Accountability through Environmental and Social Reporting by Wind Energy Sector Companies in Spain

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

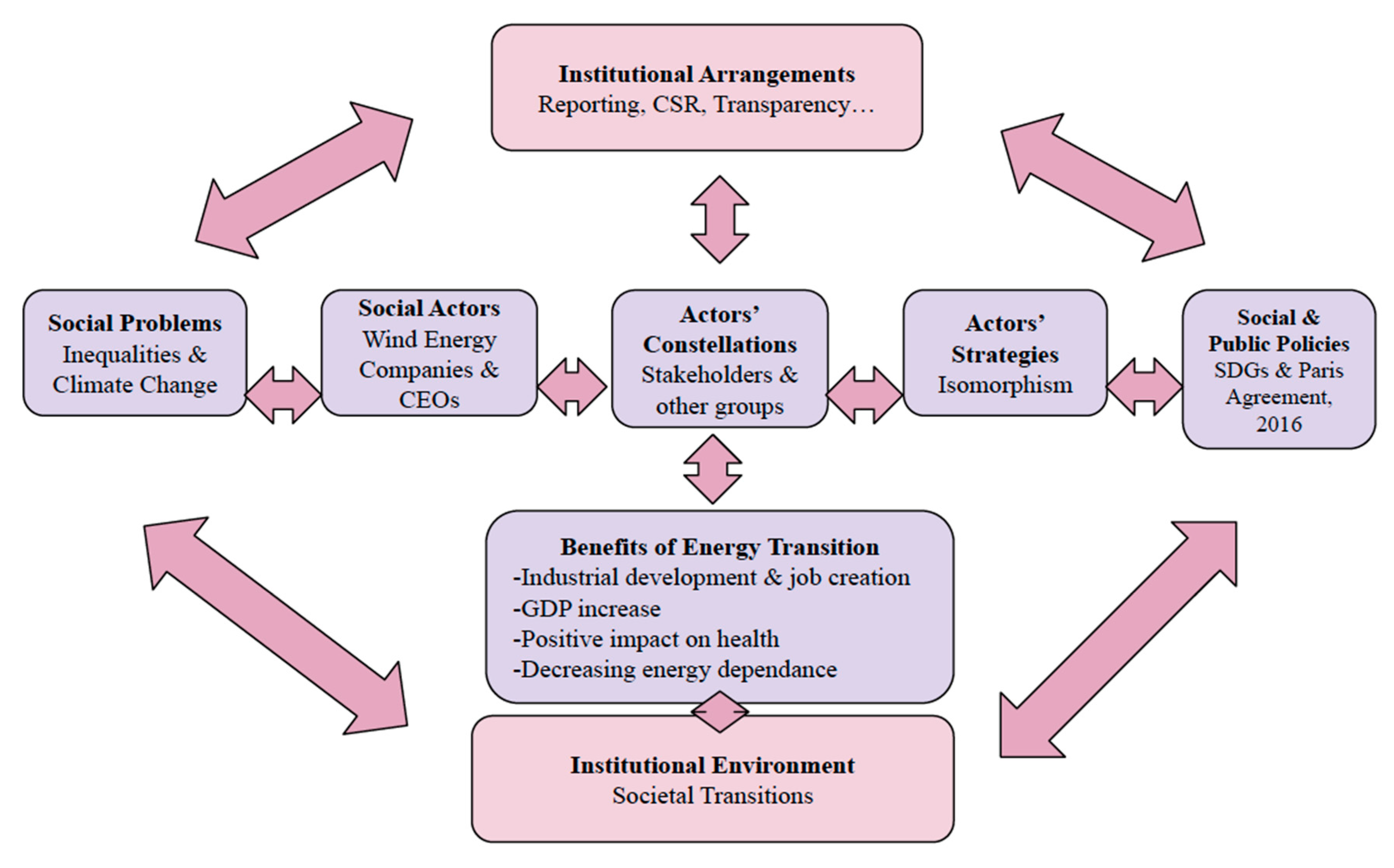

1. Introduction

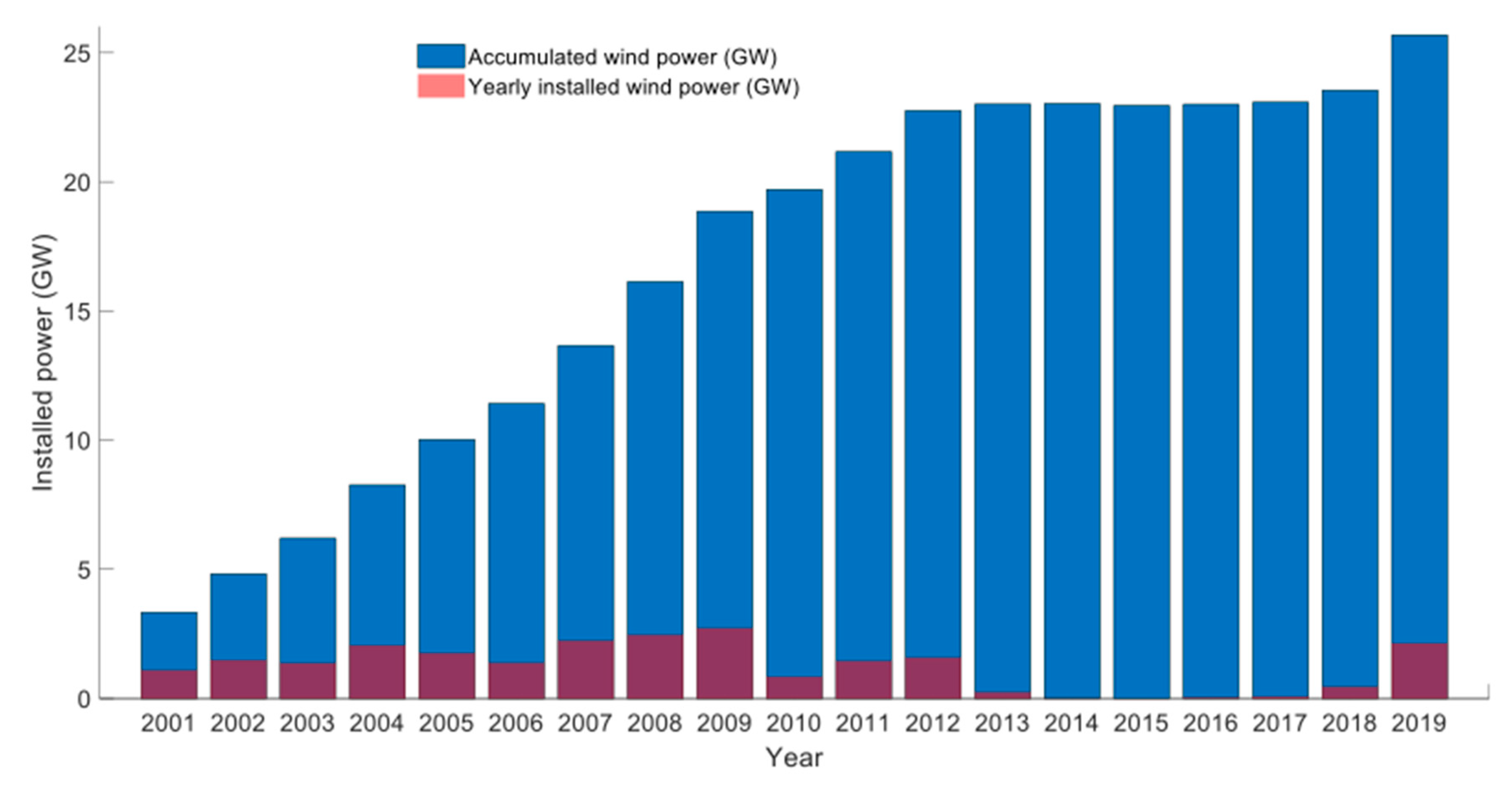

2. Context

“renewables have played a central role in this transformation, with 298 GW added to the power sector since 1995. And wind energy has been the largest single contributor, with 182 GW of capacity installed as of the end of June 2018. Wind energy now accounts for 12% of Europe’s electricity and renewables in total account for 30%”.

