Assessment of the Profitability of Environmental Activities in Forestry

, ,

, ,  ,

,  and

and

Abstract

1. Introduction

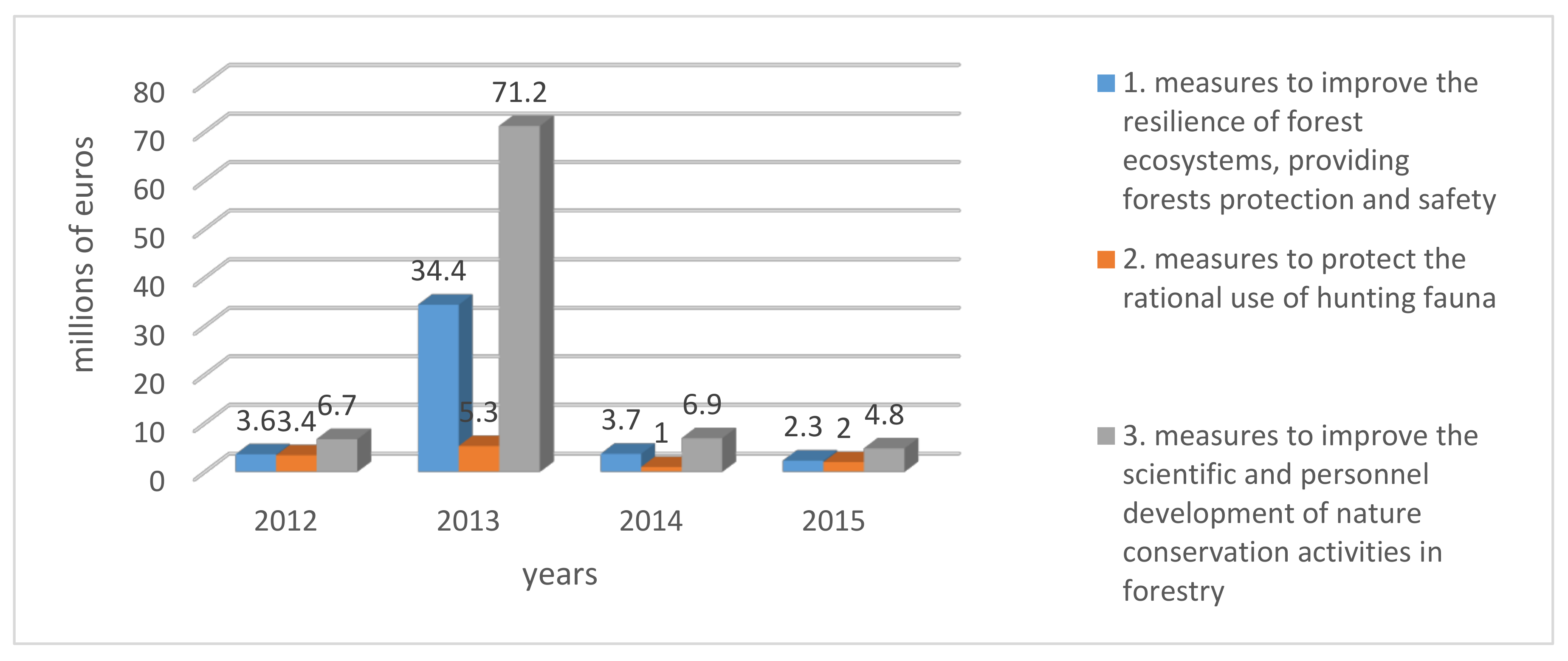

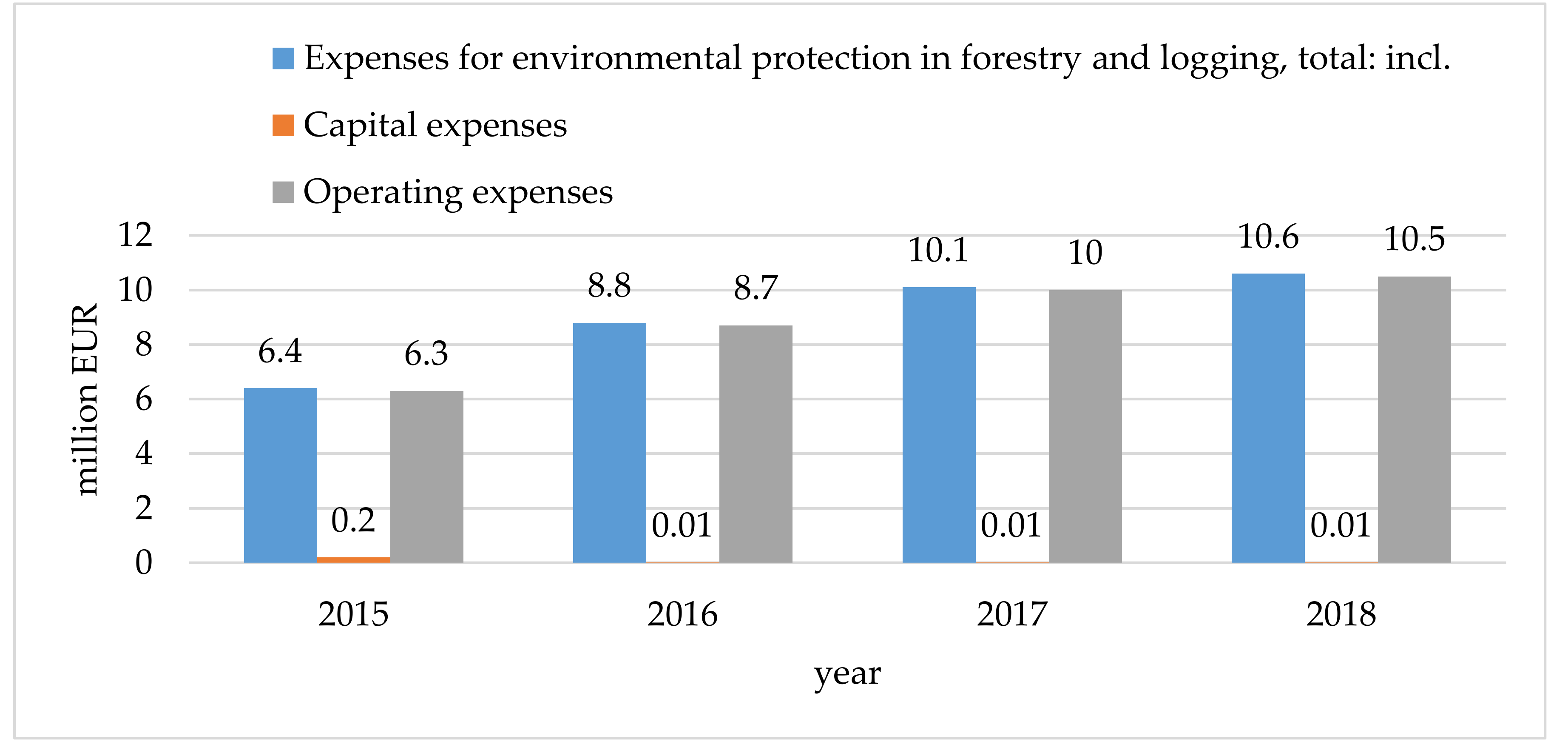

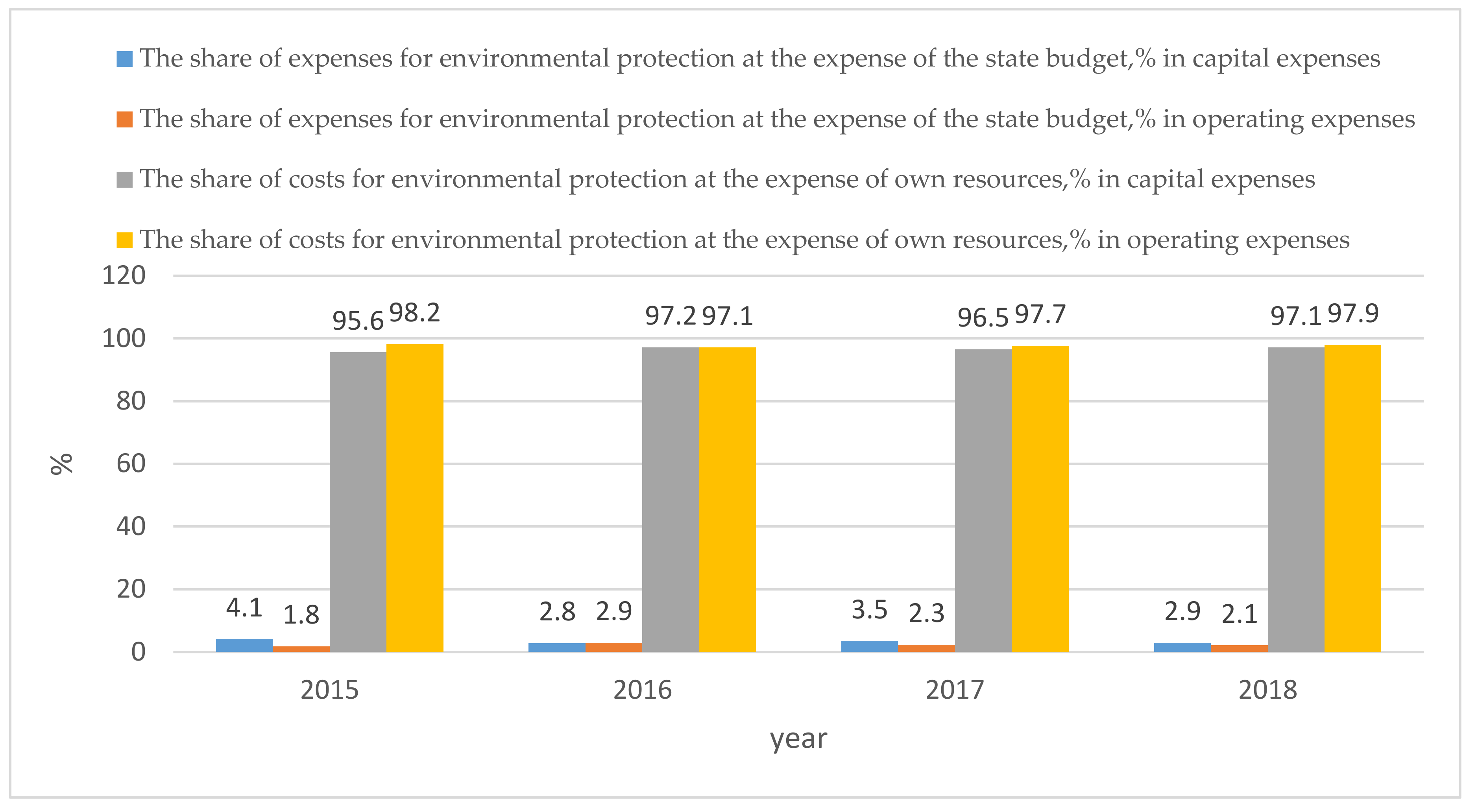

2. The Status of Implementation of Environmental Measures for Forestry in Ukraine

3. Literature Review

4. Results

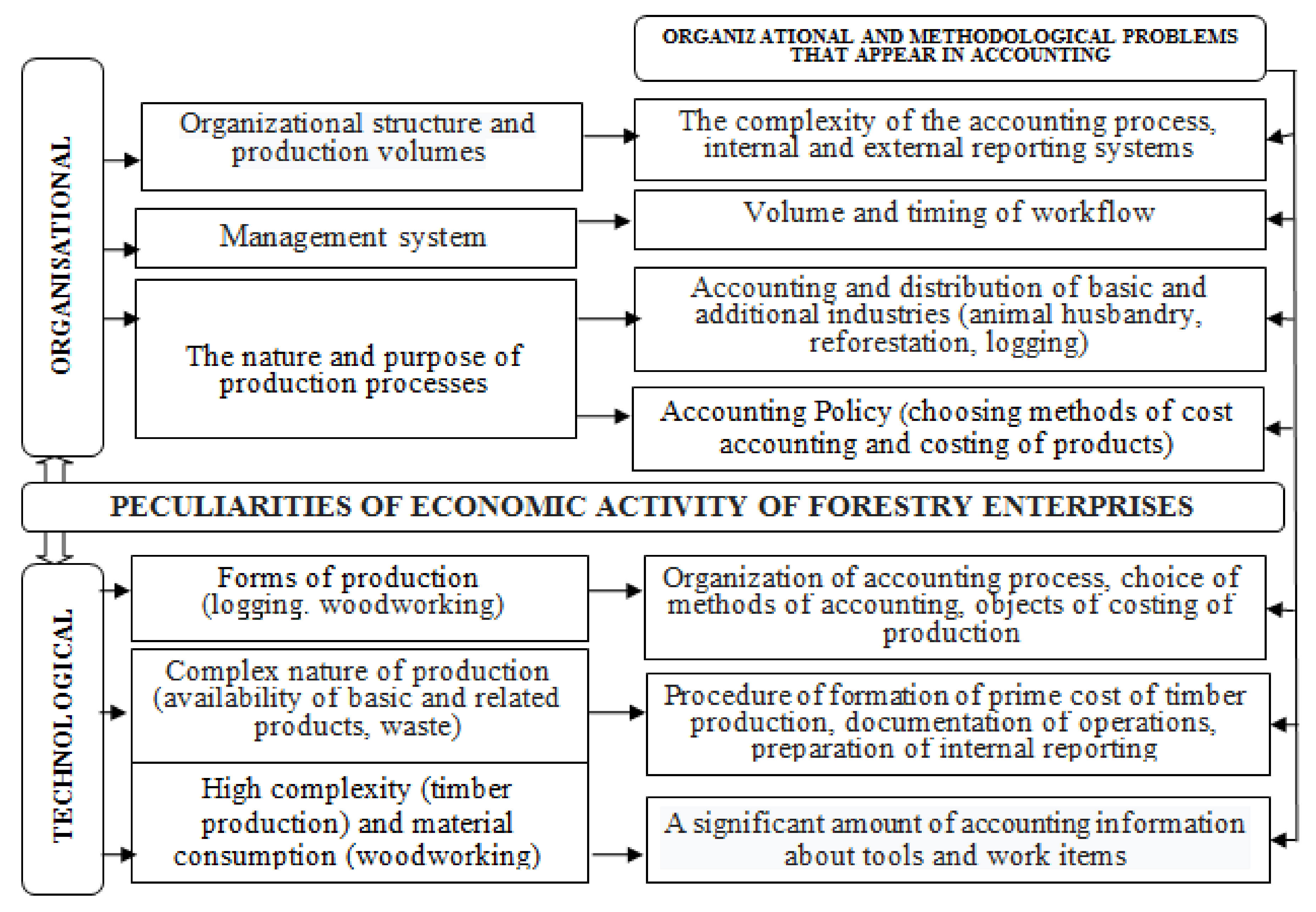

4.1. Accounting of Environmental Activities in Forestry

4.2. The Effectiveness of the Environmental Activities

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Food and Agriculture Organization of the United Nations. The State of the World’s Forests: Ways to Achieve Sustainable