1. Introduction and Literature Review

There are three most important aims of the pension system: adequacy, sustainability and integrity [

1]. As adequacy, we consider pension benefits which allow one to prevent poverty and maintain the previous standard of life. Sustainability of the pension system is strongly connected with adequacy; thus, they both have to be balanced. Integrity, on the other hand, is not considered in the study as it mainly concerns the capital part of the system, focused on the private sector. In the Polish pension system, as a result of changes introduced by the government, the capital part keeps losing its important role.

For an individual, the most important thing is an adequate pension benefit [

2]. Currently, the nominal average retirement pension in Poland is (data for March 2020) PLN 2395.11 (i.e., EUR 267.34 and PPP 1781.23—in 2017) and constitutes 44.92% of an average wage in the Polish economy. The amount of the lowest retirement pension, on the other hand, is PLN 1200 (EUR 1187.75). Thus, the amount of the average old-age pension is almost twice as high as the minimum subsistence level (PLN 1242.37), which means that it provides adequate living conditions. The minimum pension is slightly lower than the subsistence level, where the subsistence minimum is a social indicator measuring the cost of living of households. The scope and level of satisfied needs, according to this model, should provide such living conditions so as to enable the reproduction of life forces, the possession and upbringing of offspring and the maintenance of social bonds at each stage of human development.

The level of pension benefit in Poland and, as a consequence, pension adequacy depends on various factors, especially on wages and seniority. These factors are currently subject to intensive changes due to flexibilization of employment history [

3]. Flexible forms of work are associated with a lower salary and a shorter period of paying pension contributions. This will undoubtedly lead to a reduction in the level of pension benefits as well as problems with obtaining pension adequacy.

Fornero [

4] considers the working career as the most relevant factor in determining the relative retirement income of women in comparison to men. According to Draxler [

5], this is connected mainly with changes in the level of wages, which constitute one of the most decisive factors in the level of pensions. Since “‘wage flexibility’ mainly means a larger spread of earnings at the lower end of the wage scale” [

6], pension benefits should be compared for workers with a range of different earning levels, for example, between 0.4 times and 3 times of the economy-wide average (Average Wage, AW). In this context, the situation of low-wage earners or people with career breaks needs to be particularly closely monitored [

7]. Moreover, Hinrichs and Jessoula think that if pension systems were to be adapted to modified labor market conditions in time, they might not be able to either ensure adequate income maintenance or prevention of poverty, or both [

6].

In this context, it is necessary to study the decisions made during the working career in order to obtain an adequate pension [

8]. The article aims to present how changes in wages and employment breaks, caused by flexibilization of employment history, will impact pension adequacy in Poland. Another aim is to indicate factors which could be changed in a work career to achieve an adequate pension.

Future pension benefits in the research are calculated according to the rules in the pension system in Poland. We have analyzed cases of pensioner men and women with an average salary during the working time, pensioners with an individual promotion of a salary, then pensioners with different levels of a salary in the whole work career. If employment breaks have occurred, we examine consequences for pension adequacy caused by 5 and 10 years of breaks in work. In 5-year breaks, we studied breaks in different moments of a job career: at the beginning, in the middle and at the end of a working career. An assessment of the pension adequacy has been made by using the individual or the general theoretical replacement rate (TRR).

There are very extensive reports on pension adequacy by the European Commission [

7,

8,

9,

10,

11,

12]. They contain a series of scenarios describing possible predicted values of the theoretical replacement rate. These scenarios, however, apply only to people with standard pension parameters. They do not consider any other retirement age than the standard one and do not explore a broader possible range of seniority. The 2015 and 2018 edition of the Pension Adequacy Report aimed at a multi-dimensional approach to the adequacy of pensions. In this approach, three aspects of adequacy are considered: poverty protection, income maintenance, and pension duration.

The issue of pension adequacy is also discussed in OECD documents [

13,

14,

15,

16,

17,

18,

19,

20]. Research in this area is presented in the series Pension at a Glance. On the site

https://data.oecd.org/pension/gross-pension-replacement-rates.htm it is given the value of Gross pension replacement rates calculated by OECD [

21]. The Mercer reports [

1,

22,

23,

24], are widely known and include the ranking of pension systems in terms of adequacy, sustainability and integrity. Additionally, World Bank [

25,

26] conducts an analysis of retirement benefit adequacy. Scientific research in the field of measurement of pension adequacy is also carried out by Borella and Fornero [

27] and Möhring [

28]. They focus on the consequences of employment flexibility.

In Poland, the problem of pension adequacy is particularly dealt with in research by Chłoń-Domińczak [

29,

30,

31]. Additionally, Chybalski [

32] and Marcinkiewicz [

33] take up the problem of adequacy, focusing primarily on the question of its measurement. Rutkowska-Góra [

34] points to the adequacy aspects related to redistribution in the pension system. In Szarfenberg’s [

35] works, the aspect of adequacy in the context of poverty appears to be the most important. The problem of substitution between public pension wealth and private savings, which is connected with pension adequacy, is analyzed by Lachowska and Myck [

36].

However, the literature lacks in-depth research on pension adequacy with a wide range of variables and a wide range of values of these variables. The following study tries to fill in this gap. In addition, the unique use of the classification tree method allows the author to identify factors particularly important for pension adequacy and to indicate ways to proceed during the work career that will be helpful in obtaining adequate benefits. Studies made in this work provide a set of clear and useful pension decision rules for people who experience flexibilization of their employment history. An application of these rules will allow them to obtain adequate pensions. This applies particularly to women, whose retirement pension benefits will be lower than those of men. This could help support the policy of counteracting adverse demographic trends in fertility rates through the building of financialsustainable pension schemes.

2. Materials and Methods

The considerations presented in the paper relate to the Polish mandatory pension system introduced in 1999. Pension entitlements are calculated using the Polish pension model [

37,

38]. The calculations are based on Poland’s economics parameters and rules applied in 2017. The baseline economics and demographic assumptions are as follows: life expectancy tables for Poland in 2018 are used [

39]; the rate of return for Open Pension Fund is considered as 4% for all years; real wage growth is 2.5% [

1,

40]. The GDP growth was taken into account in the study by introducing the indexation of funds on the account of the Social Insurance Institution (ZUS) and by taking into account the rate of capital growth accumulated in OFE (Open Pension Funds).

The analyses are made for hypothetical persons covered by a new system. The study has been conducted separately for men and women, because their pensions differ significantly due to the different average life expectancy at the time of retirement [

16,

41]. According to the Central Statistical Office of Poland, life expectancy at birth in Poland for men is equal to 73.9 years and 81.7 years for women (in 2018). However, according to the assumptions of the EUROPOP2017 population projections, life expectancy at birth in Poland should increase in the years 2016–2070 by more than 10 years for men and 8 years for women. Currently, life expectancy years in retirement for men are 15.8 and 24.2 for women. If the retirement age remained at the level of 67, as was adopted in the Polish pension system in 2013, men would be retired for a shorter period, namely for 14.6 years and women for 18.5 years. This would undoubtedly be a significant facilitation for the financial stability in the system. In 2013, lawmakers in Poland made a decision to raise the retirement age to 67—up from 65 for men and 60 for women. This move was expected to increase pensions, add to Gross Domestic Product, and lower the country’s deficit. However, in 2017, the retirement age was lowered to its previous level as a result of protests and people’s dissatisfaction. Probably, only very low and anticipated pensions in the future or the loss of the financial sustainability of the system are able to convince Poles about the necessity to raise the retirement age. The second reason for separate research on pensions of women and men is the wage gap between the two sexes of different age. Wage differences between men and women tend to widen with age. The average earnings of women are lower than those of men, to a widening extent the older the age group. The pattern of career is taken into account by adopting different levels of seniority (from 20 to 52 years) and standard retirement age—SPA (standard pensionable age)—60 to 65 and 65 and 70 years. Pension benefits are examined for workers with a range of different earning levels, i.e., between 0.4 times and 3 times the economy-wide average (Average Wage, AW). This range permits for an analysis of future retirement benefits of both the poorest and richest workers. An individual real promotion in the salary of men and women is at the level of 0.73% in the stable promotion case. In changeable salary promotions during the work career, the salary promotion for men is 1.8% for the first few years; then, for the last 20 years of work it drops to 0.6% per year. In the case of women, the first few years saw an increase of 1.4%. However, during the last 15 years of work, this promotion has been reduced to 0.1% [

42].

