Do Reputable Underwriters Affect the Sustainability of Newly Listed Firms? Evidence from South Korea

Abstract

1. Introduction

2. Prior Literature and Hypothesis Development

3. Research Design

3.1. Measurement of an Underwriter’s Reputation

3.2. Sample Selection

3.3. Research Model

| Definition of Variables | |

| 1. | The probability that a company that existed until Time t will be delisted at Time t per unit hour |

| 2. | Baseline hazard: Probability of delisting when the covariates are all 0 |

| 3. exp(z) | Factors considered to have an impact on corporate delisting |

| Definition of Independent Variables (REPU: Reputation) | |

| 1. NUM | Number of successful public offerings a year before the IPO by the underwriter of the newly listed firms |

| 2. NUM_RATIO | Ratio of the number of the underwriter’s public offerings of newly listed firms in the year before the listing |

| 3. NUM_ORDER | Underwriter’s ranking measured (descending) by the number of public offerings made before the new firm’s listing |

| 4. AMO | Amount of successful public offerings a year before the IPO by the underwriter of the newly listed firms to be listed (Unit: Won) |

| 5. AMO_RATIO | Ratio of the amount of the underwriter’s public offerings in the year before the new firm’s listing |

| 6. AMO_ORDER | Underwriter’s ranking measured (descending) by the amount of public offerings before the new firm’s listing |

| 7. L_NUM | Number of successful public offerings a year before the IPO by the underwriter of the newly listed firms to be listed in the case of a representative underwriter |

| 8. L_NUM_RATIO | Ratio of the number of the underwriter’s public offerings of newly listed firms in the year before the listing in the case of a representative underwriter |

| 9. L_NUM_ORDER | Underwriter’s ranking measured (descending) by the number of public offerings made before the new firm’s listing in the case of a representative underwriter |

| Definition of Control Variables | |

| 1. IPO_VOL | Total number of public offerings at the time of the firm’s new listing |

| 2. SALES | Natural log of total sales |

| 3. SIZE | Natural log of total assets |

| 4. LEV | Total debt divided by total assets |

| 5. C_RATIO | Current liabilities divided by current assets |

| 6. ROA | Net income divided by total assets |

| 7. AGE | The newly listed firm’s establishment year minus the listing year |

| 8. OCF | Natural log of operating cash flow |

| 9. DA | Discretionary accrual calculated by the Jones [59] model |

| 10. AUDIT_DUM | 1 if newly listed company is from a BIG 4 firm and 0 otherwise |

