Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums

Abstract

1. Introduction

2. Literature Review

3. Theoretical Analysis and Research Hypotheses

3.1. Target Firm’s CSR and Cross-Border Acquisition Premium

3.2. The Moderating Role of Institutional Factors

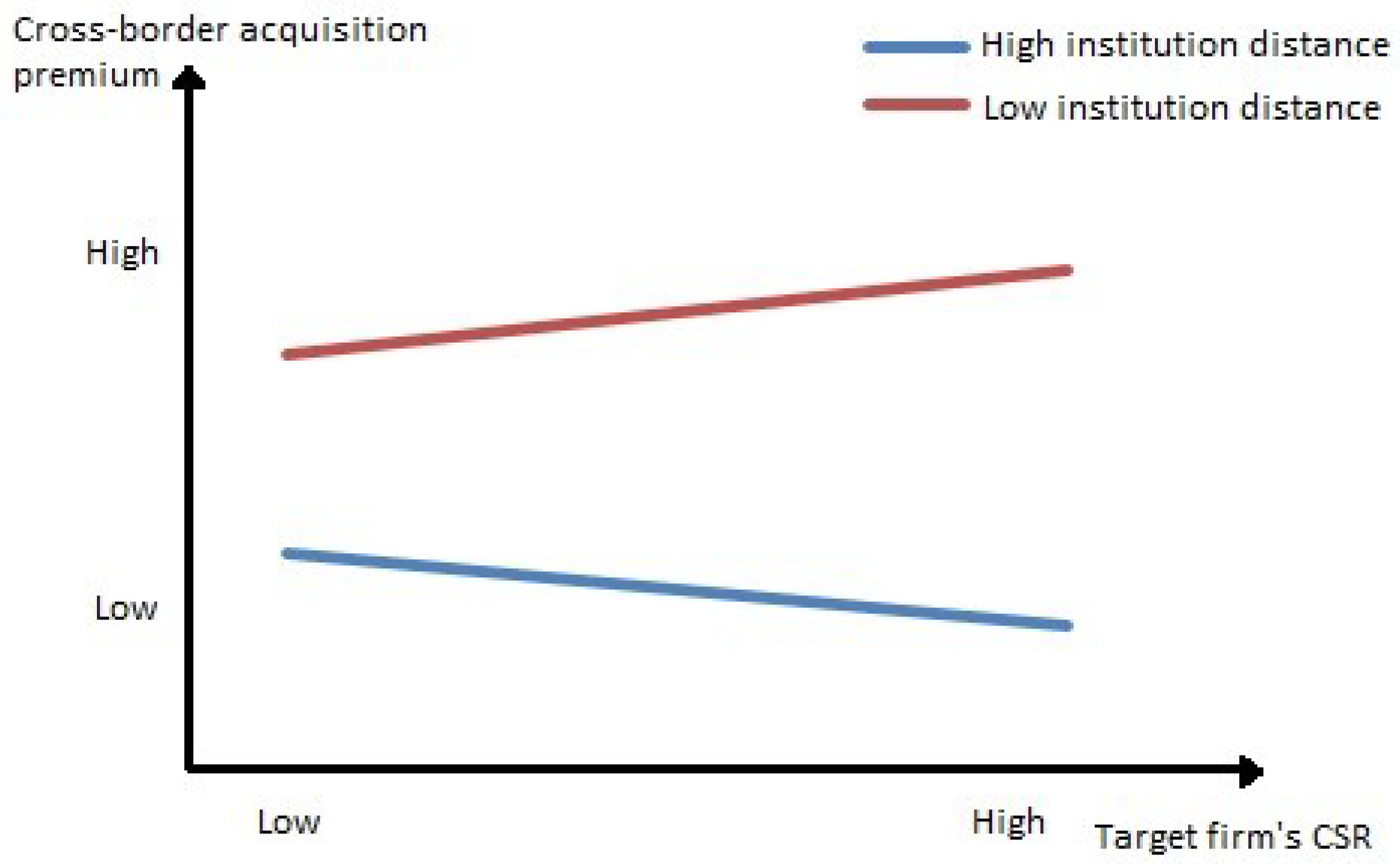

3.2.1. The Moderating Role of Institutional Distance

3.2.2. The Moderating Role of Cultural Distance

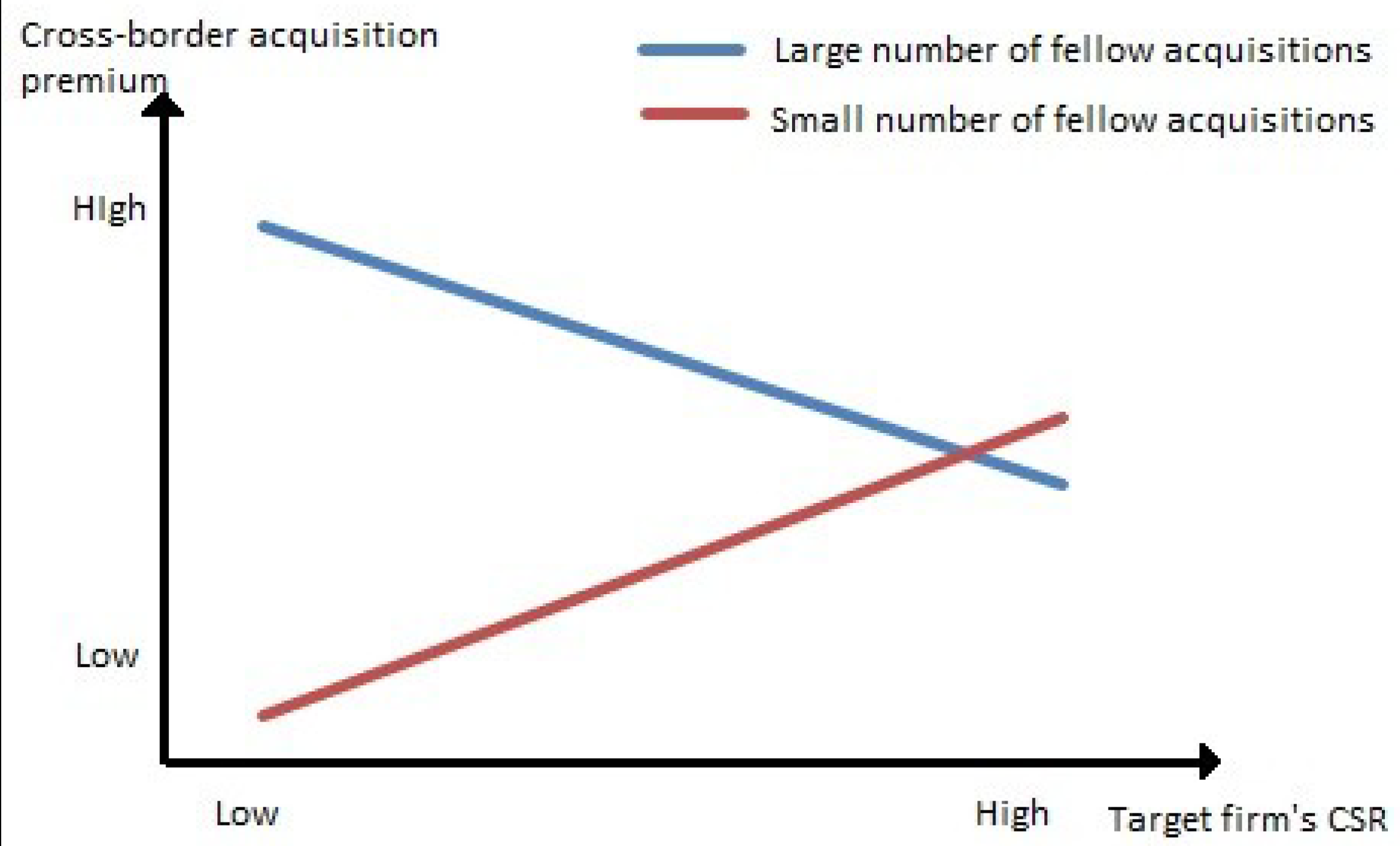

3.2.3. The Moderating Role of the Number of Fellow Acquisitions

4. Research Methodology

4.1. Data and Sample

4.2. Measures

4.2.1. Dependent Variable

4.2.2. Independent Variable

4.2.3. Moderating Variables

4.2.4. Control Variables

4.3. Model Estimation

5. Empirical Result

5.1. Descriptive Statistics and Correlation Analysis

5.2. Hypothesis Testing

5.3. Robustness Test

6. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S Back in Corporate Social Responsibility: A Multilevel Theory of Social Change in Organizations. Acad. Manag. Rev. 2007, 32, 836–865. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Shao, Y.; Gao, S. CSR and Firm Value: Evidence from China. Sustainability 2018, 10, 4597. [Google Scholar] [CrossRef]

- Hawn, O.; Chatterji, A.K.; Mitchell, W. Do investors actually value sustainability? New evidence from investor reactions to the Dow Jones Sustainability Index (DJSI). Strateg. Manag. J. 2018, 39, 949–976. [Google Scholar] [CrossRef]

- Marano, V.; Kostova, T. Unpacking the Institutional Complexity in Adoption of CSR Practices in Multinational Enterprises. J. Manag. Stud. 2016, 53, 28–54. [Google Scholar] [CrossRef]

- Flammer, C.; Jiao, L. Corporate social responsibility as an employee governance tool: Evidence from a quasi-experiment. Strateg. Manag. J. 2016, 2014, 163–183. [Google Scholar] [CrossRef]

