Business Models Addressing Sustainability Challenges—Towards a New Research Agenda

Abstract

1. Introduction

2. Conceptual Background

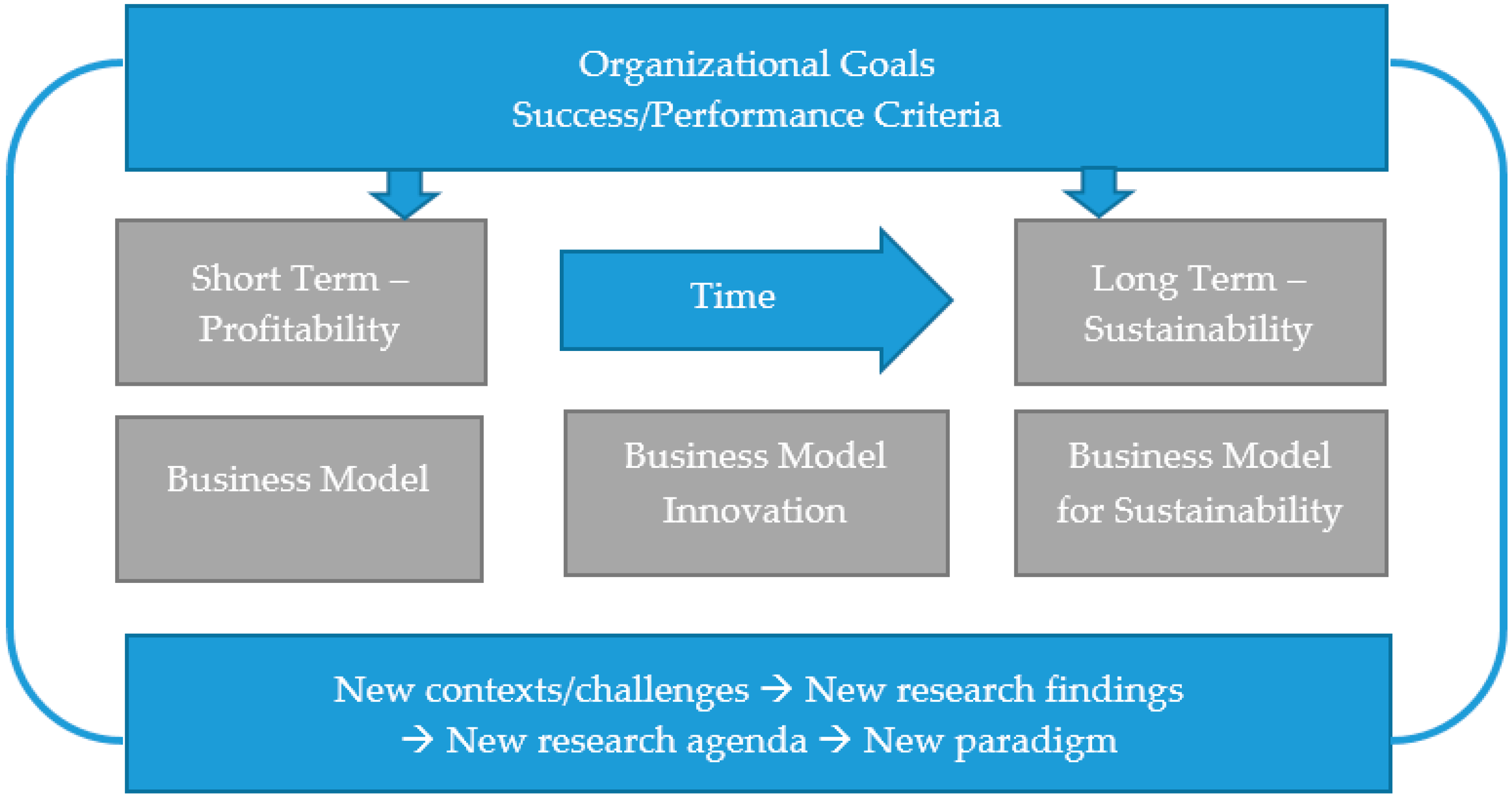

2.1. Dynamics of Organizational Goals—From Profitability to Sustainability

2.2. Bringing Organizational Goals to Life—The Role of the Business Model (Innovation)

2.3. Adding the Sustainability Dimension to the Business Model (Innovation)

3. Methodology

4. Results

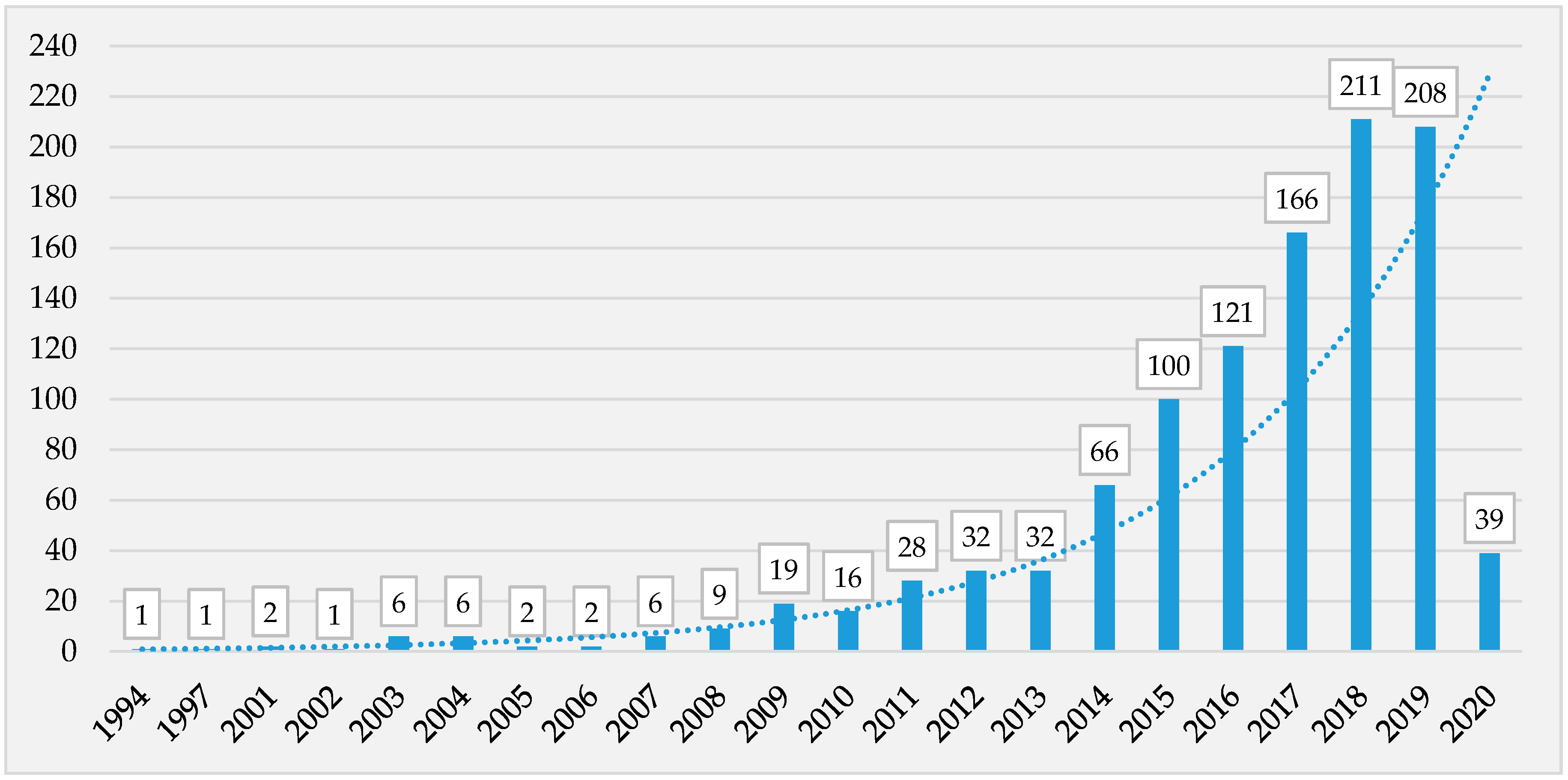

4.1. Bibliometric Analysis

- Document types (and their respective number of records—higher than “total results”, as some of them belong to more than one category): Article (733), Proceedings Paper (274), Review (65), Book Chapter (44), Editorial Material (17), Early Access (16), and Meeting Abstract (1);

- Top 10 WoS categories (and their respective numbers of records): Green Sustainable Science Technology (274), Environmental Sciences (265), Management (233), Business (192), Environmental Studies (169), Engineering Environmental (136), Engineering Industrial (68), Economics (58), Engineering Manufacturing (53), and Computer Science Information Systems (47);

- Top five source titles (and their respective numbers of records): Journal of Cleaner Production (111), Sustainability (95), Procedia CIRP (28), Business Strategy and the Environment (19), and IFIP Advances in Information and Communication Technology (11);

- Top five authors (and their respective number of records): Evans, Steve (19); Bocken, Nancy M.P. (17) / Bocken, Nancy (8), Ludeke-Freund, Florian (14), McAloone, Tim (7), Pedersen, Esben R.G., Pigosso, Daniela, C.A., and Rana, Padmakshi (6);

- Citation report: Average citations per item—12.44; sum of times cited—13362 (11105 without self-citation); citing articles—8760 (8311 without self-citation).