| 11. YD | Year dummy |

4. Empirical Results

4.1. Descriptive Statistics

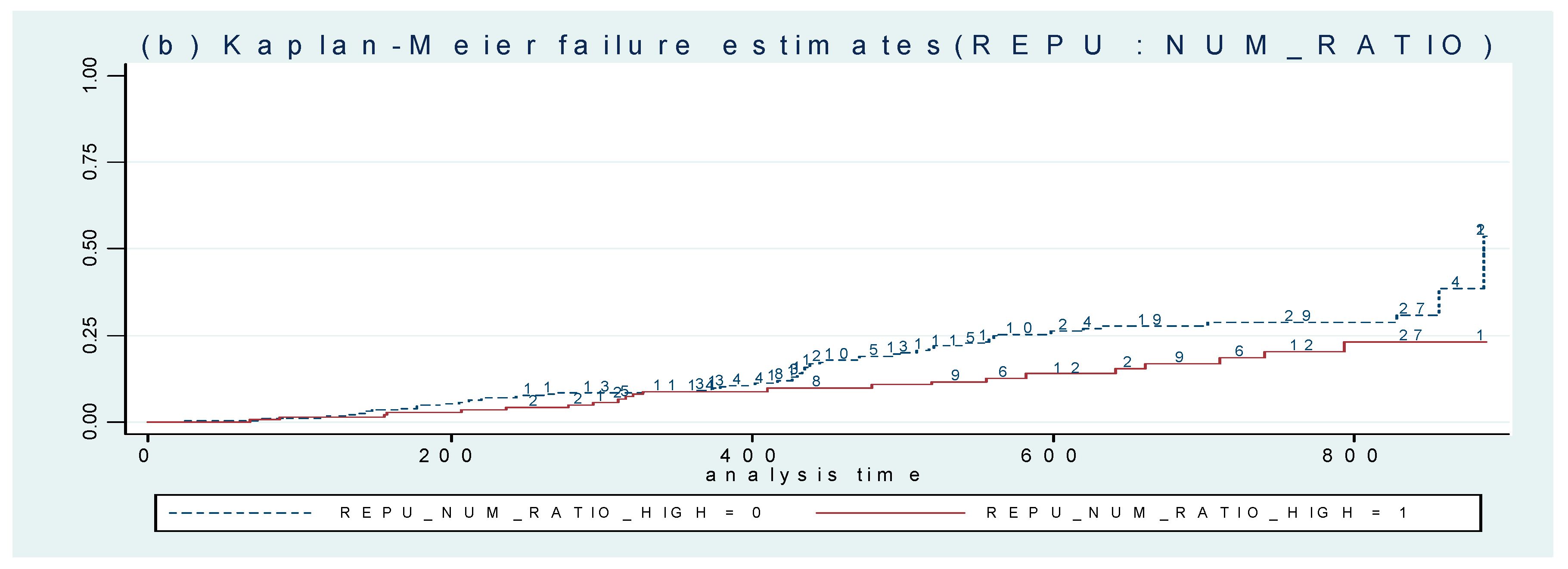

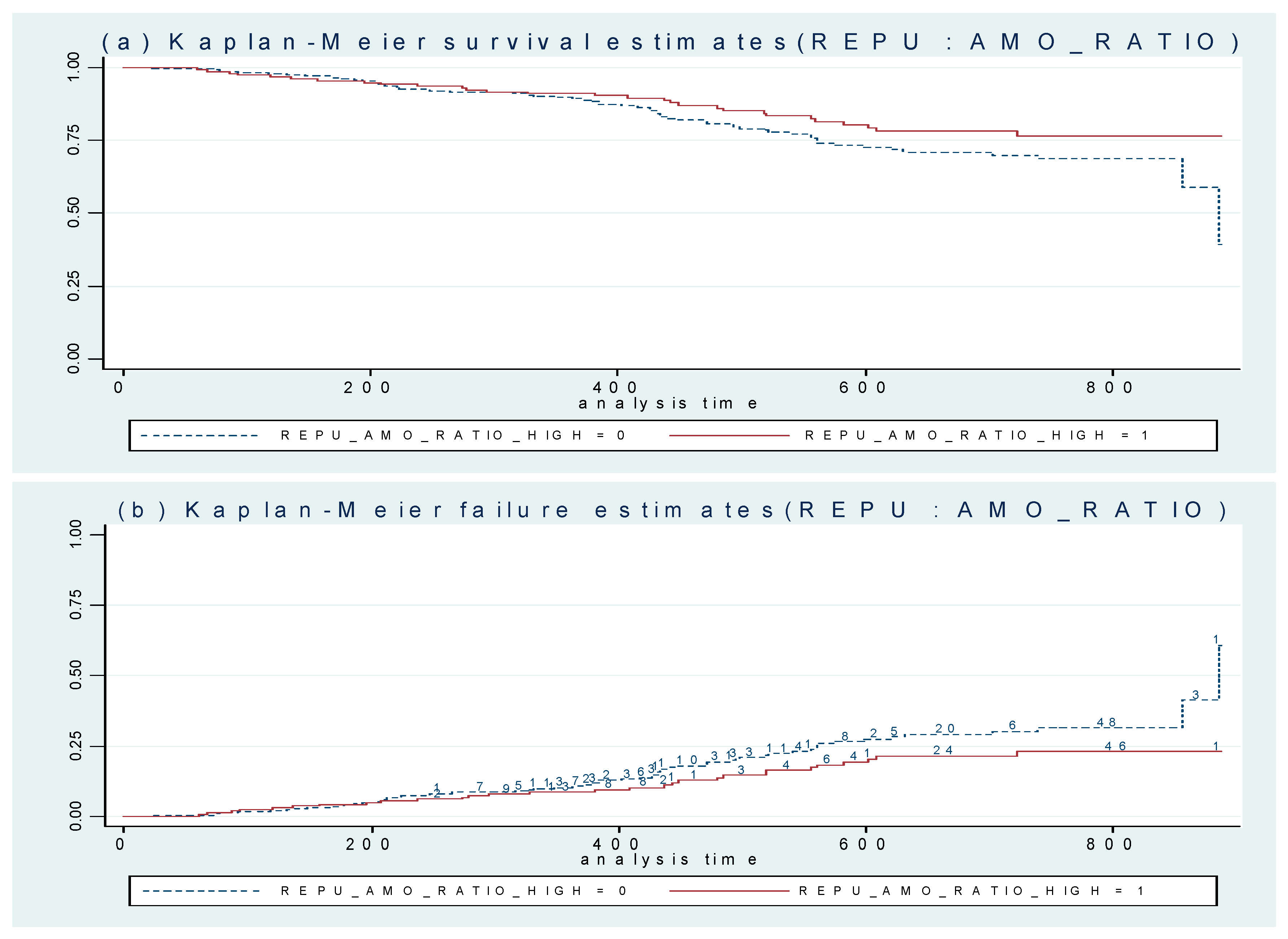

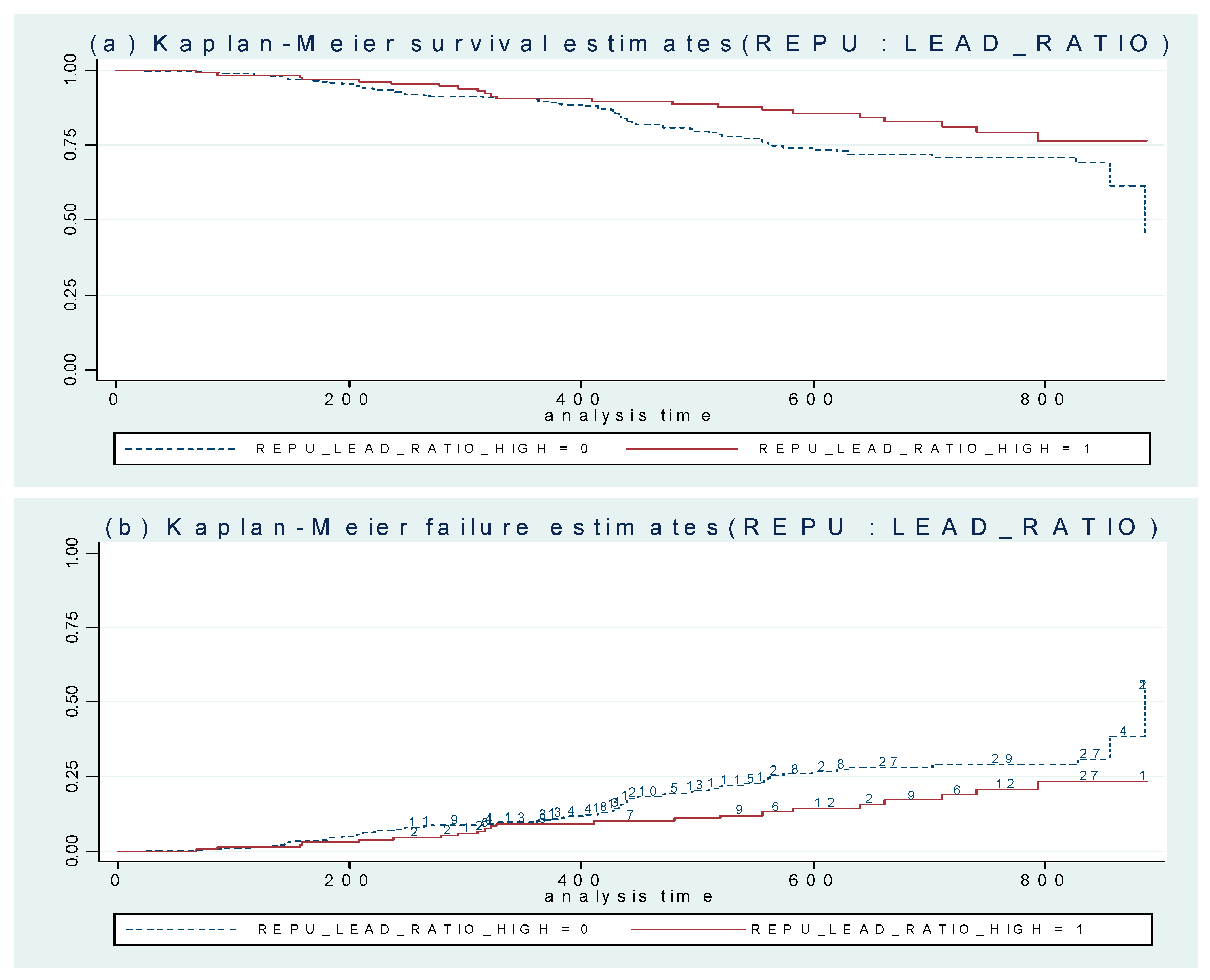

4.2. Kaplan–Meier Analysis

4.3. Cox Proportional Hazards Model

5. Discussion and Conclusions

Funding

Conflicts of Interest

References

- Li, R.; Liu, W.; Liu, Y.; Tsai, S.B. IPO Underpricing After the 2008 Financial Crisis: A Study of the Chinese Stock Markets. Sustainability 2018, 10, 2844. [Google Scholar] [CrossRef]

- Fernando, C.S.; Gatchev, V.A.; Spindt, P.A. Wanna dance? How firms and underwriters choose each other. J. Financ. 2005, 60, 2437–2469. [Google Scholar] [CrossRef]

- Carter, R.B.; Manaster, S. Initial public offerings and underwriter reputation. J. Financ. 1990, 45, 1045–1067. [Google Scholar] [CrossRef]

- Megginson, W.L.; Weiss, K.A. Venture capitalist certification in initial public offerings. J. Financ. 1991, 46, 879–903. [Google Scholar] [CrossRef]

