On the Relationship between Economic Policy Uncertainty and the Implied Volatility Index

Abstract

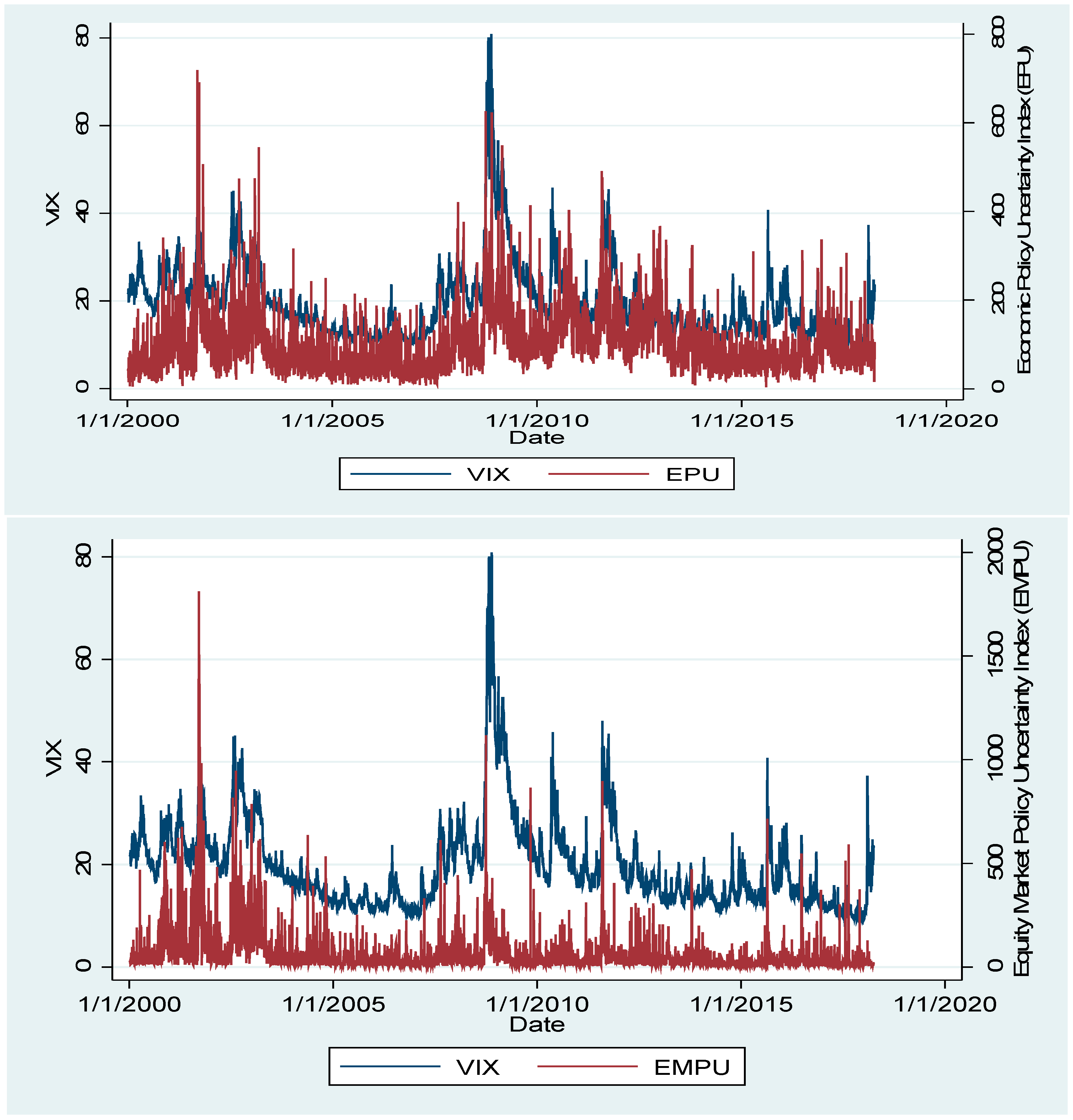

1. Introduction

2. Data Description and Summary Statistics

3. Empirical Model

- = intercept, measures change in the volatility during a non-announcements days, it should be “positive”

- = slope coefficient of FOMC, through −5 day “positive”, on report day “negative”, and through +5 day “negative”

