The Eco-Costs of Material Scarcity, a Resource Indicator for LCA, Derived from a Statistical Analysis on Excessive Price Peaks

Abstract

1. Introduction

1.1. Resource Scarcity in the Classic Environmental Life-Cycle Assessment (LCA)

1.2. Metrics on Criticality outside the LCA Community

- Concentration of metal-producing countries, applying the Herfindahl–Hirschman index;

- Political stability of producing countries, using the worldwide governance indicators;

- Potential substitution, estimated by expert opinion;

- Recycling rate, from UNEP [38].

1.3. The Issue of “Resources” in LCA and the Next Step toward LCSA

1.4. Research Questions Related to the Development of a New Socio-Economic Approach

- (a)

- Which statistical method can be applied to predict the future risk of a sudden jump in prices caused by disruptions in the supply chain?

- (b)

- For which metals are these price fluctuations relevant (i.e., are the price peaks high in comparison to the average price over a decade)?

- (c)

- How can this approach of supply chain risks and consequential price jumps be incorporated in LCA?

2. Methods and Data

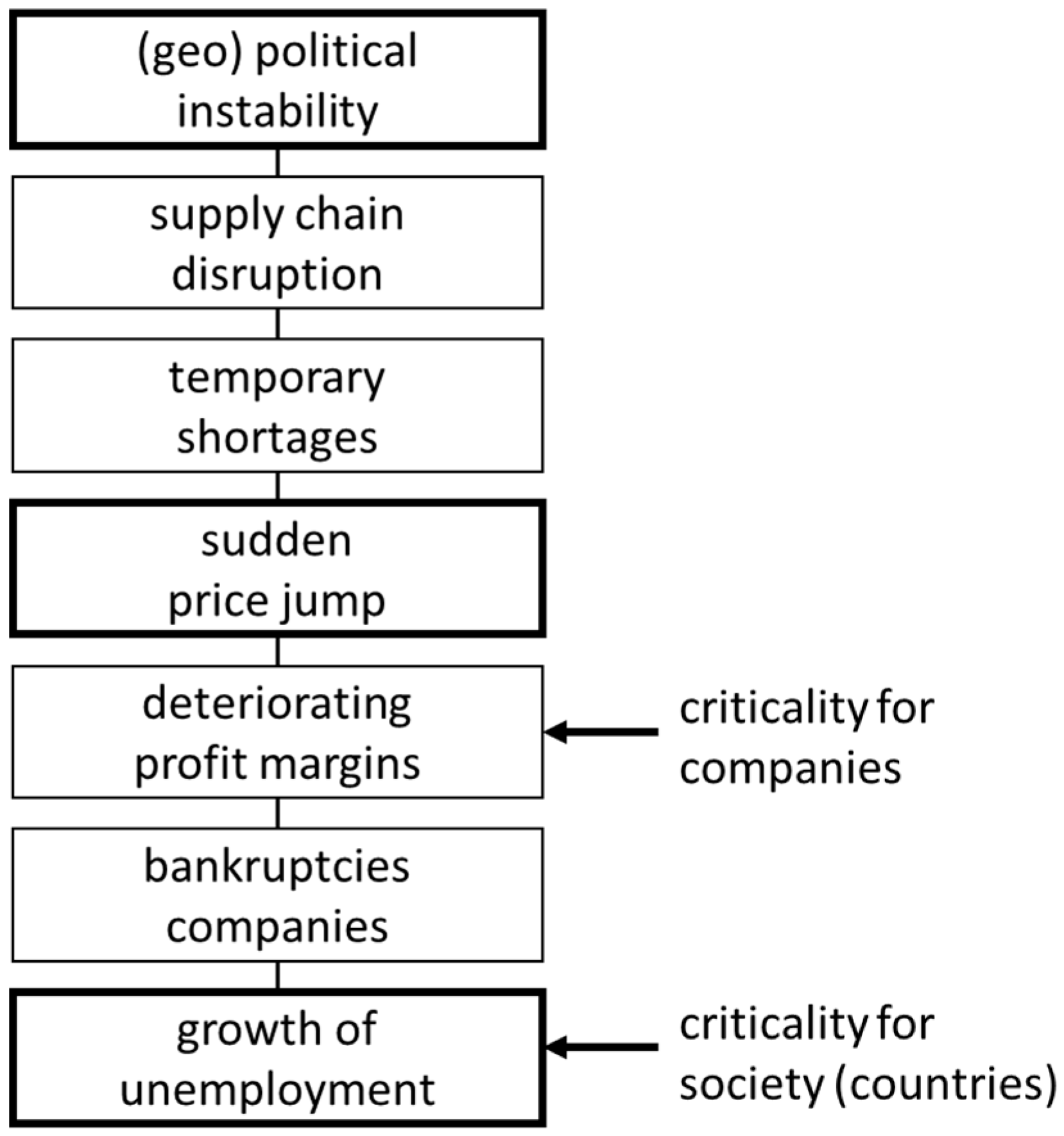

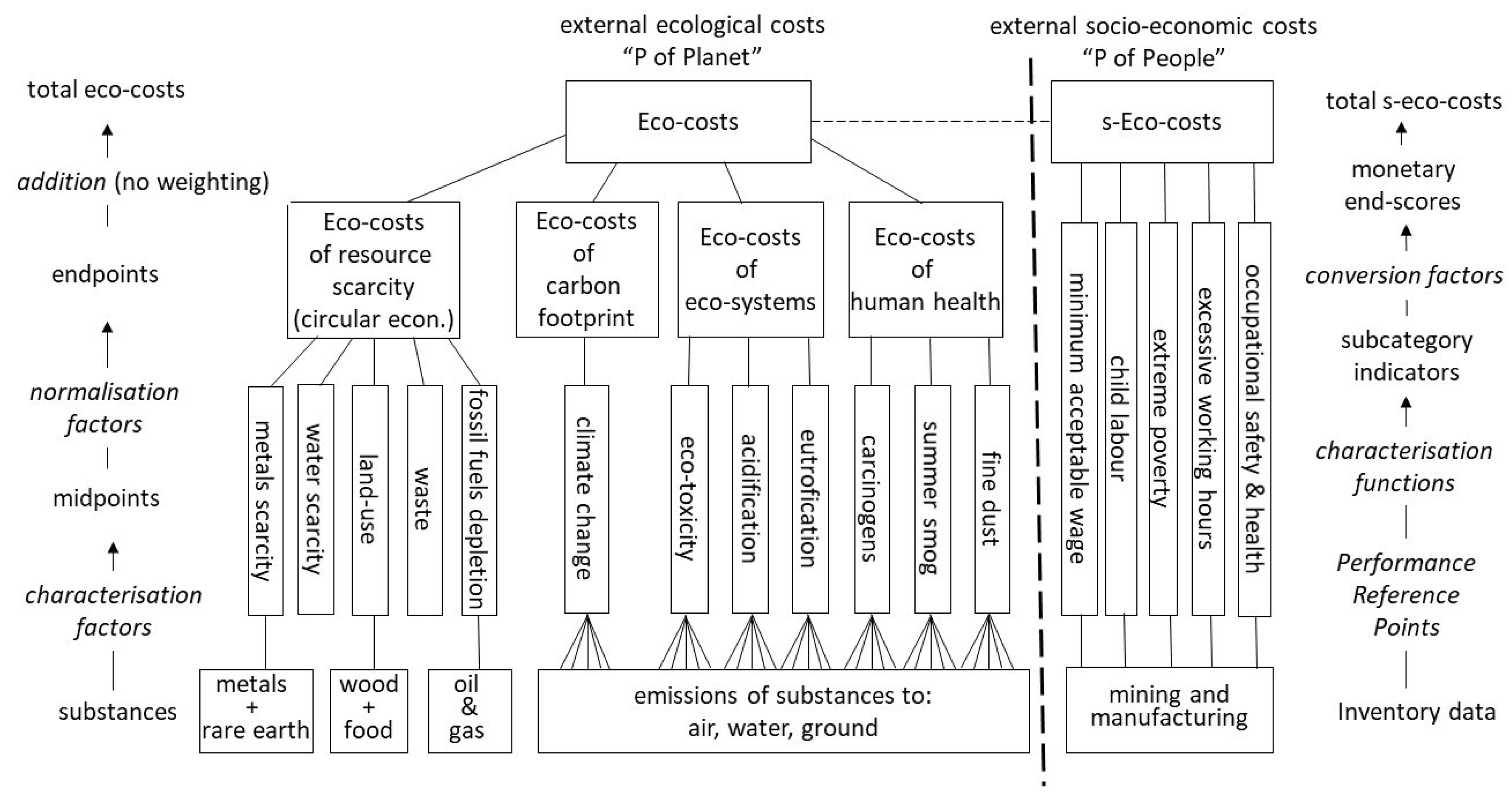

2.1. The Cause–Effect Pathway of the Socio-Economic Effects of Resource Scarcity

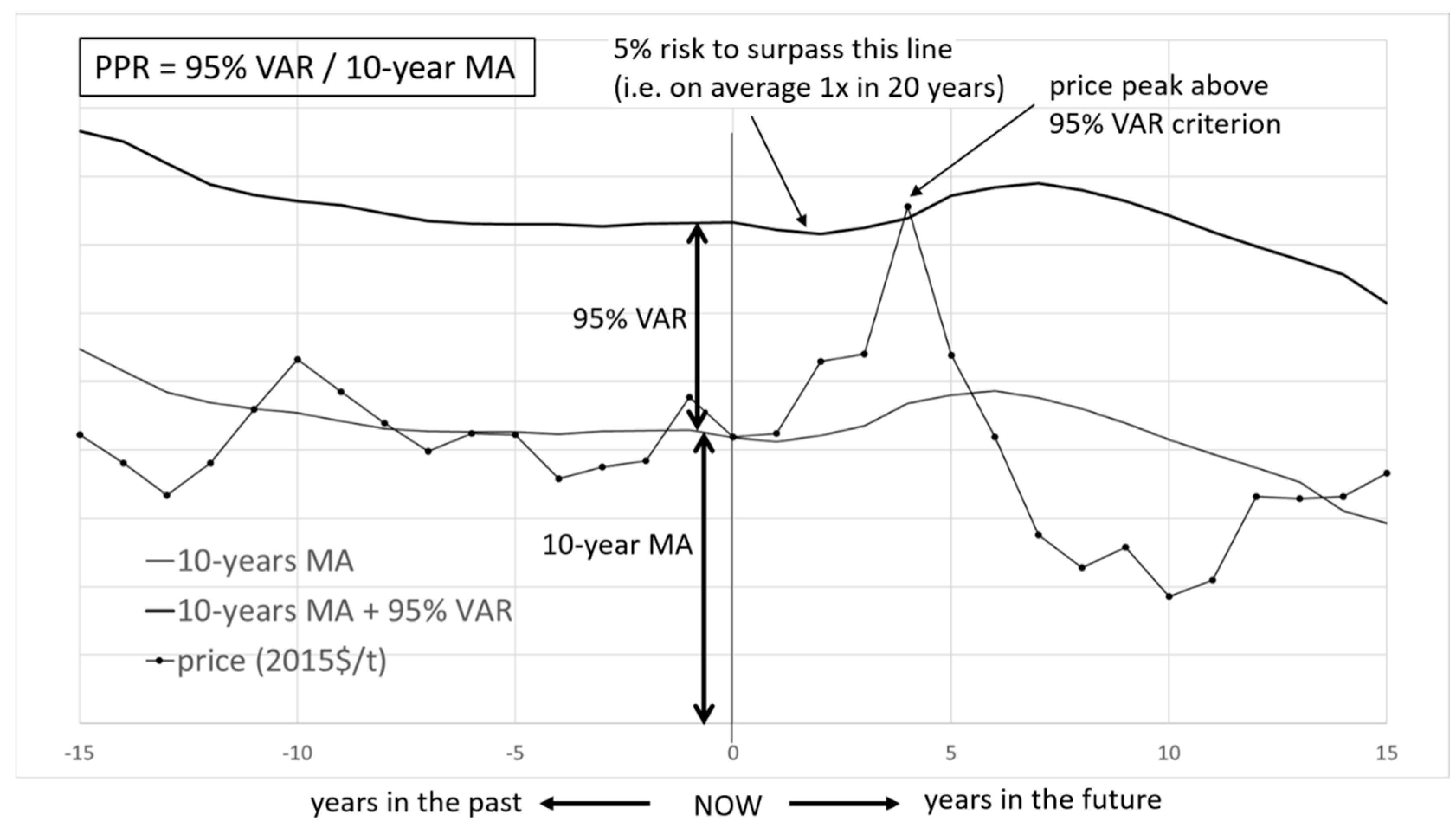

2.2. Quantifying the Risk of Price Fluctuations: The 95% Value at Risk (95% VAR)

3. Results

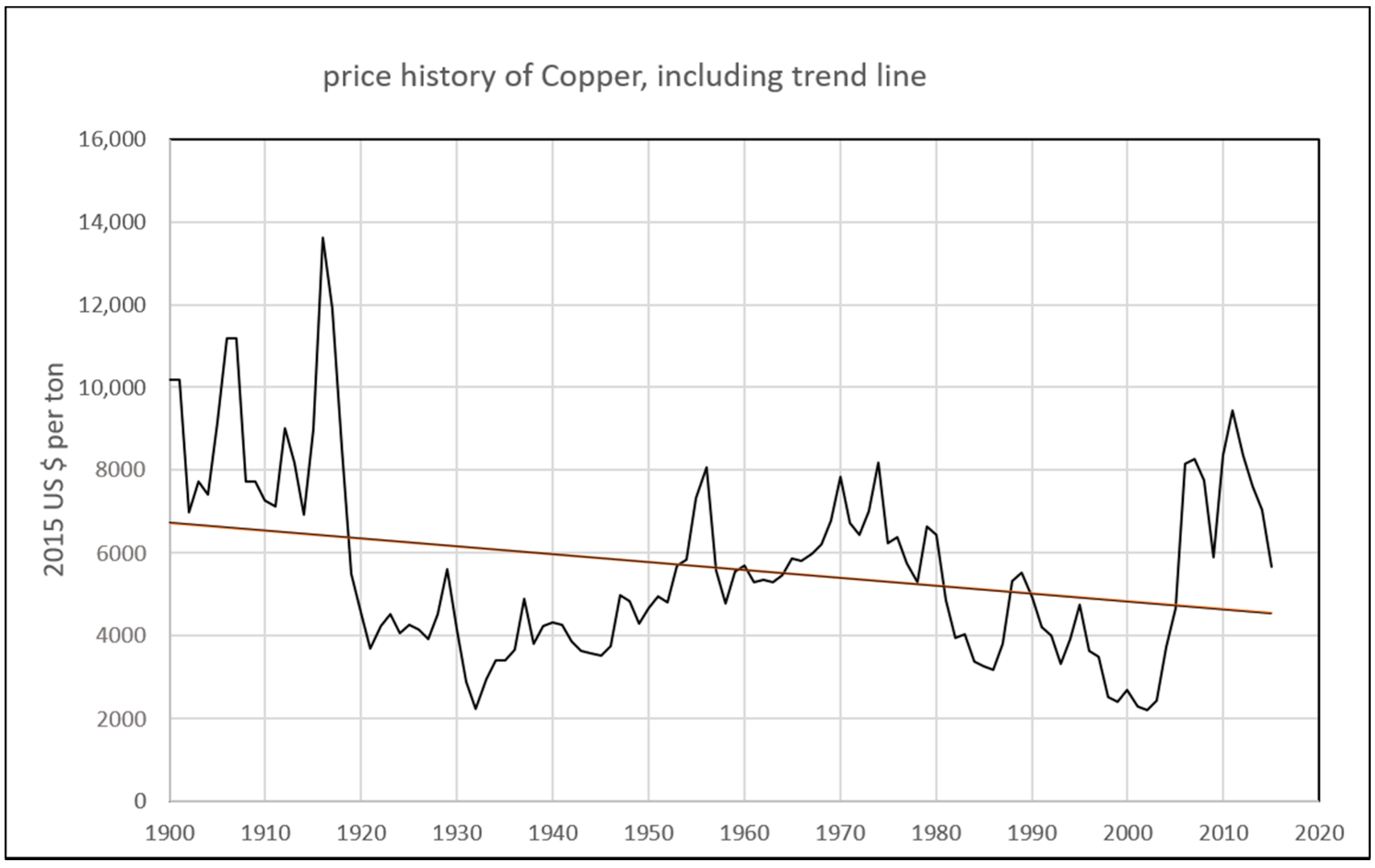

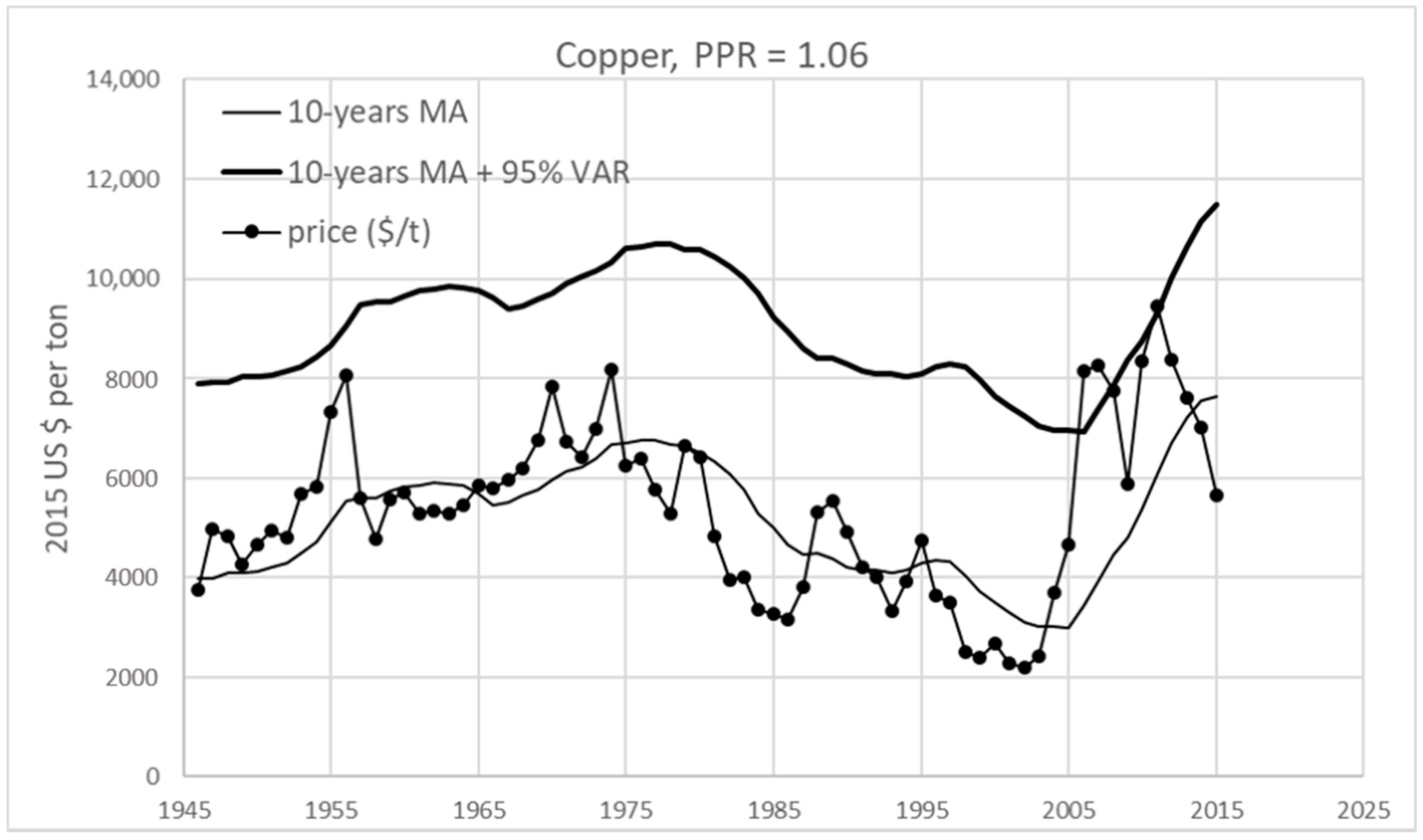

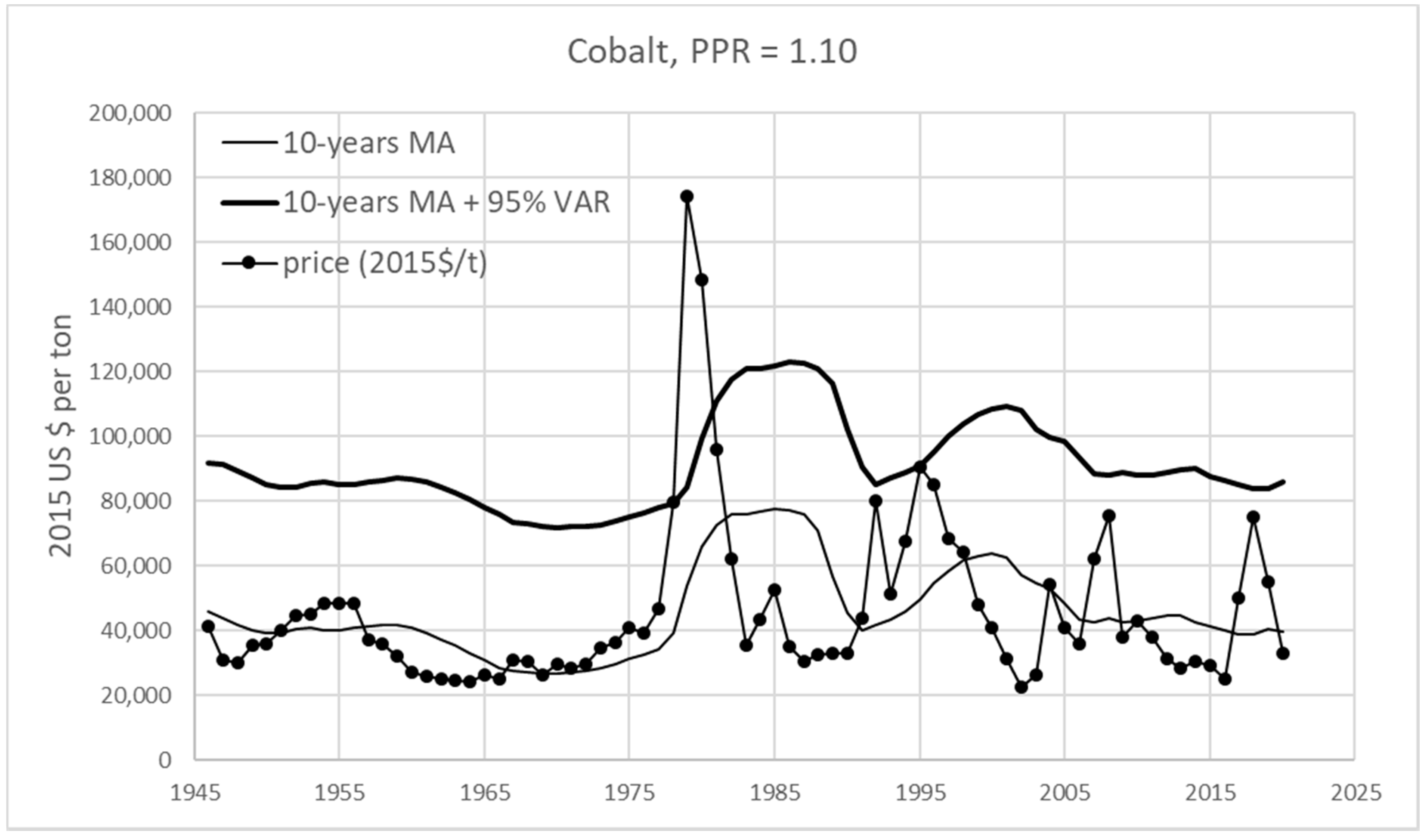

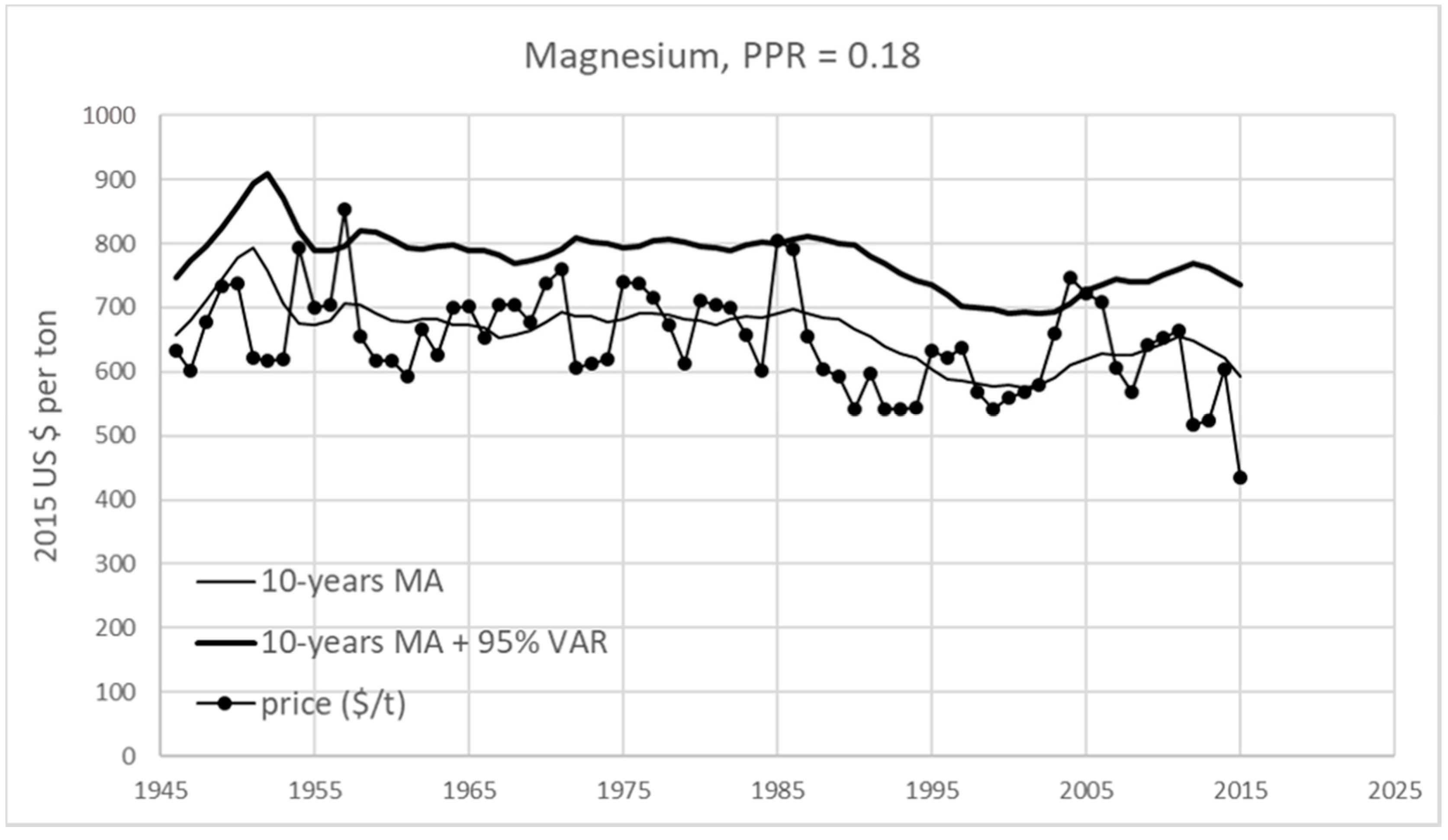

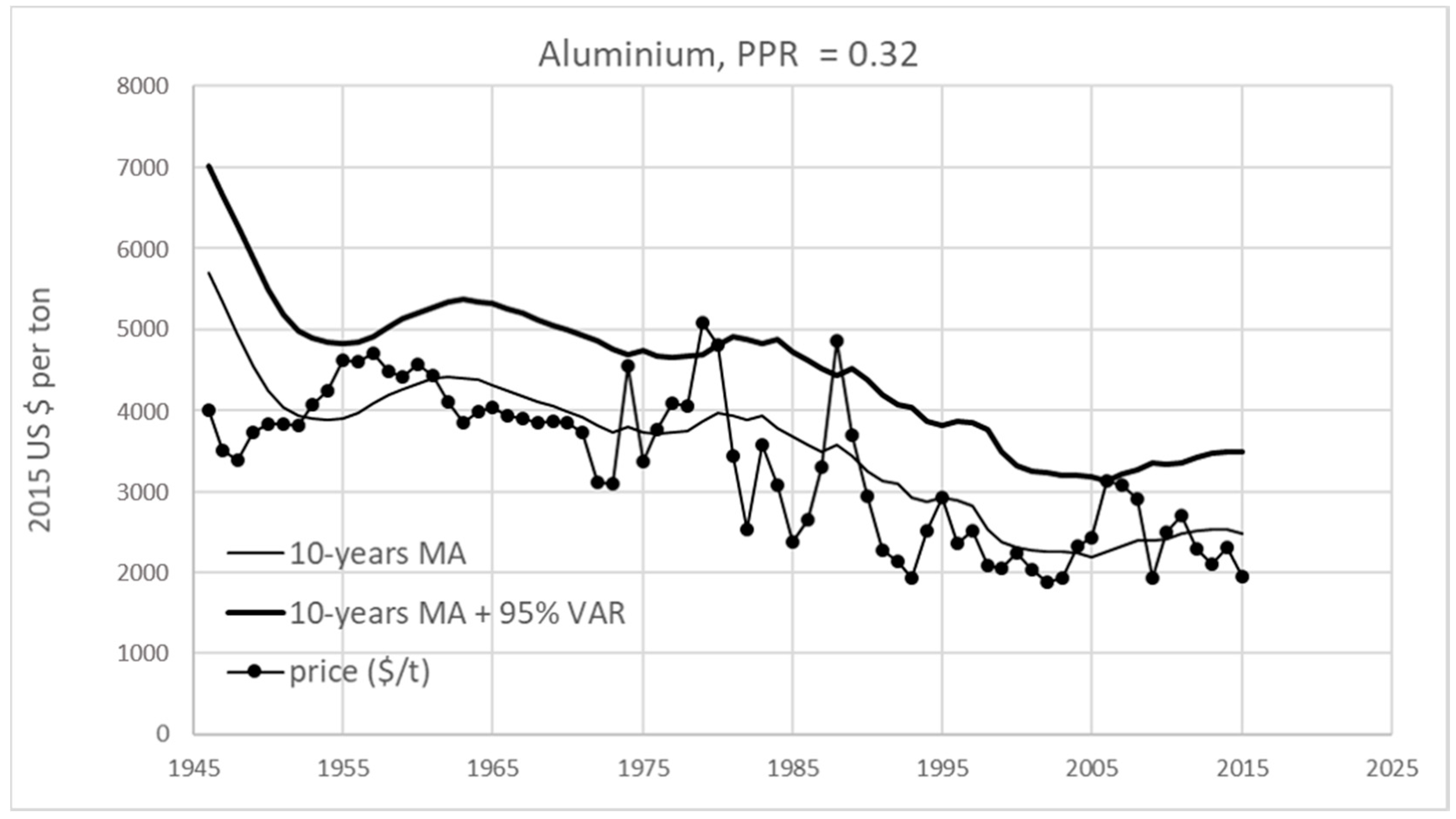

3.1. The PPR and Price Charts of 42 Raw Materials

3.2. The Potential Application of the PPR and the VAR in LCA

- FR = the Financial Risk of the scarcity of a metal in a product (US$, euro or any other currency),

- PPR = the Peak Price Ratio (dimensionless),

- 10-year MA = the average price for 10 years of a specific material in (US$/kg, euro/kg, or any other currency per kg),

- 95% VAR = the Value at Risk 95% (euro/kg, US$/kg, or any other currency) = eco-costs of materials scarcity,

- m = the mass of a specific material in the product (kg).