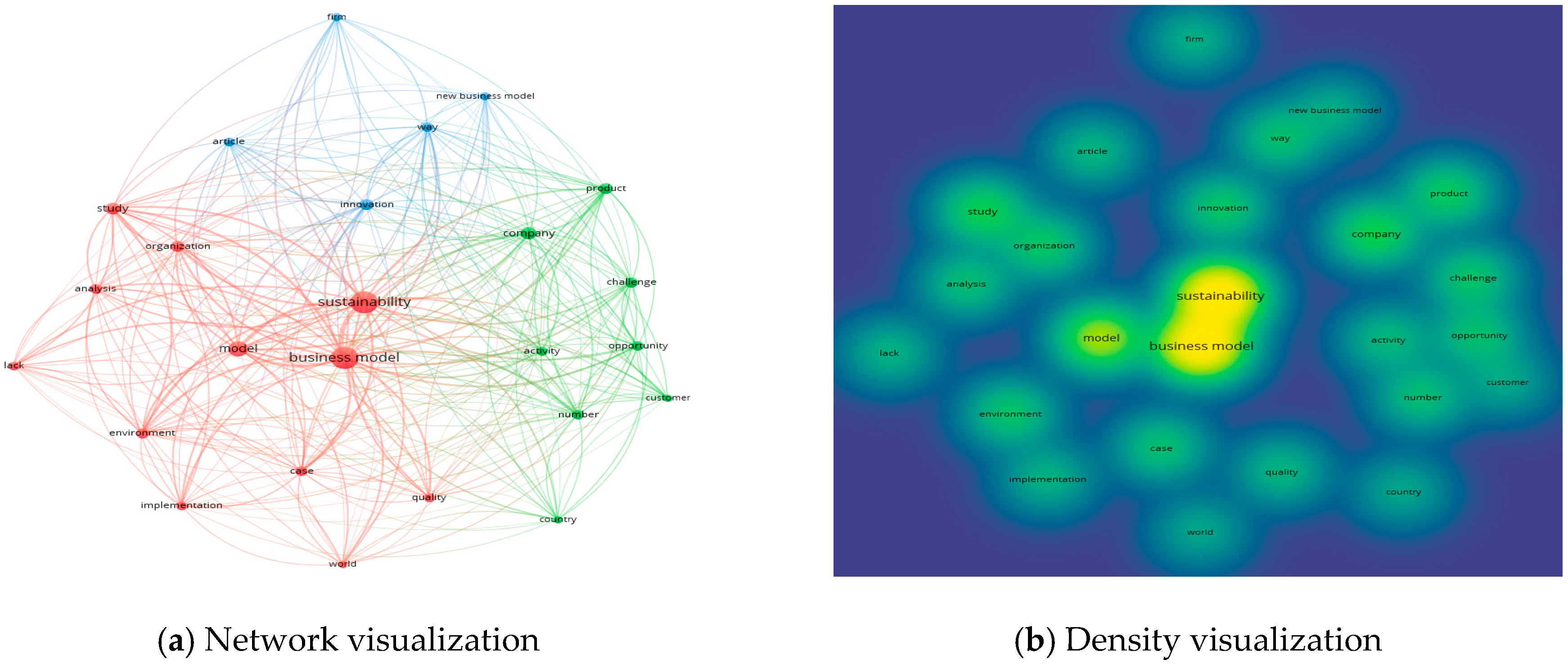

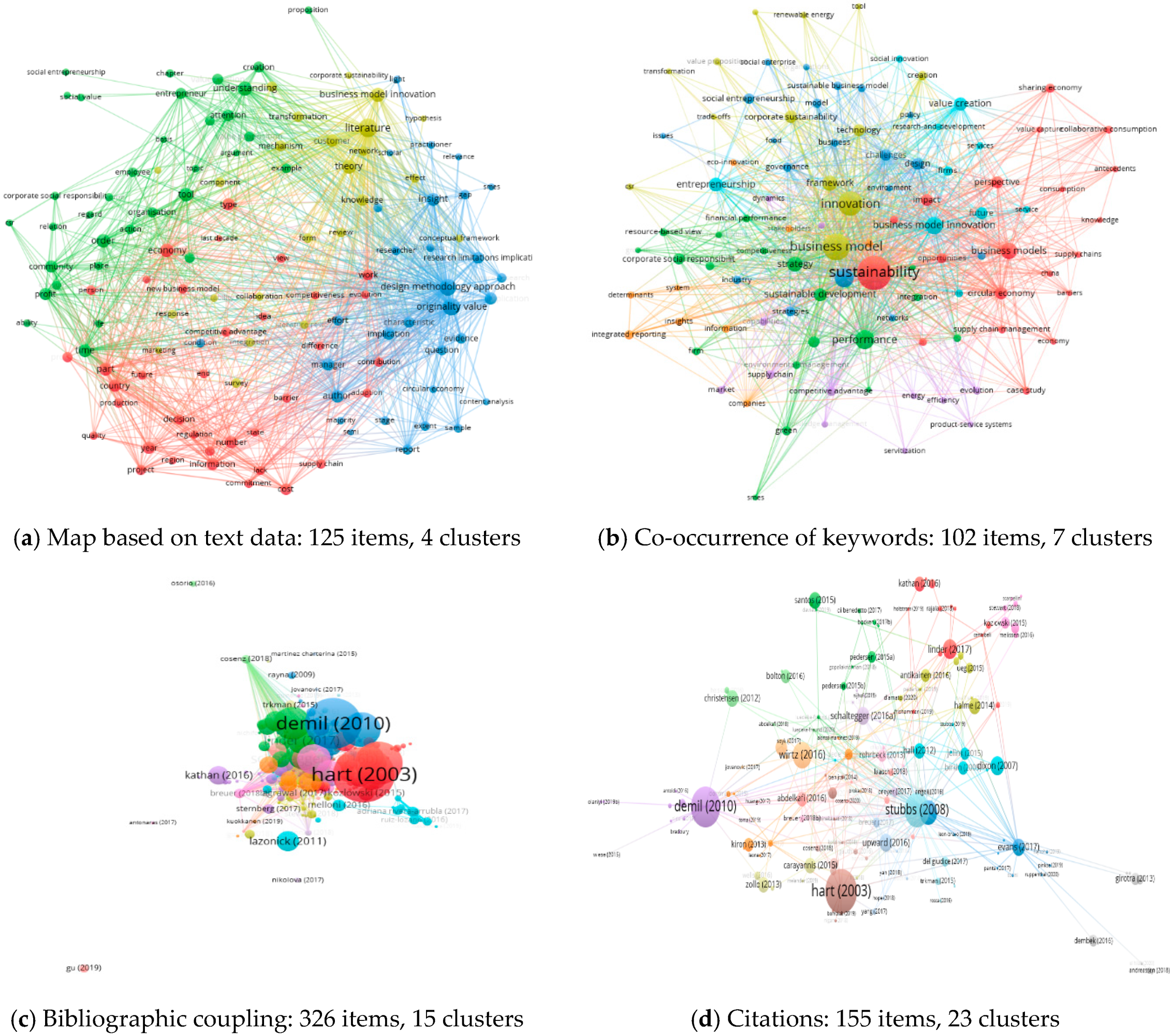

- Cluster 1 (12 items): Analysis, business model, case, environment, implementation, lack, model, organization, quality, study, sustainability, world;

- Cluster 2 (8 items): Activity, challenge, company, country, customer, number, opportunity, product;

- Cluster 3 (5 items): Article, firm, innovation, new business model, way.

- Cluster 1 (31 items): Action, activity, application, author, context, country, demand, economy, end, enterprise, example, factor, field, future research, gap, interest, knowledge, lack, number, operation, opportunity, platform, principle, relation, researcher, sample, survey, sustainable development, time, tool, user;

- Cluster 2 (23 items): Addition, attention, business model innovation, case study, characteristic, customer, element, firm, implication, importance, influence, literature, need, new business model, relationship, review, service, stakeholder, sustainable business model, theory, type, value creation, value proposition;

- Cluster 3 (19 items): Actor, barrier, challenge, circular business model, circular economy, consumption, design methodology approach, driver, interview, literature review, manager, methodology, originality value, product, product service system, production, supply chain, transition, understanding.