- Lee, K.H.; Woo, J.J.; Ryoo, H.S. The Financial Features of Venture Businesses Listed on KOSDAQ. Adv. S. E. Innov. Res. 2000, 3, 105–123. [Google Scholar]

- Park, S.W.; Lee, K.H.; Nam, K.P. The Grandstanding of Venture Capitalist and the Aftermarket Performance of IPOs. Korean Manag. Rev. 2002, 31, 1631–1657. [Google Scholar]

- Yoon, B.S. The Impact of Underwriter’s Reputation on the KOSDAQ’s IPOs. Korean J. Bus. Adm. 2003, 16, 105–220. [Google Scholar]

- Lee, J.Y.; Park, J.G.; Kim, C.G. A Study on the Earnings Management of KOSDAQ IPO Firms. Korean J. Bus. Adm. 2005, 18, 2681–2700. [Google Scholar]

- Lee, J. The Hot and Cold Market Impacts on Underpricing of Certification, Reputation and Conflicts of Interest in Venture Capital Backed Korean IPOs. Adv. S. E. Innov. Res. 2009, 12, 45–68. [Google Scholar]

- Lee, S.; Kim, J.S.; Ryu, D. Venture Capitalist Certification in Initial Public Offerings: The Case of KOSDAQ Market. Korean Corp. Manag. Rev. 2010, 17, 1–22. [Google Scholar]

- Lee, G.; Masulis, R.W. Do more reputable financial institutions reduce earnings management by IPO issuers? J. Corp. Financ. 2011, 17, 982–1000. [Google Scholar] [CrossRef]

- Hwang, K.; Kang, P.; Kim, N. The Impact of Underwriter’s Reputation on IPO Firm’s Earnings Management. Korean Acad. Soc. Account. 2015, 20, 93–120. [Google Scholar]

- Lizińska, J.; Czapiewski, L. Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance? Sustainability 2018, 10, 4349. [Google Scholar] [CrossRef]

- Kaplan, E.L.; Meier, P. Nonparametric estimation from incomplete observations. J. Am. Stat. Assoc. 1958, 53, 457–481. [Google Scholar] [CrossRef]

- Cox, D.R. Regression models and life-table (with discussion). J. R. Stat. Soc. 1972, 34, 187–220. [Google Scholar]

- Lockett, A.; Moon, J.; Visser, W. Corporate social responsibility in management research: Focus, nature, salience and sources of influence. J. Mgt. Stud. 2006, 43, 115–136. [Google Scholar] [CrossRef]

- Simões, P.; Marques, R. Influence of regulation on the productivity of waste utilities. What can we learn with the Portuguese experience? Waste Mgt. 2012, 32, 1266–1275. [Google Scholar] [CrossRef]

- Dye, R. Earnings management in an overlapping generations model. J. Account. Res. 1988, 26, 195–235. [Google Scholar] [CrossRef]

- Teoh, S.; Welch, I.; Wong, T. Earnings management and the long-run market performance of initial public offerings. J. Financ. 1998, 53, 1935–1974. [Google Scholar] [CrossRef]

- Teoh, S.; Wong, T.; Rao, G. Are accruals during initial public offerings opportunistic? Rev. Account. Stud. 1998, 3, 175–208. [Google Scholar] [CrossRef]

- Affleck-Graves, J.; Callahan, C.M.; Chipalkatti, N. Earnings predictability, information asymmetry, and market liquidity. J. Account. Res. 2002, 40, 561–583. [Google Scholar] [CrossRef]

- Li, J.; Zhang, L.; Zhou, J. Earnings Management and Delisting Risk of Initial Public Offerings; Working Paper; Simon School, University of Rochester, Research Paper Series; 2006; Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=641021 (accessed on 8 May 2019).

- Krishnan, C.N.V.; Masulis, R.W.; Ivanov, V.I.; Singh, A.K. Venture capital reputation and post-IPO performance, and corporate governance. J. Financ. Quant. Anal. 2011, 46, 1295–1333. [Google Scholar] [CrossRef]

- Barry, C.B.; Muscarella, C.J.; Peavy, J.W., III; Vetsuypens, M.R. The role of venture capital in the creation of public companies: Evidence from the going-public process. J. Financ. Econ. 1990, 27, 447–471. [Google Scholar] [CrossRef]

- De, S.; Nabar, P. Economic implications of imperfect quality certification. Econ. Lett. 1991, 37, 333–337. [Google Scholar] [CrossRef]

- Titman, S.; Trueman, B. Information Quality and the Valuation of New Issues. J. Account. Econ. 1986, 8, 159–172. [Google Scholar] [CrossRef]

- Chemmanur, T.; Fulghieri, P. Investment Bank Reputation, Information Production, and Financial Intermediation. J. Financ. 1994, 49, 57–79. [Google Scholar] [CrossRef]