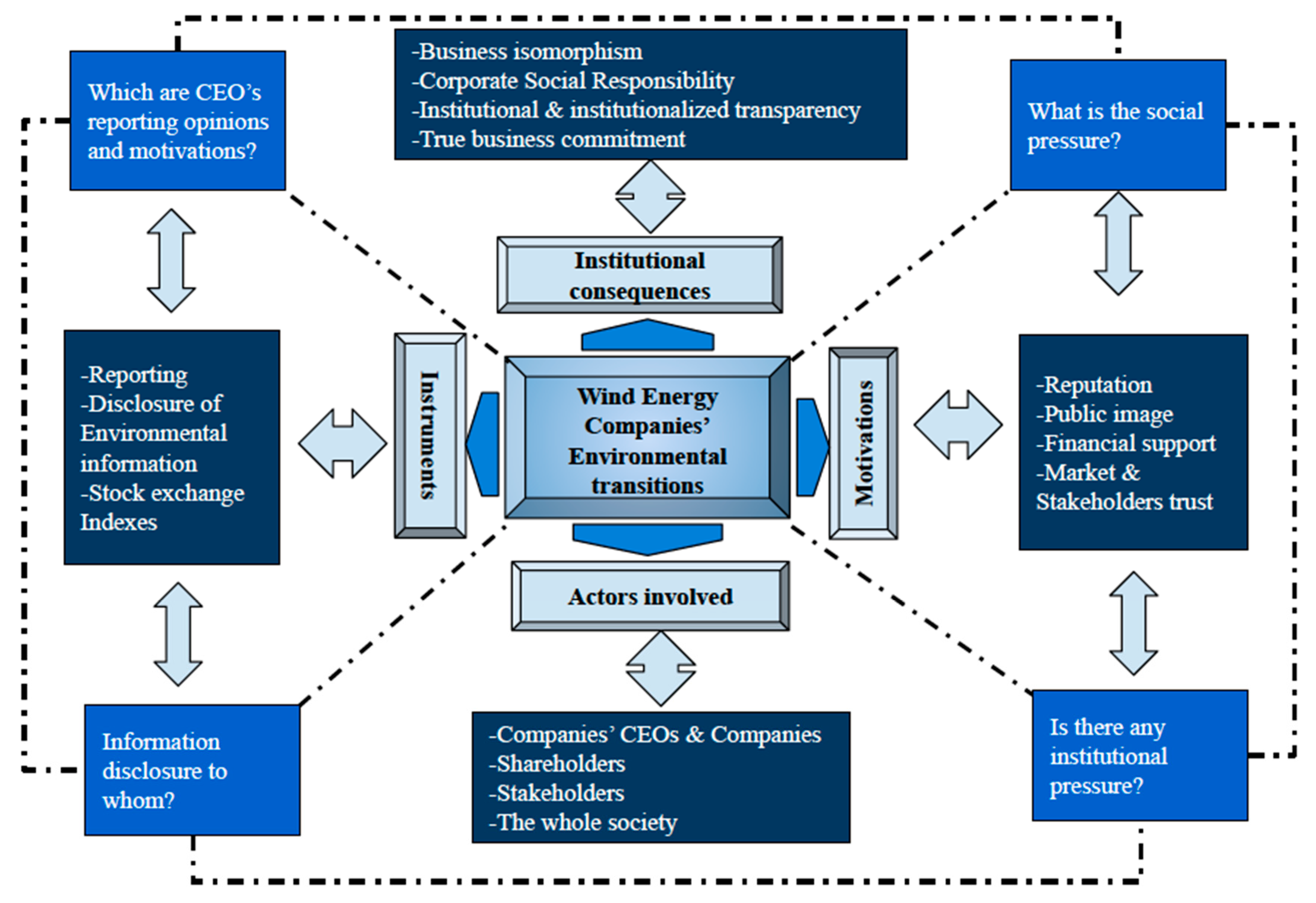

3. Method

4. Results and Discussion

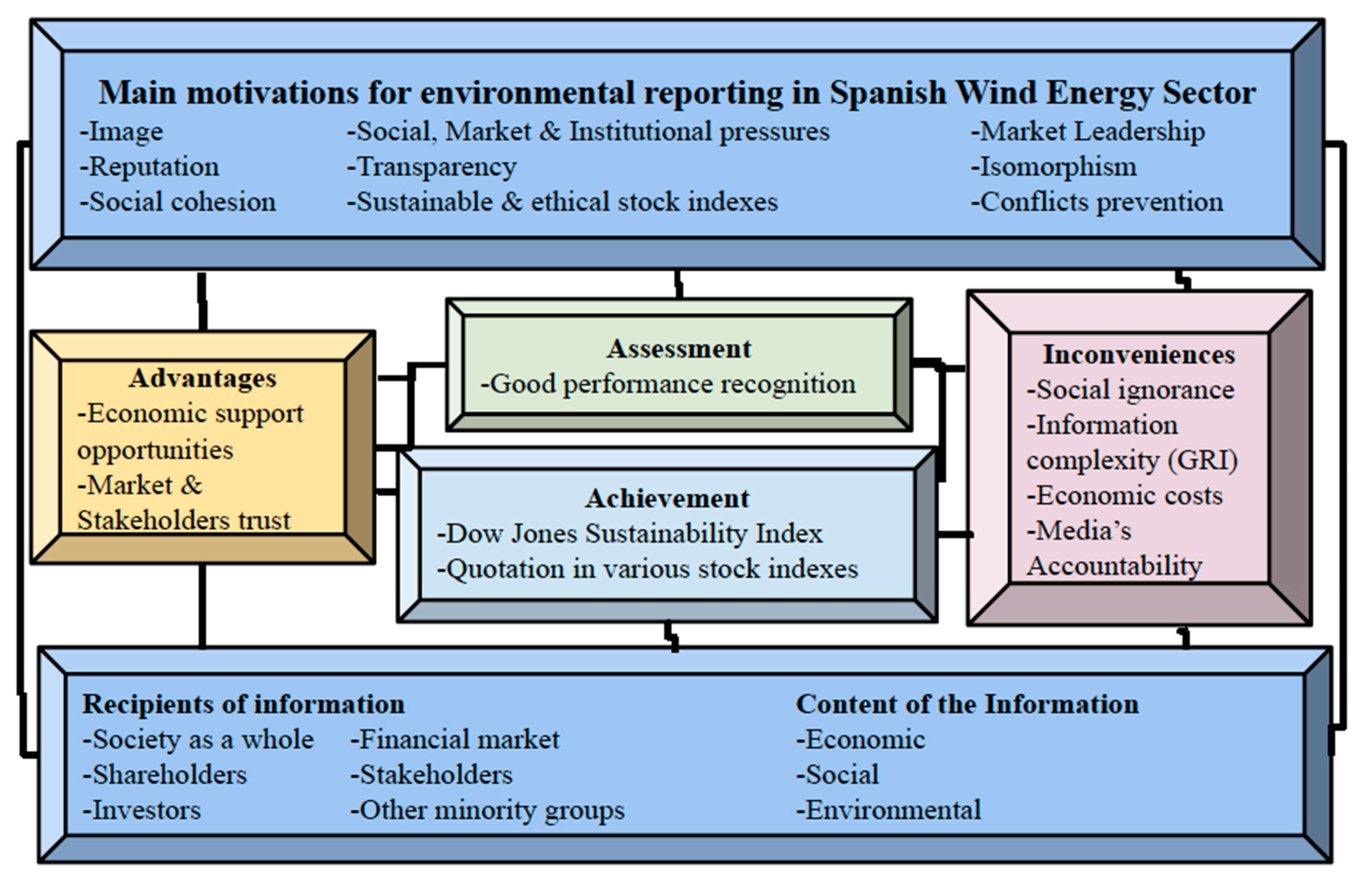

4.1. Motivations for Environmental Reporting

4.1.1. Motivations

A: The main reason is transparency, it is considered as a sign of corporate identity and the environmental variable becomes a strategic element to create and promote improvement and innovation projects.

B: To avoid future problems, to collect problems from all the groups involved and anticipate them. Reporting is essential. What it does not count, it does not exist. Prestige and status facilitate financing access and investment opportunities.

4.1.2. Realization

A: We believe that quoting in this prestigious index means achieving public recognition of the company’s commitment to sustainability within the international community of analysts and investors.

B: What we’ve done is what we disclose. But the objective is not to offer information to quote in DJSI. It is another public recognition for doing things well.

4.1.3. Assessment

A: It is a public recognition of the commitment to sustainability by the analysts and investors community. Our Co. has been in quoting since the beginning and in 2012 was chosen as the best one.

B: At the corporate level, campaigns are promoted to reinforce the image of the Company, as other companies also do. Decisions are taken at the corporate level and the image of taking advantage of the resources that were already available.

4.1.4. Advantages

A: […] is an index that measures sustainability in the short and long term. Results influence investment decisions taken by investment managers. Internally, this evaluation provides quantitative indicators that allow the evolution of different areas to be monitored.

B: […] The image of the company has been reinforced and this translates into economic repercussions. Internally to inform the whole world about what is being done in the Company and to promote Benchmarking practices.

4.1.5. Disadvantages

A: Needs media coverage, the general public is unaware of the importance of listing on this index.

B: […] It is not very clear at the internal level how this has impacted. Perhaps it is not enough to publish a lot of information, but it should be easily understandable.

4.1.6. Recipients of the Information

