Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach

Abstract

1. Introduction

2. Background

3. Materials and Methods

3.1. In-Depth Face-To-Face Interviews with Firms’ Managers and Scholar Experts

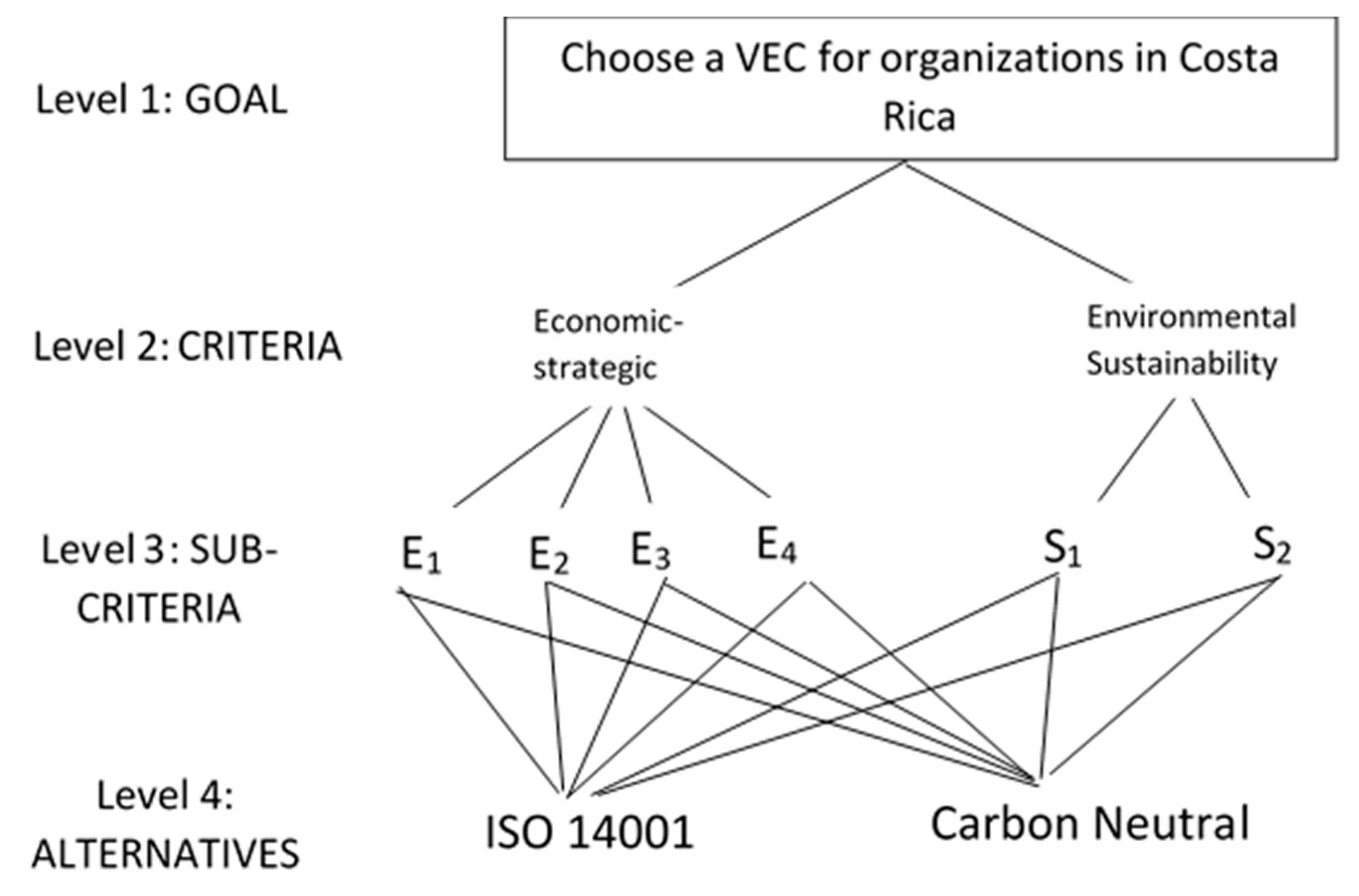

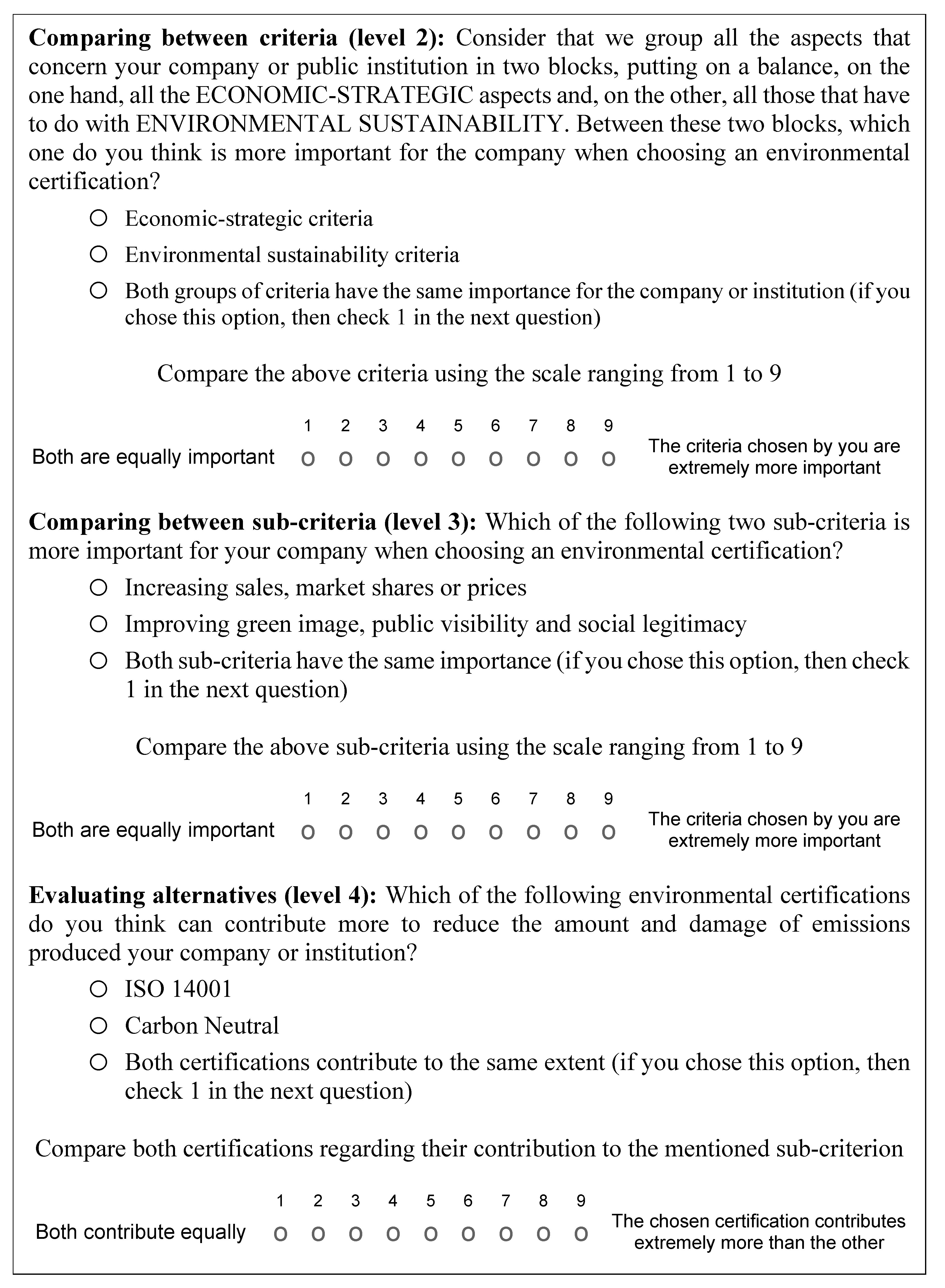

3.2. Questionnaire and AHP Application

