Corporate Environmental Responsibility through the Prism of Strategic Management

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. The Essence of Corporate Environmental Responsibility and Its Role in the Development of Environmental Management Systems

2.2. Research into the Effects of Key Factors on the Formation of Ecological Management Systems

2.3. Formation and Improvement of Environmental Management Systems and the Impact on the Efficiency of Companies

2.4. Research into the Processes for the Formation and Realization of Environmental Strategy

3. Methodology

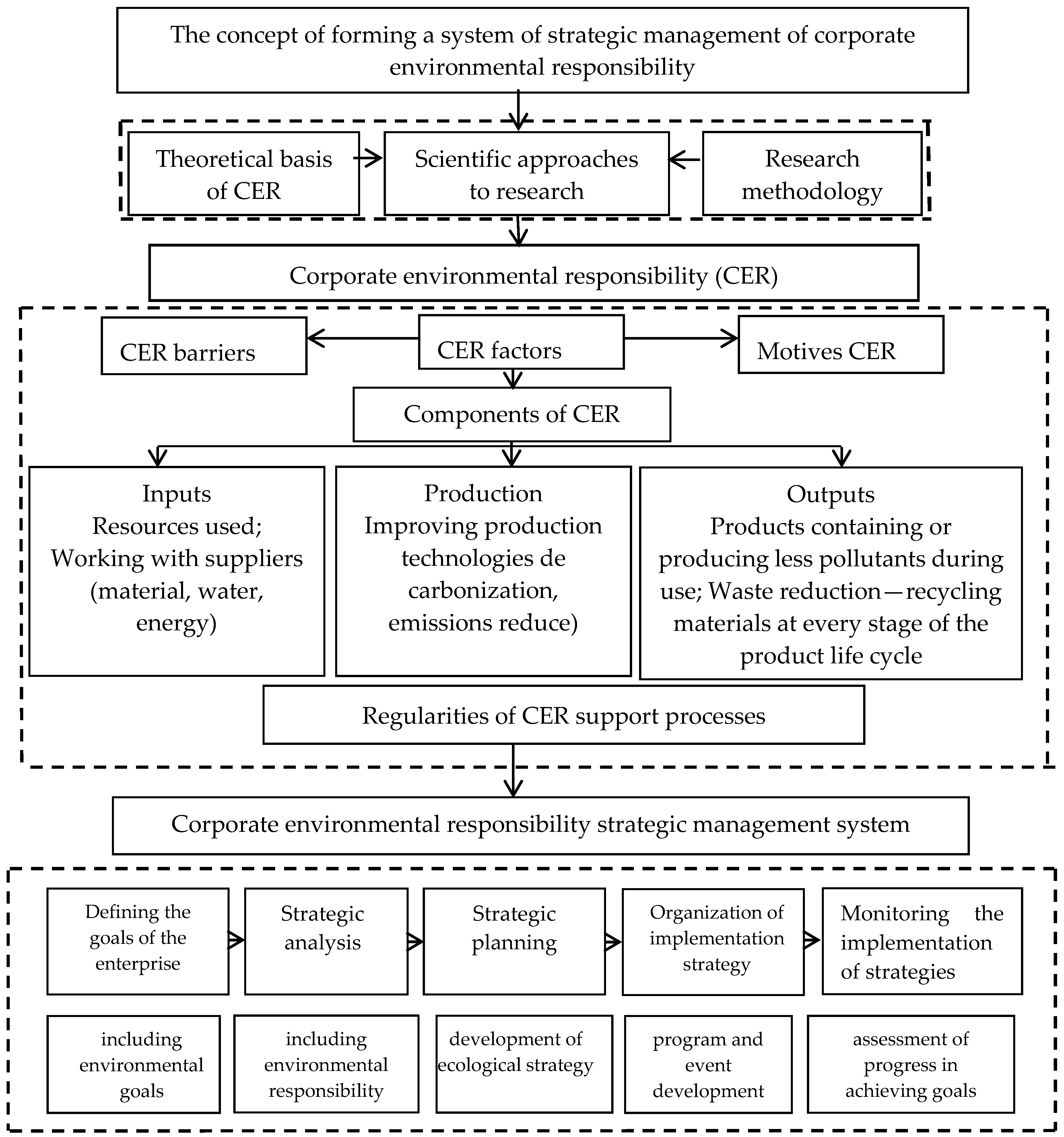

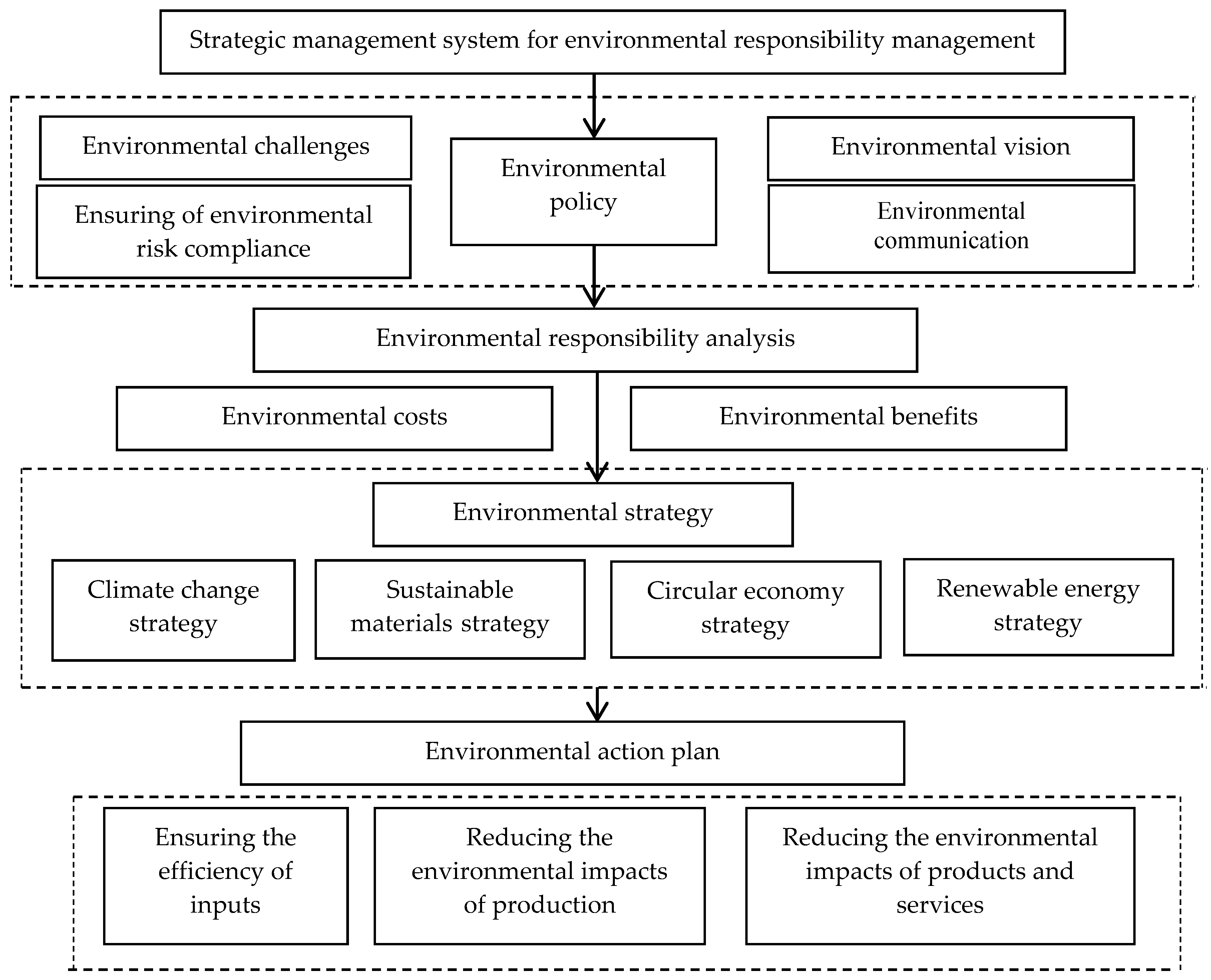

3.1. The Concept of Strategic Management of Corporate Environmental Responsibility

- -

- Theoretical level—provides a synthesis of provisions that determine the scientific basis for understanding the studied processes;

- -

- Methodological level—enables the formation of the methodical provisions for the research;

- -

- Practical level—provides a set of measures for the practical implementation of the concept, based on a comprehensive analysis.

3.2. Theoretical Basis of the Study

- (1)

- Identification of development goals—the environmental goals are reflected in the key sustainable development goals of the company;

- (2)

- Strategic analysis of the level and conditions necessary for increasing the environmental responsibility of the company—the focus is on research into the external environment and the forecasting of trends to determine the internal potential for increasing the environmental responsibility of the company;

