The Fertilizer Industry in Brazil and the Assurance of Inputs for Biofuels Production: Prospective Scenarios after COVID-19

, ,

, ,

Abstract

1. Introduction

2. Methods

3. Strategic Diagnosis

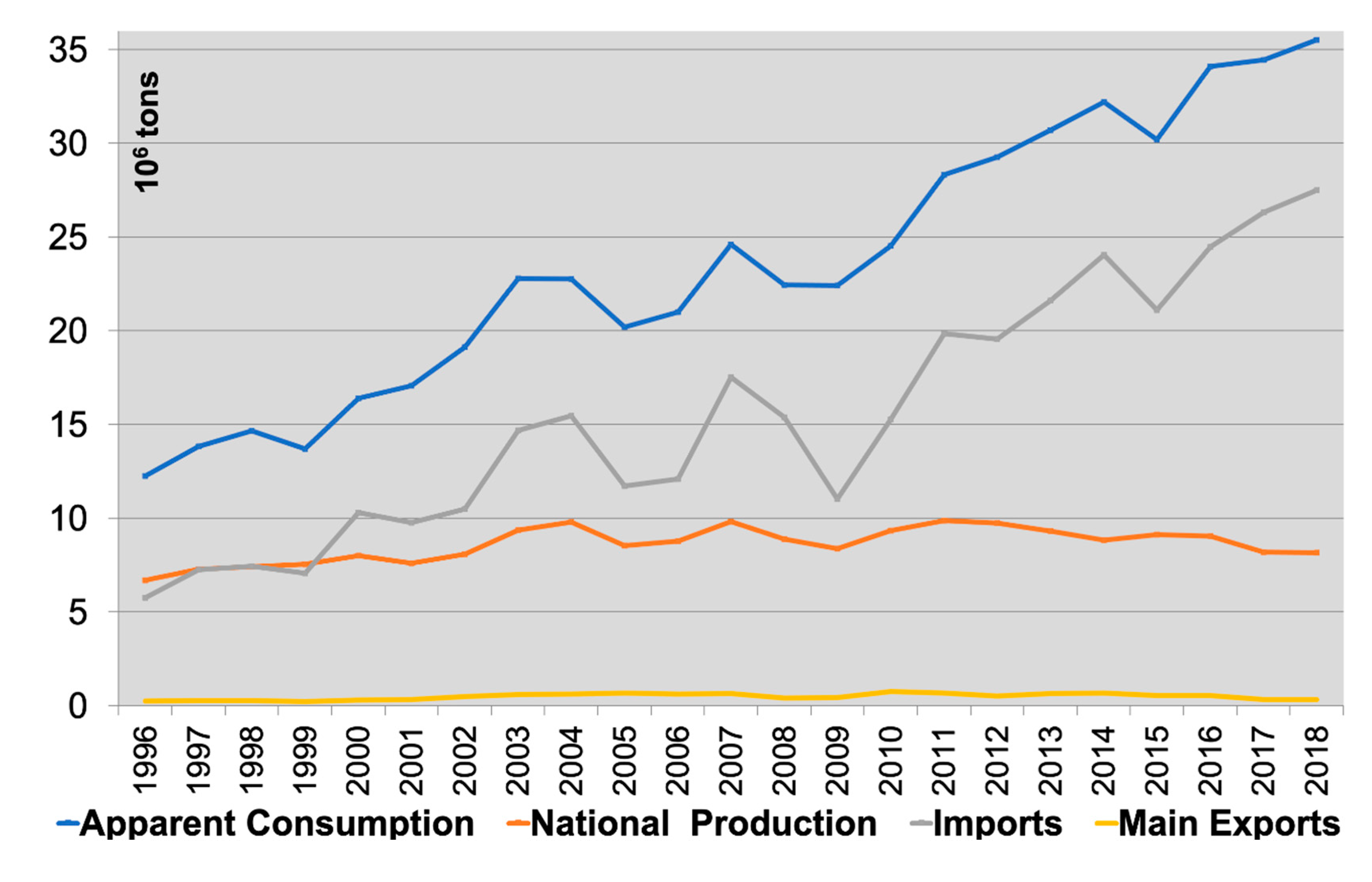

3.1. NPK Fertilizer Industry and Agribusiness Input

