1. Introduction

Just like any organization, every country has an objective to attain economic development. As such, countries undertake projects that will boost economic development. According to a report by The United Nations Economic Commission for Africa (UNECA) [

1], industrialization is one way of improving development in Africa. Industrialization focuses on expanding activities in the manufacturing sector, which calls for high financial and technological investment [

2]. Considering the limited funds available to undertake these expansionary activities in the continent, most countries fall on foreign direct investments to bridge the gap [

3]. Foreign direct investment, which is an investment made by a non-resident to have a controlling interest in the management of an organization has, therefore, become crucial in the running of developing economies, especially with the help of globalization [

2].

Foreign direct investment in Africa has been rising in recent decades. During 2014, Africa had a 65% proportion of foreign direct investments (FDIs). Between 2014 and 2015, FDIs on the continent rose by 40% [

4]. In 2018, although there was a global fall in FDIs, Africa experienced an approximate 11% increase in total FDI inflows compared to the previous year [

5,

6]. According to Globerman et al., in 2015 Africa recorded a 6% rise in the number of foreign companies established compared to the 2014 value of 495 companies [

7]. FDIs have out-performed other external financing sources such as official development assistance (ODA) in developing economies in which Africa cannot be exempted [

7]. FDI is preferred over other capital inflows because there is low risk of fluctuation shocks, which makes it more stable [

8]. The United Nations Sustainable Development Goals (UNSDG) for Africa recommended the need for African economies to attract a significant amount of foreign direct investment (FDI) to improve growth through investment in important development infrastructure. African countries are performing poorly compared to their peers in terms of infrastructure. Being predominantly agricultural economies, it would mean that these African countries must work to expand their economy if they want to achieve Sustainable Development Goal 8 of achieving GDP growth of 8% [

9].

There are many benefits attributed to FDI, which include job creation, technology transfer, capital formation, and higher export [

10]. FDI inflow in the continent has also contributed to the steady economic growth the continent has experienced [

7]. An increase in FDI will enable the continent in the attainment of the Sustainable Development Goal by 2030 [

10]. According to the United Nations Conference on Trade and Development (UNCTAD), FDI causes forward and backward linkages where multinational companies employ input resources from local firms, therefore improving domestic firm performance and efficiency [

5]. According to Appiah-Kubi et al. [

11], one of the significant prerequisites for improvement is the capacity to draw in foreign direct investment that can help with building development infrastructural facilities fit for upgrading sustainable development. FDI includes the preparation of investment funds from foreign investors for the host economy. This might be as a move of possession from local to remote financial investors or as an extension in productive limit and capital development in a nation. Therefore, it may likewise have suggestions for ownership, since local financial investors may need to yield corporate governance of businesses to outside investors. FDI gives a chance for speculators to expand their portfolio in this way, enhancing the harmony between risk and return [

11].

Several researchers have established the importance of external development and political issues in determining the level of FDI. External developments mentioned in this study include good roads, quality electricity, and better broadcast communications infrastructures like telecommunications [

10]. In their study, Dupasquier et al. found that FDI is very responsive to these external factors [

4]. UNCTAD and Chuhan et al. also confirmed the results of Dupasquier et al. that the availability of roads, electricity, and other external conditions in a country are major determinants of FDI [

4,

5,

6]. Institutionalization of an efficient judiciary also improves the level of FDI [

7].

However, corporate governance practices in organizations will also help improve information asymmetry between foreign investors and the host country [

12]. Due to this, corporate governance practices should be considered in exploring drivers of FDI. Good corporate governance eliminates adverse selection and moral hazards [

13]. Domestic firms may communicate only good investment opportunities to foreign investors but hide information when it is in their self-interest. This causes an agency problem in running business operations [

14]. Foreign investors are also aware that hidden information may exist that affects a high rate of return or causes firms to refuse to invest at all. Instituting good corporate governance ensures that information is well distributed and that resources are matched with potential investment, therefore mitigating conflict between the two parties [

8].