- Berchicci, L.; Dowell, G.; King, A.A. Environmental capabilities and corporate strategy: Exploring acquisitions among US manufacturing firms. Strateg. Manag. J. 2012, 33, 1053–1071. [Google Scholar] [CrossRef]

- Austin, J.E.; Leonard, H.B. Can the virtuous mouse and the wealthy elephant live happily ever after? Calif. Manag. Rev. 2008, 51. [Google Scholar] [CrossRef]

- Deloitte. How Green is the Deal? The Growing Role of Sustainability in M&A. 2008. Available online: https://www2.deloitte.com/content/dam/Deloitte/il/Documents/risk/CCG/other_comittees/how_green_is_the_deal_deloitte_102408.pdf. (accessed on 24 October 2008).

- Aktas, N.; De Bodt, E.; Cousin, J. Do Financial Markets Care about SRI? Evidence from Mergers and Acquisitions. J. Bank. Financ. 2011, 35, 1753–1761. [Google Scholar] [CrossRef]

- Deng, X.; Kang, J.-k.; Low, B.S. Corporate social responsibility and stakeholder value maximization: Evidence from mergers. J. Financ. Econ. 2013, 110, 87–109. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horn 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Gupta, A.; Briscoe, F.; Hambrick, D.C. Red, blue, and purple firms: Organizational political ideology and corporate social responsibility. Strateg. Manag. J. 2017, 38, 1018–1040. [Google Scholar] [CrossRef]

- Smith, N.C. Corporate Social Responsibility: Whether or How? Calif. Manag. Rev. 2003, 45, 52–76. [Google Scholar] [CrossRef]

- Shiu, Y.-M.; Yang, S.-L. Does engagement in corporate social responsibility provide strategic insurance-like effects? Strateg. Manag. J. 2017, 38, 455–470. [Google Scholar] [CrossRef]

- Mithani, M.A. Liability of foreignness, natural disasters, and corporate philanthropy. J. Int. Bus. Stud. 2017, 48, 941–963. [Google Scholar] [CrossRef]

- Menguc, B.; Ozanne, L.K. Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation-business performance relationship. J. Bus. Res. 2005, 58, 430–438. [Google Scholar] [CrossRef]

- Lim, A.; Tsutsui, K. Globalization and Commitment in Corporate Social Responsibility Cross-National Analyses of Institutional and Political-Economy Effects. Am. Sociol. R 2012, 77, 69–98. [Google Scholar] [CrossRef]

- Coulson, A.B.; Monks, V. Corporate Environmental Performance Considerations within Bank Lending Decisions. Eco-Manag. Audit. 1999, 6, 10. [Google Scholar] [CrossRef]

- Saxton, T.; Dollinger, M. Target Reputation and Appropriability: Picking and Deploying Resources in Acquisitions. J. Manag. 2004, 30, 123–147. [Google Scholar] [CrossRef]

- Wickert, C.; Vaccaro, A.; Cornelissen, J. “Buying” Corporate Social Responsibility: Organisational Identity Orientation as a Determinant of Practice Adoption. J. Bus. Eth. 2017, 142, 497–514. [Google Scholar] [CrossRef]

- Cloutier, C.; Langley, A. Negotiating the Moral Aspects of Purpose in Single and Cross-Sectoral Collaborations. J. Bus. Eth. 2017, 141, 103–131. [Google Scholar] [CrossRef]

- Hawn, O.; Ioannou, I. Mind the gap: The interplay between external and internal actions in the case of corporate social responsibility. Strateg. Manag. J. 2016, 37, 2569–2588. [Google Scholar] [CrossRef]

- Kaul, A.; Wu, B. A capabilities-based perspective on target selection in acquisitions. Strateg. Manag. J. 2016, 37, 1220–1239. [Google Scholar] [CrossRef]

- Gomes, M.; Marsat, S. Does CSR impact premiums in M&A transactions? Financ. Res. Lett. 2017, 26, 71–80. [Google Scholar] [CrossRef]

- Frynas, J.G.; Yamahaki, C. Corporate social responsibility: Review and roadmap of theoretical perspectives. Bus. Eth. Eur. 2016, 25, 258–285. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Graves, S.B.; Waddock, S.A. Institutional Owners and Corporate Social Performance. Acad. Manag. J. 1994, 37, 1034–1046. [Google Scholar] [CrossRef]

- Bravo, R.; Matute, J.; Pina, J.M. Corporate Social Responsibility as a Vehicle to Reveal the Corporate Identity: A Study Focused on the Websites of Spanish Financial Entities. J. Bus. Eth. 2012, 107, 129–146. [Google Scholar] [CrossRef]

- Ahammad, M.F.; Tarba, S.; Frynas, G.; Scola, A. Integration of nonmarket and market activities in cross-border mergers and acquisitions. Br. J. Manag. 2017, 28, 629–648. [Google Scholar] [CrossRef]

