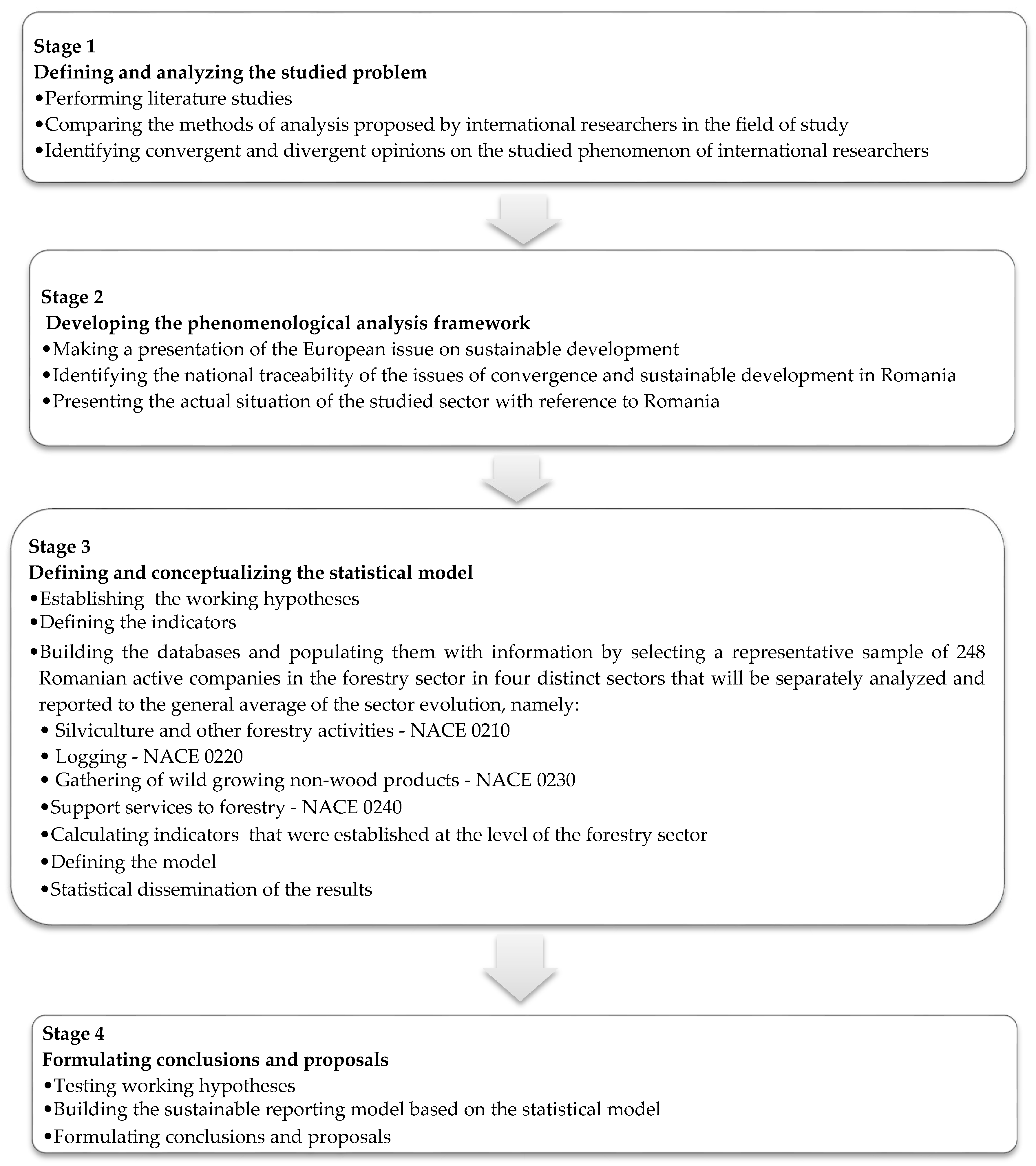

3.2. Measures

Indicators taken into account in order to establish the vulnerability of the sector or risk area from the point of view of sustainable development were based on accounting data and information provided by the financial reporting. For each of them, financial data regarding the values of the patrimonial fixed asset capitalization, the liquidity rate, the sustainable growth rate, the profitability of workforce use, the profitability rate, the risk of insolvency at 31 December were manually collected from the annual reports of the firms included in the sample. From all of the CSR indicators identified in the specialty literature, we found in the annual reports of unlisted firms, far too little information (incomplete information on the amounts spent) on health and safety costs at the workplace [

70,

71], corporate giving, waste management expenses [

72,

73], and employee training courses expenses [

70,

71,

74]. Of all the categories of indicators listed above, the only category where we found indicated amounts spent (measured as a percentage of turnover) was corporate giving [

75,

76,

77].