Based on the above, this study examines the relationship between corporate governance and Foreign Direct Investment in Africa, specifically in West Africa. Though there has been little research on FDI and corporate governance, Johnson as well as Love and Klapper conclude that good corporate governance results in high levels of FDI; their studies were conducted in developed economies where the corporate governance practices differ significantly from developing countries [

12,

13]. Considering the difference in structures, it would be an error to generalize findings to that effect. Again, the study concentrates on West Africa because regions within Africa have attained different levels of development and therefore attract unequal FDIs. In order to avoid distortion of results, we chose to conduct the study on regional bases, which effectively groups countries with similar characteristics.

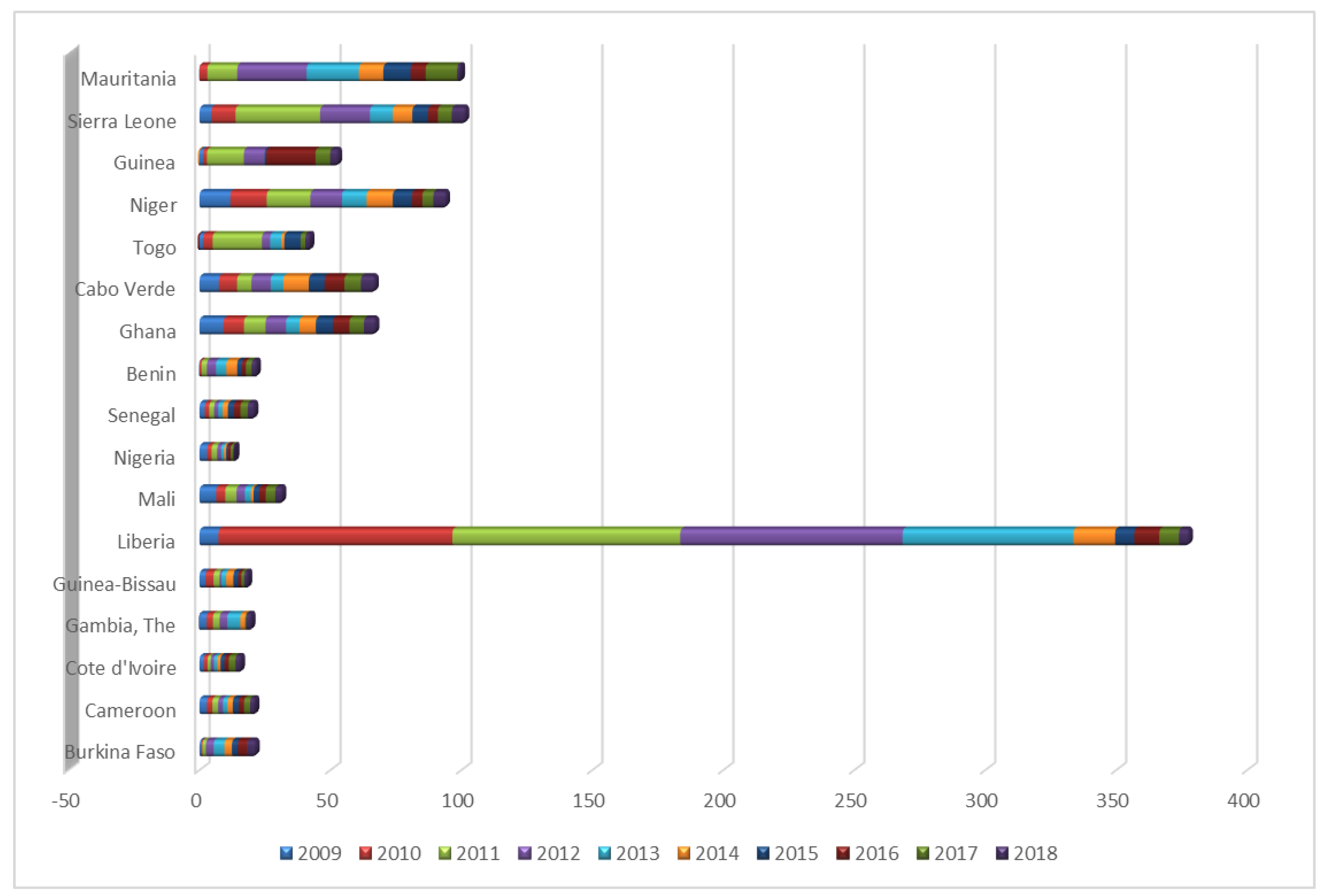

Generally, West Africa has recorded a trend of increasing FDIs over the years. Regardless, because of specific country effects, it can be observed from

