1. Introduction

The banking crises and financial scandals in 2008 hurled many retail banks into mayhem, resulting in their closures, mergers, and acquisitions. Customer confidence was gravely corroded and needed to be fully restored. This falling customer confidence in banking institutions resulted in lower satisfaction and trust, thus leading to an adverse impact on their loyalty intention, and customer turnover has become a constant scourge of businesses [

1]. Nevertheless, customer loyalty has a powerful influence on business performance as it is directly associated with lower marketing costs and higher profitability [

2]. Similarly, in this era of fierce competition, organizations are trying to cope with their rivals through different marketing strategies [

3], accentuating the fact that incorporating Corporate Social Responsibility (CSR) is an efficient way to sustain the business. Homogenization and standardization in the banking sector have also made it more troublesome for the banks to use service quality, branch environment, and location to retain customers. Therefore, nowadays, finding ways to restore confidence and to regain customer loyalty has become imperative for banking institutions across the world. Studies have confirmed that CSR is an effective marketing strategy to gain customer loyalty [

4]. CSR compels customers to stick to the company’s core mission and add value through positive, participatory behavior [

5]. It is also observed that customers may reciprocate CSR in terms of their trust, brand identification, brand image, and loyalty [

6]. Therefore, companies engaged in CSR activities result in better corporate performance thanks to the improvement of customer loyalty [

7,

8]. Consequently, it becomes a competitive advantage for most of the companies in any business industry [

9].

Marketing scholars also contended on the fact that companies sometimes engage in socially responsible behavior just to gain social legitimacy. A common term “CSR washing” is all about using false CSR claims to improve the organizational standing in terms of its reputation, competitive advantage, and to gain trust from the stakeholders. Customers are becoming more skeptical about the intentions of the companies to engage in CSR activities [

10]. Customers fear that companies use CSR to manipulate them, and it is not more than a gimmick. Likewise, customer skepticism about those firms is increasing, which takes the opportunistic advantage of sustainable development [

11].

Moreover, customers attribute negativity towards CSR motives when they think companies’ promotional efforts overstate the actual outcomes [

12]. Customer responses to CSR are complex, and customers may negatively react to CSR activities when motives of the firms are in question, i.e., profit serving purpose. Foreh and Grier [

13] believed that the firm’s profit-driven CSR practices might harm the firm reputation. Hence, there is still debate on the CSR implications for the organizations, whether CSR doctrine is gravely flawed, or it can develop mechanisms to promote and flourish the sincere CSR programs [

14].

Recently, a paper by Osakwe and Yusuf [

15] contended that customers are likely to support the companies through their positive behavior, regardless of their motives behind CSR commitments. Research on electronic word of mouth claims that CSR does have a positive effect on company reputation, financial, and social performance [

16]. Another stream of researchers has made less sweeping claims that the perception of CSR-washing is a way to dissuade customers from purchasing CSR products and to discourage firms from participating in CSR programs [

11,

14]. From an extensive review of popular media, practitioners’ record, and academician’s point of view through published journal articles, Pope and Wæraas [

14] argued that there is five sine qua non to be fulfilled for a successful CSR-washing. Furthermore, opposite to a famous general belief, they proved that a successful CSR-washing is quite uncommon. It is argued that there are several avenues through which stakeholders and particularly consumers can measure the CSR performance. For instance, CSR indices, different watch groups, CSR rating agencies, law suits from the competitors of alleged CSR washers, and customer education schemes in the form of blogs, magazines, and news from different sources. These avenues for the measurement of CSR performance have deepened in recent years and work to expose CSR washers for higher publicity criticism.

Customers in this digitized and transparent environment are pushing companies to adopt certain CSR practices and co-creation activities [

7]. A firm must interact with its customers to gain comprehension of their needs and wants as customers represent one of the most critical opportunities for innovation and value co-creation [

17]. Co-creation is "

an active, creative and dynamic process aimed at developing service innovations through collaborative customer interactions and relationships" [

18]. According to service-dominant logic (SDL), the customer is a potential source of co-creation, and they should not be considered passive receivers of value; instead, they should act as partners and co-creators. When organizations embrace co-creation, it results in several advantages in the form of cost efficiencies, risk reduction, competitive advantage, and better insights [

