Transparency as a Key Element in Accountability in Non-Profit Organizations: A Systematic Literature Review

Abstract

1. Introduction

2. Characteristics that Define the NPOs

3. Description of the Bibliometric Review

3.1. Planning the Review: Formulation of the Research Questions

- RQ1: Why should NPOs disclose transparent information to stakeholders?

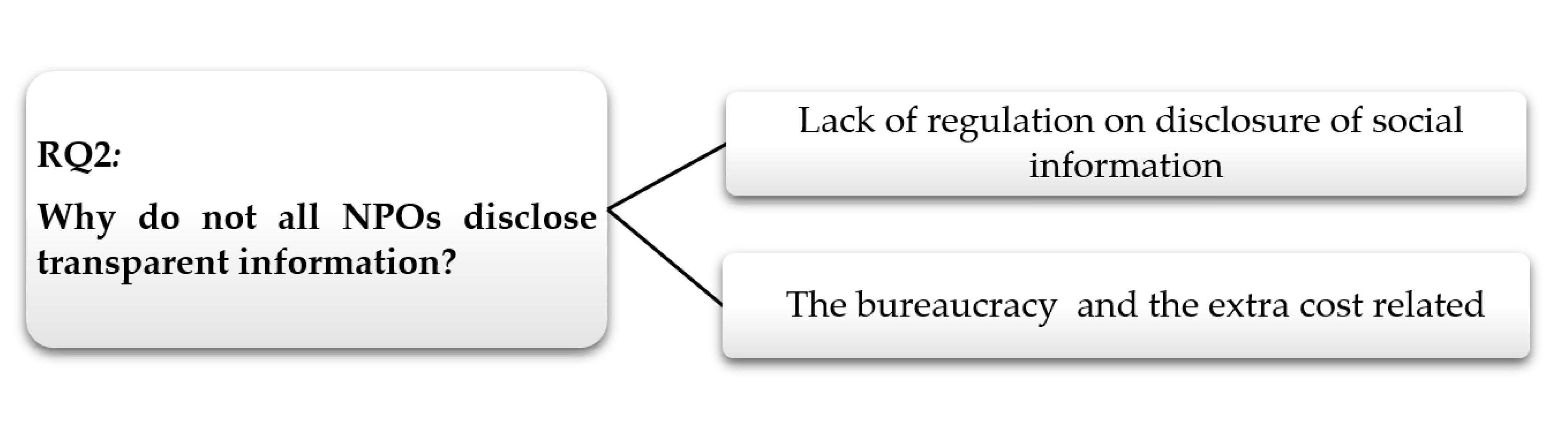

- RQ2: Why do not all NPOs disclose transparent information?

- RQ3: What means do NPOs use to disclose transparent information?

