Cooperative Entrepreneurship Model for Sustainable Development

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. Data Collection

3.2. Selection of Economic Variables

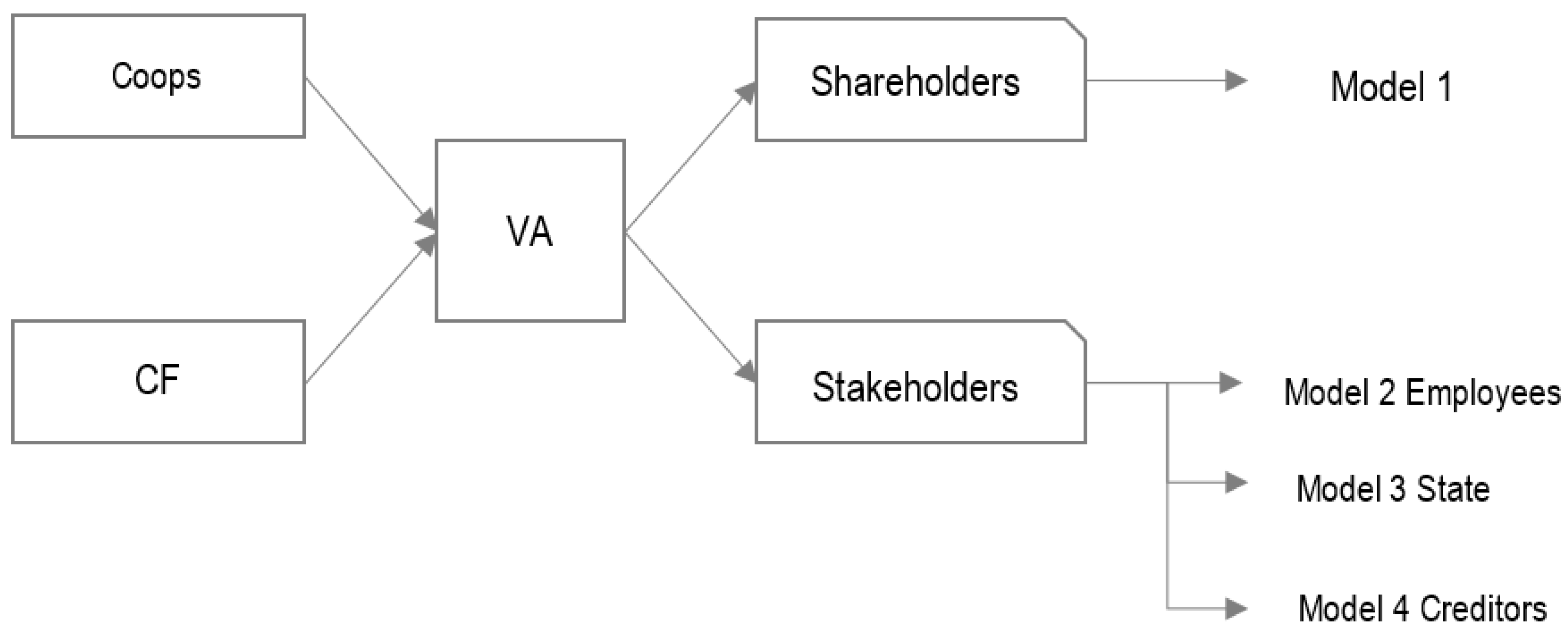

3.2.1. Dependent Variables

3.2.2. Explanatory Variables

3.3. Hypotheses and Methods

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| Coops | Cooperative Firms |

| CFs | Capitalist Firms |

References

- International Co-operative Alliance. Available online: https://www.ica.coop/en (accessed on 25 June 2020).