- Habib, M.; Ljungqvist, A. Underpricing and Entreprenurial Wealth Losses in IPOs: Theory and Evidence. Rev. Financ. Stud. 2001, 14, 433–458. [Google Scholar] [CrossRef]

- Benveniste, L.; Ljungqvist, A.; Wilhelm, W.; Yu, X. Evidence of Information Spillovers in the Production of Investment Banking Services. J. Financ. 2003, 58, 577–608. [Google Scholar] [CrossRef]

- Ljungqvist, A.; Marston, F.; Wilhelm, W. Competing for Securities Underwriting Mandates: Banking Relationships and Analyst Recommendations. J. Financ. 2006, 61, 301–340. [Google Scholar] [CrossRef]

- Beatty, R.; Ritter, J.R. Investment banking, reputation and the underpricing of initial public offerings. J. Financ. Econ. 1986, 15, 213–232. [Google Scholar] [CrossRef]

- Booth, J.R.; Smith, R.L. Capital raising, underwriting and the certification hypothesis. J. Financ. Econ. 1986, 15, 261–281. [Google Scholar] [CrossRef]

- Carter, R.B.; Dark, F.H.; Singh, A.K. Underwriter Reputation, Initial Returns, and the Long-Run Performance of IPO Stocks. J. Financ. 1998, 53, 285–311. [Google Scholar] [CrossRef]

- Dunbar, C.G. Factors affecting investment bank initial public offering market share. J. Financ. Econ. 2000, 55, 3–41. [Google Scholar] [CrossRef]

- Fang, L.H. Investment bank reputation and the price and quality of underwriting services. J. Financ. 2005, 60, 2729–2761. [Google Scholar] [CrossRef]

- Choi, K.; Kim, M. Initial Public Offerings and Earnings Management. Korean Account. Rev. 1997, 22, 1–27. [Google Scholar]

- Choi, W.S. Firm-Bank Relationship and The Corporate Governance Role of Banks: Evidence from Borrower’s Accounting Conservatism; Working Paper; California State University: Long Beach, CA, USA, 2005. [Google Scholar]

- Choi, J.S.; Kwak, Y.M.; Baek, J.H. Earnings Management around Initial Public Offerings in KOSDAQ Market Associated with Managerial Opportunism. Korean Account. Rev. 2010, 35, 37–80. [Google Scholar]

- Ragan, S. Earnings management and the performance of seasoned equity offerings. J. Financ. Econ. 1998, 50, 101–122. [Google Scholar]

- Du Charme, L.L.; Malatesta, P.H.; Sefcik, S.E. Earnings management, stock issues, and shareholder lawsuits. J. Financ. Econ. 2004, 71, 27–49. [Google Scholar] [CrossRef]

- Lee, G.; Masulis, R.W. Seasoned equity offerings: Quality of accounting information and expected flotation costs. J. Financ. Econ. 2009, 92, 443–469. [Google Scholar] [CrossRef]

- Nam, K.P.; Park, S.W.; Lee, K.H. The Long-term Performance of Venture Capital-Backed IPOs. Korean J. Bus. Adm. 2003, 37, 687–711. [Google Scholar]

- Kim, I.S.; Lee, H.I.; Choi, S.H. Earnings Management of Initial Public Offerings: Evidence from Venture Capital-Backed Firms. Korean Account. Rev. 2014, 39, 179–212. [Google Scholar]

- Cruz, N.; Marques, R. Scorecards for sustainable local governments. Cities 2014, 39, 165–170. [Google Scholar] [CrossRef]

- Jo, H.; Kim, Y.; Park, M.S. Underwriter choice and earnings management: Evidence from seasoned equity offerings. Rev. Account. Stud. 2007, 12, 23–59. [Google Scholar] [CrossRef]

- Hensler, D.A.; Rutherford, R.C.; Springer, T.M. The survival of initial public offerings in the aftermarket. J. Financ. Res. 1997, 20, 93–110. [Google Scholar] [CrossRef]

- Bradley, D.; Clarke, J.; Cooney, J. The impact of reputation on analysts’ conflicts of interest. Hot versus cold markets. J. Bank. Financ. 2012, 36, 2190–2202. [Google Scholar] [CrossRef]

- Kwak, Y.M.; Choi, J.S. Survival Analysis of IPO Firms Engaging in Earnings Management: Evidence from KOSDAQ Market. Korean Account. J. 2011, 20, 231–263. [Google Scholar]

- Alhadab, M.; Clacherm, I.; Keasey, K. Real and accrual earnings management and IPO failure risk. Account. Bus. Res. 2015, 45, 55–92. [Google Scholar] [CrossRef]

- Kim, S. Financial Information Asymmetry and Delisting of IPO Firms. J. Korean Data Anal. Soc. 2018, 20, 1269–1280. [Google Scholar]