A: Formally, this information is addressed to the “interest groups” of the Company, because they are the ones interested in knowing the activities carried out by the company and their consequences, although, in practice, not all of them dedicate the same attention to it: currently, the most interested groups are investment analysts, with particular relevance to those who work with socially responsible investment.

B: Outward, academics, investors, DJSI, and inward to inform the whole world of what is being done… Fundamentally for the DJSI, investors, auditors, but at the user level, it is not clear…

4.2. Contents of Environmental Information

A: Currently, it is generally accepted that companies must take into account not only their economic results but also environmental and social impacts when carrying out their activities.

B: It is essential to collect and tell society what is being done in the company, what is not counted does not exist.

A: It is generally accepted that companies must take into account their economic, environmental and social impacts when carrying out their activities, society demands that it should be explained how these impacts are being taken into account… We believe that the environmental and social dimensions are acquiring greater prominence and on the way to the relevance of relevance with financial information…

B: […] Doing things well has an economic answer behind… Quoting in prestigious indexes is translated into economic advantages.

Reporting Standard

A: It is a well-valued international standard, it allows stakeholders to evaluate the progress done by companies in this field and it is compatible with independent external verification. It is a solid base to elaborate information with important attributes such as truthfulness and credibility. It reflects the commitment of the organization with the groups of interest.

B: […] It follows the same process that you have with the certifications, it’s something voluntary. It is done because other companies in the sector are also doing it. The parameters are increasingly demanding, and if we can go ahead better. The GRI guidelines and standard has been chosen because it is the most worldwide recognized and used and it is easier to make comparison and verification… To certify what I am doing and what I am proposing gives me an international acknowledgment.

