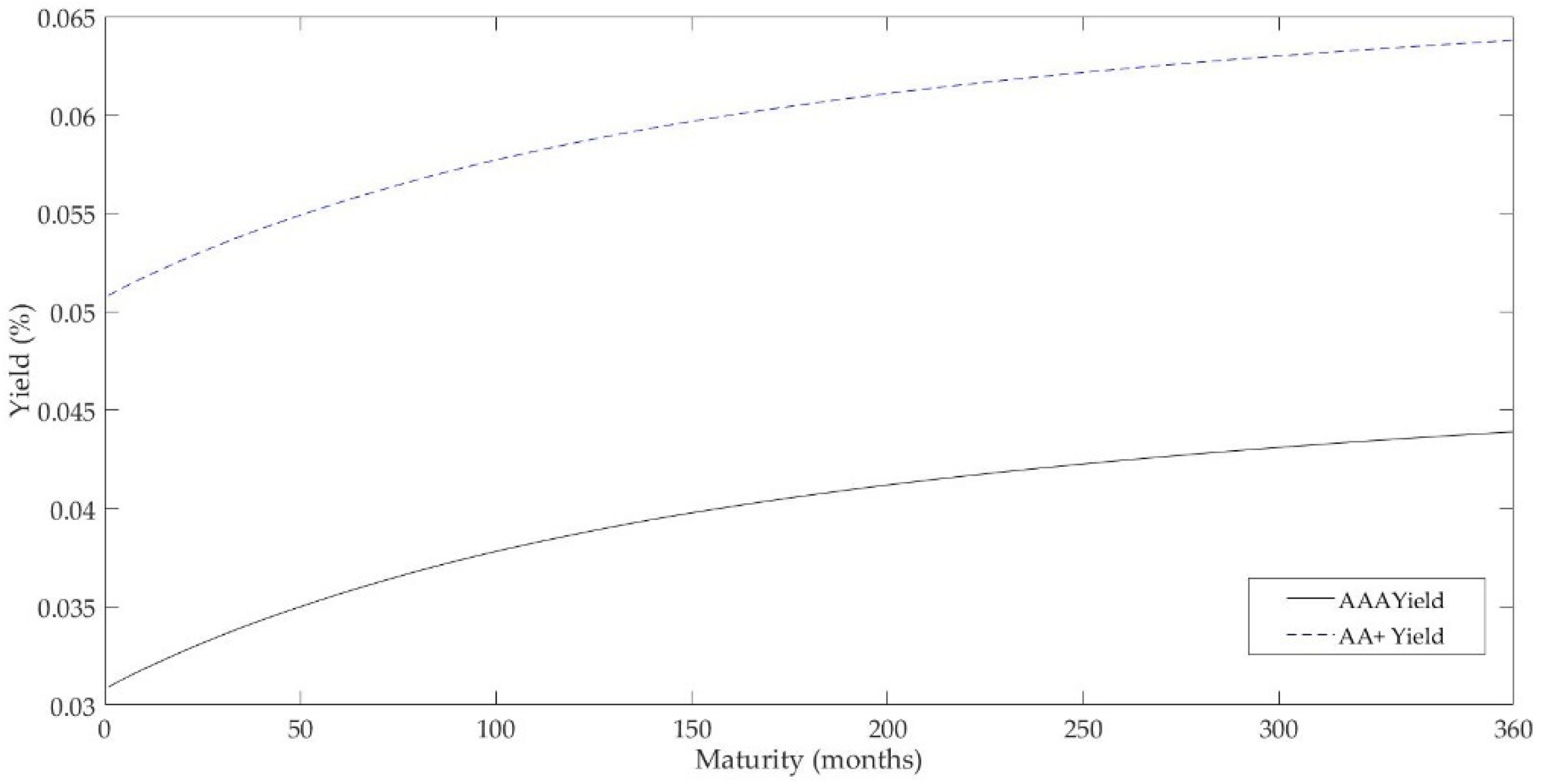

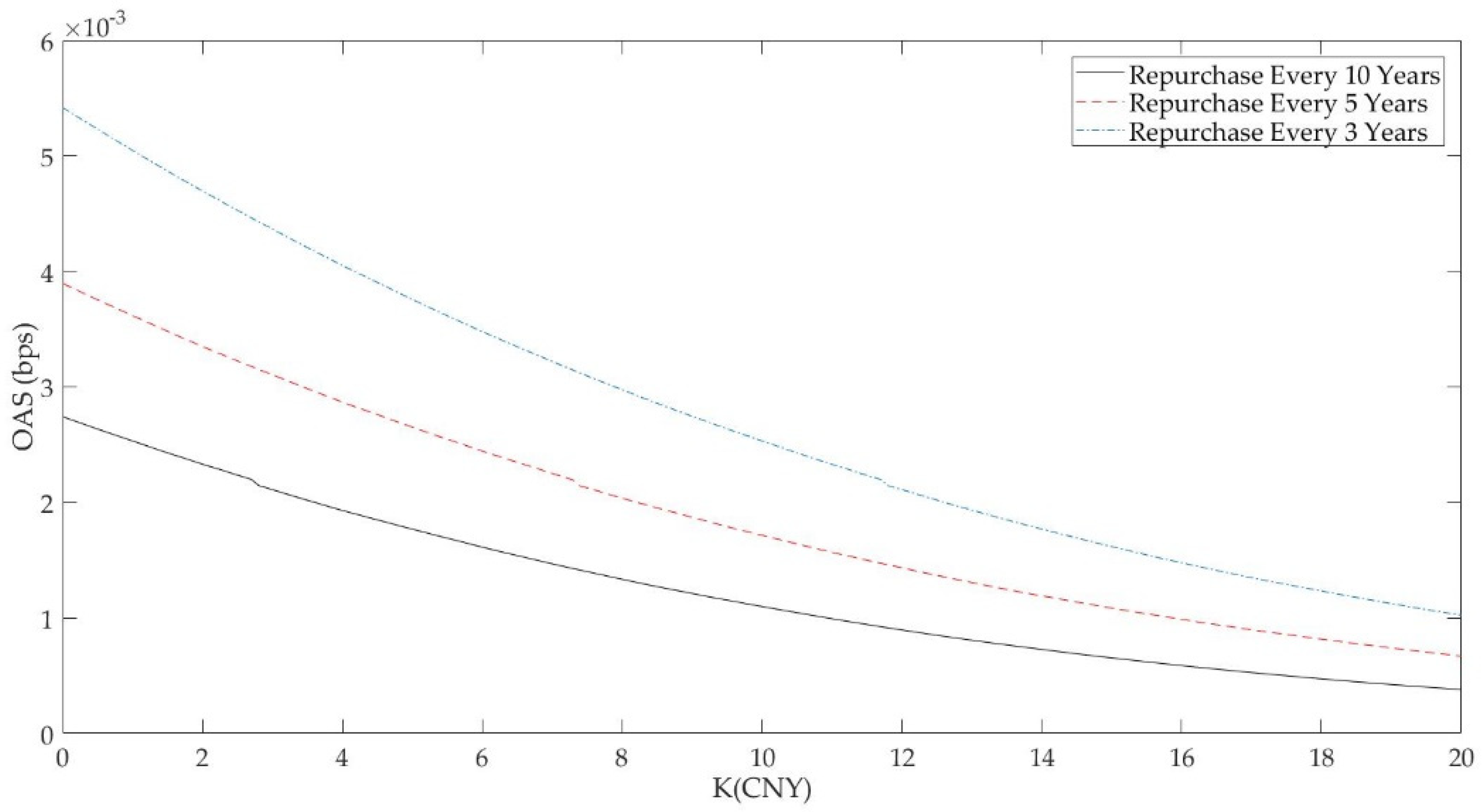

4.2. Redeemable ABN Pricing

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, D.; Li, Z.; Zhao, Z.; Zhao, X.B. Urban Infrastructure Financing in Reform-era China. Urban Stud. 2011, 48, 2975–2998. [Google Scholar] [CrossRef]

- Pan, F.; Zhang, F.; Zhu, S.; Wojcik, D. Developing by borrowing? Inter-jurisdictional competition, land finance and local debt accumulation in China. Urban Stud. 2017, 54, 897–916. [Google Scholar] [CrossRef]

- Filipović, D.; Willems, S. A term structure model for dividends and interest rates. Math. Financ. 2020, 30, 1461–1496. [Google Scholar] [CrossRef]

