Sustainability of Both Pecking Order and Trade-Off Theories in Chinese Manufacturing Firms

,

,

Abstract

1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Data

3.2. Methodology

4. Models

5. Empirical Results

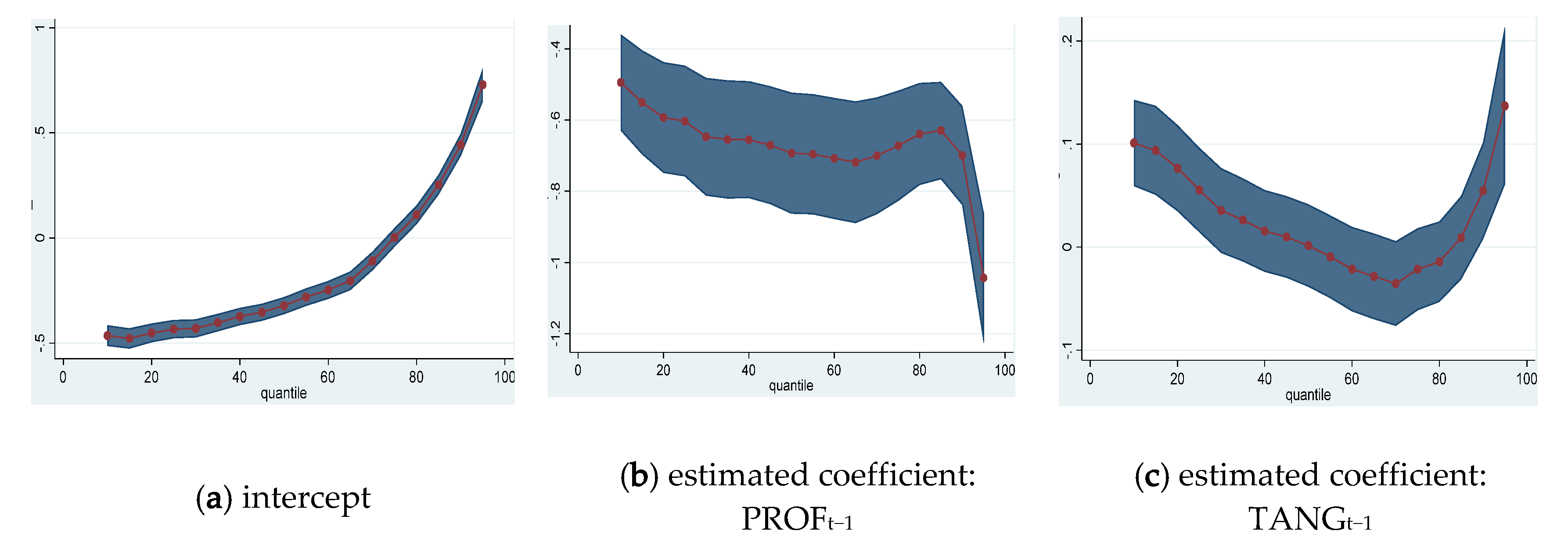

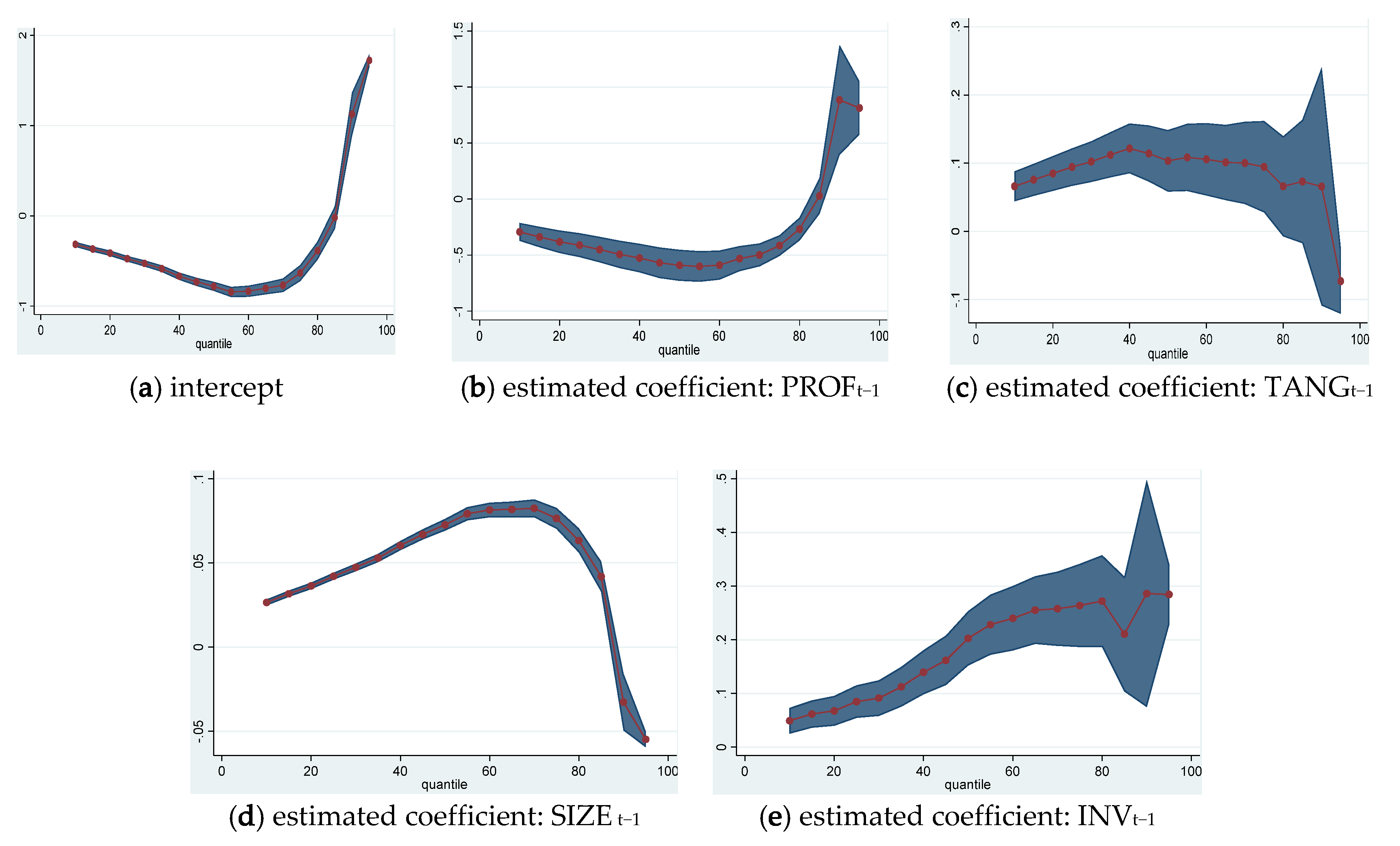