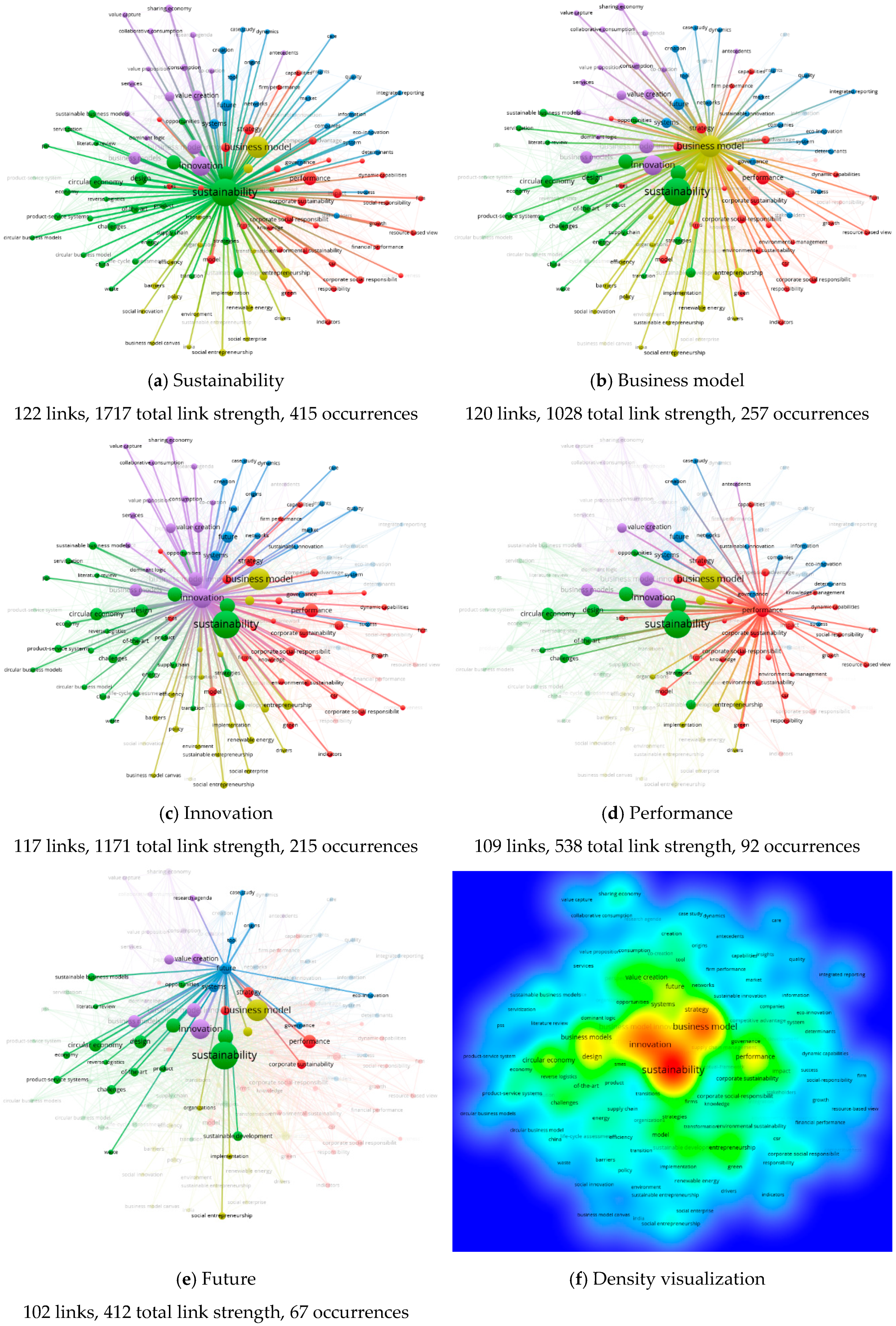

- Cluster 1 (157 items): Platform (718), program (495), effectiveness (456), consequence (434), long term (391), connection (388), vision (372), trust (363), decision making (355), emergence (349), new approach (336), cooperation (316), feasibility (285), diffusion (277), recycling (258), flexibility (261), transparency (284), bmi (243);

- Cluster 2 (152 items): Sustainable business model (1104), firm (1072), sustainable development (742) enterprise (766), business model innovation (891), value creation (681), circular economy (580), value proposition (513), product service system (432), environmental impact (419), competitive advantage (389), partnership (384), corporate social responsibility (335), business models (344), environmental sustainability (300), competitiveness (299), circular business model (266), profitability (249), reporting (223), business model canvas (222), corporate sustainability (209), social value (208), social enterprise (185), csr (183), business case (177), sustainable innovation (171), social entrepreneurship (154), sustainability performance (153), sustainable business model innovation (152), climate change (153), financial performance (150), sustainable business (150), current business model (143), triple bottom line (139), integrated reporting (138), circularity (134), sustainable business models (132), energy efficiency (132), business model concept (129), environmental performance (127), sustainable development goal (124), value capture (122), tension (121), sustainability issue (120), best practice (120), social sustainability (118), sustainability transition (117), traditional business mode (116), economic value (107), economic performance (105), environmental value (113), negative impact (110), sustainable value (104), business model perspective (104), positive impact (103);

- Cluster 3 (53 items): Investment (663), infrastructure (609), report (594), financial sustainability (267), mission (233), adaptation (190), social impact (146), business sustainability (142), key stakeholder (129), long term sustainability (108), digitalization (100).

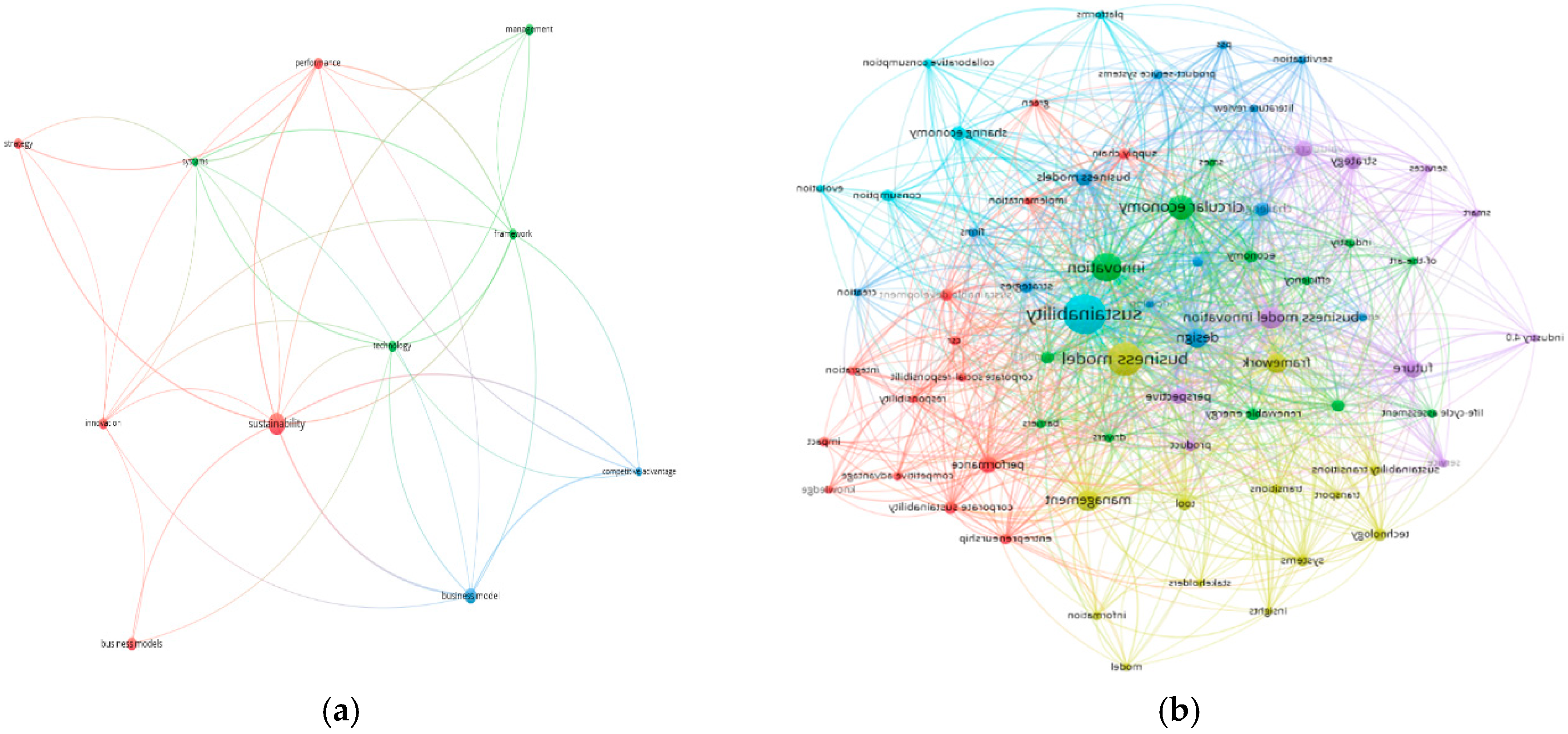

- For the 1994–2013 time span (163 records): 11 items were grouped into 3 clusters: Cluster 1 (five items): Business models, innovation, performance, strategy, sustainability; Cluster 2 (four items): Framework, management, systems, technology; Cluster 3 (two items): Business model, competitive advantage; in terms of total link strength, the ranking of the 11 items is: Sustainability, performance, business model, framework, technology, competitive advantage, systems, innovation, strategy, management, business models.