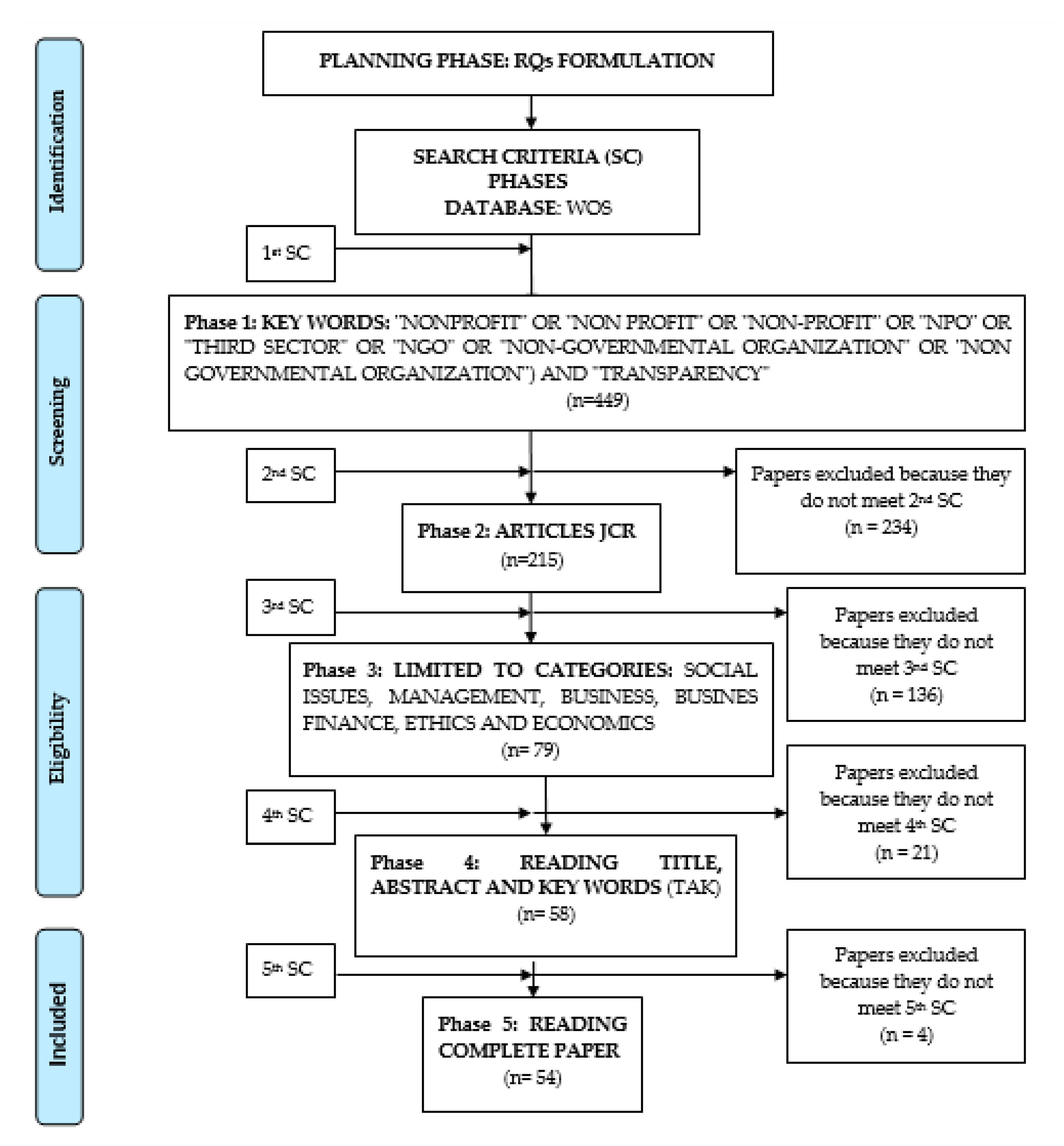

3.2. Search Criteria

4. Results of the Systematic Literature Review: Sample Description

- Journals

- Sample selection period

- Research method

- Regression models. This kind of method looks for the relationships of transparency with other variables. For instance, some authors aim to identify the influence of several factors because of the varied views on the weighting of the information disclosure of web pages [73]. Other authors study the relationship between transparency and efficiency in the allocation of funds in the NPOs [74].

- Statistical tests: This method is a more descriptive analysis, although it is used to give meaning to the aims of a study as a result. On the one hand, authors use non-parametric tests such as the Pearson’s chi-squared test to explore why NPOs would not comply with transparency and accountability standards and provide inaccurate information about their compliance [11]. On the other hand, Yasmin, Haniffa, and Hudaib [75] combine the non-parametric Mann–Whitney U test and parametric independent sample t-test in order to examine communicated accountability practices.

- Index. Lastly, a group of studies used indices to summarize, with a single, reliable, and consistent measure, several aspects that are indicative of the extent of transparency in NPOs. To begin with, Gandía [12] analyzed the information transparency on the websites of Spanish NGDOD through a transparency index which consists of four sections, checking its internal consistency through an analysis of reliability based on Cronbach’s alpha. Next, Gálvez Rodríguez et al. [73] used a Disclosure Index (IDI) to analyze the information provided in the organization web pages, regarding some principles of the Loyalty Foundation code. Finally, Cabedo et al. [30] proposed an index for measuring the level of transparency in relation to the projects of an organization, as well as determining the specific aspects in which transparency could be improved.

5. Theoretical Foundations of the Transparency of Accountability in NPOs

5.1. RQ1: Why Should NPOs Disclose Transparent Information to Stakeholders?

5.1.1. Third Sector Growth and the Consequent Increase of Fraud Cases

5.1.2. Cooperation with the Public Sector

5.1.3. Public and Private Funding

5.2. RQ2: Why Do Not All NPOs Disclose Transparent Information?

5.3. RQ3: What Means do NPOs Use to Disclose Transparent Information?

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Connolly, C.; Hyndman, N.; McConville, D. Conversion Ratios, Efficiency and Obfuscation: A Study of the Impact of Changed UK Charity Accounting Requirements on External Stakeholders. Volunt. Int. J. Volunt. Nonprofit Organ. 2013, 24, 785–804. [Google Scholar] [CrossRef]

- Pennerstorfer, A.; Rutherford, A.C. Measuring Growth of the Nonprofit Sector: The Choice of Indicator Matters. Nonprofit Volunt. Sect. Q. 2019, 48, 440–456. [Google Scholar] [CrossRef]

- Austin, J.E. Strategic Collaboration Between Nonprofits and Businesses. Nonprofit Volunt. Sect. Q. 2000, 29, 69–97. [Google Scholar] [CrossRef]

- Fernández, J.M.R.; Gil, M.I.S. Una nueva frontera en organizaciones no lucrativa. CIRIEC-España Rev. Econ. Pública, Soc. y Coop. 2011, 71, 229–251. [Google Scholar]

- Valentinov, V.; Vaceková, G. Sustainability of rural nonprofit organizations: Czech Republic and beyond. Sustainability 2015, 7, 9890–9906. [Google Scholar] [CrossRef]

- Lozano, M.R.; Valencia, P.T.; Gutiérrez, A.C.M. Transparencia y calidad de la información económico-financiera en las entidades no lucrativas. Un estudio empírico a nivel andaluz. CIRIEC-España Rev. Econ. Pública, Soc. y Coop. 2008, 63, 253–274. [Google Scholar]

