The Effectiveness of Self-Sufficiency Policy: International Price Transmissions in Beef Markets

Abstract

1. Introduction

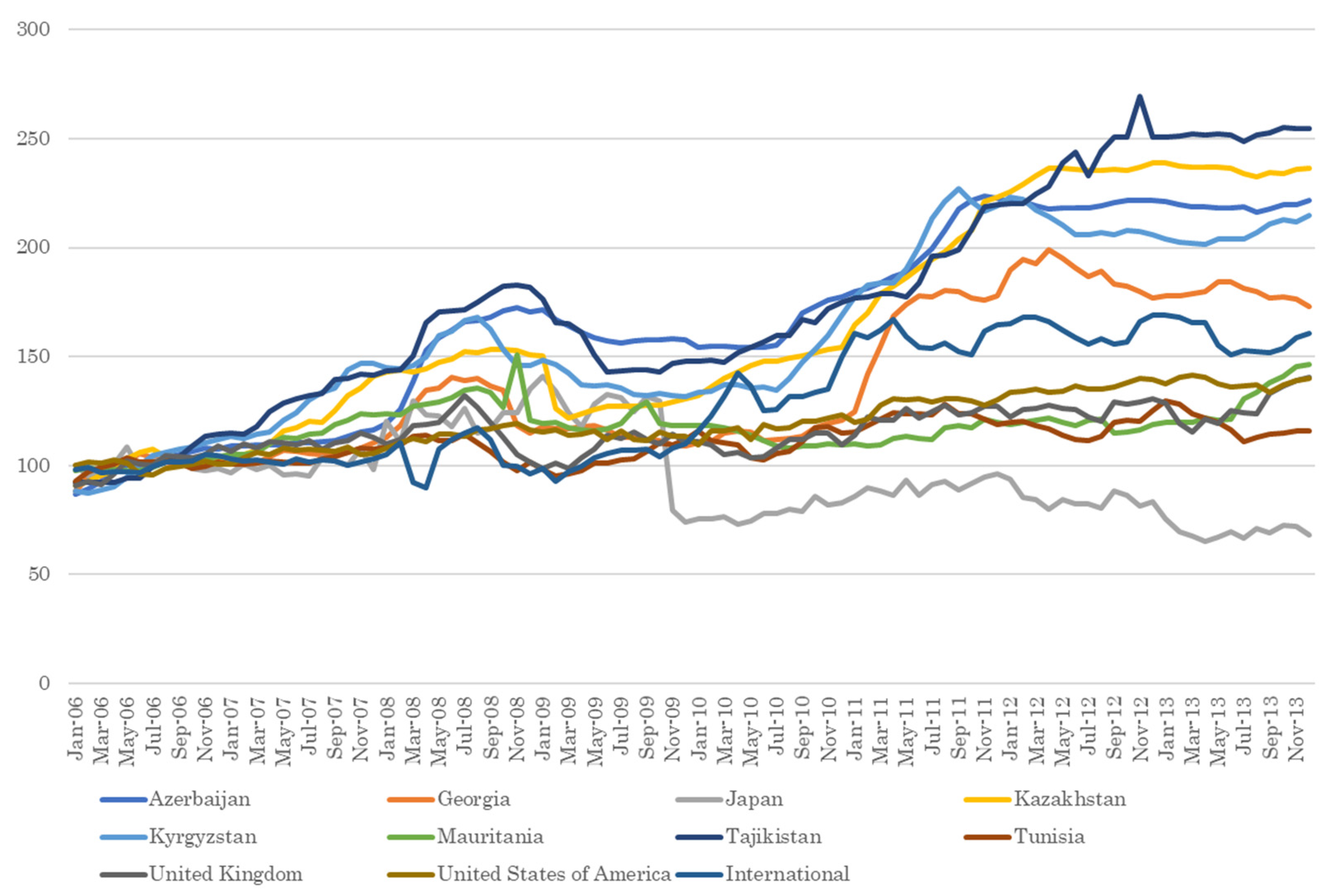

2. Data and Sample Statistics

3. Econometric Methodology

4. Empirical Results

4.1. Causal Relationships and Analysis of Lead–Lag

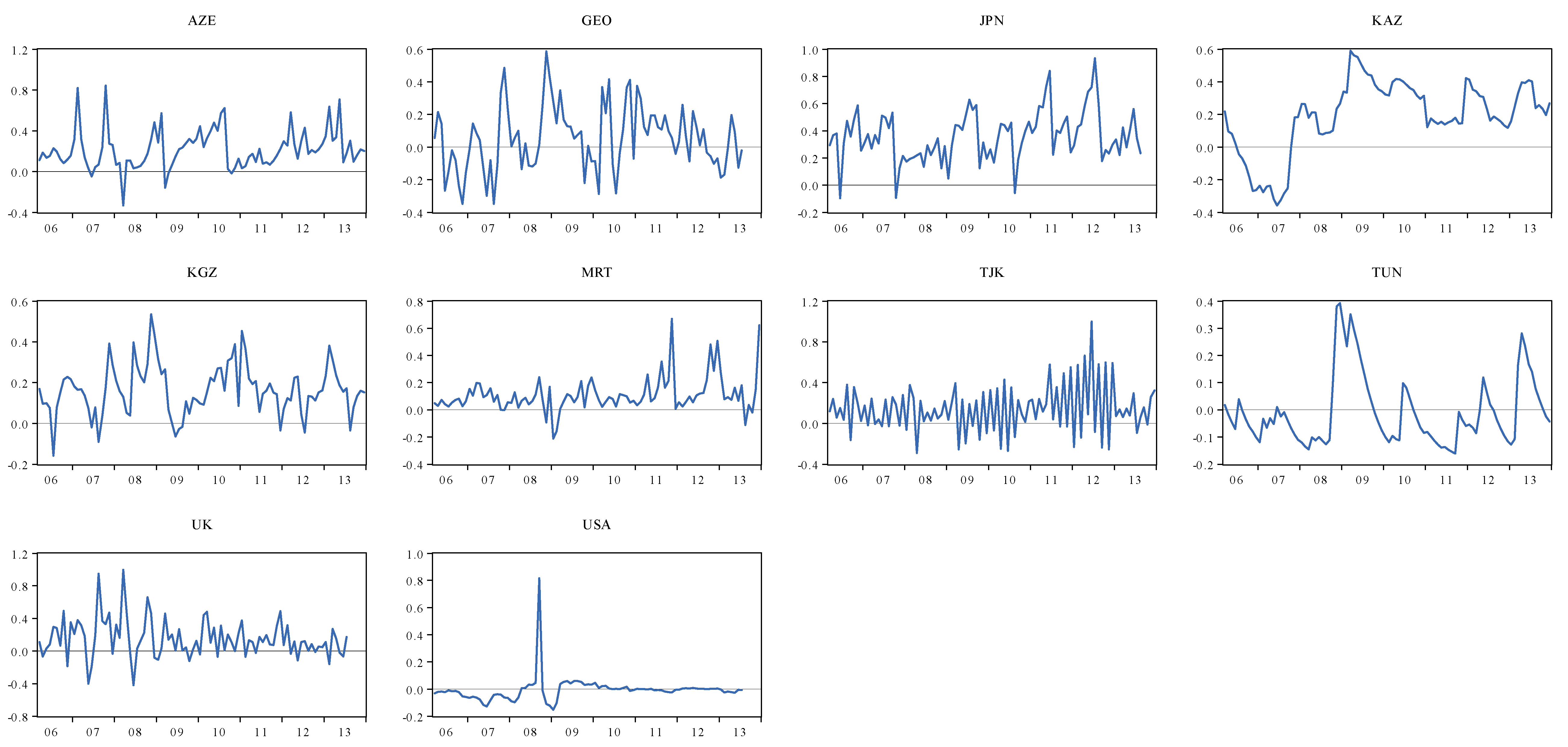

4.2. Time-Varying Dynamic Conditional Correlations

4.3. The Effect of Self-Sufficiency Rates on Dynamic Conditional Correlations

5. Discussions

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Conner, K. Is There Really a Meat Shortage? Why You’re Seeing Less Beef, Pork, and Chicken in Stores. CNET. 3 June 2020. Available online: https://www.cnet.com/health/is-there-really-a-meat-shortage-why-youre-seeing-less-beef-pork-and-chicken-in-stores/ (accessed on 10 June 2020).

