Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model

Abstract

:1. Introduction

2. Method and Modeling

2.1. Model Structure and General Description

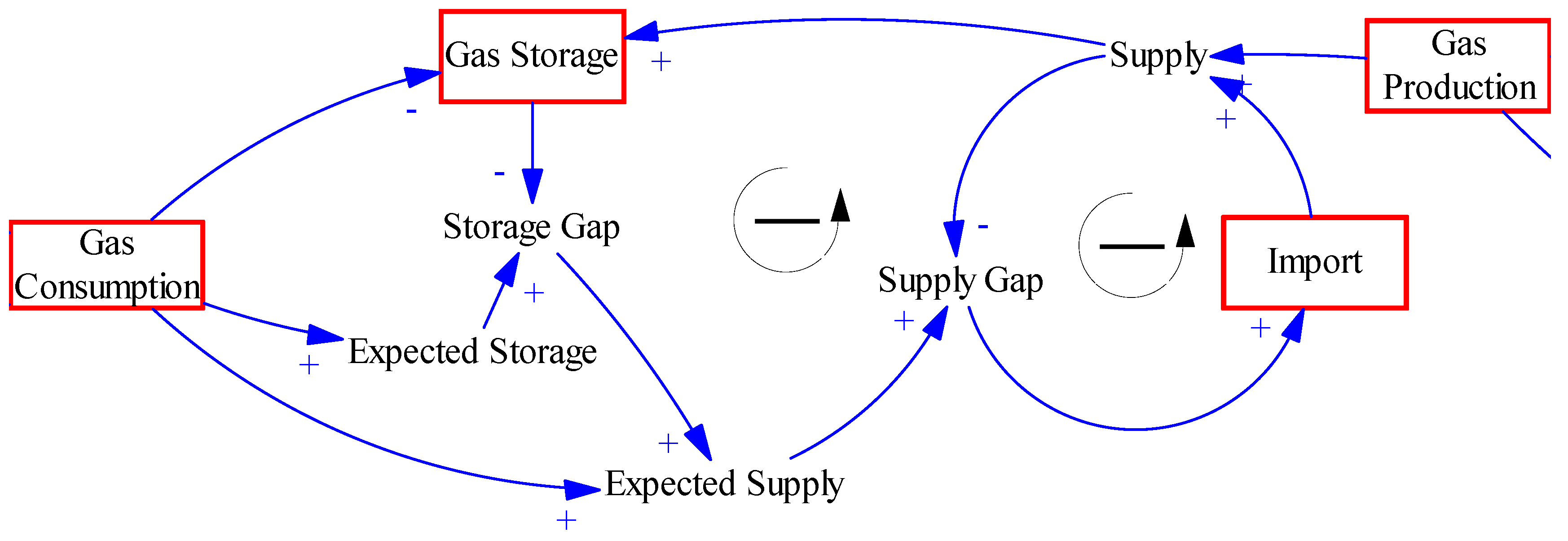