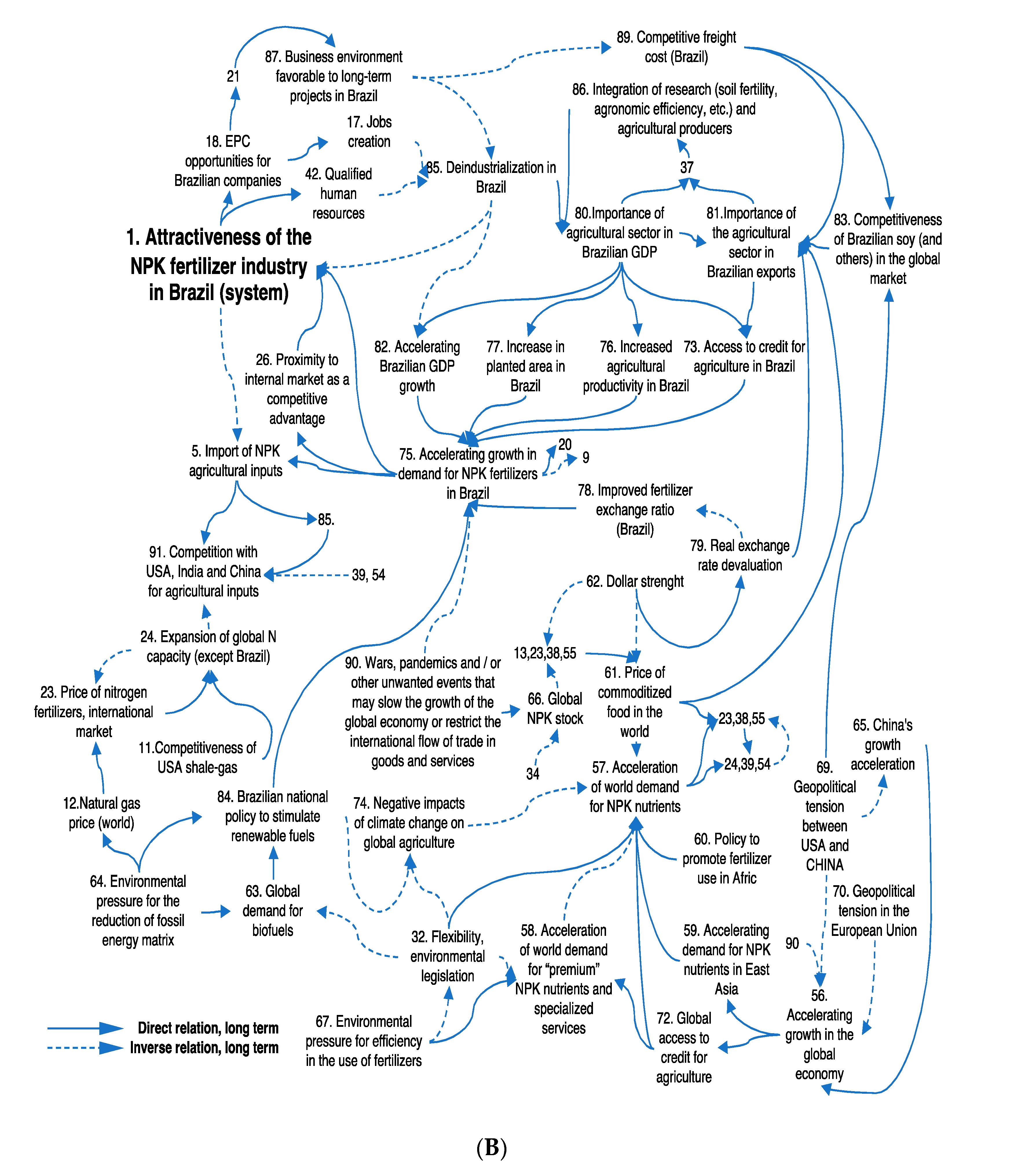

3.2. Variables Raised and Cause–Effect Map

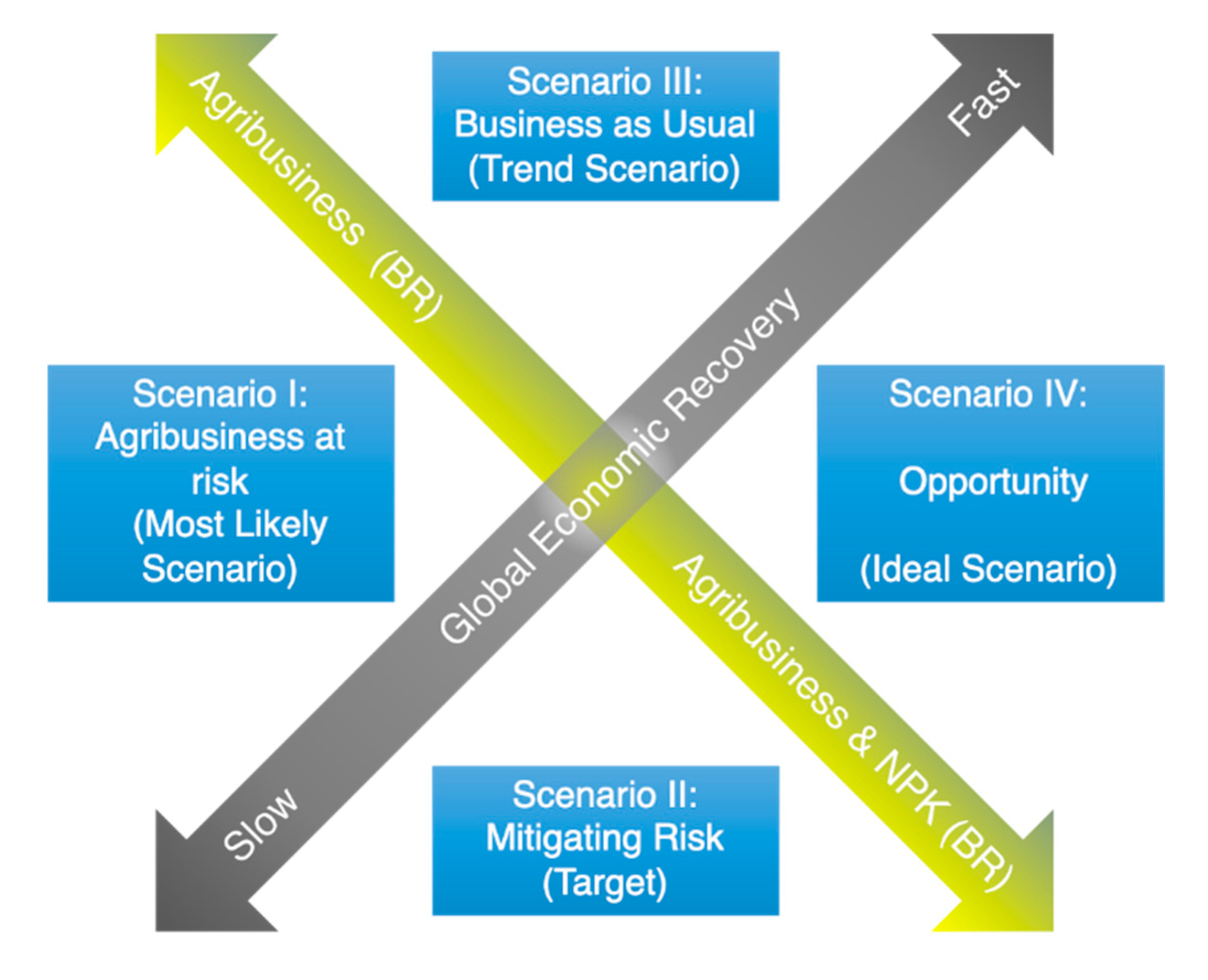

4. Results and Discussion

4.1. Scenario I: Agribusiness at Risk (Most Likely Scenario)

4.2. Scenario II: Mitigating Risk (Target)

4.3. Scenario III: Business as Usual (Trend Scenario)

4.4. Scenario IV: Opportunity (Ideal Scenario)

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- MAPA AGROSTAT. Foreign Trade Statistics-Ministry of Agriculture, Livestock and Supply of Brazil. Available online: http://indicadores.agricultura.gov.br/agrostat/index.htm (accessed on 2 June 2020).