A: Society demands that it should be explained how companies are taken into account its claims and public information is a good tool for this purpose.

B: It is reported because you have to do things well. The parameters are increasingly demanding, and if we can go ahead better for everybody. Sometimes minimums are set even in places where there is nothing. […] It tries to respond to regulatory and compulsory requirements but it also goes further.

A: The awareness of the importance of promoting sustainable development has reached all areas of society. From NGOs, Public Administrations, clients, and society in general, more responsible behavior is demanded taking care of the environment and our organization has tried to respond to these demands of all its stakeholders.

B: What happens is that sometimes the effort made by the companies does not reach the knowledge of the people in the street. Especially if we are talking about large companies. In some cases, they can have their problems and people only realize about the problems and not with the good actions taken and the progress done.

4.3. Economic-Financial Consequences of the Disclosure of Environmental Information

A: The emissions reduction is ratified with the commitment of the company for the use of the cleanest generation technologies, especially wind energy, considered today as the world leader among renewable energies. The effort done in this field has yielded us several awards in prestigious indexes.

B: The whole issue of investment in cleaner technologies has been a breakthrough. There will come a time when this energy will be much more mature. Over time it will occur even more efficiently.

A: We believe that the dissemination of environmental information promotes knowledge about environmental issues and a tendency to multiply the interest in these matters, so those concepts that were previously ready just for experts now are already part of the baggage of general society.

B: Showing the efficiency generated is very useful. It is an advantage in market competitiveness, where obtaining economic results doing things well is essential. When it comes to seeking support and funding it is essential to tell what is done.

A: It has reached a level of demand from which there is no going back regardless of the economic cycle in which we have to carry out our business. Environmental and social requirements are reaching the same relevance as the economic ones.

B: Accessing financing is increasingly being more difficult and is more demanding in environmental issues. This reinforces responsible behaviors on the part of the companies and encourages them to continue working in that line although getting money is becoming more and more complicated.

5. Conclusions and Policy Implications

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Parsons, T. El Sistema Social; Alianza Editorial: Madrid, Spain, 1951. [Google Scholar]

- Sutton, F.X.; Selznick, P. Leadership in Administration: A Sociological Interpretation. Am. Sociol. Rev. 1958, 23, 98. [Google Scholar] [CrossRef]

- Scott, W.R.; Christensen, S. In the Institutional Construction of Organizations: International and Longitudinal Studies; Sage: Thousand Oaks, CA, USA, 1995. [Google Scholar]

- DiMaggio, P.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147. [Google Scholar] [CrossRef]

- Jessop, A.; Wilson, N.; Bardecki, M.; Searcy, C. Corporate Environmental Disclosure in India: An Analysis of Multinational and Domestic Agrochemical Corporations. Sustainability 2019, 11, 4843. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W. The New Institutionalism in Organizational Análisis; Powell, W., DiMaggio, P.J., Eds.; University of Chicago Press: Chicago, IL, USA, 1991. [Google Scholar]

- Zucker, L.G. Institutional theories of organizations. Annu. Rev. Sociol. 1987, 13, 443–464. [Google Scholar]

- Scharpf, F.W. Institutions in Comparative Policy Research. Comp. Polit. Stud. 2000, 33, 762–790. [Google Scholar] [CrossRef]

- Sanz-Hernández, A.; Sanagustín-Fons, M.V.; Rodríguez, M.E.L. A transition to an innovative and inclusive bioeconomy in Aragon, Spain. Environ. Innov. Soc. Transit. 2019, 33, 301–316. [Google Scholar] [CrossRef]

- Fazzini, M.; Maso, L.D. The value relevance of “assured” environmental disclosure. Sustain. Account. Manag. Policy J. 2016, 7, 225–245. [Google Scholar] [CrossRef]

- Mason, M. Transparency for Whom? Information Disclosure and Power in Global Environmental Governance. Glob. Environ. Politics 2008, 8, 8–13. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M.; Magnan, M. Corporate environmental disclosure: Contrasting management’s perceptions with reality. J. Bus. Ethics 2004, 49, 143–165. [Google Scholar]

- Pucheta-Martínez, M.C.; López-Zamora, B. Engagement of directors representing institutional investors on environmental disclosure. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1108–1120. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I. What Do Stakeholders Care About? Investigating Corporate Social and Environmental Disclosure in China. J. Bus. Ethics 2015, 144, 169–184. [Google Scholar] [CrossRef]

- Scharpf, F.W. Games Real Actors: Actor-Centered Institutionalism in Policy Research; Routledge: New York, NY, USA, 1997. [Google Scholar]

- Scharpf, F.W. Games Real Actors Play: Actor-Centered Institutionalism in Policy Research; Routledge: New York, NY, USA, 2018. [Google Scholar]