2.1.1. Gas Storage Subsystem

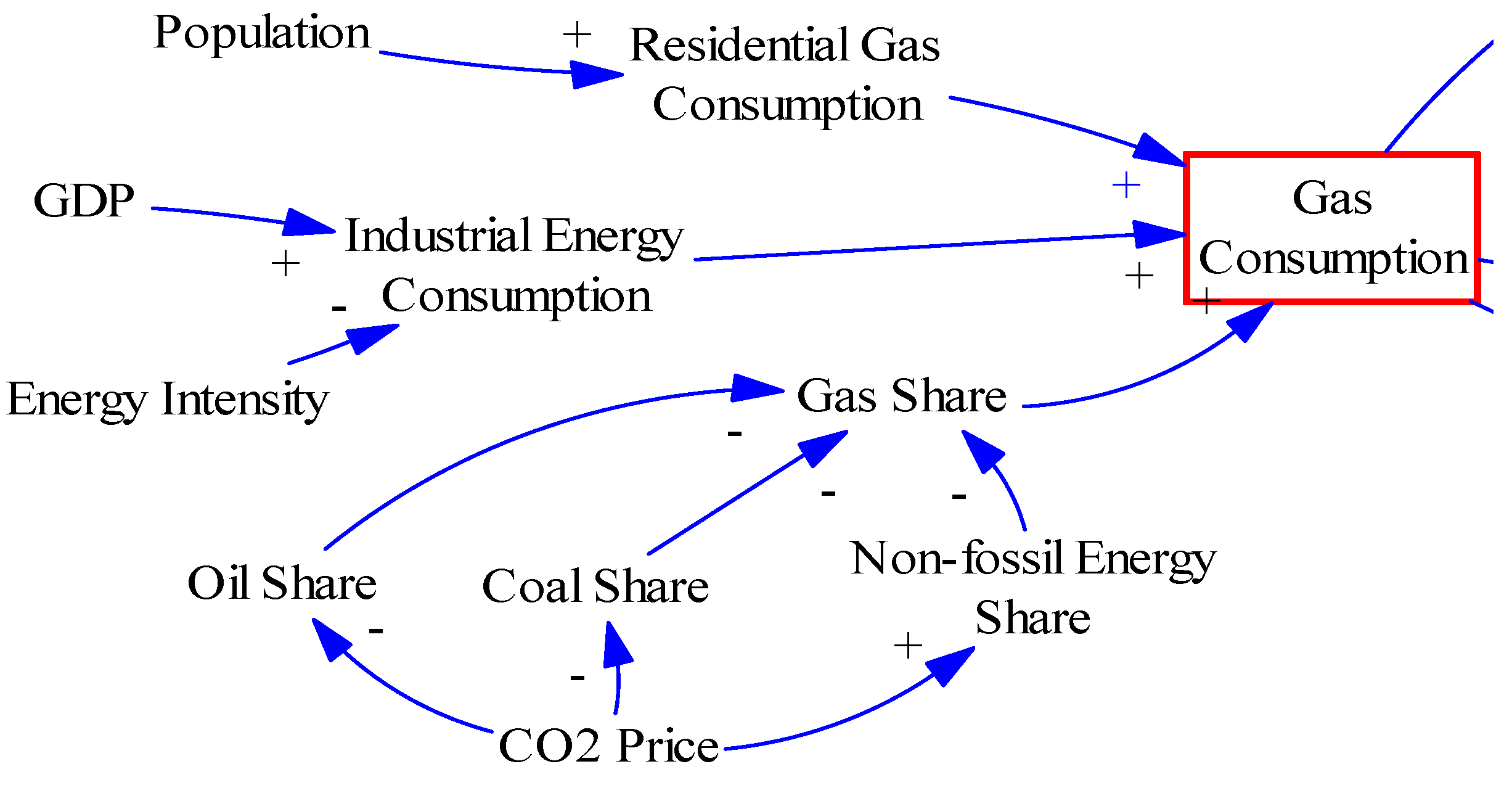

2.1.2. Gas Demand Subsystem

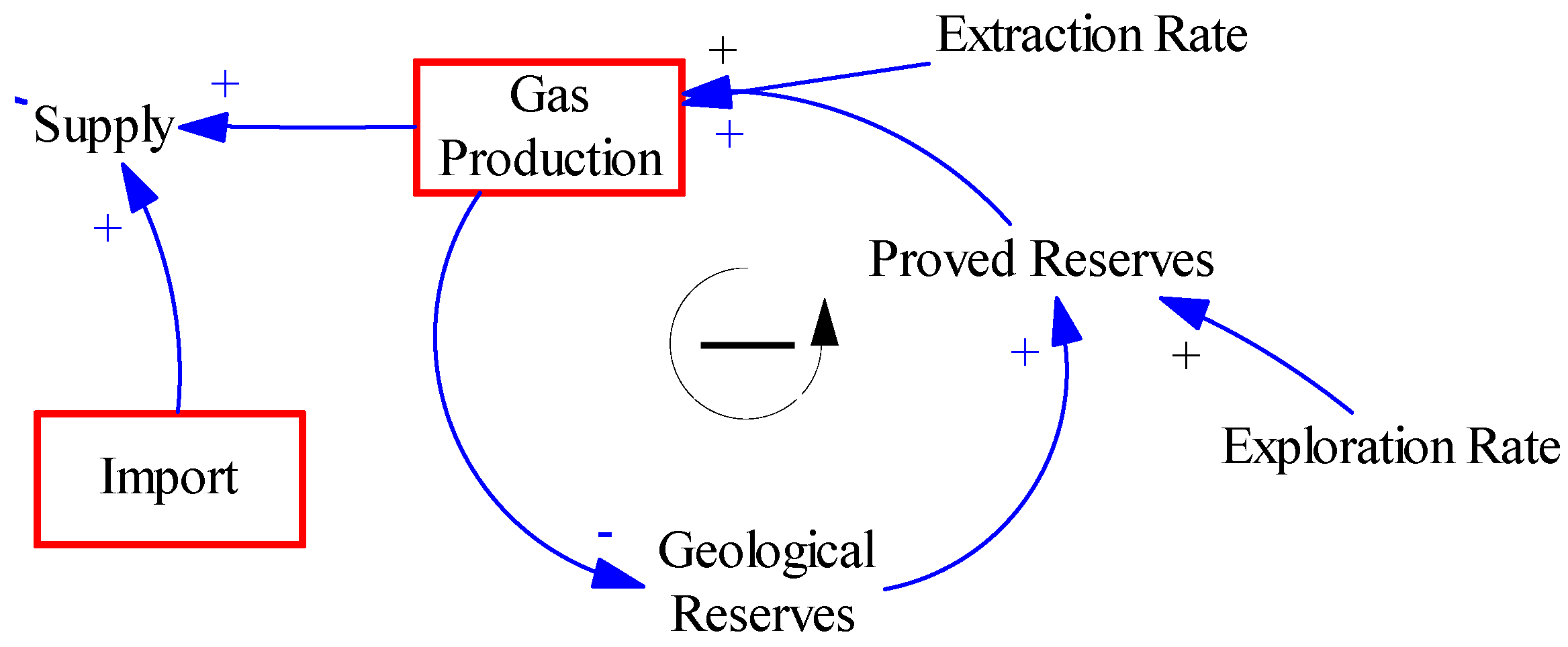

2.1.3. Gas Supply Subsystem