7]. Both co-creation and CSR come under the umbrella of social and collaborative processes. Customers perceive corporate values through CSR, and once customers understand fundamental corporate principles, they exhibit company favoring responses through co-creation [

5,

8]. Companies can co-create with customers through product development, changes in the firm structure, or even creating an influence on customer preferences [

19]. Different scholars such as Prahalad and Ramaswamy [

20] established four variables in banking that linked to co-creation, i.e., dialogue, access, risk assessment, and transparency. These four factors, which are also called the DART model used for co-creation, enable companies to engage customers better. Likewise, in retail shops of Italy, transparent sharing of information results in co-creation [

19]. But, little literature is available on how and why CSR influences co-creation in the retail banking sector. Although some research has been conducted in Western countries [

1,

7] as per the author’s knowledge, no study has investigated this relationship in an Asian context.

Furthermore, past studies have linked co-creation to emotional aspects such as affective-commitment, and limited empirical research has related to customer behavioral aspects and particularly customer loyalty [

7]. In addition to this, no empirical evidence has been found linking co-creation to customer–company identification (CCI). To the best of the author’s knowledge, no study simultaneously examines CSR, co-creation, CCI, and customer loyalty.

To address these shortcomings in the literature as mentioned above, this paper examines the impact of banks’ CSR activities on customer loyalty. Similarly, this study also adds to the literature by investigating the effect of customer-company identification (CCI) on co-creation through social identity theory. Another objective of this research is to examine the mediating effect of co-creation and CCI between CSR and customer loyalty and to unearth the underlying multiple and sequential mediation mechanisms.

Lastly, most of the research linking CSR to consumer behavior has been conducted in developed countries [

21], and findings of these studies show that more research is required in the context of developing countries [

22]. Developing countries constitute expanding economies and probably have more social and environmental impact compared to developed economies. Moreover, the banking sector of Pakistan is the backbone of the economy. It facilitates the growth and development of industries through money supply in the form of credit access to poor and business enterprises [

23]. The banking sector in Pakistan is heavily engaged in CSR activities in the form of philanthropic work, cause-related marketing, and environmental protection. As per the State Bank of Pakistan (SBP), there are forty-five banks with more than 10,000 branches and 8000 ATMs. These large numbers of banks in Pakistan are now facing fierce competition with each other, and that leads to an increase in the offering of new products and services through Islamic banking, online and mobile banking from these banks. [

23]. To improve service performance, banks look for additional marketing strategies to get the favorable attitude of the customers [

24]. The findings of the current study would be helpful for the banks in how they can build up marketing strategies based on CSR and co-creation, and this empirical work will be of great concern for the marketing practitioners and banking executives.

The remaining section of the paper constitutes theoretical background and hypotheses development, the methodology, data analysis, and finally, discussion, and conclusion.

