Sustainability and Its Place in the Self-Determination of Information-Based Companies

{kind=link}

Abstract

1. Introduction

2. Background

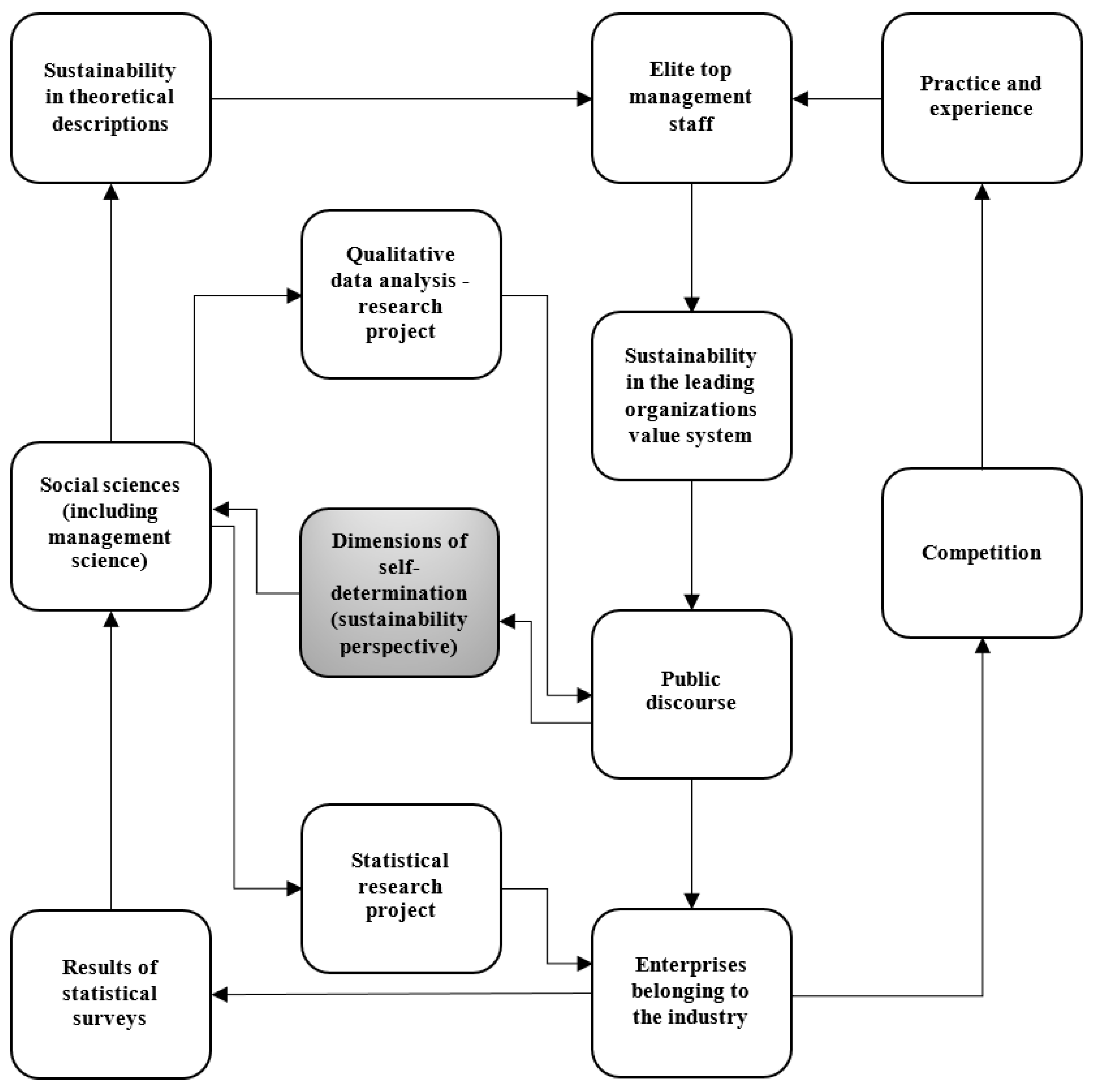

2.1. Environment of Observation of Dimensions of Self-Determination Which Are Defined from Sustainability Perspective

2.2. An Outline of Theories Shaping the Way Managers Perceive the Idea of Sustainability

- 1)

- Triple Bottom Line—this challenge is related to the postulate of maintaining a balance between profits and social and environmental benefits.