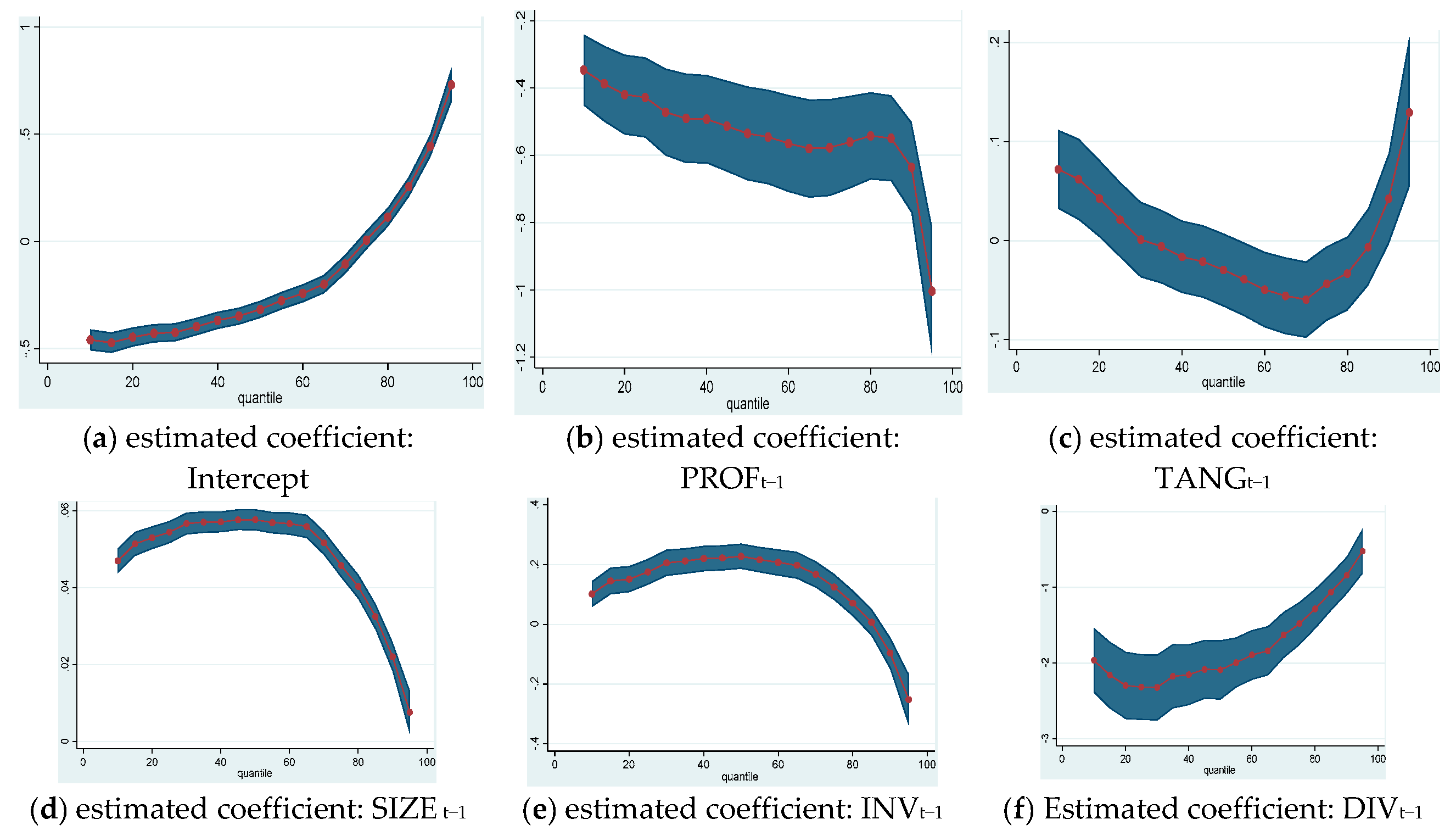

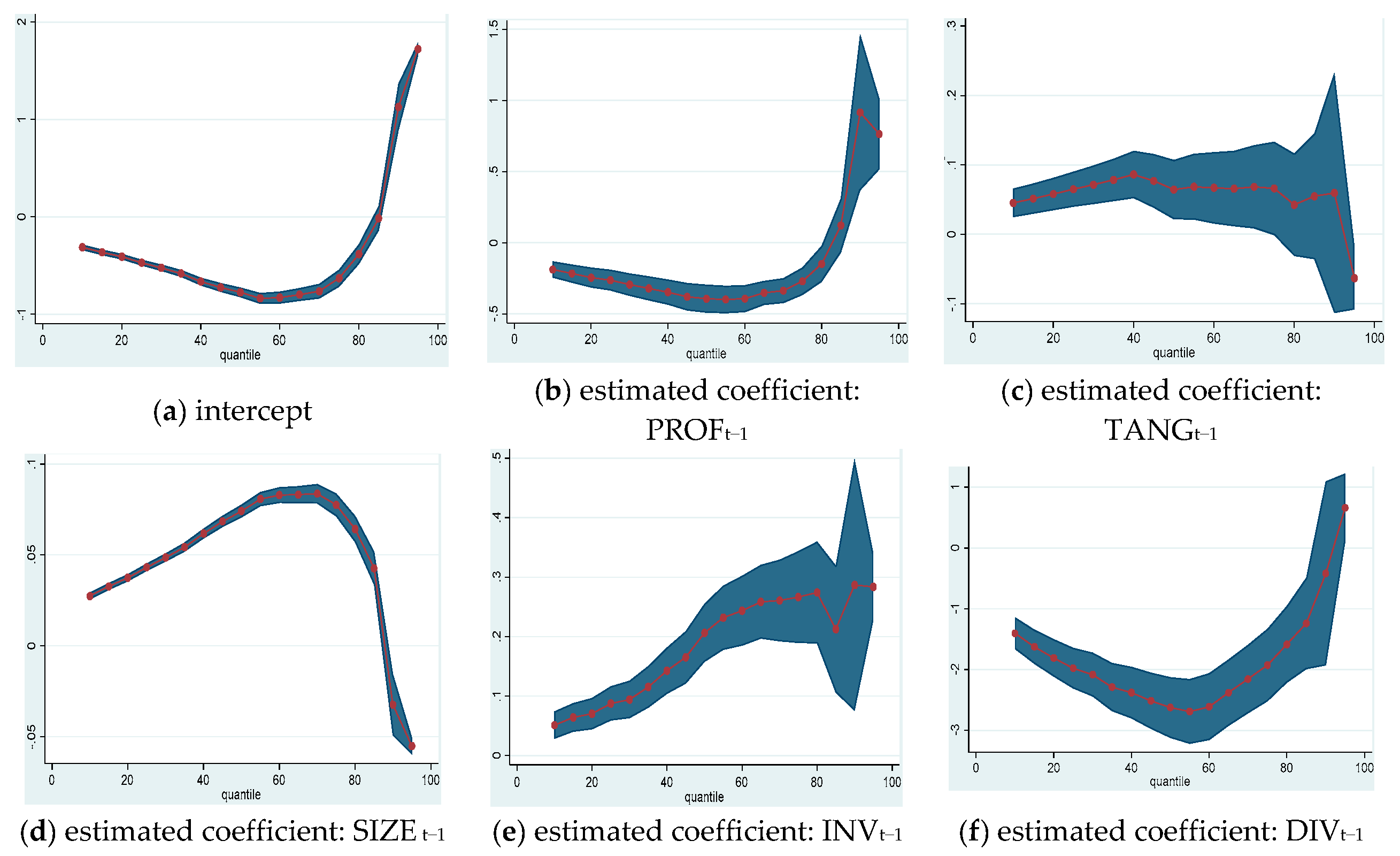

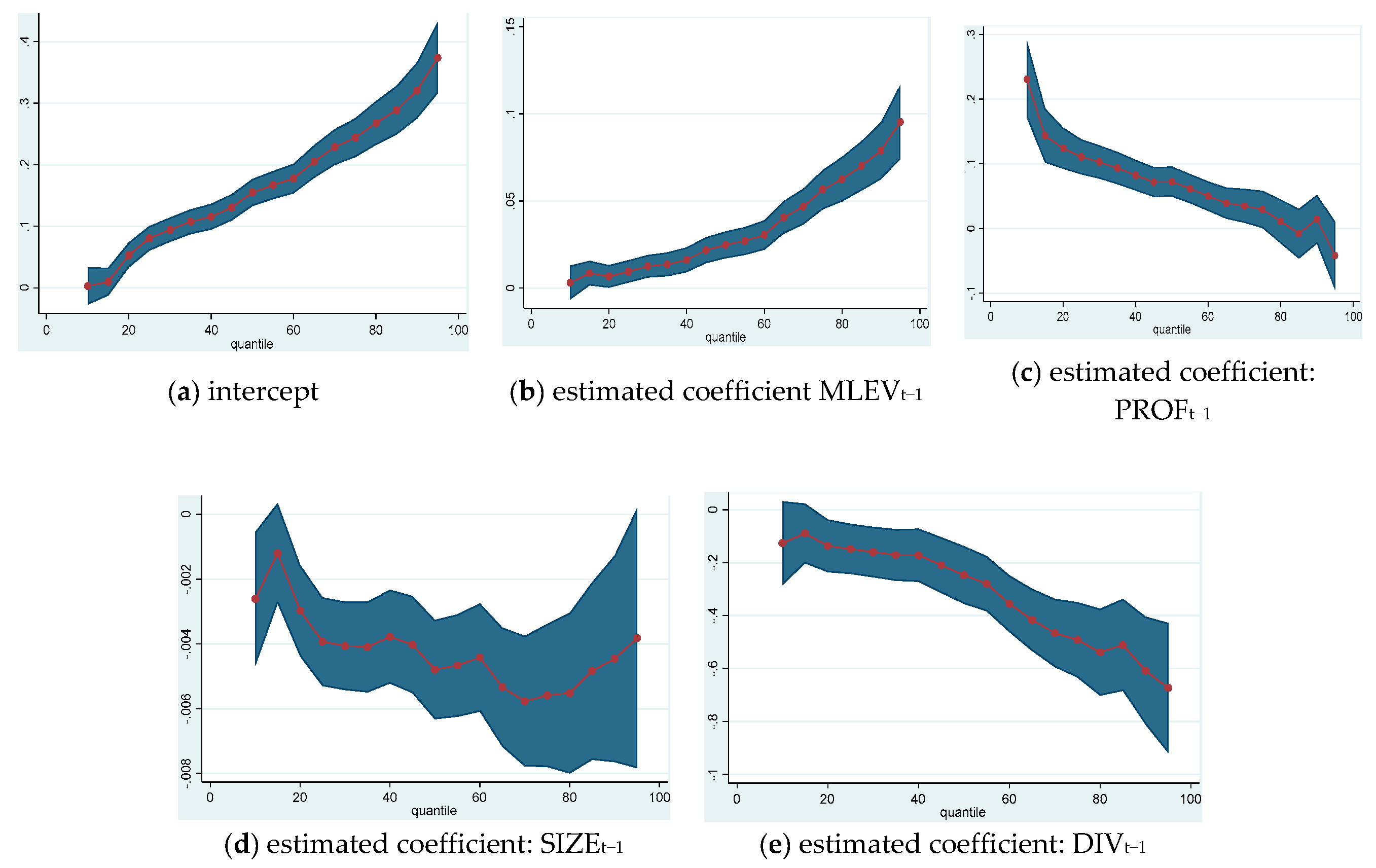

5.1. Main Findings

5.2. Leverage and Profitability

5.3. Leverage and Firm Size

5.4. Leverage and Investment Opportunities

5.5. Leverage and Dividend Payout Ratio