5. Discussion and Conclusions

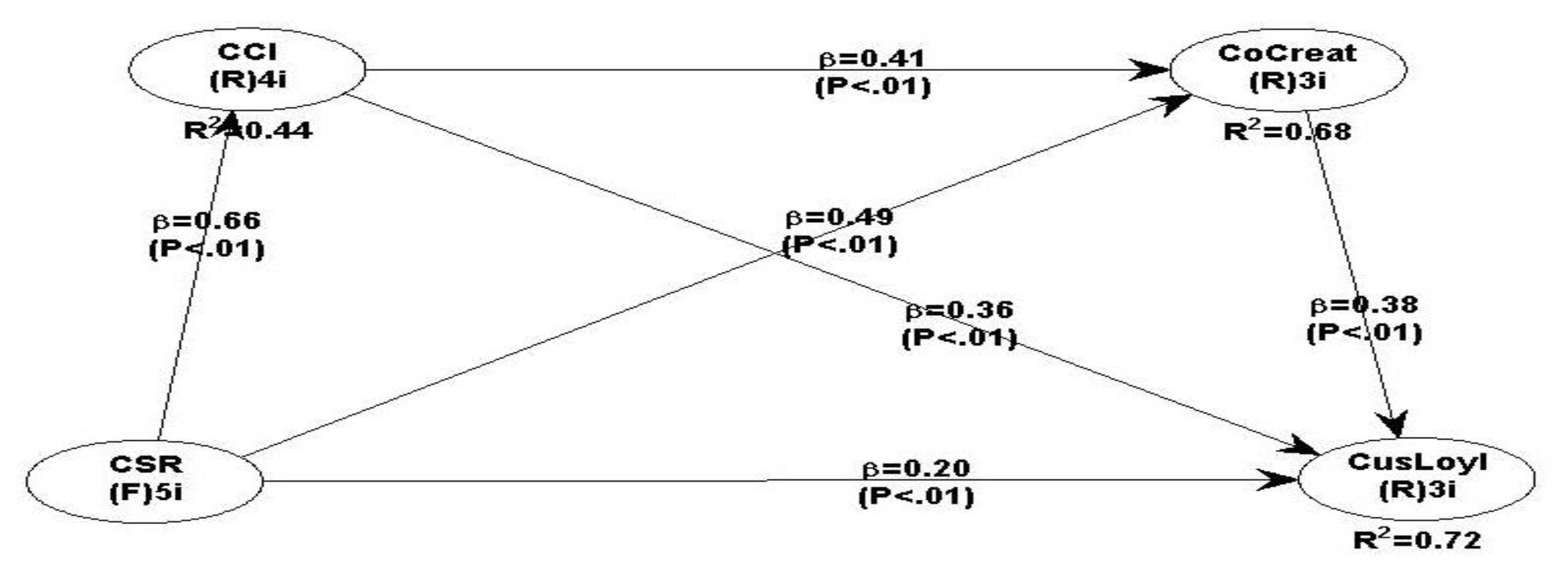

The main goal of the study is to measure the effect of banks’ CSR activities on customer loyalty directly and through intervening variables, i.e., CCI and co-creation. The results of this research confirm the previous literature that CSR has a direct and positive effect on customer’s loyalty [

23,

74,

75,

76]. Findings reveal that customers in Pakistan behave in a similar pattern, as customers in developed countries. Consumer culture theory [

77] supports the findings of this study. According to this theory, the Internet serves as a medium for convergence of the customers’ behavior, as a technological breakthrough has made it easy for everyone to access information from any part of the world, and consumers around the globe somehow think in a standardized way. That is why customers align their identities based on the consumer-driven global economy, which is highly dependent on information technology. Therefore, customers in Pakistan behave in the same way as customers in other parts of the developed world. The second reason is that the banks in Pakistan offer almost standardized service quality, same interest rate, and the same technological ease to which customers seek no difference in the products and services which they offer. In this way, customers’ lower-order needs are already met by standardized service quality and electronic service quality, such as mobile apps, self-service technologies, and traditional customer-employee interaction. So, to fulfill their higher-order needs, customers show an affinity to those banks who consider stakeholders’ concerns in their strategic plans. The customer nowadays accentuates more on ethical consumption, environment-friendly products, complaint handling procedures, and fair practices. In other words, the customer’s choice of banks is increasingly dependent on the extent to which they permit to fulfill their higher-order needs for social, environmental, and economic justice [

39]. While trying to fulfill these needs, decision-makers need to keep in mind the awareness level of its customers about the organization’s CSR claims and their actual practices. Customers will prefer to believe in and associate themselves with those organizations which have long CSR history, more local needs focused CSR activities, and are being performed without any irregularity or accidents [

10,

16].

Second objective deals with the investigation of the mediating effect of CCI and co-creation between CSR and customer loyalty. Both CCI and co-creation mediate between CSR and customer loyalty and explain the mechanism through which CSR affects customer loyalty. This study confirms the positive and significant impact of CCI on co-creation in a way that customers start identifying themselves with their banks. Then, they contribute to the bank through their feedback and involvement. Identified customers positively contribute to the new product and service development and design processes. This identification leads customers to participatory behavior, and when banks value their co-creation, a sense of ownership increases among the customers, which leads to favorable company response in the form of their loyalty.