- 2)

- Mind-set—this challenge is related to the postulate of eliminating mental restrictions imposed by rules, guidelines, behavioral norms and performance metrics.

- 3)

- Resources—this challenge is related to the postulate of eliminating inertia and internal resistance to organizational changes on the way to creating innovative solutions.

- 4)

- Technology innovation—this challenge is related to the postulate of multidimensional integration of complex technological innovations in order to achieve a synergy effect.

- 5)

- External relationships—this challenge expresses the need for creative engagement in interactions with stakeholders and the business environment.

- 6)

- Business modelling methods and tools—this challenge expresses the need for the creative use and development of existing business modelling methods and tools.

- 1)

- In a sustainable society, nature is not subject to systematically increasing concentrations of substances from the earth’s crust (such as fossil CO2, heavy metals and minerals).

- 2)

- In a sustainable society, nature is not subject to systematically increasing concentrations of substances produced by society (such as antibiotics and endocrine disruptors).

- 3)

- In a sustainable society, nature is not subject to systematically increasing degradation by physical means (such as deforestation and the draining of groundwater tables).

- 4)

- In a sustainable society there are no structural obstacles to people’s health, influence, competence, impartiality and meaning.

- 1)

- Corporate sustainability in relation to corporate responsibility (CS and CR)

- 1a)

- Corporate sustainability is similar to corporate responsibility (cs ≈ cr)

- 1b)

- Corporate sustainability is different from corporate responsibility (cs ≠ cr)

- 1c)

- Corporate responsibility leads to corporate sustainability (cr → cs)

- 2)

- Mono-focal corporate sustainability (CS1)

- 2a)

- Corporate sustainability as moral leadership (cs/moral)

- 2b)

- Corporate sustainability as a strategy (cs/strategic)

- 3)

- Inclusive approaches to corporate sustainability (CSn)

- 3a)

- Corporate sustainability as a holistic concept (cs∞)

- 3b)

- Corporate sustainability as part of the triple bottom line (csTBL)

- 3c)

- Corporate sustainability as a financial incentive (cs$)

- 3d)

- Corporate sustainability as an indexing exercise (cs/index)

- 1)

- 2)

- Create value from “waste”—The concept of “waste” is eliminated by turning waste streams into useful and valuable inputs to other production and making better use of under-utilized capacity. The limitation of this archetype results from the artificiality of the concept of “waste” itself in the context of the activities of commercial organizations [31,32].

- 3)

- Substitute with renewables and natural processes—Reduce environmental impacts and increase business resilience by addressing resource constraint “limits to growth”, associated with non-renewable resources and current production systems. The limitation of this archetype results from the insufficient pace of development of the necessary technologies in relation to the needs related to population growth and the need to improve its standard of living.

- 4)

- Deliver functionality, rather than ownership—Provide services that satisfy users’ needs without their having to own physical products. The limitation of this archetype results from doubts in relation to Product Service Systems’ eco-efficiency [33] and also from doubts that such a solution raises the opinions of consumers [34].

- 5)

- Adopt a stewardship role—This involves proactively engaging with all stakeholders to ensure their long-term health and well-being. The limitation of this archetype results from the difficulties that arise when trying to take into account the interests of all stakeholders at the same time.

- 6)

- Encourage sufficiency—Solutions that actively seek to reduce consumption and production. The limitation of this archetype is due to the fact that solutions introduced unilaterally by the organization often do not bring an effect due to the lack of systemic adjustments in society [35].