Figure 1 that there have been irregularities in the trends across nations. The figures below give a pictorial view of the FDI trends of 17 sampled countries for this study from 2009 to 2018. These West African countries were Benin, Burkina Faso, Cape Verde, Cameroon, Cote D’Ivoire, Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali, Mauritania, Nigeria, Niger, Senegal, Sierra Leone, and Togo. The vertical axes present FDI ratios plotted against the years of focus and countries on the horizontal axes. Equatorial Guinea is not included in the study due to the unavailability of data.

2. Literature Review and Research Questions

Empirical literature has discussed different determinants of FDI, and findings differ depending on the economy type and sampled countries. For instance, Saini and Singhania compared the factors that affect the level of FDI for both developed and developing countries employing a dynamic panel generalized method of moments (GMM) [

15]. The study found that determinants in developed countries are more policy-related, but developing-country factors are basically economic factors. Addison and Heshmati also used GMM to assess the effect that institution quality has on FDI inflows in Vietnam [

16]. The findings confirm that indeed institutional quality positively impacts the level of FDI, but the effect differs across provinces.

Appiah-Kubi et al. studied the impact of macroeconomic variables on the inflows of foreign direct investment in the least developed West African countries using a dynamic panel generalized method of moments (GMM) of 13 countries from 2000 to 2014. The authors found out that infrastructure development has a positive impact on the inflow of FDI to the least developed West African nations [

11].

Manuel and Roberto argued the need for policies to make FDI more effective in enhancing domestic investment in developing countries [

17]. The authors used empirical estimation and testing with panel data of the period 1971–2000 to examine the extent to which FDI in developing countries crowds in or crowds out domestic investment. The authors reveal that impacts of FDI on household investment are in no way, shape, or form constantly ideal, that oversimplified arrangements towards FDI are probably not going to be ideal, and, preeminently, that more consideration should be paid to financial approaches that encourage total domestic investment [

17].

Agosin and Machado investigated the impact of poor governance quality on FDI in Russia by using a business survey across 40 administrative districts and estimation techniques of one-stage and two-stage instrumental variables [

18]. The authors found that a higher frequency of illegal payments and higher pressure from regulatory agencies, enforcement authorities, and criminals have significantly negative effects on FDI. The authors also confirmed that the moving of governance quality from the average to the top across Russian regions more than doubles the FDI stock [

18].

Barrel and Nahhas [

19] in their paper also discussed the factors affecting bilateral foreign direct investment (FDI) stocks from 14 high-income countries to 31 OECD countries over the period 1995–2015 employing the generalized method of moments (GMM) estimator to a gravity model of bilateral FDI stocks. Their findings suggested that EU membership is a significant determinant of FDI and that European Integration has a large effect on FDI stocks [

19].

Anghel also argued that countries whose governments are highly ranked according to various indices of the quality of institutions tend to do better in attracting foreign direct investment [

20]. In an empirical analysis of cross-section data by applying estimation methods of ordinary least squares and instrumental variables, the author finds that different aspects of the quality of institutions in a country (corruption, protection of property rights, policies related to opening a business and maintaining it, etc.) are almost always significant in attracting FDI [

20].

According to Bissoon, control of corruption, better rule of law, political stability, and better freedom of expression of the media are used as indicators of good governance and institutional quality [

21]. The author’s paper empirically studied the impact of institutional quality on FDI in 45 developing countries in Africa, Latin America, and Asia from 1996 to 2005. By using the OLS estimation, results show that the quality of some institutions in the host country have a significantly large effect on inward FDI. Although different indicators of institutional quality are complementary to each other, their combined effect is found to reinforce the level of FDI inflows to the host country.