- Sheraz, M.; Preda, V.; Dedu, S. Non-extensive minimal entropy martingale measures and semi-Markov regime switching interest rate modeling. Aims Math. 2020, 5, 300–310. [Google Scholar] [CrossRef]

- Rojo-Suárez, J.; Alonso-Conde, A.B. Relative Entropy and Minimum-Variance Pricing Kernel in Asset Pricing Model Evaluation. Entropy. 2020, 22, 721. [Google Scholar] [CrossRef] [PubMed]

- Liao, Z.; Zhang, H.; Guo, K.; Wu, N. A Network Approach to the Study of the Dynamics of Risk Spillover in China’s Bond Market. Entropy. 2021, 23, 920. [Google Scholar] [CrossRef] [PubMed]

- Dunsky, R.M.; Ho, T.S. Valuing Fixed Rate Mortgage Loans with Default and Prepayment Options. J. Fixed Income 2007, 16, 7–31. [Google Scholar] [CrossRef]

- Jacob, D.P.; Hong, T.C.H.; Lee, L.H. An Options Approach to Commercial Mortgages and CMBS Valuation and Risk Analysis. The Handbook of Non-agency Mortgage-backed Securities; Wiley: Grafton, NH, USA, 2000; pp. 465–495. [Google Scholar]

- Sharp, N.J.; Newton, D.P.; Duck, P.W. An Improved Fixed-Rate Mortgage Valuation Methodology with Interacting Prepayment and Default Options. J. Real Estate Financ. Econ. 2008, 36, 307–342. [Google Scholar] [CrossRef]

- Liu, Z.Y.; Fan, G.Z.; Lim, K.G. Extreme Events and the Copula Pricing of Commercial Mortgage-Backed Securities. J. Real Estate Financ. Econ. 2009, 38, 327–349. [Google Scholar] [CrossRef]

- Hürlimann, W. Valuation of Fixed and Variable Rate Mortgages: Binomial tree versus analytical approximations. Decis. Econ. Financ. 2012, 35, 171–202. [Google Scholar] [CrossRef]

- Qian, X.S.; Jiang, L.S.; Xu, C.L.; Wu, S. Explicit formulas for pricing of callable mortgage-backed securities in a case of prepayment rate negatively correlated with interest rates. J. Math. Anal. Appl. 2012, 393, 421–433. [Google Scholar] [CrossRef]

- Fan, G.Z.; Sing, T.F.; Ong, S.E. Default Clustering Risks in Commercial Mortgage-Backed Securities. J. Real Estate Financ. Econ. 2012, 45, 110–127. [Google Scholar] [CrossRef]

- Fermanian, J.D. A Top-Down Approach for Asset-Backed-Securities: A Consistent Way of Managing Prepayment, Default and Interest Rate Risks. J. Real Estate Financ. Econ. 2013, 46, 480–515. [Google Scholar] [CrossRef]

- Hayre, L.S. Understanding Option-adjusted Spreads and Their Use. J. Portf. Manag. 1990, 16, 68–69. [Google Scholar] [CrossRef]

- Green, R.K. Chapter 11-The Yield Curve, Monte Carlo Methods, and the Option-Adjusted Spread. In Introduction to Mortgages & Mortgage Backed Securities; Elsevier Inc.: Amsterdam, The Netherlands, 2014. [Google Scholar]

- Dong, J.C.; Liu, J.X.; Wang, C.H.; Yuan, H.; Wang, W.J. Pricing Mortgage-Backed Security: An Empirical Analysis. Syst. Eng.-Theory Pract. Online 2009, 29, 46–52. [Google Scholar] [CrossRef]

- Vasicek, O. An Equilibrium Characterization of the Term Structure. J. Financ. Econ. 1977, 5, 627. [Google Scholar] [CrossRef]

- Vázquez-Vázquez, M.; Alonso-Conde, A.B.; Rojo-Suárez, J. Are the Purchase Prices of Solar Energy Projects under Development Consistent with Cost of Capital Forecasts? Infrastructures 2021, 6, 95. [Google Scholar] [CrossRef]

- Falbo, P.; Paris, F.M.; Pelizzari, C. Pricing Inflation Linked Bonds. Quant. Financ. 2010, 10, 279–293. [Google Scholar]