Pension adequacy is researched on five cases. The first one examines pensions of people who throughout their whole work life have received a salary equal with average wages in the economy. In the second case, a stable and changeable promotion in the salary is taken into consideration, while the third case deals with differences in the wages during the whole work life. Another case takes into account breaks in seniority. We have studied different times of breaks in case four—5, 10 and 15 years of break. In case five, 5 years of break was considered at the beginning, in the middle and at the end of the working career. All the cases considered in the study are presented in

Table 1.

For the studies, simulation of objects in two forms of future pension benefits is used. The first form constitutes the theoretical gross replacement rates of individual wage—individual TTR, and the second one is the theoretical gross replacement rates of average wage—general TRR [

10]. The general TRR is used only in the case with a different wage level. While individual theoretical replacement rates are about income maintenance, they measure how a retiree’s pension income in the first year after retirement would compare to their earnings immediately before retirement. They are defined as the level of pension income in the first year after retirement as a percentage of individual earnings at the moment of take-up of pensions [

12]. The general TRR is defined as the level of pension income in the first year after retirement as a percentage of economy-wide average wage at the moment of take-up of pensions.

Then, for both sexes, pension adequacy has been studied [

43]. The criterion of adequacy concerns protecting future pensioners from old-age poverty and maintaining the pre-retirement standard of living [

3] after retirement, which can be obtained at the level of at least 40% TRR [

44].

The assessment of pension adequacy is made by using the method of classification tree which belongs to the data mining methods [

45]. The algorithm CART—Classification and Regression Trees [

45,

46] has been selected to conduct the analysis. The CART algorithm is one of the most effective methods of building classification trees. Its operation is based on the recursive division of objects into two smaller subsets until homogeneity is obtained in the belonging of objects to classes. Gatnar [

47] gives the following rules for constructing a tree:

each classification test during tree construction is based on one variable;

for a feature represented by a quantitative or qualitative variable, all possible divisions in the set of objects are considered;

the Gini differentiation index is used to select the best partition that gives the most homogeneous subsets;

the division should be completed when there is no significant decrease in the diversity of objects in the set.

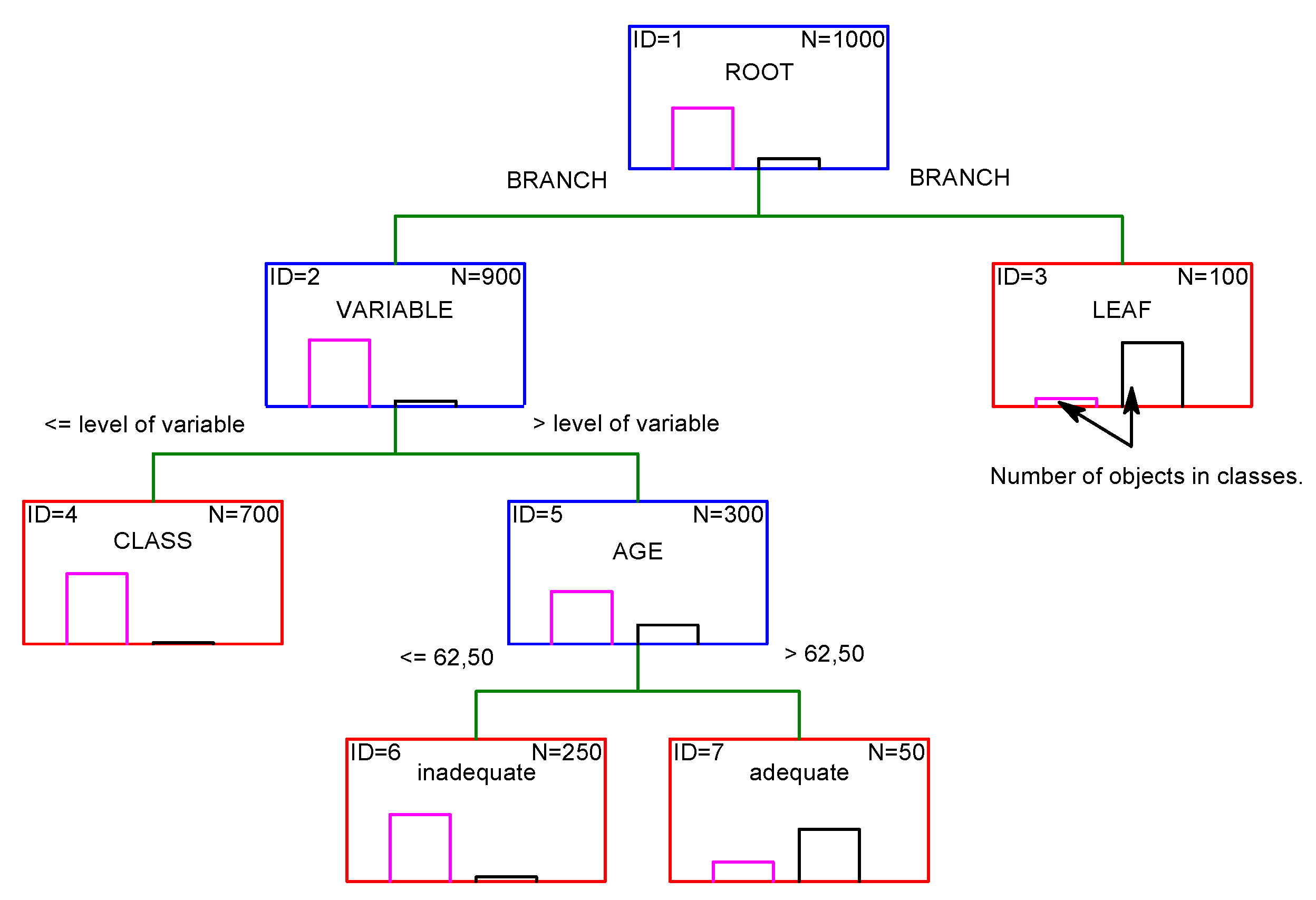

The primary feature of CART is the hierarchy of predictions. This procedure is also known as a hill-climbing strategy or greedy optimization. The goal is to create a tree with a minimum number of nodes. The classification tree begins with the root (

Scheme 1). It has at least two edges, called branches, in the nodes that lie on the lower tier. Internal nodes describe how to divide objects into homogeneous classes based on selected variables. Each node points to a splitting variable. The branches, in turn, determine the values of the features on the basis of which the division took place. The value is given on the branch. The object is then moved down an appropriate branch. Leaves are nodes from which no branches come out anymore. They represent classes to which given objects belong. The number of objects from each class are given in nodes and branches.

Cross-validation has been used for tree validation [

48]. The quality of trees is assessed by using the correct classification index, assuming that a value above 95% means a correct, well-classifying tree [

49].

The CART method also permits to construct a ranking of the variables applied in the classification. The concept of surrogate split is used here. It refers to such a split that is based on the explanatory variable, as a result of which, the probability of obtaining a goodness of fit close to that obtained as a result of the split used is the highest. This allows one to determine the significance of each variable, also when no division has been made in the best classification tree on its basis. In order to compare the significance of variables, their importance is normalized, obtaining relative significance measures (expressed in ranking points). Thanks to this, the most important variable gets 100 points in the ranking. The lowest potential significance is 0 points. This normalized importance of variables, called validity, is shown in the vertical axis in figures, with ranking of the variable validity for every researched case.

Summing up, it can be said that decision trees are a fast, computationally simple and flexible method. Their advantages also include obtaining very good results in comparison with other classifiers. Due to their successful practical application, classification trees are an accessible tool for classifying data.

Calculations are performed using TIBCO StatisticaTM 13 (TIBCO Software Inc., Palo Alto, CA, USA).

