Sustainability Transition in Industry 4.0 and Smart Manufacturing with the Triple-Layered Business Model Canvas

,

,  ,

,

Abstract

1. Introduction

2. Theoretical Background

2.1. Business Model Concept

2.2. Business Model Innovation through Industry 4.0

2.3. From Traditional to Sustainable Business Models

2.4. Building a Conceptual Framework

3. Methodology

- Phase 1—Understanding: A first construction of the reality provided by the texts of the interviews was made by the authors based on their own knowledge and experience. In this phase, a first hierarchical list of stakeholders was built.

- Phase 2—Interpretation: In this phase, the authors compared their first construction of reality (phase 1) with the individual perspectives offered by the interviewees. In this phase, a hierarchical list of stakeholders was constructed for each interviewee, assigning to each one a weighting index.

- Phase 3—Application: The lists have been merged together, respecting the weighting criteria to obtain a construction of reality that comes as close as possible to the vision that the company has of its stakeholders.

4. Case Study

5. Results

5.1. The Triple Layered Business Model Canvas

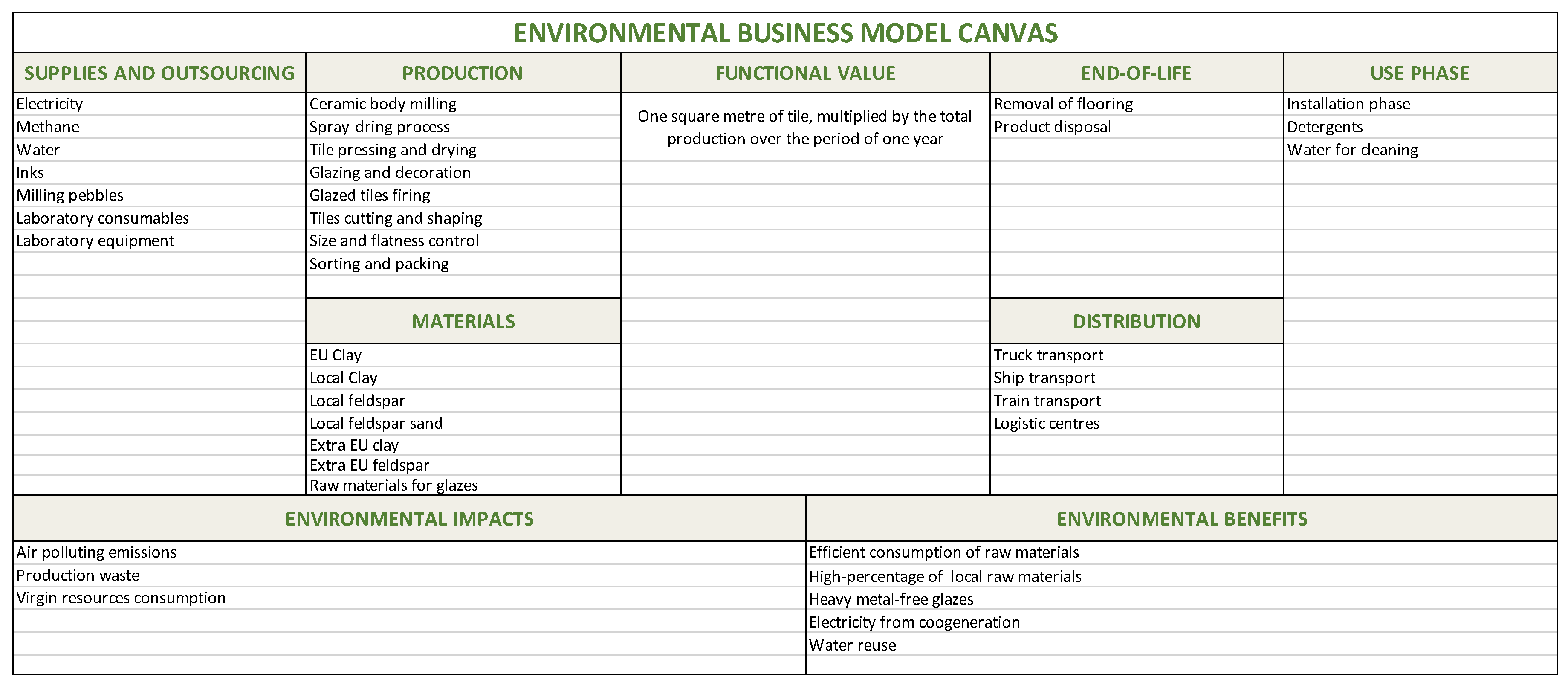

5.2. The Environmental Layer

5.3. The Social Layer

6. Discussion

7. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Carvalho, N.; Chaim, O.; Cazarini, E.; Gerolamo, M. Manufacturing in the fourth industrial revolution: A positive prospect in Sustainable Manufacturing. Procedia Manuf. 2018, 21, 671–678. [Google Scholar] [CrossRef]

- Misopoulos, F.; Michaelides, R.; Salehuddin, M.; Manthou, V.; Michaelides, Z. Addressing Organisational Pressures as Drivers towards Sustainability in Manufacturing Projects and Project Management Methodologies. Sustainability 2018, 10, 2098. [Google Scholar] [CrossRef]

- Müller, J.; Buliga, O.; Voigt, K. The role of absorptive capacity and innovation strategy in the design of industry 4.0 business Models-A comparison between SMEs and large enterprises. Eur. Manag. J. 2020. [Google Scholar] [CrossRef]

- Peukert, B.; Benecke, S.; Clavell, J.; Neugebauer, S.; Nissen, N.F.; Uhlmann, E.; Lang, K.-D.; Finkbeiner, M. Addressing Sustainability and Flexibility in Manufacturing via Smart Modular Machine Tool Frames to Support Sustainable Value Creation. Procedia CIRP 2015, 29, 514–519. [Google Scholar] [CrossRef]

