Public Procurement in the South African Economy: Addressing the Systemic Issues

Abstract

1. Introduction

2. Methodology

3. Literature Review and Background to the Study

3.1. Contextualisation of Public Procurement

3.2. A Public Procurement Policy Framework

| The National Development Plan 2030 (National Planning Commission) The National Development Plan (NDP) [20] is the underpinning South African public strategic framework for growth and development, as developed in 2012 by the National Planning Commission. The NDP encapsulates the long-term vision of the South African government towards establishing and sustaining an equitable society. With a visionary approach for 2030, the so-called “transformation imperatives” of the 20 years following the development of the NDP “envisage inclusive growth and sustainability through increased levels of employment of young people, growing sound local scale of economic competition, transformed urban landscapes, addressing racial and other societal rifts, and adapting to a low-carbon economy”. The New Growth Path (Economic Development Department) Developed and published by the Economic Development Department in November 2010, the New Growth Path (NGP) promulgates “the necessity of a more labour-intensive growth path in South Africa. The NGP identifies specific target sectors to accelerate this employment increase and recommends complementary competitive and employment-friendly growth macro and micro policy-packages” [4]. |

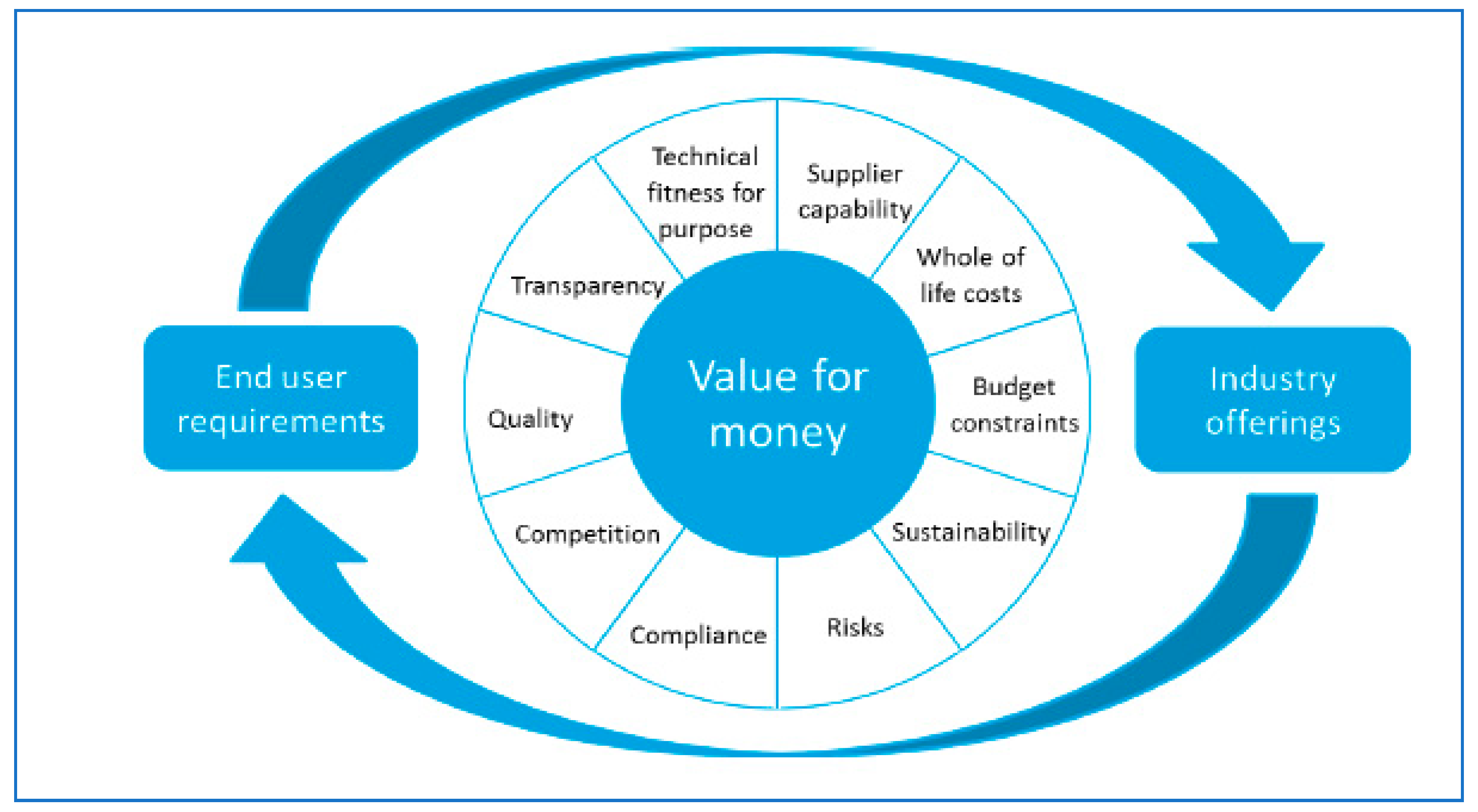

- Value for Money. The use of price as a single indicator is often unreliable, and therefore public entities cannot automatically justify best value for money by based on acceptance of the lowest price offer, as prescribed. Best value for money refers to the “best available outcome when all applicable costs and benefits over the procurement cycle have been taken into consideration”.

- Open and Effective Competition. This requires transparent policies, guidelines, procedures and practices, readily accessible to all parties so that they can compete openly and fairly.

- Ethics and Fair Dealing. This pillar requires all parties to act within ethical standards, based on of mutual respect, trust. They are required to go about their business in a reasonable and rational manner and with integrity.

- Accountability and Reporting. Individuals and organisations are accountable for their plans, actions, and outcomes, and are bound to openness and transparency in administration, by external scrutiny through public reporting.

- Equity. This fifth pillar is vital for public sector procurement in South Africa to guarantee commitment to economic growth, by implementing specific industry support measures with emphasis on the accelerated growth of Small, Medium and Micro Enterprises (SMMEs) and Historically Disadvantaged Individuals.

4. Discussion on the Issues Arising from the Document Analysis

4.1. Reality of Public Procurement in South Africa: Auditor General Findings