- = slope coefficient of GDP, through −5 day “positive”, on report day “negative”, and through +5 day “negative”

- = slope of other macro indicators through −2 day “positive”, on report day “negative”, and through +2 day “negative”

- = dummy variable, assumes 1 on the day of report release, otherwise zero

- = represent the returns on respective underlying assets/index

- = classical error term

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Pastor, L.; Veronesi, P. Uncertainty about government policy and stock prices. J. Financ. 2012, 67, 1219–1264. [Google Scholar] [CrossRef]

- Pástor, L.; Veronesi, P. Political uncertainty and risk premia. J. Financ. Econ. 2013, 110, 520–554. [Google Scholar] [CrossRef]

- Amidu, M.; Adjasi, C. The structure and behaviour of small African banks: Market power and bank diversification strategy in Ghana. Int. J. Comp. Manag. 2018, 1, 202–219. [Google Scholar] [CrossRef]

- Liao, F.-N.; Ji, X.-L.; Wang, Z.-P. Firms’ Sustainability: Does Economic Policy Uncertainty Affect Internal Control? Sustainability 2019, 11, 794. [Google Scholar] [CrossRef]

- Christou, C.; Cunado, J.; Gupta, R.; Hassapis, C. Economic policy uncertainty and stock market returns in PacificRim countries: Evidence based on a Bayesian panel VAR model. J. Multinatl. Financ. Manag. 2017, 40, 92–102. [Google Scholar] [CrossRef]

- Raza, S.A.; Zaighum, I.; Shah, N. Economic policy uncertainty, equity premium and dependence between their quantiles: Evidence from quantile-on-quantile approach. Phys. A Stat. Mech. Its Appl. 2018, 492, 2079–2091. [Google Scholar] [CrossRef]

- Gábor, E.; Georgarakos, D. Economic Policy Uncertainty and Stock Market Participation. CFS Work. Pap. Ser. 2018, 1–42. [Google Scholar] [CrossRef]

- Duan, Y.; Chen, W.; Zeng, Q.; Liu, Z. Leverage effect, economic policy uncertainty and realized volatility with regime switching. Phys. A Stat. Mech. Its Appl. 2018, 493, 148–154. [Google Scholar] [CrossRef]

- Hu, Z.; Kutan, A.M.; Sun, P.-W. Is US economic policy uncertainty priced in China’s A-shares market? Evidence from market, industry, and individual stocks. Int. Rev. Financ. Anal. 2018, 57, 207–220. [Google Scholar] [CrossRef]

- Bali, T.G.; Brown, S.J.; Tang, Y. Is economic uncertainty priced in the cross-section of stock returns? J. Financ. Econ. 2017, 126, 471–489. [Google Scholar] [CrossRef]

- Graham, M.; Nikkinen, J.; Sahlström, P. Relative importance of scheduled macroeconomic news for stock market investors. J. Econ. Financ. 2003, 27, 153–165. [Google Scholar] [CrossRef]

- Nikkinen, J.; Sahlström, P. Scheduled domestic and US macroeconomic news and stock valuation in Europe. J. Multinatl. Financ. Manag. 2004, 14, 201–215. [Google Scholar] [CrossRef]

- Nikkinen, J.; Sahlström, P. Impact of the federal open market committee’s meetings and scheduled macroeconomic news on stock market uncertainty. Int. Rev. Financ. Anal. 2004, 13, 1–12. [Google Scholar] [CrossRef]

- Nikkinen, J.; Omran, M.; Petri, S.; Äijö, J. Global stock market reactions to scheduled U.S. macroeconomic news announcements. Glob. Financ. J. 2006, 17, 92–104. [Google Scholar] [CrossRef]

- Chen, E.-T.J.; Clements, A. S&P 500 implied volatility and monetary policy announcements. Financ. Res. Lett. 2007, 4, 227–232. [Google Scholar] [CrossRef]

- Onan, M.; Salih, A.; Yasar, B. Impact of macroeconomic announcements on implied volatility slope of SPX options and VIX. Financ. Res. Lett. 2014, 11, 454–462. [Google Scholar] [CrossRef]

- Reinhart, V.; Simin, T. The market reaction to Federal Reserve policy action from 1989 to 1992. J. Econ. Bus. 1997, 49, 149–168. [Google Scholar] [CrossRef]