4. Discussion

4.1. The Issue of By-Products in Mining

4.2. Validation Checks on the System Metrics

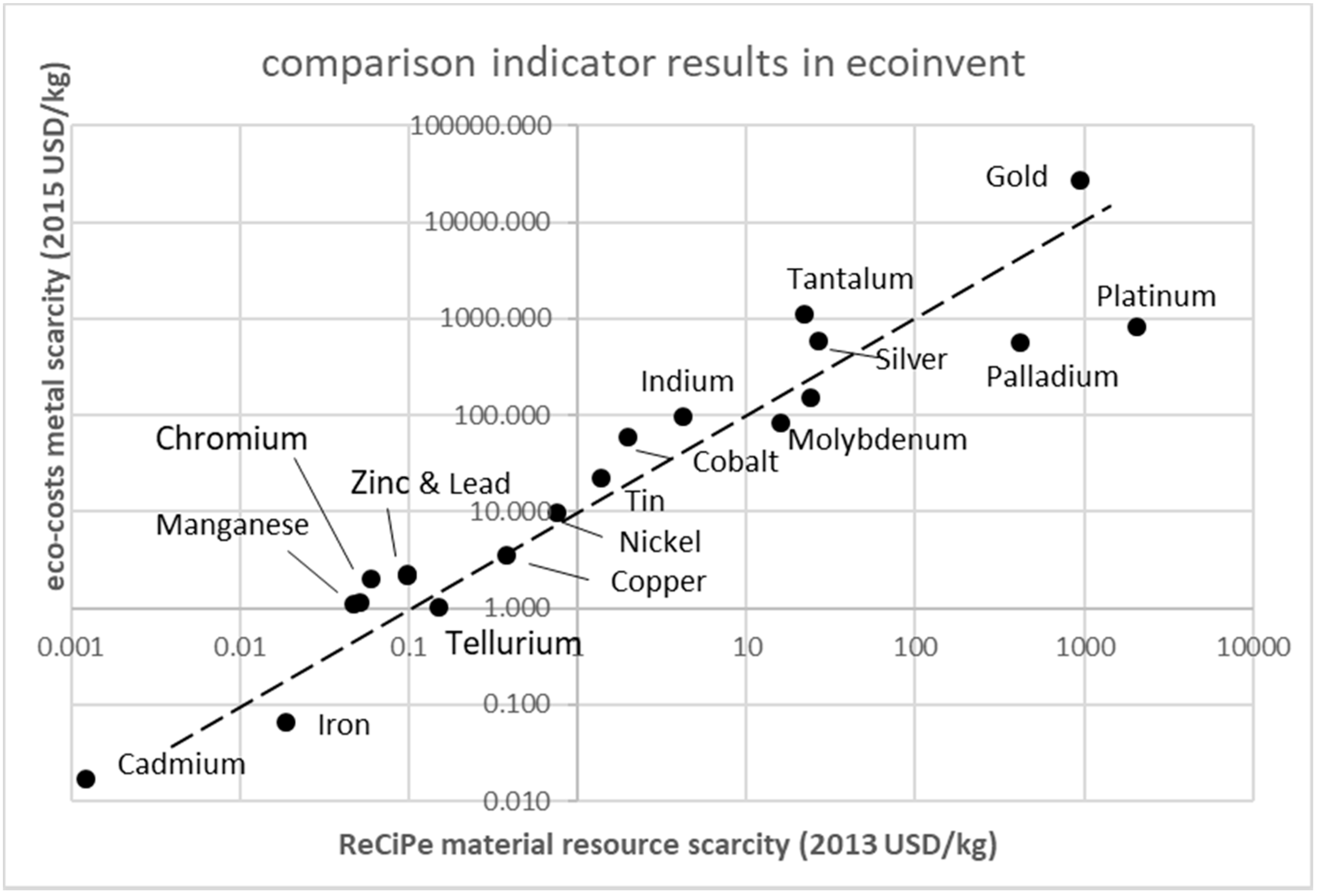

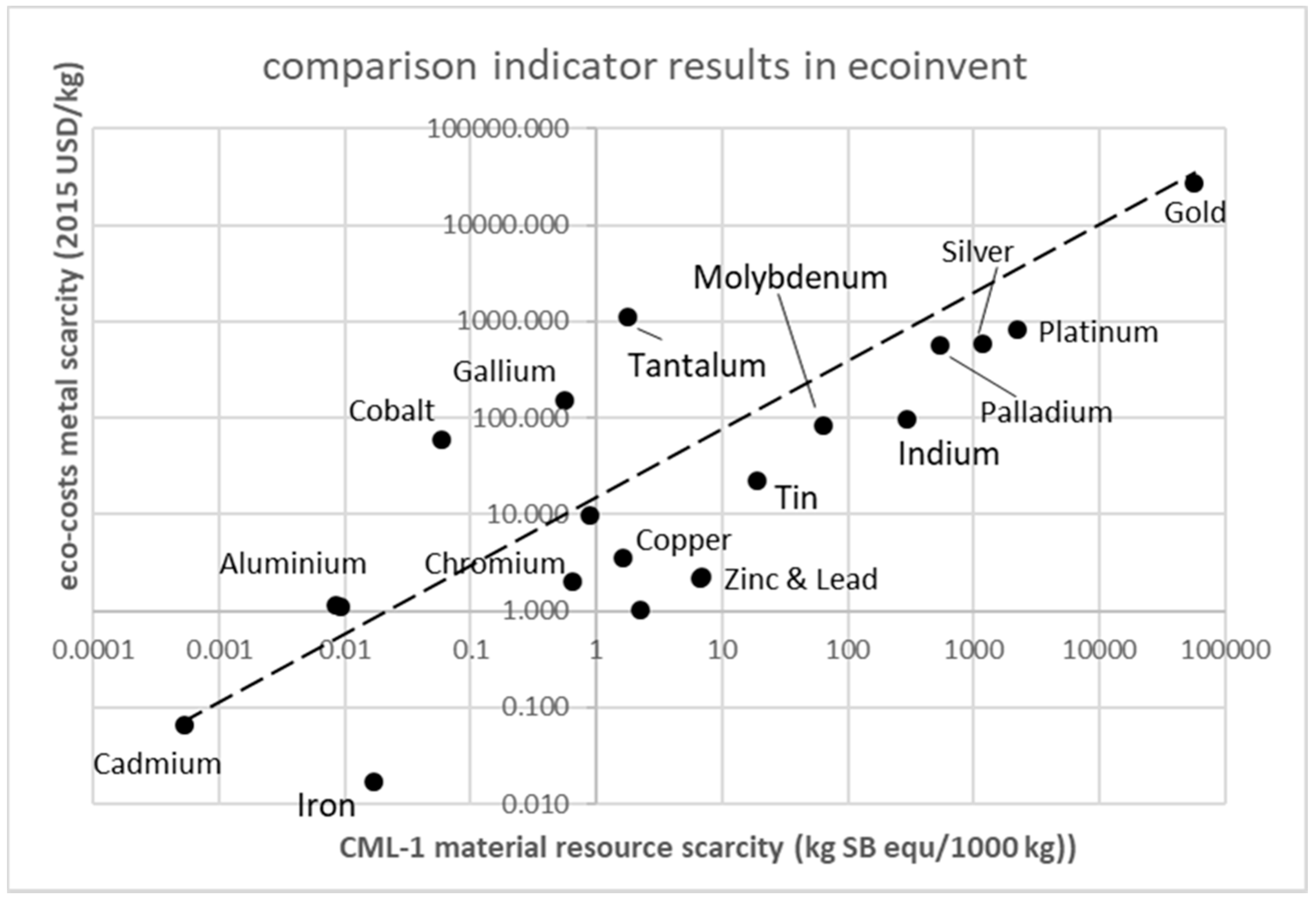

4.3. Validation in LCA

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Business Risks—A Hypothetical Case of a Manufacturer of Lithium-Ion Car Batteries