4.2. Challenges in South African Public Procurement

4.2.1. Over- and Underspending of Budgets

4.2.2. Contracts Management

- “bid documents were not published (only advertisements were published);

- bid committee meeting evaluation minutes and standard contracts were not made available to the public;

- bids were not opened in public and published—best practice requires that bidders and their prices be made known by public announcement during the opening of bids and by publishing this information;

- the entire evaluation process was not open to scrutiny (close cooperation between the public and private sectors, civil society and other stakeholders is important for the integrity of public sector SCM); and

- progress and contract implementation reports were not made publicly available” [39].

4.2.3. Lack of Requisite Capacity, Skills and Knowledge

4.2.4. Inadequate Planning and Linking of Demand to the Budget

4.2.5. Inadequate Monitoring and Evaluation (M&E) of SCM

4.2.6. Non-Compliance with SCM Policy and Regulations

- In order to curtail possible material misstatements in the financial and service delivery information in financial statements and annual reports, compliance to finance management acts (the PFMA and MFMA) as well as the Treasury Regulations’ reporting requirements, is essential;

- To prevent noncompliance such as unethical tender processes (government employees or their relatives conducting business with government, amongst others), compliance to SCM prescripts in procuring goods and services;

- Detection and prevention of any unlawful activities such as “irregular, unauthorised and fruitless and wasteful expenditure”;

- Human resource planning and appointment processes;

- Determine the degree to which funding money allocated for special projects, for example funding for the building of clinics or learner transport to/from schools, is in fact spent in line with the purpose as legislated; and

- Compliance to legislative prescripts pertaining to payments of service providers to occur within a 30-day period, in order to avoid late payments [40].

4.2.7. Lack of Accountability and Unethical Behaviour, Resulting in Possible Fraud and Corruption

4.2.8. High Level of Decentralisation of the Procurement System

4.2.9. Lack of Consequence Management at Executive Level

5. Improvement Recommendations to Challenges Faced by South African Public Procurement

5.1. Prevention Is Always Better than Finding a Cure

5.2. It Is Virtually Impossible to Get Lost with Clear Directions and a Reliable Map

5.3. As the Saying Goes—“Structure Follows Strategy”

5.4. All Actions Have Consequences and Should Be Managed Accordingly

6. Conclusions—Never Has There Been a Better Time to Address Our Shortcomings and Overcome the Obstacles of Our Past

Author Contributions

Funding

Conflicts of Interest

References

- Eye Witness News. Statement by President Cyril Ramaphosa on Escalation of Measures to Combat Covid-19 Epidemic. 23 March 2020. Available online: https://ewn.co.za/ (accessed on 30 March 2020).