2.2. Model Settings and Assumptions

2.2.1. Assumptions in Storage Subsystem

2.2.2. Assumptions in Demand Subsystem

2.2.3. Assumptions in Supply Subsystem

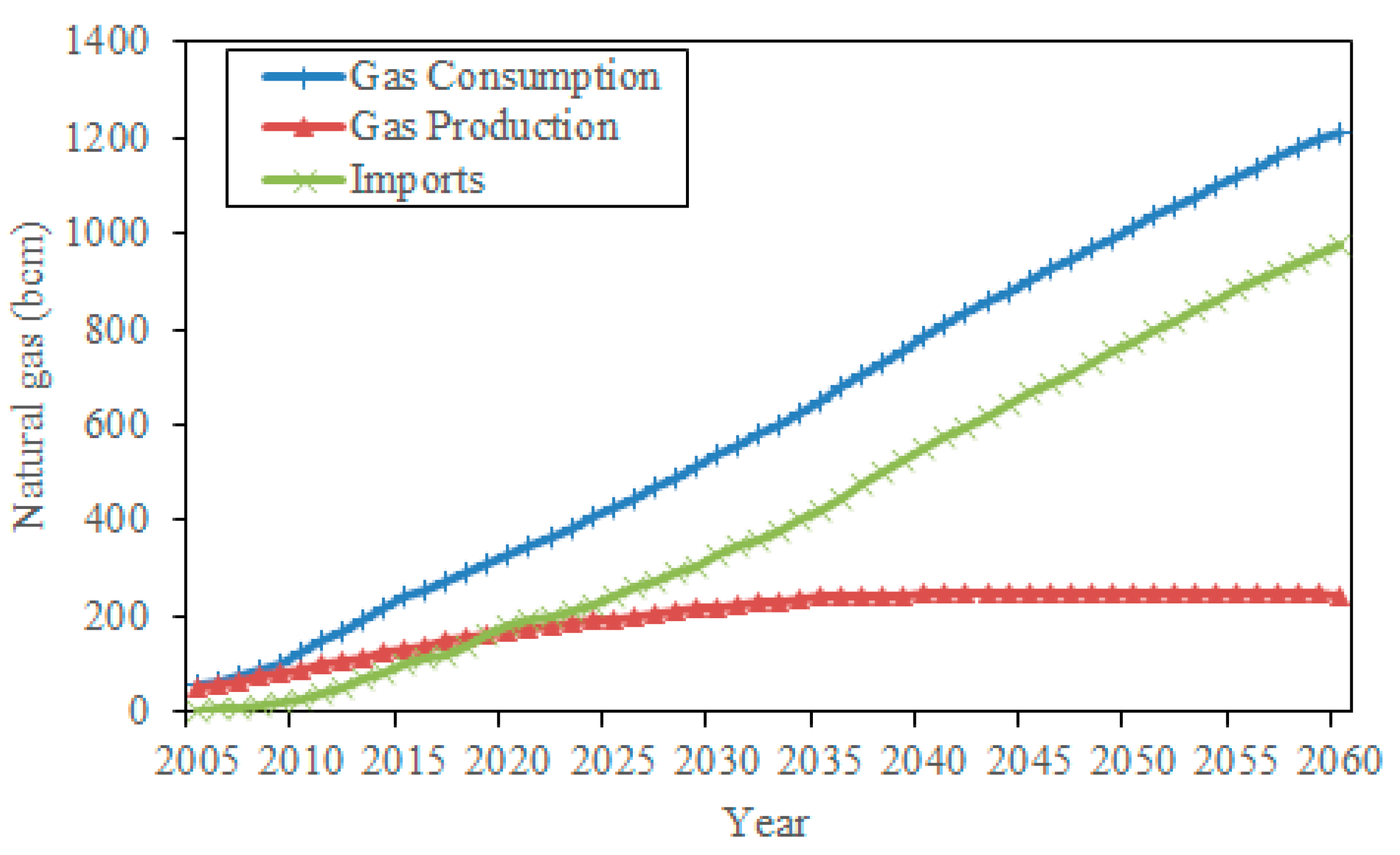