4. Results and Discussion

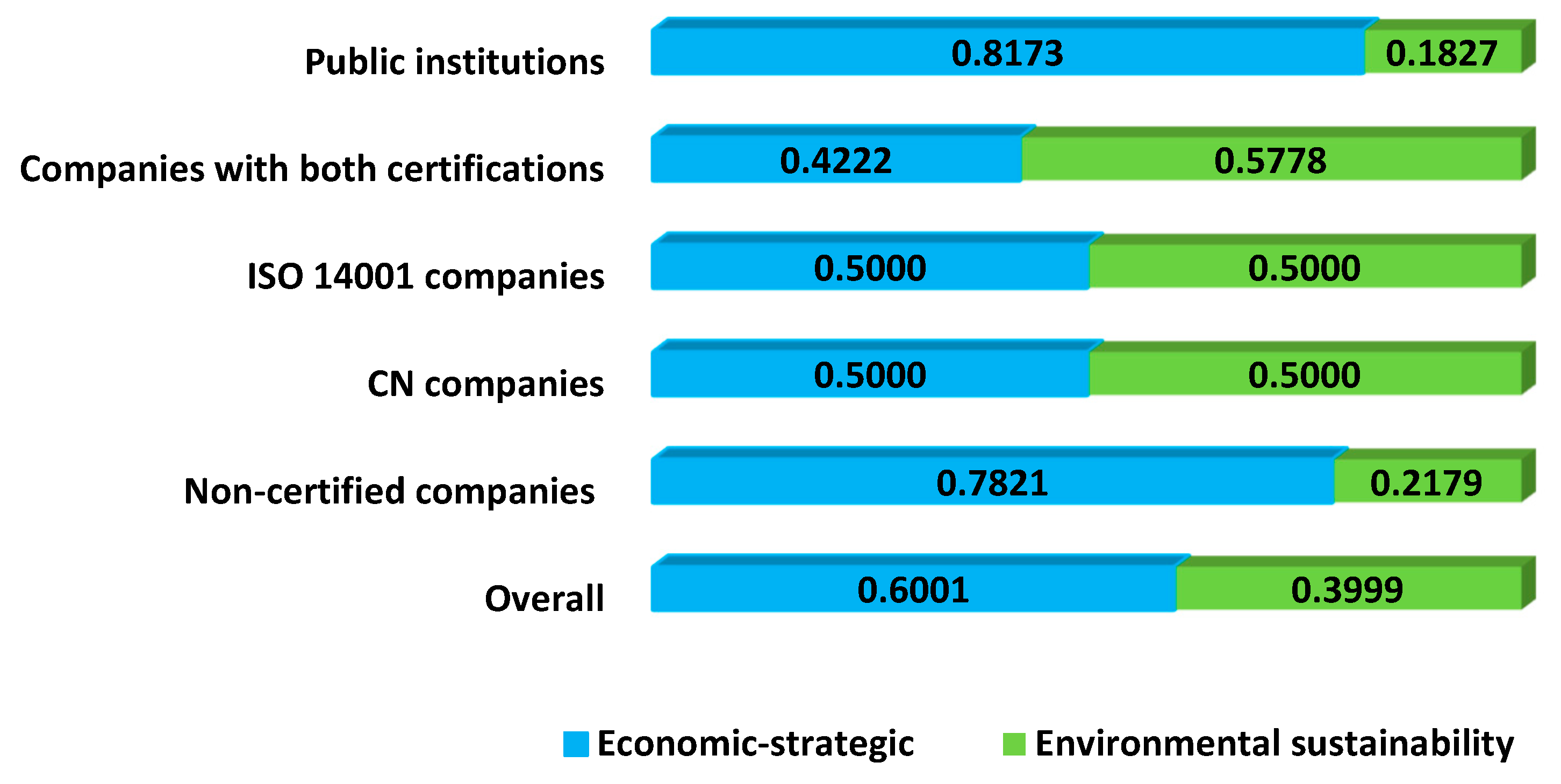

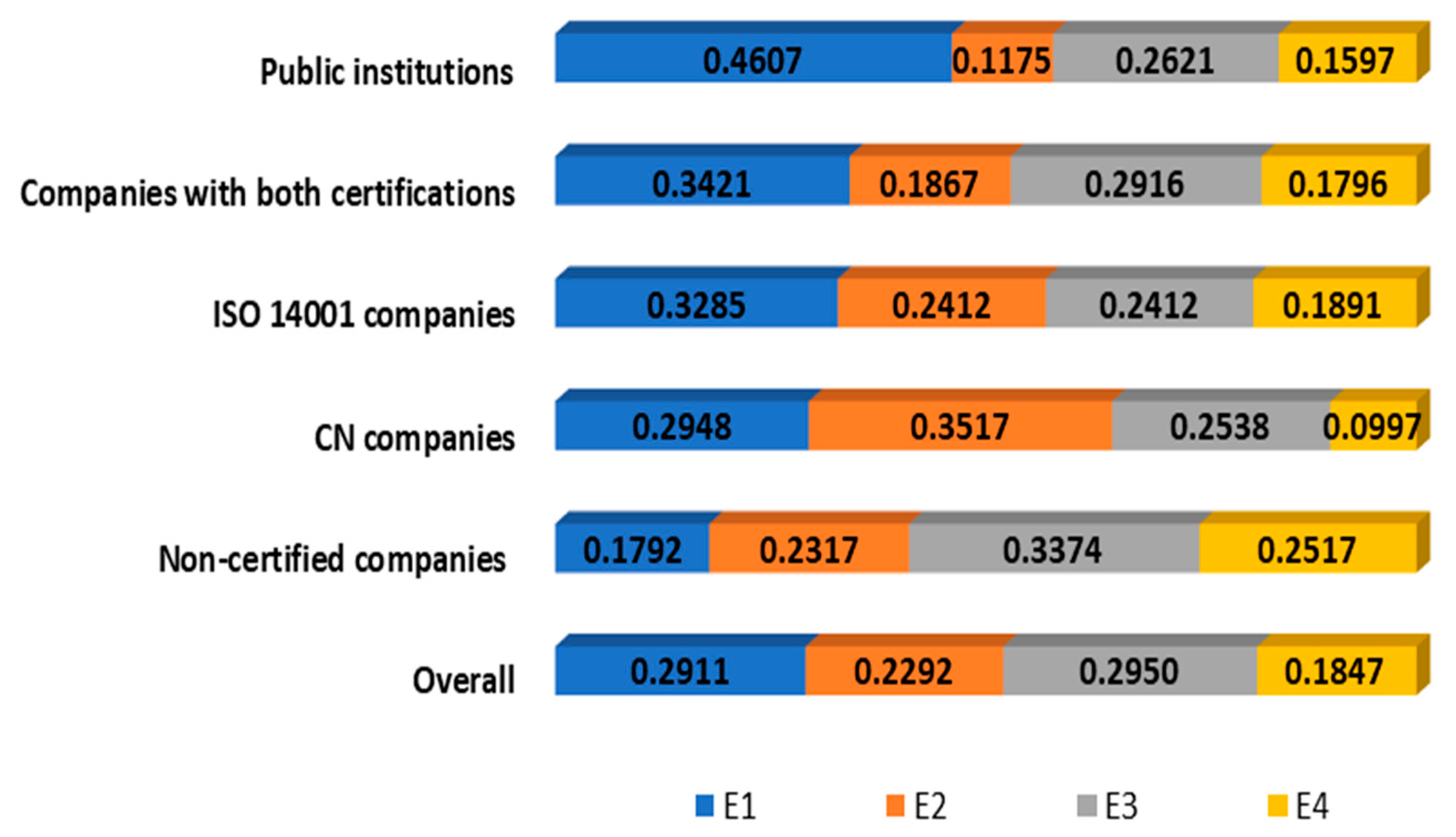

4.1. Overall Results