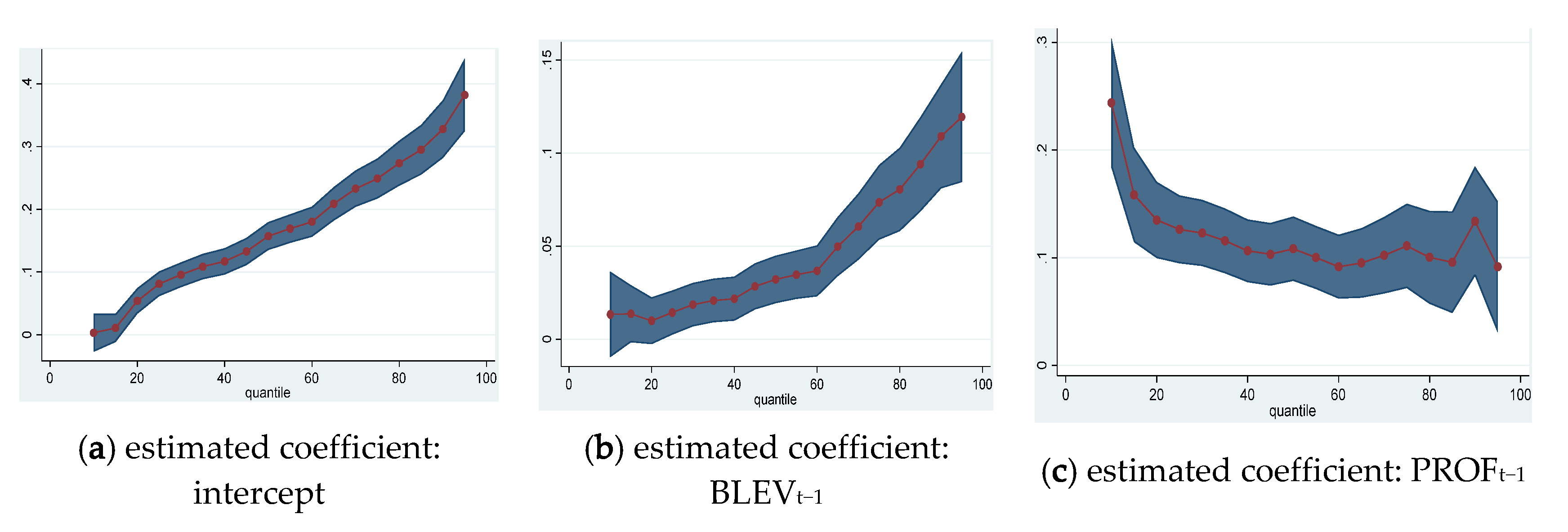

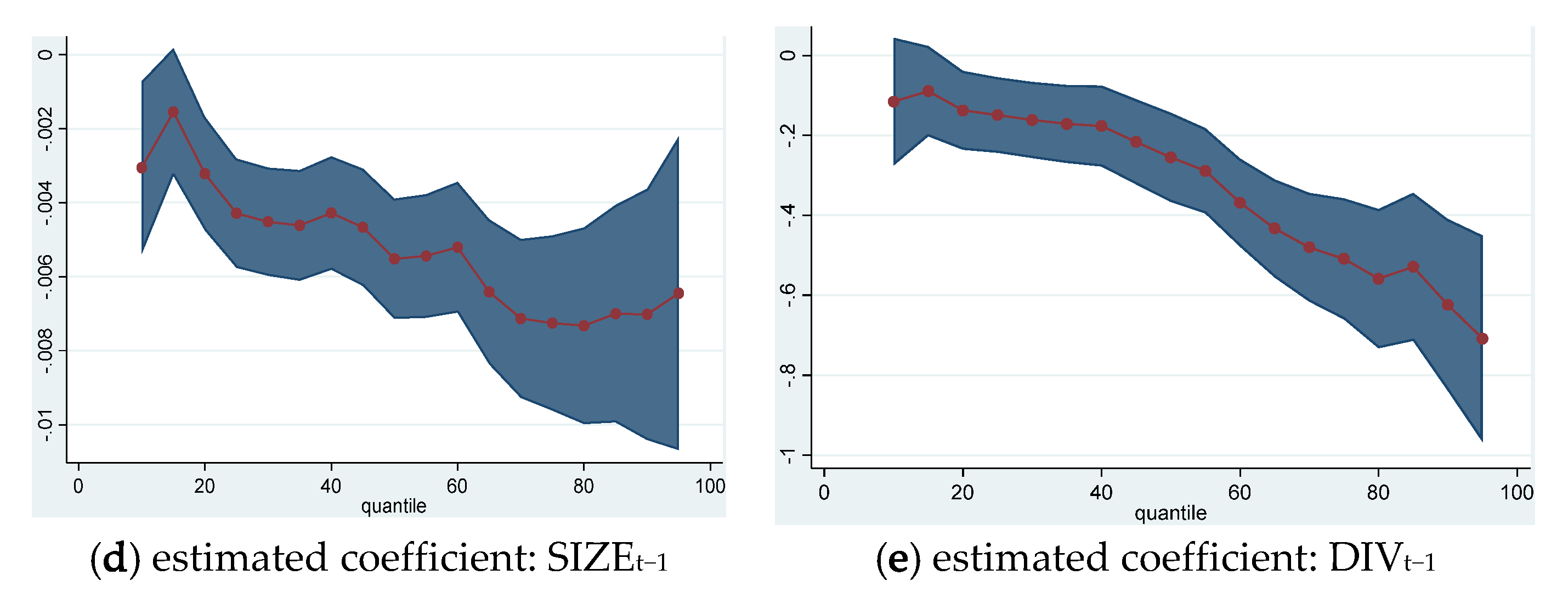

5.6. Investment Opportunities and Dividend Payout Ratio

5.7. Robustness Checks

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

References

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. American 1958, 1, 3. [Google Scholar]