- (3)

- Strategic planning—this involves the development of a set of strategies, whereby environmental strategy is becoming increasingly important, for the meaningful and long-term determination of areas for improvement with regards to the company’s interaction with the external environment;

- (4)

- Implementation of environmental strategy—this involves assessing the risks of implementing the environmental strategy, the development of a program, measures, and key documents that will ensure the practical implementation of the strategy, as well as the development of policies, the allocation of resources, and the motivation of employees;

- (5)

- Checking the implementation of the environmental strategy—a process of constant review prevents the company becoming trapped in its own irrelevant strategy.

- (1)

- The implementation of the concept of sustainable development determines the orientation of the company, including its environmental goals, which, in conjunction with economic and social goals, should be considered as important guidelines;

- (2)

- Multifaceted manifestations of environmental responsibility (products, technologies) are a condition for the formation of long-term competitiveness and a positive image;

- (3)

- Ensuring the appropriate level of environmental responsibility requires all internal subsystems and functional areas of the company to be environmentally oriented;

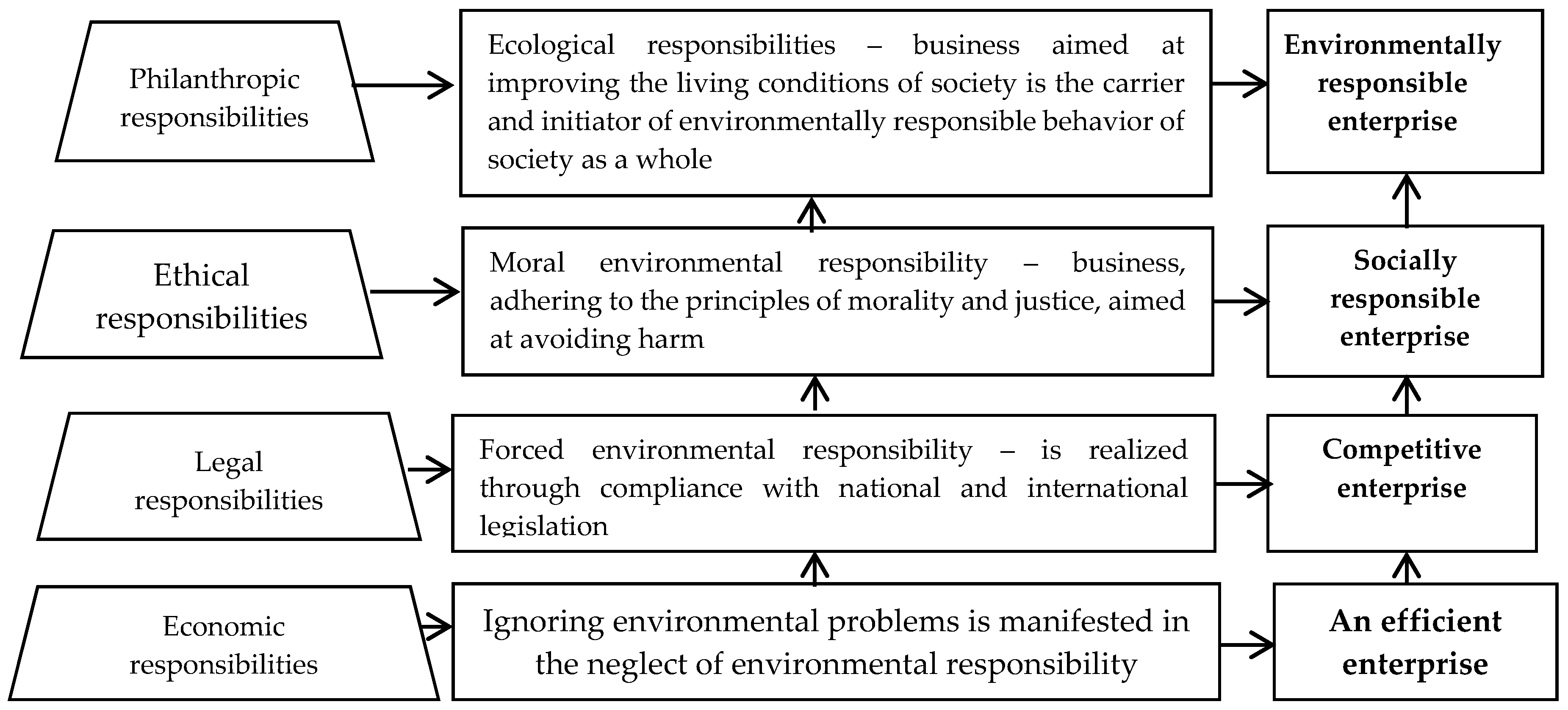

- (4)

- Environmentally responsible companies become drivers of the formation of an environmentally responsible society.