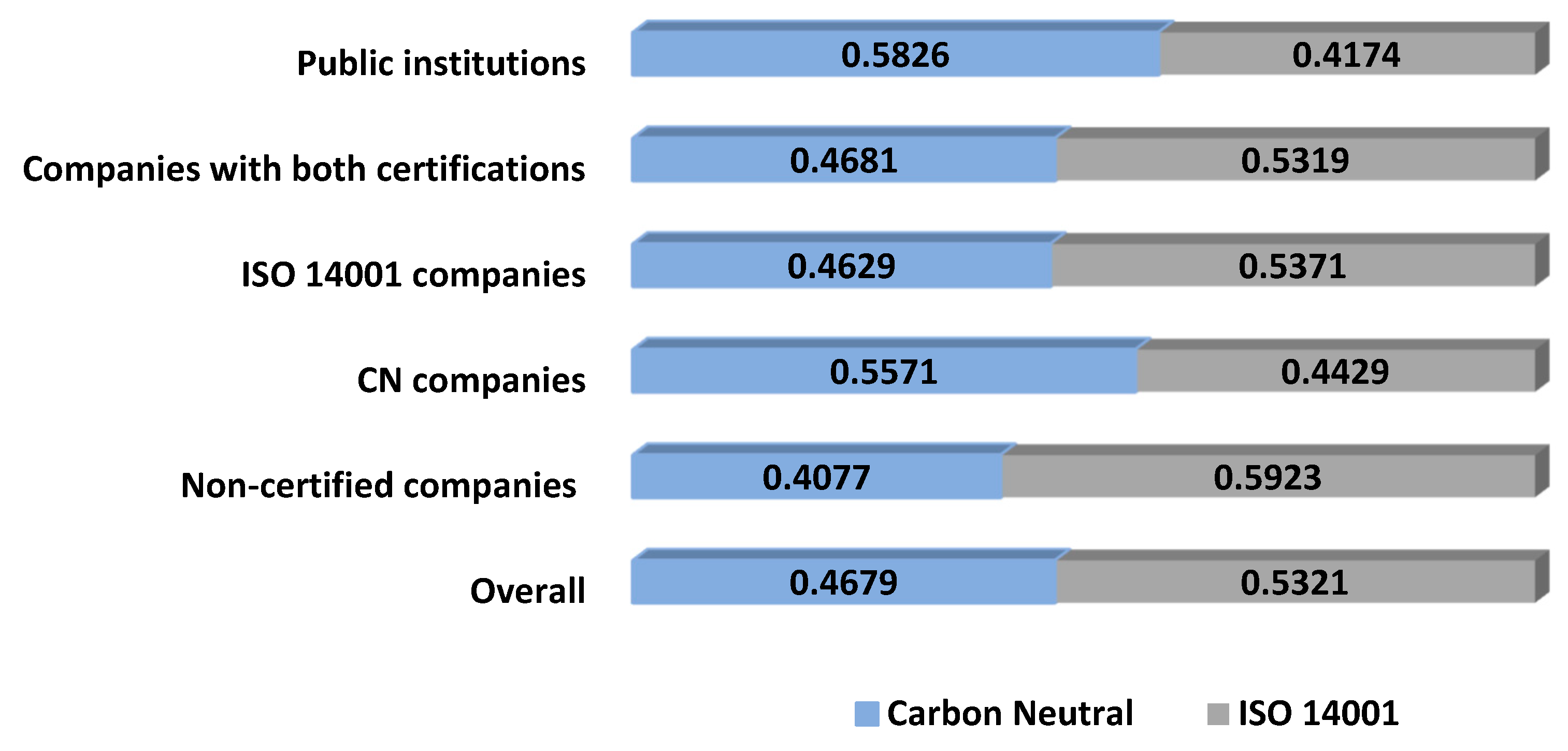

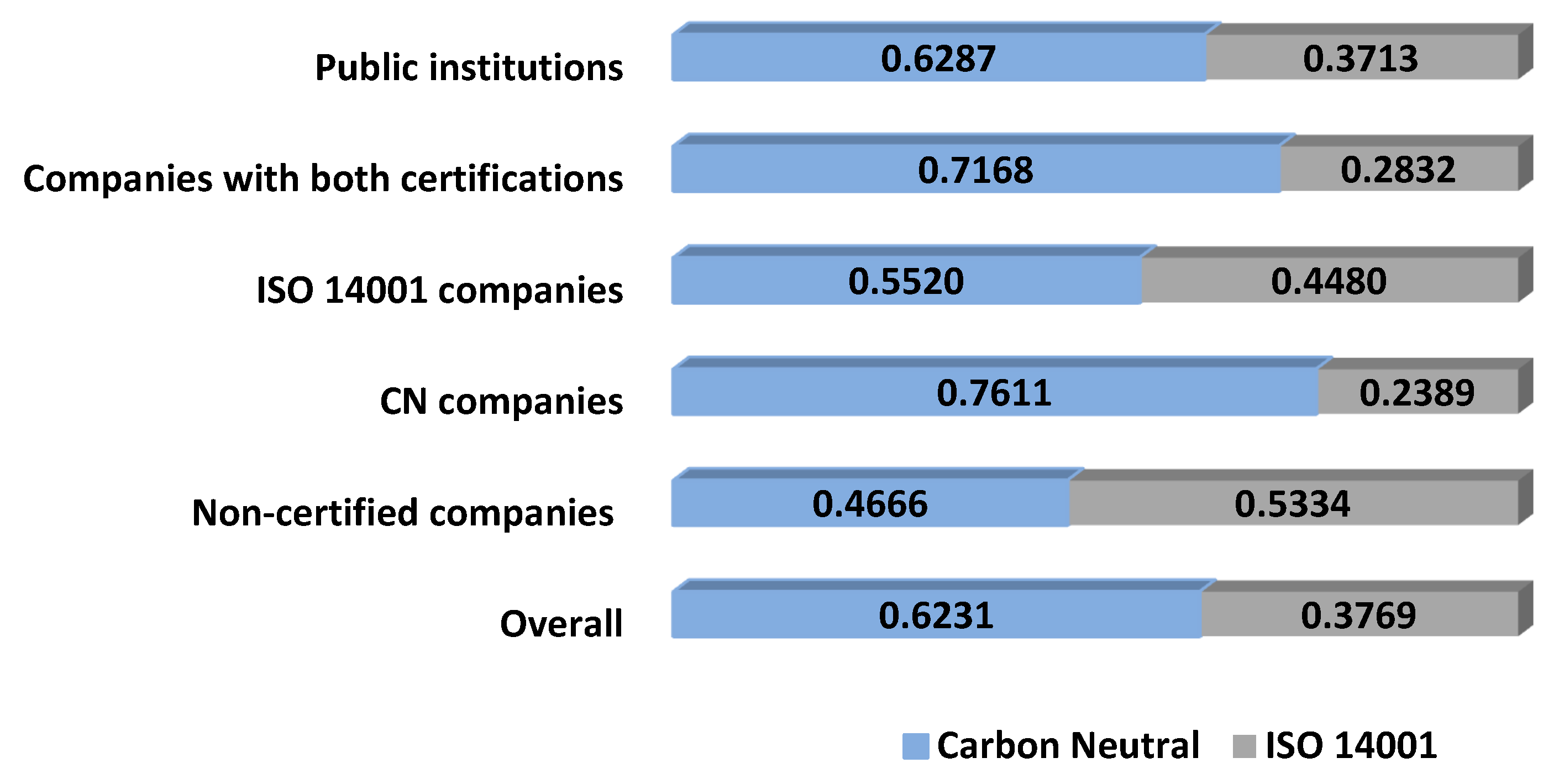

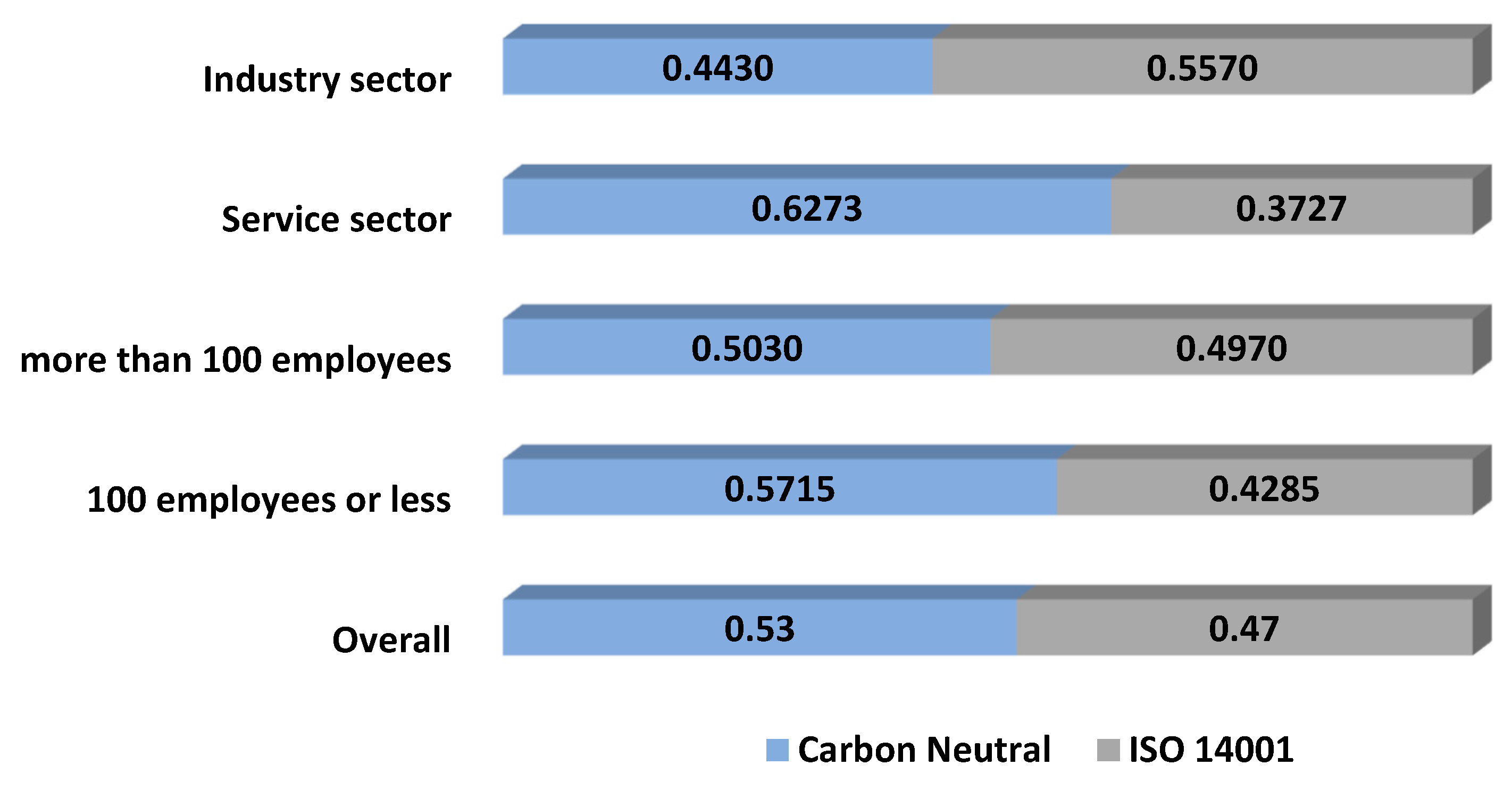

4.2. Differences Across Groups

- (i)