- Greenlee, J.; Fischer, M.; Gordon, T.; Keating, E. An investigation of fraud in nonprofit organizations: Occurrences and deterrents. Nonprofit Volunt. Sect. Q. 2007, 36, 676–694. [Google Scholar] [CrossRef]

- Sanzo-Pérez, M.J.; Rey-Garcia, M.; Álvarez-González, L.I. The Drivers of Voluntary Transparency in Nonprofits: Professionalization and Partnerships with Firms as Determinants. Volunt. Int. J. Volunt. Nonprofit Organ. 2017, 28, 1595–1621. [Google Scholar] [CrossRef]

- Benjamin, L.M. Account space: How accountability requirements shape nonprofit practice. Nonprofit Volunt. Sect. Q. 2008, 37, 201–223. [Google Scholar] [CrossRef]

- Tacon, R.; Walters, G.; Cornforth, C. Accountability in Nonprofit Governance: A Process-Based Study. Nonprofit Volunt. Sect. Q. 2017, 46, 685–704. [Google Scholar] [CrossRef]

- Burger, R.; Owens, T. Promoting transparency in the NGO sector: Examining the availability and reliability of self-reported data. World Dev. 2010, 38, 1263–1277. [Google Scholar] [CrossRef]

- Gandía, J.L. Internet disclosure by nonprofit organizations: Empirical evidence of nongovernmental organizations for development in Spain. Nonprofit Volunt. Sect. Q. 2011, 40, 57–78. [Google Scholar] [CrossRef]

- Hale, K. Understanding nonprofit transparency: The limit of formal regulation in the American nonprofit sector. Int. Rev. Public Adm. 2013, 18, 31–49. [Google Scholar] [CrossRef]

- Fernández, G.C.; Vázquez, J.M.G.; Corredoira, M.D.L.Á.Q. La importancia de los Stakeholders de la organización: Un análisis empírico aplicado a la empleabilidad del alumnado de la Universidad española. Investig. Eur. Dir. y Econ. la Empres. 2007, 13, 13–32. [Google Scholar]

- Gibson, K. The moral basis of stakeholder theory. J. Bus. Ethics 2000, 26, 245–257. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Boston, MA, USA, 1984. [Google Scholar]

- Volpentesta, J.R.; Chahín, T.; Alcaín, M.F.; Nievas, G.R.; Spinelli, H.E. Identificación del impacto de la gestión de los stakeholders en las estructuras de las empresas que desarrollan estrategias de responsabilidad social empresarial. Univ. Empres. 2014, 16, 65–94. [Google Scholar] [CrossRef]

- Jeong, B.; Kearns, K. Accountability in Korean NPOs: Perceptions and Strategies of NPO Leaders. Voluntas 2015, 26, 1975–2001. [Google Scholar] [CrossRef]

- Daub, C.H.; Scherrer, Y.M.; Verkuil, A.H. Exploring reasons for the resistance to sustainable management within non-profit organizations. Sustainability 2014, 6, 3252–3270. [Google Scholar] [CrossRef]

- Crack, A.M. The Regulation of International NGOS: Assessing the Effectiveness of the INGO Accountability Charter. Volunt. Int. J. Volunt. Nonprofit Organ. 2018, 29, 419–429. [Google Scholar] [CrossRef]

- INGO Accountability Charter. Our Accountability Commitments; Amnesty International: London, UK, 2015. [Google Scholar]

- Verbruggen, S.; Christiaens, J.; Milis, K. Can resource dependence and coercive isomorphism explain nonprofit organizations’ compliance with reporting standards? Nonprofit Volunt. Sect. Q. 2011, 40, 5–32. [Google Scholar] [CrossRef]

- Costa, E.; Ramus, T.; Andreaus, M. Accountability as a Managerial Tool in Non-Profit Organizations: Evidence from Italian CSVs. Volunt. Int. J. Volunt. Nonprofit Organ. 2011, 22, 470–493. [Google Scholar] [CrossRef]

- Young, D.R.; Jung, T.; Aranson, R. Mission-market tensions and nonprofit pricing. Am. Rev. Public Adm. 2010, 40, 153–169. [Google Scholar] [CrossRef]

- AECA. Indicadores para Entidades Sin Fines Lucrativos; Documento no 3; International Civil Society Center: Berlin, Germany, 2012; ISBN 9788415467502. [Google Scholar]

- Schmitz, H.P.; Raggo, P.; Bruno-van Vijfeijken, T. Accountability of transnational NGOs: Aspirations vs. practice. Nonprofit Volunt. Sect. Q. 2012, 41, 1175–1194. [Google Scholar] [CrossRef]

- González-Sánchez, M.; Rúa-Alonso, E. Análisis de la eficiencia en la gestión de las fundaciones: Una propuesta metodológica. CIRIEC-España Rev. Econ. pública Soc. y Coop. 2007, 117–149. [Google Scholar]