3.3. Methodical Provisions for the Analysis of Corporate Environmental Responsibility

- (1)

- Integrated approach—this involves the calculation of generalized indicators, for example:

- -

- Environmental Sustainability Index (ESI) according to the World Economic Forum [52], which reflects the overall progress towards environmental sustainability, and which allows for cross-national comparisons;

- -

- -

- Synthetic Indicator for Evaluating Environmental Performance (SIEEP), which is based on four criteria: waste and wastewater management and water protection, waste management and protection of the Earth’s surface, air pollution and climate control, nature conservation and the promotion of pro-environmental behaviors [55,56,57,58];

- (2)

- Fragmentary approach—this involves the study of individual indicators of environmental responsibility within the general monitoring system of the level of sustainability of companies, along with the analysis of economic indicators and indicators of social responsibility. Companies compile a report on sustainable development, which includes a separate section containing information on environmental indicators;

- (3)

- Econometric approach—this involves the study of existing relationships between environmental responsibility indicators and financial and economic performance indicators.

- (1)

- Reflect the achievements of the company in this direction, which is important for a growing number of stakeholders and society as a whole;

- (2)

- Allow comparisons to be made with other competitors regarding the company’s interactive processes with its external environment;

- (3)

- Enable substantiation of the company’s strategic development goals, including environmental ones.

- (1)

- Use absolute indicators, i.e., per unit (conditional unit) of production or per certain comparable value, which enables the establishment of the scale of the studied processes;

- (2)

- Analyze the dynamics of the indicators, calculating the absolute and relative deviations.