Additionally, this study also confirms the sequential mediating effect of CCI and co-creation between CSR and customer loyalty, and this finding can be explained through the social identity theory. According to this theory, customers are more inclined towards those companies which have a positive CSR reputation [

78,

79]. Moreover, customers also desire the relationship with competent, proficient, and highly capable firms to satisfy the need for self-enhancement and self-distinctiveness [

35]. Thereby, the customers must identify themselves with the bank for exhibiting loyalty behavior; without identification, loyalty cannot be formed with the banks. According to the findings of this research, the socially responsible behavior of the banks in Pakistan positively affects the co-creation of the customers. Banks throw signals to customers by participating in socially responsible activities where they value customers and embrace co-creation [

7]. Through these CSR activities, banks also try to stir up the notion of strategic partnership through both customers and employees who jointly define a beneficial solution for both parties. In short, CSR creates identification among the customers, and these identified customers become more open to companies and listen to them and participate through innovative ideas through their opinions and positive feedback. Thus, CSR and CCI enable customers to co-create with the banks, which, as a result, enhances their loyalty.

6. Theoretical and Managerial Implications

First, this study confirms the role of CSR in creating customer loyalty in the banking industry of Pakistan. That is, when companies genuinely invest in CSR activities, they make every effort to generate social benefits for their stakeholders, including customers, employees, and the environment. Customers also support the companies through their positive behavior. Investment in CSR ensures that banks engage in more philanthropic work and consider the stakeholders’ interest as their priority. In this way, they connect with the customers emotionally through the identification process, which eventually leads to loyalty.

Similarly, CSR enhances the co-creation of the customers, a legitimate approach to CSR by the banks, motivates customers to engage in dialogue and participatory behavior, and customers tend to provide more significant input regarding product and service quality designs [

7]. CSR of the banks gives customers reasons to identify with the banks rightly; as a result, their self-esteem and pride increases, consequently motivating them to go beyond their usual role behavior. Moreover, social identity theory adds to the power of the ethical values-driven marketing 3.0 paradigm in explaining the relationship between CSR and customer co-creation.

In addition to the theoretical contribution, this research contains some critical implications for banking executives. If banking executives want to derive the loyalty of the customers through CSR, then they need to engage with the customers. Banks need to promote a dialogue with the customers regarding new product and service development, and innovation-related strategies. Banks can use co-creation as a tool to enhance customers’ participatory behavior in designing the bank’s loans, their retirement plans, car leasing, and investment plans. In this way, banks can easily outsource innovation through the participatory behavior of the customers.

The literature on CSR proposes that companies should make it a priority to have a dialogue with customers [

7]. Our study also supports this fact that when companies understand the needs of the customers and involve them in the co-creation process, then their loyalty enhances. Moreover, socially responsible activities not only provide the platform to customers to identify with the organization but also this identification leads to customers’ participatory behavior. So, banks should build this identification through CSR-related initiatives as this kind of identification is much stronger than other factors [

35]. CSR strategy of the banks should be translated into those actions which are correctly oriented for different stakeholders such as employee’s personal growth, customer complaint handling procedures, following ethical and legal responsibilities, and working towards a better environment and community.

Lastly, banks should work on providing the culture that should welcome and appreciate the customers’ participation and recognizes their expertise and knowledge. Furthermore, banks should have a strategic kind of relationship with the customers based on mutual trust and more robust identification. Banks should consider them as innovative strategic partners. This approach to co-creation has the highest potential to translate CSR practices into customer loyalty.

7. Limitations and Future Research

Like every other study, this research also has some limitations. First, this research is restricted to the banking sector only, and future studies can be conducted to other services sectors such as hospitality and tourism. Moreover, future studies can also consider the manufacturing industry and compare their results with the service industries. Second, this research is the only representative of the Pakistani population, and results cannot be generalized to all developing countries. Besides, as customers from different cultural backgrounds assess CSR differently, this kind of research in other developing counties may have some useful insights. So, it is recommended to replicate this research in other developing countries to increase the research generalizability. Furthermore, a similar study can be conducted to find out the intervening role of environmental dynamics in Pakistan and some other developing countries as well.

This study used cross-sectional data with stratified sampling, and further research can be conducted through longitudinal data and other sampling techniques. Some new variables, like customer commitment, satisfaction, and perceived service quality, can be added to structure a more comprehensive and complete framework. Finally, future studies can also consider the moderating effect of leadership style on the relationship between CSR and co-creation, as servant leadership and transformational leadership may have some impact on CSR and co-creation relationship. Furthermore, demographic variables such as age, gender, and education can also be used as a moderator to check the effect of these demographics on CSR–loyalty relationships.

,

,

{kind=link}

{kind=link}

{kind=link}