Gradually, good corporate governance is becoming a focus when it comes to the factors informing the degree of FDI as multinationals and investors at large in recent times look out for these structures before taking decisions [

22]. This has therefore seemingly rendered traditional determinants of FDI such as natural resource availability, infrastructure quality, market availability and labor cost, somewhat obsolete factors or secondary as compared to good corporate governance [

23,

24]. However, the link between corporate governance and FDI, especially at the national level, has been discussed in empirical literature only to a limited extent.

A few studies such as Globerman and Shapiro, Biglaiser and DeRouen, Gani, and Lee et al. have scientifically supported the idea of good corporate governance improving FDI inflows [

25,

26,

27,

28]. The predominant view is that economies characterized by means of a generally excellent corporate governance will in general pull in more prominent foreign direct investment [

7,

25]. This is on the ground that foreign investors accept that their investments cannot be protected in a financial framework described by poor corporate governance frameworks [

25]. Jones and Pollitt contend that corporate disappointment is universally an outcome of the disintegration of corporate governance in economies, and thus the building of corporate governance structures in nations is crucial for organization sustenance and in the long run protecting the interests of foreign financial specialists [

29]. Although there has been a competitive business condition where rivalry has become a fundamental piece of nation risk analysis process, natural resources alone cannot serve as a motivation for foreign financial investors to stream capital into a specific economy. As a result, African researchers are putting forth an attempt to look at the other main thrusts behind the inflow of foreign direct investment in West African economies [

11].

Based on

Figure 2 below, it can be observed that the inflowing FDI in Africa is highest in the West African region. Unfortunately, studies on the impact that corporate governance has on the inflows of FDI in West African countries as a whole do not exist. However, the West African region has always recorded the highest inflows of FDI for the period 2009 to 2018. It became imperative for us to do a critical study, and thus it became the foundation of our research to determine the corporate structures that determine the inflows of FDI in West Africa. The Materials and Methods section of this paper describes how the secondary research was conducted as well as the model specification. The Results and Discussion section presents the results obtained, and discussion and comparison of the results of own research with similar studies in the context of the issue are conducted. Finally, conclusion, policy implications, and direction for future research on the topic is discussed.

The agency problem existing between majority and minority shareholders’ interests still prevails and remains unresolved [

30]. Reputable researchers in the area of corporate governance report that corporate governance protects the interest of minority shareholders in economies where legal systems are partial towards this class of stockholders [

31,

32,

33]. Increasingly, countries are instituting good corporate governance structures with codes of conduct to protect minority interests [

34]. These codes place both majority and minority interest on the same scale in terms of civil rights. La Porta et al. confirm that the ability for countries to attract FDIs from investors is highly contingent on how minority interest is protected or safeguarded [

35]. Likewise, McLean et al. among others posit that any economy that has systems in place to protect minority interest tends to attract a lot of foreign investors [

36,

37]. Kim et al. maintain that protecting minority shareholders’ interest has a positive impact on FDI inflows [

38]. The USA government is more generous in investing when a nation strongly has the minority shareholders’ interest at heart compared to those who just regard majority interests [

39]. The studies referenced above show how relevant minority shareholders’ interest is in the quest of exploring investment funding in any economy. The above informs the first research question of this study, which is:

Q1: Does minority shareholders’ interest protection attract FDI inflows in West Africa?

Ethical principles cannot be overlooked in attracting FDI inflows to economies, specifically developing ones. Fair and ethical dealings with stakeholders at large is established as relevant in increasing FDI inflows [

40]. This implies that foreign investors look out for economies whose companies’ conduct business ethically. Bardy et al. argue that companies that are involved in opportunistic activities expose themselves to attack from civil groups, non-governmental agencies, and others [

41]. These activities do not make companies attractive to foreign investors, thus affecting the level of FDI. It is therefore believed that economies practicing ethics attract more foreign investment. Valdes and Foster also confirm that countries with organizations that follow codes of standards and practice responsible business are considered to attract more FDI into their respective economies [

42]. Therefore, the second research question is:

Q2: Do highly ethical firms boost FDIs in West African countries?