- In 2019 (208 records): 69 items were grouped into six clusters: Cluster 1 (14 items): Competitive advantage, corporate social responsibility, corporate sustainability, csr, entrepreneurship, green, impact, implementation, integration, knowledge, performance, responsibility, supply chain, sustainable development; Cluster 2 (13 items): Barriers, circular economy, drivers, economy, efficiency, industry, innovation, life-cycle assessment, of-the-art, opportunities, renewable energy, smes, sustainable business model; Cluster 3 (13 items): Business models, challenges, creation, design, develop, energy, firms, literature review, product-service systems, pss, servitization, strategies, sustainable business models; Cluster 4 (13 items): Business model, framework, information, insights, management, model, stakeholders, sustainability transitions, systems, technology, tool, transitions, transport; Cluster 5 (10 items): Business model innovation, future, industry 4.0, perspective, product, service, services, smart, strategy, value creation; Cluster 6 (six items): Collaborative consumption, consumption, evolution, platforms, sharing economy, sustainability; in terms of total link strength, the ranking of the top 10 items is: Sustainability, business model, innovation, circular economy, business model innovation, design, framework, management, future, perspective.

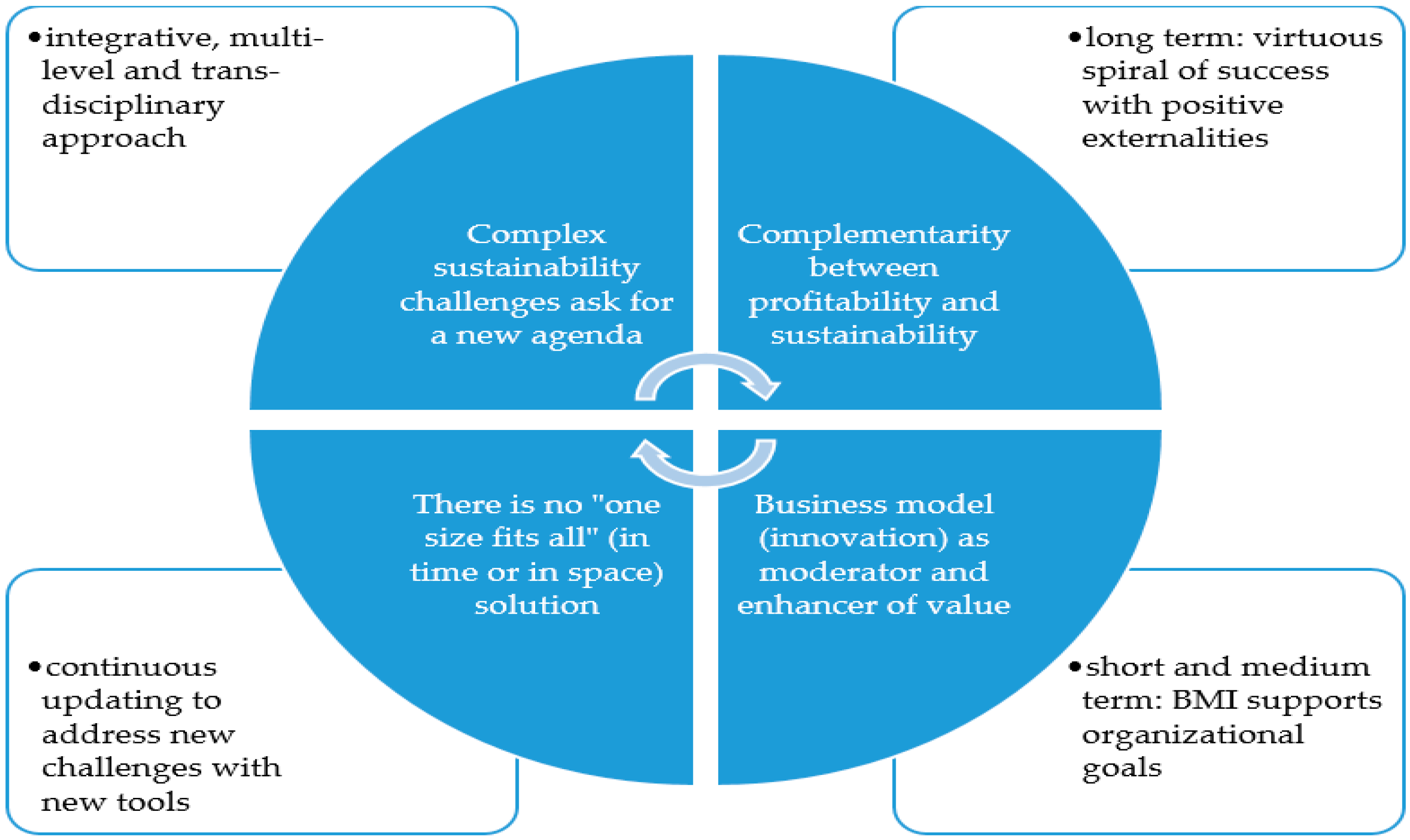

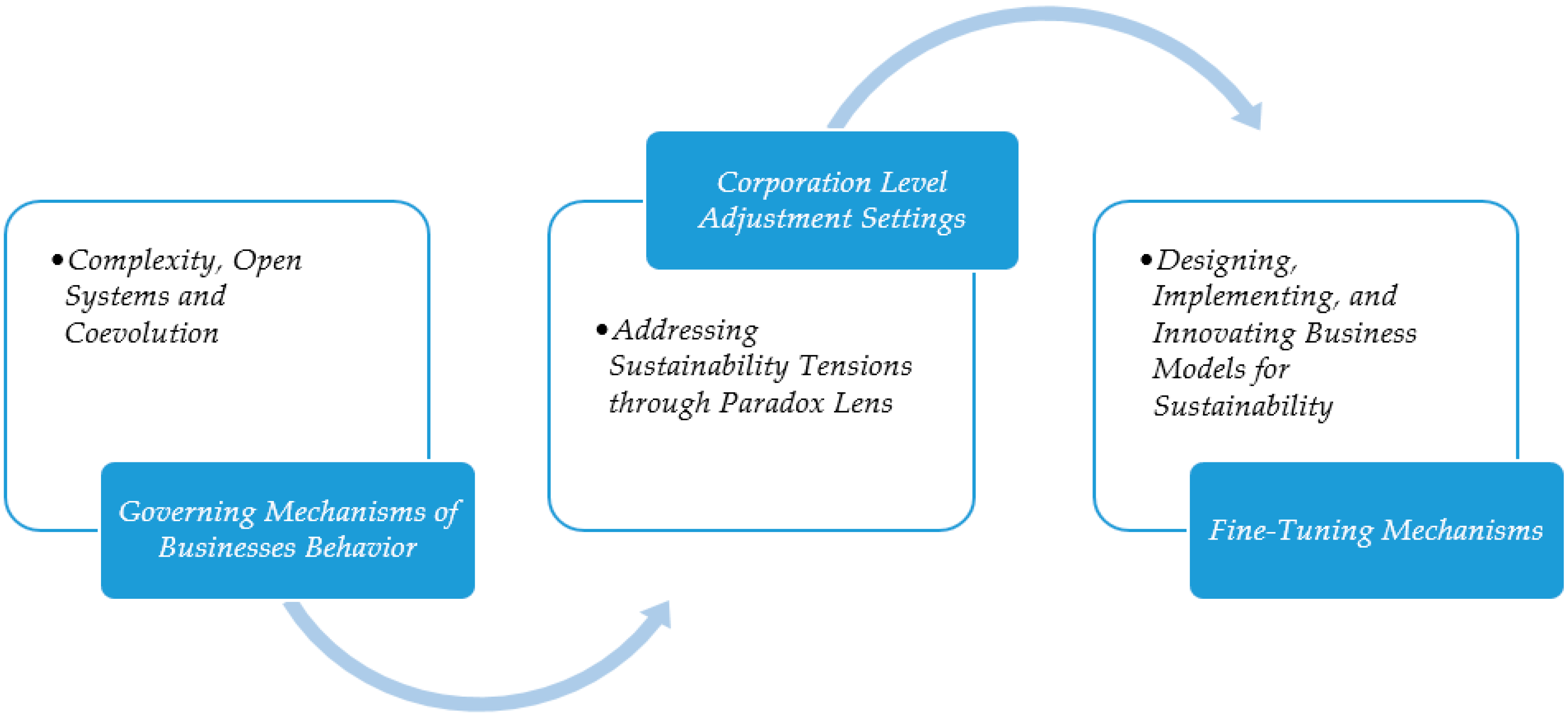

4.2. Guiding Lines for a New Approach at the Business Level and a New Research Agenda

4.2.1. Governing Mechanisms of Business Behavior—Complexity, Open Systems, and Coevolution

4.2.2. Corporation-Level Adjustment Settings—Addressing Sustainability Tensions through a Paradox Lens

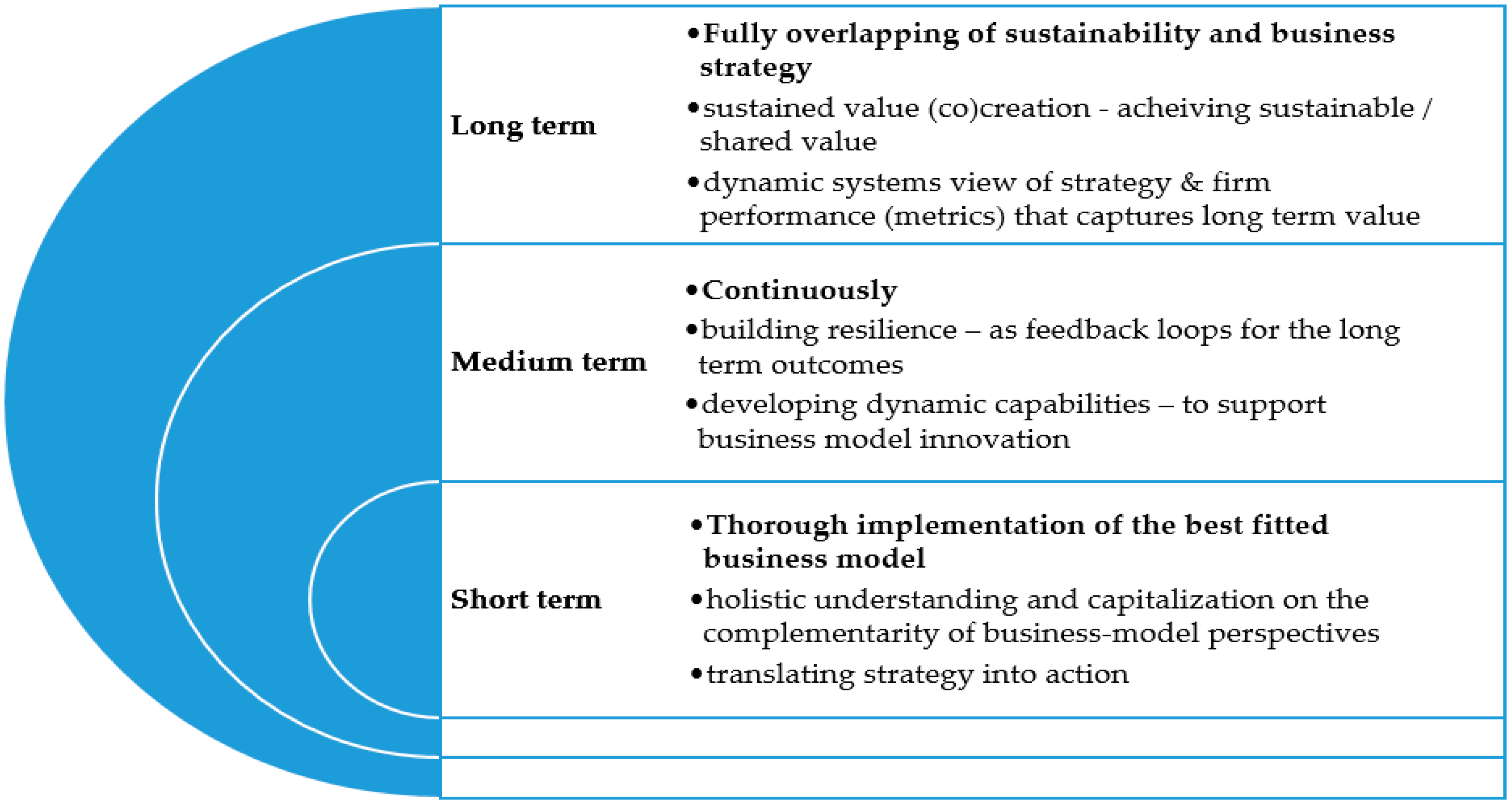

4.2.3. Fine-Tuning Mechanisms—Designing, Implementing, and Innovating Business Models for Sustainability

- Sustained value creation, which “relies on successfully shaping, adapting, and renewing the underlying business model of the company on a continuous basis” [117], and sustained value co-creation, which requires a company “to possess the capacity to structure its resource portfolios, including those of its collaborating partners (…), bundle the resources to create capabilities and leveraging/reconfiguring the capabilities to (efficiently) exploit market opportunities, and (flexibly) explore innovations for latent market demands” [118];