- Non-certified firms: Companies that are not CN nor ISO 14001 certified (n = 7),

- (ii)

- CN firms: Companies that are CN but not ISO 14001 certified (n = 4),

- (iii)

- ISO 14001 firms: Companies that are ISO 14001 but not CN certified (n = 4),

- (iv)

- Companies that are CN and ISO 14001 certified (n = 7),

- (v)

- Public institutions (n = 2), which include a university and a governmental department. Both are CN but not ISO 14001 certified.

4.2.1. Relative Importance of the Criteria and Sub-Criteria

4.2.2. Choosing a Certification

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Number of Interviewees * | Position | Activity | Environmental Certifications | Interview Day |

|---|---|---|---|---|

| 1 | MM | Industrial | CN, ISO 14001, EBF | 09/09/2016 |

| 2 | MM, EM | Financial | CN, ISO 14001 | 22/09/2016 |

| 2 | CSRC, EM | Car Sales | CN, ISO 14001 | 13/09/2016 |

| 1 | CSRC | Car Sales | CN, ISO 14001 | 16/08/2017 |

| 1 | MM | Industrial | ISO 14001 | 11/08/2017 |

| 1 | MM | Internal Audit | ISO 14001, EBF, OHAS 18000 | 17/08/2017 |

| 1 | MM | Financial | CN, ISO 14001 | 18/08/2017 |

| 1 | GM | Agricultural | Fairtrade, Eco-LOGICA, USDA organic | 22/08/2017 |

| 1 | GM | Travel agency | CST, CN, EBF | 23/08/2017 |

| Respondent Position | Activity | Size | Certifications | |

|---|---|---|---|---|

| CN | ISO 14001 | |||

| EM | Construction and building rental | L | Yes | Yes |

| EA | Energy | L | Yes | Yes |

| MM | Information and communication | L | Yes | Yes |

| MM | Pharmaceutical industry | L | Yes | Yes |

| EM | Finance | L | Yes | Yes |

| MM | Industrial | M | Yes | Yes |

| CSRC | Car Sales | L | Yes | Yes |

| MM | Education * | L | Yes | No |

| CSRC | Pension Fund Administration | L | Yes | No |

| Sub MM | Machinery sales | M | Yes | No |

| EM | Food Industry | M | Yes | No |

| HRM | Tourism Agency | M | Yes | No |

| EM | Government Department * | L | Yes | No |

| MM | Technology | L | No | Yes |

| EA | Food Industry | M | No | Yes |

| MMa | Industry | L | No | Yes |

| MM | Industry | M | No | Yes |

| GM | Food Industry | L | No | No |

| MMa | Consulting services | S | No | No |

| N.A. | Manufacture | M | No | No |

| MM | Commercialization | S | No | No |

| MM | Food Industry | M | No | No |

| GM | Food Industry | M | No | No |

| MM | Industry | L | No | No |

| Groups | Overall | Non-Certified Firms | CN Firms | ISO 14001 Firms | Firms with both Certifications | Public Institutions | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sub Criteria | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 |

| E1 | 0.5522 | 0.4478 | 0.5397 | 0.4603 | 0.6271 | 0.3729 | 0.5319 | 0.4681 | 0.4442 | 0.5558 | 0.8093 | 0.1907 |

| E2 | 0.3509 | 0.6491 | 0.3290 | 0.6710 | 0.5432 | 0.4568 | 0.4633 | 0.5367 | 0.2643 | 0.7357 | 0.2052 | 0.7948 |

| E3 | 0.4151 | 0.5849 | 0.2901 | 0.7099 | 0.5114 | 0.4886 | 0.3660 | 0.6340 | 0.5895 | 0.4105 | 0.2240 | 0.7760 |

| E4 | 0.5645 | 0.4355 | 0.5439 | 0.4561 | 0.5157 | 0.4843 | 0.4663 | 0.5337 | 0.5285 | 0.4715 | 0.7948 | 0.2052 |

| S1 | 0.5137 | 0.4863 | 0.4091 | 0.5909 | 0.7180 | 0.2820 | 0.3660 | 0.6340 | 0.5832 | 0.4168 | 0.5000 | 0.5000 |

| S2 | 0.7419 | 0.2581 | 0.6392 | 0.3608 | 0.7876 | 0.2124 | 0.7380 | 0.2620 | 0.7893 | 0.2107 | 0.7948 | 0.2052 |

References

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development. 2019. Available online: https://sustainabledevelopment.un.org/post2015/transformingourworld (accessed on 31 December 2019).

- Edenhofer, O. (Ed.) Climate Change 2014: Mitigation of Climate Change; Intergovernmental Panel on Climate; Change Contribution of Working Group III; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014; Available online: http://danida.vnu.edu.vn/cpis/files/IPCC/wg3/pdf/ipcc_wg3_ar5_frontmatter.pdf (accessed on 29 December 2019).

- Marseglia, G.; Medaglia, C.M.; Petrozzi, A.; Nicolini, A.; Cotana, F.; Sormani, F. Experimental tests and modeling on a combined heat and power biomass plant. Energies 2019, 12, 2615. [Google Scholar] [CrossRef]

- Manni, M.; Valentina, C.; Nicolini, A.; Marseglia, G.; Alessandro, P. Towards Zero Energy Stadiums: The Case Study of the Dacia Arena in Udine, Italy. Energies 2018, 11, 2396. [Google Scholar] [CrossRef]

- Shayegh, S.; Sanchez, D.L.; Caldeira, K. Evaluating relative benefits of different types of R&D for clean energy technologies. Energy Policy 2017, 107, 532–538. [Google Scholar] [CrossRef]

- Khanna, M. Non-mandatory approaches to environmental protection. J. Econ. Surv. 2001, 15, 291–324. [Google Scholar] [CrossRef]

- OECD. Voluntary Approaches for Environmental Policy: An Assessment, 1st ed.; Organisation for Economic Cooperation and Development Publishing: Paris, France, 2000. [Google Scholar]