3. Analysis of the Results

3.1. Pension Adequacy of an Average Earner

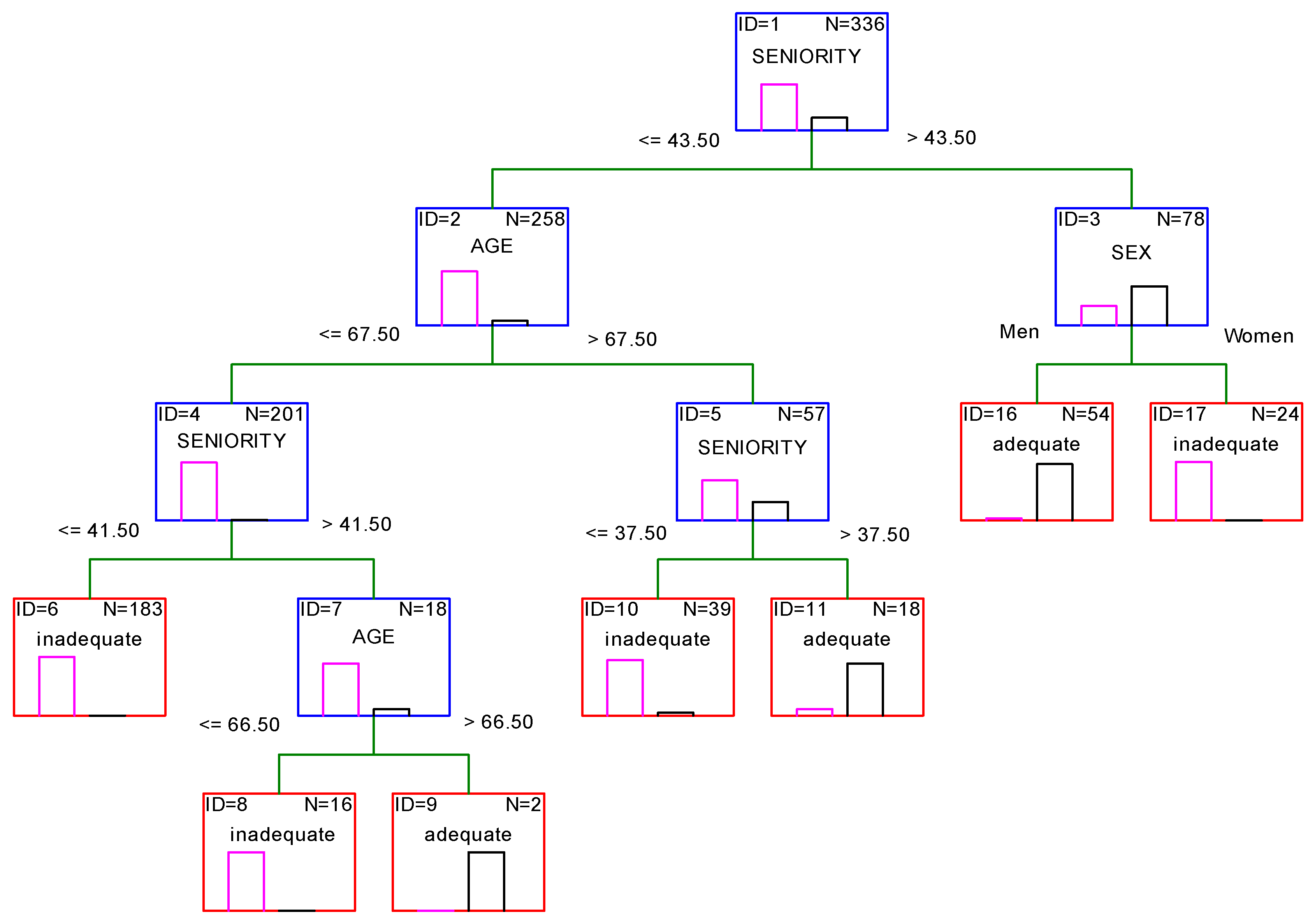

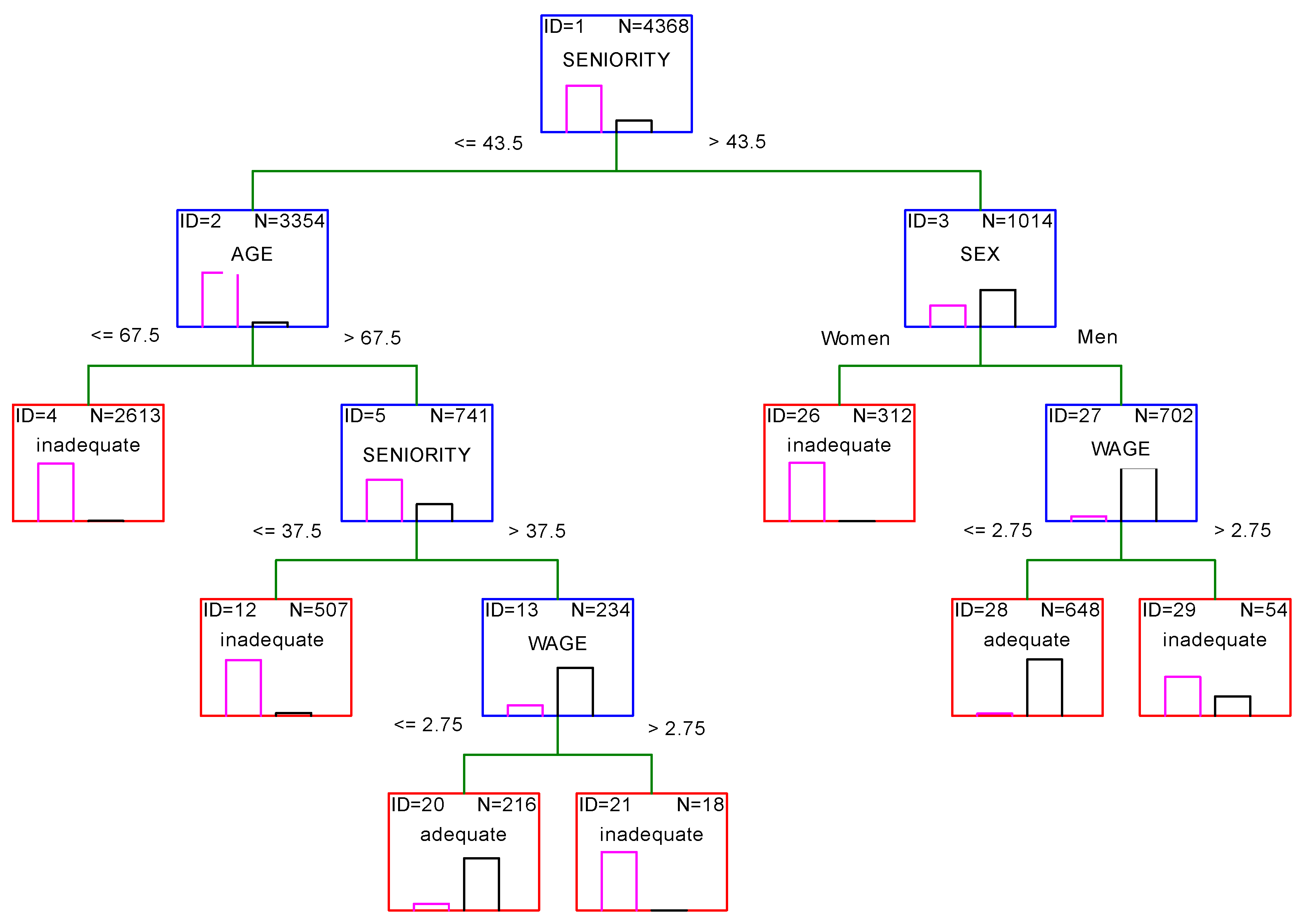

The results presented below refer to the first, the base case. The base case represents the pension adequacy for a person, a man or a woman, who retires at the standard pensionable age (SPA) or later, i.e., 60–65 for women and 65–70 for men, after an uninterrupted 20–52-year career on a standard employment contract with average earnings.

The classification tree in

Figure 1 allows us to formulate the following observation: a person wishing to have an adequate pension should obtain a combination of the following factors:

Men and Seniority >43 years long;

Men or Women with Seniority 42 or 43 years and Age 67 years.

Men or Women with Seniority between <38–43> years and Age 68 years or higher.

It means that for men, the guarantee of an adequate pension is their seniority longer than 43 years, regardless of the retirement age. If men or women have worked shorter than 43 years, they should postpone their retirement until at least 68 years of age.

The classification tree results are significant because 98.21% of objects were well-classified.