- Modigliani, F.; Miller, M.H. Corporate income taxes and the cost of capital: A correction. Am. Econ. Rev. 1963, 53, 433–443. [Google Scholar]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef]

- Allen, D.E. The pecking order hypothesis: Australian evidence. Appl. Financ. Econ. 1993, 3, 101–112. [Google Scholar] [CrossRef]

- Baskin, J. An empirical investigation of the pecking order hypothesis. Financ. Manag. 1989, 26–35. [Google Scholar] [CrossRef]

- De Jong, A.; Verbeek, M.; Verwijmeren, P. The impact of financing surpluses and large financing deficits on tests of the pecking order theory. Financ. Manag. 2010, 39, 733–756. [Google Scholar] [CrossRef]

- Easterbrook, F.H. Two agency-cost explanations of dividends. Am. Econ. Rev. 1984, 74, 650–659. [Google Scholar]

- Tong, G.; Green, C.J. Pecking order or trade-off hypothesis? Evidence on the capital structure of Chinese companies. Appl. Econ. 2005, 37, 2179–2189. [Google Scholar] [CrossRef]

- Booth, L.; Aivazian, V.; Demirguc-Kunt, A.; Maksimovic, V. Capital structures in developing countries. J. Financ. 2001, 56, 87–130. [Google Scholar] [CrossRef]

- De Jong, A.; Kabir, R.; Nguyen, T.T. Capital structure around the world: The roles of firm-and country-specific determinants. J. Bank. Financ. 2008, 32, 1954–1969. [Google Scholar] [CrossRef]

- Chen, J.J. Determinants of capital structure of Chinese-listed companies. J. Bus. Res. 2004, 57, 1341–1351. [Google Scholar] [CrossRef]

- Huang, G. The determinants of capital structure: Evidence from China. China Econ. Rev. 2006, 17, 14–36. [Google Scholar] [CrossRef]

- Ni, J.; Yu, M. Testing the pecking-order theory: Evidence from Chinese listed companies. Chin. Econ. 2008, 41, 97–113. [Google Scholar] [CrossRef]

- Li, K.; Yue, H.; Zhao, L. Ownership, institutions, and capital structure: Evidence from China. J. Comp. Econ. 2009, 37, 471–490. [Google Scholar] [CrossRef]

- Tse, C.-B.; Rodgers, T. The capital structure of Chinese listed firms: Is manufacturing industry special? Manag. Financ. 2014, 40, 469–486. [Google Scholar] [CrossRef]

- Zhou, T.; Xie, J. Ultimate ownership and adjustment speed toward target capital structures: Evidence from China. Emerg. Mark. Financ. Trade 2016, 52, 1956–1965. [Google Scholar] [CrossRef]

- Ferrarini, B.; Hinojales, M.; Scaramozzino, P. Leverage and capital structure determinants of Chinese listed companies. In Asian Development Bank Economics Working Paper Series (509); Asian Development Bank: Mandaluyong City, Philippines, 2017. [Google Scholar]

- Fattouh, B.; Scaramozzino, P.; Harris, L. Capital structure in South Korea: A quantile regression approach. J. Dev. Econ. 2005, 76, 231–250. [Google Scholar] [CrossRef]

- Sánchez-Vidal, F.J. High debt companies’ leverage determinants in Spain: A quantile regression approach. Econ. Model. 2014, 36, 455–465. [Google Scholar] [CrossRef]

- Sheikh, N.A.; Wang, Z. Determinants of capital structure. Manag. Financ. 2011, 37, 117–133. [Google Scholar]

- Liu, W.-C.; Hsu, C.-M. Financial structure, corporate finance and growth of Taiwan’s manufacturing firms. Rev. Pacif. Basin Financ. Mark. Policies 2006, 9, 67–95. [Google Scholar] [CrossRef]

- Rajan, R.G.; Zingales, L. What do we know about capital structure? Some evidence from international data. J. Financ. 1995, 50, 1421–1460. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Testing trade-off and pecking order predictions about dividends and debt. Rev. Financ. Stud. 2002, 15, 1–33. [Google Scholar] [CrossRef]

- Shyam-Sunder, L.; Myers, S.C. Testing static tradeoff against pecking order models of capital structure. J. Financ. Econ. 1999, 51, 219–244. [Google Scholar] [CrossRef]

- Frank, M.Z.; Goyal, V.K. The effect of market conditions on capital structure adjustment. Financ. Res. Lett. 2004, 1, 47–55. [Google Scholar] [CrossRef]

- Frank, M.Z.; Goyal, V.K. Trade-off and pecking order theories of debt. In Handbook of Empirical Corporate Finance; Elsevier: Amsterdam, The Netherlands, 2008; pp. 135–202. [Google Scholar]

- Chirinko, R.S.; Singha, A.R. Testing static tradeoff against pecking order models of capital structure: A critical comment. J. Financ. Econ. 2000, 58, 417–425. [Google Scholar] [CrossRef]

- Frank, M.Z.; Goyal, V.K. Testing the pecking order theory of capital structure. J. Financ. Econ. 2003, 67, 217–248. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Financing decisions: Who issues stock? J. Financ. Econ. 2005, 76, 549–582. [Google Scholar] [CrossRef]

- Hodder, J.E.; Senbet, L.W. International capital structure equilibrium. J. Financ. 1990, 45, 1495–1516. [Google Scholar] [CrossRef]

- Wald, J.K. How firm characteristics affect capital structure: An international comparison. J. Financ. Res. 1999, 22, 161–187. [Google Scholar] [CrossRef]

- Ozkan, A. Determinants of capital structure and adjustment to long run target: Evidence from UK company panel data. J. Bus. Financ. Account. 2001, 28, 175–198. [Google Scholar] [CrossRef]

- Chui, A.C.; Lloyd, A.E.; Kwok, C.C. The determination of capital structure: Is national culture a missing piece to the puzzle? J. Int. Bus. Stud. 2002, 33, 99–127. [Google Scholar] [CrossRef]

- Bevan, A.A.; Danbolt, J. Capital structure and its determinants in the UK-a decompositional analysis. Appl. Financ. Econ. 2002, 12, 159–170. [Google Scholar] [CrossRef]

- Psillaki, M.; Daskalakis, N. Are the determinants of capital structure country or firm specific? Small Bus. Econ. 2009, 33, 319–333. [Google Scholar] [CrossRef]

- Črnigoj, M.; Mramor, D. Determinants of capital structure in emerging European economies: Evidence from Slovenian firms. Emerg. Mark. Financ. Trade 2009, 45, 72–89. [Google Scholar] [CrossRef]

- Al-Najjar, B.; Hussainey, K. Revisiting the capital-structure puzzle: UK evidence. J. Risk Financ. 2011, 12, 329–338. [Google Scholar] [CrossRef]

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: Evidence from the field. J. Financ. Econ. 2001, 60, 187–243. [Google Scholar] [CrossRef]

- Flannery, M.J.; Rangan, K.P. Partial adjustment toward target capital structures. J. Financ. Econ. 2006, 79, 469–506. [Google Scholar] [CrossRef]

- Byoun, S. How and when do firms adjust their capital structures toward targets? J. Financ. 2008, 63, 3069–3096. [Google Scholar] [CrossRef]

- Lemmon, M.L.; Roberts, M.R.; Zender, J.F. Back to the beginning: Persistence and the cross-section of corporate capital structure. J. Financ. 2008, 63, 1575–1608. [Google Scholar] [CrossRef]

- Huang, R.; Ritter, J.R. Testing theories of capital structure and estimating the speed of adjustment. J. Financ. Quant. Anal. 2009, 44, 237–271. [Google Scholar] [CrossRef]

- Frank, M.Z.; Goyal, V.K.J.F.M. Capital structure decisions: Which factors are reliably important? Financ. Manag. 2009, 38, 1–37. [Google Scholar] [CrossRef]