- Organisation for Economic Co-operation and Development (OECD). Public Procurement for Sustainable and Inclusive Growth: Enabling Reform through Evidence and Peer Reviews. 2017, pp. 1–18. Available online: https://www.oecd.org/gov/ethics/Public-Procurement-for%20Sustainable-and-Inclusive-Growth_Brochure.pdf (accessed on 31 March 2020).

- Turley, L.; Perera, O. Implementing sustainable public procurement in South Africa: Where to start. Int. Inst. Sustain. Dev. 2014, 1–63. Available online: www.iisd.org (accessed on 31 March 2020).

- Brunette, R.; Klaaren, J. The Public Procurement Bill Needs Muscle to Empower Whistle-Blowers. The Daily Maverick. 5 March 2020. Available online: https://www.dailymaverick.co.za/article/2020-03-05-the-public-procurement-bill-needs-muscle-to-empower-whistle-blowers/ (accessed on 14 April 2020).

- Auriacombe, C.J. Towards the construction of unobtrusive research techniques: Critical considerations when conducting a literature analysis. Afr. J. Public Aff. 2016, 9, 1–19. [Google Scholar]

- Bowen, G.A. Document analysis as qualitative research method. Qual. Resour. J. 2009, 9, 27–40. [Google Scholar] [CrossRef]

- Burger, P. Facing the conundrum: How useful is the “developmental state” concept in South Africa? South Afr. J. Econ. 2014, 82, 159–180. [Google Scholar] [CrossRef]

- Harpe, S. Public Procurement Law: A Comparative Analysis. Ph.D. Thesis, University of South Africa, Pretoria, South Africa, 2009; pp. i–iii. [Google Scholar]

- Odhiambo, W.; Kamau, P. Public procurement: Lessons from Kenya, Tanzania and Uganda. In OECD Development Centre: Working Paper No. 208; OECD iLibrary: Paris, France, 2003; pp. 1–20. Available online: https://doi.org/10.1787/804363300553 (accessed on 15 October 2020).

- Ambe, I.M.; Badenhorst-Weiss, J.A. Procurement challenges in the South African public sector. J. Transp. Supply Chain Manag. 2012, 6, 243–261. Available online: https://jtscm.co.za/index.php/jtscm/article/view/63 (accessed on 30 March 2020).

- World Bank. Procurement for Development. 2020, pp. 1–4. Available online: https://www.worldbank.org/en/topic/procurement-for-development (accessed on 30 March 2020).

- Mazibuko, G.; Fourie, D.J. Manifestation of unethical procurement practices in the South African public sector. Afr. J. Public Aff. 2017, 9, 106–117. [Google Scholar]

- Arrowsmith, S. Public procurement Regulations: An introduction. EU Asia Inter Univ. Netw. 2010, 1, 1–30. [Google Scholar]

- Hommen, L.; Rolfstam, M. Public procurement and innovation: Towards taxonomy. J. Public Procure. 2009, 9, 20–22. [Google Scholar]

- OECD. Productivity in Public Procurement: A Case Study of Finland: Measuring the Efficiency and Effectiveness of Public Procurement. 2019, pp. 9–10. Available online: https://www.oecd.org/gov/public-procurement/publications/productivity-public-procurement.pdf (accessed on 30 March 2020).

- Deloitte Access Economics. Economic Benefits of Better Procurement Practices. 2015, pp. 47–66. Available online: https://www2.deloitte.com/content/dam/Deloitte/au/Documents/Economics/deloitte-au-the-procurement-balancing-act-170215.pdf (accessed on 31 March 2020).

- Selomo, M.R.; Govender, K.K. Procurement and Supply Chain Management in government institutions: A case study of select departments in the Limpopo Province, South Africa. Dutch J. Financ. Manag. 2016, 1, 1–10. Available online: https://s3.amazonaws.com/academia.edu.documents/50733366/ (accessed on 10 May 2020).

- Mhelembe, K.; Mafini, C. Modelling the link between supply chain risk flexibility and performance in the public sector. South Afr. J. Econ. Manag. Sci. 2019, 22, 1–12. Available online: https://doi.org/10.4102/sajems.v22i1.2368 (accessed on 30 March 2020).

- Department of Public Enterprises. Strategic Plan 2018/2019. Republic of South Africa. 2017; pp. 1–36. Available online: http://www.dpe.gov.za/ (accessed on 8 April 2020).

- National Planning Commission. National Development Plan 2030; 15 August 2012; pp. 456–478. Available online: http://www.gov.za/issues/national-development-plan/index.html (accessed on 8 April 2020).