- De Aguiar, T.R.; Fearfull, A.; Sanagustín-Fons, M.V. Calculating the carbon footprint: Implications for governing emissions and gender relations. Account. Forum 2016, 40, 63–77. [Google Scholar] [CrossRef]

- Brown, M.T.; Ulgiati, S. Emergy evaluations and environmental loading of electricity production systems. J. Clean. Prod. 2002, 10, 321–334. [Google Scholar] [CrossRef]

- Kim, S.-H. Evaluation of negative environmental impacts of electricity generation: Neoclassical and institutional approaches. Energy Policy 2007, 35, 413–423. [Google Scholar] [CrossRef]

- Saidur, R.; Rahim, N.A.; Islam, R.; Solangi, K.H. Environmental impact of wind energy. Renew. Sustain. Energy Rev. 2011, 15, 2423–2430. [Google Scholar] [CrossRef]

- Bebbington, J.; Unerman, J.; Parker, L. Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research. Account. Audit. Account. J. 2018, 31, 2–24. [Google Scholar] [CrossRef]

- United Nations Global Compact (UNGC). The SAGE Encyclopedia of Business Ethics and Society; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- KPMG. El Camino por Recorrer. Estudio KPMG sobre Reporting de Responsabilidad Corporativa 2017; Resumen ejecutivo con datos de España; KPMG International: Amstelveen, The Netherlands, 2017. [Google Scholar]

- Yusoff, H.; Othman, R.; Yatim, N. Culture and Accountants’ Perceptions of Environmental Reporting Practice. Bus. Strat. Environ. 2013, 23, 433–446. [Google Scholar] [CrossRef]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development. 2015. Available online: https://sustainabledevelopment.un.org/sdgs (accessed on 15 January 2019).

- Starik, M.; Kanashiro, P. Toward a Theory of Sustainability Management. Organ. Environ. 2013, 26, 7–30. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Red Eléctrica Española. Las Energías Renovables en el Sistema Eléctrico Español; REE: Madrid, Spain, 2017; p. 2. [Google Scholar]

- Miguel, G.S.; Del Río, P.; Hernández, F. An update of Spanish renewable energy policy and achievements in a low carbon context. J. Renew. Sustain. Energy 2010, 2, 31007. [Google Scholar] [CrossRef]

- Payan, M.B.; Roldan-Fernandez, J.M.; Garcia, A.L.T.; Bermúdez-Ríos, J.M.; Riquelme-Santos, J.M. Costs and benefits of the renewable production of electricity in Spain. Energy Policy 2013, 56, 259–270. [Google Scholar] [CrossRef]

- Pedraza, J.M. Electrical Energy Generation in Europe The Current and Future Role of Conventional Energy Sources in the Regional Generation of Electricity; Springer: Berlin/Heidelberg, Germany, 2015; p. 3. [Google Scholar] [CrossRef]

- Jacobs, D. Renewable Energy Policy Convergence in the EU: The Evolution of Feed-in Tariffs in Germany, Spain and France; Routledge: London, UK, 2016. [Google Scholar]

- Wind Europe. Wind Energy in Europe in 2018. Trends and Statistics. 2018. Available online: https://windeurope.org/about-wind/statistics/ (accessed on 10 January 2020).

- Muñoz, C.Q.G.; García Márquez, F.P. “Wind Energy Power Prospective”. In Renewable Energies. Business Outlook 2050; Springer International Publishing AG: Berlin/Heidelberg, Germany, 2018; p. 83. [Google Scholar] [CrossRef]

- Fischer, K.; Besnard, F.; Bertling, L. Reliability-Centered Maintenance for Wind Turbines Based on Statistical Analysis and Practical Experience. IEEE Trans. Energy Convers. 2012, 27, 184–195. [Google Scholar] [CrossRef]

- Saenz De Miera, G.S.; González, P.D.R.; Vizcaíno, I. Analysing the impact of renewable electricity support schemes on power prices: The case of wind electricity in Spain. Energy Policy 2008, 36, 3345–3359. [Google Scholar] [CrossRef]

- European Commission. Energy Roadmap 2050; Publications Office of the European Union: Luxembourg, 2012. [Google Scholar]

- Wustenhagen, R.; Wolsink, M.; Bürer, M.J. Social acceptance of renewable energy innovation: An introduction to the concept. Energy Policy 2007, 35, 2683–2691. [Google Scholar] [CrossRef]

- Kardooni, R.; Yusoff, S.; Kari, F.B. Renewable energy technology acceptance in Peninsular Malaysia. Energy Policy 2016, 88, 1–10. [Google Scholar] [CrossRef]

- Buritt, R.L.; Lehman, G. The body shop windfarm-an analysis of accountability and ethics. Br. Account. Rev. 1995, 27, 167–186. [Google Scholar]

- IEA Wind. Social Acceptance of Wind Energy Projects Expert Group Summary on Recommended Practices. 2013. Available online: https://community.ieawind.org/search?executeSearch=true&SearchTerm=task+28&l=1: (accessed on 28 December 2019).