- Jepson, P. Governance and accountability of environmental NGOs. Environ. Sci. Policy 2005, 8, 515–524. [Google Scholar] [CrossRef]

- Schatteman, A. Nonprofit accountability: To whom and for what? An introduction to the special issue. Int. Rev. Public Adm. 2013, 18, 1–6. [Google Scholar] [CrossRef]

- Cabedo, J.D.; Fuertes-Fuertes, I.; Maset-LLaudes, A.; Tirado-Beltrán, J.M. Improving and measuring transparency in NGOs: A disclosure index for activities and projects. Nonprofit Manag. Leadersh. 2018, 28, 329–348. [Google Scholar] [CrossRef]

- Franco, C.M.M.; Raja, I.G. Medida de la eficiencia en entidades no lucrativas: Un estudio empírico para fundaciones asistenciales. Rev. Contab. Account. Rev. 2014, 17, 47–57. [Google Scholar] [CrossRef][Green Version]

- Fritz, T.M.; von Schnurbein, G. Beyond socially responsible investing: Effects of mission-driven portfolio selection. Sustainability 2019, 11, 6812. [Google Scholar] [CrossRef]

- Kim, M. The Relationship of Nonprofits’ Financial Health to Program Outcomes: Empirical Evidence From Nonprofit Arts Organizations. Nonprofit Volunt. Sect. Q. 2017, 46, 525–548. [Google Scholar] [CrossRef]

- Hofmann, M.A.; McSwain, D. Financial disclosure management in the nonprofit sector: A framework for past and future research. J. Account. Lit. 2013, 32, 61–87. [Google Scholar] [CrossRef]

- Salamon, L.M.; Sokolowski, S.W. Beyond Nonprofits: Re-conceptualizing the Third Sector. Volunt. Int. J. Volunt. Nonprofit Organ. 2016, 27, 1515–1545. [Google Scholar] [CrossRef]

- Moreno, P.D.C.; Alcaide, T.C.H.; San Juan, A.I.S. La transparencia organizativa y económica en la Web de las fundaciones: Un estudio empírico para España. REVESCO Rev. Estud. Coop. 2016, 121, 62–88. [Google Scholar]

- Salamon, L.M.; Toepler, S. Government–Nonprofit Cooperation: Anomaly or Necessity? Volunt. Int. J. Volunt. Nonprofit Organ. 2015, 26, 2155–2177. [Google Scholar] [CrossRef]

- Álvarez-González, L.I.; García-Rodríguez, N.; Rey-García, M.; Sanzo-Perez, M.J. Business-nonprofit partnerships as a driver of internal marketing in nonprofit organizations. Consequences for nonprofit performance and moderators. BRQ Bus. Res. Q. 2017, 20, 112–123. [Google Scholar] [CrossRef]

- Kuenzi, K.; Stewart, A.J. An Exploratory Study of the Nonprofit Executive Factor. J. Nonprofit Educ. Leadersh. 2017, 7, 306–324. [Google Scholar] [CrossRef]

- Ebrahim, A. Accountability in practice: Mechanisms for NGOs. World Dev. 2003, 31, 813–829. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Unerman, J. From functional to social accountability: Transforming the accountability relationship between funders and non-governmental development organisations. Account. Audit. Account. J. 2007, 20, 446–471. [Google Scholar] [CrossRef]

- Saxton, G.D.; Guo, C. Accountability online: Understanding the web-based accountability practices of nonprofit organizations. Nonprofit Volunt. Sect. Q. 2011, 40, 270–295. [Google Scholar] [CrossRef]

- Arena, M.; Azzone, G.; Bengo, I. Performance Measurement for Social Enterprises. Volunt. Int. J. Volunt. Nonprofit Organ. 2015, 26, 649–672. [Google Scholar] [CrossRef]

- Striebing, C. Professionalization and voluntary transparency practices in nonprofit organizations. Nonprofit Manag. Leadersh. 2017, 28, 65–83. [Google Scholar] [CrossRef]

- Dumont, G.E. Transparency or Accountability? The Purpose of Online Technologies for Nonprofits. Int. Rev. Public Adm. 2013, 18, 7–29. [Google Scholar] [CrossRef]

- Pérez, V.M.; Cruz, N.M. La web como mecanismo de transparencia de las ONG. Más allá de la certificación. Rev. Española del Terc. Sect. Sect. 2017, 137, 159–170. [Google Scholar] [CrossRef]

- Kim, Y.H.; Kim, S.E. What Accounts for the Variations in Nonprofit Growth? A Cross-National Panel Study. Volunt. Int. J. Volunt. Nonprofit Organ. 2018, 29, 481–495. [Google Scholar] [CrossRef]

- Gilchrist, D.J.; Simnett, R. Research horizons for public and private not-for-profit sector reporting: Moving the bar in the right direction. Account. Financ. 2019, 59, 59–85. [Google Scholar] [CrossRef]

- Wellens, L.; Jegers, M. Effective governance in nonprofit organizations: A literature based multiple stakeholder approach. Eur. Manag. J. 2014, 32, 223–243. [Google Scholar] [CrossRef]