- Molver, A.; Noeth, G. South Africa. The Government Procurement Law Review. 2017, Volume 5, pp. 212–228. Available online: https://thelawreviews.co.uk/digital_assets/d8b0f256-b922-40d3-815d-9c7584eab2b7/The-Government-Procurement-Review-5th-ed---book.pdf (accessed on 30 March 2020).

- Bowmans. Guide to Government Contracting and Public Procurement in South Africa. 2016, pp. 8–16. Available online: https://www.bowmanslaw.com/wp-content/uploads/2016/12/Guide-Public-Procurement-and-Government-Contracting-in-SA-1.pdf (accessed on 8 April 2020).

- National Treasury. General Procurement Guidelines; 2014; pp. 1–8. Available online: http://www.treasury.gov.za/legislation/pfma/supplychain/General%20Procurement%20Guidelines.pdf (accessed on 10 May 2020).

- Knight, L. Public Procurement; Routledge: London, UK, 2007; pp. 16–24. [Google Scholar]

- National Treasury. Chief Financial Officers Handbook for Departments; 2014; pp. 27–55. Available online: https://oag.treasury.gov.za/Publications/ (accessed on 10 May 2020).

- National Treasury. CEO/AO Training Programme. 2013; pp. 8–12. Available online: http://oag.treasury.gov.za (accessed on 10 May 2020).

- Fourie, D. Centralized, Decentralized and Collaborative Participatory Public Procurement: Quo Vadis. In Proceedings of the 9th Global Conference Forum for Economists International, Amsterdam, The Netherlands, 19–22 May 2017. [Google Scholar]

- National Treasury Instruction No. 8 of 2019/2020. Media statement: 3 April 2020; South Africa. Available online: http://www.treasury.gov.za (accessed on 5 April 2020).

- National Treasury Media Statement. 19 March 2020; South Africa. Available online: http://www.treasury.gov.za (accessed on 5 April 2020).

- AGSA. Auditor General South Africa Media Release: Auditor-General report “Act Now on Accountability”; 2019; pp. 1–19. Available online: https://www.agsa.co.za/Portals/0/Reports/PFMA/201819/MR/2019%20PFMA%20media%20release.pdf (accessed on 30 March 2020).

- AGSA. PFMA 2018/2019 Consolidated General Report on National and Provincial Audit Outcomes; 2019; pp. 12–38. Available online: https://www.agsa.co.za/Reporting/PFMAReports/PFMA2018-2019.aspx (accessed on 10 May 2020).

- AGSA. PFMA 2016/2017 Consolidated General Report on National and Provincial Audit Outcomes; 2017; pp. 60–82. Available online: https://www.agsa.co.za/Reporting/PFMAReports/PFMA2016-2017.aspx (accessed on 10 May 2020).

- AGSA. PFMA 2017/2018 Consolidated General Report on National and Provincial Audit Outcomes; 2018; pp. 15–22. Available online: https://www.agsa.co.za/Reporting/PFMAReports/PFMA2017-2018.aspx (accessed on 10 May 2020).

- National Treasury. Media Statement Local Government Revenue and Expenditure: Fourth Quarter Local Government Section 71 Report (Preliminary Results) for the Period: 1 July 2018–30 June 2019, 3 September 2019. pp. 1–7. Available online: http://pmg-assets.s3-website-eu-west-1.amazonaws.com/191015_Media_statement.pdf (accessed on 10 May 2020).

- Alexander, D.P. An Assessment of Capital Budget Planning and Municipal Borrowing as Funding Source in the Overstrand Municipality in the Western Cape; University of Cape Town: Cape Town, South Africa, 2015; pp. 8–12. [Google Scholar]

- Mbanda, V.; Bonga-Bonga, L. Municipal Infrastructure Spending Capacity in South Africa: A Panel Smooth Transition Regression (PSTR) Approach. MPRA Paper No. 91499. University of Johannesburg: Johannesburg, 16 January 2019; pp. 1–15. Available online: https://mpra.ub.uni-muenchen.de/91499/ (accessed on 10 May 2020).

- National Treasury. Medium Term Expenditure Framework, Technical Guidelines 2020; 2019; pp. 1–22. Available online: http://www.treasury.gov.za/publications/guidelines/2020%20MTEF%20Technical%20Guidelines.pdf (accessed on 10 May 2020).