Studying the specialized literature, we could state that over time CSR has been correlated with different concepts, such as CFP, profit, labor turnover, sustainable development, financial performance, but neither of these studies has addressed the problem of conceptualizing an econometric model of estimating the risk/vulnerability of the sustainable development based on the general coefficient of vulnerability of the sector (GCVs). Even though CSR was analyzed, taking into account one or more financial indicators that we proposed as variables in our study, most recent studies set different aims in relation to the aims of the present study. In the following, we proceeded to analyze the recent specialized literature that had, like its topic, the study of CSR in correlation with different financial indicators used in this study in order to construct the econometric model. Thus, taking into account the variable fixed asset capitalization, various studies attempted to examine the relationship between CSR and CFP [

15,

78], with corporate political activity (CPA) serving as the moderator [

16], or correlation between CSR and profit [

79]. In the study undertaken by Dam and Scholtens [

80], the variable liquidity rate was used to investigate “how ownership concentration in European multinational firms is associated with these firms’ CSR”. The variable rate of sustainable growth has been used in numerous studies to investigate “the effect of CSR on information asymmetry between firms and creditors” [

81] and to examine the relationship between CSR and CFP [

16], as well as in the relationship between CSR and financial performance [

81]. Profitability of using workforce is one of the variables often used in studies to “investigate the relationship between the budget related to CSR, innovation, and training, defined as sustainable factors, and the financial results of small and medium-sized enterprises (SMEs)” [

19], to examine the correlation between CSR and financial performance, to examine the relationship between CFP and CSR, as well as the relationship between corporate social responsibility activities (CSRA) and human capital (HC) and the relationship between HC and CFP [

82]. To examine the relationship between CSR and CFP, Lin et al. [

16] used the variable profitability rate. The variable insolvency risk was used by Yang, Bento, and Akbar [2019] to investigate whether CSR efforts enhance firm performance.

The following indicators are control variables included in the analysis to control the reliability of the model and reduce the risk of biases in order to achieve a sustainable reporting model.

The patrimonial fixed asset capitalization (PFAC)

where:

PFAC—the patrimonial fixed asset capitalization;

FA—the value of fixed assets financially reported;

E—the amount of financially reported equity.

The indicator reflects the ability of the entities in a given sector to keep and develop, through the capitalization phenomenon, those fixed assets held at a given point in time in order to eliminate the influence of obsolescence through asset increases and periodical upgrades.

The over-unitary value of the indicator reveals a high degree of use of capital that was attracted to the detriment of the invested capital, while a negative value of the indicator reflects the failure of management policy, including the field of sustainable development.

The average value of the indicator assimilated to the statistical optimum for an analyzed sector is estimated by using the formula:

The sectorial dynamics of the indicator expressed on the basis of the average of the absolute weights of evolution in a relevant historical period is estimated by using the formula:

The sectorial analysis of the forestry sector indicator and the four domains based on the NACE (Statistical classification of economic activities in the European Community) classification of the fields of activity were generated by the following results for a sample of 248 selected entities that were analyzed over a representative reference period of 10 years (see

Table 1).

The values in

Table 1 indicated the compliance with the sustainable development strategy of the indicators achieved by the companies that had NACE 0240 as their main field of activity, while, at the opposite pole, the companies with high vulnerability towards sustainable development activated on the NACE 0220 field and NACE 0230, respectively. For the latter, there was a sub-unitary dynamic of the evolution of the indicator, making the allocation of the vulnerability coefficients difficult to be made.

● The liquidity rate (LR)

where:

The indicator reflects the degree of financial independence of the entities and the readiness to immediately access their funds in order to achieve sustainable development strategies.

The over-unitary value of the indicator reveals a high degree of financial independence as the overall average for the forestry sector is 41.58 units, mainly due to the forest resource holdings. At the same time, the accelerated diminution of the indicator may suggest the phenomenon of illegal cuts. The sub-unitary value of the indicator indicates high vulnerability and economic blockage risk. Forest fund growth efforts can be estimated based on this indicator only if the sectorial dynamics of the indicator expressed, based on the average of absolute weights of evolution in a relevant historical period, is over-unitary.

The average value of the indicator assimilated to the statistical optimum for an analyzed sector is calculated using the formula:

The sectorial dynamics of the indicator expressed on the basis of the average of absolute evolution weights in a relevant historical period is estimated by using the formula:

The sectorial analysis of the forestry sector indicator and the four branches according to the NACE classification of the fields of activity (i.e., 4 fields) generated the following results for the sample of 248 selected companies and analyzed over a representative 10 years reference period:

The values shown in

Table 2 indicated the compliance with the sustainable development strategy of the indicators achieved by the companies that had NACE 0240 as their main field of activity, while, at the opposite pole, the companies with high vulnerability having NACE 0230 and NACE 0220 as their main activity field. For the latter, there was a sub-unitary dynamics of the evolution of the indicator.

● The sustainable growth rate (SGR)

where:

SGR—the sustainable growth rate;

T—the amount of financially reported turnover;

E—the amount of financially reported equity.

The indicator reflects the ability of a business to sustainably grow the surplus of operating income (expressed through turnover), when compared to the entity’s equity, in a sector of activity, which is surprising in dynamics.