- 7)

- Re-purpose the business for society/environment—This involves prioritizing the delivery of social and environmental benefits rather than economic profit (i.e., shareholder value) maximization, through close integration between the firm and local communities and other stakeholder groups. The traditional business model, where the customer is the primary beneficiary, may shift. Again (similar to the fifth archetype) the limitation of this archetype results from the difficulties that arise when trying to take into account the interests of all stakeholders at the same time.

- 8)

- Develop scale-up solutions—This involves delivering sustainable solutions at a large scale to maximize benefits for society and the environment. The limitation of this archetype is due to the fact that it is mainly small start-ups that are a source of innovation with the right potential for change, which sometimes hinders their sufficiently effective dissemination [36,37].

3. Methods

4. Results

point to the entity itself and relate to very explicit and specific matters (so this dimension will be called BASE and the fundamental question that can be asked here is: “With what tools and by what means is the organization ready to implement the idea of sustainability?”), while the other nineteen terms focus on immeasurable, universal ideas:acquisition, business, capital, company, core business, cost, e-commerce, growth, industry, investment, margin, operation, product, production, quality, report, resource-efficiency, service, strategy, supply chain, technology

(so, this dimension will be called IDEA and the fundamental question that can be asked here is: “What paradigm and what logic shapes the interior of an organization that is sensitive to the idea of sustainability?”). However, when it comes to the context arising at the interface between the subject and its environment, the division of the terms used on such occasions results from the role played by the organization in this system. In this case one could point to the organization’s active behavior:culture, change, community, effort, examination, excellence, flexibility, information, innovation, long run, long-term, mission, safety, security, philosophy, protection, relationship, value, viability, vision

(so, this dimension will be called ROLE and the fundamental question that can be asked here is: “What role does the organization want to take, which is sensitive to the idea of sustainability?”) or its passive participation in supporting certain concepts and treating them with respect:activist, advocate, businessman, competitor, entrepreneur, leader, precursor, partner, protector

(so, this dimension will be called CARE and the fundamental question that can be asked here is: “What draws the attention of an organization sensitive to the idea of sustainability?”).benefit, climate change, consumer, education, environment, electricity, government, green electricity, healthcare, human rights, individual, live, non-profit organization, renewable energy, resources, stakeholders, poverty, rural commerce, user, villager, women, world

5. Discussion and Conclusions

5.1. Binary Oppositions As the Basis of Identified Dimensions of Self-Determination

5.2. Dimensions of Self-Determination Towards Theories Devoted to the Idea of Sustainability

5.3. Proposals Referring to the Direction of Practical Use of Dimensions of Self-Determination

5.4. Dimensions of Self-Determination Versus an Alternative Way of Categorizing Context

5.5. The Final Conclusions

Funding

Conflicts of Interest

References

- Lorenz, M.H. Information Technology and Sustainability: Essays on the Relationship between ICT and Sustainable Development; BoD—Books on Demand: Zurich, Switzerland, 2008. [Google Scholar]

- Zink, K.J. Corporate Sustainability as a Challenge for Comprehensive Management; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Lakoff, G. Why it Matters How We Frame the Environment. Environ. Commun. 2010, 4, 70–81. [Google Scholar] [CrossRef]

- Gibson, C.H. Financial Reporting and Analysis; Cengage Learning: Boston, MA, USA, 2012. [Google Scholar]

- Carroll, A.B.; Brown, J.; Buchholtz, A.K. Business & Society: Ethics, Sustainability & Stakeholder Management; Cengage Learning: Boston, MA, USA, 2017. [Google Scholar]

- Jackson, A.Y.; Mazzei, L.A. Thinking with Theory in Qualitative Research; Informa UK Limited: London, UK, 2011. [Google Scholar]

- Barrett, R. The Values-Driven Organization: Cultural Health and Employee Well-Being as a Pathway to Sustainable Performance; Taylor & Francis: London, UK, 2017. [Google Scholar]

- Landrum, N.E.; Ohsowski, B. Identifying Worldviews on Corporate Sustainability: A Content Analysis of Corporate Sustainability Reports. Bus. Strat. Environ. 2017, 27, 128–151. [Google Scholar] [CrossRef]