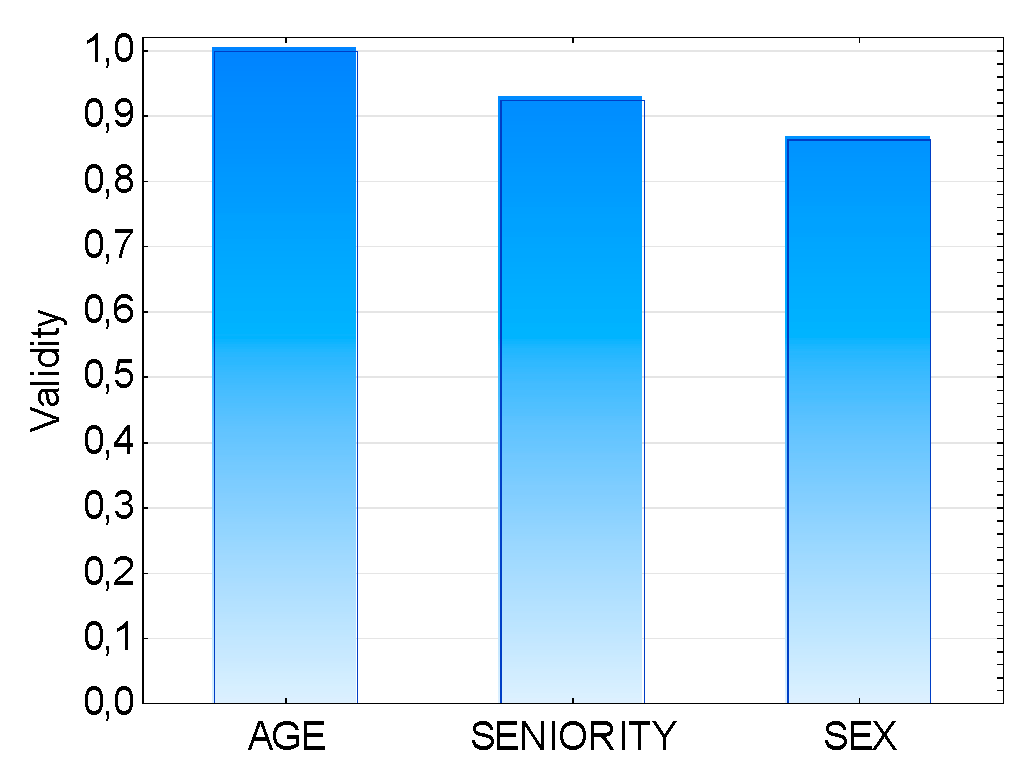

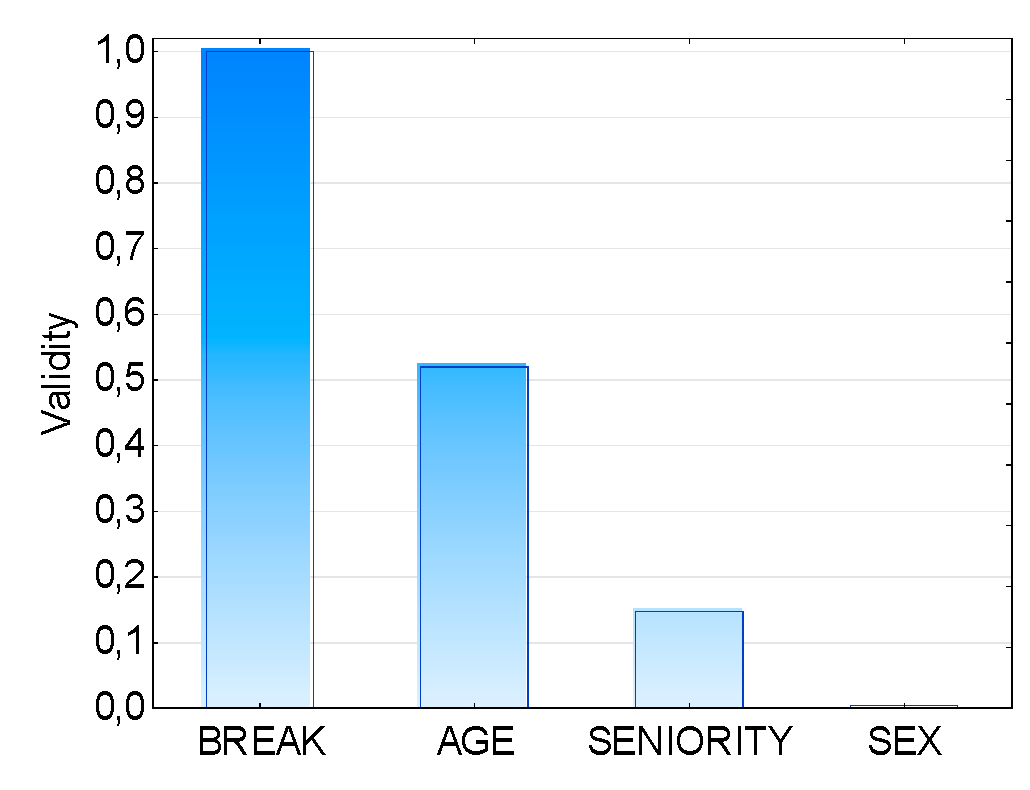

Figure 2 shows the ranking of variable validity in the base case.

The most important factor is retirement age, then seniority and the least important is sex. The last years of the working career are crucial for the level of pension, and consequently, for pension adequacy. This could be derived from the specifics of the compound percentage, according to which the pension capital is calculated. Capital growth in the final period of accumulation is greater than at the beginning.

3.2. Pension Adequacy of an Earner with Salary Promotion

The second case, shown in

Figure 3, illustrates pension adequacy for a person, a man or a woman, who retires at the standard pensionable age (SPA) or later, 60–65 for women and 65–70 for men, after an uninterrupted 20–52-year career on a standard employment contract with a salary promotion. The start earnings equal 70% of an average wage. The promotion of the salary could be stable by the whole work career or can be changeable. The salary rises faster at the beginning of the professional career, then it stabilizes and then declines towards the end of the professional career.

To have an adequate pension, one should obtain a combination of the five factors:

No promotion, Men and Seniority >41 years long;

Stable promotion, Women, Seniority >41, Age >62;

No promotion, Men or Women, Seniority between 37–41 years, Age >67;

Stable promotion, Men or Women, Seniority between 32–36 years, Age >67;

Stable promotion, Men, Seniority between 37 and 41 years, Age between 65 and 67.

Consequences of increasing labor market flexibility connected with the stable salary promotion during the work career is important for pension adequacy. Taking into account this factor has led to the mitigation of the requirement for pensioners. Adequacy is then possible with shorter seniority and with a lower retirement age. In this case, 96.73% of objects were well-classified.

Significant factors for pensions received by the earners with a salary promotion are still seniority and retirement, as shown in

Figure 4. The salary promotion has lower influence on the diversity in pension benefits. The description and a proper approach to this issue is comprehensively discussed in [

34,

35].