According to Miletkov et al. [

43], the existence of independent boards of directors increases the probability for a country to attract FDIs. This therefore encourages organizations in forming their councils and committees [

43]. Miletkov et al. also emphasize how effective governance sends positive signals to foreign investors that the economy will do well [

43]. The study further states that institutional foreign investors are optimistic about their investment given the presence of an effective board to oversee managers [

43]. Considering the weak nature of protection institutions in Africa, the existence of effective boards becomes necessary in attracting FDIs [

44]. The above motivates the third research question:

Q3: Does the existence of working corporate boards attract FDIs in West Africa?

Effectiveness of securities and trading regulations influence the degree of FDIs in an economy. This implies that financial assets traded on the stock exchange should be autonomous and independent from political influences [

44]. Agyemang et al. concluded that investors are not willing to direct funds to economies exhibiting interference in the implementation of regulations [

45]. Securities and exchanges are supposed to go about their activities in a professional manner in order to heighten investors’ confidence [

46]. This implies that ensuring independent dealing in regulations motivates and boosts confidence of foreign investors to invest in economies. This leads to the final research question:

Q4: Does establishment and implementation of regulations in securities exchanges impact the degree of FDI in West African countries?

4. Discussion and Results

Table 1 below illustrates our descriptive analysis of our research of the selected West African countries from 2009 to 2018. The mean recorded for FDI for our selected West African nations during the period under consideration was 6.6%. This implies that African nations draw a low amount of FDI compared to other parts of the world. Our result is affirmed by the investigation by Bokpin et al. [

53], which recorded a mean FDI of 5% in the period 1996–2011. The mean for the level of protection of minority shareholders’ interests in our examined countries from 2009 to 2018 was 3.7 on a scale of 1 to 7, with standard deviation of 0.7 and maximum and minimum of 2.0 and 6.3, which implies that the evaluated average is low and the degree of assurance of the interests of minority investors of our selected West African countries recorded moderately adequate results. The mean value of ethical behavior of companies from our selected West African countries from 2009 to 2018 was 3.5 based on a scale of 1 to 7, with a standard deviation of 0.6 and a scope of 2.0 to 5.0. This implies that the degree of moral conduct of firms in our West African nations is moderately adequate.

As regards the effectiveness of corporate boards in our selected West African countries during our study, their mean based on the scale of 1 to 7 was 4.1, which means that our chosen West African countries are characterized by successful corporate boards of directors. Relatively, this result confirms the work of Agyemang et al. [

33] and Romano [

54], which shows that, as a result of weak institutions for the protection of investors’ rights in emerging countries, councils play the significant role of governance systems that stimulates confidence of foreign investors. Securities regulation recorded an average value of 3.3 on a scale of 1 to 7, with a variability level of 0.4 and a maximum and minimum of 2.5 and 4.5, implying that our selected West African countries show a relatively satisfactory result.

Last but not least, in relation to control variables, the average credit score, gross domestic product, inflation, and electricity quality averaged 22.5%, $1155.7, 6.6%, and 2.5, respectively (on a scale of 1 to 7).

Table 2 below shows the correlation matrix among our variables. According to

Table 2, we recorded a positive correlation between ethical behavior of firms, security of minority shareholders’ interests, effectiveness of corporate boards, quality of electricity, and inflation with the level of inflows of FDI in our examined West African countries. On the other hand, we recorded a negative relationship between the effectiveness of regulation of securities exchanges, credit ratings score, and GDP per capita on the inflows of foreign direct investment into our selected West African countries. The extent of the relationships among the explanatory variables is satisfactory, meaning that multicollinearity was not a significant issue. Moreover, the connection among the explanatory variables falls within the limit of 0.9 (90 percent) as recommended by Romano [

54].

Table 3 below shows and discusses the results of our empirical estimates. As already mentioned, our results were based on how the selected West African countries’ levels of governance structures play a vital role in attracting inflows of foreign direct investments (FDIs) and thus help us to answer our formulated questions using the dynamic panel generated model of moments (GMM). It should be noted that the number of observations in

Table 1 and

Table 3 is different as the extreme values were omitted from the regression analysis as explained by Arellano and Bover [

52]. There is a significant debate on missing variables in models, and this is summarized in Baltagi et al. [

49].