Development, Taking into Account the Importance of Forests; Food and Agriculture Organization of the United Nations: Rome, Italy, 2018. [Google Scholar]

- Sugiura, K.; Oki, Y. Reasons for Choosing Forest Stewardship Council (FSC) and Sustainable Green Ecosystem Council (SGEC) schemes and the effects of certification acquisition by forestry enterprises in Japan. Forests 2018, 9, 173. [Google Scholar] [CrossRef]

- Bartniczak, B.; Raszkowski, A. Sustainable forest management in Poland. Manag. Environ. Qual. 2018, 29, 666–677. [Google Scholar] [CrossRef]

- Environment of Ukraine to 2018. Statistical Collection 2019. Available online: http://www.ukrstat.gov.ua (accessed on 23 September 2019).

- Sustainable Development Goals 2016–2030. Available online: http://www.un.org.ua/ua/tsili-rozvytku-tysiacholittia/tsili-staloho-rozvytku (accessed on 7 April 2020).

- Plans and Reports on the Work of the State Forest Resources Agency of Ukraine. Available online: http://dklg.kmu.gov.ua/forest/control/uk/publish/category?cat_id=34185 (accessed on 6 October 2019).

- Lu, S.; Tang, X.; Guan, X.; Qin, F.; Liu, X.; Zhang, D. The assessment of forest ecological security and its determining indicators: A case study of the Yangtze River Economic Belt in China. J. Environ. Manag. 2020, 258, 110048. [Google Scholar] [CrossRef] [PubMed]

- Schweier, J.; Magagnotti, N.; Labelle, E.R.; Athanassiadis, D. Sustainability impact assessment of forest operations: A review. Curr. For. Rep. 2019, 5, 101–113. [Google Scholar] [CrossRef]

- Mäkelä, M. Trends in environmental performance reporting in the Finnish forest industry. J. Clean. Prod. 2017, 142, 1333–1346. [Google Scholar] [CrossRef]

- Song, M.L.; Fisher, R.; Wang, J.L.; Cui, L.B. Environmental performance evaluation with big data: Theories and methods. Ann. Oper. Res. 2018, 270, 459–472. [Google Scholar] [CrossRef]

- Czyżewski, B.; Matuszczak, A.; Miśkiewicz, R. Public goods versus the farm price-cost squeeze: shaping the sustainability of the EU’s Common Agricultural Policy. Technol. Econ. Dev. Eco. 2019, 25, 82–102. [Google Scholar] [CrossRef]