- Sanjuán, A.I.; Dawson, P.J. Price transmission, BSE and structural breaks in the UK meat sector. Eur. Rev. Agric. Econ. 2003, 30, 155–172. [Google Scholar] [CrossRef]

- Lawrence, J.D.; Mintert, J.; Anderson, J.D.; Anderson, D.P. Feed grains and livestock: Impacts on meat supplies and prices. Choices 2008, 23, 11–15. [Google Scholar]

- Peterson, H.H.; Chen, Y.J. The impact of BSE on Japanese retail beef market. Agribusiness 2003, 21, 313–327. [Google Scholar] [CrossRef]

- Ishida, T.; Ishikawa, N.; Fukushige, M. Impact of BSE and bird flu on consumers’ meat demand in Japan. Appl. Econ. 2010, 42, 49–56. [Google Scholar] [CrossRef]

- Tanaka, T.; Hosoe, H.; Qiu, H. Risk Assessment of Food Supply: A Computable General Equilibrium Approach; Cambridge Scholars Publishing: Newcastle upon Tyne, UK, 2012. [Google Scholar]

- Guo, J.; Tanaka, T. Determinants of international price volatility transmissions: The role of self-sufficiency rates in wheat-importing countries. Palgrave Commun. 2019, 5, 1–13. [Google Scholar] [CrossRef]

- Tanaka, T. Agricultural self-sufficiency and market stability: A revenue-neutral approach to wheat sector in Egypt. J. Food Secur. 2018, 6, 31–41. [Google Scholar] [CrossRef]

- Tanaka, T.; Guo, J. Quantifying the effects of agricultural autarky policy: Resilience to yield volatility and export restrictions. J. Food Secur. 2019, 7, 47–57. [Google Scholar] [CrossRef]

- Tanaka, T.; Guo, J. How does the self-sufficiency rate affect international price volatility transmissions in the wheat sector? Evidence from wheat-exporting countries. Humanit. Soc. Sci. Commun. 2020, 7, 1–13. [Google Scholar] [CrossRef]

- Clapp, J. Food self-sufficiency: Making sense of it, and when it makes sense. Food Policy 2017, 66, 83–96. [Google Scholar] [CrossRef]

- Tanaka, T.; Hosoe, N. Does agricultural trade liberalization increase risks of supply-side uncertainty? Effects of productivity shocks and export restrictions on welfare and food supply in Japan. Food Policy 2011, 36, 368–377. [Google Scholar] [CrossRef]

- Bishwajit, G. Food security and food self-sufficiency in China: From past to 2050. Food Energy Secur. 2014, 3, 86–95. [Google Scholar]

- Clarete, R.L.; Adriano, L.; Esteban, A. Rice Trade and Price Volatility: Implications on ASEAN and Global Food Security. ADB Economic Working Paper Series No. 368. 2013. Available online: https://www.adb.org/sites/default/files/publication/30390/ewp-368.pdf (accessed on 20 June 2020).

- Warr, P. Food Security vs. Food Self-Sufficiency: The Indonesian Case. Crawford School Research Paper No. 2011/04. 2011. Available online: https://papers.ssrn.com/sol3/papers.cfm?.abstract_id=1910356 (accessed on 10 January 2018).

- Kouyaté, C.; von Cramon-Taubadel, S. Distance and border effects on price transmission: A meta-analysis. J. Agric. Econ. 2016, 67, 255–271. [Google Scholar] [CrossRef]

- Bakucs, L.Z.; Fertö, I. Marketing margins and price transmission on the Hungarian beef market. Food Econ. 2006, 3, 151–160. [Google Scholar]

- Fousekis, P.; Katrakilidis, C.; Trachanas, E. Vertical price transmission in the US beef sector: Evidence from the nonlinear ARDL model. Econ. Model. 2016, 52, 499–506. [Google Scholar] [CrossRef]

- Goodwin, B.K.; Holt, M.T. Price transmission and asymmetric adjustment in the U.S. beef sector. Am. J. Agric. Econ. 1999, 81, 630–637. [Google Scholar] [CrossRef]

- Pozo, V.F.; Schoroeder, T.C.; Bachmeier, L.J. Symmetric Price Transmission in the U.S. Beef Market: New Evidence from New Data. In Proceedings of the NCCC-134 Conference on Applied Commodity Price Analysis, Forecasting, and Market Risk Management, St. Louis, MO, USA, 22–23 April 2013; Available online: http://www.farmdoc.illinois.edu/nccc134 (accessed on 15 April 2020).