- Hong, P.; Jagani, S.; Kim, J.; Youn, S. Managing sustainability orientation: An empirical investigation of manufacturing firms. Int. J. Prod. Econ. 2019, 211, 71–81. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Carroux, S.; Joyce, A.; Massa, L.; Breuer, H. The sustainable business model pattern taxonomy—45 patterns to support sustainability-oriented business model innovation. Sustain. Prod. Consum. 2018, 15, 145–162. [Google Scholar]

- Gupta, S.; Czinkota, M.; Melewar, T. Embedding knowledge and value of a brand into sustainability for differentiation. J. World Bus. 2013, 48, 287–296. [Google Scholar] [CrossRef]

- Ritala, P.; Huotari, P.; Bocken, N.; Albareda, L.; Puumalainen, K. Sustainable business model adoption among S&P 500 firms: A longitudinal content analysis study. J. Clean. Prod. 2018, 170, 216–226. [Google Scholar] [CrossRef]

- Giddings, B.; Hopwood, B.; O’Brien, G. Environment, economy and society: Fitting them together into sustainable development. Sustain. Dev. 2002, 10, 187–196. [Google Scholar] [CrossRef]

- Joyce, A.; Paquin, R. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Massa, L.; Tucci, C.L.; Afuah, A. A critical assessment of business model research. Acad. Manag. Ann. 2017, 11, 73–104. [Google Scholar] [CrossRef]

- Moggi, S.; Cantele, S.; Vernizzi, S.; Beretta Zanoni, A. The Business Model Concept and Disclosure: A Preliminary Analysis of Integrated Reports. In Proceedings of the 9th Annual Conference of the EuroMed Academy of Business, Warsaw, Poland, 14–16 September 2016. [Google Scholar]

- Amit, R.; Zott, C. Value creation in E-business. Strateg. Manag. J. 2001, 22, 493–520. [Google Scholar] [CrossRef]

- Shafer, S.; Smith, H.; Linder, J. The power of business models. Bus. Horiz. 2005, 48, 199–207. [Google Scholar] [CrossRef]

- Magretta, J. Why Business Models Matter. Harv. Bus. Rev. 2002, 80, 86–92, 133. [Google Scholar]

- Osterwalder, A.; Pigneur, Y.; Clark, T. Business Model Generation; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Gassmann, O.; Frankenberger, K.; Csik, M. The Business Model Navigator; Pearson: London, UK, 2010. [Google Scholar]