- MAPA. Gross Value of Agricultural Production in 2019-Ministry of Agriculture, Livestock and Supply of Brazil. Available online: http://antigo.agricultura.gov.br/noticias/vbp-e-estimado-em-r-683-2-bilhoes-para-2020/copy_of_202002ValorBrutodaProduoPrincipaisProdutosAgropecurios.xlsx (accessed on 25 May 2020).

- IFA IFASTAT. Comsumption Report. Available online: https://www.ifastat.org/ (accessed on 1 June 2020).

- Hijbeek, R.; Van Loon, M.; Van Ittersum, M.K. Fertiliser Use and Soil Carbon Sequestration; CGIAR Research Program on Climate Chang, Agriculture and Food Security: Wageningen, The Netherlands, 2019; Volume 5. [Google Scholar]

- Burney, J.A.; Davis, S.J.; Lobell, D.B. Greenhouse gas mitigation by agricultural intensification. Proc. Natl. Acad. Sci. USA 2010, 107, 12052–12057. [Google Scholar] [CrossRef] [PubMed]

- IFA. Agenda 2030—Plant Nutrients and Climate Action. Available online: https://www.fertilizer.org/Public/Stewardship/Publication_Detail.aspx?SEQN=5854&PUBKEY=F8D6C582-AA17-4A43-BF31-43B36E10C236 (accessed on 3 August 2020).

- De Souza, L.M.; Mendes, P.; Aranda, D. Assessing the current scenario of the Brazilian biojet market. Renew. Sustain. Energy Rev. 2018, 98, 426–438. [Google Scholar] [CrossRef]

- EPE. Brazilian Energy Balance 2019-Year 2018; EPE: Rio de Janeiro, Brazil, 2019.

- BP. Statistical Review of World Energy 2018; BP: London, UK, 2019. [Google Scholar]

- EPE. National Energy Balance—Synthesis Report. Available online: https://www.epe.gov.br/sites-pt/publicacoes-dados-abertos/publicacoes/PublicacoesArquivos/publicacao-479/topico-521/RelatórioSínteseBEN2020-ab2019_Final.pdf (accessed on 29 July 2020).

- Brasil Law 13.576, 26 December 2017 (Renovabio). Available online: http://www.planalto.gov.br/ccivil_03/_ato2015-2018/2017/lei/L13576.htm (accessed on 31 July 2020).

- Ministry of Mines and Energy. Reunião da Câmara Setorial do Biodiesel. 7 June 2018. Available online: https://www.gov.br/agricultura/pt-br/assuntos/camaras-setoriais-tematicas/documentos/camaras-setoriais/oleaginosas-e-biodiesel/2018/33a-ro/apresentacao-renovabio-camara-setorial-biodiesel.pdf (accessed on 29 July 2020).

- ANDA. Setor de Fertilizantes—Anuário Estatístico de 2018, 1st ed.; Associação Nacional para Difusão de Adubos (ANDA): São Paulo, Brazil, 2019. [Google Scholar]

- COMEXTAT. Statistics from the Brazilian Foreign Trade Secretary. Available online: http://comexstat.mdic.gov.br/pt/home (accessed on 28 July 2020).

- Fernandes, F.R.C.; Kulaif, Y. Panorama dos agrominerais no Brasil: Atualidades e perspectivas. In Agrominerais para o Brasil; Fernandes, F.R.C., da Luz, A.B., Castilhos, Z.C., Eds.; CETEM: Rio de Janeiro, Brazil; MCT: Rio de Janeiro, Brazil, 2010; pp. 1–20. ISBN 9788561121617. [Google Scholar]

- Ramirez, R.; Selsky, J.W.; van der Heijden, K. Business Planning for Turbulent Times, 1st ed.; Ramirez, R., Selsky, J.W., van der Heijden, K., Eds.; Earthscan: London, UK, 2010; ISBN 978-1-84407-567-6. [Google Scholar]

- Popper, R. How are foresight methods selected? Foresight 2008, 10, 62–89. [Google Scholar] [CrossRef]

- Godet, M. Future memories. Technol. Forecast. Soc. Chang. 2010, 77, 1457–1463. [Google Scholar] [CrossRef]

- Schoemaker, P.J.H. Forecasting and scenario planning: The challenges of uncertainty and complexity. In Blackwell Handbook of Judgment and Decision Making; Blackwell Publishing Ltd.: Malden, MA, USA, 2008; pp. 274–296. ISBN 9781405107464. [Google Scholar]

