1. Introduction

In the last few decades, socially responsible investing (SRI), which focuses on ethical values, environmental protection, social issues, good governance, etc., has remarkably drawn attention not only to individual and private investors but also to researchers. The concepts of environmental, social and governance (ESG), SRI, and responsible, sustainable, and green investing have evolved rapidly over time, and are continuously changing. SRI and ESG came up strongly in the 1990s, and sustainability and long-term investing became popular in the 2000s. According to Donovan [

1], we are now living in the SRI 2.0 period, which is focused mainly on impacted investment and extension of the general awareness of responsible investing.

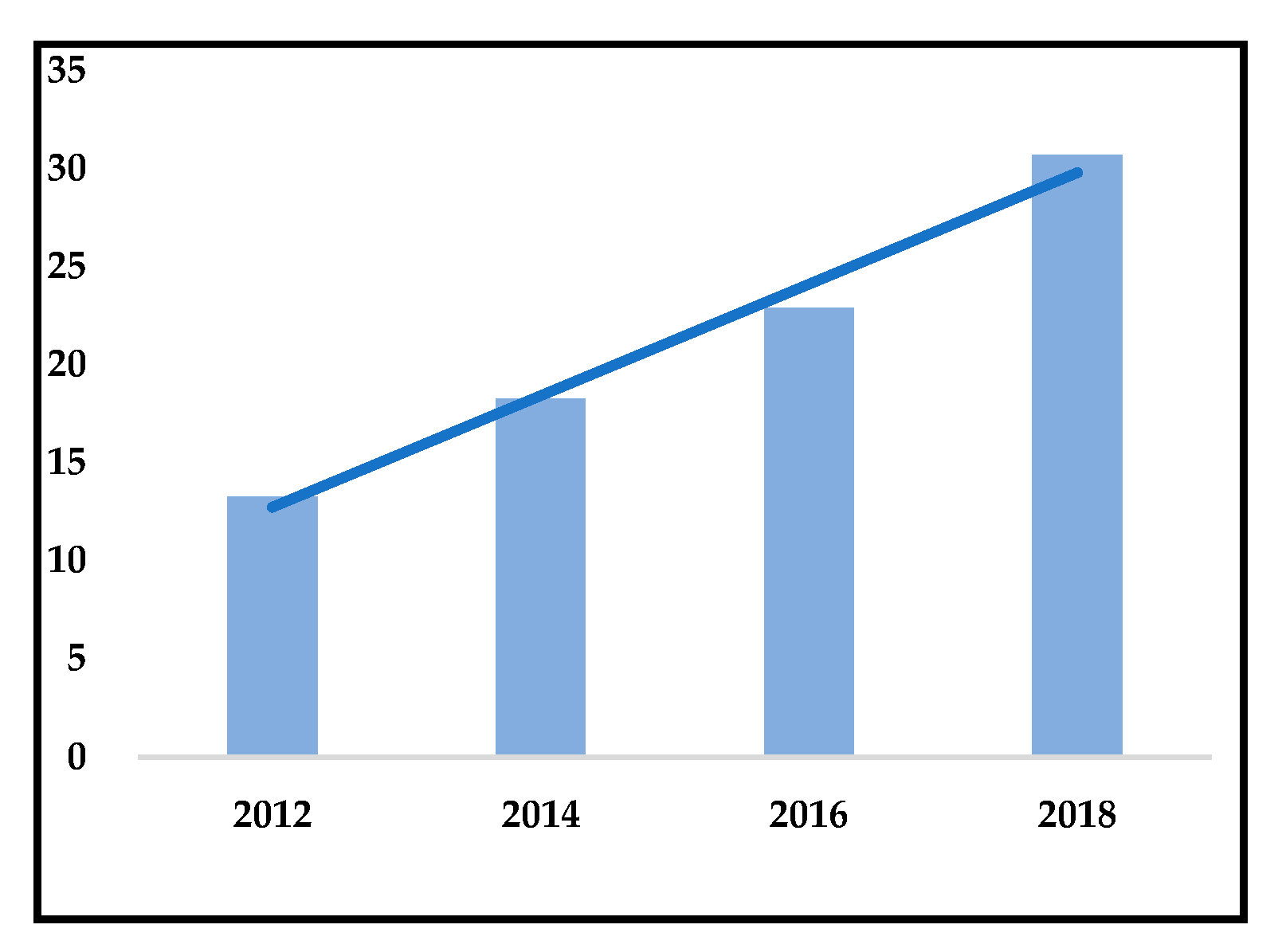

The rapid growth of the SRI market has made it more important worldwide. The global SRI asset outstanding has reached USD 30.7 trillion in 2018, which is almost 2.5 times more compared with 2012 (