- Gompers, P. Grandstanding in the venture capital industry. J. Financ. Econ. 1996, 42, 133–156. [Google Scholar] [CrossRef]

- Lee, K.H.; Woo, J.J. An Empirical Analysis of the Role of Venture Capitalists in KOSDAQ IPOs market. Korean Assoc. Small Bus. Stud. 2002, 5, 3–27. [Google Scholar]

- Yoon, B.S.; Lee, K.H. The Impact of Venture Capitalist’s Reputation on KOSDAQ IPOs. Asia Pac. J. Small Bus. 2003, 25, 239–269. [Google Scholar]

- Aggarwal, R.K.; Krigman, L.; Womack, K.L. Strategic IPO Underpricing, Information Momentum, and Lockup Expiration Selling. J. Financ. Econ. 2002, 66, 105–137. [Google Scholar] [CrossRef]

- Kim, N.; Hwang, K. Impact of Underwriter reputation on the accounting conservatism of the IPO firm: South Korean cases. Int. J. Econ. Pol. Emerg. Econ. 2018, 11, 238–247. [Google Scholar] [CrossRef]

- Lewis, S. Taking A Private Company Public; Scott Printing Corporation: Jersey City, NJ, USA, 1984. [Google Scholar]

- Monroe, A. Just like film stars Wall Streeters battle to get top billing. Wall Street Journal, 15 January 1986; p. 1. [Google Scholar]

- Mata, J.; Portugal, P.; Guimaraes, P. The Survival of New Plants: Start-up Conditions and Post-entry Evolution. Int. J. Ind. Org. 1995, 13, 459–481. [Google Scholar] [CrossRef]

- Jones, J. Earnings management during import relief investigation. J. Account. Res. 1991, 29, 193–228. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel A. Descriptive statistics for firm characteristic variables. | |||||

| Variables | Mean | Median | Max. | min. | Std. Dev. |

| NUM | 6.8535 | 5 | 23 | 0 | 5.5546 |

| NUM_RATIO | 0.0762 | 0.0694 | 0.2321 | 0 | 0.0549 |

| NUM_ORDER | 6.9712 | 5 | 25 | 1 | 5.5836 |

| AMO | 18.2314 | 18.2919 | 21.2451 | 0 | 1.3282 |

| AMO_RATIO | 0.0725 | 0.0560 | 0.4936 | 0 | 0.0771 |

| AMO_ORDER | 8.1335 | 7 | 27 | 1 | 6.1393 |

| L_NUM | 6.6705 | 5 | 23 | 0 | 5.5747 |

| L_NUM_RATIO | 0.0745 | 0.0667 | 0.2405 | 0 | 0.0559 |

| L_NUM_ORDER | 7.0221 | 5 | 25 | 1 | 5.6105 |

| IPO_VOL | 24.5681 | 24.4353 | 30.3190 | 22.1220 | 1.1179 |

| SALES | 22.6462 | 22.6617 | 28.3482 | 15.6785 | 1.5763 |

| SIZE | 24.6299 | 24.4517 | 30.1052 | 22.2987 | 1.0925 |

| LEV | 0.3104 | 0.2901 | 0.9889 | 0.0018 | 0.1726 |

| C_RATIO | 150.3353 | 2.9182 | 101362.6 | 0.1602 | 3334.598 |

| ROA | 0.0742 | 0.0793 | 0.4136 | −0.5020 | 0.0879 |

| AGE | 2.2409 | 2.1972 | 4.0604 | 0 | 0.6935 |

| OCF | 22.0942 | 22.1508 | 28.7352 | 17.2909 | 1.4817 |

| DA | 0.0583 | 0.0431 | 0.6894 | −0.8895 | 0.1559 |

| AUDIT_DUM | 0.5546 | 1 | 1 | 0 | 0.4972 |

| Panel B. Mean characteristic variable values for surviving and delisted firms and differences between them. | |||||