- Saghaian, S.H. Beef safety shocks and dynamics of vertical price adjustment: The case of BSE discovery in the U.S. beef sector. Agribusiness 2007, 23, 333–348. [Google Scholar] [CrossRef]

- Dong, X.; Waldron, S.; Brown, C.; Zhang, J. Price transmission in regional beef markets: Australia, China and Southeast Asia. Emir. J. Food Agric. 2018, 30, 99–106. [Google Scholar] [CrossRef]

- Ghoshray, A. Underlying Trends and International Price Transmission of Agricultural Commodities. In ADB Economics Working Paper Series, No. 257; Asian Development Bank: Metro Manila, Philippines, 2011. [Google Scholar]

- Ceballos, F.; Hernandez, M.A.; Minot, N.; Robles, M. Grain price and volatility transmission from international to domestic markets in developing countries. World Dev. 2017, 94, 305–320. [Google Scholar] [CrossRef]

- Guo, J.; Tanaka, T. Dynamic transmissions and volatility spillovers between global price and U.S. producer price in agricultural markets. J. Risk Financ. Manag. 2020, 3, 83. [Google Scholar] [CrossRef]

- Hatzenbuehler, P.L.; Abbott, P.C.; Abdoulaye, T. Price transmission in Nigerian food security crop markets. J. Agric. Econ. 2017, 68, 143–163. [Google Scholar] [CrossRef]

- Bekkers, E.; Brockmeier, M.; Francois, J.; Yang, F. Local food prices and international price transmission. World Dev. 2017, 96, 216–230. [Google Scholar] [CrossRef]

- Yang, L.; Cai, X.J.; Hamori, S. What determines the long-term correlation between oil prices and exchange rates? N. Am. J. Econ. Financ. 2018, 44, 140–152. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Phillips, P.C.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Kwiatkowski, D.; Phillips, P.C.B.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root. J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Newey, W.K.; West, K.D. Automatic lag selection in covariance matrix estimation. Rev. Econ. Stud. 1994, 61, 631–653. [Google Scholar] [CrossRef]

- Bauwens, L.; Laurent, S.; Rombouts, J.V. Multivariate GARCH Models: A Survey. J. Appl. Econ. 2006, 21, 79–109. [Google Scholar] [CrossRef]

- Guo, J. Causal relationship between stock returns and real economic growth in the pre- and post-crisis period: Evidence from China. Appl. Econ. 2014, 47, 12–31. [Google Scholar] [CrossRef]

- Basher, S.A.; Sadorsky, P. Hedging emerging market stock prices with oil, gold, VIX and bonds: A comparison between DCC ADCC and GO-GARCH. Energy Econ. 2016, 54, 235–247. [Google Scholar] [CrossRef]

- Guo, J. Co-movement of international copper prices, China’s economic activity and stock returns: Structural breaks and volatility dynamics. Glob. Financ. J. 2018, 36, 62–77. [Google Scholar] [CrossRef]

- Nelson, D. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Hong, Y. A test for volatility spillover with applications to exchange rates. J. Econom. 2001, 103, 183–224. [Google Scholar] [CrossRef]

- Engle, R.F. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroscedasticity models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Cappiello, L.; Engle, R.F.; Sheppard, K. Asymmetric correlations in the global equity and bond returns. J. Financ. Econ. 2006, 4, 537–572. [Google Scholar] [CrossRef]

- David, L.B.; Amir, R. Stocks and bonds during the gold standard. Econ. Lett. 2017, 159, 119–122. [Google Scholar]

- Hansen, P.R.; Lunde, A. A forecast comparison of volatility models: Does anything beat a GARCH (1,1)? J. Appl. Econ. 2005, 20, 873–889. [Google Scholar] [CrossRef]