Figure 1). In 2018, the European market of responsible investment funds reached almost USD 14.1 trillion of managed assets, nearly double the value compared with 2012. The financial means invested into RI (responsible investing) in the U.S. more than tripled in the period of 2012–2018, reaching the level of USD 12.0 trillion. It has been reported that the respective proportions of SRI to total management assets in Europe and the United States are 45.9% and 39.1% in 2018 [

2].

In Asia, Japan is in the leading position regarding socially responsible funds investment. Compared to Europe and the USA, the history of socially responsible funds in Japan is much briefer. Japan started socially responsible funds investment in the early 2000s. The initial investment in SRI was an eco-fund, and the concept of this investment came from the West as a new financial product to push cash flow from households to the SRI market [

3]. Though socially responsible investors in Europe and the USA are mostly institutional investors, most SRI in Japan hold publicly offered socially responsible funds targeting individual investors [

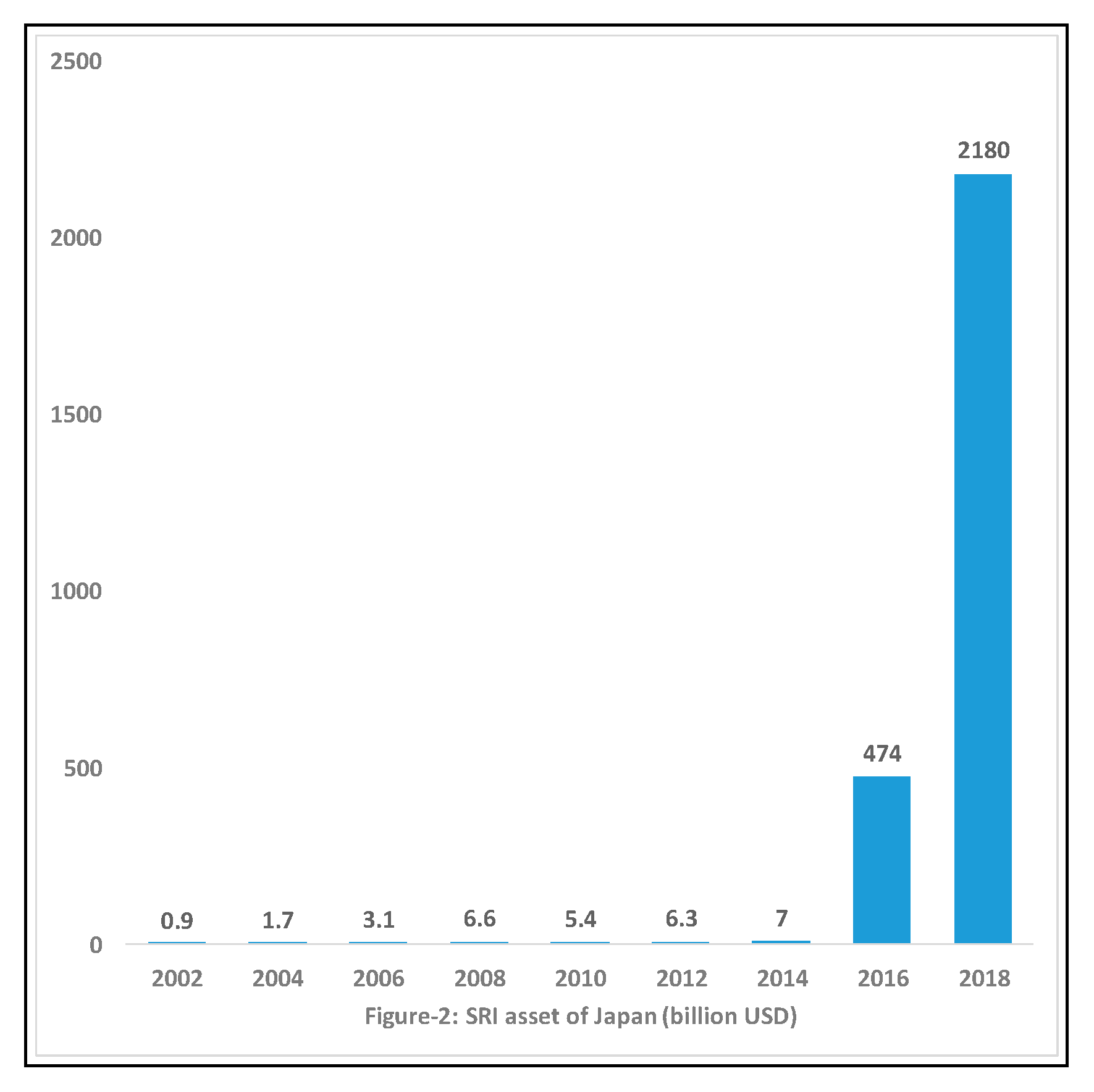

4]. According to the Japan Sustainable Investment Forum (JSIF), total net assets of socially responsible funds were around JPY 0.8 trillion at the end of December 2011, whereas the total sustainable investment balance was JPY 232 trillion in 2018 (

Figure 2), an increase of 1.7 times from the last year [

5]. On the other hand, conventional funds are already matured, so there were no sharp increases in the number and assets compared to the socially responsible fund [

4].

Though significant developments have been recorded in greening the economy, the United Nations Environment Programme (UNEP) estimates that the annual investment necessary to deliver a green economy over the 2010–2050 period will be approximately 2% of global GDP [

6]. Sustainable investment faces many challenges in the rapid transformation of the economy and society to meet the Paris 1.5 °C climate target. Green finance provides not only an opportunity for achieving environmentally sustainable innovation pathways but it also faces some institutional and financial criticalities such as uncertainty about public policies, minimum involvement of financial suppliers, short-term financial instruments, and the knowledge gap of financial options and technical expertise within firms [

7].

The finance ecosystem approach and public sector support will be necessary to ensure low carbon investment [

8]. According to Falcon and Imbert [