- Zott, C.; Amit, R. Business Model Design: An Activity System Perspective. Long Range Plan. 2010, 43, 216–226. [Google Scholar] [CrossRef]

- Weiller, C.; Neely, A. Business Model Design in an Ecosystem Context; University of Cambridge, Cambridge Service Alliance: Cambridge, UK, 2013. [Google Scholar]

- Wirtz, B.W.; Pistoia, A.; Ullrich, S.; Gottel, V. Business models: Origin, development and future research perspectives. Long Range Plan. 2016, 49. [Google Scholar] [CrossRef]

- Evans, S.; Vladimirova, D.; Holgado, M.; Van Fossen, K.; Yang, M.; Silva, E.A.; Barlow, C.Y. Business model innovation for sustainability: Towards a unified perspective for creation of sustainable business models. Bus. Strategy Environ. 2017, 26, 597–608. [Google Scholar] [CrossRef]

- Yang, M.; Evans, S.; Vladimirova, D.; Rana, P. Value uncaptured perspective for sustainable business model innovation. J. Clean. Prod. 2017, 140, 1794–1804. [Google Scholar] [CrossRef]

- Foss, N.; Saebi, T. Fifteen Years of Research on Business Model Innovation. J. Manag. 2016, 43, 200–227. [Google Scholar] [CrossRef]

- Velu, C. Business Model Innovation and Third-Party Alliance on the Survival of New Firms. Technovation 2015, 35, 1–11. [Google Scholar] [CrossRef]

- Lee, J.; Suh, T.; Roy, D.; Baucus, M. Emerging Technology and Business Model Innovation: The Case of Artificial Intelligence. J. Open Innov. Technol. Mark. Complex. 2019, 5, 44. [Google Scholar] [CrossRef]

- Falcone, P.; Lopolito, A.; Sica, E. Instrument mix for energy transition: A method for policy formulation. Technol. Forecast. Soc. Chang. 2019, 148, 119706. [Google Scholar] [CrossRef]

- Bartodziej, C.J. The concept industry 4.0. In The Concept Industry 4.0; Springer Gabler: Wiesbaden, Germany, 2017. [Google Scholar]

- Rojko, A. Industry 4.0 Concept: Background and Overview. Int. J. Interact Mob. Technol. 2017, 11, 77. [Google Scholar] [CrossRef]

- Ślusarczyk, B. Industry 4.0—Are we ready? Pol. J. Manag. Stud. 2018, 17, 232–248. [Google Scholar] [CrossRef]

- Frank, A.; Dalenogare, L.; Ayala, N. Industry 4.0 technologies: Implementation patterns in manufacturing companies. Int. J. Prod. Econ. 2019, 210, 15–26. [Google Scholar] [CrossRef]

- Agrawal, A.; Schaefer, S.; Funke, T. Incorporating Industry 4.0. in Corporate Strategy. Adv. Bus. Inf. Syst. Anal. 2018, 161–176. [Google Scholar] [CrossRef]

- Kagermann, H.; Helbig, J.; Hellinger, A.; Wahlster, W. Recommendations for Implementing the strategic initiative. In INDUSTRIE 4.0: Securing the Future of German Manufacturing Industry; Final report of the Industrie 4.0 working group; Forschungsunion: München, Germany, 2013. [Google Scholar]

- Ślusarczyk, B.; Haseeb, M.; Hussain, H. Fourth industrial revolution: A way forward to attain better performance in the textile industry. Eng. Manag. Prod. Serv. 2019, 11, 52–69. [Google Scholar] [CrossRef]

- Zheng, P.; Wang, H.; Sang, Z.; Zhong, R.; Liu, Y.; Liu, C.; Mubarok, K.; Yu, S.; Xu, X. Smart manufacturing systems for Industry 4.0: Conceptual framework, scenarios, and future perspectives. Front. Mech. Eng. 2018, 13, 137–150. [Google Scholar] [CrossRef]

- Dalenogare, L.S.; Benitez, G.B.; Ayala, N.F.; Frank, A.G. The expected contribution of Industry 4.0 technologies for industrial performance. Int. J. Prod. Econ. 2018, 204, 383–394. [Google Scholar] [CrossRef]

