Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption

Abstract

1. Introduction

2. Theoretical Background and Hypothesis

2.1. Institutional Theory on EMA Research

2.2. Stakeholder Theory on EMA Research

2.3. Environmental Management Accounting (EMA)

2.4. Institutional Pressures and EMA Adoption

2.4.1. Coercive Pressure and EMA Adoption

2.4.2. Normative Pressure and EMA Adoption

2.4.3. Mimetic Pressure and EMA Adoption

2.5. Research Conceptual Framework

3. Material and Methods

Measurement of Variables

4. Data Analysis

4.1. Assessment of Model Using PLS-SEM

4.2. Measurement Model Assessment

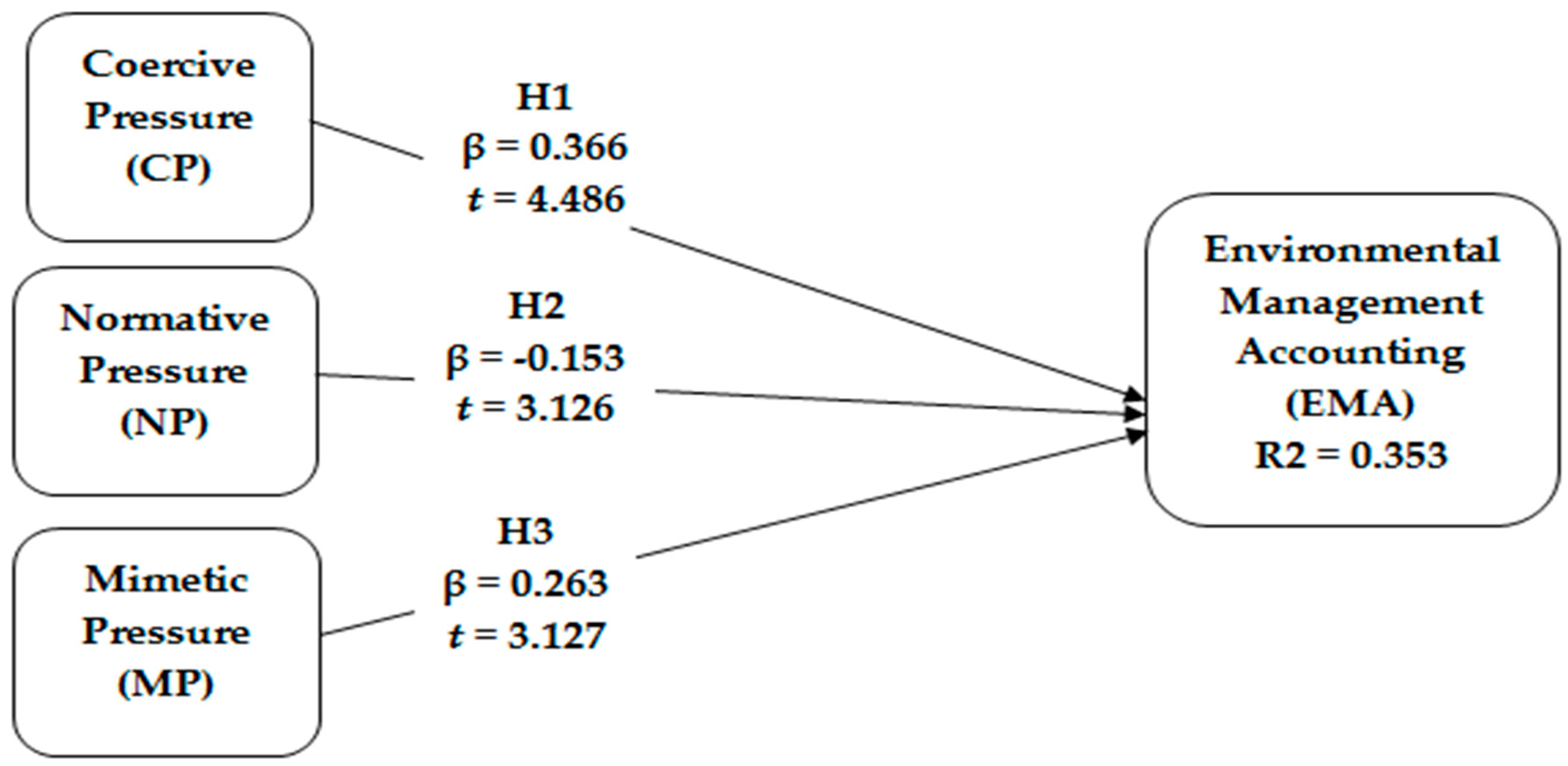

4.3. Structural Model Assessment

5. Discussion

6. Conclusions, Implications and Limitations

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Chang, H.-C.; Deegan, C. Environmental Management Accounting and environmental accountability within universities: Current practice and future potential. In Environmental Management Accounting for Cleaner Production; Springer: Berlin/Heidelberg, Germany, 2008; pp. 301–320. [Google Scholar]

- Gibassier, D.; Alcouffe, S. Environmental Management Accounting: The Missing Link to Sustainability; Taylor & Francis: Didcot, UK, 2018. [Google Scholar]

- Saeidi, S.P.; Othman, M.S.H.; Saeidi, P.; Saeidi, S. The moderating role of environmental management accounting between environmental innovation and firm financial performance. Int. J. Bus. Perform. Manag. 2018, 19, 326–348. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Business cases and corporate engagement with sustainability: Differentiating ethical motivations. J. Bus. Ethics 2018, 147, 241–259. [Google Scholar] [CrossRef]

- Burritt, R.; Environment, T. Environmental reporting in Australia: Current practices and issues for the future. Bus. Strategy Environ. 2002, 11, 391–406. [Google Scholar] [CrossRef]

- Qian, W.; Burritt, R.; Chen, J.; Change, O. The potential for environmental management accounting development in China. J. Account. Organ. Chang. 2015, 11, 406–428. [Google Scholar] [CrossRef]

- Burritt, R.L.; Herzig, C.; Tadeo, B. Environmental management accounting for cleaner production: The case of a Philippine rice mill. J. Clean. Prod. 2009, 17, 431–439. [Google Scholar] [CrossRef]