The over-unitary value of the indicator reveals a sustainable growth of the business if and only if the sectorial dynamics of the indicator expressed because of the average of the absolute evolution weights in a relevant historical period is over-unitary. The sub-unitary value of the indicator reflects vulnerability in the field of sustainable growth, whereas the negative value of the analyzed indicator indicates the risks of the business. The risk increases progressively as the negative value increases.

The average value of the indicator assimilated to the statistical optimum for an analyzed sector is estimated by using the formula:

The sectorial dynamics of the indicator based on the average of absolute evolution weights in a relevant historical period is estimated by using the formula:

The sectorial analysis of the forestry sector indicator and the four branches according to the NACE classification of the fields of activity (4 fields) generated the following results for the sample of 248 companies selected and analyzed over a representative reference period of 10 years:

The values in

Table 3 indicated the compliance with the sustainable development strategy of the indicators realized by the companies that had NACE 0220 as their main activity field, while, at the opposite pole, the companies with high vulnerability towards the sustainable development were represented by NACE 0230.

● The profitability of using workforce (PUW)

where:

PUW—the profitability of using workforce;

NP—the value of the financially reported net profit;

NE—the number of employees.

The sectorial analysis of the forestry sector indicator and the four branches according to the NACE classification of the fields of activity (four fields) for a sample of 248 selected companies whose indicators were analyzed over a representative reference period of ten years generated the following results:

As we might notice, the values presented in the above

Table 4 indicated the convergence with the sustainable development strategy of companies operating in the field of forest exploitation (NACE 0220), while, at the opposite end, there were companies operating in the field of activity (NACE 0230, NACE 0240), where negative values of the average of the indicator were recorded.

● The profitability rate (PR)

where:

PR—the profitability rate;

NP—the value of the financially reported net profit;

T—the amount of financial reported turnover.

The profitability rates are defined in terms of statistical optimum as sub-unit and positive. Their value for sustainable development has to reach at least 15%. The positive values under the statistical optimum indicate certain vulnerabilities in regards to sustainable business management as well as certain negative values that indicate major risks related to the business management and administration.

As the study revealed, as far as the Romanian forestry sector is concerned, the overall average was sub-unitary. This fact reflects that the units, especially the autonomous governments, lack the managerial capacity for sustainable business management.

The average value of the indicator assimilated to the statistical optimum for an analyzed sector was estimated by using the formula:

The sectorial dynamics of the indicator expressed because of the average of absolute evolution weights in a relevant historical period was estimated by using the formula:

In terms of the sectorial analysis of the forestry sector indicator, as well as the four branches based on the NACE classification of the fields of activity (4 fields) for the same sample of 248 selected companies whose indicators were analyzed over a representative reference period of ten years, the following results were obtained:

As could be seen, the values presented in the above

Table 5 indicated compliance with the sustainable development strategy of the companies that had NACE 0210 as their field of activity. All other branches, as well as the general indicator belonging to the level of the forestry sector, indicated the noncompliance with the sustainable development of these companies.

● The risk of insolvency (RI)

where:

As far as Romania is concerned, the bankruptcy risk has been a major area of interest, especially during the economic crisis during which the phenomenon took place at a high level throughout the Romanian economy. The proposed indicator is relevant in relation to sustainable development as the emergence of bankruptcy risk is a clear signal that sustainable development cannot take place for a particular entity or sector. The amount of the debts accumulated by the entity may represent up to one point the interest of the strategic development managers of the company only when their increase is directly related to the increase in equity. Otherwise, the accumulation of debts is likely to stop the sustainable development, especially if the full coverage of these debts would require the results of more than two consecutive financial exercises (i.e., 700 days).

The statistical optimum of the insolvency risk indicator estimated for the forest sector in Romania was 1.14. This means that for the forest sector, the average period of payment of the total liabilities is of 416 days.

The recording of a value below this optimum reflected the good exercise of capacity and the absence of the insolvency risk. The exceeding of the sectorial dynamics of the indicator that was expressed based on the average of absolute evolution weight during a relevant historical period reflected a vulnerability in terms of the insolvency risk. At the same time, the exceeding of the unit value 2 of the indicator reflected the manifestation of imminent insolvency risk for the analyzed sector.

The average value of the indicator assimilated to the statistical optimum for an analyzed sector was estimated by using the formula:

The sectorial dynamics of the indicator expressed due to the average of absolute evolution weight in a relevant historical period was estimated by using the formula:

The sectorial analysis of the insolvency risk indicator in the forestry sector and the four branches based on the NACE classification of the fields of activity for a sample of 248 selected companies that were analyzed over a representative reference of ten years generated the following results:

Similar to the previous situations, the values registered in terms of the insolvency risk indicator suggested a compliance with the sustainable development strategy of those companies operating in the NACE 0210 field, as well as the NACE 0220, respectively, while, at the opposite end, there were those companies in the field of NACE 0240 (

Table 6).

