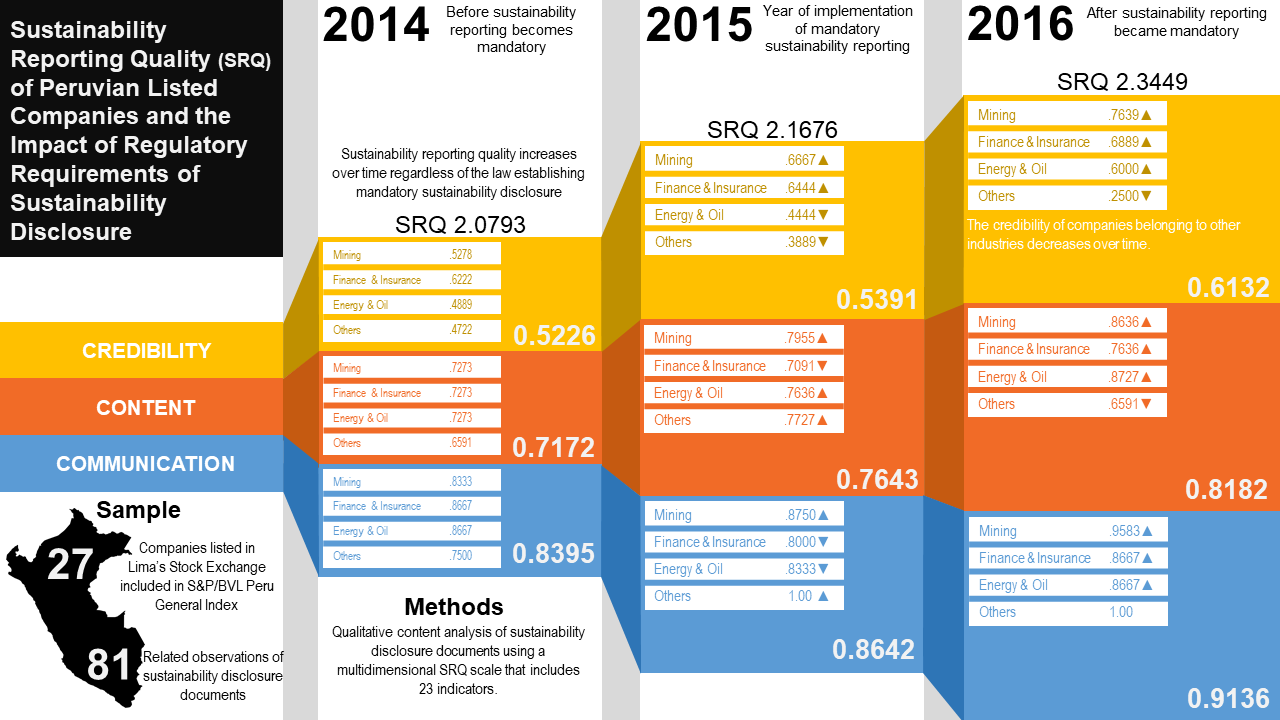

Sustainability Reporting Quality of Peruvian Listed Companies and the Impact of Regulatory Requirements of Sustainability Disclosures

Abstract

1. Introduction

2. Literature Review

3. Research Methodology

3.1. Research Design

3.2. Sampling Strategy

- Companies should have stocks listed in Lima’s Stock Exchange during three years (2014–2016).

- Companies should have stocks considered as a constituent of the S&P/BVL Peru General Index at least one year since 2015 (see Appendix A, Table A1 for details).

- Companies made a stand-alone sustainability report or an annual report available for download from one or more of the following sources: corporate website, website of Lima’s Stock Exchange, sustainability disclosure database of the Global Reporting Initiative (GRI).

3.3. Instrument of Analysis

3.4. Data Collection and Analysis

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Mean Comparisons

4.3. SRQ before and after the Implementation of New Regulatory Requirements

4.4. Trajectories of SRQ Dimensions before and after the Implementation of New Regulatory Requirements

5. Conclusions and Limitations

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Company | 2015 | 2016 | 2017 | 2018 | Included in Sample |

|---|---|---|---|---|---|

| Alicorp | Yes | Yes | Yes | Yes | Yes |

| Andino Investment Holding | No | Yes | Yes | Yes | Yes |

| Austral Grupo | Yes | Yes | Yes | Yes | Yes |

| Banco Continental | Yes | Yes | Yes | Yes | Yes |

| Banco de Crédito del Perú | No | Yes | No | No | Yes |

| Bolsa de Valores de Lima | No | Yes | Yes | Yes | Yes |

| Candente Copper Corporation | No | Yes | Yes | Yes | No |

| Casa Grande | Yes | Yes | Yes | Yes | No |

| Cementos Lima (UNACEM) | Yes | Yes | Yes | Yes | Yes |

| Cementos Pacasmayo | Yes | Yes | Yes | Yes | Yes |

| Compañía de Minas Buenaventura | Yes | Yes | Yes | Yes | Yes |

| Compañía Minera Atacocha | Yes | Yes | Yes | Yes | Yes |

| Compañía Minera Milpo (NEXA) | Yes | Yes | Yes | Yes | Yes |

| Corporación Aceros Arequipa | Yes | Yes | Yes | Yes | Yes |

| Credicorp Limited | Yes | Yes | Yes | Yes | No |

| EDEGEL (Enel Generación) | Yes | Yes | Yes | Yes | Yes |

| Empresa Agroindustrial Pomalca | Yes | Yes | Yes | No | No |

| Empresa Siderúrgica del Perú (SIDER) | No | Yes | Yes | Yes | Yes |

| Enel Distribución Perú (EDELNOR) | Yes | Yes | Yes | Yes | Yes |

| Engie Energía Perú (ENERSUR) | Yes | Yes | Yes | Yes | Yes |

| Ferreyros | Yes | Yes | Yes | Yes | Yes |

| Graña y Montero | Yes | Yes | Yes | Yes | Yes |

| InRetail Peru Corporation | Yes | Yes | Yes | Yes | No |

| Intercorp Financial Services | Yes | Yes | Yes | Yes | No |

| Inversiones Centenario | Yes | Yes | Yes | Yes | No |

| Luz del Sur | Yes | Yes | Yes | Yes | Yes |

| Minera IRL | Yes | No | No | No | No |

| Minsur | Yes | Yes | Yes | Yes | Yes |

| Morococha (SIMSA) | No | No | No | No | No |

| Panoro Minerals Ltd. | Yes | Yes | Yes | Yes | No |

| PPX Mining Corp | No | Yes | Yes | Yes | No |

| Refinería La Pampilla (RELAPSA) | Yes | Yes | Yes | Yes | Yes |

| Rimac-Internacional | No | Yes | Yes | Yes | Yes |

| Sociedad Minera Cerro Verde | Yes | Yes | Yes | Yes | Yes |

| Sociedad Minera El Brocal | Yes | Yes | Yes | Yes | Yes |

| Southern Copper Corporation | Yes | Yes | Yes | Yes | Yes |

| Trevali Mining Corporation | Yes | Yes | Yes | Yes | No |

| UCP Backus & Johnston | Yes | Yes | Yes | Yes | Yes |

| Volcan Compañía Minera | Yes | Yes | Yes | Yes | Yes |

References and Note

- Peinado-Vara, E.; Vives, A. Latin America. In The World Guide to CSR. A Country-by-Country Analysis of Corporate Sustainability and Responsibility; Visser, W., Tolhurst, N., Eds.; Greenleaf Publishing: Sheffield, UK, 2010; pp. 38–46. [Google Scholar]

- de Arruda, M.C.C. Latin America: Ethics and Corporate Social Responsibility in Latin American Small and Medium Sized Enterprises: Challenging Development. In Ethics in Small and Medium Sized Enterprises; Spence, L.J., Painter-Morland, M., Eds.; Springer: Dordrecht, The Netherlands, 2010; pp. 65–83. ISBN 978-90-481-9331-8. [Google Scholar]

- Peinado-Vara, E. Corporate Social Responsibility in Latin America. J. Corp. Citizsh. 2006, 21, 61–69. [Google Scholar] [CrossRef]