- Rigobon, R.; Sack, B. The impact of monetary policy on asset prices. J. Monet. Econ. 2004, 51, 1553–1575. [Google Scholar] [CrossRef]

- Farka, M.; Fleissig, A.R. The effect of FOMC statements on asset prices. Int. Rev. Appl. Econ. 2012, 26, 387–416. [Google Scholar] [CrossRef]

- Wang, S.; Mayes, D.G. Monetary policy announcements and stock reactions: An international comparison. N. Am. J. Econ. Financ. 2012, 23, 145–164. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Filis, G. Dynamic co-movements of stock market returns, implied volatility and policy uncertainty. Econ. Lett. 2013, 120, 87–92. [Google Scholar] [CrossRef]

- Arouri, M.; Estay, C.; Rault, C.; Roubau, D. Economic policy uncertainty and stock markets: Long-run evidence from the US. Financ. Res. Lett. 2016, 18, 136–141. [Google Scholar] [CrossRef]

- Demir, E.; Gozgor, G.; Lau, C.K.M.; Vigne, S.A. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Financ. Res. Lett. 2018, 26, 145–149. [Google Scholar] [CrossRef]

- Gabauer, D.; Gupta, R. On the Transmission Mechanism of Country-Specific and International Economic Uncertainty Spillovers: Evidence from a TVP-VAR Connectedness Decomposition Approach. Econ. Lett. 2018, 171, 63–71. [Google Scholar] [CrossRef]

- Saikia, M.; Borbora, S. India’s outward foreign direct investment: The home-country economic perspective. Int. J. Comp. Manag. 2018, 1, 162–184. [Google Scholar] [CrossRef]

- Fleming, J.; Ostdiek, B.; Whaley, R.E. Predicting stock market volatility: A new measure. J. Futures Mark. 1995, 15, 265–302. [Google Scholar] [CrossRef]

- Shaikh, I.; Padhi, P. Inter-temporal relationship between India VIX and Nifty equity index. Decision 2014, 41, 439–448. [Google Scholar] [CrossRef]

- Shaikh, I. The 2016 U.S. presidential election and the Stock, FX and VIX markets. N. Am. J. Econ. Financ. 2017, 42, 546–563. [Google Scholar] [CrossRef]

- Engle, R. The use of ARCH/GARCH models in applied econometrics. J. Econ. Perspect. 2001, 15, 157–168. [Google Scholar] [CrossRef]

- Bollerslev, T.; Melvin, M. Bid—Ask spreads and volatility in the foreign exchange market: An empirical analysis. J. Int. Econ. 1994, 36, 355–372. [Google Scholar] [CrossRef]

- Nana, G.-A.N.; Korn, R.; Erlwein-Saye, C. GARCH-extended models: Theoretical properties and applications. arXiv, 2013; arXiv:1307.6685. [Google Scholar]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Kost, K. US Equity Market Volatility Index. Chicago. 2018. Available online: http://www.policyuncertainty.com/EMV_monthly.html (accessed on 3 March 2019).

{kind=link}

| Year | Equity Market | Crude Oil | Gold | Corn Market | BP-USD | Interest Rate | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| VIX-EPU | p-Value | OVX-EPU | p-Value | GVZ-EPU | p-Value | CIV-EPU | p-Value | BPVIX-EPU | p-Value | TYVIX-EPU | p-Value | |

| 2000 | 0.242 | 0.000 a | ||||||||||

| 2001 | 0.580 | 0.000 a | ||||||||||

| 2002 | 0.285 | 0.000 a | ||||||||||

| 2003 | 0.627 | 0.000 a | −0.197 | 0.002 a | ||||||||

| 2004 | 0.075 | 0.289 | 0.067 | 0.300 | ||||||||

| 2005 | 0.135 | 0.038 b | −0.006 | 0.922 | ||||||||

| 2006 | 0.262 | 0.000 a | 0.119 | 0.069 c | ||||||||

| 2007 | 0.246 | 0.000 a | 0.271 | 0.000 a | 0.337 | 0.000 a | 0.302 | 0.000 a | ||||

| 2008 | 0.559 | 0.000 a | 0.366 | 0.000 a | 0.474 | 0.000 a | 0.539 | 0.000 a | ||||

| 2009 | 0.587 | 0.000 a | 0.572 | 0.000 a | 0.595 | 0.000 a | 0.554 | 0.000 a | 0.371 | 0.000 a | ||