- Chen, D.-H.; Chen, C.-D.; Chen, J.; Huang, Y.-F. Panel data analyses of the pecking order theory and the market timing theory of capital structure in Taiwan. Int. Rev. Econ. Financ. 2013, 27, 1–13. [Google Scholar] [CrossRef]

- Qian, Y.; Tian, Y.; Wirjanto, T.S. Do Chinese publicly listed companies adjust their capital structure toward a target level? China Econ. Rev. 2009, 20, 662–676. [Google Scholar] [CrossRef]

- Koenker, R.; Bassett, G., Jr. Regression quantiles. Econometrica 1978, 50, 33–50. [Google Scholar] [CrossRef]

- Horowitz, J.L.; Lee, S. Nonparametric estimation of an additive quantile regression model. J. Am. Stat. Assoc. 2005, 100, 1238–1249. [Google Scholar] [CrossRef]

- Koenker, R.; Hallock, K.F. Quantile regression. J. Econ. Perspect. 2001, 15, 143–156. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Agency Costs and the Theory of the Firm. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Jensen, M.C. Agency costs of free cash flow, corporate finance, and takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Kester, W.C. Capital and ownership structure: A comparison of United States and Japanese manufacturing corporations. Financ. Manag. 1986, 15, 5–16. [Google Scholar] [CrossRef]

- Friend, I.; Lang, L.H. An empirical test of the impact of managerial self-interest on corporate capital structure. J. Financ. 1988, 43, 271–281. [Google Scholar] [CrossRef]

- Chen, J.; Strange, R. The determinants of capital structure: Evidence from Chinese listed companies. Econ. Chang. Restruct. 2005, 38, 11–35. [Google Scholar] [CrossRef]

- Kadapakkam, P.R.; Kumar, P.C.; Riddick, L.A. The impact of cash flows and firm size on investment: The international evidence. J. Bank. Financ. 1998, 22, 293–320. [Google Scholar] [CrossRef]

- Marsh, P. The choice between equity and debt: An empirical study. J. Financ. 1982, 37, 121–144. [Google Scholar] [CrossRef]

- Titman, S.; Wessels, R. The determinants of capital structure choice. J. Financ. 1988, 43, 1–19. [Google Scholar] [CrossRef]

- Mazur, K. The determinants of capital structure choice: Evidence from Polish companies. Int. Adv. Econ. Res. 2007, 13, 495–514. [Google Scholar] [CrossRef]

- Redding, L.S. Firm size and dividend payouts. J. Financ. Intermed. 1997, 6, 224–248. [Google Scholar] [CrossRef]

- Chen, Y.; Dou, P.Y.; Rhee, S.G.; Truong, C.; Veeraraghavan, M. National culture and corporate cash holdings around the world. J. Bank. Financ. 2015, 50, 1–18. [Google Scholar] [CrossRef]

- Potì, V.; Pattitoni, P.; Petracci, B. Precautionary Motives for Private Firms’ Cash Holdings. Forthcoming. Int. Rev. Econ. Financ. 2020. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | N | BLEV | MLEV | PROF | INV | SIZE | TANG | DIV |

|---|---|---|---|---|---|---|---|---|

| 2001–2006 | 4044 | 0.5084 | 0.4448 | 0.0411 | 0.1452 | 14.1622 | 0.3060 | 0.0037 |

| (0.3149) | (0.2991) | (0.1352) | (0.1437) | (1.0399) | (0.1529) | (0.0163) | ||

| 2007–2012 | 6109 | 0.4799 | 0.3878 | 0.0764 | 0.1170 | 14.6168 | 0.2597 | 0.0157 |

| (0.2202) | (0.3221) | (0.0853) | (0.1339) | (1.2628) | (0.1512) | (0.0268) | ||

| 2013–2018 | 6775 | 0.4525 | 0.2926 | 0.0488 | 0.0883 | 15.4626 | 0.2501 | 0.0122 |

| (0.2034) | (0.2241) | (0.0857) | (0.1339) | (1.1921) | (0.1488) | (0.0206) | ||

| All years | 16,928 | 0.4757 | 0.3633 | 0.0569 | 0.1123 | 14.8467 | 0.2669 | 0.0114 |

| (0.2413) | (0.2876) | (0.1008) | (0.1381) | (1.2982) | (0.1523) | (0.0226) |

| Variables | Definitions |

|---|---|

| BLEV | Ratio between total liabilities to total book value of assets |

| MLEV | Ratio between total liabilities to total market value of firm (MKV) MKV = total liabilities plus market value of equity minus book value of equity |

| DIV | Ratio between dividend paid to total assets |

| PROF | Ratio between earnings before taxes and interest (EBIT) and total assets |

| TANG | ratio between net fixed assets to total assets |

| SIZE | Logarithm of total assets |

| INV | Ratio between (total asset in year t + 1 minus total asset year t) to total assets year t |

| Variables | PROF | DIV | INV | SIZE | MLEV | TANG | BLEV |

|---|---|---|---|---|---|---|---|

| PROF | 1.000 | ||||||

| – | |||||||

| DIV | 0.3270 *** | 1.000 | |||||

| (45.03) | – | ||||||

| INV | 0.0013 | 0.1965 *** | 1.000 | ||||

| (0.17) | (26.08) | – | |||||

| SIZE | −0.0283 *** | 0.0043 | −0.1989 *** | 1.000 | |||

| (−3.68) | (0.56) | (−26.40) | – | ||||

| MLEV | 0.0210 *** | −0.1325 *** | −0.6753 *** | 0.0462 *** | 1.000 | ||

| (2.74) | (−17.39) | (−119.11) | (6.02) | – | |||

| TANG | −0.0612 *** | −0.1079 *** | −0.1642 *** | 0.0691 *** | 0.1384 *** | 1.000 | |

| (−7.97) | (−14.13) | (−21.65) | (9.02) | (18.18) | – | ||

| BLEV | −0.3905 *** | −0.2360 *** | −0.1874 *** | 0.1705 *** | 0.4814 *** | 0.1311 *** | 1.000 |

| (−55.18) | (−31.60) | (−24.82) | (22.51) | (71.45) | (17.21) | – |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book Leverage, all samples (14,806 observations) | ||||||||||

| βprof | −0.494 a | −0.593 a | −0.647 a | −0.655 a | −0.693 a | −0.708 a | −0.700 a | −0.639 a | −0.699 a | −0.748 a |

| (0.026) | (0.025) | (0.024) | (0.023) | (0.022) | (0.023) | (0.022) | (0.021) | (0.024) | (0.016) | |

| βtang | 0.101 a | 0.077 a | 0.035 b | 0.035 | 0.001 | −0.021 | −0.035b | −0.014 | 0.055 a | −0.037 b |

| (0.021) | (0.020) | (0.019) | (0.018) | (0.018) | (0.018) | (0.018) | (0.016) | (0.018) | (0.021) | |

| βsize | 0.046 a | 0.052 a | 0.055 a | 0.056 a | 0.056 a | 0.056 a | 0.051 a | 0.040 a | 0.022 a | 0.013 a |

| (0.002) | (0.002) | (0.002) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | |

| βinv | 0.099 a | 0.149 a | 0.203 a | 0.218 a | 0.225 a | 0.205 a | 0.166 a | 0.069 a | −0.097 a | 0.140 a |

| (0.023) | (0.022) | (0.021) | (0.020) | (0.023) | (0.020) | (0.020) | (0.018) | (0.021) | (0.018) | |

| β0 | −0.464 a | −0.451 a | −0.430 a | −0.374 a | −0.322 a | −0.247 a | −0.109 a | 0.110 a | 0.443 a | 0.322 a |

| (0.025) | (0.023) | (0.022) | (0.021) | (0.021) | (0.021) | (0.021) | (0.020) | (0.022) | (0.025) | |

| R2 | 0.0737 | 0.1016 | 0.1228 | 0.136 | 0.1444 | 0.1379 | 0.1246 | 0.1025 | 0.0718 | 0.14 |

| Panel B: Market Leverage, all samples (14,806 Observations) | ||||||||||

| βprof | −0.293 a | −0.381 a | −0.450 a | −0.526 a | −0.591 a | −0.590 a | −0.499 a | −0.268 a | 0.885 a | 0.120 a |