- Schmidheiny, S. A View of Corporate Citizenship in Latin America. J. Corp. Citizsh. 2006, 21, 21–24. [Google Scholar]

- Duarte, F. Working with Corporate Social Responsibility in Brazilian Companies: The Role of Managers’ Values in the Maintenance of CSR Cultures. J. Bus. Ethics 2010, 96, 355–368. [Google Scholar] [CrossRef]

- Ching, H.Y.; Gerab, F.; Toste, T.H. The Quality of Sustainability Reports and Corporate Financial Performance: Evidence From Brazilian Listed Companies. SAGE Open 2017, 7, 1–9. [Google Scholar] [CrossRef]

- Lauriano, L.A.; Spitzeck, H.; Bueno, J.H.D. The State of Corporate Citizenship in Brazil. Corp. Gov. Int. J. Bus. Soc. 2014, 14, 598–606. [Google Scholar]

- Stehr, C.; Dziatzko, N.; Struve, F. (Eds.) Corporate Social Responsibility in Brazil: The Future Is Now; Springer: Cham, Switzerland, 2019. [Google Scholar]

- Vivarta, V.; Guilherrme, C. Corporate Social Responsibility in Brazil. The Role of the Press as Watchdog. J. Corp. Citizsh. 2006, 21, 95–106. [Google Scholar]

- de Abreu, M.; da Cuhna, L.; Barlow, C.Y. Institutional Dynamics and Organizations Affecting the Adoption of Sustainable Development in the United Kingdom and Brazil. Bus. Ethics A Eur. Rev. 2015, 24, 73–90. [Google Scholar] [CrossRef]

- Becker-Olsen, K.L.; Taylor, C.R.; Hill, R.P.; Yalcinkaya, G. A Cross-Cultural Examination of Corporate Social Responsibility Marketing Communications in Mexico and the United States: Strategies for Global Brands. J. Int. Mark. 2011, 19, 30–44. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Strategic Corporate Social Responsibility and Value Creation: A Study of Multinational Enterprises in Mexico. MIR Manag. Int. Rev. 2009, 49, 781–799. [Google Scholar] [CrossRef]

- Logsdon, J.M.; Thomas, D.E.; III, H.J.V.B. Corporate Social Responsibility in Large Mexican Firms. J. Corp. Citizsh. 2006, 21, 51–60. [Google Scholar] [CrossRef]

- Meyskens, M.; Paul, K. The Evolution of Corporate Social Reporting Practices in Mexico. J. Bus. Ethics 2010, 91, 211–227. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. CSR Performance in Emerging Markets Evidence from Mexico. J. Bus. Ethics 2009, 85, 325–337. [Google Scholar] [CrossRef]

- Paul, K.; Cobas, E.; Ceron, R.; Frithiof, M.; Maass, A.; Navarro, I.; Palmer, L.; Serrano, L.; Deaton, L.Z. Corporate Social Reporting in Mexico. J. Corp. Citizsh. 2006, 22, 67–80. [Google Scholar] [CrossRef]

- Lindgreen, A.; Córdoba, J.-R.; Maon, F.; Mendoza, J.M. Corporate Social Responsibility in Colombia: Making Sense of Social Strategies. J. Bus. Ethics 2010, 91, 229–242. [Google Scholar] [CrossRef]

- Canesa Illich, G.; García Vega, E. El ABC de la Responsabilidad Social Empresarial en el Perú y en el Mundo; Perú 2021: Lima, Peru, 2005. [Google Scholar]

- Caravedo Molinari, B. La Revolución de las Significaciones: Liderazgo, Empresa y Transformación Social; Universidad del Pacífico. Centro de Investigación: Lima, Peru, 2004. [Google Scholar]

- Caravedo Molinari, B. La Sociedad Oculta: El Espacio de la Transformación; SASE, Seguimiento, Análisis y Evaluación para el Desarrollo: Lima, Peru, 2007. [Google Scholar]

- Durand, F. Empresa y Responsabilidad Social Empresarial: El Caso Peruano. In Filantropía y Cambio Social en América Latina; Sanborn, C.A., Portocarrero, F., Eds.; Universidad del Pacífico: Lima, Peru, 2008; pp. 233–264. [Google Scholar]

- Loza Adaui, C.R. Perú. In The World Guide to CSR: A Country-by-Country Analysis of Corporate Sustainability and Responsibility; Visser, W., Tolhurst, N., Eds.; Greenleaf Publishing: Sheffield, UK, 2010; pp. 296–304. ISBN 978-1-906093-37-2. [Google Scholar]

- Franco, P. Diagnóstico de la Responsabilidad Social en el Perú; Universidad del Pacífico, Documento de Discusión: Lima, Peru, 2007. [Google Scholar]

- Portocarrero S, F.; Sanborn, C.; Llusera, S.; Quea, V. Empresas, Fundaciones y Medios: La Responsabilidad Social en el Perú; Universidad del Pacífico: Lima, Peru, 2000; ISBN 9972603318. [Google Scholar]

- Rostorowski de Diez Canseco, M. Reflexiones Sobre la Reciprocidad Andina. Rev. del Mus. Nac. Lima 1976, XLII, 341–353. [Google Scholar]

- Alberti, G.; Mayer, E. (Eds.) Reciprocidad e Intercambio en los Andes Peruanos; Instituto de Estudios Peruanos: Lima, Peru, 1974. [Google Scholar]

- Sanborn, C.A. Filantropía en América Latina. In Filantropía y Cambio Social en América Latina; Sanborn, C.A., Portocarrero, F.S., Eds.; Centro de Investiacion de la Universidad del Pacífico, David Rockefeller Center for Latin American Studies: Lima, Peru, 2008; pp. 23–144. [Google Scholar]

- Rossato, E. La RSE en el Perú: Casos de Síntesis Sociocompetitivas. In Responsabilidad Social y Resultados de Empresa: Hacia una Síntesis Sociocompetitiva; Molteni, M., Rossato, E., Eds.; Fondo Editorial UCSS: Lima, Perú, 2007; pp. 137–155. ISBN 9789972297090. [Google Scholar]

- Schwalb, M.M.; García, E. Evolución del Compromiso Social de las Empresas: Historia y Enfoques; Universidad del Pacífico: Lima, Peru, 2003; ISBN 9972570282. [Google Scholar]

- Schwalb, M.M.; Ortega, C.; García, E. (Eds.) Casos de Responsabilidad Social; Universidad del Pacífico: Lima, Peru, 2003; ISBN 9972570274. [Google Scholar]

- Schwalb, M.; García, E. (Eds.) Buenas Prácticas Peruanas de Responsabilidad Social Empresarial: Colección 2004; Universidad del Pacífico: Lima, Peru, 2004; ISBN 9972570681. [Google Scholar]

- Schwalb, M.M.; García, E.; Soldevilla, V. (Eds.) Buenas Prácticas Peruanas de Responsabilidad Social Empresarial: Colección 2005; Universidad del Pacífico: Lima, Peru, 2006; ISBN 9972570959. [Google Scholar]

- Marquina Feldman, P.; Goñi Avila, N.; Rizo-Patrón Pinto, C.; Castelo Salas, L.; Castro Vergara, R.; Morice Bertho, J.; Velásquez Bellido, I.; Villaseca Chávez, M. Diagnóstico de la Responsabilidad Social en Organizaciones Peruanas; CENTRUM Publishing: Lima, Peru, 2011; ISBN 9786124533181. [Google Scholar]

- Caravedo Molinari, B. Responsabilidad Social: Todos; Voces de la Sociedad Peruana por una Nueva Ética; Universidad del Pacífico: Lima, Peru, 2011. [Google Scholar]

- Garavito Masalias, C.; Hernandez Espinoza, A. Panorama de la Responsabilidad Social Empresarial: Sector Comercio, Minero y Telecomunicaciones; PLADES and FNV: Lima, Peru, 2004. [Google Scholar]

- Portocarrero, F.; Tarazona, B.; Camacho, L.A. Situación de la Responsabilidad Social Empresarial en la Micro, Pequeña y Mediana Empresa; Universidad del Pacífico: Lima, Peru, 2006. [Google Scholar]