- Tamakoshi, G.; Hamori, S. Causality-in-variance and causality-in-mean between the Greek sovereign bond yields and Southern European banking sector equity returns. J. Econ. Financ. 2014, 38, 627–642. [Google Scholar] [CrossRef]

- Ljung, G.M.; Box, G.E.P. On a measure of lack of fit in time series models. Biometrika 1978, 65, 297–303. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Econometric Analysis of Cross-Section and Panel Data; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Pesaran, M.H. General Diagnostic Tests for Cross-Section Dependence in Panels. In Cambridge Economics Working Paper No. 0435; Cambridge University: Cambridge, UK, 2004. [Google Scholar]

- Baltagi, B.H. Simultaneous equations with error components. J. Econom. 1981, 17, 189–200. [Google Scholar] [CrossRef]

- Beck, N.; Katz, J.N. What to do (and not to do) with time series cross-section data. Am. Political Sci. Rev. 1995, 89, 634–647. [Google Scholar] [CrossRef]

- Kaneko, K.; Sieg, L.; Polansek, T. For U.S. Beef Exporters, Japan Trade Deal Levels Playing Field But Sales Surge Unlikely. Reuters. 26 September 2019. Available online: https://www.reuters.com/article/us-usa-trade-japan-beef/for-u-s-beef-exporters-japan-trade-deal-levels-playing-field-but-sales-surge-unlikely-idUSKBN1WB0ZG (accessed on 8 June 2020).

- Fox, G.; Turner, J.; Gillepie, T. The value of precipitation forecast information in winter wheat production. Agric. For. Meteorol. 1999, 95, 99–111. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Mean | Std. Dev. | Max | Min | Skewness | Kurtosis | Jarque–Bera | |