4. Results and Discussions

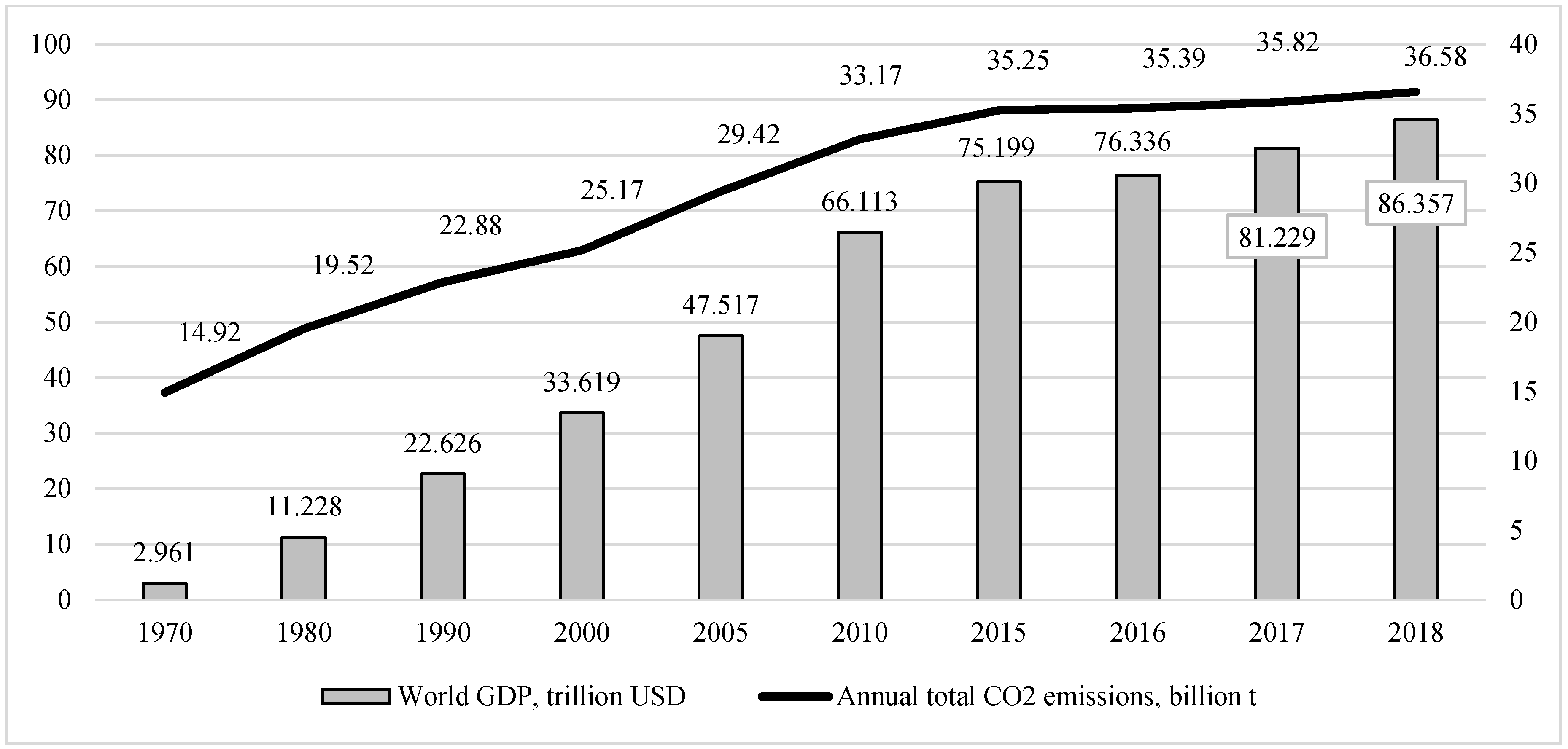

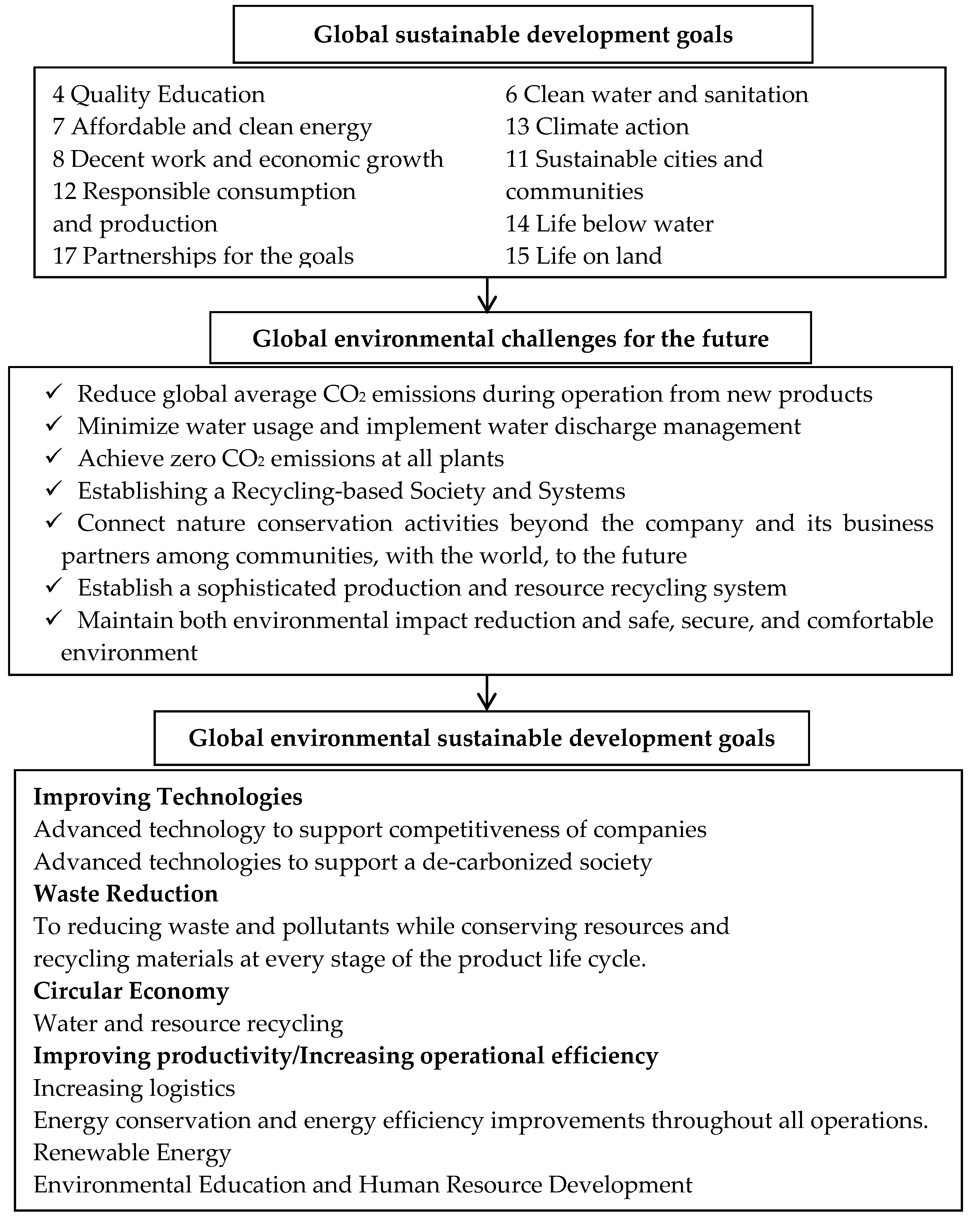

4.1. Research into Global Environmental Challenges and Sustainable Development Goals

- (1)

- (International) institutional and organizational level because it is impossible to solve problems alone, even for a large country;

- (2)

- State level because the balanced environmental policy of a state determines the characteristics of its environmental activities at the micro-level and forms the basis for interstate consensus on environmental protection;

- (3)

- Company level because it is through environmental policy development that a company looks at and adopts internal standards for production technology, the eco-friendliness of its products, and waste processing.

4.2. Monitoring the Environmental Goals of Companies and their Incorporation in Development Strategy

4.3. A Comprehensive Study of Environmental Responsibility

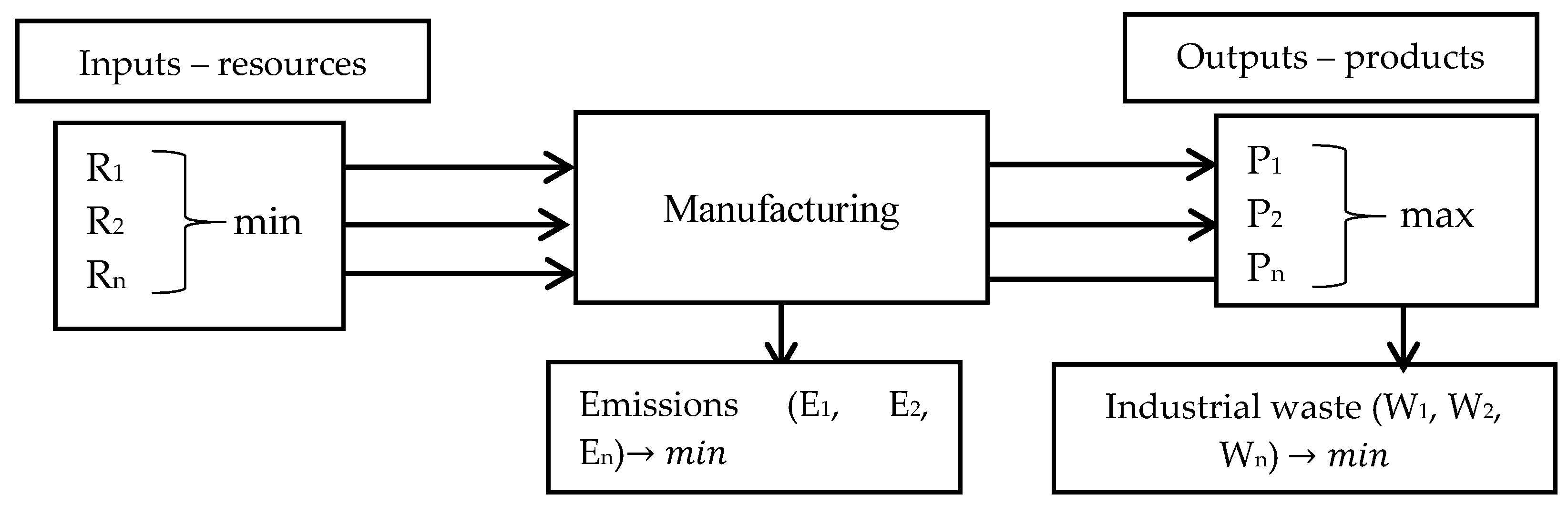

- (1)

- The total value of consumption of resources (inputs), including per unit of output, and in particular energy, has decreased;

- (2)

- There has been a positive change in the dynamics of emissions and waste, which has decreased both in terms of total volumes and per unit of output, which implies an increase in the eco-efficiency of car production;

- (3)

- Financial resources have gradually increased for protection of the environment both in terms of investment and operating costs (including per car).