- Behn, B.K.; DeVries, D.D.; Lin, J. The determinants of transparency in nonprofit organizations: An exploratory study. Adv. Account. 2010, 26, 6–12. [Google Scholar] [CrossRef]

- Aureli, S. A comparison of content analysis usage and text mining in CSR corporate disclosure. Int. J. Digit. Account. Res. 2017, 17. [Google Scholar] [CrossRef]

- Boell, S.K.; Cecez-Kecmanovic, D. On being ‘systematic’in literature reviews. In Formulating Research Methods for Information Systems; Palgrave Macmillan: London, UK, 2015. [Google Scholar]

- Pejić Bach, M.; Krstić, Ž.; Seljan, S.; Turulja, L. Text mining for big data analysis in financial sector: A literature review. Sustainability 2019, 11, 1277. [Google Scholar] [CrossRef]

- Basuony, M.A.; Mohamed, E.K.; Elragal, A.; Hussainey, K. Big data analytics of corporate internet disclosures. Account. Res. J. 2020. [Google Scholar] [CrossRef]

- Yang, R.; Yu, Y.; Liu, M.; Wu, K. Corporate risk disclosure and audit fee: A text mining approach. Eur. Account. Rev. 2018, 27, 583–594. [Google Scholar] [CrossRef]

- Lorenzo, F.C.; Ribal, C.B.; Yánez, J.S.N. Las dimensiones socioeconómicas del Tercer Sector en Canarias. CIRIEC-España, Rev. Econ. Pública, Soc. y Coop. 2017, 89, 198–226. [Google Scholar]

- Barea, J.; Pulido, A. El sector de instituciones sin fines de lucro en España. CIRIEC-España, Rev. Econ. Pública, Soc. y Coop. 2001, 35–49. [Google Scholar]

- Coraggio, J.L. Las tres corrientes vigentes de pensamiento y acción dentro del campo de la Economía Social y solidaria (ESS): Sus diferentes alcances. Univ. Nac. Gen. Sarmiento Inst. del Conurbano Argentina. 2017, 15. [Google Scholar]

- Monzón, J.; Chaves, R. The European social economy: Concept and dimensions of the third sector. Ann. Public Coop. Econ. 2008, 79, 549–577. [Google Scholar] [CrossRef]

- Teasdale, S. What’s in a Name? Making Sense of Social Enterprise Discourses. Public Policy Adm. 2012, 27, 99–119. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; PRISMA Group. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef]

- Nova-Reyes, A.; Muñoz-Leiva, F.; Luque-Martínez, T. The tipping point in the status of socially responsible consumer behavior research? A bibliometric analysis. Sustainability 2020, 12, 3141. [Google Scholar] [CrossRef]

- Dzhengiz, T. A Literature Review of Inter-Organizational Sustainability Learning. Sustainability 2020, 12, 4876. [Google Scholar] [CrossRef]

- Ramos Montesdeoca, M.; Sánchez Medina, A.J.; Blázquez Santana, F. Research Topics in Accounting Fraud in the 21st Century: A State of the Art. Sustainability 2019, 11, 1570. [Google Scholar] [CrossRef]

- Cordery, C.J.; Sim, D.; van Zijl, T. Differentiated regulation: The case of charities. Account. Financ. 2017, 57, 131–164. [Google Scholar] [CrossRef]

- Bachmann, P. Some problems of Czech nonprofit sector transparency/Vybrane problemy transparentnosti ceskeho neziskoveho sektoru. E+ M Ekon. A Manag. 2012, 15, 104–115. [Google Scholar]

- Zhuang, J.; Saxton, G.D.; Wu, H. Publicity vs. impact in nonprofit disclosures and donor preferences: A sequential game with one nonprofit organization and N donors. Ann. Oper. Res. 2014, 221, 469–491. [Google Scholar] [CrossRef]

- Lu, S.; Deng, G.; Huang, C.C.; Chen, M. External environmental change and transparency in grassroots organizations in China. Nonprofit Manag. Leadersh. 2018, 28, 539–552. [Google Scholar] [CrossRef]

- Kang, S.; Norton, H.E. Nonprofit organizations’ use the World Wide Web: Are they sufficiently fulfilling organizational goals? Public Relat. Rev. 2004, 30, 279–284. [Google Scholar] [CrossRef]

- Goatman, A.K.; Lewis, B.R. Charity e-volution? An evaluation of the attitudes of UK charities towards website adoption and use. Int. J. Nonprofit Volunt. Sect. Mark. 2007, 12, 33–46. [Google Scholar] [CrossRef]

- Waters, R.D. Nonprofit organizations’ use of the Internet. A content analysis of com- munication trends on the Internet sites of the philanthropy 400. Nonprofit Manag. Leadersh. 2007, 18, 59–76. [Google Scholar] [CrossRef]

- CONGDE. La Transparencia y Rendición de Cuentas en las ONGD: Situación Actual y Retos; CONGDE: Madrid, Spain, 2007. [Google Scholar]