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Cobalt Price | Cobalt Price | Other Costs | Total Costs | Sale Price | Profit Margin | Eco-Costs |

|---|---|---|---|---|---|---|---|

| ($/kg) | ($/unit) | ($/unit) | ($/unit) | ($/unit) | ($/unit) | ($/unit) | |

| 2014 | 31 | 31 | 32 | 63 | 76 | 13 | 45.2 |

| 2015 | 30 | 30 | 32 | 62 | 76 | 14 | 45.2 |

| 2016 | 25 | 25 | 32 | 57 | 76 | 19 | 45.2 |

| 2017 | 50 | 50 | 32 | 82 | 76 | −6 | 45.2 |

| 2018 | 75 | 75 | 32 | 107 | 76 | −31 | 45.2 |

| 2019 | 55 | 55 | 32 | 87 | 76 | −7.5 | 45.2 |

Appendix B. Scores on the Scarcity of Metals

| Metal | CRM? | CRM Supply Risk * | Risk List Index ** | Long-Term Scarcity *** |

|---|---|---|---|---|

| (Yes/No) | (Range 0–10) | (Range 3.3–10) | (Year of Depletion) | |

| Aluminum, Al | No | 0.5 | 4.8 | Over 3000 |

| Antimony, Sb | Yes | 4.3 | 9.0 | 2040 |

| Arsenic, As | No | - | 7.9 | 2490 |

| Barium, Ba | Yes | 1.6 | 7.6 | Over 3000 |

| Beryllium, Be | Yes | 2.4 | 7.1 | Over 3000 |

| Bismuth, Bi | Yes | 3.8 | 8.8 | 2190 |

| Boron, B | No | - | - | 2250 |

| Cadmium, Cd | No | - | 7.1 | 2590 |

| Cesium, Cs | No | - | - | - |

| Chromium, Cr | No | 0.9 | 6.2 | 2200 |

| Cobalt, Co | Yes | 1.6 | 8.1 | Over 3000 |

| Copper, Cu | No | 0.2 | 4.8 | 2170 |

| Gallium, Ga | Yes | 1.4 | 8.6 | Over 3000 |

| Germanium, Ge | Yes | 1.9 | 8.6 | Over 3000 |

| Gold, Au | No | 0.2 | 4.5 | 2055 |

| Hafnium, Hf | Yes | 1.3 | - | - |

| Indium, In | No | 2.4 | 8.1 | Over 3000 |

| Iron (ore), Fe | No | 0.8 | 5.2 | 2380 |

| Lead, Pb | No | 0.1 | 5.5 | 2300 |

| Lithium, Li | No | 1.0 | 7.6 | Over 3000 |

| Magnesium, Mg | Yes | 4.0 | 7.6 | Over 3000 |

| Manganese, Mn | No | 0.9 | 5.7 | Over 3000 |

| Mercury, Hg | No | - | 6.9 | Over 3000 |

| Molybdenum, Mo | No | 0.9 | 8.1 | 2100 |

| Nickel, Ni | No | 0.3 | 5.7 | 2370 |

| Niobium, Nb | Yes | 3.1 | 6.7 | Over 3000 |

| Platinum, Pt | Yes | 2.1 | 7.6 | Over 3000 |

| Palladium, Pd | Yes | 1.7 | 7.6 | Over 3000 |

| Iridium, Ir | Yes | 2.8 | 7.6 | Over 3000 |

| Osmium, Os | Yes | - | 7.6 | Over 3000 |

| Rhodium, Rh | Yes | 2.5 | 7.6 | Over 3000 |

| Ruthenium, Ru | Yes | 3.4 | 7.6 | Over 3000 |

| Rhenium, Re | No | 1.0 | 7.1 | 2130 |

| Selenium, Se | No | 0.4 | 6.9 | Over 3000 |

| Silicon, Si | Yes | 1.0 | - | - |

| Silver, Ag | No | 0.5 | 7.1 | 2290 |

| Strontium, Sr | No | - | 8.3 | Over 3000 |

| Tantalum, Ta | Yes | 1.0 | 7.1 | Over 3000 |

| Tellurium, Te | No | 0.7 | - | - |

| Thallium, Tl | No | - | - | Over 3000 |

| Thorium, Th | No | - | 5.7 | - |

| Tin, Sn | No | 0.8 | 6.0 | 2280 |

| Titanium, Ti | No | 0.3 | 4.8 | Over 3000 |

| Tungsten, W | Yes | 1.8 | 8.1 | Over 3000 |

| Vanadium, V | Yes | 1.6 | 8.6 | Over 3000 |

| Zinc, Zn | No | 0.3 | 4.8 | 2100 |

| Zirconium, Zr | no | - | 6.4 | Over 3000 |

Appendix C. Results of Calculations on the Resource Scarcity (LCI Data from Ecoinvent)

| in ADP | in ReCiPe Metal Depletion | in Eco-costs (95% VAR) | ||||

|---|---|---|---|---|---|---|

| Dominated by (%) | Dominated by (%) | Dominated by (%) | ||||

| Aluminum | Cadmium | 34% | Aluminum | 97% | Aluminum | 99% |

| Cadmium | Cadmium | 29% | Nickel | 27% | Nickel | 36% |

| Chromium | Chromium | 97% | Chromium | 52% | Chromium | 70% |

| Cobalt | Cobalt | 35% | Cobalt | 100% | Cobalt | 100% |

| Copper | Copper | 72% | Copper | 53% | Copper | 97% |

| Gallium | Cadmium | 16% | Gallium | 100% | Gallium | 99% |

| Gold | Gold | 100% | Gold | 99% | Gold | 100% |

| Indium | Cadmium | 51% | Lead | 43% | Zinc | 45% |

| Lead | Cadmium | 51% | Lead | 43% | Zinc | 45% |

| Manganese | Manganese | 69% | Manganese | 87% | Manganese | 97% |

| Molybdenum | Copper | 62% | Molybdenum | 56% | Molybdenum | 51% |

| Nickel | Copper | 81% | Nickel | 68% | Nickel | 80% |

| Palladium | Copper | 48% | Platinum | 48% | Palladium | 61% |

| iron | Cadmium | 22% | Iron | 100% | Iron | 98% |

| Platinum | Platinum | 70% | Platinum | 70% | Palladium | 49% |

| Silver | Silver | 46% | Silver | 60% | Silver | 47% |

| Tantalum | Copper | 35% | Tantalum | 99% | Tantalum | 100% |

| Tellurium | Copper | 23% | Copper | 57% | Copper | 71% |

| Tin | Tin | 100% | Tin | 100% | Tin | 100% |

| Zinc | Cadmium | 50% | Lead | 42% | Zinc | 45% |

References

- British Geological Survey Risk List. 2015. Available online: https://www.bgs.ac.uk/mineralsuk/statistics/riskList.html (accessed on 21 October 2018).

- Schulz, K.J.; DeYoung, J.H., Jr.; Bradley, D.C.; Seal, R.R., II. Critical Mineral Resources of the United States—An Introduction; United States Geological Survey: Reston, VA, USA, 2017. [CrossRef]

- European Commission. Study on the Review of the List of Critical Raw Materials. 2017. Available online: https://publications.europa.eu/en/publication-detail/-/publication/08fdab5f-9766-11e7-b92d-01aa75ed71a1/language-en (accessed on 12 October 2018).

- Schmidt, M. Scarcity and Environmental Impact of Mineral Resources—An Old and Never-Ending Discussion. Resources 2019, 8, 2. [Google Scholar] [CrossRef]

- Guinée, J.; Heijungs, R. A proposal for the definition of resource equivalency factors for use in product life-cycle assessment. Environ. Toxicol. Chem. 1995, 14, 917–925. [Google Scholar] [CrossRef]

- Van Oers, L.; de Koning, A.; Guinée, J.B.; Huppes, G. Abiotic Resource Depletion in LCA: Improving Characterisation Factors for Abiotic Resource Depletion as Recommended in the New Dutch LCA Handbook; Road and Hydraulic Engineering Institute, Ministry of Transport and Water: Amsterdam, The Netherlands, 2002.