9], linking the ecosystem change with economic opportunities and social wellbeing has always been a challenging work. It is important for sustainability to focus not only on a restricted number of sectors (e.g., renewables, eco-innovations, bio-products) but also create the basis for a sustainable financial system to finance and fuel this transition [

10]. According to Falcon et al. [

11], a longer relationship between banks and firms will foster firm involvement in green investment strategies to reduce their environmental impact. The study by Mazzucato et al. [

12] suggested that the emphasis should move from the total amount of finance to its composition by financial actors (e.g., private banks, public banks and utilities) and areas of investment to promote sustainable investment. Better environmental performance due to green investment strategies can increase returns for firms by enabling access to green markets, and a product differentiation strategy based on firm environmental reputation. Also, green investment strategies can lead to a decrease in the cost of materials and energy use, capital assets and cost of labor [

13]. The discussed measures might increase the attractiveness of green investments to many investors. However, political instability and the uncertainty of the regulatory and policy environment could lead to an additional challenge for the investment. Therefore, it is difficult to measure the performance of socially responsible investing compared to its conventional counterparts during economic shocks.

Economic shocks have huge impacts on the economy and in performing the funds. The year 2016 was vulnerable to the economic perspective for the U.S. election and the Brexit referendum. These economic events have an important impact on the Japanese economy because of high trade relations with the world’s leading economy of the United States of America and Europe. Japan has played a very important role on both sides of the U.S. and U.K. as major investors. Japan is one of the most important trade and investment partners for the United States. According to the office of United States trade representative, bilateral U.S.–Japan trade in goods and services surpassed

$300 billion in 2018. Moreover, Japan is the third largest source of foreign direct investment (FDI) into the United States, behind only the United Kingdom and Canada, with total stock of FDI in 2018 at

$484 billion. The U.S. foreign direct investment (FDI) in Japan (stock) was

$125.5 billion in 2018 [

14]. On the other hand, the trade between the U.K. and Japan was worth £29.5 billion in 2018 [

15]. These economic facts established an important impact in the Japanese market due to uncertain policy from the recent U.S. election and Brexit.