- Gálvez Rodríguez, M.M.; Caba Pérez, M.C.; Godoy, M.L. Determining Factors in Online Transparency of NGOs: A Spanish Case Study. Volunt. Int. J. Volunt. Nonprofit Organ. 2012, 23, 661–683. [Google Scholar] [CrossRef]

- Valencia, L.A.R.; Queiruga, D.; González-Benito, J. Relationship Between Transparency and Efficiency in the Allocation of Funds in Nongovernmental Development Organizations. Volunt. Int. J. Volunt. Nonprofit Organ. 2015, 26, 2517–2535. [Google Scholar] [CrossRef]

- Yasmin, S.; Haniffa, R.; Hudaib, M. Communicated Accountability by Faith-Based Charity Organisations. J. Bus. Ethics 2014, 122, 103–123. [Google Scholar] [CrossRef]

- Rey-Garcia, M.; Liket, K.; Alvarez-Gonzalez, L.I.; Maas, K. Back to Basics: Revisiting the relevance of beneficiaries and for evaluation and accountability in nonprofits. Nonprofit Manag. Leadersh. 2017, 27, 493–511. [Google Scholar] [CrossRef]

- Yang, C.; Northcott, D. How can the public trust charities? The role of performance accountability reporting. Account. Financ. 2019, 59, 1687–1713. [Google Scholar] [CrossRef]

- McDonnell, D.; Rutherford, A.C. Promoting charity accountability: Understanding disclosure of serious incidents. Account. Forum 2019, 43, 42–61. [Google Scholar] [CrossRef]

- Carnochan, S.; Samples, M.; Myers, M.; Austin, M.J. Performance Measurement Challenges in Nonprofit Human Service Organizations. Nonprofit Volunt. Sect. Q. 2014, 43, 1014–1032. [Google Scholar] [CrossRef]

- Amagoh, F. Improving the credibility and effectiveness of non-governmental organizations. Prog. Dev. Stud. 2015, 15, 221–239. [Google Scholar] [CrossRef]

- de Andrés-Alonso, P.; Azofra-Palenzuela, V.; Romero-Merino, M.E. Determinants of Nonprofit Board Size and Composition. Nonprofit Volunt. Sect. Q. 2009, 38, 784–809. [Google Scholar] [CrossRef]

- Neely, D.G. The impact of regulation on the US nonprofit sector: Initial evidence from the Nonprofit Integrity Act of 2004. Account. Horiz. 2011, 25, 107–125. [Google Scholar] [CrossRef]

- Hielscher, S.; Winkin, J.; Crack, A.; Pies, I. Saving the Moral Capital of NGOs: Identifying One-Sided and Many-Sided Social Dilemmas in NGO Accountability. Volunt. Int. J. Volunt. Nonprofit Organ. 2017, 28, 1562–1594. [Google Scholar] [CrossRef]

- Tremblay-Boire, J.; Prakash, A. Accountability. org: Online disclosures by US nonprofits. Volunt. Int. J. Volunt. Nonprofit Organ. 2015, 26, 693–719. [Google Scholar] [CrossRef]

- Gibelman, M.; Gelman, S.R. A loss of credibility: Patterns of wrongdoing among nongovernmental organizations. Volunt. Int. J. Volunt. Nonprofit Organ. 2004, 15, 355–381. [Google Scholar] [CrossRef]

- Liu, Y.; Zhang, M.; Ye, T.; Zhang, Y. Does giving always lead to getting? Evidence from the collapse of charity credibility in China. Pac.-Basin Financ. J. 2019, 58, 101207. [Google Scholar] [CrossRef]

- Feiock, R.C.; Andrew, S.A. Introduction: Understanding the Relationships Between Nonprofit Organizations and Local Governments. Int. J. Public Adm. 2006, 29, 759–767. [Google Scholar] [CrossRef]

- Boateng, A.; Akamavi, R.K.; Ndoro, G. Measuring performance of non-profit organisations: Evidence from large charities. Bus. Ethics 2016, 25, 59–74. [Google Scholar] [CrossRef]

- Neumayr, M.; Schneider, U.; Meyer, M. Public Funding and Its Impact on Nonprofit Advocacy. Nonprofit Volunt. Sect. Q. 2015, 44, 297–318. [Google Scholar] [CrossRef]

- Manville, G.; Greatbanks, R. Third Sector Performance: Management and Finance in Not-for-Profit and Social Enterprises; Routledge: Abington, UK, 2016; ISBN 9781409429616. [Google Scholar]

- Weidenbaum, M. Who will guard the guardians? The social responsibility of NGOs. J. Bus. Ethics 2009, 87, 147–155. [Google Scholar] [CrossRef]

- Keating, E.K.; Frumkin, P. Reengineering nonprofit financial accountability: Toward a more reliable foundation for regulation. Public Adm. Rev. 2003, 63, 3–15. [Google Scholar] [CrossRef]

- Haski-Leventhal, D.; Foot, C. The Relationship Between Disclosure and Household Donations to Nonprofit Organizations in Australia. Nonprofit Volunt. Sect. Q. 2016, 45, 992–1012. [Google Scholar] [CrossRef]