- Achieving “sustainable value—shareholder wealth that simultaneously drives us toward a more sustainable world” [119] or shared value, “which involves creating economic value in a way that also creates value for society by addressing its needs and challenge” [120], based on the “shared value creation framework” [54], able to generate myriads of opportunities in areas such as reconceiving products and markets, redefining productivity in the value chain, and enabling local cluster development [120];

- Adding the time dimension to the sustainable/shared value created—or “mainstreaming sustainability in strategy” [107]—which implies: (a) “A dynamic systems view of strategy (…where…) the firm’s outcomes are seen as part of a larger system of outcomes, and issues of sustainability and organizational viability over time become important”, and (b) “firm performance that captures long-term value (…namely…) a wider measure of firm performance (…) that can convey not only the firm’s profitability at a point in time, but also its sustainability over time” [107];

- Building resilience and developing dynamic capabilities as coping mechanisms able to connect the different time-level frames (upstream and downstream, respectively): (a) Resilience—“the capacity for an enterprise to survive, adapt, and grow in the face of turbulent change” [121]—will serve as precursor and enabler of sustainability while valorizing “dynamic, adaptive management rather than static optimization” [121]; (b) dynamic capabilities—“the firm’s ability to integrate, build, and reconfigure internal and external competences to address rapidly changing environments” [122]—will shape a company’s business model [46] while moderating its business model innovation capacity [49];

- Designing and implementing the most appropriate business model will crucially rely on managers’ ability to holistically understand and capitalize on the “complementarity of business-model perspectives” [49]: Business model activities (detailing the flow of value-adding processes); business model logics (detailing the consequence chain); business model archetypes (detailing overall approaches); business model elements (detailing the set of necessary parts); and business model alignment (detailing the connections between parts).