- Valladolid-Freyre, M. Responsabilidad Social Empresarial en la Pequena y Microempresa. Gestión en el Terc. Milen. 2005, 8, 19–24. [Google Scholar]

- Arellano-Yanguas, J. Aggravating the Resource Curse: Decentralisation, Mining and Conflict in Peru. J. Dev. Stud. 2011, 47, 617–638. [Google Scholar] [CrossRef]

- Gifford, B.; Kestler, A. Toward a Theory of Local Legitimacy by MNEs in Developing Nations: Newmont Mining and Health Sustainable Development in Peru. J. Int. Manag. 2008, 14, 340–352. [Google Scholar] [CrossRef]

- Lindgreen, A.; Swaen, V. Corporate Social Responsibility. Int. J. Manag. Rev. 2010, 12, 1–7. [Google Scholar] [CrossRef]

- Peña-Vinces, J.C.; Delgado-Márquez, B.L. Are Entrepreneurial Foreign Activities of Peruvian SMNEs Influenced by International Certifications, Corporate Social Responsibility and Green Management? Int. Entrep. Manag. J. 2013, 9, 603–618. [Google Scholar] [CrossRef]

- Portocarrero, F.; Sanborn, C.A.; Camacho, L.A. Moviendo Montañas: Empresas, Comunidades y ONG en Las Industrias Extractivas; Universidad del Pacífico: Lima, Peru, 2008. [Google Scholar]

- Saenz, C. The Context in Mining Projects Influences the Corporate Social Responsibility Strategy to Earn a Social Licence to Operate: A Case Study in Peru. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 554–564. [Google Scholar] [CrossRef]

- Pozas, M.D.C.S.; Lindsay, N.M.; du Monceau, M.I. Corporate Social Responsibility and Extractives Industries in Latin America and the Caribbean: Perspectives from the Ground. Extr. Ind. Soc. 2015, 2, 93–103. [Google Scholar]

- Szablowski, D. Mining, Displacement and the World Bank: A Case Analysis of Compania Minera Antamina’s Operations in Peru. J. Bus. Ethics 2002, 39, 247–273. [Google Scholar] [CrossRef]

- Quispe Salguero, J.; Rivera-Camino, J. CSR Serves to Compete in the Sport Industry? An Exploratory Research in the Football Sector in Peru. Corp. Ownersh. Control 2016, 13, 60–71. [Google Scholar]

- Marquina Feldman, P.; Guerrero Comissi, R.; Patrón Costa, C.; Semsch de la Puente, C. La Percepción sobre la Responsabilidad Social Empresarial: El Caso de la Banca Peruana; CENTRUM Publishing: Lima, Peru, 2012. [Google Scholar]

- Marquina, P.; Morales, C.E. The Influence of CSR on Purchasing Behaviour in Peru and Spain. Int. Mark. Rev. 2012, 29, 299–312. [Google Scholar] [CrossRef]

- Hernández-Pajares, J. Estado de la Situación de la Información de Sostenibilidad de las Empresas Peruanas. Rev. Contab. Sist. 2016, 9, 47–55. [Google Scholar]

- Hernández-Pajares, J. Determinantes de Información de Sostenibilidad de Empresas Peruanas. CAPIC Rev. 2017, 15, 9–18. [Google Scholar] [CrossRef]

- Hernández-Pajares, J. Influencia de la Naturaleza Internacional de Empresas Peruanas en su Información de Sostenibilidad. Rev. Comun. 2018, 17, 74–92. [Google Scholar] [CrossRef]

- KPMG; UNEP. Carrots and Sticks for Starters: Current Trends and Approaches in Voluntary and Mandatory Standards for Sustainability Reporting; KMPG: Amstelveen, The Netherlands; UNEP: Paris, France, 2006. [Google Scholar]

- KMPG; Center for Corporate Governance in Africa; GRI; UNEP. Carrots and Sticks: Promoting Transparency and Sustainability. An Update on Trends in Voluntary and Mandatory Approaches to Sustainability Reporting; KMPG: Amstelveen, The Netherlands; Center for Corporate Governance in Africa: Cape Town, South Africa; GRI: Amsterdam, The Netherlands; UNEP: Nairobi, Kenya, 2010. [Google Scholar]

- KPMG; Centre for Corporate Governance in Africa; GRI; UNEP. Carrots and Sticks: Sustainability Reporting Policies Worldwide. Today’s Best Practice, Tomorrow’s Trends; KMPG: Amstelveen, The Netherlands; Center for Corporate Governance in Africa: Cape Town, South Africa; GRI: Amsterdam, The Netherlands; UNEP: Nairobi, Kenya, 2013.

- KPMG; GRI; UNEP; Center for Corporate Governance in Africa. Carrots and Sticks: Global Trends in Sustainability Reporting Regulation and Policy; KMPG: Amstelveen, The Netherlands; GRI: Amsterdam, The Netherlands; UNEP: Nairobi, Kenya; Center for Corporate Governance in Africa: Cape Town, South Africa, 2016. [Google Scholar]

- Ministry of Economy and Finance Resolución SMV No 033-2015-SMV/01 - Incorporan Anexo Adicional a la Seccion IV de la Memoria, numeral (10180) “Reporte de Sostenibilidad Corporativa” aprobada mediante Res. N° 211-98-EF/94.11. D. Of. el Peru 2015, 569014–569017.

- KPMG. KPMG International Survey of Corporate Responsibility Reporting 2008; KPMG: Amsterdam, The Netherlands, 2008. [Google Scholar]

- KPMG. KPMG International Survey of Corporate Responsibility Reporting 2011; KPMG: Amsterdam, The Netherlands, 2011. [Google Scholar]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2013; KPMG: Amsterdam, The Netherlands, 2013. [Google Scholar]

- KPMG. Currents of Change: The KPMG Survey of Corporate Responsibility Reporting 2015; KPMG: Amsterdam, The Netherlands, 2015. [Google Scholar]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2017; KPMG: Amsterdam, The Netherlands, 2017. [Google Scholar]

- Fifka, M.S. Corporate Responsibility Reporting and its Determinants in Comparative Perspective—A Review of the Empirical Literature and a Meta-analysis. Bus. Strateg. Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of Sustainability Reporting: A Review of Results, Trends, Theory, and Opportunities in an Expanding Field of Research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Buchholz, R.A.; Rosenthal, S.B. Stakeholder Theory and Public Policy: How Governments Matter. J. Bus. Ethics 2004, 51, 143–153. [Google Scholar] [CrossRef]

- Albareda, L.; Tencati, A.; Lozano, J.M.; Perrini, F. The Government’s Role in Promoting Corporate Responsibility: A Comparative Analysis of Italy and UK from the Relational State Perspective. Corp. Gov. Int. J. Bus. Soc. 2006, 6, 386–400. [Google Scholar] [CrossRef]

- Albareda, L.; Lozano, J.M.; Ysa, T. Public Policies on Corporate Social Responsibility: The Role of Governments in Europe. J. Bus. Ethics 2007, 74, 391–407. [Google Scholar] [CrossRef]

- Albareda, L.; Lozano, J.M.; Midttun, A.; Perrini, F. The Changing Role of Governments in Corporate Social Responsibility: Drivers and Responses. Bus. Ethics A Eur. Rev. 2008, 17, 347–363. [Google Scholar] [CrossRef]

- Doh, J.P.; Guay, T.R. Corporate Social Responsibility, Public Policy, and NGO Activism in Europe and the United States: An Institutional-Stakeholder Perspective. J. Manag. Stud. 2006, 43, 47–73. [Google Scholar] [CrossRef]

- Moon, J.; Vogel, D. Corporate Social Responsibility, Government, and Civil Society. In The Oxford Handbook of Corporate Social Responsibility; Crane, A., Matten, D., McWilliams, A., Moon, J., Siegel, D.S., Eds.; Oxford University Press: Oxford, UK, 2009; pp. 303–323. ISBN 9780191576997. [Google Scholar]

- Steurer, R. The Role of Governments in Corporate Social Responsibility: Characterising Public Policies on CSR in Europe. Policy Sci. 2010, 43, 49–72. [Google Scholar] [CrossRef]