- Calabres, A.; Costa, R.; Ghiron, N.L.; Menichini, T. Materiality analysis in sustainability reporting: A tool for directing corporate sustainability towards emerging economic, environmental, and social opportunities. Technol. Econ. Dev. Econ. 2019, 25, 1016–1038. [Google Scholar] [CrossRef]

- Sustainability Topics for Sectors: What Do Stakeholders Want to Know? Research & Development Series; The Global Reporting Initiative (GRI): Amsterdam, The Netherlands, 2013.

- de Mendonca, T.; Zhou, Y. When companies improve the sustainability of the natural environment: A study of large U.S. companies. Bus. Strat. Environ. 2019, 29, 801–811. [Google Scholar] [CrossRef]

- Hanohov, R.; Baldacchino, L. Opportunity recognition in sustainable entrepreneurship: An exploratory study. Int. J. Entrep. Behav. Res. 2018, 24, 333–358. [Google Scholar] [CrossRef]

- Thomson, S.B. Sample Size and Grounded Theory. J. Adm. Gov. 2011, 1, 45–52. [Google Scholar]

- Creswell, J. Qualitative Inquiry & Research Design: Choosing among Five Approaches; Sage Publications: Thousand Oaks, CA, USA, 2007. [Google Scholar]

- Herman, R.P. The HIP Investor. Make Bigger Profits by Building a Better World; John Wiley &Sons Inc.: Hoboken, NJ, USA, 2010. [Google Scholar]

- D’Humieres, P. Towards a Sustainable European Business Model? Foundation Robert Schuman: Paris, France, 2018. [Google Scholar]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business Models for Sustainability—A Co-Evolutionary Analysis of Sustainable Entrepreneurship, Innovation, and Transformation, Organization & Environment. SAGE J. 2016, 264–289. [Google Scholar]

- Eggert, A.; Ulaga, W.; Frow, P.; Payne, A. Conceptualizing and communicating value in business markets: From value in exchange to value in use. Ind. Mark. Manag. 2018, 69, 80–90. [Google Scholar] [CrossRef]

- Jabłoński, M. Value Migration to the Sustainable Business Models of Digital Economy Companies on the Capital Market. Sustainability 2018, 10, 3113. [Google Scholar] [CrossRef]

- Evans, S.; Vladimirova, D.; Holgado, M.; Van Fossen, K.; Yang, M.; Silva, E.; Barlow, C.Y. Business Model Innovation for Sustainability: Towards a Unified Perspective for Creation of Sustainable Business Models. Bus. Strat. Environ. 2017, 26, 597–608. [Google Scholar] [CrossRef]

- Slaper, T.F.; Hall, T.J. The Triple Bottom Line: What Is It and How Does It Work? Indiana Bus. Rev. 2011, 4–8. [Google Scholar]

- Elkington, J. 25 Years Ago I Coined the Phrase “Triple Bottom Line”. Here’s Why It’s Time to Rethink It. Harvard Business Review. 2018, pp. 2–5. Available online: https://hbr.org/2018/06/25-years-ago-i-coined-the-phrase-triple-bottom-line-heres-why-im-giving-up-on-it (accessed on 10 July 2019).

- Scerri, A.; James, P. Accounting for sustainability: Combining qualitative and quantitative research in developing ‘indicators’ of sustainability. Int. J. Soc. Res. Methodol. 2010, 13, 41–53. [Google Scholar] [CrossRef]

- Lozano, R. Towards better embedding sustainability into companies’ systems: An analysis of voluntary corporate initiatives. J. Clean. Prod. 2012, 25, 14–26. [Google Scholar] [CrossRef]

- Robèrt, K.-H. Tools and concepts for sustainable development, how do they relate to a general framework for sustainable development, and to each other? J. Clean. Prod. 2000, 8, 243–254. [Google Scholar] [CrossRef]