4.4. Integrated Analysis of the Level of Environmental Responsibility

4.5. Designing a Strategic Management System for Environmental Responsibility Management

5. Conclusions

- (1)

- Companies that subordinate environmental responsibility to the economic interests of modern development;

- (2)

- Companies that provide a minimum level of environmental responsibility;

- (3)

- Companies that provide a sufficient level of environmental responsibility and are focused on preventing harmful effects to the environment;

- (4)

- Companies that determine the level of environmental responsibility in the industry and contribute to developing an environmentally responsible society.

Author Contributions

Funding

Conflicts of Interest

References

- Malthus, T. An Essay on the Principle of Population; Johnson, J., Ed.; St. Paul’s Church-Yard: London, UK, 1798. [Google Scholar]

- Indicators. The World Bank. Available online: http://www.worldbank.org/en/search?q (accessed on 3 June 2020).

- Overconsumption? Our Use of the World’s Natural Resources. Friends of the Earth England, Wales and Northern Ireland. Available online: https://cdn.friendsoftheearth.uk/sites/default/files/downloads/overconsumption.pdf (accessed on 3 June 2020).

- United Nations, Department of Economic and Social Affairs, Population Division. World Population Prospects 2019: Highlights (ST/ESA/SER.A/423). 2019. Available online: https://population.un.org/wpp/Publications/Files/WPP2019_Highlights.pdf (accessed on 3 June 2020).

- Canals, C. The Emergence of the Middle Class: An Emerging-Country Phenomenon. 2019. Available online: https://www.caixabankresearch.com/en/economics-markets/labour-market-demographics/emergence-middle-class-emerging-country-phenomenon (accessed on 29 September 2020).

- Fiorino, D.J. The New Environmental Regulation; Mit Press: Cambridge, MA, USA, 2006. [Google Scholar]

- Rumelt, R.P.; Schendel, D.; Teece, D.J. Strategic management and economics. Strat. Manag. J. 1991, 12, 5–29. [Google Scholar] [CrossRef]

- Nooraie, M. Factors influencing strategic decision-making processes. Int. J. Acad. Res. Bus. Soc. Sci. 2012, 2, 405–429. Available online: https://www.researchgate.net/publication/266228150_Factors_Influencing_Strategic_Decision-Making_Processes (accessed on 25 March 2020).

- ISO 14001 Environmental Management Systems. Available online: http://www.environmentalmanagementsystem.com.au/iso-14001-environmental-management-systems.html (accessed on 25 April 2020).

- Joshi, A. Corporate Environmental responsibility: A liability or challenge. Electron. J. 2012, 2, 34–36. [Google Scholar] [CrossRef]

- Das, T.K. Corporate environmental responsibility excellence. Corp. Soc. Responsib. 2006, 3, 166–174. [Google Scholar]

- Dominguez, C.; Varajao, J. Environmental management systems certification: Insights from Portuguese construction companies. Environ. Eng. Manag. J. 2016, 11, 2383–2394. [Google Scholar] [CrossRef]

- Giménez, G.; Leal, M.; Casadesús, F.; Valls, J. Using environmental management systems to increase firms’ competitiveness. Corp. Soc. Responsib. Environ. Manag. 2003, 10, 101–110. [Google Scholar] [CrossRef]

- Herghiligiu, I.V.; Robu, I.-B.; Pislaru, M.; Vilcu, A.; Asandului, A.L.; Avasilcăi, S.; Balan, C. Sustainable environmental management system integration and business performance: A balance assessment approach using fuzzy logic. Sustainability 2019, 11, 5311. [Google Scholar] [CrossRef]

- Johnstone, L. A systematic analysis of environmental management systems in SMEs: Possible research directions from a management accounting and control stance. J. Clean. Prod. 2019. [Google Scholar] [CrossRef]

- Successful Practices of Environmental Management Systems in Small and Medium-Size Enterprises Commission for Environmental Cooperation. A North American Perspective. Commission for Environmental Cooperation. 2005. Available online: http://www3.cec.org/islandora/en/item/2273-successful-practices-environmental-management-systems-in-small-and-medium-size-en.pdf (accessed on 25 July 2020).

- Iyer, G.V.; Mastorakis, N. Environmental management system for the organization to achieve business excellence. In Proceedings of the 6th WSEAS International Conference on Systems Theory & Scientific Computation, Elounda, Greece, 8–10 May 2006; Athina, L., Konstantinos, S., Eds.; World Scientific and Engineering Academy and Society: Stevens Point, WI, USA, 2006; pp. 484–495. [Google Scholar]

- Khanna, D.R.; Bhutiani, R.; Matta, G. Environmental Management System. J. Comp. Toxicol. Physiol. 2009, 6, 10–17. [Google Scholar]

- Dummett, K. Drivers for corporate environmental responsibility (CER). Environ. Dev. Sustain. 2006, 8, 375–389. [Google Scholar] [CrossRef]

- Cantele, S.; Zardini, A. What drives small and medium enterprise towards sustainability & role of interactions between pressures, barriers, and benefits. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 126–136. [Google Scholar] [CrossRef]

- Sindhi, S.; Kumar, N. Corporate environmental responsibility-transitional and evolving. Manag. Environ. Qual. 2012, 23, 640–657. [Google Scholar] [CrossRef]

- Cosmina, L.; Hoogenberg, B.; Fratostiteanu, C.; Hashmi, H. The Relation between environmental management systems and environmental and financial performance in emerging economies. Sustainability 2020, 12, 5309. [Google Scholar] [CrossRef]

- Henri, J.; Journeault, M. Eco-control: The influence of management control systems on environmental and economic performance. Account. Organ. Soc. 2010, 35, 63–80. [Google Scholar] [CrossRef]

- Cater, T.; Prasnikar, J.; Cater, B. Environmental strategies and their motives and results in Slovenian business practice. Econ. Bus. Rev. 2009, 11, 55–74. [Google Scholar]

- Gadenne, D.L.; Kennedy, J.; McKeiver, C. An empirical study of environmental awareness and practices in SMEs. J. Bus. Ethics 2009, 84, 45–63. [Google Scholar] [CrossRef]

- Serwach, T. Environmental Marketing Strategies in Business and the Environment; Dorozynski, T., Kuna-Marszalek, A., Eds.; Wydawnictwo Uniwersytetu Lodzkiego: Lodz, Poland, 2016; pp. 101–120. [Google Scholar]

- Atkinson, G.; Hett, T.; Newcombe, J. Measuring corporate sustainability. J. Environ. Plan. Manag. 2000, 43, 235–252. [Google Scholar] [CrossRef]

- Figge, F.; Tobias, H.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard–Theory and Application of a Tool for Value-Based Sustainability Management. Green. Ind. Netw. 2002, 11, 269–284. Available online: http://www.ecnc.org/uploads/documents/the-sustainably-balanced-scorecard-theory-and-application-of-a-tool-for-value-based-sustainability-management.pdf (accessed on 5 April 2020).