| Variables | Surviving | Delisting | t-Stats | ||

| NUM | 6.9964 | 7.9920 | −1.9951 ** | ||

| NUM_RATIO | 0.0732 | 0.0586 | 4.0674 *** | ||

| NUM_ORDER | 7.0812 | 8.6968 | −3.1560 *** | ||

| AMO | 18.1363 | 17.9491 | 1.8321 * | ||

| AMO_RATIO | 0.0719 | 0.0578 | 2.7804 *** | ||

| AMO_ORDER | 8.2052 | 9.7872 | −2.9032 *** | ||

| L_NUM | 7.0123 | 7.9894 | -1.9574 * | ||

| L_NUM_RATIO | 0.0734 | 0.0585 | 4.1321 *** | ||

| L_NUM_ORDER | 6.9234 | 8.6489 | −3.3761 *** | ||

| IPO_VOL | 24.5693 | 23.9607 | 8.1499 *** | ||

| SALES | 22.6834 | 22.4898 | 1.3365 | ||

| SIZE | 24.6029 | 24.0905 | 7.0798 *** | ||

| LEV | 0.2993 | 0.3944 | −6.0096 *** | ||

| C_RATIO | 4.8341 | 3.8558 | 2.1806 ** | ||

| ROA | 0.0875 | 0.0487 | 4.7473 *** | ||

| AGE | 2.2749 | 1.9596 | 6.5219 *** | ||

| OCF | 22.523 | 21.3319 | 4.5379 *** | ||

| DA | 0.0513 | 0.0943 | −2.6819 *** | ||

| AUDIT_DUM | 0.5636 | 0.3670 | 4.8835 *** | ||

| (1) | (2) | (3) | ||||

|---|---|---|---|---|---|---|

| Coef. | H.R. | Coef. | H.R. | Coef. | H.R. | |

| NUM | −0.0159 *** | 0.9842 | ||||

| (−22.98) | ||||||

| NUM_RATIO | −2.2490 *** | 0.1055 | ||||

| (−9.79) | ||||||

| NUM_ORDER | 0.0020 | 1.0020 | ||||

| (0.68) | ||||||

| IPO_VOL | 0.6763 *** | 1.9667 | 0.6874 *** | 1.9885 | 0.6922 *** | 1.9982 |

| (20.75) | (23.28) | (19.09) | ||||

| SALES | 0.2622 *** | 1.2998 | 0.2597 *** | 1.2965 | 0.2503 *** | 1.2844 |

| (9.33) | (9.48) | (8.08) | ||||

| SIZE | −1.4794 *** | 0.2237 | −1.5070 *** | 0.2216 | −1.5049 *** | 0.2220 |

| (−22.38) | (−22.47) | (−24.81) | ||||

| LEV | 2.1156 *** | 8.2945 | 2.1379 *** | 8.4813 | 2.1271 *** | 8.3905 |

| (3.39) | (3.47) | (3.44) | ||||

| C_RATIO | 0.0107* | 1.0107 | 0.0103 * | 1.0104 | 0.0099 * | 1.0100 |

| (1.72) | (1.66) | (1.70) | ||||

| ROA | −7.4182 *** | 0.0006 | −7.4123 *** | 0.0006 | −7.5100 *** | 0.0005 |

| (−132.57) | (−104.00) | (−112.14) | ||||

| AGE | −0.5453 *** | 0.5797 | −0.5482 *** | 0.5780 | −0.5414 *** | 0.5819 |

| (−11.06) | (−10.67) | (−10.72) | ||||

| OCF | 0.1273 | 1.1358 | 0.1271 | 1.1355 | 0.1208 | 1.1283 |

| (1.40) | (1.42) | (1.38) | ||||

| DA | −0.1482 | 0.8622 | −0.1523 | 0.8587 | −0.2336 | 0.7917 |

| (−0.77) | (−0.85) | (−1.25) | ||||

| AUDIT_DUM | −0.0562 | 0.9454 | −0.0511 | 0.9502 | −0.0683 | 0.9340 |

| (−1.21) | (−1.15) | (−1.59) | ||||

| YD | INCLUDED | INCLUDED | INCLUDED | |||

| Wald chi-sq | 11.48 *** | 12.05 *** | 266.84 *** | |||

| Obs | 477 | 477 | 477 | |||

| (1) | (2) | (3) | ||||

|---|---|---|---|---|---|---|

| Coef. | H.R. | Coef. | H.R. | Coef. | H.R. | |

| AMO | −0.0381 *** | 1 | ||||

| (−16.36) | ||||||

| AMO_RATIO | −2.2721 *** | 0.1031 | ||||

| (−8.31) | ||||||

| AMO_ORDER | 0.0111 *** | 1.0112 | ||||

| (4.71) | ||||||

| IPO_VOL | 0.6811 *** | 1.661 | 0.6699 *** | 1.940 | 0.6891 *** | 1.9920 |

| (26.99) | (35.68) | (20.81) | ||||

| SALES | 0.2611 *** | 1.3014 | 0.2635 *** | 1.3014 | 0.2568 *** | 1.2927 |

| (7.75) | (9.77) | (8.64) | ||||

| SIZE | −1.5001 *** | 0.2249 | −1.4855 *** | 0.2264 | −1.4977 *** | 0.2237 |

| (−49.80) | (-31.49) | (−23.14) | ||||

| LEV | 1.9155 *** | 7.4838 | 1.9986 *** | 7.3790 | 2.0816 *** | 8.0170 |