- Raszkowski, A.; Bartniczak, B. Towards Sustainable Regional Development: Economy, Society, Environment, Good Governance Based on the Example of Polish Regions. Transf. Bus. Econ. 2018, 17, 225–245. [Google Scholar]

- Turturean, C.I.; Asandului, L.A.; Chirila, C.; Homocianu, D. Composite index of sustainable development of EU countries’ economies (ISDE-EU). Transf. Bus. Econ. 2019, 18, 586–605. [Google Scholar]

- State Forestry Committee of Ukraine. Guidelines for Formation of the Cost of Goods (Works, Services) in Ukraine’s Forestry. 2002. Available online: http://www.kadrlis.com.ua/normatuvna_baza.htm (accessed on 12 June 2019).

- Cabinet of Ministers of Ukraine, List of Activities Belonging to Environmental Measures. 1996. Available online: http://search.ligazakon.ua/l_doc2.nsf/link1/KP961147.html (accessed on 25 September 2019).

- Report on the Results of Implementation of the State Target Program “Forests of Ukraine” for 2010–2015. Available online: http://dklg.kmu.gov.ua (accessed on 2 October 2019).

- United Nations. Environmental Management Accounting Procedures and Principles; Prepared For the Expert Working Group on “improving the role of government in the promotion of environmental management accounting”; United Nations Division for Sustainable Development: New York, NY, USA, 2001. [Google Scholar]

- Zamula, I.V. Accounting of Environmental Activities in Ensuring Sustainable Development of the Economy: Monograph; ZhDTU: Zhitomir, Ukraine, 2010. [Google Scholar]

- Popović, B.; Janković Šoja, S.; Paunović, T.; Maletić, R. Evaluation of sustainable development management in EU countries. Sustainability 2019, 11, 7140. [Google Scholar] [CrossRef]

- United Nations; European Commission; International Monetary Fund; Organization for Economic Co-operation and Development; World Bank. Integrated Environmental and Economic Accounting; United Nations: New York, NY, USA; European Commission: Brussels, Belgium; International Monetary Fund: Washington, DC, USA; Organization for Economic Co-operation and Development: Paris, France; World Bank: Washington, DC, USA, 2003. [Google Scholar]

- Zandi, G.; Lee, H. Factors affecting environmental management accounting and environmental performance: An empirical assessment. Int. J. Energy Econ. Policy 2019, 9, 342–348. [Google Scholar] [CrossRef]

- Nigri, G.; Del Baldo, M. Sustainability reporting and performance measurement systems: How do small- and mediumsized benefit corporations manage integration? Sustainability 2018, 10, 4499. [Google Scholar] [CrossRef]

- Zandi, G.; Khalid, N.; Zahurul Islam, D.M. Nexus of Knowledge Transfer, Green Innovation and Environmental Performance: Impact of Environmental Management Accounting. Int. J. Energy Econ. Policy 2019, 9, 387–393. [Google Scholar] [CrossRef]

- Alaeddin, O.; Shawtari, F.; Salem, M.; Altounjy, R. The effect of management accounting systems in influencing environmental uncertainty, energy efficiency and environmental performance. Int. J. Energy Econ. Policy 2019, 9, 346–352. [Google Scholar] [CrossRef]

- United Nations. System of Environmental Economic Accounting 2012; Central Framework; United Nations: New York, NY, USA, 2017. [Google Scholar]

- Food and Agriculture Organization of the United Nations Statistical Division. System of Environmental-Economic Accounting for Agriculture, Forestry and Fisheries (SEEA AFF); Food and Agriculture Organization of the United Nations Statistical Division: Rome, Italy, 2014. [Google Scholar]

- IUFRO. Building insights of global economy and accounting toward sustainable forest management. In Proceedings of the IUFRO unit 4.05.00 International Symposium, Lviv, Ukraine, 17–19 May 2007; Zahvoyska, L., Jobstl, H., Kant, S., Maksyv, L., Eds.; UNFU Press: Lviv, Ukraine, 2009. [Google Scholar]

- Krivačić, D.; Janković, S. Managing attitudes on Environmental Reporting: Evidence from Croatia. J. Environ. Account. Manag. 2017, 5, 327–341. [Google Scholar] [CrossRef]

- Susanto, A.; Meiryani, M. The impact of environmental accounting information system alignment on firm performance and environmental performance: A case of small and medium enterprises of Indonesia. Int. J. Energy Econ. Policy 2019, 9, 229–236. [Google Scholar] [CrossRef]