- Doorasamy, M.; Garbharran, H. The role of environmental management accounting as a tool to calculate environmental costs and identify their impact on a company’s environmental performance. Asian J. Bus. Manag. 2015, 3. [Google Scholar]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Mahmood, Z.; Ahmad, Z.; Ali, W.; Ejaz, A. Does environmental disclosure relate to environmental performance? Reconciling legitimacy theory and voluntary disclosure theory. Pak. J. Commer. Soc. Sci. 2017, 11, 1134–1152. [Google Scholar]

- Mahmood, Z.; Kouser, R.; Iqbal, Z. Why Pakistani small and medium enterprises are not reporting on sustainability practices? Pak. J. Commer. Soc. Sci. 2017, 11, 389–405. [Google Scholar]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Mahmood, Z.; Ahmad, Z. Quest for Alternative Sociological Perspectives on Corporate Social and Environmental Reporting. J. Account. Financ. Emerg. Econ. 2015, 1, 135–153. [Google Scholar] [CrossRef][Green Version]

- Baird, K.; Harrison, G.; Reeve, R.J.A. Success of activity management practices: The influence of organizational and cultural factors. Account. Financ. 2007, 47, 47–67. [Google Scholar] [CrossRef]

- Tung, A.; Baird, K.; Schoch, H. The relationship between organisational factors and the effectiveness of environmental management. J. Environ. Manag. 2014, 144, 186–196. [Google Scholar] [CrossRef] [PubMed]

- Colwell, S.R.; Joshi, A. Corporate ecological responsiveness: Antecedent effects of institutional pressure and top management commitment and their impact on organizational performance. Bus. Strategy Environ. 2013, 22, 73–91. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and intrinsic drivers of corporate social performance: Evidence from foreign and domestic firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 1983, 147–160. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L. Necessity as the mother of ‘green’inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Abdullah, M.; Zailani, S.; Iranmanesh, M.; Jayaraman, K. Barriers to green innovation initiatives among manufacturers: The Malaysian case. Rev. Manag. Sci. 2016, 10, 683–709. [Google Scholar] [CrossRef]

- Zailani, S.; Govindan, K.; Iranmanesh, M.; Shaharudin, M.R.; Chong, Y. Green innovation adoption in automotive supply chain: The Malaysian case. J. Clean. Prod. 2015, 108, 1115–1122. [Google Scholar] [CrossRef]