2.3. Validity Check and Simulation Results for the Base Case

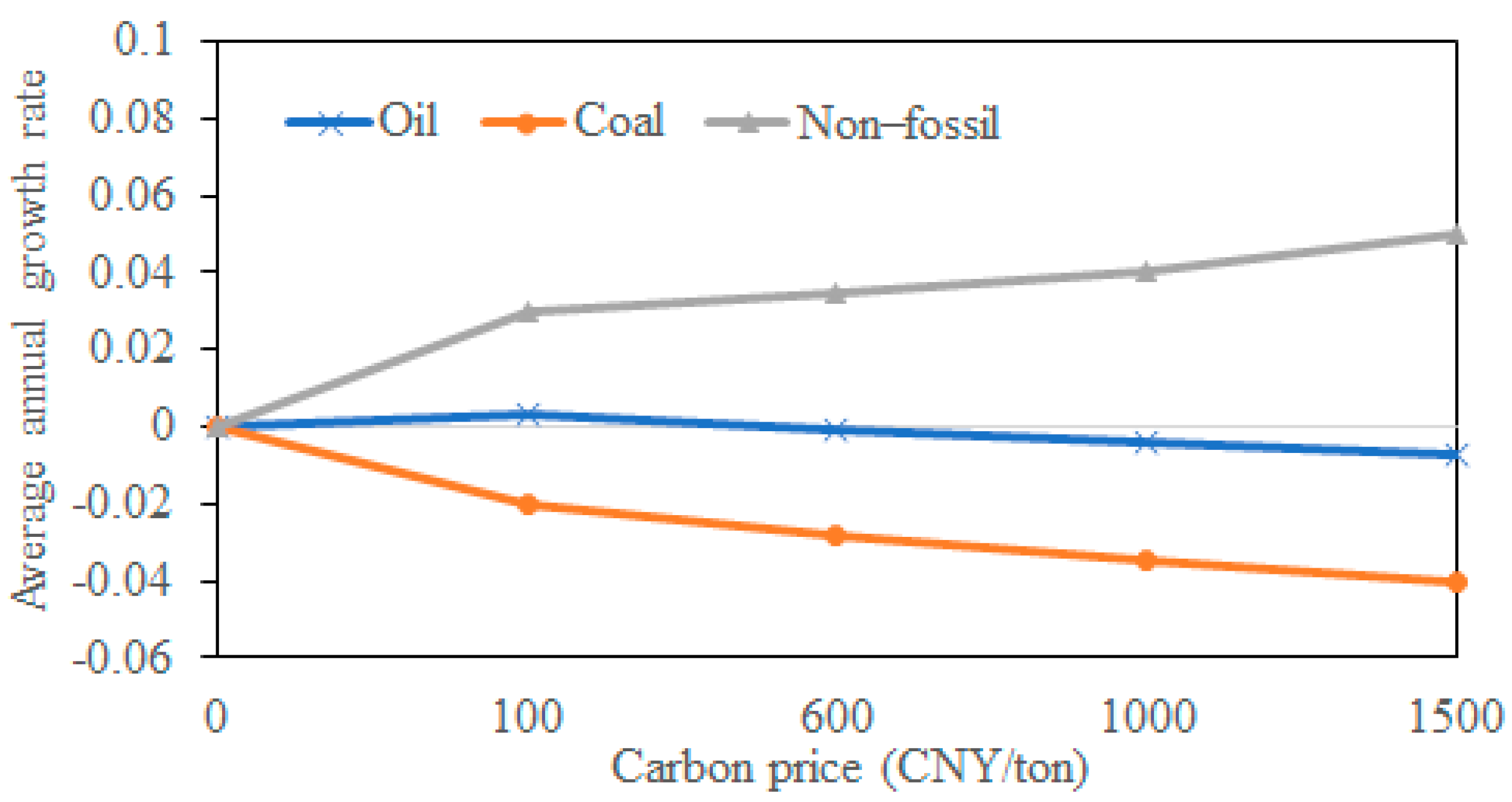

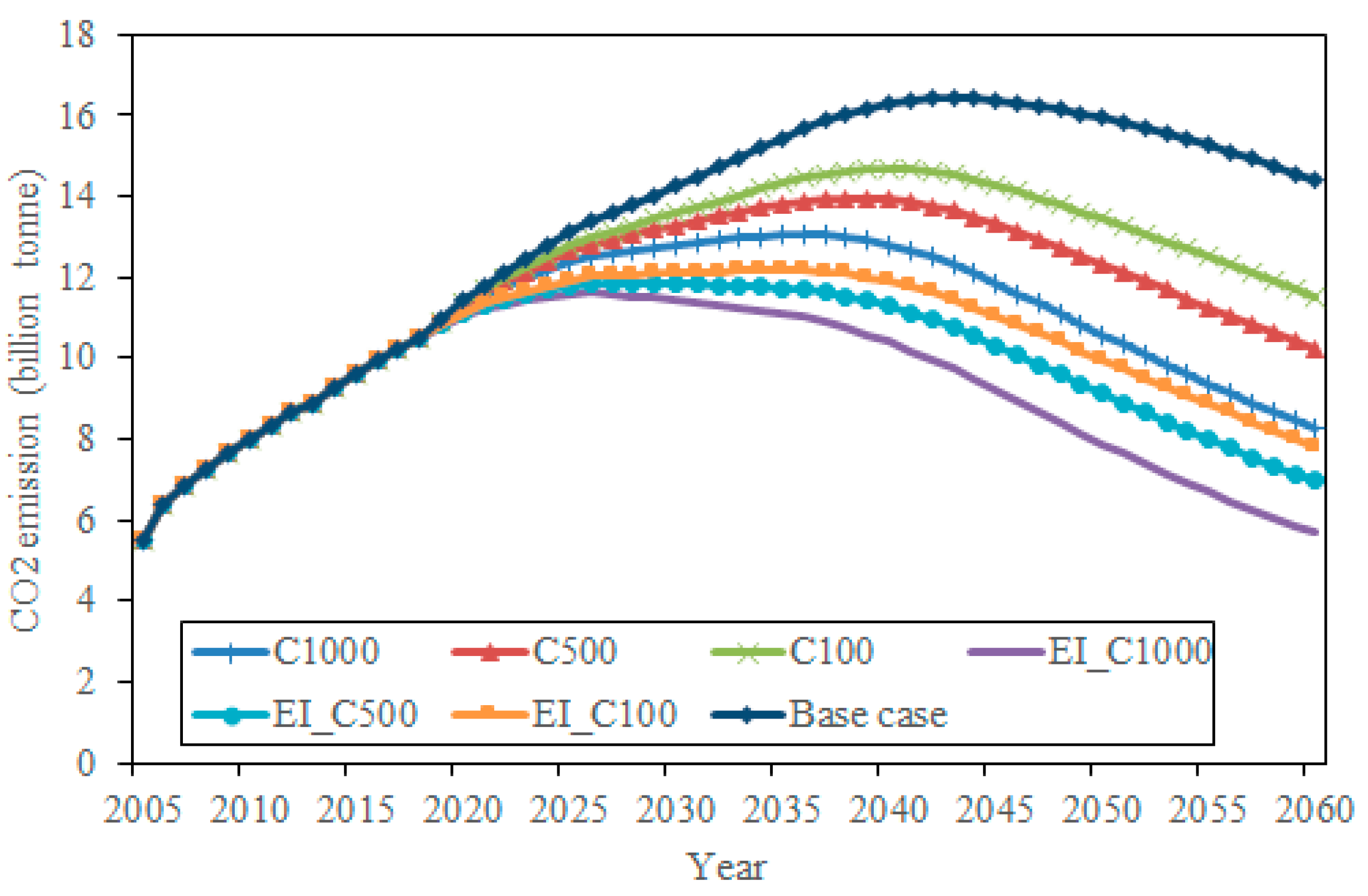

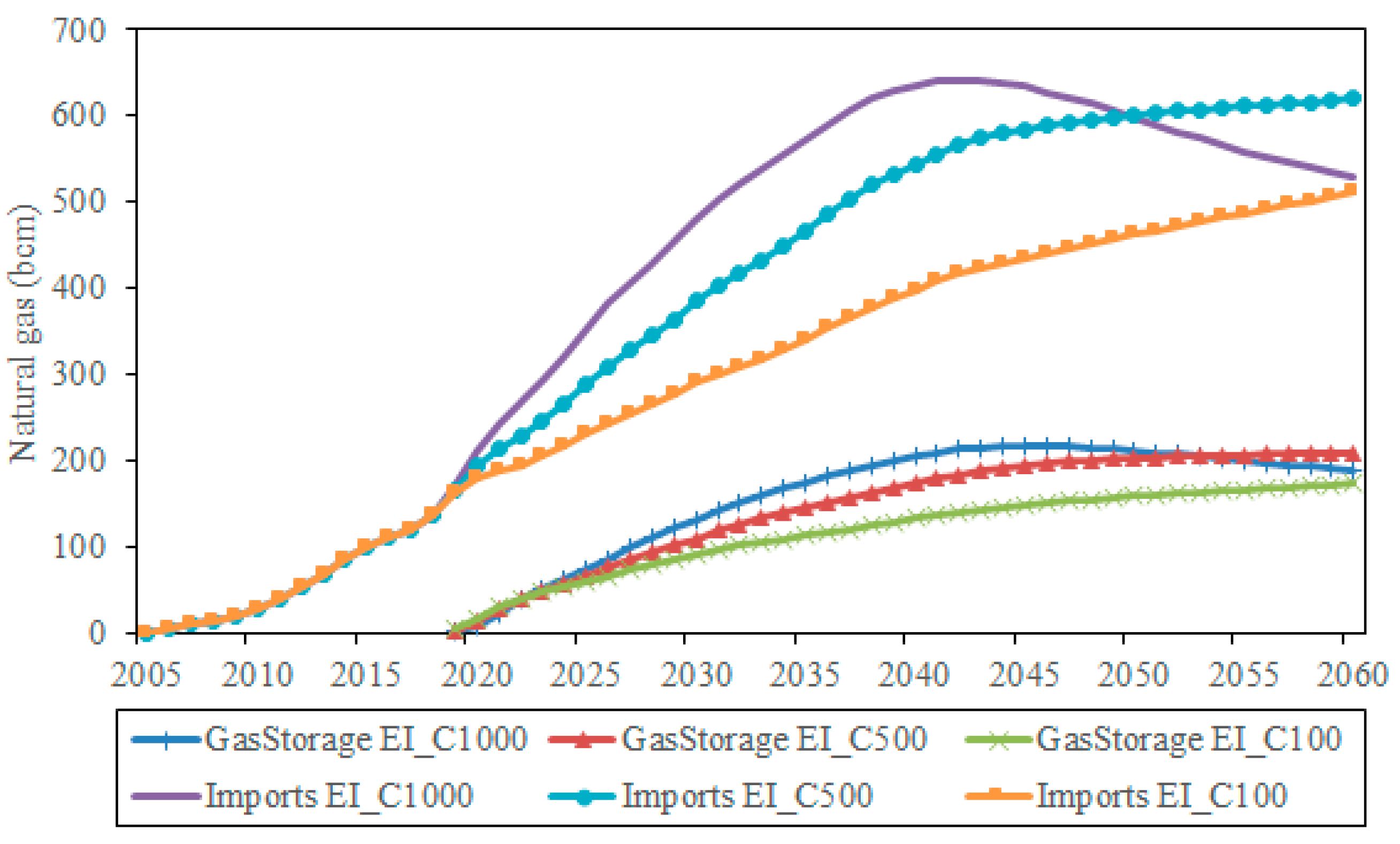