Japanese investors were increasingly worried about the possibility of Donald Trump adopting protectionist policies and backing out of international trade deals which would be negative for Japanese industries. The expected negative shock might come for some Japanese enterprises invested in the U.K. due to a possible stringent policy of exporting their product to other European countries. Almost half (48%) of U.K. goods exports went to the EU in 2016. The U.K. goods exports to the EU were worth £145 billion in 2016, or 7.4% of GDP [

16]. Motor vehicles and parts is the largest product group by value of exports: the U.K. exported £18 billion of motor vehicles (and trailers) to the EU in 2016 where Japan has considerable investment in the motor vehicle and parts industry of U.K. In the short term, the market reaction will receive high attention in Japan for unexpected policy changes in the U.S. election and Brexit. In the long run, it may have severe economic consequences of rising oil prices to market panic and interruptions in global trade.

Though investors want to maximize their return, socially responsible investor motives and willingness to pay is more than conventional investors [

17,

18]. Therefore, socially responsible investors of Japan might have retained their investments rather than selling them during the economic downturn due to the U.S. election and Brexit. We assume that socially responsible funds in Japan have registered the negative effects of the recent U.S. election and Brexit better than their conventional counterpart.

This article examines how Japanese investment funds are influenced by the U.S. election and Brexit and confirms whether these events had any market uncertainty that impacts investor risk aversion and thereby significant positive or negative impacts on performing SRI and conventional funds. Evidence has been found in previous studies that the U.S. election cycle and its political factor is the important determination of international expected return of firms [

19]. The Brexit election result showed immediate effect in the Japanese financial market with a sharp decline in share prices. This study investigates the short-term effect of the U.S. election and Brexit to the returns of both SRI and conventional funds. The main objective of this research is to investigate the fund volatility as well as the performance and resilience of the funds between SRI and conventional during the above-mentioned economic shocks in 2016.

This article is organized as follows.

Section 2 provides a literature review on SRI, its performance and resilience, etc. The section develops an insight into the existing gaps in the literature.

Section 3 presents the data, research methodology, research design, and hypothesis testing.

Section 4 analyses and presents the results and discussions of the study.

Section 5 concludes the recommendations and suggestions for further study.

4. Results and Discussion

4.1. Recent U.S. Election Impact on the Return of All Funds Together

The recent U.S. election is the concern for Japan for many reasons such as high trade relations and the possibility of the backing out of the U.S. from the transpacific trade agreement. Japan was the fourth-largest export market and trading partner for the United States in 2018. The U.S. goods exports to Japan reached

$75.7 billion in 2018, while services exports were

$45.4 billion, for a total of

$121.1 billion. Imports of goods from Japan topped

$142 billion in 2018, as services imports neared

$37 billion, for a total of

$179.1 billion. Japan has a good tie with the U.S. historically regarding foreign direct investment (FDI) and it has grown every year for the past ten years, from

$238 billion in 2009 to

$484 billion in 2018 [

64]. Thus, investors in Japan are worried about Donald Trump’s unexpected policies. In the short term, the market reaction might receive high attention due to unexpected policy changes.

Moreover, political uncertainty can impact investors and markets in several ways. For example, Doukas, Chansog, and Pantzalis [

65] found that the mispricing of stocks tends to occur when there is high information uncertainty. Moreover, Ortega and Tornero [

66] found negative returns close after elections and suggest that this could show that the market needs time to assess the election’s impact following the vote count and the coming change in policies. A similar result was found in the analysis of Nippani Arize [

67] in their article on stock market volatility by the U.S. election of 2000. They found evidence indicating that both the Canadian and Mexican stock markets were affected negatively. Thus, we hypothesize that the recent U.S. presidential election has an impact on the return of Japanese investment funds.