- André, F.J. Strategic Behavior and the Porter Hypothesis. In The WSPC Reference on Natural Resource and Environmental Policy in the Era of Global Change; Dinar, A., Espinola-Arredondo, A., Munoz-Garcia, F., Eds.; World Scientific: Hackensack, NJ, USA, 2016; Volume 1, pp. 231–262. [Google Scholar]

- Ibanez, M.; Blackman, A. Is eco-certification a win–win for developing country agriculture? Organic coffee certification in Colombia. World Dev. 2016, 82, 14–27. [Google Scholar] [CrossRef]

- Porter, M.E.; Van der Linde, C.V.D. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. Available online: www.jstor.org/stable/2138392 (accessed on 11 November 2019). [CrossRef]

- Saaty, T.L. The Analytic Hierarchy Process: Planning Priority Setting and Resource Allocation; McGraw-Hill: New York, NY, USA, 1980. [Google Scholar]

- Chin, K.; Chiu, S.; Tummala, V.M.R. An evaluation of success factors using the AHP to implement ISO 14001-based EMS. Int. J. Qual. Reliab. Manag. 1999, 16, 341–362. [Google Scholar] [CrossRef]

- Pun, K.F.; Hui, I.K. An analytical hierarchy process assessment of the ISO 14001 environmental management system. Integr. Manuf. Syst. 2001, 12, 333–345. [Google Scholar] [CrossRef]

- Mathiyazhagan, M.; Diabat, A.; Al-Refaie, A.; Xu, L. Application of analytical hierarchy process to evaluate pressures to implement green supply chain management. J. Clean. Prod. 2015, 107, 229–236. [Google Scholar] [CrossRef]

- Shen, L.; Muduli, K.; Barve, A. Developing a sustainable development framework in the context of mining industries: AHP approach. Resour. Policy 2015, 46, 15–26. [Google Scholar] [CrossRef]

- Cuadrado, J.; Zubizarreta, M.; Rojí, E.; García, H.; Larrauri, M. Sustainability-related decision making in industrial buildings: An AHP analysis. Math. Probl. Eng. 2015, 1–13. [Google Scholar] [CrossRef]

- Ho, F.H.; Abdul-Rashid, S.H.; Raja Ghazilla, R.A. Analytic hierarchy process-based analysis to determine the barriers to implementing a material efficiency strategy: Electrical and electronics’ companies in the Malaysian context. Sustainability 2016, 8, 1035. [Google Scholar] [CrossRef]

- Thanki, S.; Govindan, K.; Thakkar, J. An investigation on lean-green implementation practices in Indian SMEs using analytical hierarchy process (AHP) approach. J. Clean. Prod. 2016, 135, 284–298. [Google Scholar] [CrossRef]

- Malik, M.M.; Abdallah, S.; Hussain, M. Assessing supplier environmental performance: Applying Analytical Hierarchical Process in the United Arab Emirates health care chain. Renew. Sustain. Energy Rev. 2016, 55, 1313–1321. [Google Scholar] [CrossRef]

- Wang, Q.; Han, R.; Huang, Q.; Hao, J.; Lv, N.; Li, T.; Tang, B. Research on energy conservation and emissions reduction based on AHP-fuzzy synthetic evaluation model: A case study of tobacco enterprises. J. Clean. Prod. 2018, 201, 88–97. [Google Scholar] [CrossRef]

- Karaman, A.S.; Akman, E. Taking-off corporate social responsibility programs: An AHP application in airline industry. J. Air Transp. Manag. 2018, 68, 187–197. [Google Scholar] [CrossRef]

- United Nations Environment Programme. Costa Rica Named ‘UN Champion of the Earth’ for Pioneering Role in Fighting Climate Change. 2019. Available online: https://www.unenvironment.org/news-and-stories/press-release/costa-rica-named-un-champion-earth-pioneering-role-fighting-climate (accessed on 14 November 2019).

- Birkenberg, A.; Birner, R. The world’s first carbon neutral coffee: Lessons on certification and innovation from a pioneer case in Costa Rica. J. Clean. Prod. 2018, 189, 485–501. [Google Scholar] [CrossRef]

- Blackman, A.; Naranjo, M.A.; Robalino, J.; Alpízar, F.; Rivera, J. Does tourism eco-certification pay? Costa Rica’s Blue Flag Program. World Dev. 2014, 58, 41–52. [Google Scholar] [CrossRef]

- Blum, N. Environmental education in Costa Rica: Building a framework for sustainable. Int. J. Educ. Dev. 2008, 28, 348–358. [Google Scholar] [CrossRef]

- Flagg, J.A. Carbon Neutral by 2021: The past and present of Costa Rica’s unusual political tradition. Sustainability 2018, 10, 296. [Google Scholar] [CrossRef]

- Rivera, J. Assessing a voluntary environmental initiative in the developing world: The Costa Rican Certification for Sustainable Tourism. Policy Sci. 2002, 35, 333–360. [Google Scholar] [CrossRef]

- Sánchez-Azofeifa, G.A.; Pfaff, A.; Robalino, J.A.; Boomhower, J.P. Costa Rica’s Payment for Environmental Services Program: Intention, implementation, and impact. Conserv. Biol. 2007, 21, 1165–1173. [Google Scholar] [CrossRef] [PubMed]

- Ministerio de Ambiente y Energía. Dirección de Cambio Climático [Climate Change Department]. Costa Rica: Ministerio de Amiente y Energía. 2018. Available online: https://cambioclimatico.go.cr/recursos/empresas-ppcn/ (accessed on 14 August 2019).

- Dirección de Cambio Climático. Guía Para Diseñar un Manual que Permita a las PYMES Realizar Declaraciones de Carbono Neutralidad Bajo la Norma INTE 12.01.06. [Guide to Design a Manual that Allows SMEs to Make Carbon Emissions Declarations Under the INTE 12.01.06 Standard]. Costa Rica. 2014. Available online: http://www.digeca.go.cr/sites/default/files/documentos/manualcarbononeutral-web.pdf (accessed on 28 October 2019).

- Musmanni, S. Implementación de la estrategia de Carbono-Neutralidad como modelo de desarrollo bajo en emisiones en Costa Rica [Implementation of the Carbon-Neutrality strategy as a low-emission development model in Costa Rica]. Ambientico 2014, 247, 4–9. Available online: http://www.ambientico.una.ac.cr/pdfs/ambientico/247.pdf (accessed on 12 August 2018).

- Valenciano-Salazar, J.A. Reducción de gases de efecto invernadero: Algunos desafíos para Costa Rica [Greenhouse gas reduction: Some challenges for Costa Rica]. Ambientico 2016, 258, 76–81. Available online: http://www.ambientico.una.ac.cr/pdfs/art/ambientico/258-76-81.pdf (accessed on 2 January 2020).