- Hart, S.L.; Milstein, M.B. Creating sustainable value. Acad. Manag. Exec. 2003, 17, 56–69. [Google Scholar] [CrossRef]

- United Nations Global Compact. Available online: www.unglobalcompact.org/ (accessed on 15 April 2020).

- Grant, R.M. The resource-based theory of competitive advantage: Implications for strategy formulation. Calif. Manag. Rev. 1999, 33, 3–23. [Google Scholar] [CrossRef]

- Pearce, D.; Turner, R. Economics of Natural Resources and the Environment; Harvester Wheatsheaf: London, UK, 1990; pp. 271–287. [Google Scholar]

- Perman, R.; Ma, Y.; McGilvray, J.; Common, M. Natural Resource and Environmental Economics, 3rd ed.; Pearson Addison-Wesley: London, UK, 2003; pp. 506–536. [Google Scholar]

- Shane, S.; Kolvereid, L. National environment, strategy, and new venture performance: A three country study. J. Small Bus. Manag. 1995, 29, 37–50. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. Having trouble with your strategy? Then map it. Harv. Bus. Rev. 2000, 78, 167–176. [Google Scholar] [PubMed]

- Deari, F. Investments and financing sources of businesses: Evidence from Pollog region. Econ. Organ. 2010, 7, 245–251. [Google Scholar]

- Belderbos, R.; Fukao, K.; Ito, K.; Letterie, W. Global fixed capital investment by multinational firms. The Research Institute of Economy, Trade and Industry. 2013. Available online: http://www.rieti.go.jp/en/ (accessed on 5 April 2020).

- Fazzari, S.M.; Petersen, B.C. Working capital and fixed investment: New evidence on financing constraints. RAND J. Econ. 1993, 24, 328–342. [Google Scholar] [CrossRef]

- Drucker, P.F. The Discipline of Innovation. Harv. Bus. Rev. 2002, 80. Available online: https://www.researchgate.net/publication/11192227_The_Discipline_of_Innovation (accessed on 24 June 2020). [CrossRef]

- Freeman, C. Technology Policy and Economic Performance: Lessons from Japan; Pinter: London, UK, 1987. [Google Scholar]

- Fussler, C.; James, P. Driving Eco-Innovation: A Breakthrough Discipline for Innovation and Sustainability; Pitman Publishing: New York, NY, USA, 1996. [Google Scholar]

- Gray, B.; Ariss, S. Politics and change across organization life cycle. Acad. Manag. Rev. 1985, 10, 707–723. [Google Scholar] [CrossRef]

- Adizes, I. Corporate Lifecycles: How and Why Corporations Grow and Die and What to Do about It; Prentice Hall: Englewood Cliffs, NJ, USA, 1989. [Google Scholar]

- Cooper, R.; Haltiwanger, J.; Power, L. Machine replacement and the business cycle: Lumps and bumps. Am. Econ. Rev. 1999, 89, 921–946. [Google Scholar] [CrossRef]

- Lester, D.; Parnell, J.; Carraher, S. Organization life cycle: A five-stage empirical scale. Int. J. Organ. Anal. 2003, 11, 339–354. [Google Scholar] [CrossRef]

- Carroll, A. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Kasych, A.; Vochozka, M.; Yakovenko, Y. Diagnostic of the stability states of enterprises and the limits of their tolerance. Qual. Access Success 2019, 20, 3–12. [Google Scholar]

- Kasych, A.; Rowland, Z.; Yakovenko, Y. Modern management tools for sustainable development of mining enterprises. In Proceedings of the E3S Web of Conferences, Ukrainian School of Mining Engineering, Berdiansk, Ukraine, 3–7 September 2019; Bondarenko, V., Kovalevska, I., Cawood, F., Hardygora, M., Malova, O., Lysenko, R., Eds.; EDP Sicences: Les Ulis, France, 2019. [Google Scholar] [CrossRef]

- Grünig, R.; Kühn, R. Process-Based Strategies Planning; Springer: Berlin/Heidelberg, Germany, 2001. [Google Scholar]

- Katsoulakos, T.; Katsoulacos, Y. Strategic management, corporate responsibility and stakeholder management. Corp. Gov. 2007, 7, 355–369. [Google Scholar] [CrossRef]

- Kasych, A.; Vochozka, M. The choice of methodological approaches to the estimation of enterprise value in terms of management system goals. Qual. Access Success 2019, 20, 3–9. [Google Scholar]

- Environmental Sustainability Index (ESI) (2002). Socioeconomic Data and Applications Center. Available online: https://sedac.ciesin.columbia.edu/es/esi/ESI2002_21MAR02a.pdf (accessed on 17 June 2020).

- Environmental & Socially Responsible Index. S & P Dow Jones Indices. Available online: https://www.spglobal.com/spdji/en/indices/equity/sp-500-environmental-socially-responsible-index/#overview (accessed on 24 June 2020).

- Measuring Sustainable Development. Integrated Economic, Environmental and Social Frameworks. 2004. Available online: http://www.oecd.org/site/worldforum/33703829.pdf (accessed on 2 June 2020).