| 2010 | −0.015 | 0.988 | −0.088 | 0.218 | −0.090 | 0.155 | −0.302 | 0.000 a | 0.021 | 0.746 | ||

| 2011 | 0.423 | 0.000 a | 0.316 | 0.000 a | 0.309 | 0.000 a | −0.076 | 0.358 | 0.256 | 0.000 a | 0.310 | 0.000 a |

| 2012 | −0.062 | 0.353 | 0.123 | 0.013 b | −0.325 | 0.000 a | −0.058 | 0.366 | −0.349 | 0.000 a | −0.433 | 0.000 a |

| 2013 | 0.199 | 0.000 a | 0.132 | 0.036 b | −0.235 | 0.000 a | −0.222 | 0.000 a | −0.080 | 0.209 | −0.109 | 0.091 c |

| 2014 | 0.072 | 0.296 | −0.076 | 0.286 | 0.061 | 0.339 | −0.137 | 0.031 b | 0.015 | 0.819 | 0.013 | 0.840 |

| 2015 | 0.323 | 0.000 a | 0.198 | 0.003 a | 0.033 | 0.605 | 0.093 | 0.144 | −0.073 | 0.259 | 0.148 | 0.021 b |

| 2016 | 0.085 | 0.216 | −0.052 | 0.471 | 0.161 | 0.011 b | 0.075 | 0.243 | 0.099 | 0.119 | 0.431 | 0.000 a |

| 2017 | 0.056 | 0.454 | 0.126 | 0.053 c | 0.208 | 0.001 a | 0.028 | 0.665 | 0.257 | 0.000 a | 0.337 | 0.000 a |

| Full Sample | 0.456 | 0.000 a | 0.233 | 0.000 a | 0.320 | 0.000 a | 0.268 | 0.000 a | 0.333 | 0.000 a | 0.339 | 0.000 a |

| Equity | PP-Test | Commodity | PP-Test | FX-Market | PP-Test | Int. Rate | PP-Test | PUI | PP-Test |

|---|---|---|---|---|---|---|---|---|---|

| VIX | −5.64 a | OIV | −3.06 b | EUVIX | −3.39 b | TYVIX | −3.92 a | EPU | −61.60 a |

| VXN | −3.88 a | OVX | −3.18 c | JPYVIX | −4.63 a | EMPU | −64.35 a | ||

| VXO | −5.55 a | GVZ | −4.93 a | BPVIX | −3.65 a | ||||

| VXD | −5.30 a | CIV | −4.45 a | ||||||

| VVIX | −9.32 a | SIV | −4.93 a |

| Column (1) | Column (2) | Column (3) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FOMC Meeting | GDP Report | Other Macro | Returns | |||||||||

| Market | Intercept | FOMC(−)5 | FOMC | FOMC(+)5 | GDPB(−)5 | GDP | GDP(+)5 | MACRO(−)2 | MACRO | MACRO(+)2 | ||

| VIX | −0.0605 | 0.1573 | −0.2437 | −0.0248 | 0.0119 | −0.0741 | 0.1042 | 0.1127 | −0.007 | 0.1325 | −107.1201 | −0.0734 |

| z-stat | −1.29 | 2.86 a | −2.07 b | −0.46 | 0.26 | −0.82 | 1.99 b | 1.39 | −0.26 | 2.25 b | −80.02 a | −5.87 a |

| VXN | 0.0265 | 0.0149 | −0.1474 | −0.0108 | 0.0059 | −0.0011 | 0.1015 | 0.1557 | −0.1197 | 0.099 | −79.8738 | −0.0355 |

| z-stat | 0.61 | 0.58 | −2.59 a | −0.36 | 0.21 | −0.02 | 3.64 a | 3.04 a | −2.64 a | 2.21 b | −91.31 a | −2.09 b |

| VXO | 0.0493 | 0.0024 | 0.0442 | −0.0159 | −0.0348 | 0.0722 | 0.0697 | 0.0887 | −0.0415 | −0.039 | −117.0687 | −0.1167 |

| z-stat | 1.40 | 0.09 | 0.83 | −0.69 | −1.42 | 1.79 c | 2.95 a | 2.10 b | −1.13 | −1.06 | −115.84 a | −6.43 a |