- Caldera, H.; Desha, C.; Dawes, L. Exploring the role of lean thinking in sustainable business practice: A systematic literature review. J. Clean. Prod. 2017, 167, 1546–1565. [Google Scholar] [CrossRef]

- Mallak, S.K.; Ishak, M.B.; Mohamed, A.F.; Iranmanesh, M. Toward sustainable solid waste minimization by manufacturing firms in Malaysia: Strengths and weaknesses. Environ. Monit. Assess. 2018, 190, 575. [Google Scholar] [CrossRef] [PubMed]

- Zailani, S.; Iranmanesh, M.; Sean Hyun, S.; Ali, M. Applying the theory of consumption values to explain drivers’ willingness to pay for biofuels. Sustainability 2019, 11, 668. [Google Scholar] [CrossRef]

- Hofer, C.; Eroglu, C.; Hofer, A. The effect of lean production on financial performance: The mediating role of inventory leanness. Int. J. Prod. Econ. 2012, 138, 242–253. [Google Scholar] [CrossRef]

- Ferreira, A.; Moulang, C.; Hendro, B.J.A.A. Environmental management accounting and innovation: An exploratory analysis. Auditing 2010, 23, 920–948. [Google Scholar] [CrossRef]

- Christ, K.L.; Burritt, R. Environmental management accounting: The significance of contingent variables for adoption. J. Clean. Prod. 2013, 41, 163–173. [Google Scholar] [CrossRef]

- Johnstone, B. Discourse Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2018. [Google Scholar]

- Jasch, C. The use of Environmental Management Accounting (EMA) for identifying environmental costs. J. Clean. Prod. 2003, 11, 667–676. [Google Scholar] [CrossRef]

- Wilmshurst, T.D.; Frost, G.A. Corporate environmental reporting: A test of legitimacy theory. Auditing 2000, 13, 10–26. [Google Scholar] [CrossRef]

- Heugens, P.P.; Lander, M. Structure! Agency!(and other quarrels): A meta-analysis of institutional theories of organization. Acad. Manag. J. 2009, 52, 61–85. [Google Scholar] [CrossRef]

- Teo, H.-H.; Wei, K.K.; Benbasat, I. Predicting intention to adopt interorganizational linkages: An institutional perspective. MIS Q. 2003, 2003, 19–49. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental management in SME s in the UK: Practices, pressures and perceived benefits. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Abdulaziz, N.A.; Senik, R.; Yau, F.S.; San, O.T.; Attan, H. Influence of Institutional Pressures on the Adoption of Green Initiatives. Int. J. Econ. Manag. 2017, 11, 939–967. [Google Scholar]

- Liang, H.; Saraf, N.; Hu, Q.; Xue, Y. Assimilation of enterprise systems: The effect of institutional pressures and the mediating role of top management. MIS Q. 2007, 2007, 59–87. [Google Scholar] [CrossRef]

- Roxas, B.; Coetzer, A. Institutional environment, managerial attitudes and environmental sustainability orientation of small firms. J. Bus. Ethics 2012, 111, 461–476. [Google Scholar] [CrossRef]

- Latan, H.; Jabbour, C.J.C.; de Sousa Jabbour, A.B.L.; Wamba, S.F.; Shahbaz, M. Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. J. Clean. Prod. 2018, 180, 297–306. [Google Scholar] [CrossRef]

- Deephouse, D. Does isomorphism legitimate? Acad. Manag. J. 1996, 39, 1024–1039. [Google Scholar] [CrossRef]

- Gunarathne, N.; Lee, K.-H.; Change, O. Environmental Management Accounting (EMA) for environmental management and organizational change: An eco-control approach. J. Account. Organ. Chang. 2015, 11, 362–383. [Google Scholar] [CrossRef]

- Jansson, J.; Nilsson, J.; Modig, F.; Hed Vall, G. Commitment to sustainability in small and medium-sized enterprises: The influence of strategic orientations and management values. Bus. Strategy Environ. 2017, 26, 69–83. [Google Scholar] [CrossRef]

- Daddi, T.; Testa, F.; Frey, M.; Iraldo, F. Exploring the link between institutional pressures and environmental management systems effectiveness: An empirical study. J. Environ. Manag. 2016, 183, 647–656. [Google Scholar] [CrossRef]