3.3. Pension Adequacy of an Earner with Different Levels of Salary

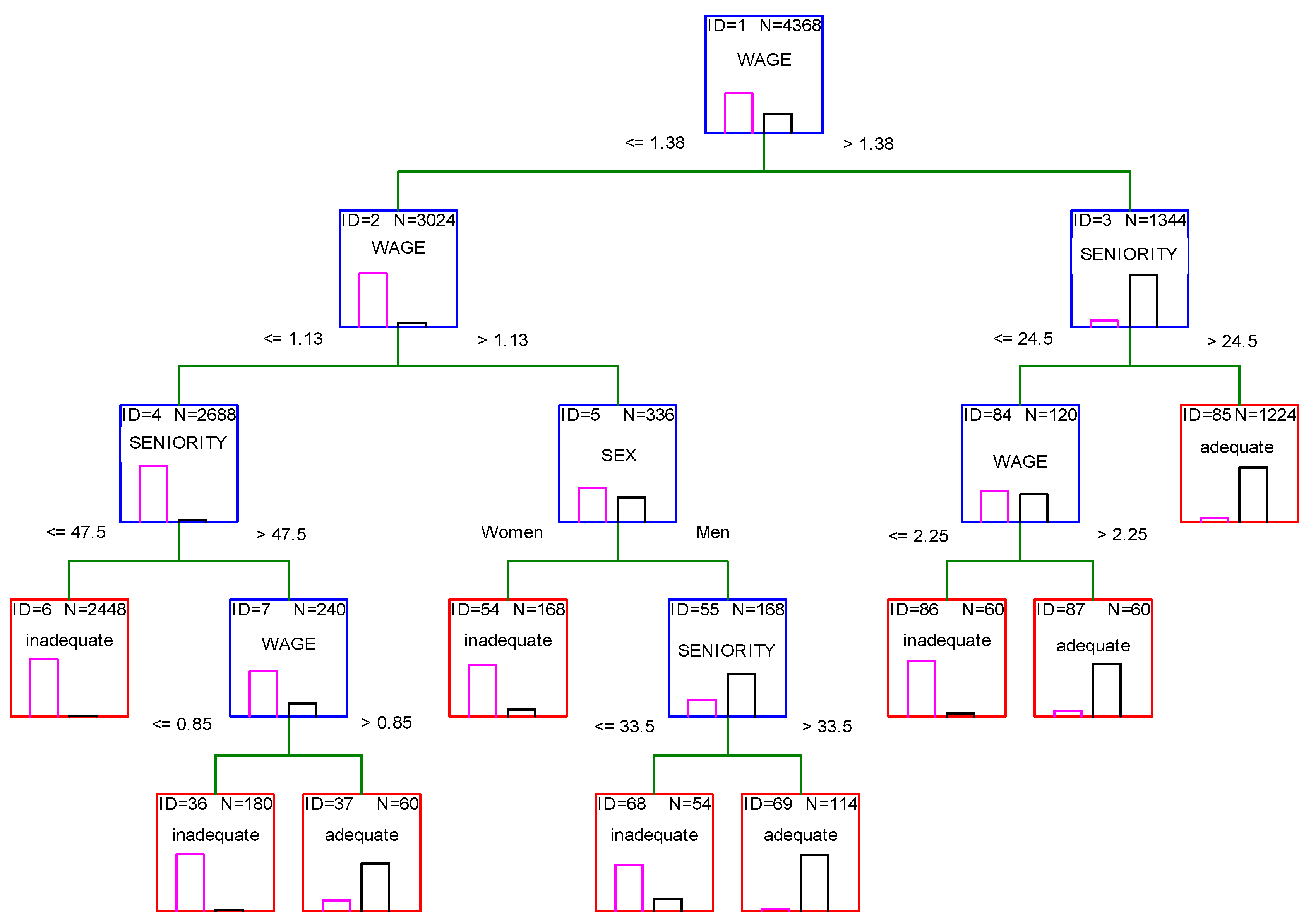

The third case presents pension adequacy for a person, a man or a woman, who retires at the standard pensionable age (SPA) or later, 60–65 for women and 65–70 for men, after an uninterrupted 20–52-year career on a standard employment contract with different salary levels. The range of earnings is between 40% and 300% of an average wage.

In Poland, pensions are almost fully proportional to work income, therefore, people with different levels of earnings have received the same individual TRR. The difference concerns only a high earner—whose earning is twice and a half times higher than the national average. The principle of collecting a pension contribution from wages up to two and a half of the average wage in the economy, which is in force in Poland, means that despite a really high salary, the contribution of such people is relatively low. In consequence, such a person will have a lower TRR than the rest of the pensioners as well as inadequate pensions, as shown in

Figure 5. Classification is correct due to the 97.39% well-classified object.

If we take into account different earning levels, it is better to use general TTR, i.e., relation pension to the average wage in economy. The generated classification tree shown in

Figure 6 gives four rules leading to pension adequacy. People should have one of the following combinations of factors:

Wage >138% of Average Wage and Seniority >24 years;

Wage >225% of Average Wage and Seniority between 20–24 years;

Wage between (113%–138%> of AW, Men and Seniority >33;

Wage between (85%–113%> of AW, Seniority >47.

A low wage leads to a low pension, but this problem can be compensated by an appropriate seniority. Short seniority, i.e., shorter than 24 years, requires from a future pensioner that they achieve earnings over 138% of an average wage.

The results are significant, because 95.76% of objects were well-classified.

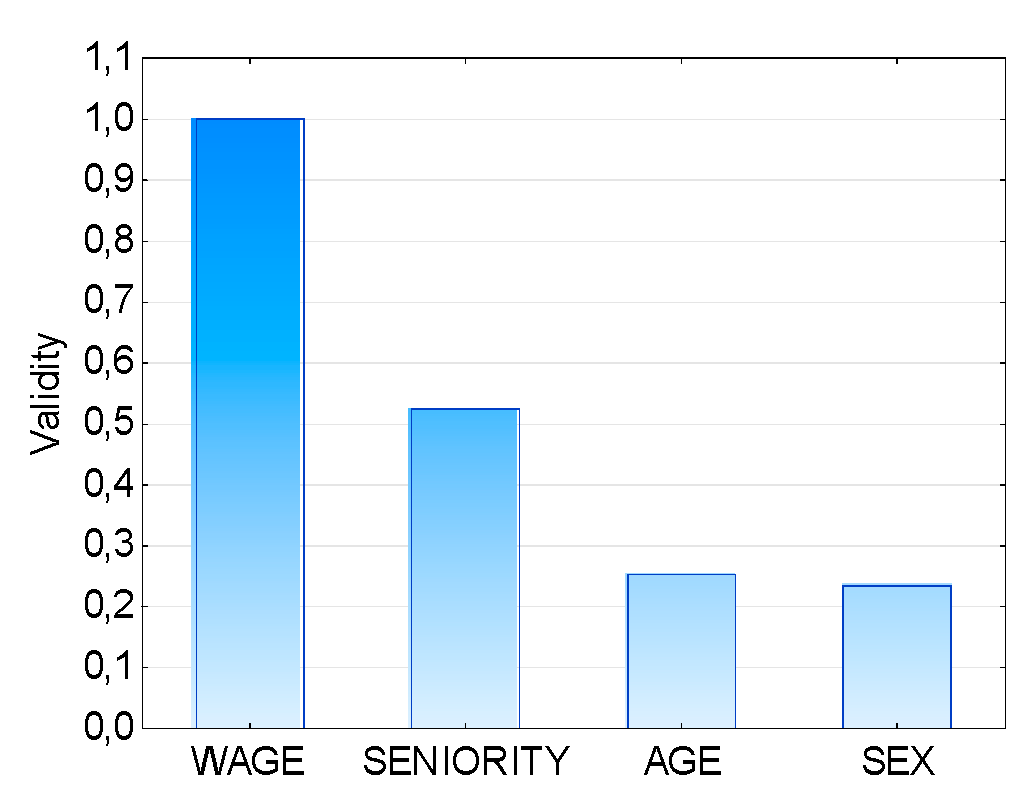

According to

Figure 7, the level of earnings played the key role for pension adequacy. However, seniority is also crucial. The importance of retirement age is shrinking in this case.