The hypothesis that “there are no abnormal returns on all funds together around the days of the recent U.S. presidential election” can be rejected at 1% significant level for all models. It is evident from

Table 5 that the event had a significant effect on the returns of funds with J-statistics of 13.96, 8.8 and 14.17 in the event study method with the market model without EGARCH, the market model with EGARCH and Fama–French factor model respectively. The average price impact of the fund is 0.3 percent, 0.2 percent and 0.3 percent in the market model without EGARCH, the market model with EGARCH and Fama–French factor model respectively, as the estimated average cumulative abnormal returns (ACAR) are 0.003, 0.002 and 0.003 in the above-mentioned models respectively. Robustness is checked by testing in three different econometric models that indicates validity in these results (

Table 5). In the analysis, the volatility of fund returns is found within the event window which is similar to the result of Bialkowski et al. [

68].

4.2. Recent U.S. Election Impact on the Return of SRI vs. Conventional Funds

Now, this study examines how the 2016 U.S. election impacts short-term fund returns in Japan between SRI and conventional funds. It is evident from the empirical result that, in uncertain times, investors tend to avoid conventional stocks since SRI stocks pay a better return. Thus, this can also help explain the more abnormal returns for socially responsible funds, because of the uncertainty that can arise around an election. This thesis is based on a large sample of funds. Therefore, it is believed that this thesis contributes to bringing clarity in the performance area of both funds during election uncertainty. The following hypotheses are investigated.

Hypothesis (H1). The U.S. election of 2016 had no effect on socially responsible fund returns in Japan.

Hypothesis (H2). The U.S. election of 2016 had no effect on conventional fund returns in Japan.

Hypothesis (H3). There is no difference in fund performance between SRI and conventional funds due to the U.S. election.

In the case of socially responsible funds, it is evident from the J-statistics value that the event of the recent U.S. election had a significant effect on the returns of socially responsible funds at the one percent (1%) level with J-statistics of 17.19, 14.04, and 9.44 in event study methodology on market model without EGARCH, market model with EGARCH, and Fama–French factor models respectively. From

Table 6, the average price impact in this event window is 0.6 percent, 0.5 percent, and 0.4 percent in the market model without EGARCH, the market model with EGARCH, and Fama–French factor models respectively as the estimated ACAR of socially responsible funds are 0.006, 0.005, and 0.004 in the above-mentioned models respectively.

In the case of conventional funds, when performing the same test as above, it is found that the recent U.S. election had a significant effect on the returns of conventional funds at the one percent (1%) level in event study methodology on market model without EGARCH (J-stat = 3.22) and Fama–French factor models (J-stat = 7.11). However, J-statistics for the market model with EGARCH was 0.24 which not significant. According to

Table 6, there is a positive estimated ACAR through all models considered in this study for conventional funds. The average price impact in this event window is 0.1 percent, 0.01 percent, and 0.3 percent in the event study on market model without EGARCH, market model with EGARCH, and Fama–French factor models respectively as the estimated ACAR of conventional funds are 0.001, 0.0001, and 0.003 in the above-mentioned models respectively.

In the event study with the market model without EGARCH and the market model with EGARCH, the difference of the ACAR between SRI and conventional funds in mean test gives a t-statistic coefficient of 2.47 for both models, which implies that the mean CAR of socially responsible funds is significantly higher than mean CAR of conventional funds at five percent (5%) significance level (

Table 6). By comparing the mean CAR of SRI and conventional funds in all models, it was found that socially responsible funds are the better performer compared to their counterpart during the benchmark event window around the recent U.S. election. However, in the Fama–French factor model, the difference of CAR between the two groups is not significant. A reason why SRI is performing better would be a positive environmental screening of the most socially responsible funds in Japan which makes investors confident not to sell the stocks during economic shock, though the environmental screening has some additional costs.