| (0.014) | (0.016) | (0.018) | (0.022) | (0.028) | (0.033) | (0.038) | (0.046) | (0.104) | (0.021) | |

| βtang | 0.066 a | 0.085 a | 0.102 a | 0.122 a | 0.103 a | 0.106 a | 0.100 a | 0.066 b | 0.066 | −0.198 a |

| (0.011) | (0.012) | (0.015) | (0.018) | (0.022) | (0.026) | (0.030) | (0.036) | (0.082) | (0.028) | |

| βsize | 0.026 a | 0.036 a | 0.047 a | 0.060 a | 0.073 a | 0.081 a | 0.082 a | 0.063 a | −0.033 a | −0.019 a |

| (0.012) | (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | (0.002) | (0.003) | (0.007) | (0.002) | |

| βinv | −0.317 | 0.068 a | 0.092 a | 0.140 a | 0.203 a | 0.240 a | 0.258 a | 0.272 a | 0.286 a | 0.412 a |

| (0.013) | (0.014) | (0.016) | (0.020) | (0.024) | (0.029) | (0.033) | (0.040) | (0.091) | (0.024) | |

| β0 | −0.317 a | −0.414 a | −0.528 a | −0.669 a | −0.781 a | −0.836 a | −0.769 a | −0.387 a | 1.126 a | 0.618 a |

| (0.013) | (0.015) | (0.017) | (0.021) | (0.026) | (0.031) | (0.035) | (0.043) | (0.098) | (0.032) | |

| R2 | 0.0908 | 0.1205 | 0.1368 | 0.1445 | 0.1316 | 0.1147 | 0.0884 | 0.0371 | 0.0079 | 0.138 |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book Leverage, all samples (14,806 observations) | ||||||||||

| βprof | −0.346 a | −0.420 a | −0.472 a | −0.493 a | −0.535 a | −0.565 a | −0.577 a | −0.542 a | −0.636 a | −0.750 a |

| (0.027) | (0.026) | (0.025) | (0.023) | (0.023) | (0.023) | (0.023) | (0.022) | (0.025) | (0.016) | |

| βtang | 0.072 a | 0.042 b | 0.001 | −0.016 | −0.030 c | −0.049 a | −0.060 a | −0.033 b | 0.042 b | −0.037 c |

| (0.020) | (0.019) | (0.019) | (0.018) | (0.017) | (0.018) | (0.017) | (0.016) | (0.019) | (0.021) | |

| βsize | 0.047 a | 0.053 a | 0.057 a | 0.057 a | 0.058 a | 0.057 a | 0.052 a | 0.071 a | 0.022 a | 0.013 a |

| (0.002) | (0.002) | (0.002) | (0.001) | (0.001) | (0.001) | (0.001) | (0.018) | (0.002) | (0.002) | |

| βinv | 0.102 a | 0.152 a | 0.206 a | 0.221 a | 0.228 a | 0.208 a | 0.071 a | 0.071 a | 0.071 a | 0.140 a |

| (0.023) | (0.022) | (0.021) | (0.001) | (0.020) | (0.020) | (0.019) | (0.018) | (0.021) | (0.018) | |

| βdiv | −1.962 a | −2.295 a | −2.321 a | −2.154 a | −2.089 a | −1.892 a | −1.629 a | −1.284 a | −0.840 a | 0.047 |

| (0.115) | (0.109) | (0.104) | (0.098) | (0.097) | (0.098) | (0.098) | (0.092) | (0.104) | (0.076) | |

| β0 | −0.460 a | −0.446 a | −0.424 a | −0.368 a | −0.317 a | −0.242 a | −0.105 a | 0.113 a | 0.445 a | 0.047 |

| (0.024) | (0.023) | (0.022) | (0.021) | (0.021) | (0.021) | (0.021) | (0.019) | (0.022) | (0.076) | |

| R2 | 0.092 | 0.128 | 0.152 | 0.163 | 0.170 | 0.159 | 0.141 | 0.114 | 0.076 | 0.140 |

| Panel B: Market Leverage, all samples (14,806 observations) | ||||||||||

| βprof | −0.187 a | −0.244 a | −0.293 a | −0.346 a | −0.393 a | −0.392 a | −0.336 a | −0.148 a | 0.916 a | 0.123 a |

| (0.014) | (0.016) | (0.019) | (0.023) | (0.029) | (0.034) | (0.040) | (0.048) | (0.110) | (0.021) | |

| βtang | 0.045 a | 0.058 a | 0.071 a | 0.086 a | 0.064 a | 0.067 b | 0.068 b | 0.042 | 0.060 | −0.199 a |

| (0.011) | (0.012) | (0.014) | (0.017) | (0.022) | (0.026) | (0.030) | (0.036) | (0.082) | (0.028) | |

| βsize | 0.027 a | 0.037 a | 0.049 a | 0.062 a | 0.074 a | 0.083 a | 0.084 a | 0.064 a | −0.032 a | −0.019 a |

| (0.012) | (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | (0.002) | (0.003) | (0.007) | (0.002) | |

| βinv | −1.404 a | 0.070 a | 0.094 a | 0.143 a | 0.206 a | 0.261 a | 0.261 a | 0.274 a | 0.287 a | 0.412 a |

| (0.059) | (0.013) | (0.016) | (0.019) | (0.024) | (0.029) | (0.033) | (0.040) | (0.091) | (0.024) | |

| βdiv | −1.404 a | −1.811 a | −2.085 a | −2.381 a | −2.627 a | −2.613 a | −2.158 a | −1.588 a | −0.419 | −0.091 |

| (0.059) | (0.068) | (0.080) | (0.097) | (0.120) | (0.144) | (0.166) | (0.203) | (0.460) | (0.098) | |

| β0 | −0.313 a | −0.410 a | −0.524 a | −0.664 a | −0.775 a | −0.829 a | −0.764 a | −0.383 a | 1.127 a | 0.616 a |

| (0.013) | (0.014) | (0.017) | (0.021) | (0.026) | (0.030) | (0.035) | (0.043) | (0.098) | (0.032) | |

| R2 | 0.12 | 0.16 | 0.17 | 0.18 | 0.16 | 0.13 | 0.10 | 0.04 | 0.01 | 0.03 |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book leverage, All samples (14,806 observations) | ||||||||||

| βblev | 0.013 c | 0.010 b | 0.019 a | 0.022 a | 0.032 a | 0.037 a | 0.061 a | 0.080 a | 0.109 a | 0.018 a |

| (0.008) | (0.005) | (0.005) | (0.005) | (0.006) | (0.006) | (0.007) | (0.009) | (0.012) | (0.006) | |

| βprof | 0.244 a | 0.135 a | 0.123 a | 0.123 a | 0.108 a | 0.092 a | 0.102 a | 0.100 a | 0.134 a | 0.035 a |

| (0.018) | (0.012) | (0.012) | (0.013) | (0.013) | (0.015) | (0.018) | (0.022) | (0.029) | (0.011) | |

| βsize | −0.003 a | −0.003 a | −0.005 a | −0.006 a | −0.006 a | −0.005 a | −0.007 a | −0.007 a | −0.007 a | −0.017 a |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | |

| βdiv | −0.115 | −0.138 a | −0.161 a | −0.176 a | −0.255 a | −0.368 a | −0.480 a | −0.559 a | −0.624 a | −0.298 a |

| (0.072) | (0.047) | (0.046) | (0.050) | (0.005) | (0.059) | (0.071) | (0.088) | (0.114) | (0.048) | |

| β0 | 0.003 | 0.054 a | 0.096 a | 0.117 a | 0.157 a | 0.180 a | 0.233 a | 0.274 a | 0.328 a | 0.339 a |

| (0.015) | (0.010) | (0.010) | (0.010) | (0.011) | (0.012) | (0.015) | (0.018) | (0.024) | (0.015) | |

| R2 (%) | 1.35 | 1.01 | 0.94 | 0.65 | 0.78 | 0.75 | 1.02 | 0.98 | 0.89 | 2.30 |

| Panel B: Market leverage, all samples (14,806 observations) | ||||||||||

| βmlev | 0.003 | 0.007 b | 0.013 a | 0.016 a | 0.025 a | 0.031 a | 0.047 a | 0.063 a | 0.079 a | 0.020 a |