| VXD | −0.0229 | 0.0494 | −0.1713 | 0.0057 | 0.008 | 0.0638 | 0.0511 | 0.0992 | −0.0536 | 0.1124 | −86.9033 | −0.118 |

| z-stat | −0.69 | 2.01 b | −3.14 a | 0.23 | 0.37 | 1.63 | 2.33 b | 2.62 a | −1.54 | 3.18 a | −112.47 a | −6.23 a |

| VVIX | 0.5017 | 0.3488 | −0.3816 | 0.1569 | −0.5795 | −0.5665 | −0.4101 | 0.289 | −0.1368 | −0.2008 | −238.3444 | −0.0297 |

| z-stat | 1.81 c | 1.82 c | −1.14 | 0.91 | −3.57 a | −1.86 c | −2.50 b | 0.81 | −0.46 | −0.64 | −41.62 a | −1.27 |

| OIV | 0.1138 | 0.0922 | −0.0727 | 0.0454 | −0.0593 | −0.2602 | 0.01 | 0.0315 | −0.3067 | 0.076 | −34.4168 | −0.0099 |

| z-stat | 0.74 | 1.17 | −0.44 | 0.53 | −0.86 | −1.82 c | 0.16 | 0.17 | −1.98 b | 0.49 | −29.45 a | −0.38 |

| OVX | 0.1471 | 0.2026 | −0.229 | −0.0123 | −0.148 | 0.3199 | 0.0618 | −0.154 | −0.2901 | 0.0642 | −39.3042 | 0.0081 |

| z-stat | 1.31 | 1.28 | −0.76 | −0.07 | −0.95 | 1.25 | 0.53 | −0.62 | −1.76 c | 0.37 | −23.28 a | 0.28 |

| GVZ | 0.1093 | 0.1326 | −0.2822 | 0.0263 | 0.0397 | −0.0617 | 0.1252 | −0.1111 | −0.2341 | −0.0987 | −7.9743 | −0.0666 |

| z-stat | 1.39 | 2.58 a | −2.68 a | 0.55 | 0.90 | −0.70 | 2.97 a | −1.13 | −2.95 a | −1.21 | −5.84 a | −2.85 a |

| CIV | 0.1031 | 0.0008 | 0.2265 | 0.1208 | 0.0732 | 0.0985 | −0.0129 | −0.2147 | −0.2603 | −0.0691 | −8.56 | −0.0344 |

| z-stat | 0.92 | 0.01 | 1.12 | 1.55 | 1.10 | 0.99 | −0.22 | −1.53 | −2.30 b | −0.60 | −3.66 a | −1.34 |

| SIV | −0.0758 | 0.2306 | −0.0403 | 0.0982 | 0.0787 | 0.1774 | 0.217 | −0.0042 | −0.1997 | 0.1052 | −12.69 | −0.0707 |

| z-stat | −0.28 | 1.85 c | −0.21 | 0.75 | 0.67 | 0.86 | 2.11 b | −0.01 | −0.73 | 0.38 | −4.56 a | −1.93 c |

| EUVIX | 0.0889 | 0.0113 | −0.0969 | 0.0071 | 0.0139 | 0.0214 | −0.0451 | −0.0498 | −0.1381 | −0.0435 | −18.9649 | 0.022 |

| z-stat | 2.22 b | 0.51 | −2.45 b | 0.36 | 0.79 | 0.56 | −2.37 b | −1.05 | −3.50 a | −1.07 | −20.36 a | 0.97 |

| JPYVIX | 0.0327 | 0.0329 | −0.0731 | −0.081 | 0.0218 | −0.0413 | 0.0291 | −0.048 | −0.0768 | −0.0009 | 22.923 | −0.0144 |

| z-stat | 0.71 | 1.35 | −1.59 | −3.39 a | 0.90 | −0.98 | 1.32 | −1.00 | −1.70 c | −0.02 | 20.65 a | −0.64 |

| BPVIX | 0.0771 | 0.0233 | −0.0677 | 0.0194 | −0.0208 | −0.0088 | −0.0497 | −0.0365 | −0.1237 | −0.0143 | −17.5863 | 0.002 |

| z-stat | 3.12 a | 1.43 | −2.07 b | 1.31 | −1.43 | −0.31 | −3.67 a | −1.12 | −5.12 a | −0.57 | −19.61 a | 0.09 |