- Lequericaonandia, M.B.V.; Galiana, M.E.I. Siguen las ONG Españolas los mecanismos voluntarios de accountability? Análisis del seguimiento de un grupo de ONG Españolas de los principios propuestos por la fundación lealtad. REVESCO Rev. Estud. Coop. 2014, 115, 186–214. [Google Scholar] [CrossRef]

- Benjamin, L.M. The Potential of Outcome Measurement for Strengthening Nonprofits’ Accountability to Beneficiaries. Nonprofit Volunt. Sect. Q. 2013, 42, 1224–1244. [Google Scholar] [CrossRef]

- Saxton, G.D.; Kuo, J.S.; Ho, Y.C. The Determinants of Voluntary Financial Disclosure by Nonprofit Organizations. Nonprofit Volunt. Sect. Q. 2012, 41, 1051–1071. [Google Scholar] [CrossRef]

- Lecy, J.D.; Schmitz, H.P.; Swedlund, H. Non-Governmental and Not-for-Profit Organizational Effectiveness: A modern synthesis. Volunt. Int. J. Volunt. Nonprofit Organ. 2012, 23, 434–457. [Google Scholar] [CrossRef]

- Goncharenko, G. The accountability of advocacy NGOs: Insights from the online community of practice. Account. Forum 2019, 43, 135–160. [Google Scholar] [CrossRef]

- Becker, A. An Experimental Study of Voluntary Nonprofit Accountability and Effects on Public Trust, Reputation, Perceived Quality, and Donation Behavior. Nonprofit Volunt. Sect. Q. 2018, 47, 562–582. [Google Scholar] [CrossRef]

- Moxham, C.; Boaden, R. The impact of performance measurement in the voluntary sector. Int. J. Oper. Prod. Manag. 2007, 27, 826–845. [Google Scholar] [CrossRef]

- Cordery, C.J.; Morgan, G.G. Special Issue on Charity Accounting, Reporting and Regulation. Volunt. Int. J. Volunt. Nonprofit Organ. 2013, 24, 757–759. [Google Scholar] [CrossRef][Green Version]

- AbouAssi, K. Testing Resource Dependency as a Motivator for NGO Self-Regulation: Suggestive Evidence From the Global South. Nonprofit Volunt. Sect. Q. 2015, 44, 1255–1273. [Google Scholar] [CrossRef]

- Peng, S.; Kim, M.; Deat, F. The Effects of Nonprofit Reputation on Charitable Giving: A Survey Experiment. Volunt. Int. J. Volunt. Nonprofit Organ. 2019, 30, 811–827. [Google Scholar] [CrossRef]

- Lee, R.L.; Joseph, R.C. An examination of web disclosure and organizational transparency. Comput. Human Behav. 2013, 29, 2218–2224. [Google Scholar] [CrossRef]

- Puentes, R.; Mozas, A.; Bernal, E.; Chaves, R. E-corporate social responsibility in small non-profit organisations: The case of Spanish ‘Non Government Organisations’. Serv. Ind. J. 2012, 32, 2379–2398. [Google Scholar] [CrossRef]

- Long, Z. Managing legitimacy crisis for state-owned non-profit organization: A case study of the Red Cross Society of China. Public Relat. Rev. 2016, 42, 372–374. [Google Scholar] [CrossRef]

- Pavlovic, J.; Lalic, D.; Djuraskovic, D. Communication of Non-Governmental Organizations via Facebook Social Network. Eng. Econ. 2014, 25, 186–193. [Google Scholar] [CrossRef][Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 15 years | (1) Articles Published in 19 Journals | (2) Articles on the Third Sector in 19 Journals | (3) Articles on Transparency in the Third Sector in 19 Journals |

|---|---|---|---|

| 2005 | 884 | 20 | 0 |

| 2006 | 893 | 34 | 3 |

| 2007 | 936 | 28 | 2 |

| 2008 | 1.234 | 37 | 0 |

| 2009 | 1.400 | 97 | 3 |

| 2010 | 1.321 | 104 | 5 |

| 2011 | 1.334 | 94 | 7 |

| 2012 | 1.345 | 120 | 3 |

| 2013 | 1.341 | 119 | 3 |

| 2014 | 1.352 | 133 | 5 |

| 2015 | 1.538 | 145 | 3 |

| 2016 | 1.439 | 156 | 4 |

| 2017 | 1.569 | 156 | 6 |

| 2018 | 1.716 | 149 | 3 |

| 2019 | 1.735 | 163 | 7 |

| Total | 20.037 | 1.555 | 54 |

| Author (Year) | Focus of Study and Sample | Method | Summary of Sajor Findings |

|---|---|---|---|

| Burger, R., & Owens, T. (2010) | Self-reported data to analyze transparency in the NGO (Non-governmental organizations) Uganda using a questionnaire to collect information on the organization’s structure, finances, and activities; and an interview with a community focus group to explore how the organizations are perceived by community members. | Pearson’s chi-squared test. | - Reported levels of transparency in the sector and accountability were reasonably high. - 85% of NGOs that produced annual reports asserted that it was available to the public upon request. - NGOs claiming to be transparent may frequently provide inaccurate information, to show a more favorable view. |