- Mondéjar-Jiménez, J.; Mondéjar-Jiménez, J.A.; Vargas-Vargas, M.; Gázquez-Abad, J.C. Personal attitudes in environmental protection. Int. J. Environ. Res. 2012, 6, 1039–1044. [Google Scholar] [CrossRef]

- Senetra, A.; Pawlewicz, K.; Pawlewicz, A. The dynamics of changes and spatial differences in the synthetic indicator for evaluating environmental performance in Poland: Current State. Int. J. Environ. Res. Public Health 2019, 16, 4490. [Google Scholar] [CrossRef] [PubMed]

- Mondéjar-Jiménez, J.; Vargas-Vargas, M.; Mondéjar-Jiménez, J.-A. Measuring environmental evolution using synthetic indicators. Environ. Eng. Manag. J. 2010, 9, 1145–1149. [Google Scholar] [CrossRef]

- Gilal, F.G.; Gilal, N.G.; Channa, N.A.; Gilal, R.G.; Tunio, M.N. Towards an integrated model for the transference of environmental responsibility. Bus. Strategy Environ. 2020, 29, 2614–2623. [Google Scholar] [CrossRef]

- Forcadell, F.J.; Úbeda, F.; Aracil, E. Effects of environmental corporate social responsibility on innovativeness of Spanish industrial SMEs. Technol. Forecast. Soc. Chang. 2021, 162. [Google Scholar] [CrossRef]

- García-Pozo, A.; Mondéjar-Jiménez, J.; Sánchez-Ollero, J.L. Internet’s user perception of corporate social responsibility in hotel services. Sustainability 2019, 11, 2916. [Google Scholar] [CrossRef]

- Eco-efficiency Indicators: Measuring Resource-Use Efficiency and the Impact of Economic Activities on the Environment. United Nations Publication/ESCAP. 2002. Available online: https://sustainabledevelopment.un.org/content/documents/785eco.pdf (accessed on 12 June 2020).

- Toshiba Group Environmental Report 2019. Available online: https://www.toshiba.co.jp/sustainability/en/report/download.htm (accessed on 14 June 2020).

- Official Site of Volkswagen Group. Available online: www.volkswagenag.com/vwag/vwcorp/content/en/homepage.html (accessed on 4 June 2020).

- Official Site of General Motors. Available online: http://www.gm.com (accessed on 18 June 2020).

- Official Site of Ford Motor. Available online: http://www.ford.com (accessed on 12 June 2020).

- Official Site of Nissan. Available online: http://www.nissan-global.com (accessed on 4 June 2020).

- Official Site of Toyota. Available online: http://www.toyota.com (accessed on 14 June 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| External Factors of a Coercive Nature | External Factors of a Motivational Nature | Internal Factors |

|---|---|---|

| Unification of regulatory norms as a result of globalization. | Competition in the business environment. | Recognition by the management of the importance to the company of increasing the level of environmental responsibility. |

| Regulations in different countries. | Development of public consciousness. | Technical and technological development of the company. |

| General Approach for the Assessment of Eco-Efficiency | |

|---|---|

| Eco-efficiency = | Enhancing quality |

| Value of a product | |

| Environmental impact of a product | |

| Reducing impact | |

| Calculation of Product Eco-Efficiency (Factor T) | Calculation of Business Process Eco-Efficiency |

| Factor T = eco-efficiency of assessed product/eco-efficiency of benchmark product | Degree of improvement in business process |

| eco-efficiency = business process eco-efficiency in assessed year/business process | |

| eco-efficiency in benchmark year | |

| Indicators | |

|---|---|

| I | Analysis of rational use of resources |

| 1 | Gross energy consumption |

| 2 | Consumption of non-renewable fuels |

| 3 | Own energy generation |

| 4 | Share of own energy generation in total energy consumption |

| 5 | Water consumption (difference between total intake and total discharge), thousand m3 |

| 6 | Specific irreversible water consumption, m3/unit of output |

| II | Analysis of environmental activities of the company |

| 1 | Number of environmental measures |

| 2 | Costs of environmental measures (indicators of costs and investments) |

| 3 | Investments in modernization of resources and energy-saving technologies |

| III | Analysis of emissions and waste management (air, water, land) |

| 1 | Emissions of pollutants into the atmosphere |

| 2 | Direct emissions of carbon dioxide, million tons of CO2-eq. |

| 3 | Specific emissions of pollutants |

| 4 | Analysis of the characteristics of the circular economy |

| 5 | Waste going to landfill |

| 6 | Use of waste in own production |

| 7 | Amount of water consumption per closed water supply system |

| 8 | Incl. share of water consumption per closed water supply system |

| Inputs—Resources | Production | Outputs—Products |

|---|---|---|

| Use of safe materials | Investments in fixed assets (resources and energy-saving technologies) | Production |

| Energy consumption | Investment in environmental protection | Emissions into the atmosphere |

| Water consumption | Costs of environmental measures | Volume of industrial effluents |

| Payments for pollution | Industrial waste | |

| Signs of environmentally responsible behavior of the company | ||

| Reduction of resource consumption | Increasing investment in resource-saving technologies | Increasing the volume and share of eco-friendly products |

| Reduction of resource costs per unit of output | Increase the cost of environmental measures | Emissions reductions |

| Nissan | GM | VW | Toyota | Ford |

|---|---|---|---|---|

| Goals (Environmental Vision) | ||||

| Realizing a zero-emission, zero-fatality society | We see a world with zero crashes, zero emissions, and zero congestion | Mission statement “GoTOzero” | Going beyond zero environmental impact and achieving a net positive impact | Zero-emission and zero-impact emission vehicles |

| Priorities | ||||

| Climate change, resource dependency (energy, materials), air quality, water scarcity, environmental compliance, waste | ||||

| Targets | ||||

| To achieve carbon neutrality by 2050. To achieve zero air emissions. To use 100 percent renewable energy by 2035. To make zero water withdrawals for production processes. To use freshwater for human consumption only. | To achieve zero waste to landfill. To eliminate single-use plastics from operations by 2030. To use recycled and renewable plastics. To use of renewable energy to create a decarbonized society by 2050. | |||

| Environmental Action Plan | ||||

| Indicator | 2010 | 2016 | 2017 | 2018 | 2019 | % 2019 (2018) to 2010 |

|---|---|---|---|---|---|---|

| Volkswagen | ||||||

| Vehicle sales (in thousands of units) | 7278 | 10,391 | 10,777 | 10,900 | 10,956 | 50.5 |

| Energy consumption, (in kWh/vehicle) | ||||||

| Total | 2519 | 2089 | 2068 | 2038 | 2010 | −20.2 |

| Electricity | 1197 | 1088 | 1060 | 1063 | 1051 | −12.2 |

| Heat | 855 | 599 | 587 | 560 | 550 | −35.7 |

| Fuel gases for production processes | 467 | 402 | 421 | 415 | 409 | −12.4 |

| CO2 emissions (in million tons/year) | 8.04 | 9.51 | 9.11 | 8.20 | 7.57 | −5.8 |

| CO2 emissions (in kg/vehicle) | 1096 | 883 | 810 | 720 | 675 | −38.4 |

| Fresh water volume (in m3/vehicle) | 4.54 | 3.89 | 3.76 | 3.86 | 3.57 | −21.4 |