- Grewal, J.; Riedl, E.J.; Serafeim, G. Market Reaction to Mandatory Nonfinancial Disclosure. Manage. Sci. 2019, 65, 3061–3084. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting. In The Oxford Handbook of Corporate Social Responsibility, 2nd. ed.; McWilliams, A., Rupp, D.E., Siegel, D.S., Stahl, G.K., Waldman, D.A., Eds.; Oxford University Press: Oxford, UK, 2019; pp. 451–489. [Google Scholar]

- Jackson, G.; Bartosch, J.; Avetisyan, E.; Kinderman, D.; Knudsen, J.S. Mandatory Non-financial Disclosure and Its Influence on CSR: An International Comparison. J. Bus. Ethics 2019. [Google Scholar] [CrossRef]

- Lin-Hi, N.; Müller, K. The CSR Bottom Line: Preventing Corporate Social Irresponsibility. J. Bus. Res. 2013, 66, 1928–1936. [Google Scholar] [CrossRef]

- Mena, S.; Rintamäki, J.; Fleming, P.; Spicer, A. On the Forgetting of Corporate Irresponsibility. Acad. Manag. Rev. 2016, 41, 720–738. [Google Scholar] [CrossRef]

- Fifka, M.S.; Loza Adaui, C.R. Corporate Social Responsibility Reporting: Administrative Burden or Competitive Advantage. In Corporate Social Responsibility: Locating the Missing Link—New Perspectives on Sustainable Management Solutions; O’Riordan, L., Heinemann, S., Zmuda, P., Eds.; Springer: Heidelberg, Germany; New York, NY, USA, 2015; pp. 283–298. [Google Scholar]

- Hess, D. Social Reporting and New Governance Regulation: The Prospects of Achieving Corporate Accountability Through Transparency. Bus. Ethics Q. 2007, 17, 453–476. [Google Scholar] [CrossRef]

- Lock, I.; Seele, P. The Credibility of CSR (Corporate Social Responsibility) Reports in Europe. Evidence From a Quantitative Content Analysis in 11 Countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef]

- European Union. DIRECTIVE 2014/95/EU Of the European Parliament and of the Council—22 October 2014-Amending Directive 2013/34/EU as Regards Disclosure of Non-financial and Diversity Information by Certain Large Undertakings and Groups. Off. J. Eur. Union 2014, L330, 1–9. [Google Scholar]

- The Alliance for Corporate Transparency Project. 2018 Research Report: The State of Corporate Sustainability Disclosure Under the EU Non-financial Reporting Directive. Available online: https://www.allianceforcorporatetransparency.org/assets/2018_Research_Report_Alliance_Corporate_Transparency-66d0af6a05f153119e7cffe6df2f11b094affe9aaf4b13ae14db04e395c54a84.pdf (accessed on 8 September 2019).

- Venturelli, A.; Caputo, F.; Leopizzi, R.; Pizzi, S. The State of Art of Corporate Social Disclosure Before the Introduction of Non-financial Reporting Directive: A Cross Country Analysis. Soc. Responsib. J. 2019, 15, 409–423. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, F.; Cosma, S.; Leopizzi, R.; Pizzi, S. Directive 2014/95/EU: Are Italian Companies Already Compliant? Sustainability 2017, 9, 1385. [Google Scholar] [CrossRef]

- Carini, C.; Rocca, L.; Veneziani, M.; Teodori, C. Ex-Ante Impact Assessment of Sustainability Information—The Directive 2014/95. Sustainability 2018, 10, 560. [Google Scholar] [CrossRef]

- Ogrean, C. The Directive 2014/95/EU—Is there a “New” Beginning for CSR in Romania? Stud. Bus. Econ. 2017, 12, 141–147. [Google Scholar] [CrossRef]

- Szczepankiewicz, E.I.; Mućko, P. CSR Reporting Practices of Polish Energy and Mining Companies. Sustainability 2016, 8, 126. [Google Scholar] [CrossRef]

- Dumitru, M.; Dyduch, J.; Gușe, R.-G.; Krasodomska, J. Corporate Reporting Practices in Poland and Romania: An Ex-ante Study to the New Non-financial Reporting European Directive. Account. Eur. 2017, 14, 279–304. [Google Scholar] [CrossRef]

- Sierra-Garcia, L.; Garcia-Benau, M.A.; Bollas-Araya, H.M. Empirical Analysis of Non-Financial Reporting by Spanish Companies. Adm. Sci. 2018, 8, 29. [Google Scholar] [CrossRef]

- Torelli, R.; Balluchi, F.; Furlotti, K. The Materiality Assessment and Stakeholder Engagement: A Content Analysis of Sustainability Reports. Corp. Soc. Responsib. Environ. Manag. 2019. [Google Scholar] [CrossRef]

- Baumüller, J.; Schaffhauser-Linzatti, M.-M. In Search of Materiality for Nonfinancial Information—Reporting Requirements of the Directive 2014/95/EU. Nachhalt. Sustain. Manag. Forum 2018, 26, 101–111. [Google Scholar] [CrossRef]

- Saenger, I. Disclosure and Auditing of Corporate Social Responsibility Standards: The Impact of Directive 2014/95/EU on the German Companies Act and the German Corporate Governance Code. In Corporate Governance Codes for the 21st Century; du Plessis, J.J., Low, C.K., Eds.; Springer: Cham, Switzerland, 2017; pp. 261–273. [Google Scholar]

- Stawinoga, M. Die Richtlinie 2014/95/EU und das CSR-Richtlinie-Umsetzungsgesetz–Eine normative Analyse des Transformationsprozesses sowie daraus resultierender Implikationen für die Rechnungslegungs- und Prüfungspraxis. uwf UmweltWirtschaftsForum Sustain. Manag. Forum 2017, 25, 213–227. [Google Scholar]

- Hoffmann, E.; Dietsche, C.; Hobelsberger, C. Between Mandatory and Voluntary: Non-financial Reporting by German Companies. Nachhalt. | Sustain. Manag. Forum 2018, 26, 47–63. [Google Scholar] [CrossRef]

- Matuszak, Ł.; Rózańska, E. CSR Disclosure in Polish-Listed Companies in the Light of Directive 2014/95/EU Requirements: Empirical Evidence. Sustainability 2017, 9, 2304. [Google Scholar] [CrossRef]

- Frost, G.R. The Introduction of Mandatory Environmental Reporting Guidelines: Australian Evidence. Abacus 2007, 43, 190–216. [Google Scholar] [CrossRef]

- Gatti, L.; Vishwanath, B.; Seele, P.; Cottier, B. Are We Moving Beyond Voluntary CSR? Exploring Theoretical and Managerial Implications of Mandatory CSR Resulting from the New Indian Companies Act. J. Bus. Ethics 2018, 1–12. [Google Scholar] [CrossRef]

- Fatima, A.H.; Abdullah, N.; Sulaiman, M. Environmental Disclosure Quality: Examining the Impact of the Stock Exchange of Malaysia’s Listing Requirements. Soc. Responsib. J. 2015, 11, 904–922. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef]

- Gulenko, M. Mandatory CSR Reporting—Literature Review and Future Developments in Germany. Nachhalt. | Sustain. Manag. Forum 2018, 26, 3–17. [Google Scholar] [CrossRef]

- Hąbek, P.; Wolniak, R. Assessing the Quality of Corporate Social Responsibility Reports: The Case of Reporting Practices in Selected European Union Member States. Qual. Quant. 2016, 50, 399–420. [Google Scholar] [CrossRef] [PubMed]

- Perrault Crawford, E.; Clark Williams, C. Should Corporate Social Reporting be Voluntary or Mandatory? Evidence from the Banking Sector in France and the United States. Corp. Gov. Int. J. Bus. Soc. 2010, 10, 512–526. [Google Scholar] [CrossRef]

- Jackson, G.; Apostolakou, A. Corporate Social Responsibility in Western Europe: An Institutional Mirror or Substitute? J. Bus. Ethics 2010, 94, 371–394. [Google Scholar] [CrossRef]

- Ferri, L.M. The Influence of the Institutional Context on Sustainability Reporting. A Cross-National Analysis. Soc. Responsib. J. 2017, 13, 24–47. [Google Scholar] [CrossRef]