- Allen, A.; Zhang, Y.; Hodge, B.-M. Impact of Increasing Distributed Wind Power and Wind Turbine Siting on Rural Distribution Feeder Voltage Profiles. In Proceedings of the International Workshop on Large-Scale Integration of Wind Power into Power Systems as Well as on Transmission Networks for Offshore Wind Power Plants, London, UK, 22–24 October 2013. [Google Scholar]

- Ruiz Olabuenaga, J.I. Metodología de la Investigación Cualitativa; Deusto: Bilbao, Spain, 2003. [Google Scholar]

- Taylor, S.; Bogdan, R. Introducción a los Métodos Cualitativos de Investigación; Paidós: Barcelona, Spain, 1984. [Google Scholar]

- Moseñe, J.A.; Burritt, R.L.; Sanagustín-Fons, M.V.; Moneva, J.M.; Tingey-Holyoak, J. Environmental reporting in the Spanish wind energy sector: An institutional view. J. Clean. Prod. 2013, 40, 199–211. [Google Scholar] [CrossRef]

- Vallés, M. Técnicas Cualitativas de Investigación Social. Reflexión Metodológica y Práctica Profesional; Síntesis: Madrid, Spain, 1997. [Google Scholar]

- Asociación Empresarial Eólica. Informe Annual 2018. Available online: https://www.aeeolica.org/anuario/2018/ (accessed on 12 January 2019).

- Mattley, C.; Strauss, A.; Corbin, J. Grounded Theory in Practice. Contemp. Sociol. A J. Rev. 1999, 28, 489. [Google Scholar] [CrossRef]

- Cárcamo, H. Hermenéutica y Análisis Cualitativo. Rev. Epistemol. Cienc. Soc. 2005, 23, 204–216. [Google Scholar]

- Blanco-Gregory, R.; Martínez-Quintana, V.; Sanagustín-Fons, M.V. Microemprendimientos en agricultura ecológica y mercado slow food. RIO Int. J. Organ. 2020, 24, 159. [Google Scholar] [CrossRef]

- Archel, P.; Lizarraga, F. Algunos determinantes de la información medioambiental divulgada por las empresas españolas cotizadas. Rev. Contab. 2001, 4, 129–153. [Google Scholar]

- Brown, H.S.; De Jong, M.; Levy, D.L. Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. J. Clean. Prod. 2009, 17, 571–580. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M. Some determinants of social and environmental disclosures in New Zealand companies. Accounting, Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- García-Ayuso, M.; Larrinaga, C. Environmental Disclosure in Spain: Corporate Characteristics and Media Exposure. Rev. Esp. Financ. Contab. 2003, 32, 184–214. [Google Scholar] [CrossRef]

- Deegan, C. Environmental disclosures and share prices—A discussion about efforts to study this relationship. Account. Forum 2004, 28, 87–97. [Google Scholar] [CrossRef]

- Lorraine, N.; Collison, D.; Power, D. An analysis of the stock market impact of environmental performance information. Account. Forum 2004, 28, 7–26. [Google Scholar] [CrossRef]

- Gupta, S.; Goldar, B. Do stock markets penalize environment-unfriendly behaviour? evidence from India. Ecol. Econ. 2005, 52, 81–95. [Google Scholar] [CrossRef]

- Correa, C.; Moneva, J.M. Contabilidad e información sobre responsabilidad social en tiempos de recesión/crisis de sostenibilidad. Span. Account. Rev. 2011, 14, 187–211. [Google Scholar] [CrossRef]

- Logsdon, J.M.; Wood, D.J. Global Business Citizenship and Voluntary Codes of Ethical Conduct. J. Bus. Ethics 2005, 59, 55–67. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Logsdon, J.M. Global Business Citizenship: Applications to Environmental Issues. Bus. Soc. Rev. 2004, 109, 67–87. [Google Scholar] [CrossRef]

- Kolk, A. Sustainability, accountability and corporate governance: Exploring multinationals’ reporting practices. Bus. Strat. Environ. 2007, 17, 1–15. [Google Scholar] [CrossRef]

- Deegan, C.; Rankin, M. The materiality of environmental information to users of annual reports. Accounting, Audit. Account. J. 1997, 10, 562–583. [Google Scholar] [CrossRef]

- Hughes, K.E. The Value Relevance of Nonfinancial Measures of Air Pollution in the Electric Utility Industry. Account. Rev. 2000, 75, 209–228. [Google Scholar] [CrossRef]

- Mahapatra, S. Investor Reaction to a Corporate Social Accounting. J. Bus. Financ. Account. 1984, 11, 29–40. [Google Scholar] [CrossRef]