3.4. Pension Adequacy of an Earner with Different Moments of a Break in the Working Career

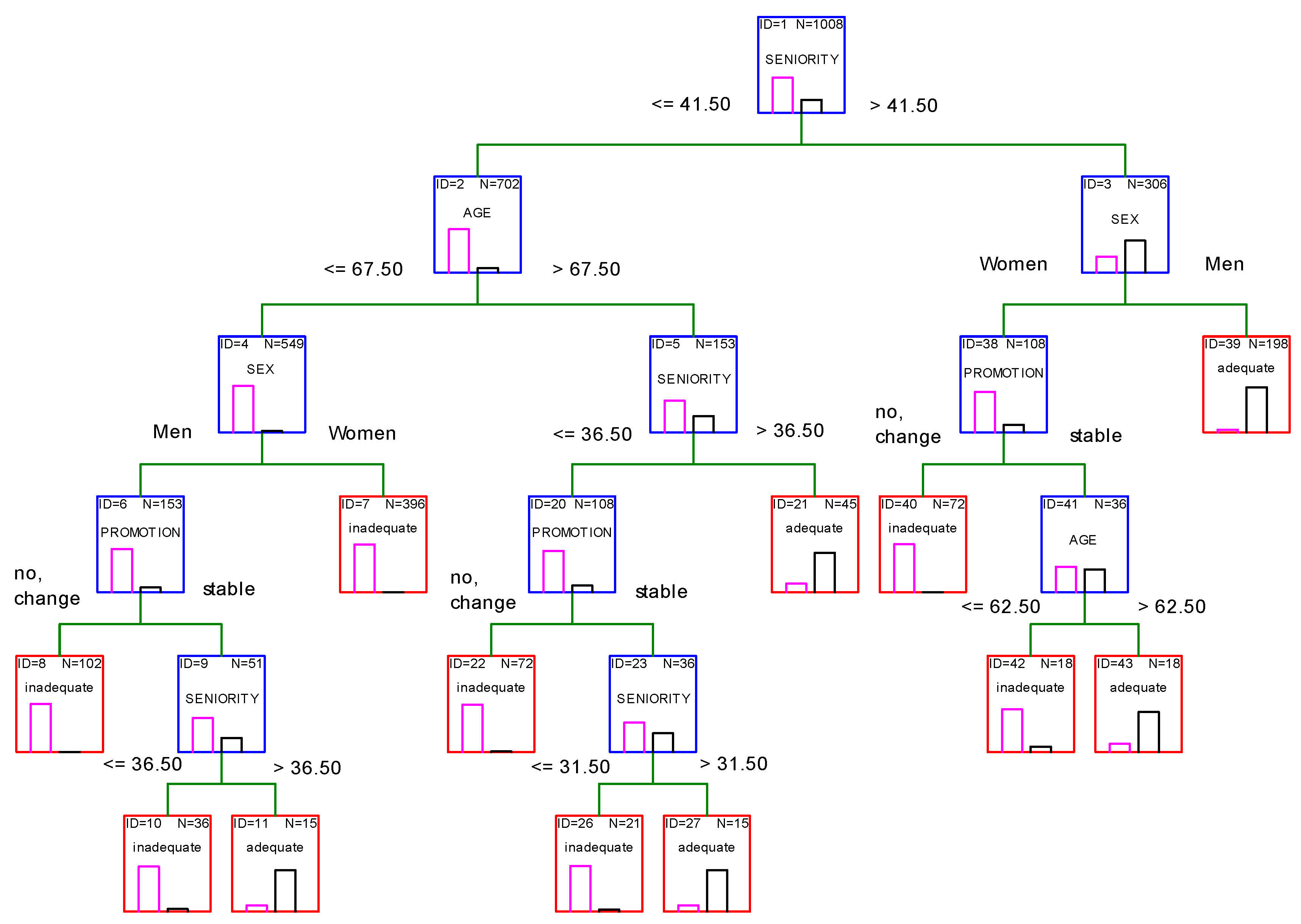

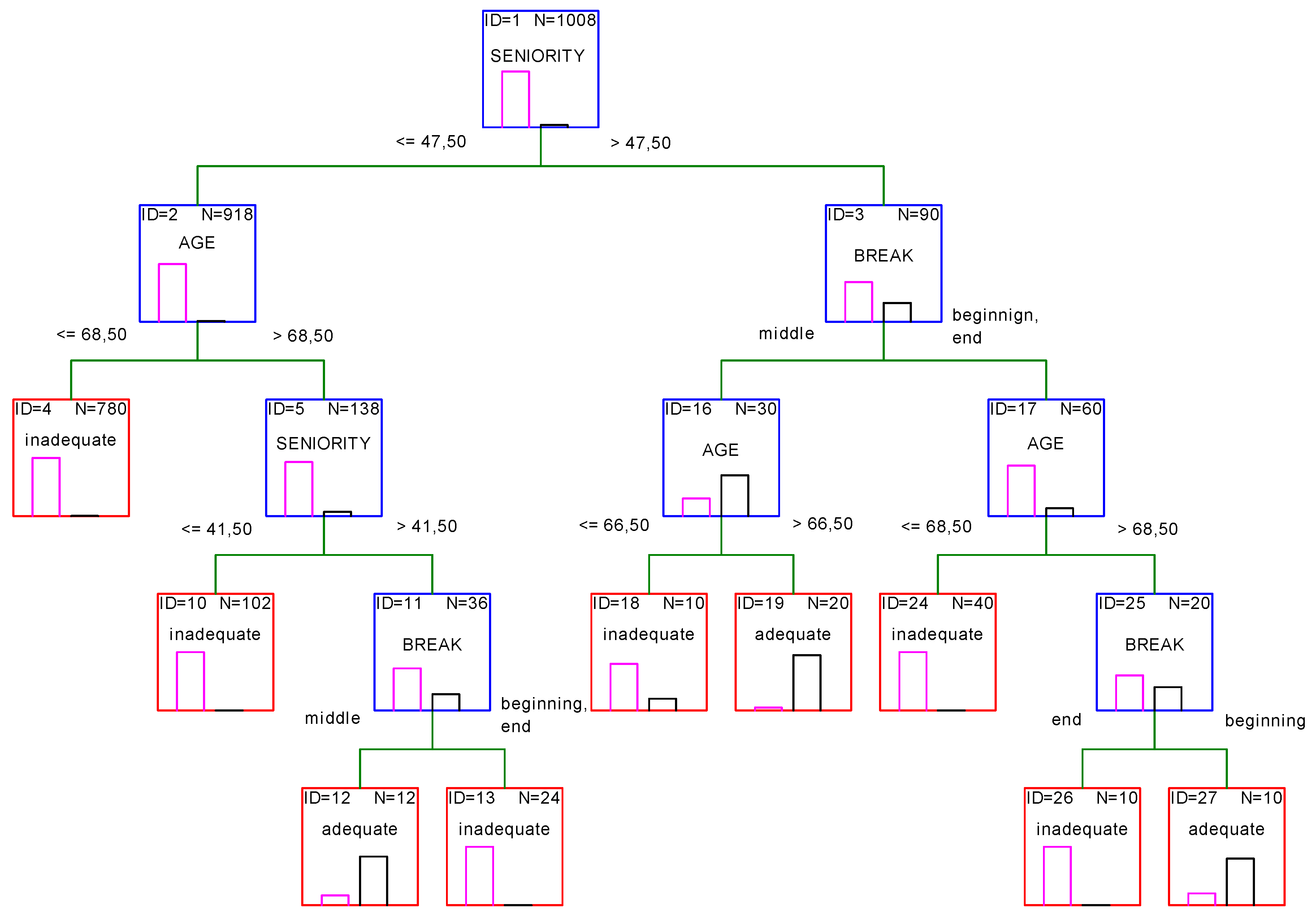

In the fourth case, an analysis of importance of breaks in the working career for an average earner is performed. Such an analysis provides detailed guidance on how to create one’s own work career to improve pension adequacy. Pension adequacy in this case is analyzed for a person, a man or a woman, who retires at the standard pensionable age (SPA) or later, i.e., 60–65 for women and 65–70 for men, after an interrupted 20–52-year career on a standard employment contract with average earnings. The break in the work career equals five years and could take place at the beginning, in the middle or at the end of the working career.

Figure 8 contains the classification tree for future pensioners with different moments of the five year-long break in the work career.

According to

Figure 8, three rules lead to an adequate pension:

Break in the middle, Seniority between 42–47 years, Age >68;

Break in the middle, Seniority >47, Age >66;

Break in the beginning, Seniority >47, Age >68.

Every kind of a break in the working career brings a decrease in the pension benefit and can lead to inadequacy. However, the break in the middle is less damaging for pension adequacy than breaks in the working career at the beginning or at the end of the working career. In this case, shorter seniority caused by the break can be replaced by a higher retirement age.

Definitely, the worst break for the level of TRR is the break at the end of the working time. This is due to the fact that at the end of the working career, we have achieved the largest cumulated capital and every lost year gives a great loss of interest in pension capital.

Our classification tree is correct due to the high level of proper classified objects equal to 99.11%.