The average price impact of socially responsible funds over the benchmark event window consisting of three days is 0.6 per cent in the market model without EGARCH. Hence, if one million yen were invested in a socially responsible fund in the sample when there is a U.S. presidential election, there would be an average gain of approximately 6000 yen over the three trading-days around the election but the gain for the conventional fund is 1000 yen. The gain for the socially responsible fund is more than its counterpart in the other two models too. Therefore, it can be concluded that socially responsible funds showed greater sensitivity (ACAR of SRI > ACAR of conventional) to uncertainty around the recent U.S. presidential election compared to conventional funds.

Moreover, when there is uncertainty about future government policies, stock market volatility tends to increase. This rise in volatility is caused by increases in systematic risk rather than firm-specific risk. Nakai et al. [

4] found that the estimated ACAR of socially responsible funds is significantly positive, which is similar to the findings of this research. They stated that the Japanese socially responsible funds were more resilient compared to conventional funds in the Lehman Brothers bankruptcy during the global financial crisis in 2008. According to their analysis, socially responsible fund holders did not sell their stocks even in difficult situations. Regarding the return of funds during economic shock, they indicated the negative return for conventional funds, but this study found the opposite result. There might be scaling intensity of the events concerning economic shocks.

4.3. Recent U.S. Election Impact on the Return of SRI vs. Conventional Funds in Cases of Domestic and International Funds

To investigate the attachment of the fund orientation, this study investigates the quick reaction of funds separately for domestic and internationally involved firms. This study found that international funds had a better return in comparison with domestic funds for both funds. A positive average price impact was found for international funds, whereas it was negative for domestic funds in almost all models. Therefore, it can be said that the fund returns are more attributable to international. Investors might think international enterprises had more CSR activities and domestic firms had less diversification.

In comparison with the estimated ACAR, the socially responsible funds were more resilient (ACAR of SRI > ACAR of conventional) than conventional funds in both domestic and international cases during the U.S. elections for all models (

Table 7). In the case of international orientation, the differences of ACAR between SRI and conventional funds are significant at the 5% level (t-stat = 2.45) in the event study with the Fama–French factor model, whereas this difference was not significant for domestic funds.

4.4. The Brexit Referendum Impact on the Return of All Funds together

The term Brexit came to a discussion when the United Kingdom was divided on whether they would remain in or leave the European Union. This decision had a great impact not only for Britain but also for other countries. The U.K. has a great impact on the Japanese economy due to factors regarding international trade, international investment, financial sector, and the stock market. It is estimated that there are nearly 1000 Japanese firms based in the U.K., employing over 150,000 people. The total exports to the U.K. were 1.53 trillion yen (cars, power engines, car parts) and imports from the U.K. were 0.91 trillion yen (medical and pharmaceutical products, cars, power engines) in 2018 [

15]. Large Japanese companies such as Toyota, Nissan, etc., have plants in the U.K. These plants sell their products not only in the U.K. but also to other European countries.

The U.K. referendum on whether to stay in or leave the European Union ended with a big surprise to the global economy as well as to Japan. According to the Japan Centre for Economic Research (Saito), Brexit causes stock price volatility which will lead to realized and unrealized losses in investor’s portfolios, and it will ultimately change people’s expectations in the future [

69]. The Brexit referendum result reflected quickly in the Japanese share market with a sharp decline in the price. Therefore, our hypothesis is that “there are no significant abnormal fund returns on all funds together around the Brexit referendum result days”.

This study investigates how Japanese investment funds are influenced by the U.K. referendum. The significant (1% level of significance) negative estimated average cumulative abnormal return (

) of the funds together in all models confirmed the negative shock in Japan (

Table 5) due to the isolation of Britain from the European Union (

Table 5). It is evident from

Table 5 that the average price impact of the fund is −1.4 percent, −1.5 percent and −2.3 percent in the event study on the market model without EGARCH, market model with EGARCH and the Fama–French factor model respectively, as the estimated average cumulative abnormal returns (ACAR) are −0.014, −0.015 and −0.023 in all models respectively.

4.5. The Brexit Referendum Impact on the Return of SRI vs. Conventional Funds

The Brexit referendum had a significant adverse effect on the returns of both SRI and conventional funds. The difference of the estimated

between SRI and a conventional fund is also significant in all models (

Table 8). The results show that in uncertain times, investors tend to avoid socially responsible funds which is opposite to the U.S. election impact on socially responsible funds. The possibility would be a real connection between Japanese socially responsible firms with the U.K. or the European Union market.