- Wang, S.; Li, J.; Song, J.; Li, Y.; Sherk, M. Institutional pressures and product modularity: Do supply chain coordination and functional coordination matter? Int. J. Prod. Res. 2018, 56, 6644–6657. [Google Scholar] [CrossRef]

- Phan, T.N.; Baird, K.; Su, S. The use and effectiveness of environmental management accounting. J. Environ. Manag. 2017, 24, 355–374. [Google Scholar] [CrossRef]

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3. Acad. Manag. Rev. 2014, 9, 419–445. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Matthews, L.M.; Matthews, R.L.; Sarstedt, M. PLS-SEM or CB-SEM: Updated guidelines on which method to use. Int. J. Multivar. Data Anal. 2017, 1, 107–123. [Google Scholar] [CrossRef]

- Nitzl, C.; Roldan, J.L.; Cepeda, G. Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Ind. Manag. Data Syst. 2016, 116, 1849–1864. [Google Scholar] [CrossRef]

- Gefen, D.; Straub, D.; Boudreau, M.-C. Structural equation modeling and regression: Guidelines for research practice. Commun. Assoc. Inf. Syst. 2000, 4, 7. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM) An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- George, D. SPSS for Windows Step by Step: A Simple Study Guide and Reference, 17.0 Update, 10/e; Pearson Education India: Bengaluru, India, 2011. [Google Scholar]

{kind=link}

{kind=link}

| Demographic Constructs | Frequency | Percentage (%) | |

|---|---|---|---|

| Gender | Male | 214 | 89.16 |

| Female | 26 | 10.83 | |

| Age | 21 to 30 | 34 | 14.16 |

| 31 to 40 | 74 | 30.83 | |

| 41 to 50 | 130 | 54.16 | |

| Above 50 | 2 | 0.833 | |

| Working experience | 1–5 years | - | - |

| 6–10 years | 20 | 8.33 | |

| 11–15 years | 40 | 16.66 | |

| More than 15 years | 180 | 75.00 | |

| Education | Undergraduate | 40 | 16.67 |

| Post Graduate (Certification) | 200 | 83.33 | |

| Industry Type | Chemical and Fertilizer | 65 | 27.08 |

| Textile | 77 | 32.08 | |

| Oil and Refinery | 12 | 5.00 | |

| Food and Beverages | 86 | 35.83 | |

| Total | 240 | 100 |

| Constructs | Operationalization | Adapted From |

|---|---|---|

| Coercive Pressure | 1. Our firm tries to reduce the threat from the environmental regulations by implementing environmental management accounting; 2. Environmental regulations are important for our firm to implement environmental management accounting; 3. The local government has set strict environmental standards, which our firm needs to comply with; 4. Several penalties have been imposed on firms that violate environmental standards and regulations. | Adapted from the scales of several authors [17,37,42,43] |

| Normative Pressure | 1. The increasing environmental consciousness of consumers has spurred our firm to implement environmental management accounting; 2. Being environmentally responsible and disclosure of environmental information is a basic requirement for our firm to be part of this industry; 3. Nongovernmental organizations around our firm expect all firms in the industry to implement environmental management accounting; 4. Stakeholders may not support our firm if our firm does not implement environmental management accounting. | Adapted from the scales of several authors [17,37,42,43] |

| Mimetic Pressure | 1. The leading companies in our industry set an example in the field of implementing environmental management accounting; 2. The leading companies in our industry are well-known for implementing environmental management accounting; 3. The leading companies in our industry are intending to reduce their impacts on the environment by implementing environmental management accounting; 4. The leading companies in our industry have obtained competitive advantages by implementing environmental management accounting. | Adapted from the scales of several authors [17,37,42,43] |

| Environmental Management Accounting | 1. Our firm’s accounting system records all physical inputs and outputs (such as energy, water, materials, wastes, and emissions); 2. Our firm’s accounting system can carry out product inventory analyses, product improvement analysis and product environmental impacts analyses; 3. Our firm uses environmental performance targets for physical inputs and outputs; 4. Our firm’s accounting system can identify, estimate and classify environmental-related costs and liabilities; 5. Our firm’s accounting system can create and use environmental-related cost accounts; 6. Our firm’s accounting system can allocate environmental-related costs to products. | Adapted from the scales of several authors [27,28,44] |