- Bergman, M.M.; Bergman, Z.; Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 2017, 9, 753. [Google Scholar] [CrossRef]

- Boons, F.; Lüdeke-Freund, F. Business models for sustainable innovation: State-of-the-art and steps towards a research agenda. J. Clean. Prod. 2013, 45, 9–19. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Herring, H.; Sorrell, S. Energy Efficiency and Sustainable Consumption: The Rebound Effect; Palgrave Macmillan: London, UK, 2009. [Google Scholar]

- Ashford, N.; Hall, R.P.; Ashford, R.H. The crisis in employment and consumer demand: Reconciliation with environmental sustainability. Environ. Innov. Soc. Trans. 2012, 2, 1–22. [Google Scholar] [CrossRef]

- Lambert, A.; Boons, F. Eco-industrial parks: Stimulating sustainable development in mixed industrial parks. Technovation 2002, 22, 471–484. [Google Scholar] [CrossRef]

- Gibbs, D.; Deutz, P. Reflections on implementing industrial ecology through eco-industrial park development. J. Clean. Prod. 2007, 15, 1683–1695. [Google Scholar] [CrossRef]

- Mont, O.; Tukker, A. Product-Service Systems: Reviewing achievements and refining the research agenda. J. Clean. Prod. 2006, 14, 1451–1454. [Google Scholar] [CrossRef]

- Catulli, M. What uncertainty? Further insight into why consumers might be distrustful of product service systems. J. Manufac. Technol. Manag. 2012, 23, 780–793. [Google Scholar] [CrossRef]

- Jackson, T. Prosperity without Growth; Informa UK Limited: Colchester, UK, 2009. [Google Scholar]

- Nerkar, A.; Shane, S. When do start-ups that exploit patented academic knowledge survive? Int. J. Ind. Organ. 2003, 21, 1391–1410. [Google Scholar] [CrossRef]

- Giarratana, M. The birth of a new industry: Entry by start-ups and the drivers of firm growth. Res. Policy 2004, 33, 787–806. [Google Scholar] [CrossRef]

- Bawa, K.S.; Seidler, R. Dimensions of Sustainable Development—Volume I; EOLSS Publications: Abu Dhabi, UAE, 2009. [Google Scholar]

- Bawa, K.S.; Seidler, R. Dimensions of Sustainable Development—Volume II; EOLSS Publications: Abu Dhabi, UAE, 2009. [Google Scholar]

- Creswell, J.W.; Creswell, J.D. Research Design: Qualitative, Quantitative, and Mixed Methods Approaches, 5th ed.; SAGE: Los Angeles, CA, USA, 2018. [Google Scholar]

- Shelley, M.; Krippendorff, K. Content Analysis: An Introduction to its Methodology. J. Am. Stat. Assoc. 1984, 79, 240. [Google Scholar] [CrossRef]

- Agarwal, N.K. Exploring Context in Information Behavior: Seeker, Situation, Surroundings, and Shared Identities. Synth. Lect. Inf. Concepts Retr. Serv. 2017, 9. [Google Scholar] [CrossRef][Green Version]

- Feldman, M. Strategies for Interpreting Qualitative Data; SAGE Publications: Los Angeles, CA, USA, 1995. [Google Scholar]

- Gibbs, G.R. Analysing Qualitative Data; SAGE Publications: Los Angeles, CA, USA, 2008. [Google Scholar]

- Kuckartz, U. Qualitative Text Analysis: A Guide to Methods, Practice & Using Software; SAGE Publications: Los Angeles, CA, USA, 2014. [Google Scholar]

- Annual Report Accenture PLC, Form 10-K (dated 31 August 2019). Available online: https://www.sec.gov/ix?doc=/Archives/edgar/data/1467373/000146737319000339/acn831201910k.htm (accessed on 30 January 2020).

- Annual Report Akamai Technologies Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1086222/000108622219000066/akam10k123118.htm (accessed on 30 January 2020).

