1. Introduction

Institutions are crucial for understanding the shape of human interaction. “In consequence, they structure incentives in human exchange, whether political, social, or economic” [

1]. After the publication of North’s work, the institutionalist literature increased exponentially, allowing the use and debate of the concept in many fields, from economics to politics and management. Many development economists and academics from sociology, anthropology and political science recognized the consistency of North’s arguments; they were sure of the value of their insights into the development process and, in particular, into the economic significance of institutions other than markets. The works of Ostrom [

2] and Acemoglu, Johnson and Robinson [

3] are under the influence of North’s work, and they are the basis of the analysis that influenced the literature in development, internationalization and competitiveness.

In this sense, it is widely acknowledged, both on empirical and theoretical discussions, that the institutional quality is closely related to growth and economic development. The set of institutions (inclusive and extractive) in a specific economy is called the institutional framework [

3,

4,

5,

6,

7].

It is also widely accepted that the internationalization of economies is not only driven by specific industry conditions [

8] or business-specific differences [

9] but also by the institutions that exist as background conditions that directly determine the strategies and interactions of firms with the institutional environment [

10,

11,

12,

13,

14,

15,

16,

17,

18,

19,

20].

Home country institutions’ importance for economic actors’ performance is well known in the literature [

1,

21,

22]. Extant literature regarded the home market’s structural environment as either supportive or constraining decisions for foreign expansion. The rationale is that strategic decisions, such as the outward FDI (OFDI) undertaking, are guided by industrial and firm-specific resources and reflect the formal and informal supports-constraints faced by managers in a specific institutional context.

Literature shows two different structural forces that influence firms’ OFDI decisions from emerging markets [

23]. On the one hand, in emerging markets, institutional environments are troubled by a poor defense of property rights, insufficient laws and judicial regulation, an unpredictable political climate and other ineffective institutions that serve the sector. In essence, these inefficiencies affect the availability and quality of factor inputs and thus limit companies’ production pursuits. Therefore, internationalization is a reaction to the escape of domestic markets from the stifling bureaucratic climate. On the other hand, emerging markets governments promote local companies through a combination of formal and informal incentives to seek international expansion [

23]. Despite their lack of clear ownership benefits, such institutional support helps emerging market firms resolve foreign liability and seek international expansion. Firms would have a distinct tendency to adapt to the stresses of the home country’s institutional environment.

For this study, we reviewed works with an explicit focus on the institutional framework in emerging economies. We established three criteria to identify relevant articles to analyze within the limits of the present study: (1) that they describe the role of institutions in emerging economies; (2) that they are published in journals (Q1 and Q2) that can be accessed through Scopus; and (3) that they are published between the years 2000 and 2020. The findings of the literature review will be discussed in detail in

Section 3.

Nonetheless, significant literature focuses on establishing the relation between institutional quality and OFDI [

24,

25,

26,

27,

28,

29,

30,

31,

32,

33,

34,

35]; this paper contributes to the existing literature in at least three ways. First, our paper differs from previous studies in the data sources used and the indicators selected to measure institutional quality; we used the Fragile States Index as an alternative source. Second, we propose a methodological approach that combines multivariate analysis and panel data techniques, which allows us to reduce the number of variables and avoid collinearity problems keeping the most representative variables to explain how institutional framework affects OFDI. Third, we selected Emerging and Developing economies because they are beneficial for studying the causes and consequences of institutional variations; for this purpose, we built a data panel with 30 variables for 48 countries in the years 2007–2017.

This paper is structured as follows;

Section 2 briefly reviews the theoretical approaches and develops the hypothesis;

Section 3 describes the literature review findings and the methodological approach;

Section 4 presents the results and discussion;

Section 5 and

Section 6 present the conclusions, limitations and future research directions.