We are now approaching the presentation of our results related to our formulated research questions. Based on the GMM regression (

Table 3), our outcome recorded a noteworthy positive connection between the degree of minority shareholders’ interest (PIM) and FDI in our selected West African countries. This outcome affirms the primary formulated research question (Q1) of our examination: Does minority shareholders’ interest protection attract FDI inflows in West Africa? This is on the grounds that foreign investors are worried about amplifying their profitability, and they are similarly worried about how the host economy shields its interests. Scholars have contended that when an economy is precarious and unable to ensure the interests of minority shareholders, it discourages foreign investors from directing their extreme assets to such an economy as foreign direct ventures [

11,

22]. In addition to this, economies that seek strategies that ensure more noteworthy assurance for minority shareholders result in lower capital expenses and effectively raise support [

27]. Our outcome was consistent with other studies [

24,

28,

39,

55] showing that West African nations that guarantee the security of the interests of shareholders, particularly minorities, draw in a more significant level of FDI.

In addition to this, our results show a noteworthy positive connection between ethical behaviors of countries’ businesses (EBF) and the degree of FDI inflows into our selected West African countries. This outcome affirms our subsequent research question (Q2) on whether the extent of profoundly ethical local firms assists West African countries in attracting the inflows of foreign direct investments. Empirically speaking, West African countries that give high premiums to their local organizations to act ethically have the advantage of a progressively higher increase of the inflows of foreign direct investment. Although economic writings have of late centered mostly on the role of institutional structures at the nation level in guaranteeing the strength of foreign proprietorship [

37], in a seriously competitive business condition, business ethics could assume a crucial role in pulling in foreign direct investments. The ongoing worldwide money-related emergency connected to different company scandals has featured the significance of ethical, monetary, and accounting reporting codes and standards to guarantee that companies are being fair and transparent, which forestalls extortion and improves the confidence of investors. This outcome affirms the discoveries that economies described by firms to adhere to codes and ethics and stick to dependable strategic approaches are viewed as significant resources that help pull in foreign direct investment into West African countries [

24,

33].

Furthermore, our investigation recorded a noteworthy positive connection between the efficiency of corporate administration (ECB) and the degree of FDI in our chosen West African nations. This outcome answers the third inquiry (Q3) of this examination of whether the presence of a successful corporate administration can assist with drawing in more FDI to an economy. This implies that when business councils from the West African countries are viable, the degree of foreign direct interest in these countries expands. Most West African nations have discovered these principles and regulations; however, enforcing requirement is dangerous [

24,

37,

48]. One result of this is the availability of a strong company’s board of directors (BODs) that helps to build investors’ trust in these countries. This is on the grounds that most investors accept that their investments would be safe with the successful guidance of effective and efficient executives [

50]. This finding affirms the discoveries that foreign investors are prepared to direct their assets or stretch out their investments to nations characterized by powerful corporate administration [

24,

34,

56].

Moreover, our study uncovered a negative connection between the level of foreign direct investment and effectiveness of securities and conversion standard regulation (ERSE) for our selected West African countries. This result was surprising as it conflicted with our last inquiry (Q4), which was whether the adequacy of securities and foreign trade regulations in general influence the degree of FDI in an economy. This outcome might be a result of political obstruction in the definition, execution, and assessment of securities and trade regulations. Securities and exchanges are relied upon to be free and self-governing, without any type of political obstruction in the satisfaction of their commitments by the administrations of West African countries [

53]. In this way, economies characterized by steady political impedance in the activities of forex and securities exchanges have a likelihood to pull in low foreign investments [

11]. One can imagine that our selected West African economies are characterized by unjustified administrative weights, capricious arrangements, and an absence of responsibility with respect to their legislatures [

53]. These events, therefore, reduce investor confidence in economies, which ultimately reduces the degree of foreign direct interest in the selected West African countries. This was consistent with the study by Lee et al. [

24]

Finally, the lag of FDI and gross domestic product (GDP) reported a negative but statistically significant relationship with the inflows of FDI to West African countries. The significance of the lag variable confirms that it is an important instrumental variable as suggested by Barrell and Nahhas [