- Christine, D.; Yadiati, W.; Nur Afiah, N.; Fitrijanti, T. The relationship of environmental management accounting, environmental strategy and managerial commitment with environmental performance and economic performance. Int. J. Energy Econ. Policy 2019, 9, 458–464. [Google Scholar] [CrossRef]

- Cavatassi, R. Validation Methods for Environmental Benefits in Forestry and Watt Investment Projects; The Food and Agriculture Organization of the United Nations: Rome, Italy, 2004. [Google Scholar]

- IUFRO Research Group. Managing economy and accounting in an ever changing paradise of forest management. In International Symposium, 2nd ed.; Jobstl, H., Roder, C., Eds.; University of Applied Forest Sciences: Rottenburg, Germany, 2009. [Google Scholar]

- Jobstl, H.A.; Hogg, J.N. State of forestry accounting in some European countries. Account. Manag. Econ. Environ. Friendly For. 2009, 15, 17–40. [Google Scholar]

- Toscani, P.; Walter Sekot, W. Forest accountancy data networks—A European approach of empirical research, its achievements, and potentials in regard to sustainable multiple use forestry. Forests 2018, 9, 220. [Google Scholar] [CrossRef]

- Appiah, B.; Donghui, Z.; Majumder, S.; Monaheng, M. Effects of environmental strategy, uncertainty and top management commitment on the environmental performance: Role of environmental management accounting and environmental management control system. Int. J. Energy Econ. Policy 2020, 10, 360–370. [Google Scholar] [CrossRef]

- Ning, Y.; Liu, Z.; Ning, Z.; Zhang, H. Measuring eco-efficiency of state-owned forestry enterprises in northeast China. Forests 2018, 9, 455. [Google Scholar] [CrossRef]

- Head, M.; Bernier, P.; Levasseur, A.; Beauregard, R.; Margni, M. Forestry carbon budget models to improve biogenic carbon accounting in life cycle assessment. J. Clean. Prod. 2019, 213, 289–299. [Google Scholar] [CrossRef]

- Yaremko, A.P. Analysis of efficiency of functioning and prospects of development of ecologically balanced forestry. Innovation 2017, 5, 103–108. [Google Scholar]

- Lesyuk, G.M. Modern socio-economic approaches to forest management in Ukraine. Econ. Soc. 2017, 8, 470–476. [Google Scholar]

- Sahoo, K.; Bergman, R.; Alanya-Rosenbaum, S.; Gu, H.; Liang, S.H. Life cycle assessment of forest-based products: A review. Sustainability 2019, 11, 4722. [Google Scholar] [CrossRef]

- Tanasiieva, M.M. The Accounting and Analysis of Environmental Activities in Forestry: Author’s Degree of Scientific Research; Accounting, Analysis and Audit (by Types of Economic Activity): Ternopil, Ukraine, 2016. [Google Scholar]

- Berendt, F.; Fortin, M.; Suchomel, C.; Schweier, J. Productivity, costs, and selected environmental impacts of remote-controlled mini forestry crawlers. Forests 2018, 9, 591. [Google Scholar] [CrossRef]

- Saienko, K. The Environmental Cost Accounting: Monographs; Finance and Statistics: Moscow, Russia, 2005. [Google Scholar]

- Belousov, A.I. Course of Ecological and Economic Analysis: Teaching Method; Finance and Statistics: Moscow, Russia, 2010. [Google Scholar]

- Demina, T.A. The Accounting and Analysis of Environmental Costs of Enterprises; Finance and Statistics: Moscow, Russia, 1990. [Google Scholar]

- Balatsky, O.F. Economics and the Quality of the Natural Environment; Hydrometeoizdat: Moscow, Russia, 1984. [Google Scholar]

- Krepsha, N.V. The Environmental Management and Environmental Economics: Study Method; Tomsk Political Engineering University: Tomsk, Russia, 2011. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicator, Dimension | 2015 | 2016 | 2017 | 2018 | Rate of Growth, % |

|---|---|---|---|---|---|

| Forest area, thousand ha | 10,630.3 | 10,423.1 | 10,674.9 | 10,674.9 | 0.4 |

| out of which covered with tree cover | 9695.2 | 9690 | 8424.6 | 8424.6 | −5.6 |

| Cutting area, thousand ha | 399.3 | 386.3 | 419.1 | 445.5 | 4.1 |

| Volume of harvested liquid wood, thousand m3 | 21,924.2 | 22,602.3 | 21,923 | 22,529.7 | 0.5 |