- Xu, L.; Xu, E.; Li, L. Industry 4.0: State of the art and future trends. Int. J. Prod. Res. 2018, 56, 2941–2962. [Google Scholar] [CrossRef]

- Arnold, C.; Kiel, D.; Voigt, K.I. Innovative business models for the industrial internet of things. BHM Berg-und Hüttenmännische Mon. 2017, 162, 371–381. [Google Scholar] [CrossRef]

- Parida, V.; Sjödin, D.; Reim, W. Reviewing Literature on Digitalization, Business Model Innovation, and Sustainable Industry: Past Achievements and Future Promises. Sustainability 2019, 11, 391. [Google Scholar] [CrossRef]

- Ibarra, D.; Ganzarain, J.; Igartua, J.I. Business model innovation through Industry 4.0: A review. Procedia Manuf. 2018, 22, 4–10. [Google Scholar] [CrossRef]

- Pereira, A.; Romero, F. A review of the meanings and the implications of the Industry 4.0 concept. Procedia Manuf. 2017, 13, 1206–1214. [Google Scholar] [CrossRef]

- Stock, T.; Seliger, G. Opportunities of Sustainable Manufacturing in Industry 4.0. Procedia CIRP 2016, 40, 536–541. [Google Scholar] [CrossRef]

- Luthra, S.; Mangla, S. Evaluating challenges to Industry 4.0 initiatives for supply chain sustainability in emerging economies. Process Saf. Environ. Prot. 2018, 117, 168–179. [Google Scholar] [CrossRef]

- Müller, J.; Kiel, D.; Voigt, K. What Drives the Implementation of Industry 4.0? The Role of Opportunities and Challenges in the Context of Sustainability. Sustainability 2018, 10, 247. [Google Scholar] [CrossRef]

- Varela, L.; Araújo, A.; Ávila, P.; Castro, H.; Putnik, G. Evaluation of the Relation between Lean Manufacturing, Industry 4.0, and Sustainability. Sustainability 2019, 11, 1439. [Google Scholar] [CrossRef]

- Birkel, H.; Veile, J.; Müller, J.; Hartmann, E.; Voigt, K. Development of a Risk Framework for Industry 4.0 in the Context of Sustainability for Established Manufacturers. Sustainability 2019, 11, 384. [Google Scholar] [CrossRef]

- Man, J.; Strandhagen, J. An Industry 4.0 Research Agenda for Sustainable Business Models. Procedia CIRP 2017, 63, 721–726. [Google Scholar] [CrossRef]

- Abdul-Rashid, S.; Sakundarini, N.; Raja Ghazilla, R.; Thurasamy, R. The impact of sustainable manufacturing practices on sustainability performance. Int. J. Oper. Prod. Manag. 2017, 37, 182–204. [Google Scholar] [CrossRef]

- Bocken, N.; Boons, F.; Baldassarre, B. Sustainable business model experimentation by understanding ecologies of business models. J. Clean. Prod. 2018, 208C, 1498–1512. [Google Scholar] [CrossRef]

- Nosratabadi, S.; Mosavi, A.; Shamshirband, S.; Kazimieras Zavadskas, E.; Rakotonirainy, A.; Chau, K. Sustainable Business Models: A Review. Sustainability 2019, 11, 1663. [Google Scholar] [CrossRef]

- Geissdoerfer, M.; Vladimirova, D.; Evans, S. Sustainable business model innovation: A review. J. Clean. Prod. 2018, 198, 401–416. [Google Scholar] [CrossRef]

- Linder, M.; Williander, M. Circular Business Model Innovation: Inherent Uncertainties. Bus. Strategy Environ. 2015, 26, 182–196. [Google Scholar] [CrossRef]

- D’Adamo, I.; Gastaldi, M.; Rosa, P. Recycling of end-of-life vehicles: Assessing trends and performances in Europe. Technol. Forecast. Soc. Chang. 2020, 152, 119887. [Google Scholar] [CrossRef]