- Van Oers, L.; Guinee, J. The Abiotic Depletion Potential: Background, Updates, and Future. Resources 2016, 5, 16. [Google Scholar] [CrossRef]

- Schneider, L.; Berger, M.; Finkbeiner, M. Abiotic resource depletion in LCA—Background and update of the anthropogenic stock extended abiotic depletion potential (AADP) model. Int. J. Life Cycle Assess. 2015, 20, 709–721. [Google Scholar] [CrossRef]

- Graedel, T.E.; Barr, R.; Cordier, D.; Enriquez, M.; Hagelüken, C.; Hammond, N.Q.; Kesler, S.; Mudd, G.; Nassar, N.; Peacey, J.; et al. Estimating Long-Run Geological Stocks of Metals; UNEP International Panel on Sustainable Resource Management; Working Group on Geological Stocks of Metals; Working Paper, 11 June 2011; UNEP: Nairobi, Kenya, 2011. [Google Scholar]

- Wilkinson, B.H.; Kesler, S.E. Strüngman forum reports. In Linkages of Sustainability; Graedel, T.E., van der Voet, E., Eds.; The MIT Press: Cambridge, MA, USA, 2010; p. 122. [Google Scholar]

- Speirs, J.; McGlade, C.; Slade, R. Uncertainty in the availability of natural resources: Fossil fuels, critical metals and biomass. Energy Policy 2015, 87, 654–664. [Google Scholar] [CrossRef]

- Mudd, G.M.; Yellishetty, M.; Reck, B.K.; Graedel, T.E. Quantifying the Recoverable Resources of Companion Metals: A Preliminary Study of Australian Mineral Resources. Resources 2014, 3, 657–671. [Google Scholar] [CrossRef]

- Henckens, M.L.C.M. Managing Raw Materials Scarcity: Safeguarding the Availability of Geologically Scarce Mineral Resources for Future Generations. Ph.D. Thesis, University of Utrecht, Utrecht, The Netherlands, 2016. [Google Scholar]

- Sprecher, B.; Reemeyer, L.; Alonso, E.; Kuipers, K.; Graedel, T.E. How “black swan” disruptions impact minor metals. Resources Policy 2017, 54, 88–96. [Google Scholar] [CrossRef]

- Singer, D.A. Future copper resources. Ore Geol. Rev. 2017, 86, 271–279. [Google Scholar] [CrossRef]

- Drielsma, J.A.; Russell-Vaccari, A.J.; Drnek, T.; Tom Brady, T.; Weihed, P.; Mistry, M.; Perez Simbor, L. Mineral resources in life cycle impact assessment—Defining the path forward. Int. J. Life Cycle Assess. 2016, 21, 85–105. [Google Scholar] [CrossRef]

- Chapman, F.P.; Roberts, F. Metal Resources and Energy; Butterworth Scientific: Oxford, UK, 1983. [Google Scholar]

- Dewulf, J.; Van Langenhove, H.; Muys, B.; Bruers, S.; Bakshi, B.R.; Grubb, G.F.; Paulus, D.M.; Sciubba, E. Exergy: Its potential and limitations in environmental science and technology. Environ. Sci. Technol. 2008, 42, 2221–2232. [Google Scholar] [CrossRef]

- Liao, W.; Heijungs, R.; Huppes, G. Thermodynamic resource indicators in LCA: A case study on the Titania produced in Panzhihua city, southwest China. Int. J. Life Cycle Assess. 2012, 17, 951–961. [Google Scholar] [CrossRef]

- Goedkoop, M.; Spriensma, R. The Eco-Indicator 99, a Damage Oriented Method for Life Cycle Impact Assessment; Pre Consultants BV: Amersfoort, The Netherlands, 2001. [Google Scholar]

- Goedkoop, M.; Heijungs, R.; Huijbregts, M.A.J.; De Schryver, A.; Struijs, J.; Van Zelm, R. Mineral Resource Depletion in ReCiPe 2008: A life cycle impact assessment method which comprises harmonised category indicators at the midpoint and the endpoint level. In Report I: Characterisation Factors, 1st ed.; Ministerie van Volkhuisvesting, Ruimtelijke Ordening en Milieubeheer: Den Haag, The Netherlands, 2008. [Google Scholar]

- Vieira, M.D.M.; Ponsioen, T.C.; Goedkoop, M.J.; Huijbregts, M.A.J. Surplus Cost Potential as a Life Cycle Impact Indicator for Metal Extraction. Resources 2016, 5, 2. [Google Scholar] [CrossRef]

- Rötzer, N.; Schmidt, M. Decreasing Metal Ore Grades—Is the Fear of Resource Depletion Justified? Resources 2018, 7, 88. [Google Scholar] [CrossRef]

- Vogtländer, J.G.; Brezet, H.C.; Hendriks, C.F. The virtual Eco-costs ‘99: A single LCA-based indicator for sustainability and the Eco-costs—Value ratio (EVR) model for economic allocation: A new LCA-based calculation model to determine the sustainability of products and services. Int. J. Life Cycle Assess. 2001, 6, 157–166. [Google Scholar] [CrossRef]

- Hotelling, H. The economics of Exhaustible Resources. J. Political Econ. 1931, 39, 137–175. [Google Scholar] [CrossRef]

- Frischknecht, R.; Büsser Knöpfel, S. Ecological scarcity 2013—New features and its application in industry and administration—54th LCA forum, Ittigen/Berne, Switzerland, December 5, 2013. Int. J. Life Cycle Assess. 2014, 19, 1361–1366. [Google Scholar] [CrossRef]

- Steen, B. Calculation of Monetary Values of Environmental Impacts from Emissions and Resource Use. J. Sustain. Dev. 2016, 9. [Google Scholar] [CrossRef]

- Laurent, A.; Olsen, S.I.; Hauschild, M.Z. Normalization in EDIP97 and EDIP2003: Updated European inventory for 2004 and guidance towards a consistent use in practice. Supplementary Material. Int. J. Life Cycle Assess. 2011, 16, 401–409. [Google Scholar] [CrossRef]

- EN 15804: 2012+ A1: 2013: Sustainability of Construction Works. Environmental Product Declarations. Core Rules for the Product Category of Construction Products. Available online: https://shop.bsigroup.com/ProductDetail/?pid=000000000030279721 (accessed on 18 April 2019).

- European Commission, Joint Research Centre, Institute for Environment and Sustainability. Characterisation Factors of the ILCD Recommended Life Cycle Impact Assessment Methods. Database and Supporting Information, 1st ed.; EUR 25167; Publications Office of the European Union: Luxembourg, 2012. [Google Scholar]

- Jolliet, O.; Margni, M.; Charles, R.; Humbert, S.; Payet, J.; Rebitzer, G.; Rosenbaum, R. IMPACT 2002+: A new life cycle impact assessment methodology. Int. J. Life Cycle Assess. 2003, 8, 324. [Google Scholar] [CrossRef]

- Graedel, T.E.; Reck, B.K. Six Years of Criticality Assessments, What have we learned so far? Forum Yale Univ. 2015, 20. [Google Scholar] [CrossRef]

- Schneider, L.; Berger, M.; Schüler-Hainsch, E.; Knöfel, S.; Ruhland, K.; Mosig, J.; Bach, V.; Finkbeiner, M. The economic resource scarcity potential (ESP) for evaluating resource use based on life cycle assessment. Int. J. Life Cycle Assess. 2014, 19, 601–610. [Google Scholar] [CrossRef]

- Dewulf, J.; Benini, L.; Mancini, L.; Sala, S.; Andrea Blengini, G.; Ardente, F.; Recchioni, M.; Maes, J.; Pant, R.; Pennington, D. Rethinking the Area of Protection “Natural Resources” in Life Cycle Assessment. Environ. Sci. Technol. 2015, 49, 5310–5317. [Google Scholar] [CrossRef]

- Sonnemann, G.; Gemechu, E.D.; Adibi, N.; De Bruille, V.; Bulle, C. From a critical review to a conceptual framework for integrating the criticality of resources into Life Cycle Sustainability Assessment. J. Clean. Prod. 2015, 94, 20–34. [Google Scholar] [CrossRef]

- Achzet, B.; Helbig, C. How to evaluate raw material supply risk—An overview. Resour. Policy 2013, 38, 435–447. [Google Scholar] [CrossRef]

- European Commission. Methodology for Establishing the EU List of Critical Raw Materials—Guidelines; European Commission: Luxembourg, 2017; ISBN 978-92-79-68051-9. [Google Scholar]

- UNEP. Recycling Rates of Metals. A Status Report of the International Resource Panel. 2011. Available online: http://www.unep.org/resourcepanel/Portals/24102/PDFs/Metals_Recycling_Rates_110412-1.pdf (accessed on 18 April 2019).