The following indicators were control variables included in the analysis to control the reliability of the model and reduce the risk of biases.

The following working hypotheses were formulated in order to achieve the proposed objective:

On a sectorial level, the patrimonial capitalization of fixed assets is a vulnerability that can affect sustainable development only when the sector evolution average of the indicator is below the overall average of the evolution on the forestry segment.

The liquidity rate of the entities operating in the forest segment affects and indicates the vulnerability of the sustainable development only when the average value of the sectorial calculated indicator exceeds a standard deviation (+/−) of 50%, whereas there is a sub-unitary evolution of the trend.

The sustainable growth rate that is calculated as a ratio between turnover and equity indicates a development vulnerability only when the overall dynamics of the indicator in a relevant reference period (of at least 10 years) is sub-unitary or when the indicator registers more than 3 negative values during the reference period.

Productivity represents a direct vulnerability and risk measurement indicator. The values exceeding with a standard deviation (+/−) of 50% the statistical optimum are represented by the general average of the forestry sector calculated in dynamics during a specific period (of at least 10 years) and are considered an indicator of high vulnerability. Consequently, if the negative values of profitability from the use of the workforce regardless of their values occur more than 3 times in the reference range, then this fact is an indication of the manifestation of the same systemic risk of the sustainable development vulnerability.

The risk of insolvency, given by the ratio between total debts and the turnover, exceeding the value of the statistical optimum calculated for the forest sector at 1.14 indicates an intrinsic vulnerability by de-capitalizing the companies in the analyzed segment and, implicitly, through their incapacity to ensure economic performance and sustainable development.