- Guzman, C.; Santos, F.J.; Barroso, M.D. Cooperative Essence and Entrepreneurial Quality: A Comparative Contextual Analysis. Ann. Public Coop. Econ. 2019, 91, 95–118. [Google Scholar] [CrossRef]

- UN. The Millennium Development Goals Report 2015. Available online: https://www.undp.org/content/dam/undp/library/MDG/english/UNDP_MDG_Report_2015.pdf (accessed on 25 June 2020).

- Mozas-Moral, A.; Puente-Poyatos, R. Corporate Social Responsibility and its Parallelism with Cooperative Societies. REVESCO Rev. Estud. Coop. 2010, 103, 75–100. [Google Scholar]

- Bastida, M.; Vaquero García, A.; Cancelo Márquez, M.; Olveira Blanco, A. Fostering the Sustainable Development Goals from an Ecosystem Conducive to the SE: The Galician’s Case. Sustainability 2020, 12, 500. [Google Scholar] [CrossRef]

- Bijman, J. Exploring the Sustainability of the Cooperative Model in Dairy: The Case of the Netherlands. Sustainability 2018, 10, 2498. [Google Scholar] [CrossRef]

- Pérez-Sanz, F.J.; Gargallo-Castel, A.F.; Esteban-Salvador, M.L. CSR Practices Among Co-operatives. Experience and Results of Case Studies. Ciriec España Rev. Econ. Pública Soc. Coop. 2019, 97, 137–178. [Google Scholar]

- Fukukawa, K.; Balmer, J.M.T.; Gray, E.R. Mapping the Interface Between Corporate Identity, Ethics and Corporate Social Reponsibility. J. Bus. Ethics 2007, 76, 1–5. [Google Scholar] [CrossRef]

- Novkovic, S. Defining the co-operative difference. J. Socio-Econ. 2008, 37, 2168–2177. [Google Scholar] [CrossRef]

- Shen, Y.; Tyedmers, P.; Adams, M.; Beaubien, L. Role of Co-operatives in Facilitating the Implementation of the Sustainable Development Goals. In Proceedings of the UNTFSSE International Conference, Geneva, Italy, 25–26 June 2019. [Google Scholar]

- Martinez-Leon, I.M.; Olmedo-Cifuentes, I.; Martínez-Victoria, M.; Arcas-Lario, N. Leadership Style and Gender: A Study of Spanish Cooperatives. Sustainability 2020, 12, 5107. [Google Scholar] [CrossRef]

- Bretos, I.; Marcuello, C. Revisiting globalization challenges and opportunities in the development of cooperatives. Ann. Public Coop. Econ. 2017, 88, 47–73. [Google Scholar] [CrossRef]

- Alcaniz, L.; Aguado, R.; Luis Retolaza, J. New Business Models: Beyond the Shareholder Approach. Rev. Bras. Gestão Negócios 2020, 22, 48–64. [Google Scholar] [CrossRef]

- Domar, E.D. The Soviet Collective Farm as a Producer Cooperative. Am. Econ. Rev. 1966, 56, 734–757. [Google Scholar]

- Ireland, N.J. The Economic Analysis of Labour Management Firms. Bull. Econ. Res. 1987, 39, 249–272. [Google Scholar] [CrossRef]

- Melgarejo-Molina, Z.; Vera-Colina, M.A.; Mora-Piapira, E.H. The Survival of Associated Labor Cooperatives in Colombia. A Theoretical Approach. Innovar 2012, 22, 5–16. [Google Scholar]

- Park, R.; Kruse, D.; Sesil, J. Does Employee Ownership Enhance Firm Survival? In Employee Participation, Firm Performance and Survival (Advances in the Economic Analysis of Participatory & Labor-Managed Firms, Volume 8); Perotin, V., Robinson, A., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2004; pp. 3–33. [Google Scholar]

- Dow, G. Allocating Control Over Firms: Stock Markets Versus Membership Markets. Rev. Ind. Organ. 2001, 18, 201–2018. [Google Scholar] [CrossRef]