| (0.005) | (0.003) | (0.003) | (0.004) | (0.004) | (0.004) | (0.005) | (0.006) | (0.008) | (0.004) | |

| βprof | 0.231 a | 0.124 a | 0.103 a | 0.082 a | 0.073 a | 0.050 a | 0.035 b | 0.011 | 0.015 | 0.014 |

| (0.017) | (0.011) | (0.011) | (0.012) | (0.013) | (0.014) | (0.017) | (0.021) | (0.027) | (0.010) | |

| βsize | −0.003 c | −0.003 a | −0.004 a | −0.004 a | −0.005 a | −0.004 a | −0.006 a | −0.006 a | −0.004 a | −0.015 a |

| (0.072) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | |

| βdiv | 0.003 c | −0.137 a | −0.161 a | −0.172 a | −0.247 a | −0.355 a | −0.465 a | −0.539 a | −0.608 a | −0.292 a |

| (0.015) | (0.047) | (0.046) | (0.050) | (0.053) | (0.059) | (0.071) | (0.088) | (0.114) | (0.047) | |

| β0 | 0.003 | 0.053 a | 0.095 a | 0.116 a | 0.155 a | 0.177 a | 0.229 a | 0.268 a | 0.321 a | 0.321 a |

| (0.015) | (0.010) | (0.010) | (0.010) | (0.011) | (0.012) | (0.015) | (0.018) | (0.024) | (0.016) | |

| R2 (%) | 1.30 | 1.00 | 0.90 | 0.70 | 0.80 | 0.90 | 1.10 | 1.10 | 1.00 | 2.50 |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βprof | −0.264 a | −0.331 a | −0.374 a | −0.402 a | −0.452 a | −0.477 a | −0.531 a | −0.638 a | −0.734 a | −0.647 a |

| (0.029) | (0.033) | (0.034) | (0.034) | (0.036) | (0.036) | (0.037) | (0.042) | (0.047) | (0.024) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −0.525 a | −0.544 a | −0.566 a | −0.560 a | −0.572 a | −0.620 a | −0.658 a | −0.659 a | −0.818 a | −1.039 a |

| (0.046) | (0.039) | (0.037) | (0.036) | (0.037) | (0.039) | (0.040) | (0.041) | (0.049) | (0.034) | |

| Biggest size (5440 observations) | ||||||||||

| βprof | −1.248 a | −1.212 a | −1.179 a | −1.063 a | −1.017 a | −0.897 a | −0.772 a | −0.682 a | −0.744 a | −0.502 a |

| (0.062) | (0.052) | (0.046) | (0.043) | (0.040) | (0.036) | (0.033) | (0.033) | (0.041) | (0.025) | |

| Panel B: Market Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βprof | −0.118 a | −0.153 a | −0.173 a | −0.180 a | −0.202 a | −0.243 a | −0.245 a | −0.182 a | 4.777 a | 0.244 a |

| (0.013) | (0.015) | (0.017) | (0.020) | (0.024) | (0.032) | (0.050) | (0.078) | (0.465) | (0.035) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −0.118 a | −0.153 a | −0.173 a | −0.180 a | −0.202 a | −0.243 a | −0.245 a | −0.182 a | 4.777 a | 0.244 a |

| (0.013) | (0.015) | (0.017) | (0.020) | (0.024) | (0.032) | (0.050) | (0.078) | (0.465) | (0.035) | |

| Panel C: Biggest size (5440 observations) | ||||||||||

| βprof | −1.120 a | −1.276 a | −1.354 a | −1.357 a | −1.172 a | −1.035 a | −0.845 a | −0.674 a | −0.119 a | −0.308 a |

| (0.044) | (0.049) | (0.055) | (0.058) | (0.060) | (0.062) | (0.064) | (0.075) | (0.135) | (0.038) | |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βprof | −0.198 a | −0.247 a | −0.287 a | −0.304 a | −0.360 a | −0.387 a | −0.437 a | −0.550 a | −0.669 a | −0.650 a |

| (0.030) | (0.033) | (0.035) | (0.035) | (0.036) | (0.036) | (0.038) | (0.043) | (0.049) | (0.024) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −0.364 a | −0.397 a | −0.434 a | −0.427 a | −0.443 a | −0.499 a | −0.538 a | −0.557 a | −0.744 a | −1.045 a |

| (0.047) | (0.041) | (0.038) | (0.037) | (0.038) | (0.040) | (0.042) | (0.043) | (0.051) | (0.035) | |

| Biggest size (5440 observations) | ||||||||||

| βprof | −0.882 a | −0.881 a | −0.889 a | −0.813 a | −0.797 a | −0.722 a | −0.629 a | −0.578 a | −0.671 a | −0.466 a |

| (0.068) | (0.058) | (0.051) | (0.047) | (0.044) | (0.040) | (0.036) | (0.036) | (0.045) | (0.025) | |

| Panel B: Market Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βprof | −0.081 a | −0.105 a | −0.121 a | −0.120 a | −0.139 a | −0.174 a | −0.166 a | −0.128 a | 4.431 a | 0.233 a |

| (0.013) | (0.015) | (0.017) | (0.020) | (0.024) | (0.032) | (0.051) | (0.080) | (0.479) | (0.035) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −0.081 a | −0.105 a | −0.121 a | −0.120 a | −0.139 a | −0.174 a | −0.166 a | −0.128 a | 4.431 a | 0.157 a |

| (0.013) | (0.015) | (0.017) | (0.020) | (0.024) | (0.032) | (0.051) | (0.080) | (0.479) | (0.038) | |

| Panel C: Biggest size (5440 observations) | ||||||||||

| βprof | −0.711 a | −0.862 a | −0.901 a | −0.921 a | −0.773 a | −0.682 a | −0.541 a | −0.381 a | 0.178 a | −0.211 a |

| (0.047) | (0.053) | (0.060) | (0.064) | (0.066) | (0.069) | (0.071) | (0.084) | (0.151) | (0.039) | |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: The first model | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βtang | −0.016 | 0.066 c | 0.109 a | 0.071 c | 0.077 b | 0.120 a | 0.198 a | 0.262 a | 0.374 a | 0.275 a |

| (0.031) | (0.035) | (0.036) | (0.037) | (0.038) | (0.038) | (0.040) | (0.045) | (0.051) | (0.041) | |

| Medium size (4,895 observations) | ||||||||||

| βtang | 0.148 a | 0.068 a | 0.041 | 0.021 | −0.004 | −0.032 | −0.029 | −0.012 | 0.057 | −0.147 a |

| (0.035) | (0.031) | (0.028) | (0.028) | (0.028) | (0.029) | (0.031) | (0.032) | (0.038) | (0.043) | |

| Biggest size (5440 observations) | ||||||||||

| βtang | −0.009 | −0.099 a | −0.158 a | −0.166 a | −0.180 a | −0.151 a | −0.125 a | −0.099 a | −0.039 c | −0.173 a |

| (0.035) | (0.029) | (0.026) | (0.024) | (0.022) | (0.020) | (0.018) | (0.018) | (0.023) | (0.025) | |

| Panel B: The second model | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βtang | −0.034 | 0.440 | 0.085 b | 0.044 | 0.052 | 0.096 b | 0.173 a | 0.238 a | 0.357 a | 0.277 a |

| (0.031) | (0.035) | (0.036) | (0.036) | (0.038) | (0.038) | (0.039) | (0.045) | (0.051) | (0.041) | |

| Medium size (4895 observations) | ||||||||||

| βtang | 0.116 a | 0.040 | 0.015 | −0.005 | −0.029 | −0.055 c | −0.052 c | −0.032 | 0.043 | −0.146 b |

| (0.035) | (0.030) | (0.028) | (0.027) | (0.028) | (0.029) | (0.031) | (0.032) | (0.038) | (0.043) | |

| Biggest size (5440 observations) | ||||||||||

| βtang | −0.044 | −0.131 a | −0.185 a | −0.191 a | −0.201 a | −0.168 a | −0.139 a | −0.106 a | −0.046 b | −0.178 a |