- Annual Report Alibaba Group Holding Ltd., Form 20-F (dated 31 March 2019). Available online: https://www.sec.gov/Archives/edgar/data/1577552/000104746919003492/a2238953z20-f.htm (accessed on 30 January 2020).

- Annual Report Alphabet Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1652044/000165204419000004/goog10-kq42018.htm (accessed on 30 January 2020).

- Annual Report Amazon.com Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1018724/000101872419000004/amzn-20181231x10k.htm (accessed on 30 January 2020).

- Annual Report Atlassian Corporation PLC, Form 20-F (dated 30 June 2019). Available online: https://www.sec.gov/Archives/edgar/data/1650372/000165037219000020/a20-f06302019.htm (accessed on 30 January 2020).

- Annual Report Automatic Data Processing Inc., Form 10-K (dated 30 June 2019). Available online: https://www.sec.gov/Archives/edgar/data/8670/000000867019000021/q4fy1910k.htm (accessed on 30 January 2020).

- Annual Report Alibaba Baidu Inc., Form 20-F (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1329099/000119312519076779/d657854d20f.htm (accessed on 30 January 2020).

- Annual Report Cerner Corp., Form 10-K (dated 29 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/804753/000080475319000009/a201810-k.htm (accessed on 30 January 2020).

- Annual Report Cisco Systems Inc., Form 10-K (dated 27 July 2019). Available online: https://www.sec.gov/Archives/edgar/data/858877/000085887719000012/csco-2019727x10k.htm (accessed on 30 January 2020).

- Annual Report IAC Interactive Corp., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/891103/000089110319000006/iac-20181231x10k.htm (accessed on 30 January 2020).

- Annual Report Match Group Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1575189/000157518919000020/mtch10-k20181231.htm (accessed on 30 January 2020).

- Annual Report Microsoft Corporation, Form 10-K (dated 30 June 2019). Available online: https://www.sec.gov/Archives/edgar/data/789019/000156459019027952/msft-10k_20190630.htm (accessed on 30 January 2020).

- Annual Report Oracle Corp., Form 10-K (dated 31 May 2019). Available online: https://www.sec.gov/Archives/edgar/data/1341439/000156459019023119/orcl-10k_20190531.htm (accessed on 30 January 2020).

- Annual Report PayPal Holdings Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1633917/000163391719000043/pypl201810-k.htm (accessed on 30 January 2020).

- Annual Report Sea Limited, Form 20-F (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1703399/000114420419011639/tv512574_20f.htm (accessed on 30 January 2020).

- Annual Report Servicenow Inc., Form 10-K (dated 31 December 2018). Available online: https://www.sec.gov/ix?doc=/Archives/edgar/data/1373715/000137371519000070/now-20181231x10k.htm (accessed on 30 January 2020).

- Annual Report Spotify Technology S.A., Form 20-F (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1639920/000156459019002688/ck0001639920-20f_20181231.htm (accessed on 30 January 2020).

- Annual Report Tencent Music Entertainment Group, Form 20-F (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1744676/000156459019012066/tme-20f_20181231.htm (accessed on 30 January 2020).

- Annual Report Yandex N.V., Form 20-F (dated 31 December 2018). Available online: https://www.sec.gov/Archives/edgar/data/1513845/000151384519000009/yndx-20181231x20f.htm (accessed on 30 January 2020).

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Baran, M. Sustainability and Its Place in the Self-Determination of Information-Based Companies. Sustainability 2020, 12, 4991. https://doi.org/10.3390/su12124991

Baran M. Sustainability and Its Place in the Self-Determination of Information-Based Companies. Sustainability. 2020; 12(12):4991. https://doi.org/10.3390/su12124991

Chicago/Turabian StyleBaran, Michał. 2020. "Sustainability and Its Place in the Self-Determination of Information-Based Companies" Sustainability 12, no. 12: 4991. https://doi.org/10.3390/su12124991

APA StyleBaran, M. (2020). Sustainability and Its Place in the Self-Determination of Information-Based Companies. Sustainability, 12(12), 4991. https://doi.org/10.3390/su12124991