- Burdín, G.; Dean, A. Revisiting the Objectives of Worker-Managed Firms: An Empirical Assessment. Econ. Syst. 2012, 36, 158–171. [Google Scholar] [CrossRef]

- Poulain-Rehm, T.; Lepers, X. Does Employee Ownership Benefit Value Creation? The Case of France (2001–2005). J. Bus. Ethics 2013, 112, 325–340. [Google Scholar] [CrossRef]

- Abad Segura, E.; Vall Martínez, M. Analysis of Viability of the Ethics Bank in Spain Through Triodos Bank. Comparison Economic-Financial with Traditional Bank. REVESCO Rev. Estud. Coop. 2018, 128, 7–35. [Google Scholar]

- Amat, O.; Perramon, J. High-Growth Cooperatives: Financial Profile and Key Factors For Competitiveness. Ciriec España Rev. Econ. Pública Soc. Coop. 2011, 73, 81–98. [Google Scholar]

- Parliament, C.; Lerman, Z.; Fulton, J.R. Performance of Cooperatives and Investor-Owned Firms in the Dairy Industry. J. Agric. Coop. 1990, 5, 1–16. [Google Scholar]

- Atienza Montero, P.; Rodríguez Pacheco, Á. Capitalist Enterprises Versus Cooperative Enterprises: Comparative Analysis of Economic and Financial Results for Spain in 2008–2015. Ciriec España Rev. Econ. Pública Soc. Coop. 2018, 93, 115–1542. [Google Scholar] [CrossRef]

- Lajara Camilleri, N.; Server Izquierdo, R.J. Market Orientation and Typology of Agrifood Cooperatives According to Competitiveness. Case-study of Spanish Citrus Cooperatives. REVESCO Rev. Estud. Coop. 2016, 121, 145–172. [Google Scholar]

- ORBIS. Available online: https://www.bvdinfo.com/es-es/nuestros-productos/datos/internacional/orbis (accessed on 25 June 2020).

- Maghraoui, R.; Zidai, J. Effects of Employee Ownership on the Performance of French Companies SBF120: Empirical Validation. J. Account. Financ. Audit. Stud. 2016, 2, 195–217. [Google Scholar]

- Richter, A.; Schrader, S. Levels of Employee Share Ownership and the Performance of Listed Companies in Europe. Br. J. Ind. Relat. 2017, 55, 396–420. [Google Scholar] [CrossRef]

- Fernández-Guadaño, J.; Sarria-Pedroza, J. Impact of Corporate Social Responsibility on Value Creation from a Stakeholder Perspective. Sustainability 2018, 10, 2062. [Google Scholar] [CrossRef]

- Fernández-Guadaño, J.; López-Millán, M. Employee-Owned Firms from a Stakeholder Perspective: Employee-Owned Firms. J. Int. Dev. 2018, 30, 1044–1059. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach; Nelson Education: Scarborough, ON, Canada, 2015. [Google Scholar]

- Chamberlain, G. Multivariate regression models for panel data. J. Econom. 1982, 18, 5–46. [Google Scholar] [CrossRef]

- Papke, L.; Wooldridge, J. Panel Data Methods for Fractional Response Variables with an Application to Test Pass Rates. J. Econom. 2008, 145, 121–133. [Google Scholar] [CrossRef]

- Schunck, R. Within and Between Estimates in Random-Effects Models: Advantages and Drawbacks of Correlated Random Effects and Hybrid Models. Stata J. 2013, 13, 65–76. [Google Scholar] [CrossRef]

- Melgarejo, Z.; Arcelus, F.J.; Simon, K. Managerial Performance Differences Between Labor-Owned and Participatory Capitalist Firms. J. Small Bus. Manag. 2014, 52, 808–828. [Google Scholar]

- Calderón Milán, B.; Calderón Milán, M.J. How Cooperatives Societies Face Economic Crisis in Spain: A Comparison of Careers Based on the Continous Sample of Working Lives Database. Ciriec España Rev. Econ. Pública Soc. Coop. 2012, 76, 5–26. [Google Scholar]