It is clear from empirical findings that conventional funds show greater resilience to the uncertainty around the recent Brexit referendum compared to socially responsible funds. Moreover, when there is uncertainty about future government policies, stock market volatility increases. In comparison with conventional funds, socially responsible funds were more resilient in Japan in the event of the Lehman Brothers bankruptcy during the global financial crisis in 2008 [

4]. This result is opposite to the findings of this study. They also indicated negative returns for conventional funds, which is similar to this study.

4.6. The Brexit Referendum Impact on the Return of SRI vs. Conventional Funds in Cases of Domestic and International Funds

The Brexit referendum had a significant (1% level of significance) negative effect on the performance of all funds except domestic conventional funds. One possibility would be less influence of domestic funds by the U.K. business entity. In both domestic and international cases, a significant difference on the estimated

was observed between the SRI and conventional funds. The conventional funds had a positive estimated ACAR in the case of domestic funds and negative estimated ACAR for the international funds in the Fama–French factor model (

Table 9). The reason may be the international orientation of the fund. Regardless of the domestic and international orientation of the funds, conventional funds were more resilient during the Brexit referendum shock.

4.7. Limitations of the Study

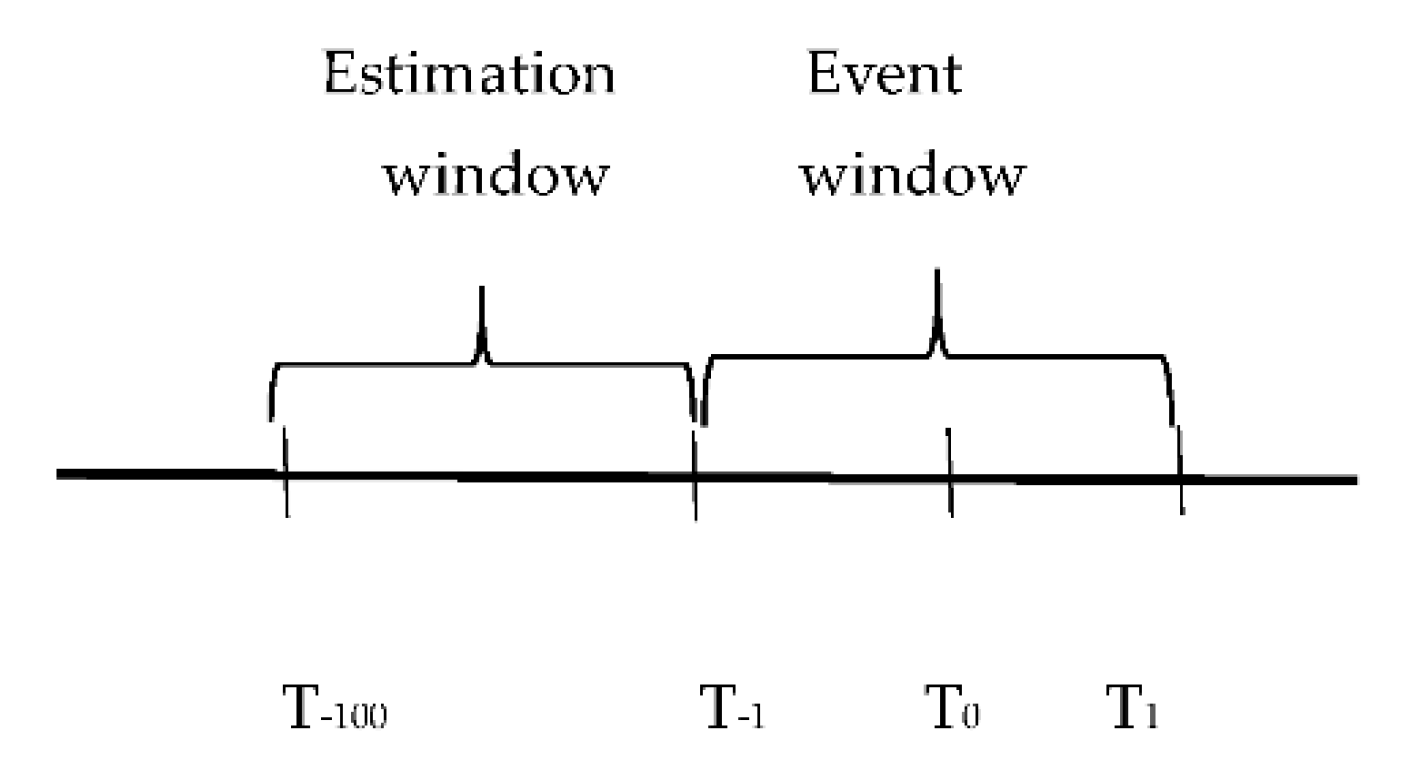

Usually, an event study methodology can have several problems regarding the exact event date, estimation window selection, daily returns, time horizon, confounding effects, market models, etc. The exact event date was known for this study, which ensured the unexpected outcome of the funds. However, the modern election poll survey might have some impact on the volatility of the funds, which violates the assumption of completely unexpected event results. Also, this study is not free from confounding effects. Fund-specific noise might be observed as we have selected the individual funds instead of indices. However, as the short-term event study was conducted, the mis-specification problem of expected returns was not as severe as in a long-term event study.

5. Concluding Remarks

This study investigated the performance and resilience of both SRI and conventional funds in Japan during the U.S. election and Brexit referendum in 2016 using an event study methodology. It is expected that these economic shocks affected fund volatility in Japan. Empirical results obtained using the market model without EGARCH, the market model with EGARCH, and the Fama–French three-factor models showed that the U.S. election had a significant positive effect whereas the Brexit referendum event had a significant negative impact on the performance of the fund returns in Japan around the event window. The negative average cumulative abnormal return (ACAR) of both SRI and conventional funds confirmed the negative shock in Japanese funds due to the isolation of Britain from the European Union.