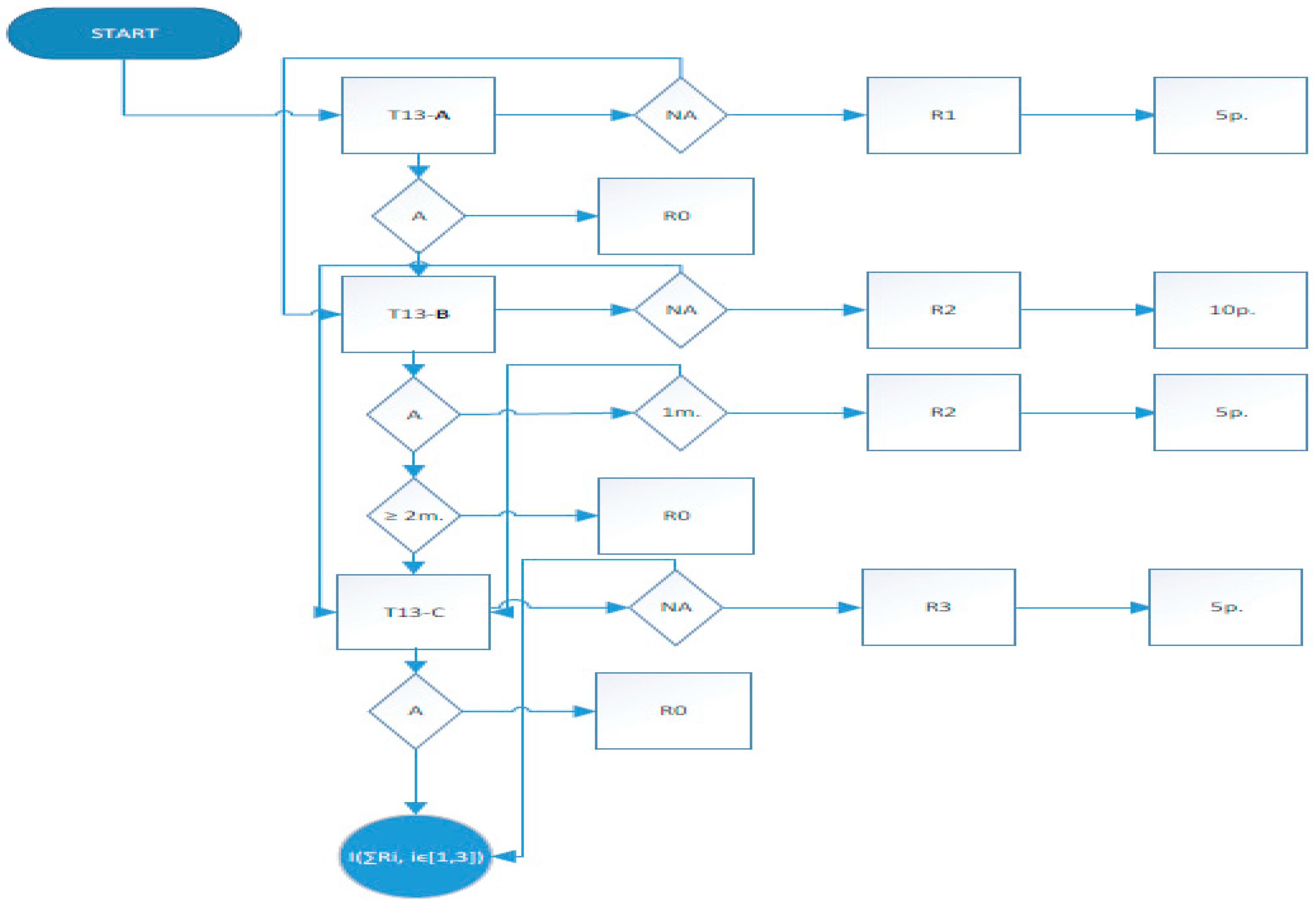

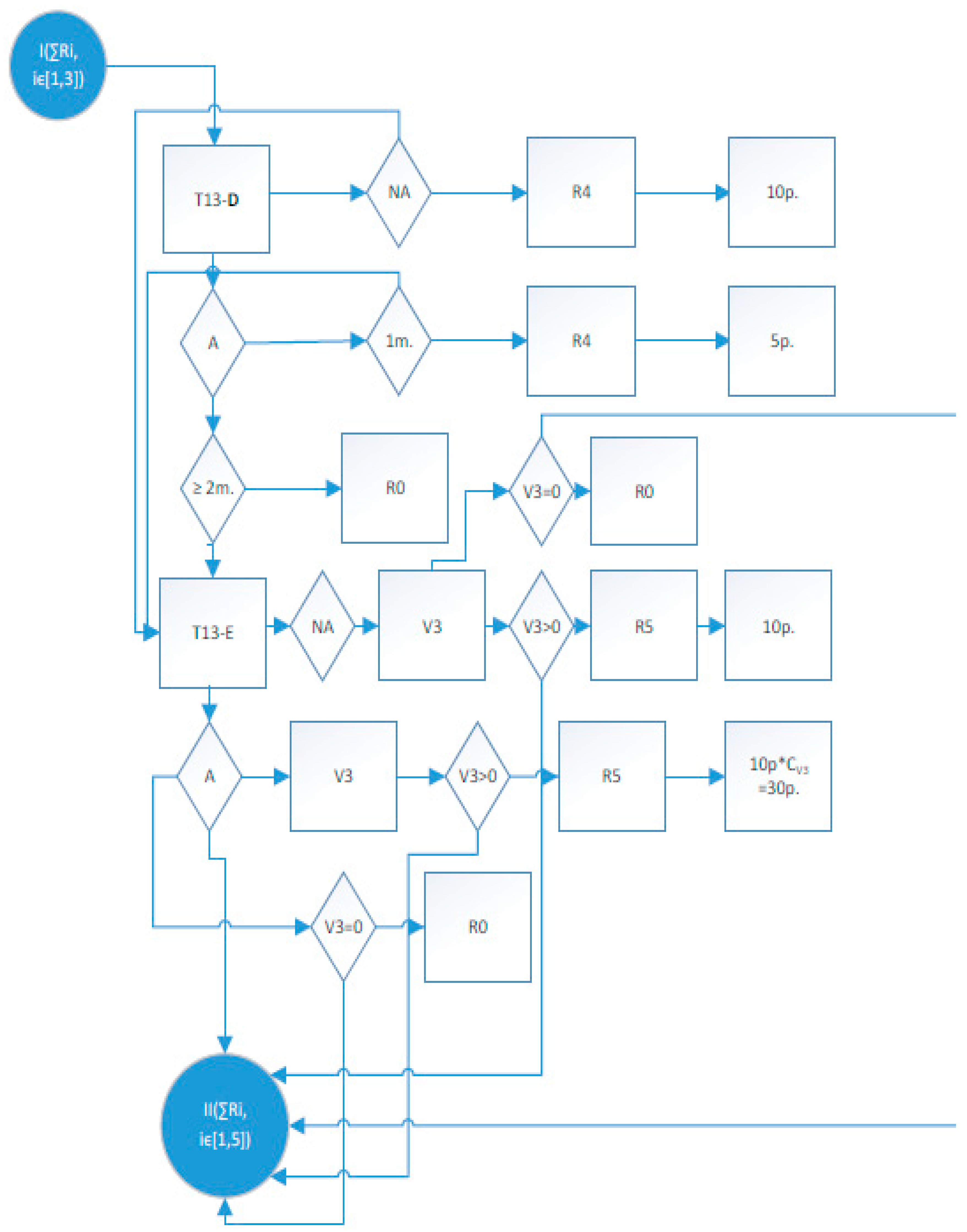

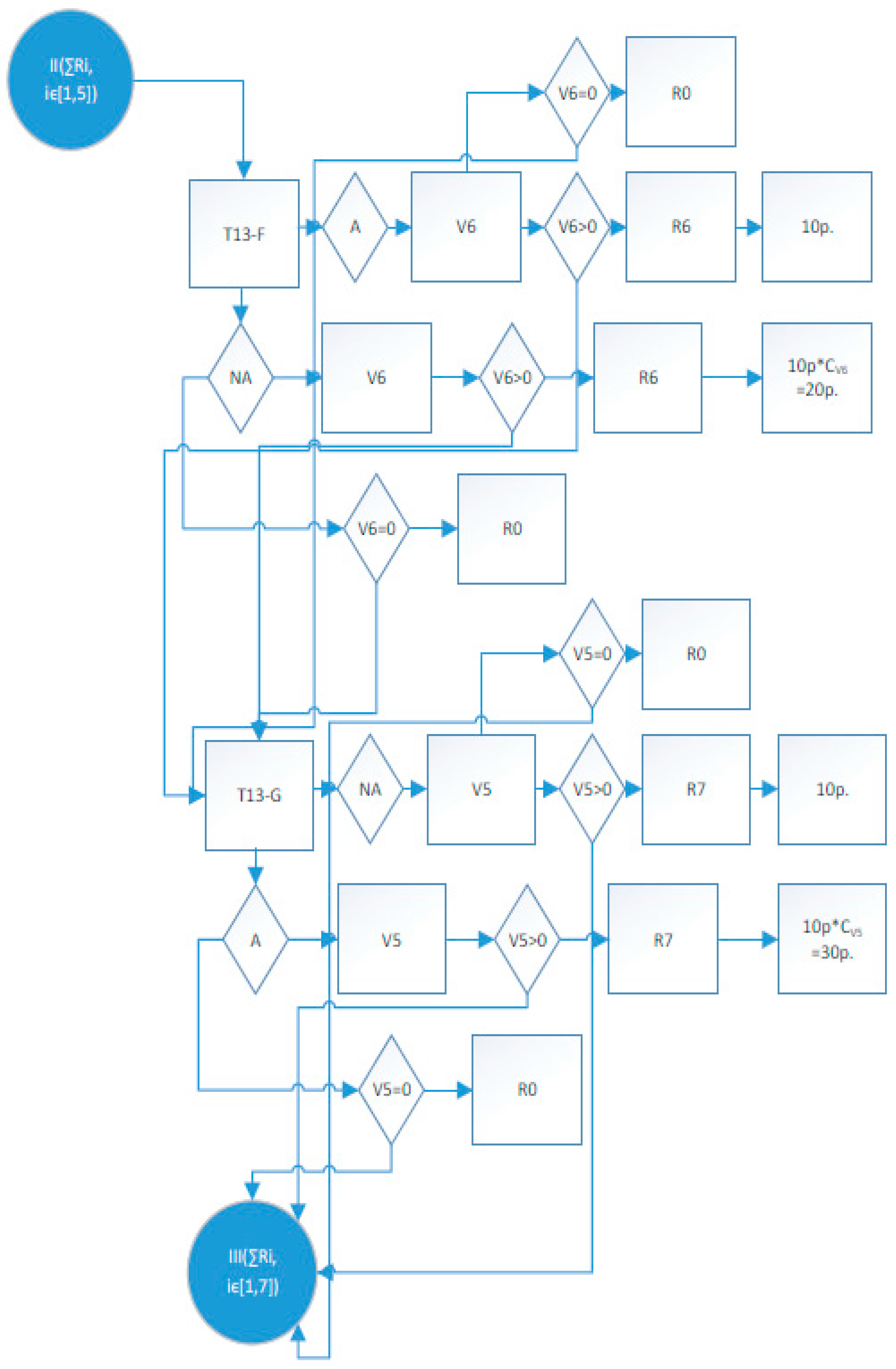

The risk chart, based on such indicators as the patrimonial fixed asset capitalization, the liquidity rate, the sustainable growth rate, the profitability of workforce use, the profitability rate, the risk of insolvency, can be built based on the historical data. It practically ensures the control levers of voluntary disclosure of managers regarding the sustainability report suggested to be implemented.

The reliability of using the sustainable reporting model is based on the model facility for managers and its ability to be confirmed by computing the reported financial information over a relevant historical period of at least 10 years.

The projection of a non-financial performance-reporting model for the microenterprises operating in the field of forest holdings and districts involved the estimation of the sectorial vulnerabilities, as shown in

Table 7.

The presence of the vulnerabilities was coated as Vi > 0, while their absence was coated as Vi = 0.

The information that results from every section of the nonfinancial reports was quantified in a qualitative manner in order to trace out the positive aspects (i.e., the absence of the risk, R