- Burdín, G.; Dean, A. New Evidence on Wages and Employment in Worker Cooperatives Compared with Capitalist Firms. J. Comp. Econ. 2009, 37, 517–533. [Google Scholar] [CrossRef]

- Sala Ríos, M.; Torres Solé, T.; Farré Perdiguer, M. Employment in Cooperative Societies—A Comparative Analysis of Cyclical Phases and Synchronization. Ciriec España Rev. Econ. Pública Soc. Coop. 2015, 83, 115–141. [Google Scholar]

- Roelants, B.; Dovgan, D.; Eum, H.; Terrasi, E. The Resilence of the Cooperative Model.: How Worker Cooperatives, Social Cooperatives and Other Worker-Owned Enterprises Respond to the Crisis and its Consequences, 1st ed.; CECOP-CICOPA Europe EU: Schaerbeek, Belgium, 2012. [Google Scholar]

- Lampel, J.; Bhalla, A.; Jha, P. The Employee Owned Model During Growth and Adversary: How Well Does it Hold Up? Eur. Bus. Rev. 2013, 20–23. [Google Scholar]

- Marín-Sánchez, M.M. La Compensación Fiscal de Pérdidas en Cooperativas y Su Impacto Como Fuente de Financiación Derivada de la Crisis. In Proceedings of the XVI Congreso de Investigadores de Economía Social y Cooperativa, Economía Social: Crecimiento y Bienestar, Universitat de València, València, Spain, 19–21 October 2016. [Google Scholar]

- Ferruzza, A.; Baldazzi, B.; Costanzo, L.; Patteri, P.; Tagliacozzo, G.; Ungaro, P. Statistics for Measuring Sustainable Development Goals: Challenges, Opportunities Progress and Innovations. In Proceedings of the 16th Conference of IAOS, Paris, France, 19–21 September 2018. [Google Scholar]

- International Cooperative Alliance (ICA). World Cooperative Monitor, Exploring The Cooperative Economy, Report. 2019. Available online: https://monitor.coop/sites/default/files/publication-files/wcm2019-final-1671449250.pdf (accessed on 5 May 2020).

- Harris, A.; Fulton, M. Comparative Financial Performance Analysis of Canadian Cooperatives, Investor-Owned Firms, and Industry Norms, 1st ed.; Centre for the Study of Co-operatives, University of Saskatchewan: Saskatoon, SK, Canada, 1996. [Google Scholar]

- Lazcano, L.; San-Jose, L.; Retolaza, J.L. Social Accounting in the Social Economy: A Case Study of Monetizing Social Value. In Modernization and Accountability in the Social Economy Sector; Ferreira, A., Marques, R., Azevedo, G., Inácido, H., Santos, C., Eds.; IGI Global: Hershey, PA, USA, 2018; pp. 132–150. [Google Scholar]