- Lahti, T.; Wincent, J.; Parida, V. A Definition and Theoretical Review of the Circular Economy, Value Creation, and Sustainable Business Models: Where Are We Now and Where Should Research Move in the Future? Sustainability 2018, 10, 2799. [Google Scholar] [CrossRef]

- Ferella, F.; D’Adamo, I.; Leone, S.; Innocenzi, V.; De Michelis, I.; Vegliò, F. Spent FCC E-Cat: Towards a Circular Approach in the Oil Refining Industry. Sustainability 2018, 11, 113. [Google Scholar] [CrossRef]

- Aranda-Usón, A.; Portillo-Tarragona, P.; Marín-Vinuesa, L.; Scarpellini, S. Financial Resources for the Circular Economy: A Perspective from Businesses. Sustainability 2019, 11, 888. [Google Scholar] [CrossRef]

- Klymenko, O.; Nerger, A.J. Application of the Triple Layered Business Model Canvas-A Case Study of the Maritime and Marine Industry. Master’s Thesis, Institutt for internasjonal forretningsdrift, Norwegian University of Science and Technology, Gjøvik, Norway, 2018. [Google Scholar]

- Nie, Y. Combining Narrative Analysis, Grounded Theory and Qualitative Data Analysis Software to Develop a Case Study Research. J. Manag. Res. 2017, 9, 53. [Google Scholar] [CrossRef]

- Verner, J.; Abdullah, L. Exploratory case study research: Outsourced project failure. Inf. Softw. Technol. 2012, 54, 866–886. [Google Scholar] [CrossRef]

- Harrison, H.; Birks, M.; Franklin, R.; Mills, J. Case Study Research: Foundations and Methodological Orientations. Forum Qual. Soc. Res. 2017, 18, 19. [Google Scholar] [CrossRef]

- Garcia-Muiña, F.; González-Sánchez, R.; Ferrari, A.; Settembre-Blundo, D. The Paradigms of Industry 4.0 and Circular Economy as Enabling Drivers for the Competitiveness of Businesses and Territories: The Case of an Italian Ceramic Tiles Manufacturing Company. Soc. Sci. 2018, 7, 225. [Google Scholar] [CrossRef]

- Kallio, H.; Pietilä, A.M.; Johnson, M.; Kangasniemi, M. Systematic methodological review: Developing a framework for a qualitative semi-structured interview guide. J. Adv. Nurs. 2016, 72, 2954–2965. [Google Scholar] [CrossRef]

- Settembre Blundo, D.; García-Muiña, F.; Pini, M.; Volpi, L.; Siligardi, C.; Ferrari, A. Sustainability as source of competitive advantages in mature sectors: The case of Ceramic District of Sassuolo (Italy). Smart Sustain. Built Environ. 2019, 8, 53–79. [Google Scholar] [CrossRef]

- Fleming, V.; Robb, Y. A critical analysis of articles using a Gadamerian based research method. Nurs. Inq. 2019, 26, e12283. [Google Scholar] [CrossRef]

- Settembre Blundo, D.; Maramotti Politi, A.; Fernández del Hoyo, A.; García Muiña, F. The Gadamerian hermeneutics for a mesoeconomic analysis of Cultural Heritage. J. Cult. Herit. Manag. Sustain. Dev. 2019, 9, 300–333. [Google Scholar] [CrossRef]

- Vessey, D. Gadamer and the Fusion of Horizons. Int. J. Philos. Stud. 2009, 17, 531–542. [Google Scholar] [CrossRef]

- Confindustria Ceramica. Osservatorio Previsionale sul Mercato Mondiale delle PIASTRELLE di Ceramica: Italia e Principali Competitori a Confronto; Confindustria Ceramica: Sassuolo, Italy, 2018. [Google Scholar]

- Confindustria Ceramica. L’evoluzione del Comparto Ceramico tra Innovazione, Sostenibilità e Nuove Sfide; Arpae Emilia-Romagna: Ecoscienza, Italy, 2018. [Google Scholar]

- Finkbeiner, M.; Schau, E.; Lehmann, A.; Traverso, M. Towards Life Cycle Sustainability Assessment. Sustainability 2010, 2, 3309–3322. [Google Scholar] [CrossRef]