| (0.034) | (0.029) | (0.025) | (0.023) | (0.022) | (0.020) | (0.018) | (0.018) | (0.023) | (0.025) | |

| Coefficient | Quantiles | Fixed Effect Regression | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | ||

| Panel A: Book Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βdiv | −1.253 a | −1.586 a | −1.656 a | −1.849 a | −1.739 a | −1.700 a | −1.774 a | −1.662 a | −1.226 a | 0.135 |

| (0.136) | (0.153) | (0.161) | (0.162) | (0.167) | (0.167) | (0.175) | (0.197) | (0.224) | (0.126) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −2.192 a | −1.998 a | −1.804 a | −1.812 a | −1.574 a | −1.652 a | −1.637 a | −1.397 a | −1.009 a | 0.171 |

| (0.196) | (0.169) | (0.158) | (0.155) | (0.158) | (0.166) | (0.174) | (0.178) | (0.212) | (0.158) | |

| Biggest size (5440 observations) | ||||||||||

| βprof | −2.913 a | −2.637 a | −2.301 a | −1.994 a | −1.751 a | −1.389 a | −1.137 a | −0.823 a | −0.582 a | −0.492 a |

| (0.249) | (0.211) | (0.186) | (0.172) | (0.162) | (0.146) | (0.133) | (0.029) | (0.036) | (0.100) | |

| Panel B: Market Leverage | ||||||||||

| Smallest size (4471 observations) | ||||||||||

| βprof | −0.702 a | −0.917 a | −0.986 a | −1.137 a | −1.181 a | −1.291 a | −1.494 a | −1.019 a | 6.547 a | 0.532 a |

| (0.061) | (0.068) | (0.078) | (0.092) | (0.112) | (0.149) | (0.235) | (0.371) | (2.212) | (0.179) | |

| Medium size (4895 observations) | ||||||||||

| βprof | −1.587 a | −1.674 a | −1.863 a | −2.098 a | −2.139 a | −2.131 a | −1.746 a | −1.198 a | 0.766 | −0.009 |

| (0.102) | (0.112) | (0.124) | (0.143) | (0.168) | (0.206) | (0.232) | (0.304) | (0.581) | (0.170) | |

| Panel C: Biggest size (5440 observations) | ||||||||||

| βprof | −3.252 a | −3.292 a | −3.608 a | −3.466 a | −3.177 a | −2.184 a | −2.424 a | −2.337 a | −2.373 a | −1.337 a |

| (0.174) | (0.193) | (0.218) | (0.233) | (0.240) | (0.251) | (0.259) | (0.305) | (0.550) | (0.153) | |

| Quantiles | F-Statistic (p Value) | ||

|---|---|---|---|

| The First Model | The Second Model | The Third Model | |

| 0.1 versus 0.2 | chi2 (4) = 36.98 Prob > chi2 = 0.0000 | chi2 (5) = 48.88 Prob > chi2 = 0.0000 | chi2 (4) = 82.13 Prob > chi2 = 0.0000 |

| 0.2 versus 0.3 | chi2 (4) = 25.40 Prob > chi2 = 0.0000 | chi2 (5) = 25.51 Prob > chi2 = 0.0001 | chi2 (4) = 21.41 Prob > chi2 = 0.0003 |

| 0.3 versus 0.4 | chi2 (4) = 2.70 Prob > chi2 = 0.6087 | chi2 (5) = 8.48 Prob > chi2 = 0.1316 | chi2 (4) = 17.36 Prob > chi2 = 0.0016 |

| 0.4 versus 0.5 | chi2 (4) = 7.56 Prob > chi2 = 0.1092 | chi2 (5) = 8.55 Prob > chi2 = 0.1282 | chi2 (4) = 30.43 Prob > chi2 = 0.0000 |

| 0.5 versus 0.6 | chi2 (4) = 19.00 Prob > chi2 = 0.0008 | chi2 (5) = 28.29 Prob > chi2 = 0.0000 | chi2 (4) = 37.44 Prob > chi2 = 0.0000 |

| 0.6 versus 0.7 | chi2 (4) = 48.60 Prob > chi2 = 0.0000 | chi2 (5) = 64.15 Prob > chi2 = 0.0000 | chi2 (4) = 44.84 Prob > chi2 = 0.0000 |

| 0.7 versus 0.8 | chi2 (4) = 173.84 Prob > chi2 = 0.0000 | chi2 (5) = 198.82 Prob > chi2 = 0.0000 | chi2 (4) = 23.53 Prob > chi2 = 0.0001 |

| 0.8 versus 0.9 | chi2 (4) = 320.66 Prob > chi2 = 0.0000 | chi2 (5) = 349.57 Prob > chi2 = 0.0000 | chi2 (4) = 11.53 Prob > chi2 = 0.0212 |

| Quantiles | The First Model | The Second Model | The Third Model |

|---|---|---|---|

| 0.1 versus 0.2 | chi2 (4) = 201.79 Prob > chi2 = 0.0000 | chi2 (5) = 254.70 Prob > chi2 = 0.0000 | chi2 (4) = 82.43 Prob > chi2 = 0.0000 |

| 0.2 versus 0.3 | chi2 (4) = 220.87 Prob > chi2 = 0.0000 | chi2 (5) = 244.66 Prob > chi2 = 0.0000 | chi2 (4) = 23.25 Prob > chi2 = 0.0001 |

| 0.3 versus 0.4 | chi2 (4) = 256.90 Prob > chi2 = 0.0000 | chi2 (5) = 279.11 Prob > chi2 = 0.0000 | chi2 (4) = 11.24 Prob > chi2 = 0.0240 |

| 0.4 versus 0.5 | chi2 (4) = 142.25 Prob > chi2 = 0.0000 | chi2 (5) = 153.02 Prob > chi2 = 0.0000 | chi2 (4) = 27.00 Prob > chi2 = 0.0000 |

| 0.5 versus 0.6 | chi2 (4) = 52.72 Prob > chi2 = 0.0000 | chi2 (5) = 52.74 Prob > chi2 = 0.0000 | chi2 (4) = 29.78 Prob > chi2 = 0.0000 |

| 0.6 versus 0.7 | chi2 (4) = 17.38 Prob > chi2 = 0.0016 | chi2 (5) = 36.14 Prob > chi2 = 0.0000 | chi2 (4) = 48.57 Prob > chi2 = 0.0000 |

| 0.7 versus 0.8 | chi2 (4) = 155.26 Prob > chi2 = 0.0000 | chi2 (5) = 173.58 Prob > chi2 = 0.0000 | chi2 (4) = 19.23 Prob > chi2 = 0.0007 |

| 0.8 versus 0.9 | chi2 (4) = 527.63 Prob > chi2 = 0.0000 | chi2 (5) = 539.02 Prob > chi2 = 0.0000 | chi2 (4) = 12.45 Prob > chi2 = 0.0143 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nguyen, H.M.; Vuong, T.H.G.; Nguyen, T.H.; Wu, Y.-C.; Wong, W.-K. Sustainability of Both Pecking Order and Trade-Off Theories in Chinese Manufacturing Firms. Sustainability 2020, 12, 3883. https://doi.org/10.3390/su12093883

Nguyen HM, Vuong THG, Nguyen TH, Wu Y-C, Wong W-K. Sustainability of Both Pecking Order and Trade-Off Theories in Chinese Manufacturing Firms. Sustainability. 2020; 12(9):3883. https://doi.org/10.3390/su12093883

Chicago/Turabian StyleNguyen, Huu Manh, Thi Huong Giang Vuong, Thi Huong Nguyen, Yang-Che Wu, and Wing-Keung Wong. 2020. "Sustainability of Both Pecking Order and Trade-Off Theories in Chinese Manufacturing Firms" Sustainability 12, no. 9: 3883. https://doi.org/10.3390/su12093883

APA StyleNguyen, H. M., Vuong, T. H. G., Nguyen, T. H., Wu, Y.-C., & Wong, W.-K. (2020). Sustainability of Both Pecking Order and Trade-Off Theories in Chinese Manufacturing Firms. Sustainability, 12(9), 3883. https://doi.org/10.3390/su12093883