| Cabedo, J. D. Fuertes-Fuertes, I. Maset-LLaudes, A. & Tirado-Beltrán, J. M. (2018) | Analyze the level of transparency of the portfolio of projects, detect the specific aspects that could be improved in each organization, and carry out comparisons among NPOs. The sample of this research was selected from organizations that belong to CONGDE (Spanish Development NGO Coordinator). | Index to measure the information (technical, financial, and scope) transparency of the projects implemented. | - This index also uses the individualized analysis of the items included in it to determine the particular aspects in which transparency could be improved. - Social impact of the projects is information that is not disclosed by any of the organizations analyzed. |

| Gandía, J. L. (2011) | Empirical study through a proposed model of information disclosure for the evolution of the websites to improve accountability and transparency. The sample of this study was selected from organizations rated by CONGDE. | Transparency index (Transparency index based on the work carried out by other authors [69,70,71] and transparency and accountability recommendations [72].) and analysis of reliability based on Cronbach’s alpha. | - Donations are positively related to the amount of information disclosed on the web. - Voluntary disclosure of information provides signals and information that are relevant to current and potential donors. |

| Gálvez Rodríguez, M. M.; Caba Pérez, M. C. & Godoy, M. L. (2012) | A sample of 130 NGOs that were voluntarily analyzed by Loyalty Foundation was utilized to obtain the necessary information through its webs. | Disclosure Index (IDI) and multivariable linear regression analysis. | - The use of the Internet in Spanish NGOs to disclose information is scarce. - More accountability mechanisms that promote the Internet as a tool for the communication and interaction are needed. |

| Valencia, L. A. R., Queiruga, D., & González-Benito, J. (2015) | Empirical analysis of 62 organizations from the CONGDE studying the indicators from Loyalty Foundation. | Multiple regression models. | - Reporting on aspects related to four transparency variables (administration, project details, source of funds and use of funds) is linked to greater efficiency in the allocation of funds. |

| Yasmin, S., Haniffa, R., & Hudaib, M. (2014) | Design of a research instrument to capture transparency through the qualitative characteristics of the Trustees Annual Report and accountability with the Statement of Recommended Practice and Scale Stewart Accounts (1984) (Stewart, J. D. (1984). The role of information in public accountability. In Hopwood, A. & Tomkins, C. (Eds.), Issues in public sector accounting. Oxford: Philip Allen.). The population consisted of Muslim Charity Organization (MCOs) registered with the Charity Commission for England and Wales. | Parametric independent sample t test and non-parametric Mann–Whitney U test. | - There is a lack of commitment in substantive accountability for several reasons: High donor confidence; weak demand for information from the stakeholders; internal organizational problems related to organizational structure and culture; and lack of internal professional. |

| Author (Year) | Method | Sample | |||||

|---|---|---|---|---|---|---|---|

| Spanish Context | Other | ||||||

| Regression Models | Statistical Tests | Index | Predefined Model | CONGDE | Loyalty Foundation | ||

| Burger, R., & Owens, T. (2010) | x | x | |||||

| Cabedo, J. D.Fuertes-Fuertes, I.Maset-LLaudes, A. & Tirado-Beltrán, J. M. (2018) | x | x | |||||

| Gandía, J. L. (2011) | x | x | |||||

| Gálvez Rodríguez, M. M. Caba Pérez, M. C. Godoy, M. L. (2012) | x | x | x | ||||

| Valencia, L. A. R., Queiruga, D., & González-Benito, J. (2015) | x | x | x | ||||

| Yasmin, S., Haniffa, R., & Hudaib, M. (2014) | x | x | |||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ortega-Rodríguez, C.; Licerán-Gutiérrez, A.; Moreno-Albarracín, A.L. Transparency as a Key Element in Accountability in Non-Profit Organizations: A Systematic Literature Review. Sustainability 2020, 12, 5834. https://doi.org/10.3390/su12145834

Ortega-Rodríguez C, Licerán-Gutiérrez A, Moreno-Albarracín AL. Transparency as a Key Element in Accountability in Non-Profit Organizations: A Systematic Literature Review. Sustainability. 2020; 12(14):5834. https://doi.org/10.3390/su12145834

Chicago/Turabian StyleOrtega-Rodríguez, Cristina, Ana Licerán-Gutiérrez, and Antonio Luis Moreno-Albarracín. 2020. "Transparency as a Key Element in Accountability in Non-Profit Organizations: A Systematic Literature Review" Sustainability 12, no. 14: 5834. https://doi.org/10.3390/su12145834

APA StyleOrtega-Rodríguez, C., Licerán-Gutiérrez, A., & Moreno-Albarracín, A. L. (2020). Transparency as a Key Element in Accountability in Non-Profit Organizations: A Systematic Literature Review. Sustainability, 12(14), 5834. https://doi.org/10.3390/su12145834