| Wastewater volume (in m3/vehicle) | 3.76 | 2.96 | 2.93 | 2.69 | 2.66 | −29.3 |

| Waste for recycling (in kg/vehicle) | ||||||

| Non-hazardous waste | 33.28 | 38.42 | 42.07 | 47.05 | 52.91 | 58.9 |

| Hazardous waste | 12.43 | 13.56 | 13.89 | 14.07 | 13.98 | 12.5 |

| Metallic waste | 217.27 | 212.24 | 211.54 | 208.89 | 204.96 | −5.7 |

| R&D expenditure (in EUR millions) | 6.866 | 13.612 | 13.135 | 13.640 | - | 98.7 |

| Capital expenditures on property, plant, and equipment (in EUR millions) | 6.275 | 13.2 | 13.1 | 13.6 | - | 2.2 times |

| Environmental protection costs | ||||||

| Investment (in USD/vehicle) | 13 | 10 | 16 | 14 | 9 | - |

| Operating costs (in USD/vehicle) | 208 | 209 | 216 | 240 | 253 | - |

| General Motors | ||||||

| Total sales (in thousands of units) | 9958 | 10,008 | 9600 | 8400 | 7718 | −22.5 |

| Total electricity consumption (in kWh) | 38,456,432 | 33,364,439 | 30,313,931 | 30,069,475 | 27,112,428 | −29.5 |

| Energy intensity (in MWh/vehicle) | 2.31 | 2.00 | 1.96 | 2.03 | 2.13 | −7.8 |

| Water intensity (in m3/vehicle) | 4.77 | 4.13 | 4.21 | 4.23 | 4.26 | −10.7 |

| Volatile Organic Compounds intensity (in metric tons/vehicle) | 0.0038 | 0.0028 | 0.0025 | 0.0024 | 0.00235 | −2.1 |

| Waste intensity (in kg/vehicle) | 307 | 222 | 229 | 224 | 222 | −27.7 |

| R&D expenditure (in USD billions) | 4.259 | 6.600 | 7.300 | 7.800 | 6.800 | 59.7 |

| Capital expenditure (in USD billions) | 4.200 | 8.300 | 8.300 | 8.700 | 7.500 | 78.6 |

| Toyota | ||||||

| Vehicle Sales (in thousands of units) | 7237 | 8681 | 8971 | 8964 | 8977 | 24.0 |

| Energy consumption per unit produced (in GJ/unit) | 9.36 | 9.12 | 8.76 | 8.85 | 8.61 | −8.0 |

| Total CO2 emissions (in million tons) | 8.0 | 8.09 | 8.46 | 8.42 | 8.29 | +3.6 |

| CO2 emissions per unit produced (in tons/unit) | 0.830 | 0.795 | 0.803 | 0.800 | 0.772 | −6.9 |

| Water usage per unit produced (in m3/unit) | 3.4 | 2.9 | 3.1 | 3.1 | 3.2 | −5.9 |

| Waste volume per unit (in kg/unit) | 56.2 | 53.1 | 52.8 | 55.7 | 55.3 | −1.6 |

| R&D expenditure (in Japanese Yen (JPY) billions | 725.345 | 1055.6 | 1037.5 | 1064.2 | 1048.8 | 44.6 |

| Capital expenditure on property, plant, and equipment (in JPY billions) | 604.536 | 1292.5 | 1211.8 | 1302.7 | 1465.8 | 2.42 times |

| Net income (in JPY billions) | 209.456 | 2312.6 | 1831.1 | 2493.9 | 1882.8 | 9 times |

| Environmental protection costs | ||||||

| Investment (in JPY billions) | 23.4 | 18.9 | 76 | 63.6 | 77.2 | 3.3 times |

| Operating costs (in JPY billions) | 324.4 | 451.0 | 425.1 | 392.6 | 432.4 | 33.3 |

| Investment (in USD/vehicle) | 31 | 21 | 81 | 68 | 83 | - |

| Operating costs (in USD/vehicle) | 431 | 500 | 456 | 421 | 463 | - |

| Cost of Environmental Measures (Y) | Sales Volume (X1) | Profit (X2) | Energy Consumption (X3) | CO2 Emissions (X4) | b3 | b1 | b0 | |

|---|---|---|---|---|---|---|---|---|

| Y | 1 | 0.78826 | −0.39025438 | −0.802878037 | −0.76083875 | −643.89 | 190.24 | 871,079.04 |

| X1 | - | 1 | −0.27692139 | −0.9610118 | 0.88007923 | 1974.846337 | 200.1409682 | 3,613,599.5 |

| X2 | - | - | 1 | 0.446954004 | −0.5227298 | 0.627017731 | 261,997.6415 | |

| X3 | - | - | - | 1 | 0.88007923 | 5.883824079 | 7 | |

| X4 | - | - | - | - | 1 | 8.07764 × 1011 | 4.80499 × 1011 |

| Company | Model | The Relationship between Environmental and Economic Results |

|---|---|---|

| Nissan | 128.9 ≥ 103.3 ≥ 100.4 ≥ 53.3 ≤ 111.9 | Environmental indicators are unbalanced, although increased investment can guarantee economic stabilization. |

| General Motors | 99.1 ≤ 104.9 ≥ 91.9 ≥ 85.5 ≤ 86.6 | Negative economic trends manifest themselves in environmental indicators. |

| Volkswagen | 98.1 ≤ 98.6 ≤ 100.5 ≤ 106.0 ≤ 105.8 | Balanced ecological and economic development. |

| Toyota | 96.5 ≤ 97.3 ≤ 1001 ≥ 75.5 ≤ 112.5 | A slight decrease in profitability is not a threat to the environmentally responsible behavior of the company. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kasych, A.; Suler, P.; Rowland, Z. Corporate Environmental Responsibility through the Prism of Strategic Management. Sustainability 2020, 12, 9589. https://doi.org/10.3390/su12229589

Kasych A, Suler P, Rowland Z. Corporate Environmental Responsibility through the Prism of Strategic Management. Sustainability. 2020; 12(22):9589. https://doi.org/10.3390/su12229589

Chicago/Turabian StyleKasych, Alla, Petr Suler, and Zuzana Rowland. 2020. "Corporate Environmental Responsibility through the Prism of Strategic Management" Sustainability 12, no. 22: 9589. https://doi.org/10.3390/su12229589

APA StyleKasych, A., Suler, P., & Rowland, Z. (2020). Corporate Environmental Responsibility through the Prism of Strategic Management. Sustainability, 12(22), 9589. https://doi.org/10.3390/su12229589