- International Organization for Standardization. ISO Survey of Certifications to Management System Standards. 2019. Available online: https://isotc.iso.org/livelink/livelink?func=ll&objId=20719433&objAction=browse&viewType=1 (accessed on 2 April 2019).

- International Organization for Standardization. Introduction to ISO 14001:2015. Geneva, Switzerland. 2015. Available online: https://www.iso.org/files/live/sites/isoorg/files/archive/pdf/en/introduction_to_iso_14001.pdf (accessed on 9 August 2019).

- Abdul Rashid, S. An Investigation into the Material Efficiency Practices of UK Manufacturers. Ph.D. Thesis, Cranfield University, Cranfield, UK, October 2009. Available online: http://hdl.handle.net/1826/4477 (accessed on 28 October 2019).

- Verschoor, A.H.; Reijnders, L. Toxics reduction in ten large companies, why and how. J. Clean. Prod. 2000, 8, 69–78. [Google Scholar] [CrossRef]

- Doczy, R.; AbdelRazig, Y. Green buildings case study analysis using AHP and MAUT. J. Arch. Eng. 2017, 23. [Google Scholar] [CrossRef]

- Eltayeb, T.K.; Zailani, S.; Ramayah, T. Green supply chain initiatives among certified companies in Malaysia and environmental sustainability: Investigating the outcomes. Resour. Conserv. Recycl. 2011, 55, 495–506. [Google Scholar] [CrossRef]

- Govindan, K.; Rajendran, S.; Sarkis, J.; Murugesan, P. Multi criteria decision making approaches for green supplier evaluation and selection: A literature review. J. Clean. Prod. 2015, 98, 66–83. [Google Scholar] [CrossRef]

- Faggi, A.M.; Zuleta, G.A.; Homberg, M. Motivations for implementing voluntary environmental actions in Argentine forest companies. Land Use Policy 2014, 41, 541–549. [Google Scholar] [CrossRef]

- Hillary, R. Environmental management systems and the smaller enterprise. J. Clean. Prod. 2004, 12, 561–569. [Google Scholar] [CrossRef]

- Mariotti, F.; Kadasah, N.; Abdulghaffar, N. Motivations and barriers affecting the implementation of ISO 14001 in Saudi Arabia: An empirical investigation. Total Qual. Manag. Bus. Excell. 2014, 25, 1352–1364. [Google Scholar] [CrossRef]

- Morrow, D.; Rondinelli, D. Adopting corporate environmental management systems: Motivations and results of ISO 14001 and EMAS certification. Eur. Manag. J. 2002, 20, 159–171. [Google Scholar] [CrossRef]

- Okereke, C. An exploration of motivations, drivers and barriers to carbon management: The UK FTSE 100. Eur. Manag. J. 2007, 25, 475–486. [Google Scholar] [CrossRef]

- Ormazabal, M.; Sarriegi, J.M. Environmental management evolution: Empirical evidence from Spain and Italy. Bus. Strateg. Environ. 2014, 23, 73–88. [Google Scholar] [CrossRef]

- Pérez-Ramírez, M.; Phillips, B.; Lluch-Belda, D.; Lluch-Cota, S. Perspectives for implementing fisheries certification in developing countries. Mar. Policy 2012, 36, 297–302. [Google Scholar] [CrossRef]

- Schylander, E.; Martinuzzi, A. ISO 14001–experiences, effects and future challenges: A national study in Austria. Bus. Strateg. Environ. 2007, 16, 133–147. [Google Scholar] [CrossRef]

- Yiridoe, E.K.; Clark, J.S.; Marett, G.E.; Gordon, R.; Duinker, P. ISO 14001 EMS standard registration decisions among Canadian organizations. Agribusiness 2003, 19, 439–457. [Google Scholar] [CrossRef]

- Zeng, S.X.; Tam, C.M.; Tam, V.; Deng, Z.M. Towards implementation of ISO 14001 environmental management systems in selected industries in China. J. Clean. Prod. 2005, 13, 645–656. [Google Scholar] [CrossRef]

- Zeppel, H.; Beaumont, N. Assessing motivations for carbon offsetting by environmentally certified tourism enterprises. Anatolia 2013, 24, 297–318. [Google Scholar] [CrossRef]

- Bansal, P.; Bogner, W.C. Deciding on ISO 14001: Economics, institutions, and context. Long Range Plan. 2002, 35, 269–290. [Google Scholar] [CrossRef]

- Barham, B.L.; Callenes, M.; Gitter, J.; Lewis, J.; Weber, J. Fair Trade/Organic coffee, rural livelihoods, and the “agrarian question”: Southern Mexican coffee families in transition. World Dev. 2011, 39, 134–145. [Google Scholar] [CrossRef]

- Lyngbæk, A.E.; Muschler, R.G.; Sinclair, F.L. Productivity and profitability of multistrata organic versus conventional coffee farms in Costa Rica. Agrofor. Syst. 2001, 53, 205–213. [Google Scholar] [CrossRef]

- Méndez, V.E.; Bacon, C.M.; Olson, M.; Petchers, S.; Herrador, D.; Carranza, C.; Trujillo, L.; Guadarrama-Zugasti, C.; Cordón, A.; Mendoza, A. Effects of Fair Trade and organic certifications on small-scale coffee farmer households in Central America and Mexico. Renew. Agric. Food Syst. 2010, 25, 236–251. [Google Scholar] [CrossRef]

- Pan, J.-N. A comparative study on motivation for and experience with ISO 9000 and ISO 14000 certification among Far Eastern countries. Ind. Manag. Data Syst. 2003, 103, 564–578. [Google Scholar] [CrossRef]

- Weber, J.G. How much more do growers receive for Fair Trade-organic coffee? Food Policy 2011, 36, 678–685. [Google Scholar] [CrossRef]

- Fryxell, G.E.; Szeto, A. The influence of motivations for seeking ISO 14001 certification: An empirical study of ISO 14001 certified facilities in Hong Kong. J. Environ. Manag. 2002, 65, 223–238. [Google Scholar] [CrossRef]

- González-Benito, J.; Gonzáles-Benito, O. An analysis of the relationship between environmental motivations and ISO14001 certification. Br. J. Manag. 2005, 16, 133–148. [Google Scholar] [CrossRef]

- Lim, S.; Prakash, A. Voluntary regulations and innovation: The case of ISO 14001. Public Adm. Rev. 2014, 74, 233–244. [Google Scholar] [CrossRef]

- Quazi, H.A.; Khoo, Y.K.; Tan, C.M.; Wong, P.S. Motivation for ISO 14000 certification: Development of a predictive model. Omega 2001, 29, 525–542. [Google Scholar] [CrossRef]