| TYVIX | 0.0282 | 0.0179 | −0.1836 | −0.0042 | 0.004 | 0.0001 | −0.0138 | −0.0005 | −0.0811 | 0.0163 | −11.9532 | −0.0549 |

| z-stat | 1.95 c | 1.56 | −9.68 a | −0.46 | 0.39 | 0.01 | −1.54 | −0.03 | −5.44 a | 1.03 | −13.16 a | −2.72 a |

| Market | Intercept | ARCH | GARCH | EPU | EMPUI | 2KBoom | ECC | GFC | FPB | PEQ42004 | PEQ42008 | PEQ42012 | PEQ42016 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| VIX | 0.0216 | 0.1463 | 0.7458 | 0.0225 | 0.1379 | −0.0256 | −0.0046 | 0.034 | −0.0237 | −0.0037 | 0.5567 | −0.0592 | −0.0404 |

| z-stat | 2.86 a | 16.88 a | 64.44 a | 2.33 b | 10.69 a | −5.36 a | −0.36 | 1.84 c | −4.25 a | −0.23 | 1.99 b | −3.19 a | −3.23 a |

| VXN | 0.0205 | 0.1507 | 0.7402 | 0.0253 | 0.1366 | −0.0255 | −0.0024 | 0.0343 | −0.0235 | −0.0055 | 0.5597 | −0.0612 | −0.0402 |

| z-stat | 2.64 a | 17.03 a | 62.35 a | 2.49 b | 10.35 a | −5.07 a | −0.19 | 1.75 c | −3.89 a | −0.36 | 1.96 b | −3.16 a | −3.13 a |

| VXO | 0.0572 | 0.1886 | 0.7052 | 0.0147 | 0.0831 | −0.0545 | 0.0069 | 0.0842 | −0.0289 | 0.0347 | 1.1546 | −0.0234 | 0.0049 |

| z-stat | 7.19 a | 15.7 a | 54.24 a | 1.69 a | 10.07 a | −9.26 a | 0.45 | 3.12 a | −3.96 a | 1.53 | 2.09 b | −0.95 | 0.19 |

| VXD | 0.031 | 0.2402 | 0.6325 | 0.0275 | 0.0563 | −0.0071 | 0.0269 | 0.0954 | 0.0035 | 0.0049 | 0.8127 | 0.2001 | −0.0108 |

| z-stat | 5.64 a | 18.77 a | 49.88 a | 3.16 a | 7.03 a | −1.83 c | 1.98 c | 3.91 a | 0.49 | 0.21 | 1.99 b | 7.58 a | −0.65 c |

| VVIX | 4.1337 | 0.2211 | 0.4306 | 1.1237 | 4.6104 | −2.5638 | −1.4851 | −3.2913 | 13.8929 | −0.9373 | −2.0476 | ||

| z-stat | 9.71 a | 14.01 a | 13.38 a | 3.32 a | 11.17 a | −4.57 a | −2.36 a | −9.42 a | 2.15 b | −1.03 | −2.42 b | ||

| OIV | 0.1747 | 0.1626 | 0.7832 | −0.1196 | 0.2109 | 0.0648 | −0.0414 | 0.0841 | |||||

| z-stat | 6.59 a | 13.35 a | 54.85 a | −4.17 a | 6.24 a | 3.26 a | −1.02 | 1.24 | |||||

| OVX | 3.1314 | 0.1444 | 0.5688 | −0.4847 | −0.2089 | −2.5746 | −1.3284 | 0.0679 | −0.8342 | 3.036 | −0.7624 | −0.9781 | |

| z-stat | 13.75 a | 11.91 a | 22.31 a | −9.64 a | −8.45 a | −9.71 a | −7.06 a | 0.28 | −4.63 a | 4.57 a | −9.21 a | −3.79 a | |

| GVZ | 0.0779 | 0.1769 | 0.7229 | −0.0601 | 0.1815 | 0.2565 | 0.0828 | −0.0232 | 0.0151 | ||||

| z-stat | 6.13 a | 15.02 a | 43.63 a | −3.93 a | 7.03 a | 6.29 a | 5.95 a | −0.97 | 0.53 | ||||