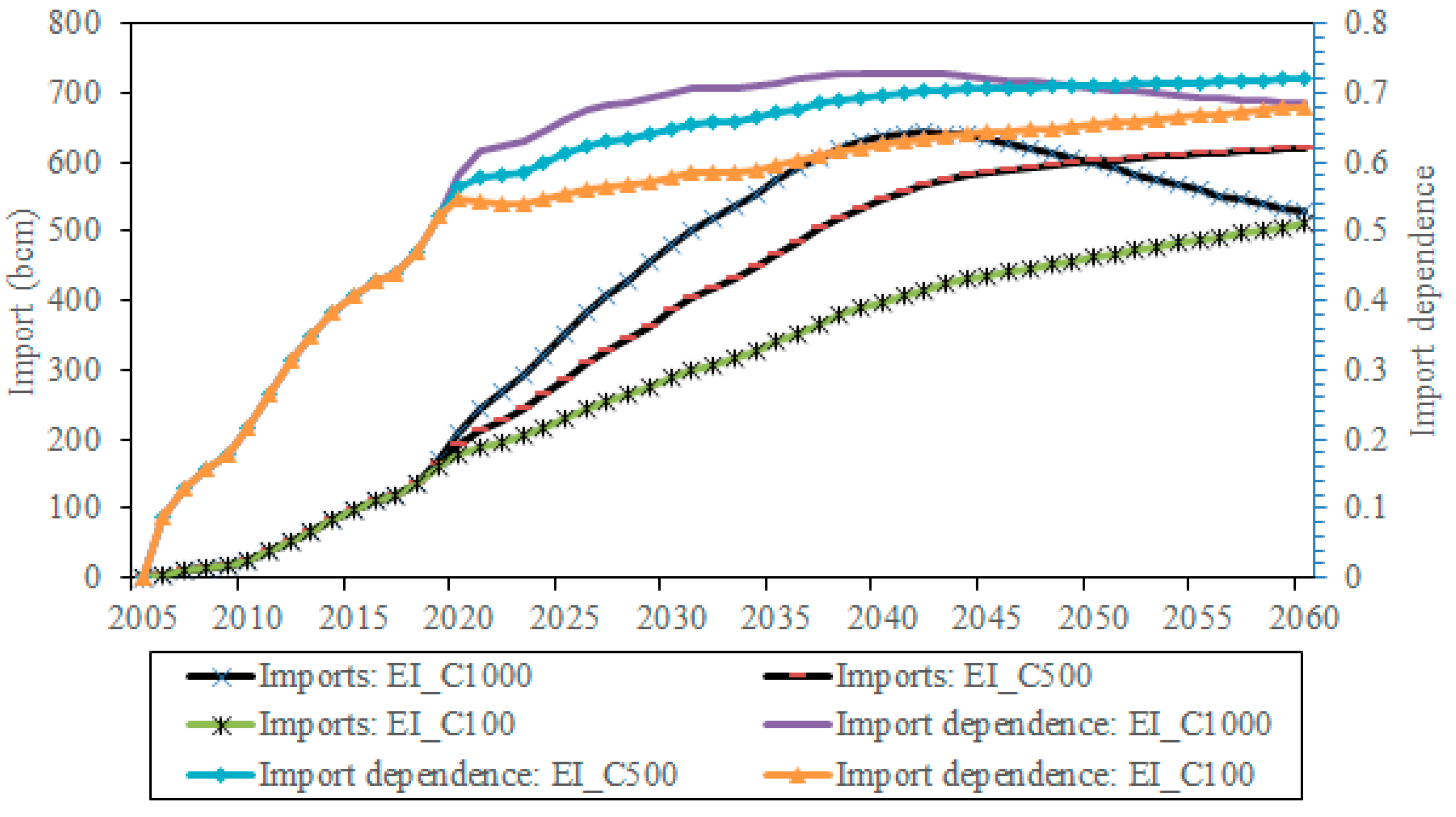

3. Analysis of Alternative Scenarios

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| GC | Gas Consumption (cubic meters) |