- Habisch, A.; Patelli, L.; Pedrini, M.; Schwartz, C. Different Talks with Different Folks: A Comparative Survey of Stakeholder Dialog in Germany, Italy, and the U.S. J. Bus. Ethics 2011, 100, 381–404. [Google Scholar] [CrossRef]

- Habisch, A.; Jonker, J.; Wegner, M.; Schmidpeter, R. (Eds.) Corporate Social Responsibility Across Europe; Springer: Berlin, Germany, 2005; ISBN 3-540-23251-6. [Google Scholar]

- Baldini, M.; Maso, L.D.; Liberatore, G.; Mazzi, F.; Terzani, S. Role of Country- and Firm-Level Determinants in Environmental, Social, and Governance Disclosure. J. Bus. Ethics 2018, 150, 79–98. [Google Scholar] [CrossRef]

- Scheuch, A. Soft Law Requirements with Hard Law Effects? The Influence of CSR on Corporate Law from a German Perspective. In Globalisation of Corporate Social Responsibility and its Impact on Corporate Governance; du Plessis, J.J., Varottil, U., Veldman, J., Eds.; Springer: Cham, Switzerland, 2018; pp. 203–229. ISBN 9783319691282. [Google Scholar]

- Mitra, N.; Schmidpeter, R. (Eds.) Mandated Corporate Social Responsibility:Eevidence from India; Springer: Cham, Switzerland, 2020; ISBN 9783030244446. [Google Scholar]

- Beretta, S.; Bozzolan, S. Quality versus Quantity: The Case of Forward-Looking Disclosure. J. Account. Audit. Financ. 2008, 23, 333–376. [Google Scholar] [CrossRef]

- Leuz, C.; Wysocki, P.D. Economic Consequences of Financial Reporting and Disclosure Regulation: A Review and Suggestions for Future Research. SSRN Electron. J. 2008, 79, 24. [Google Scholar] [CrossRef]

- Helfaya, A.; Whittington, M. Does Designing Environmental Sustainability Disclosure Quality Measures Make a Difference? Bus. Strateg. Environ. 2019, 28, 525–541. [Google Scholar] [CrossRef]

- Corporate Reporting Dialogue. Understanding the Value of Transparency and Accountability; International Integrated Reporting Council: London, UK, 2019. [Google Scholar]

- Corporate Reporting Dialogue. Statement of Common Principles of Materiality of the Corporate Reporting Dialogue; International Integrated Reporting Council: London, UK, 2016. [Google Scholar]

- Fox, T.; Ward, H.; Howard, B. Public Sector Roles in Strengthening Corporate Social Responsibility: A Baseline Study; The World Bank: Washington, DC, USA, 2002. [Google Scholar]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the Relation Between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Fang, X.; Li, Y.; Richardson, G. The Relevance of Environmental Disclosures: Are Such Disclosures Incrementally Informative? J. Account. Public Policy 2013, 32, 410–431. [Google Scholar] [CrossRef]

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring More Sustainable Reporting in Europe using Non-financial Disclosure-de Facto and de Jure Evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef]

- Helfaya, A.; Kotb, A. Environmental Reporting Quality. In Handbook of Research on Green Economic Development Initiatives and Strategies; Erdoğdu, M.M., Arun, T., Ahmad, I.H., Eds.; IGI Global: Hershey, PA, USA, 2016; pp. 625–654. [Google Scholar]

- Helfaya, A.; Whittington, M.; Alawattage, C. Exploring the Quality of Corporate Environmental Reporting. Account. Audit. Account. J. 2019, 32, 163–193. [Google Scholar] [CrossRef]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR Reporting Practices and the Quality of Disclosure: An Empirical Analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. The Effect of Mandatory Publication of Nonfinancial Disclosurein Europe on Sustainability Reporting Quality: First Insights About Italian and German Companies. In Non-Financial Disclosure and Integrated Reporting: Practices and Critical Issues; Songini, L., Pistoni, A., Baret, P., Kunc, M., Eds.; Emerald Publishing Limited: Bingley, UK, 2020; pp. 55–80. ISBN 9781838679644. [Google Scholar]

- Moreno, A.; Capriotti, P. Communicating CSR, Citizenship and Sustainability on the Web. J. Commun. Manag. 2009, 13, 157–175. [Google Scholar] [CrossRef]

- El-Bassiouny, D.; El-Bassiouny, N. Diversity, Corporate Governance and CSR Reporting. Manag. Environ. Qual. Int. J. 2019, 30, 116–136. [Google Scholar] [CrossRef]

- Kühn, A.-L.; Stiglbauer, M.; Fifka, M.S. Contents and Determinants of Corporate Social Responsibility Website Reporting in Sub-Saharan Africa: A Seven-Country Study. Bus. Soc. 2018, 57, 437–480. [Google Scholar] [CrossRef]

- Etikan, I. Comparison of Convenience Sampling and Purposive Sampling. Am. J. Theor. Appl. Stat. 2016, 5, 1. [Google Scholar] [CrossRef]

- Sutantoputra, A.W. Social Disclosure Rating System for Assessing Firms’ CSR Reports. Corp. Commun. 2009, 14, 34–48. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. Credibility of Sustainability Reports: The Contribution of Audit Committees. Bus. Strateg. Environ. 2018, 27, 973–986. [Google Scholar] [CrossRef]

- Chauvey, J.-N.; Giordano-Spring, S.; Cho, C.H.; Patten, D.M. The Normativity and Legitimacy of CSR Disclosure: Evidence from France. J. Bus. Ethics 2015, 130, 789–803. [Google Scholar] [CrossRef]

- Dando, N.; Swift, T. Transparency and Assurance: Minding the Credibility Gap. J. Bus. Ethics 2003, 44, 195–200. [Google Scholar] [CrossRef]

- Hummel, K.; Schlick, C. The Relationship between Sustainability Performance and Sustainability Disclosure—Reconciling Voluntary Disclosure Theory and Legitimacy Theory. J. Account. Public Policy 2016, 35, 455–476. [Google Scholar] [CrossRef]

- Braam, G.J.M.; Uit De Weerd, L.; Hauck, M.; Huijbregts, M.A.J. Determinants of Corporate Environmental Reporting: The Importance of Environmental Performance and Assurance. J. Clean. Prod. 2016, 129, 724–734. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the Adoption of Sustainability Assurance Statements: An International Investigation. Bus. Strateg. Environ. 2010, 19, 182–198. [Google Scholar] [CrossRef]

- Peters, G.F.; Romi, A.M. The Association between Sustainability Governance Characteristics and the Assurance of Corporate Sustainability Reports. Audit. A J. Pract. Theory 2015, 34, 163–198. [Google Scholar] [CrossRef]

- Rossi, A.; Tarquinio, L. An Analysis of Sustainability Report Assurance Statements Evidence from Italian Listed Companies. Manag. Audit. J. 2017, 32, 578–602. [Google Scholar] [CrossRef]

- Simnett, R.; Vanstraelen, A.; Chua, W.F. Assurance on Sustainability Reports: An International Comparison. Account. Rev. 2009, 84, 937–967. [Google Scholar] [CrossRef]

- Font, X.; Guix, M.; Bonilla-Priego, M.J. Corporate Social Responsibility in Cruising: Using Materiality Analysis to Create Shared Value. Tour. Manag. 2016, 53, 175–186. [Google Scholar] [CrossRef]

- Khan, M.; Serafeim, G.; Yoon, A. Corporate Sustainability: First Evidence on Materiality. Account. Rev. 2016, 91, 1697–1724. [Google Scholar] [CrossRef]

- Bellantuono, N.; Pontrandolfo, P.; Scozzi, B. Capturing the Stakeholders’ View in Sustainability reporting: A novel approach. Sustainability 2016, 8, 379. [Google Scholar] [CrossRef]

- Manetti, G. The Quality of Stakeholder Engagement in Sustainability Reporting: Empirical Evidence and Critical Points. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 110–122. [Google Scholar] [CrossRef]

- Manetti, G.; Toccafondi, S. The Role of Stakeholders in Sustainability Reporting Assurance. J. Bus. Ethics 2012, 107, 363–377. [Google Scholar] [CrossRef]