2. Theoretical Approaches and Hypothesis Development on Institutional Quality and Outward FDI

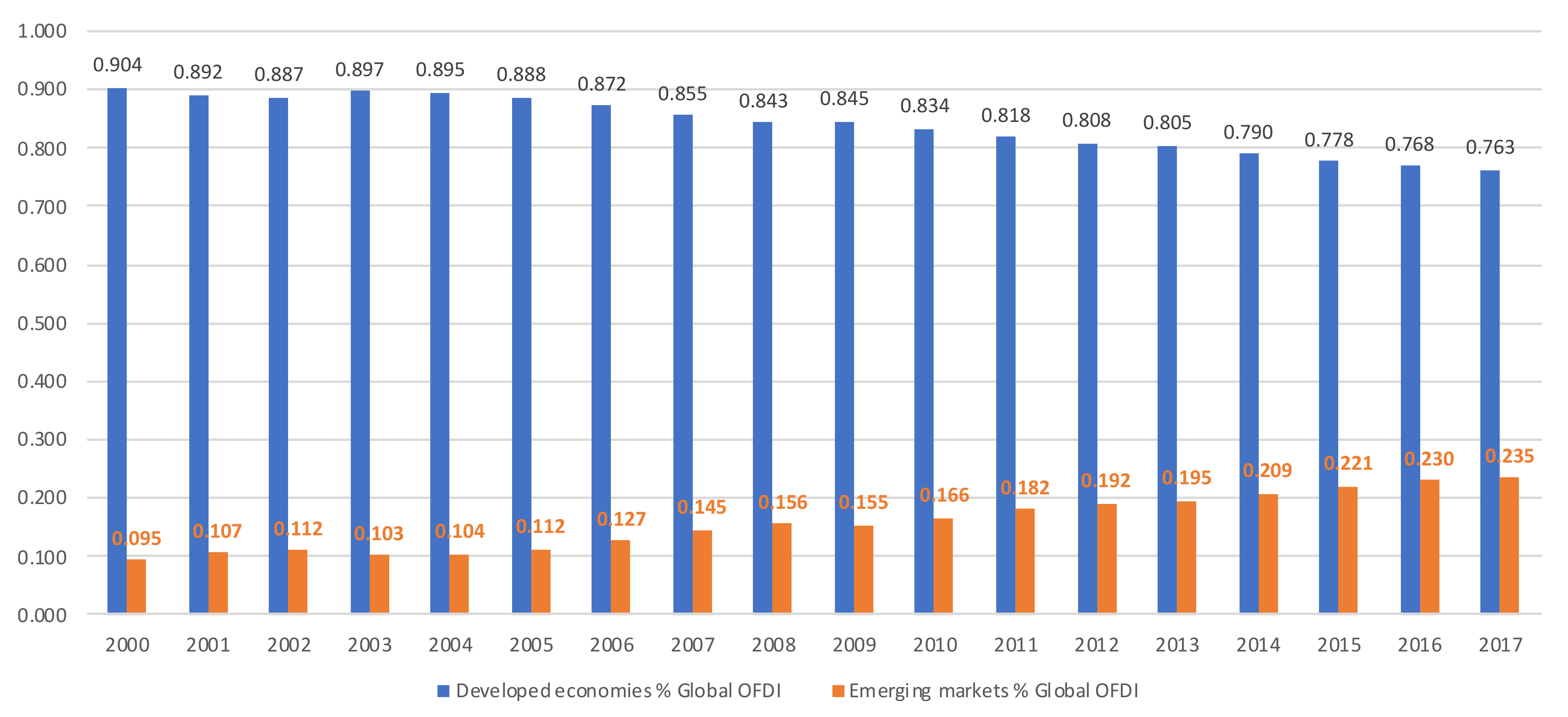

The stocks of OFDI grew dramatically in recent years, from nearly 1% of global stocks in 2000 up to 23.5% in 2017, see

Figure 1. The rise of OFDI has different motivations, including the need to develop new markets, the need for a way to leverage capital and technology, as well as the need for a way to gain knowledge in international markets [

24,

36,

37]. Another point of view is the escape OFDI, in this case, firms look for international markets to avoid institutional misalignments or uneven conditions hindering competition in their home countries [

38,

39,

40].

In the first case, it is necessary to consider the institutional framework that contributes to developing firms’ ownership advantages as proposed by Dunning. These advantages include unique assets relating to technological know-how, marketing expertise and managerial skills that help the firm to compete in local and foreign markets [

12,

19,

20,

42].

According to Dunning [

19] as well as Narula and Kodiyat [

30], firms require a good knowledge infrastructure to foster innovation and absorptive capacity, which are known to be some of the ownership advantages needed for a firm to pursue OFDI. An adequate home country knowledge environment ensures the creation and dissemination of knowledge, the protection of knowledge and creating a skilled workforce [

30].

One crucial component of the home country knowledge environment is the protection of intellectual property; the stronger the protection of intellectual property, the better the research and development (R&D) of firms [

43]. A rule of law that protects intellectual property promotes the R&D endeavor of firms at home, and fosters them to engage in OFDI to gain ground-breaking capabilities [

38,

39,

40,

41,

42,

43,

44,

45,

46]; hence, strong intellectual property protection positively influences OFDI.