|---|---|---|---|---|---|---|---|

| IBP | 0.005 | 0.037 | 0.166 | −0.194 | −0.639 | 14.489 | 528.916 *** |

| AZE | 0.009 | 0.018 | 0.091 | −0.025 | 1.763 | 8.688 | 177.291 *** |

| GEO | 0.007 | 0.026 | 0.109 | −0.109 | −0.122 | 7.676 | 86.800 *** |

| JPN | 0.000 | 0.027 | 0.076 | −0.066 | 0.519 | 3.602 | 5.706 * |

| KAZ | 0.010 | 0.025 | 0.070 | −0.169 | −3.561 | 28.609 | 2796.815 *** |

| KGZ | 0.009 | 0.022 | 0.066 | −0.053 | −0.114 | 3.162 | 0.308 |

| MRT | 0.004 | 0.034 | 0.170 | −0.211 | −1.657 | 24.438 | 1862.623 *** |

| TJK | 0.010 | 0.024 | 0.073 | −0.065 | −0.638 | 4.465 | 14.934 *** |

| TUN | 0.002 | 0.022 | 0.053 | −0.053 | −0.235 | 2.987 | 0.878 |

| UK | 0.004 | 0.032 | 0.086 | −0.092 | −0.042 | 3.751 | 2.261 |

| USA | 0.003 | 0.019 | 0.068 | −0.050 | 0.239 | 4.249 | 7.083 ** |

| ADF | PP | KPSS | ARCH-LM Test | |

|---|---|---|---|---|

| IBP | −8.845 *** (0) | −8.809 *** (3) | 0.107 (4) | 2.502 ** |

| AZE | −3.255 *** (1) | −3.210 *** (1) | 0.052 (6) | 2.230 ** |

| GEO | −6.174 *** (0) | −6.230 *** (3) | 0.083 (2) | 0.101 |

| JPN | −9.134 *** (0) | −9.159 *** (2) | 0.113 (2) | 1.966 * |

| KAZ | −5.880 *** (0) | −5.880 *** (3) | 0.092 (5) | 3.029 * |

| KGZ | −3.993 *** (0) | −3.817 *** (5) | 0.101 (5) | 2.400 * |

| MRT | −13.271 *** (0) | −12.900 *** (4) | 0.171 (2) | 9.879 *** |

| TJK | −2.875 *** (2) | −7.042 *** (5) | 0.101 (5) | 1.772 * |

| TUN | −7.687 *** (0) | −7.701 *** (3) | 0.044 (4) | 3.422 * |

| UK | −9.749 *** (0) | −9.750 *** (3) | 0.055 (2) | 2.892 * |

| USA | −12.733 *** (0) | −12.884 *** (2) | 0.051 (3) | 1.787 * |

| Mean | Median | Std. Dev. | |

|---|---|---|---|

| AZE | 0.948 | 0.956 | 0.024 |

| GEO | 0.721 | 0.718 | 0.056 |

| JPN | 0.446 | 0.447 | 0.014 |

| KAZ | 0.947 | 0.950 | 0.019 |

| KGZ | 0.972 | 0.971 | 0.013 |

| MRT | 1.000 | 1.000 | 0.000 |

| TJK | 0.970 | 0.967 | 0.013 |

| TUN | 0.924 | 0.918 | 0.013 |

| UK | 0.711 | 0.713 | 0.055 |

| USA | 0.982 | 0.986 | 0.036 |

| Parameters | Specification Tests | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| ARCH-LM Test | BIC | ||||||||

| IBP | 0.003 * | 0.128 | −1.623 *** | 0.124 *** | −0.207 * | 0.863 *** | 4.456 | 0.313 | −4.199 |

| AZE | 0.002 ** | 0.714 *** | −5.659 ** | 0.232 ** | 0.487 *** | 0.401 ** | 4.492 | 0.347 | −6.031 |

| GEO | 0.002 | 0.518 *** | −4.828 *** | 0.327 *** | −0.520 ** | 0.632 *** | 3.044 | 0.248 | −4.456 |

| JPN | 0.000 | 0.047 | −13.239 *** | 0.067 ** | 0.223 | 0.848 *** | 3.291 | 0.617 | −4.218 |

| KAZ | 0.008 *** | 0.218 *** | −13.758 *** | 0.101 *** | 0.236 | 0.803 *** | 3.114 | 0.226 | −4.826 |

| KGZ | 0.003 * | 0.712 *** | −13.828 *** | 0.393 * | −0.124 | 0.638 *** | 7.249 | 0.580 | −5.109 |

| MRT | 0.007 *** | 0.025 | −5.403 *** | 0.004 *** | 0.094 | 0.902 ** | 7.115 | 0.512 | −4.607 |

| TJK | 0.009 *** | 0.223 * | −5.166 ** | 0.299 *** | 0.045 | 0.692 ** | 6.282 | 0.712 | −4.517 |

| TUN | 0.004 * | 0.261 *** | −1.173 | 0.169 ** | −0.222 ** | 0.897 *** | 6.604 | 1.068 | −4.800 |

| UK | 0.004 | −0.099 | −6.982 ** | 0.130 ** | −0.159 | 0.867 ** | 12.411 | 0.906 | −3.829 |

| USA | 0.003 ** | −0.113 | −11.950 *** | 0.103 *** | 0.125 | 0.883 *** | 8.039 | 0.533 | −5.025 |

| Causality from Global Price to Local Price | Causality-in-Mean (M = 5) | Causality-in-Variance (M = 5) | Causality from Local Price to Global Price | Causality-in-Mean (M = 5) | Causality-in-Variance (M = 5) |

|---|---|---|---|---|---|

| IBP → AZE | 0.491 | −1.333 | AZE → IBP | −0.143 | −0.995 |

| IBP → GEO | 1.986 ** | −0.173 | GEO → IBP | 0.300 | −0.122 |

| IBP → JPN | 1.839 ** | 3.051 *** | JPN → IBP | 2.556 *** | −0.560 |

| IBP → KAZ | 0.461 | −1.479 | KAZ → IBP | −1.335 | −0.871 |

| IBP → KGZ | 0.458 | −0.137 | KGZ → IBP | 0.794 | 0.761 |

| IBP → MRT | −0.789 | −0.540 | MRT → IBP | −1.073 | 0.618 |

| IBP → TJK | 0.856 | 0.469 | TJK → IBP | −0.024 | −0.460 |

| IBP → TUN | 0.111 | 0.611 | TUN → IBP | 0.282 | −0.553 |

| IBP → UK | 2.323 *** | 3.052 *** | UK → IBP | 0.487 | −1.255 |

| IBP → USA | 1.938 ** | −0.338 | USA → IBP | −0.216 | 0.367 |

| DCC | A-DCC | G-DCC | BIC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| AZE | 0.113 ** | −0.737 *** | 0.876 *** | 0.701 *** | −873.252 | |||||