- Greenwood, M. Stakeholder Engagement: Beyond the Myth of Corporate Responsibility. J. Bus. Ethics 2007, 74, 315–327. [Google Scholar] [CrossRef]

- Moratis, L.; Brandt, S. Corporate Stakeholder Responsiveness? Exploring the State and Quality of GRI-based Stakeholder Engagement Disclosures of European Firms. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 312–325. [Google Scholar] [CrossRef]

- Barkemeyer, R.; Comyns, B.; Figge, F.; Napolitano, G. CEO Statements in Sustainability Reports: Substantive Information or Background Noise? Account. Forum 2014, 38, 241–257. [Google Scholar] [CrossRef]

- da Silva Monteiro, S.M.; Aibar-Guzmán, B. Determinants of Environmental Disclosure in the Annual Reports of Large Companies Operating in Portugal. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 185–204. [Google Scholar] [CrossRef]

- Michelon, G.; Patten, D.M.; Romi, A.M. Creating Legitimacy for Sustainability Assurance Practices: Evidence from Sustainability Restatements. Eur. Account. Rev. 2019, 28, 395–422. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The Influence of Governance Structure and Strategic Corporate Social Responsibility Toward Sustainability Reporting Quality. Bus. Strateg. Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Cho, C.H.; Michelon, G.; Patten, D.M. Impression Management in Sustainability Reports: An Empirical Investigation of the Use of Graphs. Account. Public Interes. 2012, 12, 16–37. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Factors Influencing the Quality of Corporate Environmental Disclosure. Bus. Strateg. Environ. 2008, 17, 120–136. [Google Scholar] [CrossRef]

- Criado-Jiménez, I.; Fernández-Chulián, M.; Larrinaga-González, C.; Husillos-Carqués, F.J. Compliance with Mandatory Environmental Reporting in Financial Statements: The Case of Spain (2001–2003). J. Bus. Ethics 2008, 79, 245–262. [Google Scholar] [CrossRef]

- Adler, R.W.; Milne, M.J. Exploring the Reliability of Social and Environmental Disclosures Content Analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar]

- Krippendorff, K. Reliability in Content Analsis. Hum. Commun. Res. 2004, 30, 411–433. [Google Scholar]

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology, 4th ed.; SAGE: Los Angeles, CA, USA, 2004. [Google Scholar]

- Fifka, M.S. The Development and State of Research on Social and Environmental Reporting in Global Comparison. J. für Betr. 2012, 62, 45–84. [Google Scholar] [CrossRef]

- Camodeca, R.; Almici, A.; Sagliaschi, U. Sustainability Disclosure in Integrated Reporting: Does It Matter to Investors? A Cheap Talk Approach. Sustainability 2018, 10, 4393. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of Voluntary CSR Disclosure: Empirical Evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef]

| 2014 | 2015 | 2016 | ||||

|---|---|---|---|---|---|---|

| Industrial Sector | STA | INT | STA | INT | STA | INT |

| Consumer goods | 2 | 1 | 2 | 1 | 2 | 1 |

| Mining and extractive | 4 | 4 | 4 | 4 | 5 | 3 |

| Energy, utilities, and oil | 1 | 4 | 1 | 4 | 1 | 4 |

| Finance and insurance | 3 | 2 | 3 | 2 | 3 | 2 |

| Cement and construction | 3 | - | 2 | 1 | 2 | 1 |

| Iron and steel | - | 2 | - | 2 | 1 | 1 |

| Industrial | - | 1 | 1 | - | 1 | - |

| Total | 13 | 14 | 13 | 14 | 15 | 12 |

| Quality Dimension | SRQ Indicator |

|---|---|

| CRE: Standards | Explicit adoption of external sustainability reporting standards for the elaboration of the sustainability disclosure document [78,97,114,125,126,127,128,129]. |

| CRE: Assurance | Inclusion of third-party independent assurance of sustainability report or assurance of sustainability information in integrated report [97,114,120,128,130,131,132,133,134]. |

| CRE: Accuracy | Inclusion of a section with methodological clarifications regarding the sustainability disclosure document [78]. |

| CRE: Materiality | Inclusion of a materiality analysis in sustainability disclosure document [88,89,97,112,135,136]. |

| CRE: Stakeholder dialogue | Evidence of stakeholder dialogue in sustainability disclosure document [97,104,137,138,139]. |

| CRE: Stakeholder engagement | Evidence of stakeholder engagement including a description of the instruments used for different stakeholders [97,104,138,139,140,141]. |

| CRE: Top management | Inclusion of a top management statement in stand-alone reports or reference to sustainability in top management statements of integrated reports [81,82,97,119,142,143]. |

| CRE: Strategy | Description of a sustainability policy or sustainability strategy in sustainability disclosure document [81,82,97,143,144]. |

| CRE: Governance | Existence of a sustainability governance entity in the organizational structure [122,126,132,145]. |

| CON: Environment | Disclosure of Greenhouse Gas Emissions in sustainability disclosure document [56,81,82,144]. |

| CON: Environment | Disclosure of energy consumption in sustainability disclosure document [56,81,82,144]. |

| CON: Environment | Disclosure of water consumption in sustainability disclosure document [56,81,82,144]. |

| CON: Environment | Disclosure of waste management in sustainability disclosure document [56,81,82,144]. |

| CON: Social | Disclosure of information regarding social issues in sustainability disclosure document [56,81,82,144]. |

| CON: Social | Disclosure of information regarding personnel and labor issues in sustainability disclosure document [56,81,82,144]. |

| CON: Social | Disclosure of information regarding community relations in sustainability disclosure document [56,81,82,144]. |

| CON: Socio-economic | Disclosure of information regarding suppliers in sustainability disclosure document [56,81,82,144]. |

| CON: Socio-economic | Disclosure of information regarding clients in sustainability disclosure document [56,81,82,144]. |

| CON: Social | Disclosure of information regarding human rights issues in sustainability disclosure document [56,81,82,144]. |

| CON: Social | Disclosure of information regarding anti-corruption and bribery issues [56,81,82,144]. |

| COM: Communication | Inclusion of tables in sustainability disclosure document [110,117,118]. |

| COM: Communication | Inclusion of graphs in sustainability disclosure document [110,117,118,146]. |

| COM: Communication | Inclusion of pictures/images in sustainability disclosure document [110,117,118]. |

| Number of Indicators | 2014 (N = 27) | 2015 (N = 27) | 2016 (N = 27) | |

|---|---|---|---|---|

| SRQ | 23 | 0.952 | 0.945 | 0.908 |

| Credibility | 9 | 0.925 | 0.919 | 0.903 |

| Content | 11 | 0.909 | 0.899 | 0.806 |

| Communication | 3 | 0.821 | 0.612 | 0.532 |

| 2014 | 2015 | 2016 | Total | |||||

|---|---|---|---|---|---|---|---|---|

| SRQ Indicators | f | f/n | f | f/n | f | f/n | Mean | |

| SRQ01 | Sustainability reporting standards | 16 | 0.59 | 16 | 0.59 | 17 | 0.63 | 0.60 |

| SRQ02 | Independent assurance | 6 | 0.22 | 4 | 0.15 | 3 | 0.11 | 0.16 |

| SRQ03 | Methodological section | 14 | 0.52 | 17 | 0.63 | 18 | 0.67 | 0.60 |

| SRQ04 | Materiality analysis | 12 | 0.44 | 13 | 0.48 | 18 | 0.63 | 0.52 |

| SRQ05 | Stakeholder dialogue | 18 | 0.67 | 17 | 0.63 | 20 | 0.74 | 0.68 |

| SRQ06 | Stakeholder engagement | 12 | 0.44 | 12 | 0.44 | 12 | 0.44 | 0.44 |

| SRQ07 | Top management statement | 20 | 0.74 | 21 | 0.78 | 24 | 0.89 | 0.80 |

| SRQ08 | Sustainability policy or strategy | 18 | 0.67 | 18 | 0.67 | 24 | 0.89 | 0.74 |