| CIV | 0.0954 | 0.0978 | 0.8421 | −0.0476 | 0.0314 | 0.0694 | −0.0052 | 0.2952 | |||||

| z-stat | 6.34 a | 9.76 a | 67.21 a | −3.23 a | 1.92 c | 4.81 a | −0.17 | 8.36 a | |||||

| SIV | 2.7683 | 0.2807 | 0.0093 | −0.1327 | −0.1785 | 0.3664 | −1.1089 | −1.7899 | |||||

| z-stat | 22.65 a | 8.88 a | 0.61 | −1.12 | −3.60 a | 2.71 a | −4.06 a | −14.69 a | |||||

| EUVIX | 0.0111 | 0.1525 | 0.7171 | 0.0182 | 0.0063 | −0.0099 | 0.011 | −0.0125 | 0.3712 | −0.0232 | 0.3659 | ||

| z-stat | 4.82 a | 13.62 a | 38.87 a | 5.79 a | 2.12 b | −4.82 a | 1.75 c | −5.52 a | 3.49 a | −6.69 a | 10.13 a | ||

| JPYVIX | 0.0216 | 0.2011 | 0.7085 | −0.0122 | 0.068 | −0.0024 | −0.0004 | −0.0002 | 0.2142 | −0.0043 | 0.0182 | ||

| z-stat | 5.21 a | 14.89 a | 44.26 a | −3.29 a | 10.27 a | −0.41 | −0.09 | −0.06 | 2.65 a | −0.57 | 1.09 | ||

| BPVIX | 0.0074 | 0.2054 | 0.7464 | −0.0017 | 0.0109 | −0.0034 | 0.0615 | −0.0007 | 0.1081 | −0.0053 | 0.1103 | ||

| z-stat | 6.65 a | 14.29 a | 58.29 a | −1.65 c | 5.92 a | −2.71 a | 4.94 a | −0.84 | 1.38 | −3.59 a | 7.56 a | ||

| TYVIX | 0.0071 | 0.1785 | 0.7267 a | −0.003 | 0.0078 | −0.0022 | 0.0129 | 0.0159 | 0.0047 | 0.0077 | 0.0474 | −0.0038 | −0.0007 |

| z-stat | 6.95 a | 15.46 a | 43.2 a | −2.88 a | 5.98 a | −3.61 a | 6.26 a | 5.68 a | 5.18 a | 2.77 a | 2.05 b | −1.97 b | −0.27 |

| Market | Null Ho: FOMC = GDP = Macro = 0 | Null Ho: P.E Year 2004 = 2008 = 2012 = 2016 = 0 | ||

|---|---|---|---|---|

| Wald F-stat | p-Value | Wald F-stat | p-Value | |

| VIX | 2.88 | 0.035 b | 25.23 | 0.000 a |

| VXN | 39.39 | 0.000 a | 5.85 | 0.000 a |

| VXO | 1.60 | 0.187 | 1.87 | 0.112 |

| VXD | 4.97 | 0.002 a | 15.26 | 0.000 a |

| VVIX | 24.85 | 0.000 a | 14.16 | 0.000 a |

| OIV | 2.50 | 0.058 c | 1.27 | 0.282 |

| OVX | 1.61 | 0.186 | 34.34 | 0.000 a |

| GVZ | 5.66 | 0.001 a | 0.61 | 0.546 |

| CIV | 2.35 | 0.070 | 34.45 | 0.000 a |

| SIV | 0.43 | 0.732 | 54.51 | 0.000 a |

| EUVIX | 2.31 | 0.074 c | 39.04 | 0.000 a |

| JPYVIX | 1.94 | 0.121 | 2.78 | 0.040 b |

| BPVIX | 10.57 | 0.000 a | 21.62 | 0.000 a |

| TYVIX | 44.65 | 0.000 a | 3.67 | 0.006 a |

| Market | VIX | OVX | GVZ | CIV | BPVIX | TYVIX | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Regressors | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | |

| Regime-1 | Intercept | 0.0052 | 0.679 | −0.0145 | 0.669 | −0.1826 | 0.000 a | −0.0687 | 0.812 | −0.6069 | 0.000 a | 0.0701 | 0.000 a |

| 0.0001 | 0.585 | 0.0011 | 0.096 | −0.0013 | 0.080 c | 0.0640 | 0.000 a | −0.0068 | 0.045 b | 0.0001 | 0.242 | ||