Another pillar of the home country knowledge environment is skilled human capital; having a well-trained labor force is essential for a firm to deal with the complexities of managing and operating in international contexts. The availability of a skilled workforce helps in the process of assimilation, adoption and application of new knowledge and reduces firms’ in-house training costs [

30,

31]. Therefore, home country policies oriented to the development of skilled human resources are likely to influence OFDI positively.

A country’s OFDI is related to the “stage of its economic development, the structure of its factor endowments and markets; its political and economic systems; and the nature and extent of market failure in the transaction of intermediate products across national boundaries.” [

19] Therefore, having national institutions that are strong to ensure the efficient allocation of factors and improve economic performance is a prerequisite for OFDI. In contrast, countries where institutions are weak can have several economic problems such as a lack of productivity, reduced investment rates and lower GDP growth, which deters OFDI [

3,

46,

47,

48,

49].

Hence, we wanted to explore which dimensions of home country institutions motivate OFDI and which dimensions deter it. We hypothesized:

H1: Perceived political and legal hazards positively moderate OFDI

H2: Perceived financial constraints positively moderate OFDI

H3: Uneven access to factor endowments negatively moderates OFDI

H4: Human capital positively moderates OFDI

H5: High levels of research and development positively moderate OFDI

H6: Protection of inward FDI positively moderates OFDI

4. Results and Discussion

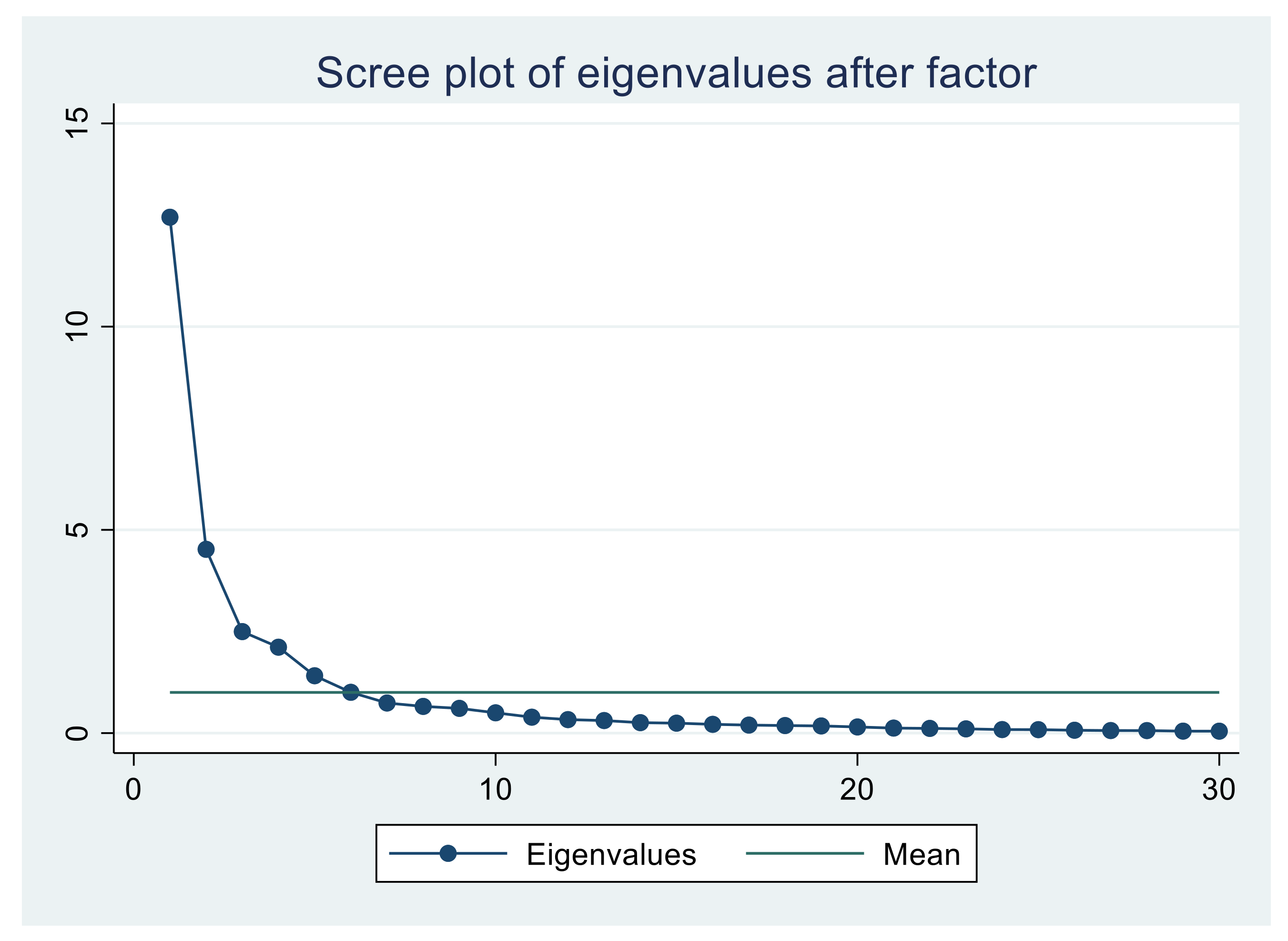

Followed the criteria explained in section methods, we found that 11 factors explain at least 90% of the variance. Simultaneously, only 6 of them had eigenvalues greater than the unit (View

Appendix A,

Table A4). Moreover, the scree plot shows that the most significant change in the slope occurs at factor six; therefore, the first six factors should be retained. Around 80% of the total variation can be captured by the first six factors, each representing a different institutional quality aspect in a country.

We named the factors after the factor’s major loadings, as shown in

Table 5; complete results are shown in

Table A5 in the

Appendix A. The extracted factors were subsequently used as new variables to represent institutional conditions. These are transparency of the government, research, development, and innovation, inequality, rules for inward FDI, education and training and financial market.

The first factor included heavy loadings of diversion of public funds, public trust in politicians and favoritism in decisions of government officials, which capture perceptions of the extent to which agents have confidence in and abide by society’s rules and have credibility in the government and public-sector development. We thus called this factor “transparency of the government.”

The second factor was focused on indicators as university-industry collaboration in R&D, capacity for innovation, company spending on R&D and availability of research and training services, all of which promote innovation and competitiveness through helping businesses to adapt rapidly to a changing environment, making it intuitively sensible to interpret this factor as “R&D+I.”