{kind=link}

| Sector | CF | Coop | ||

|---|---|---|---|---|

| N | Percent | N | Percent | |

| Industry | 109 | 27.7 | 52 | 43.7 |

| Services | 284 | 72.3 | 67 | 56.3 |

| Total | 393 | 119 | ||

| Size T | CF | Coop | ||

|---|---|---|---|---|

| N | Percent | N | Percent | |

| Micro (0–9 employees) | 281 | 71.5 | 70 | 58.8 |

| Small (10–49 employees) | 112 | 28.3 | 49 | 41.2 |

| Total | 393 | 119 | ||

| Abbreviation For the Variable | Variables |

|---|---|

| Stakeholder value creation | |

| PCVA | Log Staff Cost/Value Added |

| TAXVA | Log Taxes/Value Added |

| INTVA | Log Interest Expenses/Value Added |

| DIVVA | Log Dividends/Value Added |

| Explanatory and control variables | |

| Type | Type of firm, dichotomous variable: Coop = 1 CF = 0 |

| Size | 0 = Micro 1 = SME |

| Sector | Economic activity Secondary = 0 Tertiary = 1 |

| Inv | Log Fixed Assets/Net Sales |

| Leverage | Log Debt Coefficient |

| CF | Coop | |||||

|---|---|---|---|---|---|---|

| N | Mean | Std. Dev | N | Mean | Std. Dev | |

| Inv | 393 | 23.90 | 758.01 | 119 | 2.834 | 30.63 |

| Leverage | 393 | 88.76 | 134.27 | 119 | 64.15 | 90.20 |

| PCVA | 393 | 0.8032 | 1.000 | 119 | 0.7348 | 0.3215 |

| TAXVA | 393 | 0.0358 | 0.0462 | 119 | 0.0170 | 0.0275 |

| INTVA | 393 | 0.0492 | 0.1510 | 119 | 0.0637 | 0.1011 |

| DIVVA | 393 | 0.1025 | 0.4392 | 119 | 0.1234 | 0.4639 |

| Model 1: DIVVA | Model 2: PCVA | Model 3: TAXVA | Model 4: INTVA | |

|---|---|---|---|---|

| Type | 0.4796646 *** (0.1504098) | −0.1057451 ** (0.0413318) | −0.857507 *** (0.1301242) | 0.3119037 ** (0.1379757) |

| Size | −0.4775728 *** (0.147619) | 0.0427199 (0.0312053) | −0.2972845 *** (0.1053224) | −0.331231 *** (0.1118877) |

| Sector | −0.3799097 *** (0.1450873) | −0.0396391 (0.0336853) | 0.4069808 *** (0.1076507) | −0.1976776 * (0.1132788) |

| Leverage | 0.0450992 (0.0904224) | 0.0200099 ** (0.0095659) | −0.0970921 *** (0.0371706) | 0.2721943 *** (0.0562196) |

| Inv | −0.0044809 | 0.0499374 ** | −0.0814099 | 0.1357864 * |

| (0.1694699) | (0.0199685) | (0.1008912) | (0.0752091) | |

| MLeverage | −0.1880955 (0.1017708) | −0.025204 * (0.0138383) | 0.0239241 (0.0438861) | 0.111192 (0.0695469) |

| MInv | 0.1688187 (0.1744245) | −0.1016388 *** (0.0214712) | 0.1153734 (0.1018735) | 0.0143535 (0.076385) |

| Cons | −2.370522 *** | −0.3737572 *** | −3.68629 *** | −4.820358 *** |

| (0.2108041) | 0(.0515791) | (0.141528) | (0.1961528) | |

| Wald Chi2 | 60.41 *** | 45.63 *** | 92.55 *** | 166.69 *** |

| rho | 0.34688706 | 0.64566633 | 0.54992303 | 0.66435751 |

| N. obs | 962 | 2212 | 1904 | 2212 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fernandez-Guadaño, J.; Lopez-Millan, M.; Sarria-Pedroza, J. Cooperative Entrepreneurship Model for Sustainable Development. Sustainability 2020, 12, 5462. https://doi.org/10.3390/su12135462

Fernandez-Guadaño J, Lopez-Millan M, Sarria-Pedroza J. Cooperative Entrepreneurship Model for Sustainable Development. Sustainability. 2020; 12(13):5462. https://doi.org/10.3390/su12135462

Chicago/Turabian StyleFernandez-Guadaño, Josefina, Manuel Lopez-Millan, and Jesús Sarria-Pedroza. 2020. "Cooperative Entrepreneurship Model for Sustainable Development" Sustainability 12, no. 13: 5462. https://doi.org/10.3390/su12135462

APA StyleFernandez-Guadaño, J., Lopez-Millan, M., & Sarria-Pedroza, J. (2020). Cooperative Entrepreneurship Model for Sustainable Development. Sustainability, 12(13), 5462. https://doi.org/10.3390/su12135462