| RGC | Residents Gas Consumption (cubic meters) |

| IGC | Industrial Gas Consumption (cubic meters) |

| RECC | Residents Energy consumption per capita (tce/capita) |

| GDPC | GDP per Capita (CNY/capita) |

| REC | Residential Energy Consumption (tce) |

| RGS | Residential Gas Share (%) |

| UP | Urban Population (capita) |

| TP | Total Population (capita) |

| UR | Urbanization Rate (%) |

| RCS | Residential Coal Share (%) |

| ROS | Residential Oil Share (%) |

| RNFES | Residential Non-fossil Energy Share (%) |

| BR | Birth Rate (capita per year) |

| DR | Death Rate (capita per year) |

| IEC: | Industrial Energy Consumption (tce) |

| EI | Energy Intensity (tce/CNY) |

| IGS | Industrial Gas Share (%) |

| ICS | Industrial Coal Share (%) |

| IOS | Industrial Oil Share (%) |

| INFES | Industrial Non-fossil Energy Share (%) |

| AGP | Annual Gas Production (cubic meters/year) |

| PGRR | Proved Gas Residual Reserve (cubic meters) |

| ETR | Extraction Rate (cubic meters/year) |

| APR | Annual Proved Reserve (cubic meters/year) |

| GR | Geological Reserves (cubic meters) |

| EPR | Exploration Rate (cubic meters/year) |

| IC | Import Change (cubic meters) |

| SG | Supply Gap (cubic meters) |

| TAI | Time to Adjust Import (1 year) |

| ID | Import Dependence (%) |

| GST | Gas Storage (cubic meters) |

| GS | Gas Supply (cubic meters) |

| STG | Storage Gap (cubic meters) |

| EST | Expected Storage (cubic meters) |

| SR | Storage Ratio (%) |

| ES | Expected Supply (cubic meters) |

| GP | Gas Production (cubic meters) |

| SA | Storage Adjustment (cubic meters) |

| TAS | Time to Adjust Storage (0.5 year) |

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Production (bcm) | Consumption (bcm) | Import (bcm) | |||

|---|---|---|---|---|---|---|

| Sim Data | Real Data | Sim Data | Real Data | Sim Data | Real Data | |

| 2005 | 50.7337 | 49.32 | 41.8656 | 46.763 | 0.001 | 0.001 |

| 2006 | 58.0327 | 58.553 | 52.6966 | 56.141 | 1.206 | 0.99 |

| 2007 | 65.5992 | 69.24 | 65.162 | 70.523 | 3.512 | 4.02 |

| 2008 | 73.4019 | 80.3 | 80.1555 | 81.294 | 5.032 | 4.6 |

| 2009 | 81.409 | 85.269 | 93.5419 | 89.52 | 10.371 | 7.6 |

| 2010 | 89.5888 | 94.848 | 108.545 | 106.941 | 21.034 | 16.47 |

| 2011 | 97.9095 | 102.69 | 125.391 | 130.53 | 32.127 | 31.15 |

| 2012 | 106.34 | 107.22 | 144.316 | 146.3 | 40.6265 | 42.06 |

| 2013 | 114.848 | 117.38 | 161.984 | 170.537 | 53.202 | 52.54 |

| 2014 | 123.403 | 128.49 | 181.347 | 187.057 | 65.32 | 59.13 |

| 2015 | 131.976 | 134.61 | 202.567 | 193.175 | 79.1457 | 61.14 |

| 2016 | 140.537 | 136.865 | 224.29 | 207.806 | 87.7504 | 74.56 |

| 2017 | 149.057 | 148.035 | 247.7 | 239.37 | 105.096 | 94.56 |

| 2018 | 155.608 | 160.159 | 271.557 | - | 120.31 | - |

| 2019 | 162.039 | 176.174 | 297.141 | - | 141.833 | - |

| 2020 | 168.339 | - | 324.545 | - | 161.399 | - |

| 2025 | 195.263 | - | 426.956 | - | 241.953 | - |

| 2030 | 219.73 | - | 536.739 | - | 326.466 | - |

| 2035 | 239.34 | - | 651.794 | - | 422.107 | - |

| 2040 | 245.215 | - | 782.01 | - | 547.386 | - |

| 2045 | 248.291 | - | 902.392 | - | 664.544 | - |

| 2050 | 248.953 | - | 1013.04 | - | 774.003 | - |

| 2055 | 247.574 | - | 1119.11 | - | 881.154 | - |

| 2060 | 244.503 | - | 1213.44 | - | 977.89 | - |

| Year | Gas Storage (bcm) | Imports (bcm) | ||||

|---|---|---|---|---|---|---|

| EI_C1000 | EI_C500 | EI_C100 | EI_C1000 | EI_C500 | EI_C100 | |

| 2020 | 7.32 | 12.27 | 16.32 | 209.76 | 193.27 | 179.19 |

| 2025 | 72.65 | 64.89 | 58.66 | 351.81 | 287.51 | 230.39 |

| 2030 | 130.33 | 108.58 | 89.05 | 480.23 | 384.93 | 289.87 |

| 2035 | 174.17 | 143.82 | 112.36 | 573.03 | 466.95 | 340.13 |

| 2040 | 205.45 | 173.90 | 132.96 | 635.39 | 545.02 | 398.36 |

| 2045 | 217.30 | 193.83 | 148.66 | 634.54 | 585.16 | 436.02 |

| 2050 | 211.29 | 202.16 | 158.02 | 598.46 | 601.51 | 462.17 |

| 2055 | 199.69 | 206.43 | 165.93 | 558.74 | 611.78 | 487.38 |

| 2060 | 188.39 | 208.87 | 173.08 | 529.96 | 619.81 | 510.95 |

References

- Feng, T.; Yang, Y.; Xie, S.; Dong, J.; Ding, L. Economic drivers of greenhouse gas emissions in China. Renew. Sustain. Energy Rev. 2017, 78, 996–1006. [Google Scholar] [CrossRef]

- BP. Energy Outlook 2020 Edition; British Petroleum (BP p.l.c): London, UK, 2020. [Google Scholar]

- Baranes, E.; Mirabel, F.; Poudou, J.C. Access to natural gas storage facilities: Strategic and regulation issues. Energy Econ. 2014, 41, 19–32. [Google Scholar] [CrossRef]

- Quattrocchi, F.; Boschi, E.; Spena, A.; Buttinelli, M.; Cantucci, B.; Procesi, M. Synergic and conflicting issues in planning underground use to produce energy in densely populated countries, as Italy Geological storage of CO2, natural gas, geothermics and nuclear waste disposal. Appl. Energy 2013, 101, 393–412. [Google Scholar] [CrossRef]

- Ding, G.S.; Liang, J.; Ren, Y.S.; Zhao, X.F.; Ran, L.N. Suggestions on establishing peak-shaving reserve and emergency system in China. Nat. Gas Ind. 2009, 5, 98–100. [Google Scholar]