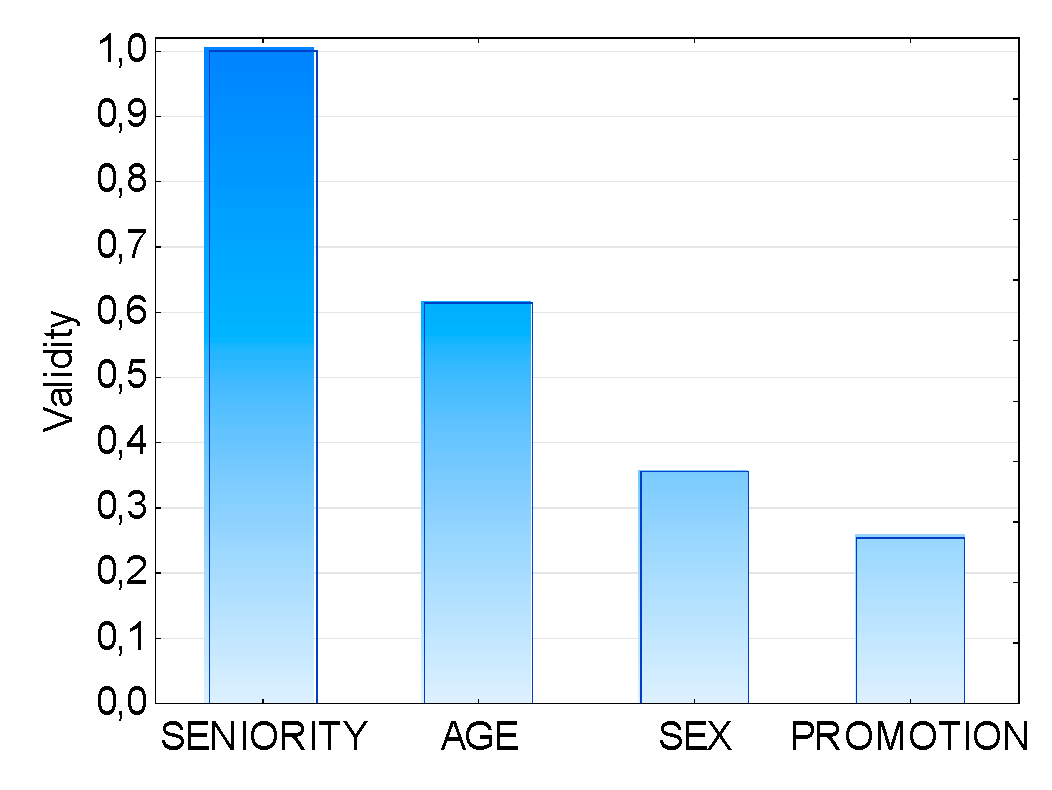

As we can see in

Figure 9, ‘break’ constitutes the most important variable for the level of pension and its adequacy. Losses can be mostly compensated for by a higher retirement age or little by seniority.

3.5. Pension Adequacy of an Earner with a Different Length of a Break in the Working Career

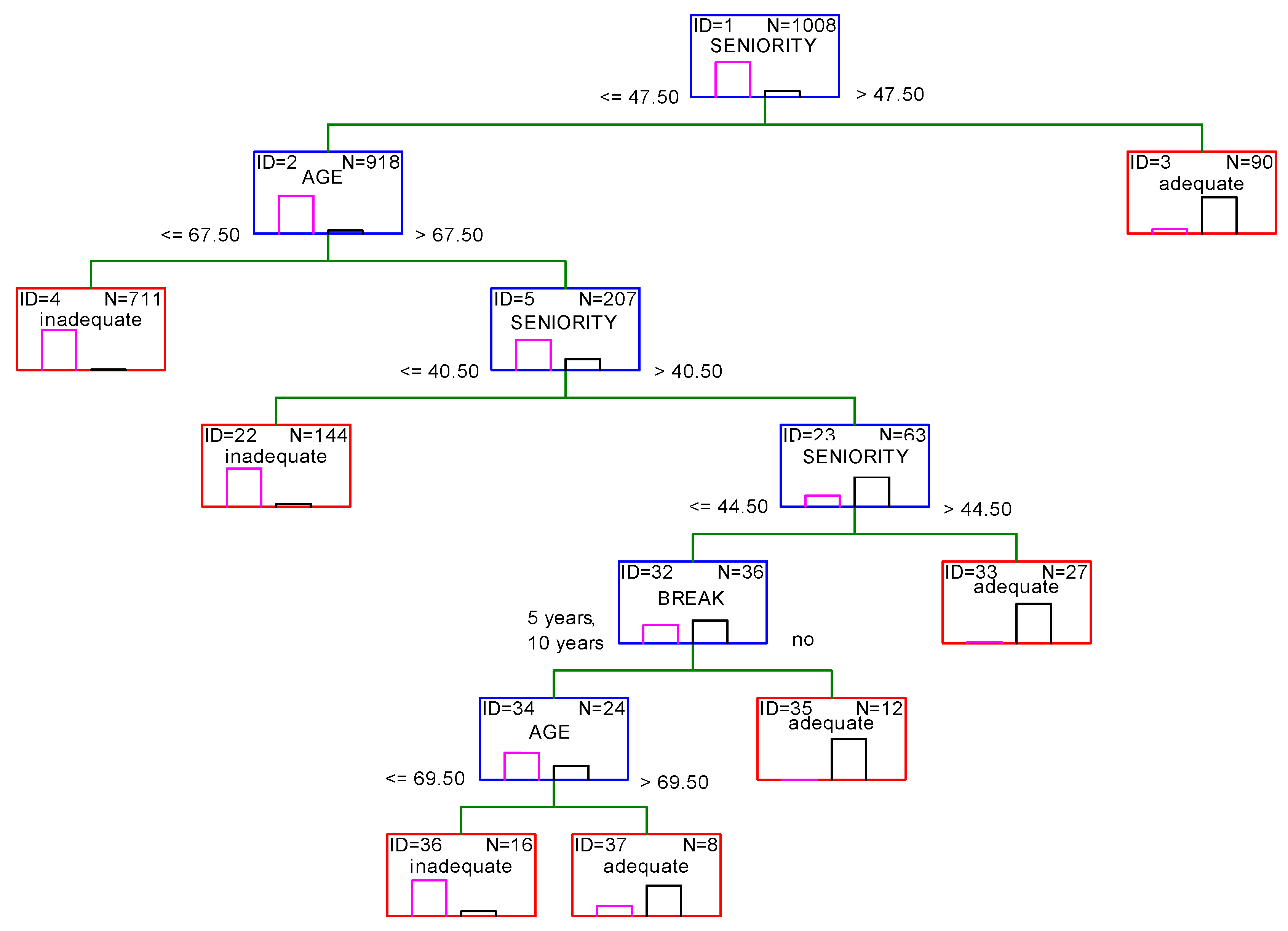

The last case investigates pension adequacy for a person, a man or a woman, who retires at the standard pensionable age (SPA) or later, i.e., 60–65 for women and 65–70 for men, after an interrupted 20–52-year career on a standard employment contract with average earnings. The break in work career is equal to 5 or 10 years and happened in the middle of the working career.

Figure 10 illustrates the classification tree for pension adequacy of earners with a different length of the break in the working career.

As we can see in

Figure 8, four rules give an adequate pension:

No break, Seniority >47 years;

No break, Seniority between 45–47 years, Age >67;

No break, Seniority between 41–44 years, Age >67;

5 or 10 years’ break, Seniority between 41–44 years, Age >69.

As in the previous case, it can be detected that every kind of break in the working career brings a decrease in the pension benefit and can lead to inadequacy. In the situation of 5 or 10 years’ break in the working career, pension adequacy can be achieved only by people with a very high retirement age and with long seniority.

In this case, 96.33% of objects is well-classified.