| 0.0000 | 0.906 | 0.0011 | 0.102 | −0.0004 | 0.547 | 0.0219 | 0.001 a | −0.0202 | 0.000 a | 0.0002 | 0.095 c | ||

| 0.0009 | 0.000 a | 0.0018 | 0.001 a | 0.0009 | 0.195 | −0.0258 | 0.000 a | −0.0009 | 0.562 | 0.0004 | 0.000 a | ||

| 0.0002 | 0.171 | 0.0007 | 0.183 | 0.0004 | 0.578 | 0.0461 | 0.000 a | 0.0051 | 0.000 a | 0.0001 | 0.202 | ||

| −97.5962 | 0.000 a | −25.5191 | 0.000 a | −77.9618 | 0.000 a | −53.3292 | 0.000 a | −185.2961 | 0.000 a | −33.3041 | 0.000 a | ||

| −0.0466 | 0.000 a | −0.0079 | 0.651 | 0.0221 | 0.636 | −0.9245 | 0.000 a | 0.4904 | 0.000 a | −0.0126 | 0.000 a | ||

| Regime-2 | Intercept | −0.3204 | 0.000 a | −0.2192 | 0.322 | −0.0596 | 0.045 b | 0.0084 | 0.815 | −0.0013 | 0.890 | 0.1200 | 0.002 a |

| 0.0025 | 0.063 c | 0.0104 | 0.005 a | −0.0006 | 0.344 | 0.0008 | 0.319 | 0.0003 | 0.132 | 0.0002 | 0.514 | ||

| 0.0012 | 0.450 | 0.0116 | 0.000 a | 0.0001 | 0.852 | 0.0006 | 0.470 | 0.0010 | 0.000 a | −0.0002 | 0.396 | ||

| −0.0024 | 0.000 a | 0.0003 | 0.861 | 0.0025 | 0.000 a | 0.0000 | 0.954 | 0.0007 | 0.000 a | 0.0005 | 0.001 a | ||

| −0.0046 | 0.000 a | 0.0022 | 0.478 | 0.0023 | 0.000 a | −0.0008 | 0.204 | 0.0004 | 0.005 a | 0.0004 | 0.029 | ||

| −263.8217 | 0.000 a | −114.2135 | 0.000 a | 46.5499 | 0.000 a | 17.5654 | 0.000 a | −15.3536 | 0.000 a | 65.5653 | 0.000 a | ||

| 0.0671 | 0.000 a | −1.0081 | 0.000 a | −0.1949 | 0.000 a | 0.0288 | 0.194 | −0.0525 | 0.003 a | −0.0231 | 0.000 a | ||

| Transition | Matrix | P11 | P21 | P11 | P21 | P11 | P21 | P11 | P21 | P11 | P21 | P11 | P21 |

| Parameters | 3.7887 | −0.4831 | 2.5556 | 2.4937 | 2.6719 | −2.9322 | −0.7045 | −3.5057 | −0.7019 | −3.9190 | 3.3587 | −2.0403 | |

| p-value | 0.000 a | 0.026 b | 0.000 a | 0.000 a | 0.000 a | 0.000 a | 0.081 c | 0.000 a | 0.029 | 0.000 a | 0.000 a | 0.000 a | |

| DW-stat | 2.11 | 2.22 | 2.04 | 2.17 | 2.01 | 2.05 | |||||||

| AIC | 2.51 | 3.93 | 2.91 | 3.69 | 1.46 | 0.37 | |||||||

| Log likelihood | −5701.20 | −5286.63 | −3330.27 | −3082.19 | −2027.79 | −672.82 | |||||||

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shaikh, I. On the Relationship between Economic Policy Uncertainty and the Implied Volatility Index. Sustainability 2019, 11, 1628. https://doi.org/10.3390/su11061628

Shaikh I. On the Relationship between Economic Policy Uncertainty and the Implied Volatility Index. Sustainability. 2019; 11(6):1628. https://doi.org/10.3390/su11061628

Chicago/Turabian StyleShaikh, Imlak. 2019. "On the Relationship between Economic Policy Uncertainty and the Implied Volatility Index" Sustainability 11, no. 6: 1628. https://doi.org/10.3390/su11061628

APA StyleShaikh, I. (2019). On the Relationship between Economic Policy Uncertainty and the Implied Volatility Index. Sustainability, 11(6), 1628. https://doi.org/10.3390/su11061628