| SRQ09 | Sustainability governance | 11 | 0.41 | 13 | 0.48 | 14 | 0.52 | 0.47 |

| SRQ10 | Greenhouse Gas Emissions | 15 | 0.56 | 18 | 0.67 | 20 | 0.74 | 0.65 |

| SRQ11 | Energy consumption | 18 | 0.67 | 20 | 0.74 | 23 | 0.85 | 0.75 |

| SRQ12 | Water consumption | 16 | 0.59 | 21 | 0.78 | 20 | 0.74 | 0.70 |

| SRQ13 | Waste management | 23 | 0.85 | 24 | 0.89 | 24 | 0.89 | 0.88 |

| SRQ14 | Social issues | 25 | 0.93 | 24 | 0.89 | 26 | 0.96 | 0.93 |

| SRQ15 | Personnel and labor issues | 25 | 0.93 | 26 | 0.96 | 26 | 0.96 | 0.95 |

| SRQ16 | Community relations | 24 | 0.89 | 24 | 0.89 | 26 | 0.96 | 0.91 |

| SRQ17 | Suppliers relations | 29 | 0.70 | 28 | 0.67 | 24 | 0.89 | 0.75 |

| SRQ18 | Clients relations | 20 | 0.74 | 22 | 0.81 | 23 | 0.85 | 0.80 |

| SRQ19 | Human rights issues | 13 | 0.48 | 15 | 0.56 | 17 | 0.63 | 0.56 |

| SRQ20 | Anti-corruption and bribery | 15 | 0.56 | 15 | 0.56 | 14 | 0.52 | 0.54 |

| SRQ21 | Inclusion of tables | 26 | 0.96 | 27 | 1.00 | 27 | 1.00 | 0.99 |

| SRQ22 | Inclusion of graphs | 21 | 0.78 | 23 | 0.85 | 25 | 0.93 | 0.85 |

| SRQ23 | Inclusion of pictures and images | 21 | 0.78 | 20 | 0.74 | 22 | 0.81 | 0.78 |

| Year | N | Min | Max | Mean | Std Dev. |

|---|---|---|---|---|---|

| 2014 | 27 | 0.20 | 3.00 | 2.0793 | 0.89766 |

| 2015 | 27 | 0.61 | 3.00 | 2.1676 | 0.79034 |

| 2016 | 27 | 1.17 | 3.00 | 2.3449 | 0.59493 |

| Year | Credibility | Content | Communication | SRQ |

|---|---|---|---|---|

| 2014 | 0.5226 | 0.7172 | 0.8395 | 2.0793 |

| 2015 | 0.5391 | 0.7643 | 0.8642 | 2.1676 |

| 2016 | 0.6132 | 0.8182 | 0.9136 | 2.3449 |

| 2014 | 2015 | 2016 | Total | |||||

|---|---|---|---|---|---|---|---|---|

| N | Mean | N | Mean | N | Mean | N | Mean | |

| Reporting form | ||||||||

| Stand-alone reports | 13 | 2.6107 | 13 | 2.6426 | 15 | 2.6020 | 41 | 2.6184 |

| Integrated reports | 14 | 1.5859 | 14 | 1.7266 | 12 | 2.0236 | 40 | 1.7787 |

| Industry affiliation | ||||||||

| Mining industry | 8 | 2.0884 | 8 | 2.3371 | 8 | 2.5859 | 24 | 2.3371 |

| Finance and insurance | 5 | 2.2162 | 5 | 2.1535 | 5 | 2.3192 | 15 | 2.2296 |

| Energy, electricity, and oil | 10 | 2.0828 | 10 | 2.0414 | 10 | 2.3394 | 30 | 2.1545 |

| Other industries | 4 | 1.8813 | 4 | 2.1616 | 4 | 1.9091 | 12 | 1.9840 |

| Environmentally-sensitive industry | ||||||||

| Yes | 18 | 2.0595 | 18 | 2.1717 | 18 | 2.4416 | 54 | 2.2242 |

| No | 9 | 2.0892 | 9 | 2.1594 | 9 | 2.1515 | 27 | 2.1333 |

| Membership of transnational groups | ||||||||

| Domestic company | 14 | 2.1962 | 14 | 2.2734 | 14 | 2.4221 | 42 | 2.2972 |

| International company | 13 | 1.9534 | 13 | 2.0536 | 13 | 2.2618 | 39 | 2.0896 |

| Company | SRQ 2014 | SRQ 2015 | SRQ2016 | Δ 2015–2014 | Δ 2016–2015 | Δ 2016–2014 |

|---|---|---|---|---|---|---|

| PE01 | 2.4141 | 1.3838 | 1.2020 | −1.0303 | −0.1818 | −1.2121 |

| PE02 | 1.7677 | 1.7879 | 1.6768 | 0.0202 | −0.1111 | −0.0909 |

| PE03 | 0.2020 | 2.2424 | 1.7273 | 2.0404 | −0.5152 | 1.5253 |

| PE04 | 3.0000 | 3.0000 | 3.0000 | 0.0000 | 0.0000 | 0.0000 |

| PE05 | 3.0000 | 2.5556 | 2.6667 | −0.4444 | 0.1111 | −0.3333 |

| PE06 | 0.6970 | 0.8081 | 1.5455 | 0.1111 | 0.7374 | 0.8485 |

| PE07 | 2.8182 | 2.8889 | 2.8889 | 0.0707 | 0.0000 | 0.0707 |

| PE08 | 2.7778 | 2.7778 | 2.6869 | 0.0000 | −0.0909 | −0.0909 |

| PE09 | 0.9899 | 1.6768 | 1.7879 | 0.6869 | 0.1111 | 0.7980 |

| PE10 | 2.6667 | 2.8889 | 2.7778 | 0.2222 | −0.1111 | 0.1111 |

| PE11 | 1.2020 | 1.1818 | 2.7980 | −0.0202 | 1.6162 | 1.5960 |

| PE12 | 2.5556 | 2.1111 | 2.4848 | −0.4444 | 0.3737 | −0.0707 |

| PE13 | 0.7879 | 0.6970 | 1.2626 | −0.0909 | 0.5657 | 0.4747 |

| PE14 | 2.4444 | 2.4444 | 2.4848 | 0.0000 | 0.0404 | 0.0404 |

| PE15 | 1.6566 | 1.7273 | 2.2424 | 0.0707 | 0.5152 | 0.5859 |

| PE16 | 2.7778 | 2.7778 | 2.6667 | 0.0000 | −0.1111 | −0.1111 |

| PE17 | 2.7071 | 2.7980 | 2.7980 | 0.0909 | 0.0000 | 0.0909 |

| PE18 | 0.9899 | 0.8990 | 1.1717 | −0.0909 | 0.2727 | 0.1818 |

| PE19 | 2.7071 | 2.8889 | 2.7980 | 0.1818 | −0.0909 | 0.0909 |

| PE20 | 2.5556 | 1.9495 | 1.8384 | −0.6061 | −0.1111 | −0.7172 |

| PE21 | 2.8889 | 2.8889 | 2.5758 | 0.0000 | −0.3131 | −0.3131 |

| PE22 | 2.6162 | 2.6162 | 2.7071 | 0.0000 | 0.0909 | 0.0909 |

| PE23 | 0.5152 | 0.6061 | 2.7980 | 0.0909 | 2.1919 | 2.2828 |

| PE24 | 2.8889 | 2.8889 | 2.8889 | 0.0000 | 0.0000 | 0.0000 |

| PE25 | 3.0000 | 3.0000 | 3.0000 | 0.0000 | 0.0000 | 0.0000 |

| PE26 | 2.1313 | 2.2424 | 2.0404 | 0.1111 | −0.2020 | −0.0909 |

| PE27 | 1.3838 | 2.7980 | 2.7980 | 1.4141 | 0.0000 | 1.4141 |

| Effect | Δ 2015–2014 | Δ 2016–2015 | Δ 2016–2014 |

|---|---|---|---|

| SRQ increases | 12 | 11 | 15 |

| SRQ decreases | 7 | 10 | 9 |

| No change in SRQ | 8 | 6 | 3 |

| Δ 2015–2014 | Δ 2016–2015 | Δ 2016–2014 | ||||

|---|---|---|---|---|---|---|

| Z | p | Z | p | Z | p | |

| SRQ | −0.866 | 0.386 | −0.906 | 0.365 | −1.531 | 0.126 |

| Credibility | −0.617 | 0.537 | −1.130 | 0.258 | −1.543 | 0.123 |

| Content | −0.860 | 0.390 | −0.804 | 0.421 | −1.402 | 0.161 |

| Communication | −0.412 | 0.680 | −1.633 | 0.102 | −1.382 | 0.167 |

| Reporting form | ||||||

| Stand-alone reports | −1.572 | 0.116 | −0.102 | 0.919 | −1.179 | 0.239 |

| Integrated reports | −0.210 | 0.833 | −1.158 | 0.247 | −0.864 | 0.387 |

| Industry affiliation | ||||||

| Mining industry | −1.363 | 0.173 | −0.137 | 0.891 | −1.572 | 0.116 |

| Finance and insurance | 0.000 | 1.00 | −0.921 | 0.357 | −0.184 | 0.854 |

| Energy, electricity, and oil | −0.682 | 0.495 | −1.680 | 0.093 * | −1.378 | 0.168 |