| (3.20) | (3.39) | (3.32) | ||||

| C_RATIO | 0.0119 * | 1.0099 | 0.0099 | 1.0099 | 0.0103 * | 1.0103 |

| (2.04) | (1.61) | (1.71) | ||||

| ROA | −7.2541 *** | 0.0005 | −7.6232 *** | 0.0005 | −7.5459 *** | 0.0005 |

| (−68.88) | (−148.01) | (−157.45) | ||||

| AGE | −0.4514 *** | 0.5848 | −0.5420 *** | 0.5816 | −0.5458 *** | 0.5794 |

| (−7.59) | (−10.04) | (−10.68) | ||||

| OCF | 0.0793 | 1.1387 | 0.1316 | 1.1406 | 0.1263 | 1.1346 |

| (0.84) | (1.42) | (1.42) | ||||

| DA | −0.1132 | 0.8406 | −0.1617 | 0.8507 | −0.1809 | 0.8345 |

| (−0.60) | (−0.73) | (−0.96) | ||||

| AUDIT_DUM | −0.0002 | 0.9528 | −0.0395 | 0.9613 | −0.0581 | 0.9436 |

| (0) | (−0.72) | (−1.31) | ||||

| YD | INCLUDED | INCLUDED | INCLUDED | |||

| Wald chi-sq | 224.98 *** | 11.48 *** | 11.03 *** | |||

| Obs | 477 | 477 | 477 | |||

| (1) | (2) | (3) | ||||

|---|---|---|---|---|---|---|

| Coef. | H.R. | Coef. | H.R. | Coef. | H.R. | |

| L_NUM | −0.0159 *** | 0.9842 | ||||

| (−21.90) | ||||||

| L_NUM_RATIO | −2.2541 *** | 0.1050 | ||||

| (−9.87) | ||||||

| L_NUM_ORDER | 0.0026 | 1.0026 | ||||

| (0.92) | ||||||

| IPO_VOL | 0.6764 *** | 1.9669 | 0.6875 *** | 1.9887 | 0.6922 *** | 1.9980 |

| (20.57) | (23.01) | (19.09) | ||||

| SALES | 0.2622 *** | 1.2997 | 0.2695 *** | 1.2963 | 0.2507 *** | 1.2850 |

| (7.75) | (9.51) | (8.13) | ||||

| SIZE | −1.4974 *** | 0.2237 | −1.1508 *** | 0.2216 | −1.5051 *** | 0.2220 |

| (−22.25) | (−22.30) | (−24.61) | ||||

| LEV | 2.1164 *** | 8.3011 | 2.1393 *** | 8.4933 | 2.1261 *** | 8.3819 |

| (3.39) | (3.47) | (3.44) | ||||

| C_RATIO | 0.0107 * | 1.0107 | 0.0104 * | 1.0104 | 0.0100 * | 1.0100 |

| (1.72) | (1.67) | (1.70) | ||||

| ROA | −7.4154 *** | 0.0006 | −7.4054 *** | 0.0006 | −7.5086 *** | 0.0005 |

| (−130.20) | (−101.04) | (−113.17) | ||||

| AGE | −0.5454 *** | 0.5796 | −0.5482 *** | 0.5780 | −0.5417 *** | 0.5818 |

| (−11.11) | (−10.73) | (−10.73) | ||||

| OCF | 0.1274 | 1.1359 | 0.1272 | 1.1357 | 0.1213 | 1.1289 |

| (1.40) | (1.42) | (1.39) | ||||

| DA | −0.1473 | 0.8631 | −0.1506 | 0.8602 | −0.2296 | 0.949 |

| (−0.77) | (−0.84) | (−1.23) | ||||

| AUDIT_DUM | −0.0562 | 0.9453 | −0.0512 | 0.9501 | −0.0679 | 0.9344 |

| (−1.22) | (−1.16) | (−1.58) | ||||

| YD | INCLUDED | INCLUDED | INCLUDED | |||

| Wald chi-sq | 11.46 *** | 500.02 *** | 299.37 *** | |||

| Obs | 477 | 477 | 477 | |||

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, N.-Y. Do Reputable Underwriters Affect the Sustainability of Newly Listed Firms? Evidence from South Korea. Sustainability 2019, 11, 2665. https://doi.org/10.3390/su11092665

Kim N-Y. Do Reputable Underwriters Affect the Sustainability of Newly Listed Firms? Evidence from South Korea. Sustainability. 2019; 11(9):2665. https://doi.org/10.3390/su11092665

Chicago/Turabian StyleKim, Na-Youn. 2019. "Do Reputable Underwriters Affect the Sustainability of Newly Listed Firms? Evidence from South Korea" Sustainability 11, no. 9: 2665. https://doi.org/10.3390/su11092665

APA StyleKim, N.-Y. (2019). Do Reputable Underwriters Affect the Sustainability of Newly Listed Firms? Evidence from South Korea. Sustainability, 11(9), 2665. https://doi.org/10.3390/su11092665