5. Discussion

Author Contributions

Funding

Conflicts of Interest

References

- Osterwalder, A.; Pigneur, Y.; Clark, T. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; Wiley: Hoboken, NJ, USA, 2010; ISBN 978-0-470-87641-1. [Google Scholar]

- Crane, A.; Matten, D. Business Ethics: Managing Corporate Citizenship and Sustainability in the Age of Globalization, 4th ed.; Oxford University Press: Oxford, UK, 2016; ISBN 978-0-19-969731-1. [Google Scholar]

- Gladwin, T.N.; Kennelly, J.J.; Krause, T.-S. Shifting paradigms for sustainable development: Implications for management theory and research. Acad. Manag. Rev. 1995, 20, 874–907. [Google Scholar] [CrossRef]

- Jia, Q.; Wei, L.; Li, X. Visualizing sustainability research in business and management (1990–2019) and emerging topics: A large-scale bibliometric analysis. Sustainability 2019, 11, 5596. [Google Scholar] [CrossRef]

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for sustainable development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Steger, U. The Business Case for Sustainability: Building Industry Cases for Corporate Sustainability; Palgrave Macmillan: Basingstoke, UK, 2004; ISBN 978-0-230-52447-7. [Google Scholar]

- Brønn, P.S.; Vidaver-Cohen, D. Corporate motives for social initiative: Legitimacy, sustainability, or the bottom line? J. Bus. Ethics 2009, 87, 91–109. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hörisch, J. In search of the dominant rationale in sustainability management: Legitimacy- or profit-seeking? J. Bus. Ethics 2017, 145, 259–276. [Google Scholar] [CrossRef]

- Wright, C.; Rwabizambuga, A. Institutional pressures, corporate reputation, and voluntary codes of conduct: An examination of the equator principles. Bus. Soc. Rev. 2006, 111, 89–117. [Google Scholar] [CrossRef]

- Perez-Batres, L.A.; Doh, J.P.; Miller, V.V.; Pisani, M.J. Stakeholder pressures as determinants of CSR strategic choice: Why do firms choose symbolic versus substantive self-regulatory codes of conduct? J. Bus. Ethics 2012, 110, 157–172. [Google Scholar] [CrossRef]

- Fowler, S.J.; Hope, C. Incorporating sustainable business practices into company strategy. Bus. Strategy Environ. 2007, 16, 26–38. [Google Scholar] [CrossRef]

- Gao, J.; Bansal, P. Instrumental and integrative logics in business sustainability. J. Bus. Ethics 2013, 112, 241–255. [Google Scholar] [CrossRef]

- Dyllick, T.; Muff, K. Clarifying the meaning of sustainable business: Introducing a typology from business-as-usual to true business sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Bernardo, M.; de Oliveira, O.J. Rethinking the way of doing business: A reframe of management structures for developing corporate sustainability. Sustainability 2020, 12, 1177. [Google Scholar] [CrossRef]

- Howard, A. A new global ethic. J. Manag. Dev. 2010, 29, 506–517. [Google Scholar] [CrossRef]

- Elkington, J. The 6 Ways Business Leaders Talk About Sustainability. Harv. Bus. Rev. 2017, 1–5. Available online: https://hbr.org/2017/10/the-6-ways-business-leaders-talk-about-sustainability?utm_medium=email&utm_source=newsletter_daily&utm_campaign=dailyalert&referral=00563&spMailingID=18302410&spUserID=OTY0OTMwNTk5NwS2&spJobID=1121123502&spReportId=MTEyMTEyMzUwMgS2 (accessed on 25 April 2020).

- Dentchev, N.; Baumgartner, R.; Dieleman, H.; Jóhannsdóttir, L.; Jonker, J.; Nyberg, T.; Rauter, R.; Rosano, M.; Snihur, Y.; Tang, X.; et al. Embracing the variety of sustainable business models: Social entrepreneurship, corporate intrapreneurship, creativity, innovation, and other approaches to sustainability challenges. J. Clean. Prod. 2016, 113, 1–4. [Google Scholar] [CrossRef]

- Jørgensen, S.; Pedersen, L.J.T. RESTART Sustainable Business Model Innovation; Palgrave studies in sustainable business in association with Future Earth; Palgrave Macmillan: Cham, Switzerland, 2018; ISBN 978-3-319-91971-3. [Google Scholar]

- Nosratabadi, S.; Mosavi, A.; Shamshirband, S.; Kazimieras Zavadskas, E.; Rakotonirainy, A.; Chau, K.W. Sustainable business models: A review. Sustainability 2019, 11, 1663. [Google Scholar] [CrossRef]

- Kennedy, S.; Bocken, N. Innovating business models for sustainability: An essential practice for responsible managers. In The Research Handbook of Responsible Management; Edward Elgar: Cheltenham, UK, 2020. [Google Scholar]

- Eells, R. Social responsibility: Can business survive the challenge? Bus. Horiz. 1959, 2, 33–41. [Google Scholar] [CrossRef]

- Tisdale, E.W. Modern Man and the Natural Environment. Natl. Forum 1963, 43, 32. [Google Scholar]

- Friedman, M. Capitalism and Freedom; University of Chicago Press: Chicago, IL, USA, 1962. [Google Scholar]

- Clifton, C.; Hershey, H.F. “Maximizing Shareholder Value”: A theory run amok. i-Manag. J. Manag. 2016, 10, 45. [Google Scholar] [CrossRef]

- Mackey, J.; Friedman, M.; Rodgers, T.J. Rethinking the social responsibility of business. J. Reason 2005, 10, 15–17. [Google Scholar]

- Waddock, S.A.; Bodwell, C.; Graves, S.B. Responsibility: The new business imperative. Acad. Manag. Perspect. 2002, 16, 132–148. [Google Scholar] [CrossRef]

- Visser, W. The age of responsibility: CSR 2.0 and the new DNA of business. J. Bus. Syst. Gov. Ethics 2010, 5, 7–22. [Google Scholar] [CrossRef]

- Lubin, D.A.; Esty, D.C. The sustainability imperative. Harv. Bus. Rev. 2010, 88, 4–50. [Google Scholar]

- Bergman, M.; Bergman, Z.; Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 2017, 9, 753. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: A literature review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- van Marrewijk, M. Multiple levels of corporate sustainability. J. Bus. Ethics 2003, 44, 107–119. [Google Scholar] [CrossRef]

- Kiron, D.; Kruschwitz, N.; Haanaes, K.; von Streng Velken, I. Sustainability nears a tipping point. MIT Sloan Rev. 2012, 53, 69–74. [Google Scholar] [CrossRef]

- Chen, B. Moral and ethical foundations for sustainability: A multi-disciplinary approach. J. Glob. Citizsh. Equity Educ. 2012, 2, 1–20. [Google Scholar]

- Elms, H.; Brammer, S.; Harris, J.D.; Phillips, R.A. New Directions in Strategic Management and Business Ethics. Bus. Ethics Q. 2010, 20, 401–425. [Google Scholar] [CrossRef]

- Frederick, R. Global Business Ethics. In International Encyclopedia of Ethics; Lafollette, H., Ed.; Blackwell Publishing Ltd: Oxford, UK, 2013; p. 453. ISBN 978-1-4051-8641-4. [Google Scholar]

- Bonn, I.; Fisher, J. Sustainability: The missing ingredient in strategy. J. Bus. Strategy 2011, 32, 5–14. [Google Scholar] [CrossRef]

- Laszlo, C.; Zhexembayeva, N. Embedded Sustainability: The Next Big competitive Advantage, 1st ed.; Routledge: London, UK, 2017; ISBN 978-1-351-27832-4. [Google Scholar]

- Hawkins, D.E. Corporate Social Responsibility Balancing Tomorrow’s Sustainability and Today’s Profitability; Palgrave Macmillan: New York, NY, USA, 2009; ISBN 978-0-230-62581-5. [Google Scholar]

- Salzmann, O.; Ionescu-somers, A.; Steger, U. The Business Case for Corporate Sustainability. Eur. Manag. J. 2005, 23, 27–36. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Lozano, R. Towards better embedding sustainability into companies’ systems: An analysis of voluntary corporate initiatives. J. Clean. Prod. 2012, 25, 14–26. [Google Scholar] [CrossRef]

- Sneirson, J.F. Green is good: Sustainability, profitability, and a new paradigm for corporate governance. Iowa Rev. 2008, 94, 987–1022. [Google Scholar]

- Du, W.; Pan, S.L.; Zuo, M. How to Balance Sustainability and Profitability in Technology Organizations: An Ambidextrous Perspective. IEEE Trans. Eng. Manag. 2013, 60, 366–385. [Google Scholar] [CrossRef]

- Rodriguez-Fernandez, M. Social responsibility and financial performance: The role of good corporate governance. BRQ Bus. Res. Q. 2016, 19, 137–151. [Google Scholar] [CrossRef]

- DaSilva, C.M.; Trkman, P. Business Model: What It Is and What It Is Not. Long Range Plan. 2014, 47, 379–389. [Google Scholar] [CrossRef]

- Magretta, J. Why business models matter. Harv. Bus. Rev. 2002, 80, 86–92. [Google Scholar]

- Wirtz, B.W.; Pistoia, A.; Ullrich, S.; Göttel, V. Business Models: Origin, Development and Future Research Perspectives. Long Range Plann. 2016, 49, 36–54. [Google Scholar] [CrossRef]

- Ritter, T.; Lettl, C. The wider implications of business-model research. Long Range Plan. 2018, 51, 1–8. [Google Scholar] [CrossRef]

- Shafer, S.M.; Smith, H.J.; Linder, J.C. The power of business models. Bus. Horiz. 2005, 48, 199–207. [Google Scholar] [CrossRef]