- Zhang, J.D.; Tan, Y.F.; Zhang, T.T.; Yu, K.C.; Wang, X.M.; Zhao, Q. Natural gas market and underground gas storage development in China. J. Energy Storage 2020, 29, 101338. [Google Scholar] [CrossRef]

- Xie, N.-M.; Yuan, C.-Q.; Yang, Y.-J. Forecasting China’s energy demand and self-sufficiency rate by grey forecasting model and Markov model. Int. J. Electr. Power Energy Syst. 2015, 66, 1–8. [Google Scholar] [CrossRef]

- Aktunc, E.A.; Yukseltan, E.; Yucekaya, A.; Bilge, A.H. Managing natural gas demand for free consumers under uncertainty and limited storage capacity. J. Nat. Gas Sci. Eng. 2020, 79, 103322. [Google Scholar] [CrossRef]

- Confort, M.J.F.; Mothe, C.G. Estimating the required underground natural gas storage capacity in Brazil from the gas industry characteristics of countries with gas storage facilities. J. Nat. Gas Sci. Eng. 2014, 18, 120–130. [Google Scholar] [CrossRef]

- Hoffler, F.; Kubler, M. Demand for storage of natural gas in northwestern Europe: Trends 2005–30. Energy Policy 2007, 35, 5206–5219. [Google Scholar] [CrossRef]

- de Joode, J.; Ozdemir, O. Demand for seasonal gas storage in northwest Europe until 2030: Simulation results with a dynamic model. Energy Policy 2010, 38, 5817–5829. [Google Scholar] [CrossRef]

- Flouri, M.; Karakosta, C.; Kladouchou, C.; Psarras, J. How does a natural gas supply interruption affect the EU gas security? A Monte Carlo simulation. Renew. Sustain. Energy Rev. 2015, 44, 785–796. [Google Scholar] [CrossRef]

- Zeng, Y.; Klabjan, D.; Arinez, J. Distributed solar renewable generation: Option contracts with renewable energy credit uncertainty. Energy Econ. 2015, 48, 295–305. [Google Scholar] [CrossRef]

- Yepes Rodriguez, R. Real option valuation of free destination in long-tern liquefied natural gas supplies. Energy Econ. 2008, 30, 1909–1932. [Google Scholar] [CrossRef]

- Askari, S.; Montazerin, N.; Zarandi, M.H.F. Forecasting semi-dynamic response of natural gas networks to nodal gas consumptions using genetic fuzzy systems. Energy 2015, 83, 252–266. [Google Scholar] [CrossRef]

- Yu, L.; Zhao, Y.; Tang, L. A compressed sensing based AI learning paradigm for crude oil price forecasting. Energy Econ. 2014, 46, 236–245. [Google Scholar] [CrossRef]

- Yu, F.; Xu, X. A short-term load forecasting model of natural gas based on optimized genetic algorithm and improved BP neural network. Appl. Energy 2014, 134, 102–113. [Google Scholar] [CrossRef]

- Guo, M.J.; Bu, Y.; Cheng, J.H.; Jiang, Z.Y. Natural Gas Security in China: A Simulation of Evolutionary Trajectory and Obstacle Degree Analysis. Sustainability 2019, 11, 96. [Google Scholar] [CrossRef] [Green Version]

- Strachan, N.; Kannan, R. Hybrid modelling of long-term carbon reduction scenarios for the UK. Energy Econ. 2008, 30, 2947–2963. [Google Scholar] [CrossRef]

- Morales, K. Response from a MARKAL technology model to the EMF scenario assumptions. Energy Econ. 2004, 26, 655–674. [Google Scholar] [CrossRef]

- Gao, F.; Shao, X. Forecasting annual natural gas consumption via the application of a novel hybrid model. Environ. Sci. Pollut. Res. 2021, 28, 21411–21424. [Google Scholar] [CrossRef]

- Wood, D.A. A review and outlook for the global LNG trade. J. Nat. Gas Sci. Eng. 2012, 9, 16–27. [Google Scholar] [CrossRef]

- Chi, K.C.; Nuttall, W.J.; Reiner, D.M. Dynamics of the UK natural gas industry: System dynamics modelling and long-term energy policy analysis. Technol. Forecast. Soc. Chang. 2009, 76, 339–357. [Google Scholar]

- Xiao, B.; Niu, D.; Guo, X. Can natural gas-fired power generation break through the dilemma in China? A system dynamics analysis. J. Clean. Prod. 2016, 137, 1191–1204. [Google Scholar] [CrossRef]

- Hsu, C.-W. Using a system dynamics model to assess the effects of capital subsidies and feed-in tariffs on solar PV installations. Appl. Energy 2012, 100, 205–217. [Google Scholar] [CrossRef]

- Jiao, J.-L.; Han, K.-Y.; Wu, G.; Li, L.-L.; Wei, Y.-M. The effect of an SPR on the oil price in China: A system dynamics approach. Appl. Energy 2014, 133, 363–373. [Google Scholar] [CrossRef]

- Li, J.C.; Dong, X.C.; Shangguan, J.X.; Hook, M. Forecasting the growth of China’s natural gas consumption. Energy 2011, 36, 1380–1385. [Google Scholar] [CrossRef] [Green Version]

- Mu, X.Z.; Li, G.H.; Hu, G.W. Modeling and scenario prediction of a natural gas demand system based on a system dynamics method. Pet. Sci. 2018, 15, 912–924. [Google Scholar] [CrossRef] [Green Version]

- Gomez, C.R.; Arango-Aramburo, S.; Larsen, E.R. Construction of a Chilean energy matrix portraying energy source substitution: A system dynamics approach. J. Clean. Prod. 2017, 162, 903–913. [Google Scholar] [CrossRef] [Green Version]

- Xiong, W.W.; Yan, L.; Wang, T.; Gao, Y.G. Substitution Effect of Natural Gas and the Energy Consumption Structure Transition in China. Sustainability 2020, 12, 7853. [Google Scholar] [CrossRef]

- Ejarque, J.M. Evaluating the economic cost of natural gas strategic storage restrictions. Energy Econ. 2011, 33, 44–55. [Google Scholar] [CrossRef]