- Marcial, E.C.; Grumbach, R.J.D.S. Cenários Prospectivos: Como Construir um Futuro Melhor, 5th ed.; FGV Editora: Rio de Janeiro, Brazil, 2008; ISBN 9788522506880. [Google Scholar]

- Marchais-Roubelat, A.; Roubelat, F. The Delphi method as a ritual: Inquiring the Delphic Oracle. Technol. Forecast. Soc. Chang. 2011, 78, 1491–1499. [Google Scholar] [CrossRef]

- Ringland, G.; Young, L. Scenarios in Marketing: From Vision to Decision; John Wiley & Sons, Inc.: Chichester, UK, 2015; ISBN 9780470666265. [Google Scholar]

- FIESP. Outlook FIESP 2029—Projections for the Brazilian Agribusiness; FIESP: São Paulo, Brazil, 2020; ISBN 978-65-5786-001-04. [Google Scholar]

- de Miranda, R.A.; Duraes, F.O.M.; Garcia, J.C.; Parentoni, S.; Santada, D.P.; Purcino, A.A.C.; de Alves, E.R.A. Supersafra de milho e o papel da tecnologia no aumento da produção. Rev. Política Agrícola 2019, 1, 149–150. [Google Scholar]

- CONAB. Acompanhamento da safra brasileira 2019/2020. In Acompanhamento da Safra Brasileira de Grãos 2019/2020; CONAB: Brasília, Brazil, 2020; Volume 7, pp. 1–74. [Google Scholar]

- CONAB. Planilhas de Custos de Produção-Culturas de 1 a Safra. Available online: https://www.conab.gov.br/info-agro/custos-de-producao/planilhas-de-custo-de-producao/itemlist/category/406-planilhas-de-custos-de-producao-culturas-de-1-safra (accessed on 30 July 2020).

- CONAB. Planilhas de Custos de Produção-Culturas de 2 a Safra. Available online: https://www.conab.gov.br/info-agro/custos-de-producao/planilhas-de-custo-de-producao/itemlist/category/404-planilhas-de-custos-de-producao-culturas-de-2-safra (accessed on 30 July 2020).

- CONAB. Planilhas de Custos de Produção-Culturas Semiperenes. Available online: https://www.conab.gov.br/info-agro/custos-de-producao/planilhas-de-custo-de-producao/itemlist/category/407-planilhas-de-custos-de-producao-culturas-semi-perenes (accessed on 30 July 2020).

- FAO. Lessons from the world food crisis of 2006–08. In The State Food Insecurity in the World; FAO: Rome, Italy, 2011; Volume 2008, pp. 21–31. [Google Scholar]

- CETEM. Mineraldata from Ministry of Science and Technology (Brazil). Available online: http://mineraldata.cetem.gov.br/mineraldata/app/* (accessed on 20 July 2020).

- ANDA. III Congresso Brasileiro de Fertilizantes-Indústria Nacional de Matéria Prima para Fertilizantes: Investimentos 2013 a 2018. Available online: http://anda.org.br/wp-content/uploads/2018/10/Investimentos_Rodolfo_Galvani.pdf (accessed on 30 July 2020).

- IFA. Fertilizer Outlook 2016–2020; IFA: Paris, France, 2016; pp. 21–23. [Google Scholar]

- IFA. Fertilizer outlook 2018–2022. In Proceedings of the 86th IFA Annual Conference Production & International Trade and Agriculture Services, Berlin, Germany, 18–20 June 2018; pp. 1–8. [Google Scholar]

- IFA. Short-Term Fertilizer Outlook; IFA: Paris, France, 2018; pp. 26–28. [Google Scholar]

- IFA. Short-Term Fertilizer Outlook. Available online: https://www.ifastat.org/market-outlooks (accessed on 30 July 2020).

- Word Bank Group. Global Economic Prospects-SLow Growth, Policy Challenges. Available online: https://openknowledge.worldbank.org/handle/10986/2140 (accessed on 31 July 2020).

- IFA. COVID-19 Implications for the Fertilizer Industry. Available online: https://www.arabfertilizer.org/news/item/id/215 (accessed on 31 July 2020).