19]. However, the negative relationship deviates from the existing literature. It can be explained that a negative relationship indicates no persistence in FDI inflows to West African countries. Countries that have high GDP are seen to be developed and as such have little or no investment opportunities. However, low GDP countries are viewed as countries with potential, since there are a lot of investment avenues to explore. Along these lines, the assumption that supports the approach toward FDI in most developing nations including West Africa is that a liberal arrangement toward multinational enterprises (MNEs) is adequate to guarantee constructive effects suggested by Agosin and Machado [

17]. The inflation and level of a country’s credit scores (CCR) demonstrated a negative relationship with FDI. This was consistent with the study by Appiah-Kubi et al. [

11]. The quality of electricity (QES) showed a positive relationship with FDI. However, these variables are insignificant in determining the level of FDI in West African countries. This conflicts with the examination of Smutka, Pawlak, Kotyza, and Svatoš [

57].

5. Conclusions and Recommendations

The objective of the paper was to ascertain a correlation between corporate governance structures at a country level and FDI in West Africa countries via the estimation technique of difference dynamic panel generalized method of moments (GMM). This study was carried out for 17 West African countries from 2009 to 2018. Our outcomes show that economies displaying ethical firms will in general pull in more FDI. Empirically speaking, West African countries that give high premiums to their local organizations to act ethically have the advantage of progressively higher increase of the inflows of foreign direct investment. The ongoing worldwide money-related emergency connected to different companies’ scandals has featured the significance of ethical, monetary, and accounting codes and standards to guarantee companies are being fair and transparent, which forestalls extortion and improves confidence of investors. Furthermore, our outcomes show that when the boards of organizations in the economy are successful in managing, this adds to a significant increase of FDI inflows into the economy. This implies that when business councils from the West African countries are viable, the degree of foreign direct investment in these countries expands. Most West African nations have discovered these principles and regulations; however, enforcing requirement is dangerous. One result of this is the availability of strong boards of directors that help to build investors’ trust in these countries. This is on the grounds that most investors accept that, with successful guidance of effective and efficient executives, their investments would be safe. The discoveries further show that economies displaying solid minority shareholders’ interest protection will in general draw in more foreign direct investment. This is because foreign investors are worried about amplifying their profitability; they are similarly worried about how the host economy shields its interests. Scholars have contended that when an economy is precarious and unable to ensure the interests of minority shareholders, it discourages foreign investors from directing their extreme assets to such an economy as foreign direct ventures. Be that as it may, our examination uncovers the insignificant link between effectiveness of securities and stock exchange regulation on the inflows of FDI. This outcome can be ascribed to political impedance in the detailing, execution, and assessment of securities and stock trade regulations.

Concerning political ramifications, the outcomes unequivocally propose that dependence on nation-level corporate governance structures by West African countries can make a landmass that will draw in important foreign direct investment for financial development. We recommend the setting up of practical corporate governance structures in African economies without political mediation to accomplish the objective of utilizing foreign direct investment to mitigate poverty by 2025 under the Millennium Development Goals. The accompanying explicit measures are proposed to African economies. First, West African countries should provide a guarantee that proper implementation measures are set up to ensure that the privileges of minority shareholders can be accomplished by fortifying the institutional structures in their economies. Second, West African nations should endeavor to urge domestic organizations to work ethically through the required foundation of morals and consistence units in associations. Third, they should guarantee the alleviation of approach impedance in the detailing and usage of corporate regulations. Moreover, African economies should publicly introduce and supply guidelines, policies, administrative formalities, and preferential treatments in provinces through means of communication (televisions, radios, newspapers, et cetera). Lastly, African countries should periodically hold economic forums to collect foreign investors’ ideas and economic experts’ policy implications for attracting FDI inflows.

Despite the useful findings, there were some limitations to our results, which must be dealt with to improve future research in this area. The first limitation was a lack of long-term longitudinal data in the sample of the West African countries. This has been a common problem with several studies on developing countries, which highlights the need for more extensive, better-quality data on such economies. Future research should take into consideration incidence of corruption and freedom of the press of our sampled West African countries when establishing the relationship between corporate governance and FDI. This may limit the reliability of our results. To overcome this issue, similar studies can expand our model to include both incidence of corruption and freedom of the press.

,

,

{kind=link}

{kind=link}