- Green, R. Gas prices in the UK: Markets and insecurity of supply. Energy J. 2007, 28, 187–189. [Google Scholar]

- Zeren, F.; Akkus, H.T. The relationship between renewable energy consumption and trade openness: New evidence from emerging economies. Renew. Energy 2020, 147, 322–329. [Google Scholar] [CrossRef]

- Wang, X.L.; Economides, M.J. Purposefully built underground natural gas storage. J. Nat. Gas Sci. Eng. 2012, 9, 130–137. [Google Scholar] [CrossRef]

- Xu, D.T. Guoqiang, Policy evolution and research progress of investment, construction and operation management of gas storage in China. Oil Gas Storage Transp. 2020, 39, 481–491. [Google Scholar]

- Anser, M.K.; Yousaf, Z.; Zaman, K.; Nassani, A.A.; Alotaibi, S.M.; Jambari, H.; Khan, A.; Kabbani, A. Determination of resource curse hypothesis in mediation of financial development and clean energy sources: Go-for-green resource policies. Resources Policy 2020, 66, 101640. [Google Scholar] [CrossRef]

- Wang, X.L.; Cheng, J.H.; Chen, J.; Xiao, J.Z. Substitution effect of natural gas consumption and energy transition security in China. China Popul. Resour. Environ. 2021, 31, 138–149. [Google Scholar]

- Malzi, M.J.; Sohag, K.; Vasbieva, D.G.; Ettahir, A. Environmental policy effectiveness on residential natural gas use in OECD countries. Resources Policy 2020, 66, 101651. [Google Scholar] [CrossRef]

- National Bureau of Statistics of China. China Statistical Yearbook 2020 Edition; China Statistics Press: Beijing, China, 2020.

- Guo, Y.J.; Hawkes, A. Asset stranding in natural gas export facilities: An agent-based simulation. Energy Policy 2019, 132, 132–155. [Google Scholar] [CrossRef]

- Zhao, G.M. China’s LNG terminal construction and future development. Petrochem. Saf. Environ. Prot. Technol. 2020, 36, 1–6. [Google Scholar]

| Year | 2005–2016 | 2017–2050 | 2051–2060 |

|---|---|---|---|

| GDP growth rate | 9.8% | 3.5% | 2.0% |

| Year | 2005 | 2020 | 2030 | 2060 |

|---|---|---|---|---|

| Birth rate | 0.0124 | 0.008 | 0.007 | 0.006 |

| Death rate | 0.007 | |||

| 2005–2018 | 2019 | 2030 | 2060 | |

|---|---|---|---|---|

| Exploration rate | 0.0075 | |||

| Extraction rate | 0.018 | 0.03 | 0.036 | 0.04 |

| Studies | Methods | Study Area | Simulation Error | Features |

|---|---|---|---|---|

| Confort and Mothe [9] | Linear regression analysis | Brazil | 37.4–89.1% | Short-term forecast, No scenario analysis |

| Hoffler and Kubler [10] | Top-down extrapolation | Northwest Europe | No model calibration | Long-term forecast, Scenario analysis |

| de Joode and Ozdemir [11] | Game-theory equilibrium model | Northwest Europe | Unarticulated | Long-term forecast, Scenario analysis |

| Yu and Xu [17] | Artificial neural networks | Shanghai, China | Less than 10% | Short-term forecast, No scenario analysis |

| This study | System dynamics model | China | Less than 10% | Long-term forecast, Scenario analysis |

| Alternative Cases | Energy Intensity Growth Rate | Carbon Prices (RMB/t) |

|---|---|---|

| Base case | −2% | 50 |

| C100 | −2% | 100 |

| C500 | −2% | 500 |

| C1000 | −2% | 1000 |

| EI_C100 | −3% | 100 |

| EI_C500 | −3% | 500 |

| EI_C1000 | −3% | 1000 |

| Year | EI_C1000 | EI_C500 | EI_C100 | |

|---|---|---|---|---|

| Storage (bcm) | 2025 | 72.6 | 64.9 | 58.7 |

| 2030 | 130.3 | 108.6 | 89.1 | |

| 2060 | 188.4 | 208.9 | 173.1 | |

| Import (bcm) | 2025 | 351.8 | 287.5 | 230.4 |

| 2030 | 480.2 | 384.9 | 289.9 | |

| 2060 | 529.9 | 619.8 | 510.9 |

| Project Type | Status | Gas Source | Operating Date | Capacity (bcm/Year) |

|---|---|---|---|---|

| Gas Pipeline | In operation | Central Asia-A/B | 2012.12 | 30 |

| In operation | Central Asia-C | 2014.6 | 25 | |

| Under construction | Central Asia-D | 2022 | 30 | |

| In operation | Burma | 2013.6 | 12 | |

| In operation | Russia-eastern line | 2019 | 38 | |

| Under construction | Russia-western line | 2022 | 30 | |

| LNG Terminals | In operation | Middle East, Asia-Pacific | 2006–2019 | 126 |

| Under construction | Middle East, Asia-Pacific | 2020–2022 | 33.8 | |

| Planning | Middle East, Asia-Pacific | 2023–2030 | 166 |

| Year | 2019 | 2022 | 2030 |

|---|---|---|---|

| Pipeline gas (bcm/year) | 105 | 165 | 165 |

| LNG (bcm/year) | 126 | 159.8 | 325.8 |

| Total capacity (bcm/year) | 231 | 324.8 | 490.8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, Z.; Wang, H.; Li, T.; Si, I. Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model. Sustainability 2021, 13, 8674. https://doi.org/10.3390/su13158674

Chen Z, Wang H, Li T, Si I. Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model. Sustainability. 2021; 13(15):8674. https://doi.org/10.3390/su13158674

Chicago/Turabian StyleChen, Zhihua, Hui Wang, Tongxia Li, and Ieongcheng Si. 2021. "Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model" Sustainability 13, no. 15: 8674. https://doi.org/10.3390/su13158674

APA StyleChen, Z., Wang, H., Li, T., & Si, I. (2021). Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model. Sustainability, 13(15), 8674. https://doi.org/10.3390/su13158674