0) or the presence of the risk (R

i). For each R

i ≠ R

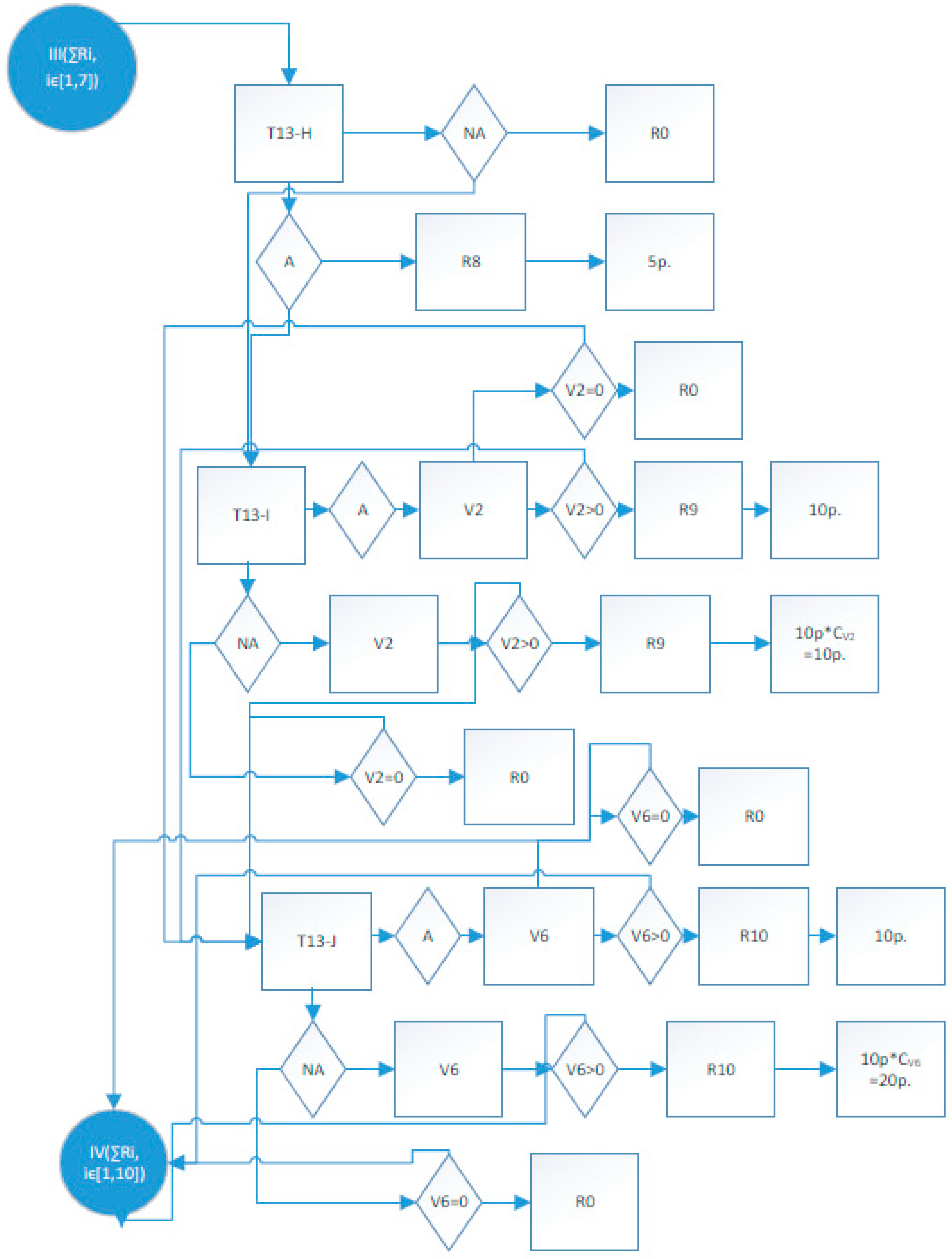

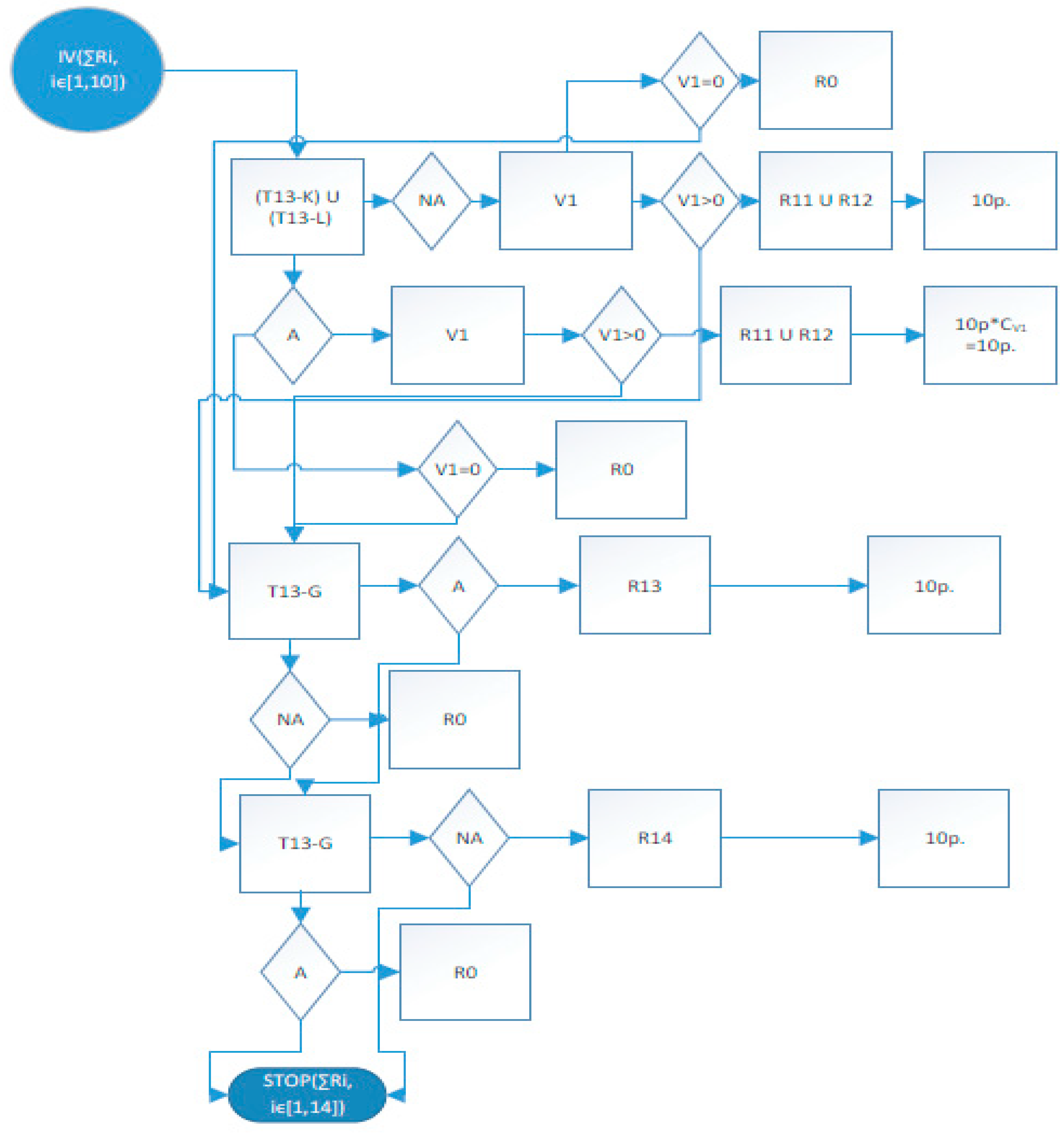

0, the risk level was quantified with a multiple of 5 points based on the risk level. The flowchart of risks, which could be transposed (depending on the authorities’ needs) on the software analysis, is presented step by step (Step 1—

Figure A1, Step 2—

Figure A2, Step 3—

Figure A3, Step 4—

Figure A4, Step 5—

Figure A5). The steps presented in the diagrams

Figure A1–A5 could be interpreted after quantifying each risk in a set of measures taken by the authorities, depending on the difference between the total level of risk and the minimum level of risk and a majority fixed on the basis of the legislative norms. These measures should lead to a high level of development of the sustainability of each entity included in the process.

The data interpretation was as follows:

| - —indicator number | - —allowed; |

| - —risks; | - —not allowed; |

| - —absence of the risk; | - —coefficient of vulnerability; |

| - T13-A up to T13-N—indicators of nonfinancial reporting; |

The sustainable reporting model of non-financial information devised by the authors should include at least the non-financial information presented from T13-A up to T13-N.

Your company has implemented an assimilation program of sustainable development principles comprised in the National Strategy of Sustainable Development (T13-A);

Have you taken measures within the company related to environmental protection? If yes, specify clearly these measures in the observations’ section (T13-B);

Do the organization and the functioning regulation comprise certain provisions regarding the ethical behavior of the employees within a group? (T13-C);