The third factor consisted of the Fragile States Index components on group grievance, factionalized elites, state legitimacy, economic inequality, human flight and public services. Therefore, this final index can readily be interpreted as a measure of structural inequality, mainly focused on divisions based on social or political characteristics and their role in access to services or resources.

The fourth factor captured the indicators related to the rules for inward FDI as the prevalence of foreign ownership, the business impact of rules on FDI as well as the relationship between FDI and technology transfers. Thus, it considered the government’s openness and explained its regulatory quality to formulate and implement policies and regulations that permit private sector development.

The fifth factor included the quality of math and science education, scientists and engineers’ availability, and the education system’s quality. Hence, the “education and training” is an indicator of the possibility of generating more value and transfer and adaptive knowledge to promote competitiveness.

Finally, the sixth factor measured financing through the local equity market and venture capital availability. It was expected that an underdeveloped financial market fosters OFDI due to the need for a competitive source of capital.

The unbundling of institutions allowed us to examine which of these different dimensions matter for outward FDI stocks in emerging markets.

Table 6 presents the results of estimated models for OFDI stocks from 48 emerging economies in the 2007–2017 period.

We applied the Breusch-Pagan test (LM test), and we concluded that the RE estimator is preferable to OLS because the p-value is lower than 0.05. Then, the rejection of the OLS model is consistent. In this case, our results may suggest that transparency of the government and research and development plus innovation promote outward FDI, while inequality and financial market reduce it (model 2).

As displayed in model 2, the positive coefficients for both factor 1 and factor 2 (

p-value < 0.05,

p-value < 0.01, respectively) indicate that the measure of the transparency of government is positively correlated with outward FDI, as well as with R&D+I. In this way, the estimates in model 2 provide partial support for H1 and H5, suggesting that, in this case, a strong institutional framework encourages OFDI. Our findings supported the notion that fair and clear governmental actions within emerging markets introduce competition and market transparency that promote new forms of corporate governance encouraging international ventures [

87]. They also supported the idea that the production capacity of innovative features (R&D+I) depends on the market structure, government policies and the resources available, which is positively linked to the tendency of the OFDI [

88,

89].

In contrast, the negative and significant at the 0.01 level coefficients for the third and sixth factors show both structural inequality and financial market are negatively related to outward FDI, indicating that a weak institutional framework discourages OFDI. These results provide partial support for H2 and H3, and are in line with the notion that institutions can be a problem in politics (corruption, instability, policies), law (economic liberalization, regulations) and society (norms, attitudes, culture) that may affect the internationalization of firms and their strategies [

11,

90]. The remaining two factors do not significantly affect OFDI stocks.