- National Treasury. Principles of Public Administration and Financial Management Delegations. Cabinet Memorandum 56 of 2013; 2013; pp. 30–35. Available online: http://www.treasury.gov.za/legislation/pumas/delegations/ (accessed on 10 May 2020).

- National Treasury. 2015 Public Sector Supply Chain Management Review. 2015; Volume 3, pp. 15–25. Available online: http://www.treasury.gov.za/publications/other/SCMR%20REPORT%202015.pdf (accessed on 10 May 2020).

- AGSA Compliance with Laws and Regulations in Government will Fulfil the Aspirations of Citizens. Auditor-General Column. 2014. Available online: https://www.agsa.co.za/portals/0/AG/Compliance_with_laws.pdf (accessed on 10 May 2020).

- Ngwakwe, C.C. Public sector financial accountability and service delivery. J. Public Adm. 2012, 47, 311–329. Available online: https://journals.co.za/content/jpad/47/si-1/EJC121938 (accessed on 10 May 2020).

- Fourie, D.; Poggenpoel, W. Public sector inefficiencies: Are we addressing the root causes? South Afr. J. Account. Res. 2017, 31, 169–180. Available online: https://doi.org/10.1080/10291954.2016.1160197 (accessed on 1 April 2020). [CrossRef]

- Abrahams, M.A. A review of the growth of monitoring and evaluation in South Africa: Monitoring and evaluation as a profession, an industry and a governance tool. Afr. Eval. J. 2015, 3, 1–8. Available online: http://dx.doi.org/10.4102/aej.v3i1.14 (accessed on 10 May 2020). [CrossRef]

- Cloete, G.S. Measuring Good Governance in South Africa. 2009, pp. 1–8. Available online: https://www.researchgate.net/profile/G_S_Cloete/publication/242124530_Measuring_Good_Governance_in_South_Africa/links/5d372ce4a6fdcc370a59a27a/Measuring-Good-Governance-in-South-Africa.pdf (accessed on 10 May 2020).

- Mertens, D.M.; Ginsberg, P.E. The Handbook of Social Research Ethics; Sage: Los Angeles, CA, USA, 2009; pp. 3–26. [Google Scholar]

- Porter, S.; Goldman, I. A growing demand for monitoring and evaluation in Africa. Afr. Eval. J. 2013, 1, 8–9. Available online: http://dx.doi.org/10.4102/aej.v1i1.25 (accessed on 10 May 2020). [CrossRef]

- Sithomola, T.; Auriacombe, C.J. Developing a monitoring and evaluation (M&E) classification system to improve democratic good governance. Int. J. Soc. Sci. Humanit. Stud. 2019, 11, 86–101. Available online: https://www.researchgate.net/profile/Tshilidzi_Sithomola/publication/333043553 (accessed on 10 May 2020).

- Shai, L.; Molefinyana, C.; Qui, G. Public procurement in the context of Broad-Based Black Economic Empowerment (BBBEE) in South Africa—Lessons learned for sustainable public procurement. Sustainability 2019, 11, 7164. Available online: www.mdpi.com/journal/sustainability) (accessed on 1 April 2020). [CrossRef]

- Meyer, N.; Auriacombe, C. Good urban governance and city resilience: An Afrocentric approach to sustainable development. Sustainability 2019, 11, 5514. Available online: https://www.mdpi.com/2071-1050/11/19/5514 (accessed on 10 May 2020). [CrossRef]

- Dullah Omar Institute. Civic Protest Barometer 2018 Fact Sheet #3—Violence in Protests. 2020. Available online: https://dullahomarinstitute.org.za/acsl/barometers/civic-protest-barometer-2018-factsheet-3-violence-in-protests-final.pdf/view (accessed on 10 May 2020).

- Deliwe, M.C. The potential impact of the Public Audit Amendment Act of 2018, on the effectiveness of the Auditor-General South Africa. South. Afr. J. Account. Audit. Res. 2019, 21, 47–57. [Google Scholar]