Are the measures of social cohesion promoted amongst the company’s employees? If yes, specify clearly these measures in the observations’ section (T13-D);

Have you taken measures to grow the company’s competitiveness? If yes, specify clearly these measures in the observations’ section (T13-E);

Has your company registered losses in the last three complete financial years? (T13-F);

Has your company registered profit in the last complete financial year? (T13-G);

From the point of view of the number of employees, do you fall into the category of microenterprises? If the answer is negative, please specify the category in the observations’ section (T13-H);

Do you think that the ratio between the current assets and the fixed assets held by the company is an improper one? (T13-I);

Does the period of payment of total liabilities exceed two full years? (T13-J);

Has the evolution of the turnover in the last 3 years been an upward one? If no, please specify in the observations’ section if the evolution was fluctuating or heading downwards (T13-K);

Is the ratio between the turnover and the shareholder’s capital improper? (T13-L);

Do you register debts for a due date more than 45 days to the state budget? (T13-M);

How do you appreciate the future evolution of the company? (T13-N).

The model of sustainable reporting of non-financial information could be implemented by the monitoring bodies of the sustainable development set up based on the implementation of the National Strategy for Sustainable Development. It could also be implemented in parallel with the implementation of a smart reporting model of assimilating the criteria of sustainable development, similar to the model of sustainable reporting previously presented.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}