- Casadesus-Masanell, R.; Ricart, J.E. From Strategy to Business Models and onto Tactics. Long Range Plan. 2010, 43, 195–215. [Google Scholar] [CrossRef]

- Zott, C.; Amit, R.; Massa, L. The Business Model: Recent Developments and Future Research. J. Manag. 2011, 37, 1019–1042. [Google Scholar] [CrossRef]

- Massa, L.; Tucci, C.L.; Afuah, A. A Critical Assessment of Business Model Research. Acad. Manag. Ann. 2017, 11, 73–104. [Google Scholar] [CrossRef]

- Rothärmel, F.T. Strategic Management, 4th ed.; McGraw-Hill Education: New York, NY, USA, 2018; ISBN 978-1-260-09237-0. [Google Scholar]

- Zott, C.; Amit, R. Business Model Design and the Performance of Entrepreneurial Firms. Organ. Sci. 2007, 18, 181–199. [Google Scholar] [CrossRef]

- Lambert, S.C.; Davidson, R.A. Applications of the business model in studies of enterprise success, innovation and classification: An analysis of empirical research from 1996 to 2010. Eur. Manag. J. 2013, 31, 668–681. [Google Scholar] [CrossRef]

- Afuah, A. Business Model Innovation: Concepts, Analysis, and Cases; Routledge: New York, NY, USA, 2014; ISBN 978-0-415-81739-4. [Google Scholar]

- Purkayastha, A.; Sharma, S. Gaining competitive advantage through the right business model: Analysis based on case studies. J. Strategy Manag. 2016, 9, 138–155. [Google Scholar] [CrossRef]

- D’Aveni, R.A.; Gunther, R.E. Hypercompetition: Managing the Dynamics of Strategic Maneuvering; The Free Press: New York, NY, USA, 1994; ISBN 978-1-4391-2263-1. [Google Scholar]

- Casadesus-Masanell, R.; Ricart, J.E. Competing through business models. In Handbook of Research on Competitive Strategy; Edward Elgar: Chelthenham, UK, 2012. [Google Scholar]

- Massa, L.; Tucci, C.L. Business model innovation. In The Oxford Handbook of Innovation Management; Oxford University Press: Oxford, UK, 2013; pp. 420–441. [Google Scholar]

- Chesbrough, H. Business Model innovation: Opportunities and barriers. Long Range Plan. 2010, 43, 354–363. [Google Scholar] [CrossRef]

- Christensen, C.M.; Bartman, T.; Van Bever, D. The hard truth about business model innovation. MIT Sloan Manag. Rev. 2016, 58, 31–40. [Google Scholar]

- Spieth, P.; Schneckenberg, D.; Ricart, J.E. Business model innovation—State of the art and future challenges for the field: State of art and future challenges. RD Manag. 2014, 44, 237–247. [Google Scholar] [CrossRef]

- Foss, N.J.; Saebi, T. Fifteen Years of Research on Business Model Innovation: How Far Have We Come, and Where Should We Go? J. Manag. 2017, 43, 200–227. [Google Scholar] [CrossRef]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.R. Why Sustainability Is Now the Key Driver of Innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Clark, T.; Charter, M. Sustainable innovation: Key conclusions from Sustainable Innovation Conferences 2003–2006 Organized by the Centre for Sustainable Design; The Centre for Sustainable Design, University College for the Creative Arts: Farnham, UK, 2007. [Google Scholar]

- Grigorescu, A.; Maer-Matei, M.M.; Mocanu, C.; Zamfir, A.-M. Key Drivers and Skills Needed for Innovative Companies Focused on Sustainability. Sustainability 2019, 12, 102. [Google Scholar] [CrossRef]

- Inigo, E.A.; Albareda, L.; Ritala, P. Business model innovation for sustainability: Exploring evolutionary and radical approaches through dynamic capabilities. Ind. Innov. 2017, 24, 515–542. [Google Scholar] [CrossRef]

- Evans, S.; Vladimirova, D.; Holgado, M.; Van Fossen, K.; Yang, M.; Silva, E.A.; Barlow, C.Y. Business Model Innovation for Sustainability: Towards a Unified Perspective for Creation of Sustainable Business Models. Bus. Strategy Environ. 2017, 26, 597–608. [Google Scholar] [CrossRef]

- Stubbs, W.; Cocklin, C. Conceptualizing a “Sustainability Business Model”. Organ. Environ. 2008, 21, 103–127. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hansen, E.G.; Lüdeke-Freund, F. Business Models for Sustainability: Origins, Present Research, and Future Avenues. Organ. Environ. 2016, 29, 3–10. [Google Scholar] [CrossRef]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Carroux, S.; Joyce, A.; Massa, L.; Breuer, H. The sustainable business model pattern taxonomy—45 patterns to support sustainability-oriented business model innovation. Sustain. Prod. Consum. 2018, 15, 145–162. [Google Scholar] [CrossRef]

- Geissdoerfer, M.; Vladimirova, D.; Evans, S. Sustainable business model innovation: A review. J. Clean. Prod. 2018, 198, 401–416. [Google Scholar] [CrossRef]

- Saunders, M.N.K.; Lewis, P. Doing Research in Business and Management, 2nd ed.; Pearson: Harlow, UK, 2018; ISBN 978-1-292-13352-2. [Google Scholar]

- Barends, E.; Rousseau, D.M. Evidence-Based Management: How to Use Evidence to Make Better Organizational Decisions; Kogan Page Ltd: London, UK; New York, NY, USA, 2018; ISBN 978-0-7494-8374-6. [Google Scholar]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Zhang, X.; Estoque, R.C.; Xie, H.; Murayama, Y.; Ranagalage, M. Bibliometric analysis of highly cited articles on ecosystem services. PLoS ONE 2019, 14, e0210707. [Google Scholar] [CrossRef]

- Lang, D.J.; Wiek, A.; Bergmann, M.; Stauffacher, M.; Martens, P.; Moll, P.; Swilling, M.; Thomas, C.J. Transdisciplinary research in sustainability science: Practice, principles, and challenges. Sustain. Sci. 2012, 7, 25–43. [Google Scholar] [CrossRef]

- Petticrew, M.; Roberts, H. Systematic Reviews in the Social Sciences: A Practical Guide; Blackwell Pub: Malden, MA, USA; Oxford, UK, 2006; ISBN 978-1-4051-2110-1. [Google Scholar]

- van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. Visualizing Bibliometric Networks. In Measuring Scholarly Impact; Ding, Y., Rousseau, R., Wolfram, D., Eds.; Springer International Publishing: Cham, Switzerland, 2014; pp. 285–320. ISBN 978-3-319-10376-1. [Google Scholar]

- Martínez-López, F.J.; Merigó, J.M.; Gázquez-Abad, J.C.; Ruiz-Real, J.L. Industrial marketing management: Bibliometric overview since its foundation. Ind. Mark. Manag. 2020, 84, 19–38. [Google Scholar] [CrossRef]

- Castillo-Vergara, M.; Alvarez-Marin, A.; Placencio-Hidalgo, D. A bibliometric analysis of creativity in the field of business economics. J. Bus. Res. 2018, 85, 1–9. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. VOSviewer Manual; Leiden University: Leiden, The Netherlands, 2019. [Google Scholar]

- Saunders, M.N.K.; Lewis, P.; Thornhill, A. Research Methods for Business Students, 5th ed.; Prentice Hall: New York, NY, USA, 2009; ISBN 978-0-273-71686-0. [Google Scholar]

- Anderson, P. Perspective: Complexity theory and organization science. Organ. Sci. 1999, 10, 216–232. [Google Scholar] [CrossRef]

- Smith, W.K.; Lewis, M.W. Toward a Theory of Paradox: A Dynamic equilibrium Model of Organizing. Acad. Manag. Rev. 2011, 36, 381–403. [Google Scholar] [CrossRef]

- Gowdy, J.M. Coevolutionary Economics: The Economy, Society and the Environment; Springer: Dordrecht, The Netherlands, 1994; ISBN 978-90-481-5798-3. [Google Scholar]

- Kates, R.W. Environment and development: Sustainability science. Science 2001, 292, 641–642. [Google Scholar] [CrossRef]

- Homer-Dixon, T. Complexity Science. Oxf. Leadersh. J. 2011, 2, 1–15. [Google Scholar]

- Suh, N.P. Complexity: Theory and Applications; MIT-Pappalardo series in mechanical engineering; Oxford University Press: New York, NY, USA, 2005; ISBN 978-0-19-517876-0. [Google Scholar]

- Arthur, W.B. Complexity and the economy. Science 1999, 284, 107–109. [Google Scholar] [CrossRef] [PubMed]