{kind=link}

| Irregular Expenditure (IE) | Material Irregularity (MI) |

|---|---|

| IE is all expenditure where there was procedural non-compliance with legislation prior to the payment. When IE is identified, the accounting officer or authority is required to perform an investigation to determine the impact by considering if the non-compliance resulted in a financial loss, whether there was any fraud involved, and if an official should be held accountable. If there was no loss or fraud, the IE will be condoned after the necessary disciplinary action had been taken. | As with IE, a MI also originates from legislative and procedural non-compliance, but has a broader scope and can include instances of fraud, theft and a breach of fiduciary duty. Another key difference is that for any non-compliance to be considered an MI, there must already be an indication that the non-compliance resulted in, or is likely to have, a so-called “material impact”, for example the misappropriation or loss of a material public resource, a material financial loss incurred, or substantial harm to a public sector institution or the general public has ensued. |

| AGSA Most Common Findings | Financial Year | Reasons | Possible Solutions |

|---|---|---|---|

| Audits not been completed | 16/17, 17/18, 18/19 | Late or non-submission of financial statements and outstanding information resulting in non-completion of audits. | This could be resolved by strengthening financial management, and financial record keeping and ensuring the availability and effective management of procurement documentation |

| Dearth of commitment and accountability towards sound administration | 16/17, 17/18, 18/19 | The Leadership response focused on contesting of the audit conclusions instead of strengthening the fragile control environment. | Strengthened and stabilised leadership is required, who are held accountable; as well as an implementation and strengthening of especially procurement controls. |

| Irregular expenditure | 16/17, 17/18, 18/19 |

|

|

| Promotion of local production and content | 16/17 | Lack of awareness and understanding demonstrated by Auditees pertaining to requirements, even a disdain for such in certain instances. |

|

| Contracts awarded to employees and their families without the necessary declarations of interest | 16/17, 17/18, 18/19 |

|

|

| Fruitless and wasteful expenditure | 16/17, 17/18 |

|

|

| Trend of contestations | 17/18, 18/19 |

|

|

| Increase material non-compliance with legislation | 17/18 |

|

|

| Lack of consequence management in addressing instances of transgressions or poor performance/compliance levels | 18/19 | Investigations and proper consequence management are not followed, which means that there is little deterrence for continuous poor performance. |

|

| Key positions with vacancy rates or challenged by constant changes of appointments | 18/19 | High vacancy rates of key positions lead to an increase in unauthorised, irregular and wasteful and fruitless expenditure. It also leads to poor financial management and poor financial statements. |

|

| Trend noticed of lack implementation of AGSA’s recommendations pertaining to requisite improvement of internal controls and address risks | 18/19 | AGSA’s recommendations are not being implemented, resulting in repeat findings. |

|

| Legal action and claims against government departments | 18/19 |

|

|

| Increase in failingtopay creditors within 30 days | 18/19 |

| Proper budget and payment controls, cash flow management and consequence management need to be implemented to serve as a deterrent. |

| 2015/16 | |||

|---|---|---|---|

| R thousands | (Over) | Under | Nett |

| Total | (3,079,327) | 43,699,930 | 40,620,603 |

| Capital | (1,037,171) | 13,408,789 | 12,371,618 |

| Operating | (3,053,249) | 31,302,234 | 28,248,985 |

| 2016/17 | |||

| R thousands | (Over) | Under | Nett |

| Total | (1,766,257) | 53,093,175 | 51,326,919 |

| Capital | (1,389,980) | 15,828,308 | 14,438,328 |

| Operating | (1,482,741) | 38,371,331 | 36,888,591 |

| 2017/18 | |||

| R thousands | (Over) | Under | Nett |

| Total | (22,626,540) | 66,833,502 | 44,206,962 |

| Capital | (8,186,799) | 20,812,583 | 12,625,783 |

| Operating | (15,108,441) | 46,689,620 | 31,581,179 |

| 2018/19 | |||

| R thousands | (Over) | Under | Nett |

| Total | (3,843,598) | 57,804,639 | 53,961,040 |

| Capital | (836,236) | 18,982,576 | 18,146,340 |

| Operating | (4,871,939) | 40,686,639 | 35,814,700 |

| OECD 2015 Recommendations on Public Procurement | Challenges in SA Public Procurement |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fourie, D.; Malan, C. Public Procurement in the South African Economy: Addressing the Systemic Issues. Sustainability 2020, 12, 8692. https://doi.org/10.3390/su12208692

Fourie D, Malan C. Public Procurement in the South African Economy: Addressing the Systemic Issues. Sustainability. 2020; 12(20):8692. https://doi.org/10.3390/su12208692

Chicago/Turabian StyleFourie, David, and Cornel Malan. 2020. "Public Procurement in the South African Economy: Addressing the Systemic Issues" Sustainability 12, no. 20: 8692. https://doi.org/10.3390/su12208692

APA StyleFourie, D., & Malan, C. (2020). Public Procurement in the South African Economy: Addressing the Systemic Issues. Sustainability, 12(20), 8692. https://doi.org/10.3390/su12208692