- Delgado-Márquez, B.L.; Pedauga, L.E.; Cordón-Pozo, E. Industries Regulation and Firm Environmental Disclosure: A Stakeholders’ Perspective on the Importance of Legitimation and International Activities. Organ. Environ. 2015, 30, 103–121. [Google Scholar] [CrossRef]

- Voinea, C.L.; Van Kranenburg, H. Media Influence and Firms Behaviour: A Stakeholder Management Perspective. Int. Bus. Res. 2017, 10, 23. [Google Scholar] [CrossRef]

- Global Reporting Initiative. G4 Development. Full Survey Report; Global Reporting Initiative: Amsterdam, The Netherlands, 2012. [Google Scholar]

- Freeman, R.E.; Reed, D.L. Stockholders and Stakeholders: A New Perspective on Corporate Governance. Calif. Manag. Rev. 1983, 25, 88–106. [Google Scholar] [CrossRef]

- Onkila, T. Multiple forms of stakeholder interaction in environmental management: Business arguments regarding differences in stakeholder relationships. Bus. Strat. Environ. 2010, 20, 379–393. [Google Scholar] [CrossRef]

- Burritt, R.L.; Schaltegger, S. Sustainability accounting and reporting: Fad or trend? Account. Audit. Account. J. 2010, 23, 829–846. [Google Scholar] [CrossRef]

- Gray, R.; Milne, M.J. Sustainability reporting: Who’s kidding whom? Chartered Account. J. N. Z. 2005, 81, 66–70. [Google Scholar]

- Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Brown, H.S.; De Jong, M.; Lessidrenska, T. The rise of the global reporting initiative (GRI) as a case of institutional entrepreneurship. Corp. Soc. Responsib. Initiat. Work. Pap. 2007, 18, 36. [Google Scholar] [CrossRef]

- Moneva, J.M.; Archel, P.; Correa, C. GRI and the camouflaging of corporate unsustainability. Account. Forum 2006, 30, 121–137. [Google Scholar] [CrossRef]

- Newton, A. GRI reporters; who’s fooling whom? Ethical Corp. Mag. 2004, 5, 44–47. [Google Scholar]

- Adams, C.A.; Evans, R. Accountability, Completeness, Credibility and the Audit Expectations Gap. J. Corp. Citizsh. 2004, 2004, 97–115. [Google Scholar] [CrossRef]

- Moneva, J.M. Mecanismos de verificación de la información sobre responsabilidad social corporativa. Papeles de Economía Española 2006, 108, 75–90. [Google Scholar]

- Gustafsson, V.; My, J. A study of Environmental Disclosure within the OMXS30: With reference to the Global Reporting Initiative. Master’s Thesis, Jönköping University, Jönköping, Sweden, 2017. [Google Scholar]

- Blacconiere, W.G.; Patten, D.M. Environmental disclosures, regulatory costs, and changes in firm value. J. Account. Econ. 1994, 18, 357–377. [Google Scholar] [CrossRef]

- Chan, C.C.C.; Milne, M. Investor reactions to corporate environmental saints and sinners: An experimental analysis. Account. Bus. Res. 1999, 29, 265–279. [Google Scholar] [CrossRef]

- Spicer, B.H. Market Risk, Accounting Data and Companies’Pollution Control Records. J. Bus. Financ. Account. 1978, 5, 67–83. [Google Scholar] [CrossRef]

- Werther, W.B.; Chandler, D. Strategic corporate social responsibility as global brand insurance. Bus. Horizons 2005, 48, 317–324. [Google Scholar] [CrossRef]

- Ortas, E.; Moseñe, J.A. Sustainability in times of crisis. A bet to failure or an up and coming value? evidence from the Spanish energy sector. Span. Account. Rev. 2011, 14, 299–320. [Google Scholar]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fierro, J.A.M.; Sanagustín-Fons, M.V.; Álvarez Alonso, C. Accountability through Environmental and Social Reporting by Wind Energy Sector Companies in Spain. Sustainability 2020, 12, 6375. https://doi.org/10.3390/su12166375

Fierro JAM, Sanagustín-Fons MV, Álvarez Alonso C. Accountability through Environmental and Social Reporting by Wind Energy Sector Companies in Spain. Sustainability. 2020; 12(16):6375. https://doi.org/10.3390/su12166375

Chicago/Turabian StyleFierro, José A. Moseñe, M. Victoria Sanagustín-Fons, and César Álvarez Alonso. 2020. "Accountability through Environmental and Social Reporting by Wind Energy Sector Companies in Spain" Sustainability 12, no. 16: 6375. https://doi.org/10.3390/su12166375

APA StyleFierro, J. A. M., Sanagustín-Fons, M. V., & Álvarez Alonso, C. (2020). Accountability through Environmental and Social Reporting by Wind Energy Sector Companies in Spain. Sustainability, 12(16), 6375. https://doi.org/10.3390/su12166375