- Schneider, M.; Somers, M. Organizations as complex adaptive systems: Implications of Complexity Theory for leadership research. Leadersh. Q. 2006, 17, 351–365. [Google Scholar] [CrossRef]

- Holland, J.H. Studying Complex Adaptive Systems. J. Syst. Sci. Complex. 2006, 19, 1–8. [Google Scholar] [CrossRef]

- Atkinson, S.R.; Moffat, J. The Agile Organisation: From Informal Networks to Complex Effects and Agility; Information Age Transformation Series; CCRP Publications: Washington, DC, USA, 2005; ISBN 978-1-893723-16-0. [Google Scholar]

- Carayannis, E.G.; Sindakis, S.; Walter, C. Business Model innovation as lever of organizational sustainability. J. Technol. Transf. 2015, 40, 85–104. [Google Scholar] [CrossRef]

- Peltoniemi, M.; Vuori, E. Business ecosystem as the new approach to complex adaptive business environments. In Proceedings of the eBusiness Research Forum, Tamper, Finland, 20–22 September 2004; Volume 2, pp. 267–281. [Google Scholar]

- Anggraeni, E.; Den Hartigh, E.; Zegveld, M. Business ecosystem as a perspective for studying the relations between firms and their business networks. In Proceedings of the ECCON 2007 Annual Meeting, Veldhoven, The Netherlands, 19–21 October 2007; pp. 1–28. [Google Scholar]

- Porter, T.B. Coevolution as a Research Framework for Organizations and the Natural Environment. Organ. Environ. 2006, 19, 479–504. [Google Scholar] [CrossRef]

- Stead, J.G.; Stead, W.E. The Coevolution of Sustainable Strategic Management in the Global Marketplace. Organ. Environ. 2013, 26, 162–183. [Google Scholar] [CrossRef]

- Benn, S.; Edwards, M.; Williams, T. Organizational Change for Corporate Sustainability, 4th ed.; Routledge: London, UK; New York, NY, USA, 2018; ISBN 978-1-315-61962-0. [Google Scholar]

- Hahn, T.; Figge, F.; Pinkse, J.; Preuss, L. A paradox perspective on corporate sustainability: Descriptive, instrumental, and normative aspects. J. Bus. Ethics 2018, 148, 235–248. [Google Scholar] [CrossRef]

- Elkington, J. Enter the triple bottom line. In The Triple Bottom Line; Routledge: London, UK, 2013; pp. 23–38. [Google Scholar]

- Bansal, P.; DesJardine, M.R. Business sustainability: It is about time. Strateg. Organ. 2014, 12, 70–78. [Google Scholar] [CrossRef]

- Guerras-Martín, L.Á.; Madhok, A.; Montoro-Sánchez, Á. The evolution of strategic management research: Recent trends and current directions. BRQ Bus. Res. Q. 2014, 17, 69–76. [Google Scholar] [CrossRef]

- Smith, W.K.; Erez, M.; Jarvenpaa, S.; Lewis, M.W.; Tracey, P. Adding complexity to theories of paradox, tensions, and dualities of innovation and change: Introduction to organization studies special issue on paradox, tensions, and dualities of innovation and change. Organ. Stud. 2017, 38, 303–317. [Google Scholar] [CrossRef]

- de Wit, B.; Meyer, R. Strategy Synthesis: Resolving Strategy Paradoxes to Create Competitive Advantage: Text and Readings, 3rd ed.; South-Western/CENGAGE Learning: Andover, UK, 2010; ISBN 978-1-4080-1899-6. [Google Scholar]

- Kim, W.C.; Mauborgne, R. Blue Ocean Strategy How to Create Uncontested Market Space and Make the Competition Irrelevant; Harvard Business Review Press: Boston, USA, 2015; ISBN 978-1-62527-450-2. [Google Scholar]

- Pertusa-Ortega, E.M.; Molina-Azorín, J.F. A joint analysis of determinants and performance consequences of ambidexterity. BRQ Bus. Res. Q. 2018, 21, 84–98. [Google Scholar] [CrossRef]

- Van der Byl, C.A.; Slawinski, N. Embracing tensions in corporate sustainability: A review of research from win-wins and trade-offs to paradoxes and beyond. Organ. Environ. 2015, 28, 54–79. [Google Scholar] [CrossRef]

- Laasch, O.; Conaway, R.N. Principles of Responsible Management: Glocal Sustainability, Responsibility, and Ethics; Cengage Learning: Stamford, Australia; Stamford, CT, USA, 2015; ISBN 978-1-285-08026-0. [Google Scholar]

- Haffar, M.; Searcy, C. Classification of Trade-offs Encountered in the Practice of Corporate Sustainability. J. Bus. Ethics 2017, 140, 495–522. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Massa, L.; Bocken, N.; Brent, A.; Musango, J. Business models for shared value: Main Report; Network for Business Sustainability South Africa: Cape Town, South Africa, 2016; ISBN 978-0-620-70726-8. [Google Scholar]

- Achtenhagen, L.; Melin, L.; Naldi, L. Dynamics of Business Models—Strategizing, Critical Capabilities and Activities for Sustained Value Creation. Long Range Plan. 2013, 46, 427–442. [Google Scholar] [CrossRef]

- Chew, E.; Semmelrock-Picej, M.T.; Novak, A. Value co-creation in the organizations of the future. In Proceedings of the European Conference on Management, Leadership & Governance, Klagenfurt, Austria, 9 January 2013; pp. 16–23. [Google Scholar]

- Hart, S.L.; Milstein, M.B. Creating sustainable value. Acad. Manag. Perspect. 2003, 17, 56–67. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The big idea: Creating shared value. Harv. Bus. Rev. 2011, 1–17. Available online: https://hbr.org/2011/01/the-big-idea-creating-shared-value (accessed on 24 April 2020).

- Fiksel, J. Sustainability and resilience: Toward a systems approach. Sustain. Sci. Pract. Policy 2006, 2, 14–21. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Radoynovska, N.; Ocasio, W.; Laasch, O. The emerging logic of responsible management: Institutional pluralism, leadership, and strategizing. In The Research Handbook of Responsible Management; Edward Elgar: Chelthenham, UK, 2019. [Google Scholar]

- Roome, N.; Louche, C. Journeying Toward Business Models for Sustainability: A Conceptual Model Found Inside the Black Box of Organisational Transformation. Organ. Environ. 2016, 29, 11–35. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Source | Documents | Citations | Total Link Strength |

|---|---|---|---|

| 1. Journal of cleaner production | 111 | 3731 | 549 |

| 2. Sustainability | 95 | 307 | 291 |

| 3. Organization and environment | 10 | 913 | 263 |

| 4. Business strategy and the environment | 18 | 485 | 156 |

| 5. Long range planning | 6 | 745 | 65 |

| Document | Citations | Links |

|---|---|---|

| 1. Bocken, N.M., Short, S.W., Rana, P., and Evans, S. (2014). A literature and practice review to develop sustainable business model archetypes. Journal of Cleaner Production, 65, 42–56. | 657 | 189 |

| 2. Boons, F., and Lüdeke-Freund, F. (2013). Business models for sustainable innovation: state-of-the-art and steps towards a research agenda. Journal of Cleaner Production, 45, 9–19. | 558 | 174 |

| 3. Stubbs, W., and Cocklin, C. (2008). Conceptualizing a “sustainability business model”. Organization & Environment, 21(2), 103–127. | 346 | 133 |

| 4. Schaltegger, S., Hansen, E.G., and Lüdeke-Freund, F. (2016). Business models for sustainability: Origins, present research, and future avenues. Organization & Environment, 29(1), 3–10 | 173 | 81 |

| 5. Pieroni, M.P., McAloone, T.C., and Pigosso, D.C. (2019). Business model innovation for circular economy and sustainability: A review of approaches. Journal of Cleaner Production, 215, 198–216. | 28 | 67 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ogrean, C.; Herciu, M. Business Models Addressing Sustainability Challenges—Towards a New Research Agenda. Sustainability 2020, 12, 3534. https://doi.org/10.3390/su12093534

Ogrean C, Herciu M. Business Models Addressing Sustainability Challenges—Towards a New Research Agenda. Sustainability. 2020; 12(9):3534. https://doi.org/10.3390/su12093534

Chicago/Turabian StyleOgrean, Claudia, and Mihaela Herciu. 2020. "Business Models Addressing Sustainability Challenges—Towards a New Research Agenda" Sustainability 12, no. 9: 3534. https://doi.org/10.3390/su12093534

APA StyleOgrean, C., & Herciu, M. (2020). Business Models Addressing Sustainability Challenges—Towards a New Research Agenda. Sustainability, 12(9), 3534. https://doi.org/10.3390/su12093534