| Area of forest reproduction, thousand ha | 60.4 | 63.2 | 64.7 | 51.5 | −4.5 |

| Net income from the sale of forest products, thousand EUR | 429,997.8 | 426,047.3 | 455,772.7 | 511,986 | 5.9 |

| Cost of sold forest products, thousand EUR | 296,613.3 | 306,352.1 | 340,421 | 390,021.8 | 9.3 |

| Operating expenses, thousand EUR | 36,751.16 | 23,622.66 | 25,728.49 | 30,803.71 | −4.4 |

| Net profit, thousand EUR | 41,326.67 | 26,119.21 | 16,757.6 | 14,526.34 | −35.8 |

| Dimension | Indicator | Definition | Desirable Trend of the Indicator | Sources of Information for Calculation |

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 |

| Economic impact | Overall economic effectiveness of environmental expenditures | , where is the overall effectiveness of environmental costs; is the ecological and economic impact of environmental measures implemented (the total increase in the forest resource value); CEE is the cumulative environmental expenditure that has contributed to this effect. | max | Data of analytical account 237 “Environmental expenses”, 915 “Environmental expenses”, 719 “Operational income from environmental activities”, 747 “Income from capital environmental measures”. Analytical accounting on accounts 15 “Capital construction”, 98 “Tax on profit”. |

| Effectiveness of capital environmental expenditure | , where Ek is effectiveness of capital environmental costs; is operating expenses for maintenance of environmental objects; CNE is the capital expenses for nature protection. | max | ||

| Normative effectiveness of environmental costs | , where is the normative coefficient of capital investments. | min | ||

| Net economic impact of environmental measures | NEE = Egen – Ee, where NEE is the net economic effect; Ee is the costs of relevant environmental activities; Egen - the economic effect of the implementation of nature protection activities: Egen EL is prevented loss from pollution of forests; is the growth of income from the activities of the enterprise due to environmental improvement. | max | ||

| Environmental impact | Average reduction in negative impact on forest resources | , where is the average reduction in the negative impact on forest resources; - reduction in negative impacts on forest resources; TEE is the total environmental expenditure that has contributed to this effect. | max | Management reporting data: “Statement of cost accounting for environmental activities of forestry”, “Summary of cost accounting for environmental activities by sources of financing”, form 10-LH “Report on the implementation of the production plan for forestry”. |

| Average impact on forest resources | , where is an indicator of the average increase in the impact on forest resources; is improvement in the value of forest resources. | max | ||

| Social impact | Profitability of environmental activities from the social viewpoint | R = , where R-profitability of environmental activities from the point of view of society; is reduction in environmental fees and payments; is additional profit from the sales of waste to third party enterprises or their own processing and sale of products to buyers; is the costs of implementation of I environmental action. | max | Data of analytical accounting on accounts 36 “Calculations with buyers and customers”, 37 “Calculations with other debtors”, 915 “Expenses on environmental activity”. Tax and financial reporting data. |