| Other industries | −0.535 | 0.593 | −1.826 | 0.068 * | −0.365 | 0.715 |

| Environmentally-sensitive industry | ||||||

| Yes | −0.707 | 0.479 | −1.385 | 0.166 | −1.733 | 0.083 * |

| No | −0.508 | 0.611 | −0.593 | 0.553 | −0.142 | 0.887 |

| Membership of transnational groups | ||||||

| Domestic company | −1.020 | 0.308 | −0.463 | 0.643 | −0.809 | 0.419 |

| International company | −0.178 | 0.858 | −0.845 | 0.398 | −1.156 | 0.248 |

| Industry Affiliation | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mining Industry (N = 8) | Finance and Insurance (N = 5) | Energy, Electricity, Extractive, and Oil (N = 10) | Other Industries (N = 4) | |||||||||

| CRE | CON | COM | CRE | CON | COM | CRE | CON | COM | CRE | CON | COM | |

| 2014 | 0.5278 | 0.7273 | 0.8333 | 0.6222 | 0.7273 | 0.8667 | 0.4889 | 0.7273 | 0.8667 | 0.4722 | 0.6591 | 0.7500 |

| 2015 | 0.6667 | 0.7955 | 0.8750 | 0.6444 | 0.7091 | 0.8000 | 0.4444 | 0.7636 | 0.8333 | 0.3889 | 0.7727 | 1.000 |

| 2016 | 0.7639 | 0.8636 | 0.9583 | 0.6889 | 0.7636 | 0.8667 | 0.6000 | 0.8727 | 0.8667 | 0.2500 | 0.6591 | 1.000 |

| Δ 2015–2014 | 0.1389 | 0.0682 | 0.0417 | 0.0222 | −0.0182 | −0.0667 | −0.0445 | 0.0363 | −0.0334 | −0.0833 | 0.1136 | 0.25 |

| p | 0.109 | 0.588 | 0.655 | 0.564 | 0.317 | 0.317 | 0.046 * | 0.234 | 0.317 | 1.00 | 0.655 | 0.317 |

| Z | −1.604 | −0.542 | −0.447 | −0.577 | −1.000 | −1.000 | −2.000 | −1.190 | −1.000 | 0.000 | −0.447 | −1.000 |

| Δ 2016–2015 | 0.0972 | 0.0681 | 0.0833 | 0.0445 | 0.0545 | 0.0667 | 0.1556 | 0.1091 | 0.0334 | −0.1389 | −0.1136 | - |

| p | 0.705 | 0.655 | 0.317 | 0.414 | 0.180 | 0.317 | 0.112 | 0.324 | 0.317 | 0.102 | 0.102 | - |

| Z | −0.378 | −0.447 | −1.000 | −0.816 | −1.342 | −1.000 | −0.1.590 | −0.986 | −1.000 | −1.633 | −1.633 | - |

| Δ 2016–2014 | 0.2361 | 0.1363 | 0.125 | 0.0667 | 0.0363 | - | 0.1111 | 0.1454 | - | −0.2222 | - | 0.25 |

| p | 0.104 | 0.416 | 0.276 | 0.317 | 0.414 | - | 0.230 | 0.198 | - | 0.102 | - | 0.317 |

| Z | −1.625 | −0.813 | −1.089 | −1.000 | −0.816 | - | −1.200 | −1.287 | - | −1.633 | - | −1.000 |

| Environmentally-Sensitive Industry | Membership of Transnational Groups | |||||||||||

| Yes (N = 18) | No (N = 9) | Domestic Company (N = 14) | International Company (N = 13) | |||||||||

| CRE | CON | COM | CRE | CON | COM | CRE | CON | COM | CRE | CON | COM | |

| 2014 | 0.5000 | 0.7374 | 0.8519 | 0.5679 | 0.6768 | 0.8148 | 0.6032 | 0.6883 | 0.9048 | 0.4359 | 0.7483 | 0.7692 |

| 2015 | 0.5370 | 0.7828 | 0.8519 | 0.5432 | 0.7273 | 0.8889 | 0.6111 | 0.7338 | 0.9286 | 0.4615 | 0.7972 | 0.7949 |

| 2016 | 0.6605 | 0.8737 | 0.9074 | 0.5185 | 0.7071 | 0.9259 | 0.6905 | 0.7792 | 0.9524 | 0.5299 | 0.8601 | 0.8718 |

| Δ 2015–2014 | 0.0370 | 0.0454 | - | −0.0247 | 0.0505 | 0.0741 | 0.0079 | 0.0455 | 0.0238 | 0.0256 | 0.0489 | 0.0257 |

| p | 0.726 | 0.325 | - | 0.666 | 0.854 | 0.655 | 0.942 | 0.394 | 0.655 | 0.334 | 0.750 | 1.000 |

| Z | −0.351 | −0.984 | - | −0.431 | −0.184 | −0.447 | −0.073 | −0.852 | −0.447 | −0.966 | −0.318 | 0.000 |

| Δ 2016–2015 | 0.1235 | 0.0909 | 0.0555 | −0.0247 | −0.0202 | 0.0370 | 0.0794 | 0.0454 | 0.0238 | 0.0684 | 0.0629 | 0.0769 |

| p | 0.126 | 0.239 | 0.180 | 0.680 | 0.581 | 0.317 | 0.236 | 0.671 | 0.317 | 0.571 | 0.473 | 0.180 |

| Z | −1.531 | −1.178 | −1.342 | −0.412 | −0.552 | −1.000 | −1.186 | −0.425 | −1.000 | −0.566 | −0.718 | −1.342 |

| Δ 2016–2014 | 0.1605 | 0.1363 | 0.0555 | −0.0494 | 0.0303 | 0.1111 | 0.0873 | 0.0909 | 0.0476 | 0.0940 | 0.1118 | 0.1026 |

| p | 0.060 ** | 0.147 | 0.276 | 0.593 | 0.606 | 0.414 | 0.309 | 0.222 | 0.414 | 0.250 | 0.283 | 0.285 |

| Z | −1.879 | −1.451 | −1.089 | −0.535 | −0.516 | −0.816 | −1.018 | −1.222 | −0.816 | −1.150 | −1.074 | −1.069 |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Loza Adaui, C.R. Sustainability Reporting Quality of Peruvian Listed Companies and the Impact of Regulatory Requirements of Sustainability Disclosures. Sustainability 2020, 12, 1135. https://doi.org/10.3390/su12031135

Loza Adaui CR. Sustainability Reporting Quality of Peruvian Listed Companies and the Impact of Regulatory Requirements of Sustainability Disclosures. Sustainability. 2020; 12(3):1135. https://doi.org/10.3390/su12031135

Chicago/Turabian StyleLoza Adaui, Cristian R. 2020. "Sustainability Reporting Quality of Peruvian Listed Companies and the Impact of Regulatory Requirements of Sustainability Disclosures" Sustainability 12, no. 3: 1135. https://doi.org/10.3390/su12031135

APA StyleLoza Adaui, C. R. (2020). Sustainability Reporting Quality of Peruvian Listed Companies and the Impact of Regulatory Requirements of Sustainability Disclosures. Sustainability, 12(3), 1135. https://doi.org/10.3390/su12031135