- Garcia-Muiña, F.E.; González-Sánchez, R.; Ferrari, A.M.; Volpi, L.; Pini, M.; Siligardi, C.; Settembre-Blundo, D. Identifying the equilibrium point between sustainability goals and circular economy practices in an Industry 4.0 manufacturing context using eco-design. Soc. Sci. 2019, 8, 241. [Google Scholar] [CrossRef]

- Kiel, D.; Müller, J.; Arnold, C.; Voigt, K. Sustainable Industrial Value Creation: Benefits and Challenges of Industry 4.0. Int. J. Innov. Manag. 2017, 21, 1740015. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Chofreh, A.; Goni, F. Review of Frameworks for Sustainability Implementation. Sustain. Dev. 2017, 25, 180–188. [Google Scholar] [CrossRef]

- Bossle, M.; De Barcellos, M.; Vieira, L.; Sauvée, L. The drivers for adoption of eco-innovation. J. Clean. Prod. 2020, 113, 861–872. [Google Scholar] [CrossRef]

- Ye, L.; Hong, J.; Ma, X.; Qi, C.; Yang, D. Life cycle environmental and economic assessment of ceramic tile production: A case study in China. J. Clean. Prod. 2018, 189, 432–441. [Google Scholar] [CrossRef]

- Souza, D.; Lafontaine, M.; Charron-Doucet, F.; Bengoa, X.; Chappert, B.; Duarte, F.; Lima, L. Comparative Life Cycle Assessment of ceramic versus concrete roof tiles in the Brazilian context. J. Clean. Prod. 2015, 89, 165–173. [Google Scholar] [CrossRef]

- Almeida, M.; Dias, A.; Demertzi, M.; Arroja, L. Environmental profile of ceramic tiles and their potential for improvement. J. Clean. Prod. 2016, 131, 583–593. [Google Scholar] [CrossRef]

- Siano, A.; Vollero, A.; Conte, F.; Amabile, S. “More than words”: Expanding the taxonomy of greenwashing after the Volkswagen scandal. J. Bus. Res. 2017, 71, 27–37. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Business Function | Job Position | Topics |

|---|---|---|

| Board of Directors | Chief Executive Officer | INTEREST: Which stakeholders have an interest in the company’s business? POWER: Which stakeholders have the power to influence the company’s business? PRIORITY: Depending on the level and type of stakeholder involvement, what priority should be given to their needs? |

| Top Management (C-Level) | Chief Financial Officer B2B Sales Director B2C Sales Director Procurement Director Technical Director | |

| Management (B-Level) | Innovation Manager Marketing Manager Administrative Manager Controller Manager HR Manager IT Manager Credit Manager Sourcing Manager Logistic Manager Security Manager Quality Manager R&D Manager Plant Manager 1 Plant Manager 2 Plant Manager 3 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

García-Muiña, F.E.; Medina-Salgado, M.S.; Ferrari, A.M.; Cucchi, M. Sustainability Transition in Industry 4.0 and Smart Manufacturing with the Triple-Layered Business Model Canvas. Sustainability 2020, 12, 2364. https://doi.org/10.3390/su12062364

García-Muiña FE, Medina-Salgado MS, Ferrari AM, Cucchi M. Sustainability Transition in Industry 4.0 and Smart Manufacturing with the Triple-Layered Business Model Canvas. Sustainability. 2020; 12(6):2364. https://doi.org/10.3390/su12062364

Chicago/Turabian StyleGarcía-Muiña, Fernando E., María Sonia Medina-Salgado, Anna Maria Ferrari, and Marco Cucchi. 2020. "Sustainability Transition in Industry 4.0 and Smart Manufacturing with the Triple-Layered Business Model Canvas" Sustainability 12, no. 6: 2364. https://doi.org/10.3390/su12062364

APA StyleGarcía-Muiña, F. E., Medina-Salgado, M. S., Ferrari, A. M., & Cucchi, M. (2020). Sustainability Transition in Industry 4.0 and Smart Manufacturing with the Triple-Layered Business Model Canvas. Sustainability, 12(6), 2364. https://doi.org/10.3390/su12062364