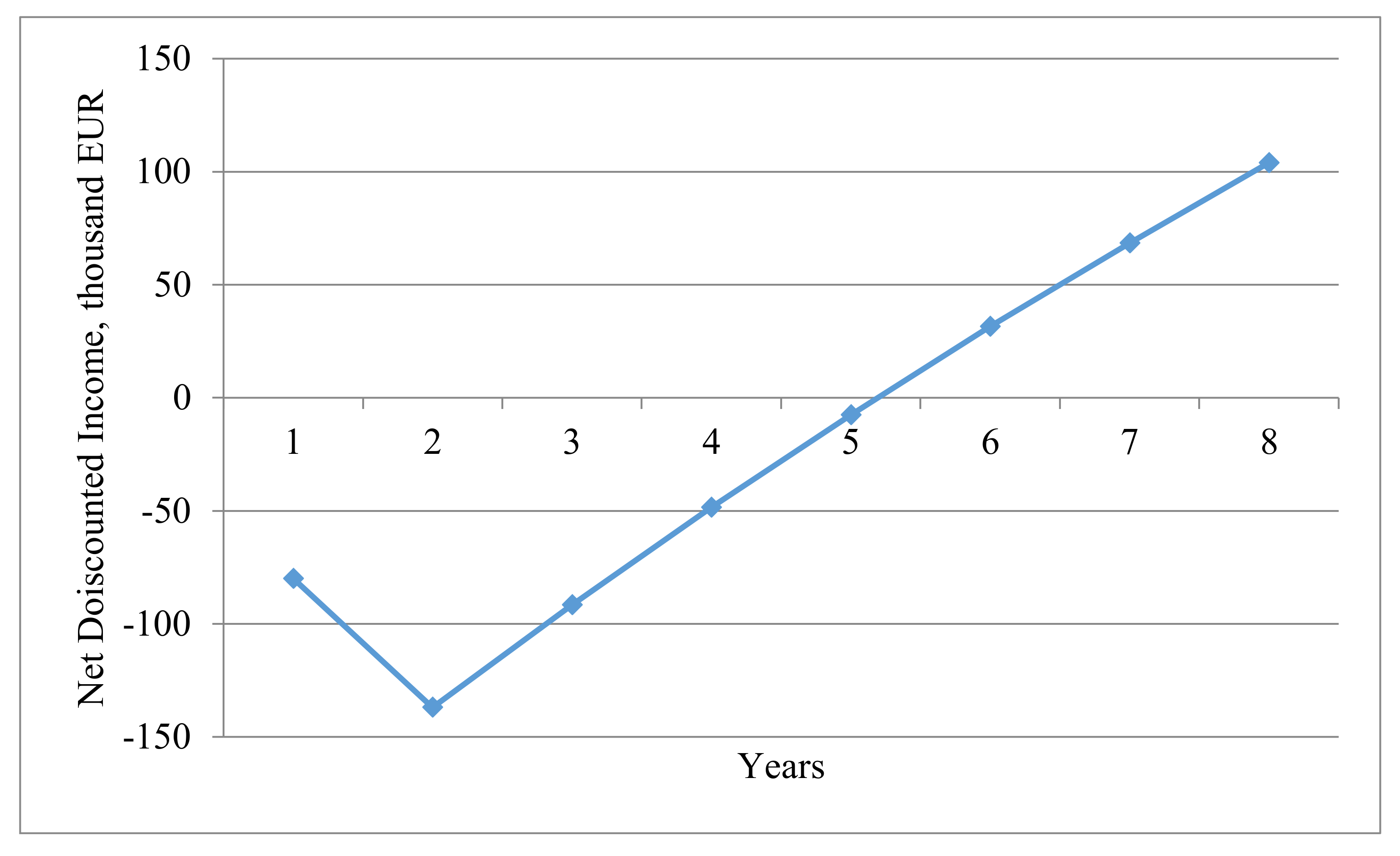

| Year | Annual Reduction in Damage to Forest Resources, Thousand Euro | Annual Amount of Capital Conservation Expenditures, Thousand Euro | Cash Flow, Thousand Euro | Discount Factor | Discounted Cash Flow, thousand Euro | NDI, Thousand Euro |

|---|---|---|---|---|---|---|

| 1 | – | 80 | −80 | 1 | −80.0 | −80.0 |

| 2 | – | 60 | −60 | 0.95 | −57.0 | −137.0 |

| 3 | 50 | – | 50 | 0.91 | 45.5 | −91.5 |

| 4 | 50 | – | 50 | 0.86 | 43.0 | −48.5 |

| 5 | 50 | – | 50 | 0.82 | 41.0 | −7.5 |

| 6 | 50 | – | 50 | 0.78 | 39.0 | 31.5 |

| 7 | 50 | – | 50 | 0.74 | 37.0 | 68.5 |

| 8 | 50 | – | 50 | 0.71 | 35.5 | 104.0 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zamula, I.; Tanasiieva, M.; Travin, V.; Nitsenko, V.; Balezentis, T.; Streimikiene, D. Assessment of the Profitability of Environmental Activities in Forestry. Sustainability 2020, 12, 2998. https://doi.org/10.3390/su12072998

Zamula I, Tanasiieva M, Travin V, Nitsenko V, Balezentis T, Streimikiene D. Assessment of the Profitability of Environmental Activities in Forestry. Sustainability. 2020; 12(7):2998. https://doi.org/10.3390/su12072998

Chicago/Turabian StyleZamula, Iryna, Maryna Tanasiieva, Vitalii Travin, Vitalii Nitsenko, Tomas Balezentis, and Dalia Streimikiene. 2020. "Assessment of the Profitability of Environmental Activities in Forestry" Sustainability 12, no. 7: 2998. https://doi.org/10.3390/su12072998

APA StyleZamula, I., Tanasiieva, M., Travin, V., Nitsenko, V., Balezentis, T., & Streimikiene, D. (2020). Assessment of the Profitability of Environmental Activities in Forestry. Sustainability, 12(7), 2998. https://doi.org/10.3390/su12072998