However, by performing a Hausman test, we could reject the hypothesis that the coefficients are the same in both random and fixed effects models, so random effects are dismissed in favor of fixed effects (p-value < 0.05). In general, the results indicated that R&D+I and financial market factors affect OFDI. Thus, we confirmed our previous results about H5 y H2.

Here, we found that the more capacity for innovation and spending on research and development, the higher the involvement in OFDI, because the relevant coefficient was found to be positive and significant at the 0.10 level (model 3). This suggests that emerging markets firms tend to seek strategic assets to acquire and integrate particular knowledge to improve the research and development capabilities [

91].

We also found support for H2 because the financial market’s coefficient was negative and significant at the 0.01 level (model 3). We found that more financing through the local equity market and venture capital availability exists in the home country’s economy, thereby discouraging OFDI. This suggested that the availability of resources to minimize the cost of capital in the home country is more attractive for emerging market firms [

92,

93]. In this case, transparency of the government, inequality, rules for inward FDI and education were not statistically significant.

On the other hand, the statistically significant positive coefficient of lagged values of OFDI stocks showed that OFDI stocks are influenced by the previous year’s OFDI (model 5) as expected. These results also showed that government transparency positively and significantly affects OFDI stocks, indicating that high transparency increases OFDI. Models 2 and 5 showed a positive relationship between the transparency of the government factor and the outward FDI. These results support H1, which states that perceived political and legal hazards positively moderate OFDI.

This finding makes sense because the literature indicates that the institutional environment creates two streams of OFDI: leverage and escapism [

17,

94]. Firms are willing to invest abroad because they have institutional support or are trying to escape from institutional hazards. Emerging-markets companies mainly consider investing abroad to escape from their home countries’ poor institutional climates [

55,

95,

96].

Also, the signs of our control variables were typical as expected: GDP per capita was positively associated with outward FDI, and inflation displayed a negative association (model 7). The findings for the institutional quality point towards the importance of the financial market because the coefficient remained statistically significant with the same (negative) sign as in random and fixed effects models. Thus, the estimates in models 2, 3 and 7 provided support for H2. In hypothesis 2, we suggested that perceived financial constraints positively moderate ODFI; here, we found support for a negative relationship between financial markets and outward FDI. Specifically, we argued that increasing open access to capital resources promotes local firms’ finance [

33,

97]. Our findings confirmed that firms often have difficulty expanding overseas because of the constraints from underdeveloped financial markets in their home country [

58].

Our results indicated that the fourth factor never gained significance. We failed to find support for H4 and H6. The results revealed that the coefficients for rules for inward FDI and education and training are insignificant. This means that rules for inward FDI and education and training have no significant effect on OFDI. Although this result surprised us, prior studies that support the idea that there are positive effects of inward FDI on OFDI exist, though they are focused on the firm level in China [

98,

99,

100], not on the country level and covering multiple countries.

In sum, empirical results demonstrate that institutional framework had a strong influence on the outward foreign direct investment (OFDI). Our results provide evidence that outward FDI depends on home country institutions.

5. Conclusions

Which dimensions of home country institutions motivates outward FDI (OFDI) and which dimensions deter it was the research question. Consequently, this paper has explored the association between different institutional factors and outward FDI stocks for a panel of 48 emerging markets over the period of 2007–2017. We employed 30 indicators to form six factors to represent institutional conditions using factor analysis. These are transparency of the government, research, development, and innovation, inequality, rules for inward FDI, education and training and financial market.

Our findings revealed that not all institutional quality indicators have a significant effect on outward FDI in emerging markets. Specifically, our study provided new insights to extend our understanding of the relationship between institutional framework and outward FDI, while considering some unexplored moderating effects. We found that research and development plus innovations and transparency of the government have significant positive effects on OFDI stocks, while the financial market has a significant negative impact.

Another finding was the negative relationship between financial markets and external FDI. Specifically, we supported the idea that increasing open access to capital resources facilitates funding in local firms. Our findings reinforce the view that firms frequently find it challenging to grow overseas due to the constraints of underdeveloped financial markets in their home countries.

These results show that we have a limited understanding of the real effect of the home country institutional environment; our panel involves a very diverse number of emerging economies; while some of the findings could support the idea of institutional leverage, others could be related to institutional escapism.

These findings promote an interest in probing the role played by home country institutions behind outward internationalization. In addition, improving institutional quality in firms’ home country is essential to outward FDI in emerging economies.

{kind=link}

{kind=link}