| GEO | 0.441 *** | 0.519 ** | −739.933 | |||||||

| JPN | 0.551 *** | −0.237 | 0.834 *** | 0.286 | −739.375 | |||||

| KAZ | 0.013 *** | 0.928 *** | −803.753 | |||||||

| KGZ | 0.264 ** | 0.647 ** | −824.018 | |||||||

| MRT | 0.886 *** | −0.062 *** | 0.474 *** | 1.024 *** | −748.935 | |||||

| TJK | 0.405 *** | 0.342 *** | 0.881 *** | −1.009 *** | −812.306 | |||||

| TUN | 0.000 | 0.864 *** | −0.444 ** | −834.120 | ||||||

| UK | 0.270 *** | 0.987 *** | 1.021 *** | −0.127 | −709.671 | |||||

| USA | −0.062 *** | 0.302 *** | −1.019 *** | −0.987 *** | −794.574 | |||||

| Mean | Median | Maximum | Minimum | Std. Dev. | |

|---|---|---|---|---|---|

| AZE | 0.219 | 0.187 | 0.844 | −0.332 | 0.192 |

| GEO | 0.053 | 0.055 | 0.589 | −0.349 | 0.196 |

| JPN | 0.361 | 0.352 | 0.935 | −0.097 | 0.183 |

| KAZ | 0.187 | 0.212 | 0.591 | −0.359 | 0.222 |

| KGZ | 0.163 | 0.157 | 0.535 | −0.160 | 0.124 |

| MRT | 0.109 | 0.081 | 0.669 | −0.212 | 0.131 |

| TJK | 0.142 | 0.127 | 0.999 | −0.292 | 0.237 |

| TUN | −0.008 | −0.045 | 0.393 | −0.162 | 0.129 |

| UK | 0.152 | 0.112 | 0.998 | −0.420 | 0.233 |

| USA | −0.006 | −0.006 | 0.817 | −0.153 | 0.099 |

| Modified Wald Test for Group-Wise Heteroskedasticity | Pesaran’s Test of Cross-Sectional Independence | Wooldridge Test for Autocorrelation | |

|---|---|---|---|

| Statistics | 163.880 *** | 0.047 | 3.822 * |

| Pool OLS Model | FGLS Model with Heteroskedasticity and Autocorrelation | Prais–Winsten Regression with PCSEs | |

|---|---|---|---|

| SSR () | −0.385 *** | −0.316 ** | −0.291 *** |

| BEEF () | 0.242 | −0.017 | −0.075 |

| PORK () | −0.144 | −0.071 | −0.096 |

| CHIKEN () | 0.018 | 0.028 | 0.024 |

| CPI () | 0.348 | 0.524 | 0.145 |

| GDP () | −0.045 | −0.052 | −0.074 |

| Constant () | 0.448 *** | 0.378 *** | 0.379 *** |

| 0.171 | – | 0.077 | |

| Wald test | 24.390 *** | 15.31 * | 10.38 ** |

| Observations | 80 | 80 | 80 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, J.; Tanaka, T. The Effectiveness of Self-Sufficiency Policy: International Price Transmissions in Beef Markets. Sustainability 2020, 12, 6073. https://doi.org/10.3390/su12156073

Guo J, Tanaka T. The Effectiveness of Self-Sufficiency Policy: International Price Transmissions in Beef Markets. Sustainability. 2020; 12(15):6073. https://doi.org/10.3390/su12156073

Chicago/Turabian StyleGuo, Jin, and Tetsuji Tanaka. 2020. "The Effectiveness of Self-Sufficiency Policy: International Price Transmissions in Beef Markets" Sustainability 12, no. 15: 6073. https://doi.org/10.3390/su12156073

APA StyleGuo, J., & Tanaka, T. (2020). The Effectiveness of Self-Sufficiency Policy: International Price Transmissions in Beef Markets. Sustainability, 12(15), 6073. https://doi.org/10.3390/su12156073