It is evident from the study that socially responsible funds showed greater sensitivity to the uncertainty around the recent U.S. presidential election in 2016 compared to conventional funds. However, the opposite result was found regarding the Brexit referendum. There might be a reason for more bilateral business involvements of conventional Japanese enterprises with the U.K. and European Union, more than the U.S.A compared to socially responsible funds. This study also found that the performance and resilience of socially responsible funds during the U.S. election event were largely attributable to international funds. Similar results were found by Nakai et al. [

4] where they noted that “socially responsible funds better resisted the Lehman Brothers bankruptcy than conventional funds did”. They discussed the two possibilities of the international socially responsible funds resilience, such as “more CSR activities by international firms” and “less diversified domestic socially responsible funds”. Moreover, this study found that conventional funds had a positive ACAR in the case of domestic funds and negative ACAR for international funds during the Brexit referendum. The reason might be the international orientation of the funds.

The important implications of these findings are the optimal strategies of institutional or individual investors who have direct or indirect exposure to the fund volatility risk. The study shows a significant connection between social performance and financial performance of the Japanese funds during the recent U.S. election and Brexit referendum in 2016, meaning that a ‘good’ level of social performance allows responsible investors to suffer less from the negative effects of economic downturn. The buffer effect of a good level of social performance found in this study should motivate investors to invest in socially responsible investing, particularly in times of uncertainty, when investors are facing a hostile environment. We expect that adhering to social and environmental practices does not harm an investor’s competitive position, but on the contrary, constitutes a competitive advantage. We find that the evidence that Japanese socially responsible funds provide additional downside risk protection to investors compared to conventional funds in times of economic shocks, but that they also do not imply any sacrifice in terms of financial performance, is consistent with the study of Nofsinger and Varma [

45]. As most of the socially responsible funds in Japan are environmentally screened, socially responsible investors might successfully navigate the dynamic challenges of economic shocks. This pattern could be valued by investors seeking downside protection.

This study can be extended to examine why funds perform better during economic shocks in the context of periods, scaling, risk exposure, screening, etc. This will also help to discover the resilience factors of the funds in the Japanese market.

{kind=link}

{kind=link}

{kind=link}