- Longstaff, F.A.; Schwartz, E.S. Valuing American Options by Simulation: A Simple Least Squares Approach. Rev. Financ. Stud. 2001, 14, 113–147. [Google Scholar] [CrossRef]

- Fabozzi, F.J. Fixed Income Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2007; Volume 6. [Google Scholar]

- Nelson, C.; Siegel, A.F. Parsimonious Modeling of Yield Curves. J. Bus. 1987, 60, 473–489. [Google Scholar] [CrossRef]

- Svensson, L.E. Estimating and Interpreting Forward Interest Rates: Sweden 1992-1994. Natl. Bur. Econ. Res. 1994. [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | ||||||

|---|---|---|---|---|---|---|

| Value | 0.0421 | −0.041834 | 0.113045 | −0.129213 | 1.773025 | 1.887328 |

| Maturity (Years) | 1 | 2 | 3 | 5 | 10 | 20 | 30 |

|---|---|---|---|---|---|---|---|

| Spot Rate (%) | 0.011381 | 0.015799 | 0.019473 | 0.025125 | 0.033514 | 0.036471 | 0.038727 |

| Parameter | |||||||

|---|---|---|---|---|---|---|---|

| Value | 0.0573 | 0.0262 | 0.0163 | 0.2013 | 0.0837 | 0.0464 | 0.0493 |

| Senior A Bonds, Class AAA, Coupon Rate 4.21%, The Issuance Period Is 20 Years | |||||

| Yield Change (%) | Duration | Convexity Change (%) | Price Change (%) | Initial Price | New Price |

| +100 | 13.4450 | −5.4113 | 12.2433 | 100 | 87.7567 |

| +50 | 13.6753 | −2.9661 | −6.3872 | 100 | 93.6128 |

| +10 | 13.8575 | −0.5393 | −1.3224 | 100 | 98.6775 |

| 0 | 13.9027 | 0.0000 | 0.0000 | 100 | 100.0000 |

| −10 | 13.9478 | 0.5394 | 1.3459 | 100 | 101.3459 |

| −50 | 14.1269 | 2.6972 | 6.9730 | 100 | 106.9730 |

| −100 | 14.3474 | 5.3929 | 14.5927 | 100 | 114.5927 |

| Senior B bonds, Class AA+, Coupon Rate 6.38%, The Issuance Period Is 25 Years | |||||

| Yield Change (%) | Duration | Convexity Change (%) | Price Change (%) | Initial Price | New Price |

| +100 | 13.1436 | −10.6206 | −11.9497 | 100 | 88.0503 |

| +50 | 13.5989 | −5.4212 | −6.2801 | 100 | 93.7199 |

| +10 | 13.9720 | −1.1017 | −1.3086 | 100 | 98.6914 |

| 0 | 14.0664 | 0.0000 | 0.0000 | 100 | 100.0000 |

| −10 | 14.1613 | 1.1103 | 1.3362 | 100 | 101.3362 |

| −50 | 14.5451 | 5.6363 | 6.9717 | 100 | 106.9717 |

| −100 | 15.0338 | 11.4788 | 14.7284 | 100 | 114.7284 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Q.; Tjia, L.Y.-n.; Wang, B.; Ersoy, A. Sustainable Construction and Financing—Asset-Backed Securitization of Expressway’s Usufruct with Redeemable Rights. Sustainability 2021, 13, 9113. https://doi.org/10.3390/su13169113

Zhang Q, Tjia LY-n, Wang B, Ersoy A. Sustainable Construction and Financing—Asset-Backed Securitization of Expressway’s Usufruct with Redeemable Rights. Sustainability. 2021; 13(16):9113. https://doi.org/10.3390/su13169113

Chicago/Turabian StyleZhang, Qiming, Linda Yin-nor Tjia, Biyue Wang, and Aksel Ersoy. 2021. "Sustainable Construction and Financing—Asset-Backed Securitization of Expressway’s Usufruct with Redeemable Rights" Sustainability 13, no. 16: 9113. https://doi.org/10.3390/su13169113

APA StyleZhang, Q., Tjia, L. Y.-n., Wang, B., & Ersoy, A. (2021). Sustainable Construction and Financing—Asset-Backed Securitization of Expressway’s Usufruct with Redeemable Rights. Sustainability, 13(16), 9113. https://doi.org/10.3390/su13169113