| CP | EMA | MP | NP | |

|---|---|---|---|---|

| CP1 | 0.834 | 0.409 | 0.482 | −0.039 |

| CP2 | 0.823 | 0.403 | 0.528 | −0.074 |

| CP3 | 0.827 | 0.483 | 0.510 | −0.005 |

| CP4 | 0.828 | 0.470 | 0.578 | 0.016 |

| EMA1 | 0.304 | 0.784 | 0.376 | −0.197 |

| EMA2 | 0.478 | 0.854 | 0.468 | −0.111 |

| EMA3 | 0.493 | 0.853 | 0.362 | −0.148 |

| EMA4 | 0.453 | 0.868 | 0.420 | −0.156 |

| EMA5 | 0.417 | 0.847 | 0.379 | −0.152 |

| EMA6 | 0.480 | 0.737 | 0.449 | −0.094 |

| MP1 | 0.523 | 0.359 | 0.830 | 0.024 |

| MP2 | 0.598 | 0.436 | 0.808 | −0.040 |

| MP3 | 0.474 | 0.356 | 0.829 | −0.015 |

| MP4 | 0.478 | 0.459 | 0.809 | −0.043 |

| NP1 | 0.021 | −0.091 | −0.019 | 0.763 |

| NP2 | −0.038 | −0.130 | −0.014 | 0.892 |

| NP3 | −0.025 | −0.115 | 0.009 | 0.914 |

| NP4 | −0.035 | −0.201 | −0.046 | 0.858 |

| Constructs | Item | Factor Loading | Cronbach’s Alpha (CA) | Composite Reliability (CR) | Average Variance Extracted (AVE) |

|---|---|---|---|---|---|

| Coercive Pressure (CP) | CP1 | 0.834 | 0.848 | 0.897 | 0.686 |

| CP2 | 0.823 | ||||

| CP3 | 0.827 | ||||

| CP4 | 0.828 | ||||

| Normative Pressure (NP) | NP1 | 0.763 | 0.887 | 0.918 | 0.737 |

| NP2 | 0.892 | ||||

| NP3 | 0.914 | ||||

| NP4 | 0.858 | ||||

| Mimetic Pressure (MP) | MP1 | 0.830 | 0.838 | 0.891 | 0.671 |

| MP2 | 0.808 | ||||

| MP3 | 0.829 | ||||

| MP4 | 0.809 | ||||

| Environmental Management Accounting (EMA) | EMA1 | 0.784 | 0.906 | 0.927 | 0.681 |

| EMA2 | 0.854 | ||||

| EMA3 | 0.853 | ||||

| EMA4 | 0.868 | ||||

| EMA5 | 0.847 | ||||

| EMA6 | 0.737 |

| CP | EMA | MP | NP | |

|---|---|---|---|---|

| Coercive Pressure (CP) | ---------- | |||

| Environmental Management Accounting (EMA) | 0.601 | |||

| Mimetic Pressure (MP) | 0.747 | 0.561 | ||

| Normative Pressure (NP) | 0.056 | 0.177 | 0.042 | ---------- |

| Constructs | R2 Value | Interpretation |

|---|---|---|

| Environmental Management Accounting (EMA) | 0.353 | Moderate |

| Hypotheses | Relationships | β | Standard Deviation | t-Values | p-Values | Assessments |

|---|---|---|---|---|---|---|

| H1 | CP -> EMA | 0.366 | 0.081 | 4.486 | 0.000 | Supported |

| H2 | NP -> EMA | −0.153 | 0.049 | 3.126 | 0.002 | Supported |

| H3 | MP -> EMA | 0.263 | 0.084 | 3.127 | 0.002 | Supported |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Latif, B.; Mahmood, Z.; Tze San, O.; Mohd Said, R.; Bakhsh, A. Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability 2020, 12, 4506. https://doi.org/10.3390/su12114506

Latif B, Mahmood Z, Tze San O, Mohd Said R, Bakhsh A. Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability. 2020; 12(11):4506. https://doi.org/10.3390/su12114506

Chicago/Turabian StyleLatif, Badar, Zeeshan Mahmood, Ong Tze San, Ridzwana Mohd Said, and Allah Bakhsh. 2020. "Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption" Sustainability 12, no. 11: 4506. https://doi.org/10.3390/su12114506

APA StyleLatif, B., Mahmood, Z., Tze San, O., Mohd Said, R., & Bakhsh, A. (2020). Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability, 12(11), 4506. https://doi.org/10.3390/su12114506