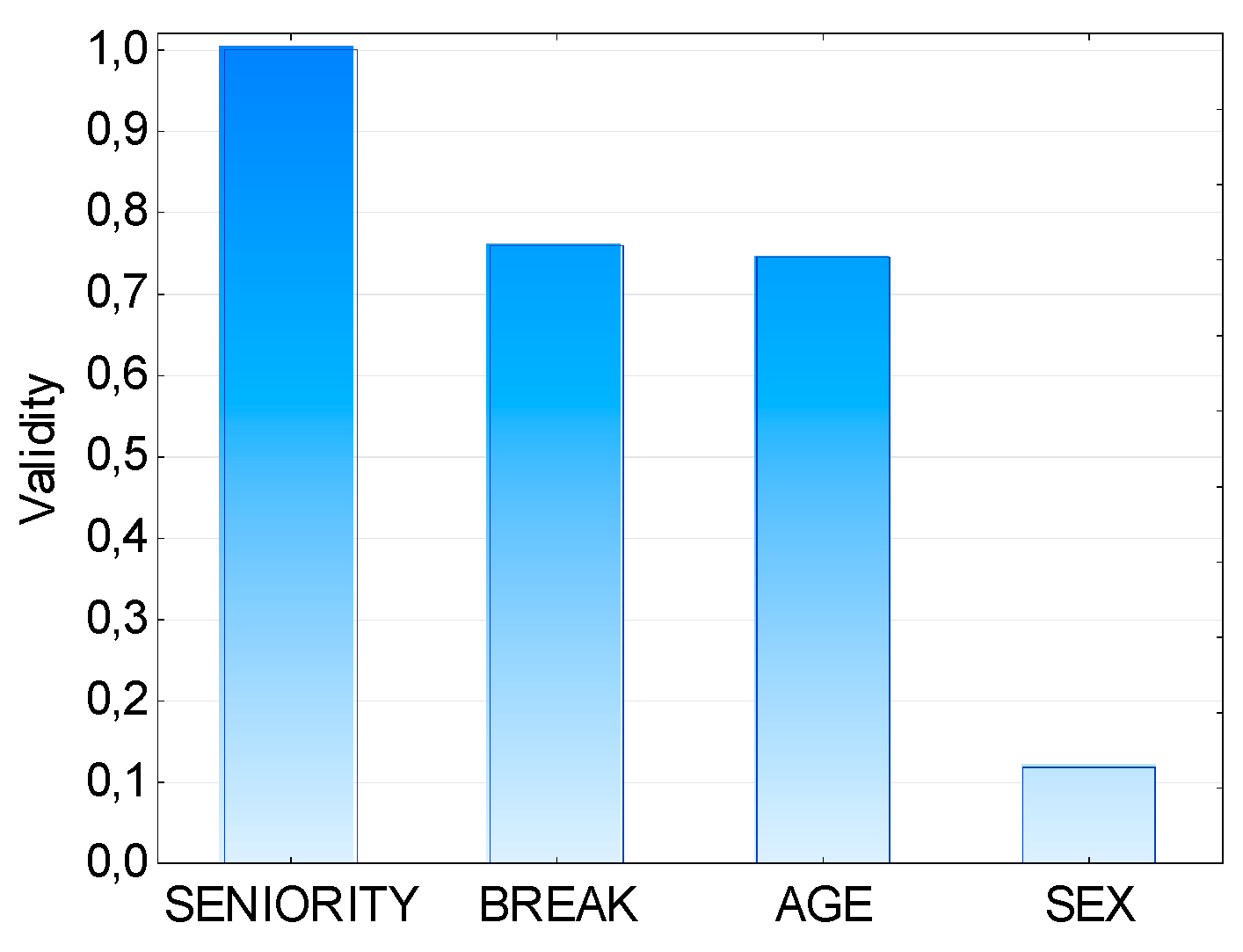

The most important variable in this case is seniority, then the time of break, and finally, the retirement age (See

Figure 11). It should be emphasized that the sex of pensioners is irrelevant in this case.

4. Conclusions

Case studies in this work provide a set of combinations of factors connected with pension adequacy. Future pensions in Poland depend on various factors, especially on wages and on the length of the working career. The conducted research has shown a strong relationship between the adequacy of pensions and earnings and seniority. Pensioners with high wages will be allowed to work shorter and to retire earlier. An individual stable promotion of earnings is also very important for the level of pensions, especially for women who have lower earnings. A number of recent research studies have confirmed the problem [

4,

31,

41]. Rules for men are less demanding, also because they will receive higher pensions due to the lower life expectancy for men at the time of retirement. The factors which should be changed in order to achieve adequate pensions are seniority and retirement age. Low wages can be compensated for by appropriately long seniority and a high retirement age. Women, according to their earnings, should make a series of decisions, especially about seniority. Future pension benefits will be significantly lower than the current ones. The results of the general trend of descending pension benefits in Poland are consistent with the findings of Chłoń-Domińczak [

30]. This means problems with an adequacy of pension and threats to the sustainability of the pension system. Flexibility of the labor market constitutes the factor that influences such a situation. This includes breaks in work as a consequence of employment on irregular contracts and breaks in paying contributions. The antidote to such problems may be a stable promotion in the salary during a work career, for example, due to an increase in qualifications. Moreover, earning a high salary will allow people to generate an adequate pension.

A solution that could mitigate the effects of the anticipated reduction in the replacement rate in the future would be to increase the amount of the contribution transferred to the second capital pillar of the Polish pension system. An increase in the contribution level from the current 2.92 % to the level of 7.3% that was planned in 1999, when the current pension system was introduced, would mean an increase in pension benefits by as much as 25 %. Unfortunately, increasing the contribution is currently impossible due to the lack of such political will. On the contrary, the importance of the capital part in the system is systematically reduced. This is due to the fact that funds are transferred from the capital part to the current needs of the pension system.

Any kind of breaks in work which are considered in the research will lead to a reduction in the level of retirement benefits and difficulties in maintaining adequacy. The most unfavorable, however, are breaks immediately before the end of work. This means that the possible finish of work several years earlier before the SPA will have very negative consequences. Therefore, people in the pre-retirement age should be particularly supported to continue working. For people who will have such a break at the beginning or in the middle of their career, it would be advisable to mention the forms of compensation for the time outside the pension system. This is the case, for example, with people who are on parental leave. In Poland, for such persons, a contribution to the pension system is paid from the level of 60% of AW. Such a relatively small State participation, for persons taking care of their children, can cause that they will be able to work out an adequate pension on their own, and therefore, in the future, it will not be necessary to spend budget money on these people. Jędrzychowska et al. [

41], report that the effects of having children may be significant for a mother 30–40 years later, when she retires. It would definitely be very beneficial for the State because of a short parental leave period in contrast to the long retirement period. Such an investment would be a significant benefit, especially for women in the future. It would also strengthen the sustainability of the pension system. Hinrichs and Jessoula [

6], found that adequate economic security in old age is likely to depend on the combination of flexibility and security mechanism on the market at employable age.

The main suggestion from the study is that even if you are unemployed or receive a low salary, you should leave at least a low contribution to the pension system. The obtained results indicate that even a small contribution, but paid regularly over a long period of time, will minimize the risk of receiving an inadequate pension benefit. Too low of a pension is a potential cost for the State, which will be forced to pay extra for such a pension throughout the entire period of its receipt by the pensioner, which in Polish conditions means about 18 years on average. Moreover, over 25% of retirees in Poland receive benefits for a period of 25–35 years, which is almost as long as their length of seniority. Hence, the suggestion to pay contributions even in the event of no income seems reasonable. The contribution period during the pension capital accumulation period will be shorter than the later potential pension subsidy period. Various sources of financing pension contributions should be sought. The first potential source are the future pensioner’s own savings. The second are State resources, managed, for example, in the case of the unemployed by appropriate funds. Finally, the third possible source of funding for contributions is the person’s last employer. This should particularly apply to people on maternity or parental leave.

It is worth adding here that the Polish pension system is already financially inefficient and requires transfers from the state budget. According to the data of the Social Insurance Institution, in 2017, it amounted to nearly PLN 41 million, i.e., 19% of the total income of the Social Insurance Fund. However, in connection with the expected decrease in the level of self-generated pension benefits by system participants, a further increase in transfers can be expected. However, they will rather aim not at providing adequate pension benefits, but only at the payment of minimum pensions. Forecasts indicate that in the next five years, ensuring the solvency of pensions will require a subsidy in the amount of PLN 44 to 85 million, depending on the forecast variant.

In Poland, solutions aimed at co-financing the Social Insurance Fund from sources used in other countries, e.g., U.S., where in some states the pension funds are supplemented with revenues from airport or bridge taxes, are not being considered. It is possible that the need for such solutions will appear in the future due to the growing deficit of the Social Insurance Fund. Meanwhile, the financial resources needed for current retirement needs are derived from the Demographic Reserve Fund established in 1999 and supported by privatization funds and transfers from Open Pension Funds, which constitute the second pillar of the Polish pension system, and whose functioning is systematically limited.

In order to prevent poverty and maintain thepre-retirement standard of living, pensioners should have to make up for the difference in income from other sources, especially from the third pillar as well. Chłoń et al. [

29] also emphasize the need to use additional sources of funding for the pension.

We should point out that the classification tree method can be successfully used for mining big databases, such as pension benefits. The decision tree and its rules provide descriptive information about the adequacy of future pensions. Classification trees help to assess the pension level in relationship to the changes in the earnings and breaks in the work career. Taking into account the factors such as the promotion of a salary during the career and wage variability, we may obtain precise rules which will help future pensioners with different career paths to make individual decisions in order to achieve adequate pensions.

It seems that there is a real need to continue to monitor an adequacy of pensions in relation to the level of earnings and the length of work career. This is especially important because of the fast increase in the labor market flexibility, which involves changes in wages and changes in the level of pension benefits based on contributions to the system. This indication can be found also in previous studies [

12]. In the pension adequacy research, it is necessary to include new variables, such as the number of children or marital status. For future studies of pension adequacy, the use of projected life tables is also recommended. It will take into account that people’s life extends, which means that future benefits will be even lower than is now anticipated, and maintaining the adequacy of pensions will be even more difficult. The threat to the sustainability of the pension system will therefore be much greater. According to OECD [

20], against dealing with the challenges of ageing societies, working longer will be crucial to maintaining pension adequacy and financial sustainability. Next, it is worth examining pension adequacy in countries with different pension systems, while crucially differing in the level of state and market influences on pensions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}