- Globalfert Outlook 2020. Available online: https://globalfert.com.br/pdf/outlook_globalfert2020.pdf (accessed on 31 July 2020).

- Jank, M.S. Postface. In China-Brazil Partnership on Agriculture and Food Security; Jank, M.S., Guo, P., de Miranda, S.H.G., Eds.; Escola Superior de Agricultura “Luiz de Queiroz”, Universidade de São Paulo: Piracicaba, Brazil, 2020; ISBN 9786587391007. [Google Scholar]

- Ministry of Mines and Energy. Boletim Mensal de Acompanhameno da Indústria de Gás Natural-Março de 2020. Available online: http://www.mme.gov.br/web/guest/secretarias/petroleo-gas-natural-e-biocombustiveis/publicacoes/boletim-mensal-de-acompanhamento-da-industria-de-gas-natural/-/document_library_display/M02KzA2dNdQq/view_file/1161936?_110_INSTANCE_M02KzA2dNdQq_redirect=http%25 (accessed on 30 July 2020).

- Acron. 2018 Annual Report—Acron Group. Available online: https://www.acron.ru/en/press-center/press-releases/200627/ (accessed on 6 May 2020).

- PhosAgro. Integrated Report 2018—Pure Mineral for Healthy Lifes. Available online: https://www.phosagro.com/upload/iblock/604/604e741aa079745b02a0c47ca360a814.pdf (accessed on 25 May 2020).

- Word Bank Group. Global Economic Prospects, January 2018: Broad-Based Upturn, but for How Long? Global Economic Prospects; The World Bank: Washington, DC, USA, 2018; ISBN 978-1-4648-1163-0. [Google Scholar]

- Brasil Resolution N° 16–24 June 2019. Available online: http://www.mme.gov.br/documents/36112/491934/1.+Resolução_CNPE_16_2019.pdf/2d2e22aa-b6d8-d939-4eab-826b117f560b (accessed on 31 July 2020).

- Brasil National Congress Bill 6407/2013. Available online: https://www.camara.leg.br/proposicoesWeb/fichadetramitacao?idProposicao=593065 (accessed on 31 July 2020).

- IBRAM. Políticas Públicas para Indústria Mineral. Available online: https://portaldamineracao.com.br/wp-content/uploads/2018/11/eleicoes-2018-politicas-publicas-para-a-industria-mineral.pdf (accessed on 31 July 2020).

- Abram, M.B.; Bahiense, I.C.; Porto, C.G.; Brito, R.S. Projeto Fosfato Brasil, 1st ed.; Abram, M.B., Ed.; CPRM: Salvador, Brazil, 2011; ISBN 978-85-7499-125-2.

- Vale Formulário 20-F para o Exercício Encerrado em 31 de Dezembro de 2018. Available online: http://www.vale.com/brasil/PT/investors/information-market/annual-reports/20f/Paginas/default.aspx (accessed on 31 July 2020).

- National Mining Agency. Sumário Mineral 2017, 1st ed.; Costa, M.M.D., Medeiros, K.A., Lima, T.M., Eds.; ANM/MME: Brasília, Brazil, 2019; Volume 37.

- Sinprifert; Abiquim. Fertilizantes: A Busca do Produtor Nacional por Condições de Igualdade com o Produto Importado-National Congress. Available online: https://www2.camara.leg.br/atividade-legislativa/comissoes/comissoes-permanentes/capadr/audiencias-publicas/audiencias-publicas-2015/mesa-tecnica-16-de-dezembro-vale-fertilizantes (accessed on 20 July 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Event | Question | Average Result (2 Rounds) |

|---|---|---|

| 1—Slowdown in global economic growth | How likely is it that, until 2035, there will be an overall slowdown in the growth of the global economy (rates below 2.5% growth in 2020–2035)? | 55.09% |

| 2—Slowdown in China’s GDP growth | How likely is it that by 2035 Chinese GDP growth will have slowed (rates below 5.0% growth per year in 2020–2035)? | 61.99% |

| 3—Maintenance of moderate prices, food commodities | How likely is that the main food commodities will largely remain at moderate prices until 2035? | 56.91% |