- Poksinska, B.; Dahlgaard, J.J.; Eklund, J.A.E. Implementing ISO 14000 in Sweden: Motives, benefits and comparisons with ISO 9000. Int. J. Qual. Reliab. Manag. 2003, 20, 585–606. [Google Scholar] [CrossRef]

- Babakri, K.; Bennett, R.; Franchetti, M. Critical factors for implementing ISO 14001 standard in United States industrial companies. J. Clean. Prod. 2003, 11, 749–752. [Google Scholar] [CrossRef]

- Santos, G.; Rebelo, M.; Lopes, N.; Alves, M.R.; Silva, R. Implementing and certifying ISO 14001 in Portugal: Motives, difficulties and benefits after ISO 9001 certification. Total Qual. Manag. Bus. Excell. 2016, 27, 1211–1223. [Google Scholar] [CrossRef]

- Snider, A.; Gutiérrez, I.; Sibelet, N.; Faure, G. Small farmer cooperatives and voluntary coffee certifications:Rewarding progressive farmers of engendering widespread change in Costa Rica. Food Policy 2017, 69, 231–242. [Google Scholar] [CrossRef]

- Tellman, B.; Gray, L.C.; Bacon, C.M. Not fair enough: Historic and institutional barriers to Fair Trade coffee in El Salvador. J. Lat. Am. Geogr. 2011, 10, 107–127. [Google Scholar] [CrossRef]

- INTECO. Instituto de Normas Técnicas de Costa Rica [Institute of Technical Standards of Costa Rica]. 2019. Available online: https://www.inteco.org/ (accessed on 11 October 2019).

- Saaty, T. Decision Making for Leaders: The Analytical Hierarchy Process for Decisions in a Complex World, 3rd ed.; RWS Publications: Pittsburg, PA, USA, 2012. [Google Scholar]

- Aczél, J.; Alsina, C. On synthesis of judgements. Socio Econ. Plan. Sci. 1986, 20, 333–339. [Google Scholar] [CrossRef]

- Xu, Z. On consistency of the weighted geometric mean complex judgement matrix in AHP. Eur. J. Oper. Res. 2000, 126, 683–687. [Google Scholar] [CrossRef]

- Perron, O. Zur Theorie der Matrices. Math. Ann. 1907, 64, 248–263. [Google Scholar] [CrossRef]

- Aznar Bellver, J.; Caballer Mellado, V. An application of the analytic hierarchy process method in farmland appraisal. Span. J. Agric. Res. 2005, 3, 17–24. Available online: http://revistas.inia.es/index.php/sjar/article/view/120/117 (accessed on 14 November 2019). [CrossRef]

- Vázquez-Burgos, J.L.; Carbajal-Hernández, J.J.; Sánchez-Fernández, L.P.; Moreno-Armendáriz, M.A.; Tello-Ballinas, J.A.; Hernández-Bautista, I. An Analytical Hierarchy Process to manage water quality in white fish (Chirostoma estor estor) intensive culture. Comput. Electron. Agric. 2019, 167, 105071. [Google Scholar] [CrossRef]

- Cater, J.; Collins, L.A.; Beal, B.D. Ethics, faith, and profit: Exploring the motives of the U.S. Fair Trade social entrepreneurs. J. Bus. Ethics 2017, 146, 185–201. [Google Scholar] [CrossRef]

- Muñoz, A. El Presupuesto Nacional en Costa Rica [The National Budget in Costa Rica]. Ministerio de Hacienda de Costa Rica, Cooperación Alemana, FOCEVAL. Available online: https://www.hacienda.go.cr/docs/5228c0e0637a1_Folleto_Presupuesto_Nacional.pdf (accessed on 11 December 2019).

| Economic-Strategic (E) | Environmental Sustainability (S) |

|---|---|

| Improving green image, public visibility and social legitimacy of the company (E1). Increasing sales, market shares or prices (E2) * Saving production costs or increasing productivity (E3). Cost of the certification and investment in clean technologies (E4). | Materials and energy use reductions during the production and distribution (S1). Reduction in the amount and damage of emissions (gas, solid and water) generated by the company (S2). |

| Note: * Since public institutions do not have a profit motive, we reformulate sub-criterion E2 for them as “the possible improvements in the quality of the services offered and the increase in user satisfaction.” | |

| Numerical Values | Definition | Explanation |

|---|---|---|

| 1 | Equal | Two elements contribute equally to the objective |

| 3 | Moderate | Experience and judgment slightly favor one aspect over another |

| 5 | Strongly | Experience and judgment strongly or essentially favor one aspect over another |

| 7 | Very strongly | An aspect is strongly favored over another and its dominance demonstrated in practice |

| 9 | Extremely | The evidence favoring one aspect over another is of the highest degree possible for affirmation |

| 2, 4, 6, 8 | Intermediate values | Used to represent a compromise between preferences listed above |

| Criteria | Vc | Sub-Criteria | VEC and VSC | VGEC and VGSC | Comparing Alternatives (VAi) | |

|---|---|---|---|---|---|---|

| ISO 14001 | CN | |||||

| Economics-strategic (Ei) | we 0.6001 | E1 | 0.2911 | 0.1747 | 0.4478 | 0.5522 |

| E2 | 0.2292 | 0.1376 | 0.6491 | 0.3501 | ||

| E3 | 0.2950 | 0.1770 | 0.5849 | 0.4151 | ||

| E4 | 0.1847 | 0.1108 | 0.4355 | 0.5645 | ||

| Environmental sustainability (Si) | ws 0.3999 | S1 | 0.5207 | 0.2082 | 0.4863 | 0.5137 |

| S2 | 0.4793 | 0.1917 | 0.2581 | 0.7419 | ||

| Alternatives | According to Each Criterion | According to Global Weights | |||

|---|---|---|---|---|---|

| WAE | WAS | VGEC × VAE | VGSC × VAS | WGA | |

| CN | 0.4679 | 0.6231 | 0.2808 | 0.2492 | 0.5300 |

| ISO 14001 | 0.5321 | 0.3769 | 0.3193 | 0.1507 | 0.4700 |

| Total | 1 | 1 | 0.6001 | 0.3999 | 1 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

André, F.J.; Valenciano-Salazar, J.A. Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach. Sustainability 2020, 12, 737. https://doi.org/10.3390/su12020737

André FJ, Valenciano-Salazar JA. Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach. Sustainability. 2020; 12(2):737. https://doi.org/10.3390/su12020737

Chicago/Turabian StyleAndré, Francisco J., and Jorge A. Valenciano-Salazar. 2020. "Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach" Sustainability 12, no. 2: 737. https://doi.org/10.3390/su12020737

APA StyleAndré, F. J., & Valenciano-Salazar, J. A. (2020). Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach. Sustainability, 12(2), 737. https://doi.org/10.3390/su12020737