- Mancini, L.; Benini, L.; Sala, S. Characterization of raw materials based on supply risk indicators for Europe. Int. J. Life Cycle Assess. 2018, 23, 726–738. [Google Scholar] [CrossRef]

- Vogtlander, J. The model of the Eco-Costs/Value Ratio. Ph.D. Thesis, Delft University of Technology, Delft, The Netherlands, 2001. [Google Scholar]

- Peck, D.; Kandachar, P.; Tempelman, E. Critical materials from a product design perspective. Mater. Des. 2015, 65, 147–159. [Google Scholar] [CrossRef]

- Peck, D. Prometheus Missing: Critical Materials and Product Design; Delft University of Technology: Delft, The Netherlands, 2016; ISBN 9-789065-63997. [Google Scholar] [CrossRef]

- Tapia Cortez, C.A.; Saydam, S.; Coulton, J.; Sammut, C. Alternative techniques for forecasting mineral commodity prices. Int. J. Min. Sci. Technol. 2018, 28, 309–322. [Google Scholar] [CrossRef]

- Taleb, N.N. Fooled by Randomness; Texere: London, UK, 2001; ISBN 1-58799-071-7. [Google Scholar]

- Taleb, N.N. The Black Swan: The Impact of the Highly Improbable; Penguin: London, UK, 2007; ISBN 978-0-14103459-1. [Google Scholar]

- Supplementary Materials. Available online: www.ecocostsvalue.com/EVR/scarcity.html (accessed on 15 March 2019).

- Kelly, T.D.; Matos, G.R. Historical Statistics for Mineral and Material Commodities in the United States, USGS 2015. Available online: https://minerals.usgs.gov/minerals/pubs/historical-statistics/ (accessed on 21 October 2018).

- Van der Velden, N.M.; Vogtlander, J.G. Monetisation of external socio-economic costs of industrial production: A social-LCA-based case of clothing production. J. Clean. Prod. 2017, 153, 320–330. [Google Scholar] [CrossRef]

- Vogtlander, J. A Practical Guide to LCA for Students, Designers and Business Managers, 5th ed.; Delft Academic Press: Delft, The Netherlands, 2017; ISBN 97890-6562-3614. Available online: https://en.wikipedia.org/wiki/Eco-costs (accessed on 15 March 2019).

| Method | Indicator | Approach | Fixed-Stock Paradigm? | Reference |

|---|---|---|---|---|

| CML-1 | ADP | Equation (1) | Yes | [5,6,7] |

| Anthropogenic stock extended ADP model | AADP | Equation (1), including anthropogenic stock | Yes | [8] |

| Eco-indicator 99 | MJ surplus | Extra energy required | Yes | [20] |

| ReCiPe 2008 | US$ | Surplus cost mining | Yes | [21] |

| ReCiPe 2016 | US$ | Surplus cost mining | Yes | [22] |

| Eco-costs 2007 | euro | Surplus cost mining | Yes | [24,25] |

| Ecological Scarcity 2013 | UBP (ADP) | Equation (1) | Yes | [26] |

| EPS 2015 | ELU (euro) | Replacement | No | [27] |

| EDIP 2003 | PR | Time of depletion | Yes | [28] |

| EPD 2013 (EN15804) | ADP | Equation (1) | Yes | [29] |

| ILCD 2011 Midpoint+ | ADP | Equation (1) | Yes | [30] |

| IMPACT 2002+ | MJ surplus | Extra energy required | Yes | [31] |

| Eco-costs 2017 | euro | Short term scarcity | No | This paper |

| Metal | PPR | VAR (95) | Metal | PPR | VAR (95) |

|---|---|---|---|---|---|

| $/kg | $/kg | ||||

| Aluminum, Al | 0.32 | 0.95 | Manganese, Mn | 0.56 | 0.48 |

| Antimony, Sb | 1.29 | 8.45 | Mercury, Hg | 1.18 | 37.69 |

| Arsenic, As | 0.66 | 1.01 | Molybdenum, Mo | 2.12 | 48.18 |

| Barium, Ba | 0.47 | 0.039 | Nickel, Ni | 1.01 | 12.58 |

| Beryllium, Be | 0.18 | 249 | Niobium, Nb | 1.43 | 37.46 |

| Bismuth, Bi | 1.02 | 23.64 | Platinum, Pt | 0.53 | 8660 |

| Boron, B | 0.28 | 0.36 | Rhenium, Re | 2.87 | 5340 |

| Cadmium, Cd | 0.93 | 18.1 | Selenium, Se | 2.64 | 94.62 |

| Cesium, Cs | no data | no data | Silicon, Si | 0.48 | 1.1 |

| Chromium, Cr | 0.75 | 1.01 | Silver, Ag | 1.29 | 605 |

| Cobalt, Co | 1.1 | 45.16 | Strontium, Sr | 0.84 | 0.38 |

| Copper, Cu | 1.06 | 3.94 | Tantalum, Ta | 4.24 | 627 |

| Gallium, Ga | 0.17 | 123 | Tellurium, Te | 1.14 | 108 |

| Germanium, Ge | 0.58 | 927 | Thallium, Tl | 1.21 | 3060 |

| Gold, Au | 1.14 | 25,290 | Thorium, Th | 0.86 | 119 |

| Hafnium, Hf | 0.91 | 253 | Tin, Sn | 0.78 | 19.06 |

| Indium, In | 1.14 | 667 | Titanium, Ti | 1.47 | 14.13 |

| Iron (ore), Fe | 0.86 | 0.046 | Tungsten, W | 0.78 | 32.26 |

| Lead, Pb | 0.82 | 1.52 | Vanadium, V | 0.94 | 22.16 |

| Lithium, Li | 0.6 | 2.97 | Zinc, Zn | 0.83 | 1.51 |

| Magnesium, Mg | 0.18 | 0.12 | Zirconium, Zr | 1.04 | 0.62 |

| Calculation Period of VAR | Period of Simulation | “Average Losses by Price Peaks”/Eco-Costs (%) |

|---|---|---|

| VAR calculated for 1946–2015 | 1996–2000 | 0.00% |

| 1996–2005 | 0.76% | |

| 2006–2010 | 7.83% | |

| 2006–2015 | 10.32% | |

| VAR calculated for 1946–1995 | 1996–2000 | 0.00% |

| 1996–2005 | 1.44% | |

| VAR calculated for 1946–2005 | 2006–2010 | 22.43% |

| 2006–2015 | 30.14% |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vogtländer, J.; Peck, D.; Kurowicka, D. The Eco-Costs of Material Scarcity, a Resource Indicator for LCA, Derived from a Statistical Analysis on Excessive Price Peaks. Sustainability 2019, 11, 2446. https://doi.org/10.3390/su11082446

Vogtländer J, Peck D, Kurowicka D. The Eco-Costs of Material Scarcity, a Resource Indicator for LCA, Derived from a Statistical Analysis on Excessive Price Peaks. Sustainability. 2019; 11(8):2446. https://doi.org/10.3390/su11082446

Chicago/Turabian StyleVogtländer, Joost, David Peck, and Dorota Kurowicka. 2019. "The Eco-Costs of Material Scarcity, a Resource Indicator for LCA, Derived from a Statistical Analysis on Excessive Price Peaks" Sustainability 11, no. 8: 2446. https://doi.org/10.3390/su11082446

APA StyleVogtländer, J., Peck, D., & Kurowicka, D. (2019). The Eco-Costs of Material Scarcity, a Resource Indicator for LCA, Derived from a Statistical Analysis on Excessive Price Peaks. Sustainability, 11(8), 2446. https://doi.org/10.3390/su11082446