| 4—Reduction in the participation of O&G in the world energy matrix | How likely is it that by 2035 the global energy market will have reduced its dependence on the O&G industry (currently around 58%, accounting for oil and natural gas) to 45% or less? | 62.15% |

| 5—Increase in biofuel consumption by the Brazilian transportation sector | How likely is that by 2035 biofuels (biodiesel and ethanol) will provide 30% (or more) of the fuel needs of the transport sector in Brazil? | 64.16% |

| 6—Increase in mergers and acquisitions in the global NPK fertilizer industry | How likely is that there will be an increase in the number of mergers and acquisitions in the global industry of production of essential inputs for the agribusiness chain (NPK fertilizers) until 2035? | 64.33% |

| 7—Increase in gross value of agricultural production in Brazil | How likely is that by 2035 the gross value of agricultural production (considering only crops) will have shown (predominantly) average annual growth of more than 6% per year in the last 15 years? | 54.52% |

| 8—Increased share of the manufacturing industry in Brazilian GDP | How likely is that by 2035 the Brazilian manufacturing industry will again account for at least 20% of GDP? | 44.82% |

| 9—Government incentives (tax, credit, or other) for the fertilizer industry in Brazil | How likely is it that until 2035 the Brazilian government will have created tax, credit or other forms of incentives for the fertilizer industry in Brazil? | 47.76% |

| Event | Most Likely Scenario | Ideal Scenario | Trend Scenario | Event Classification | Target Scenario |

|---|---|---|---|---|---|

| 1—Slowdown in global economic growth | Occurs | Does not occur | Does not occur | Moderate threat, change in trend | Occurs |

| 2—Slowdown in China’s GDP growth | Occurs | Does not occur | Does not occur | Moderate threat, change in trend | Occurs |

| 3—Maintenance of moderate prices for food commodities | Occurs | Does not occur | Occurs | Strong threat, no change in trend | Occurs |

| 4—Reduction in the participation of O&G in the world energy matrix | Occurs | Occurs | Does not occur | Moderate opportunity, change in trend | Occurs |

| 5—Increase in biofuel consumption by the Brazilian transportation sector | Occurs | Occurs | Occurs | Strong opportunity, no change in trend | Occurs |

| 6—Increase in mergers and acquisitions in the global NPK fertilizer industry | Occurs | Does not occur | Occurs | Strong threat, no change in trend | Occurs |

| 7—Increase in the gross value of agricultural production in Brazil | Occurs | Occurs | Does not occur | Moderate opportunity, change in trend | Occurs |

| 8—Increased share of the manufacturing industry in Brazilian GDP | Does not occur | Occurs | Does not occur | Strong threat, no change in trend | Does not occur |

| 9—Government incentives (tax, credit or other) for the fertilizer industry in Brazil | Does not occur | Occurs | Does not occur | Strong threat, no change in trend | Occurs |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Farias, P.I.V.; Freire, E.; Cunha, A.L.C.d.; Grumbach, R.J.d.S.; Antunes, A.M.d.S. The Fertilizer Industry in Brazil and the Assurance of Inputs for Biofuels Production: Prospective Scenarios after COVID-19. Sustainability 2020, 12, 8889. https://doi.org/10.3390/su12218889

Farias PIV, Freire E, Cunha ALCd, Grumbach RJdS, Antunes AMdS. The Fertilizer Industry in Brazil and the Assurance of Inputs for Biofuels Production: Prospective Scenarios after COVID-19. Sustainability. 2020; 12(21):8889. https://doi.org/10.3390/su12218889

Chicago/Turabian StyleFarias, Pedro Igor Veillard, Estevão Freire, Armando Lucas Cherem da Cunha, Raul José dos Santos Grumbach, and Adelaide Maria de Souza Antunes. 2020. "The Fertilizer Industry in Brazil and the Assurance of Inputs for Biofuels Production: Prospective Scenarios after COVID-19" Sustainability 12, no. 21: 8889. https://doi.org/10.3390/su12218889

APA StyleFarias, P. I. V., Freire, E., Cunha, A. L. C. d., Grumbach, R. J. d. S., & Antunes, A. M. d. S. (2020). The Fertilizer Industry in Brazil and the Assurance of Inputs for Biofuels Production: Prospective Scenarios after COVID-19. Sustainability, 12(21), 8889. https://doi.org/10.3390/su12218889