- Knudsen, J.S.; Brown, D. Why governments intervene: Exploring mixed motives for public policies on corporate social responsibility. Public Policy Adm. 2014, 30, 51–72. [Google Scholar] [CrossRef]

- Luo, X.R.; Wang, D.; Zhang, J. Whose Call to Answer: Institutional Complexity and Firms’ CSR Reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C.; Carroll, C.E.; Georgiadis, A.P.; Siegel, D.S. Does Media Attention Drive Corporate Social Responsibility? J. Bus. Res. 2010, 65, 1622–1627. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate Social Responsibility and Firm Financial Performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Xie, E.; Reddy, K.S.; Liang, J. Country-specific determinants of cross-border mergers and acquisitions: A comprehensive review and future research directions. J. World Bus. 2017, 52, 127–183. [Google Scholar] [CrossRef]

- Groening, C.; Kanuri, V.K. Investor reaction to positive and negative corporate social events. J. Bus. Res. 2013, 66, 1852–1860. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. “Implicit” and “Explicit” CSR: A Conceptual Framework for a Comparative Understandingof Corporate Social Responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. R. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized Organizations: Formal Structure as Myth and Ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef]

- Scott, W.R. Institutions and Organizations. Ideas, Interests and Identities; Sage: London, UK, 1995. [Google Scholar]

- Boehe, D.M.; Barin Cruz, L. Corporate Social Responsibility, Product Differentiation Strategy and Export Performance. J. Bus. Eth. 2010, 91, 325–346. [Google Scholar] [CrossRef]

- Dikova, D.; Sahib, P.R.; van Witteloostuijn, A. Cross-border acquisition abandonment and completion: The effect of institutional differences and organizational learning in the international business service industry, 1981–2001. J. Int. Bus. Stud. 2009, 41, 223–245. [Google Scholar] [CrossRef]

- Kostova, T.; Zaheer, S. Organizational Legitimacy under Conditions of Complexity: The Case of the Multinational Enterprise. Acad. Manag. Rev. 1999, 24, 64–81. [Google Scholar] [CrossRef]

- Shenkar, O.; Luo, Y.; Yeheskel, O. From “Distance” to “Friction”: Substituting Metaphors and Redirecting Intercultural Research. Acad. Manag. Rev. 2008, 33, 905–923. [Google Scholar] [CrossRef]

- Makino, S.; Tsang, E.W. Historical ties and foreign direct investment: An exploratory study. J. Int. Bus. Stud. 2011, 42, 545–557. [Google Scholar] [CrossRef]

- Hernández, V.; Nieto, M.J.; Boellis, A. The asymmetric effect of institutional distance on international location: Family versus nonfamily firms. Glob. Strateg. J. 2018, 8, 22–45. [Google Scholar] [CrossRef]

- Julian, S.D.; Ofori-dankwa, J.C. Financial resource availability and corporate social responsibility expenditures in a sub-Saharan economy: The institutional difference hypothesis. Strateg. Manag. J. 2013, 34, 1314–1330. [Google Scholar] [CrossRef]

- Barin Cruz, L.; Dwyer, R.; Avila Pedrozo, E. Corporate social responsibility and green management. Manag. Decis. 2009, 47, 1174–1199. [Google Scholar] [CrossRef]

- Wang, H.; Qian, C. Corporate Philanthropy and Corporate Financial Performance: The Roles of Stakeholder Response and Political Access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Gautier, A.; Pache, A.-C. Research on Corporate Philanthropy: A Review and Assessment. J. Bus. Eth. 2015, 126, 343–369. [Google Scholar] [CrossRef]

- Mirvis, P.H. Commentary: Can You Buy CSR? Calif. Manag. Rev. 2008, 51, 9. [Google Scholar] [CrossRef]

- Tihanyi, L.; Griffith, D.A.; Russell, C.J. The effect of cultural distance on entry mode choice, international diversification, and MNE performance: A meta-analysis. J. Int. Bus. Stud. 2005, 36, 270–283. [Google Scholar] [CrossRef]

- Reus, T.H.; Lamont, B.T. The double-edged sword of cultural distance in international acquisitions. J. Int. Bus. Stud. 2009, 40, 1298–1316. [Google Scholar] [CrossRef]

- Campbell, J.T.; Eden, L.; Miller, S.R. Multinationals and corporate social responsibility in host countries: Does distance matter? J. Int. Bus. Stud. 2012, 43, 84–106. [Google Scholar] [CrossRef]

- Sousa, C.M.P.; Tan, Q. Exit from a foreign market: Do poor performance, strategic fit, cultural distance, and international experience matter? J. Int. Market. 2015, 15, 1–53. [Google Scholar] [CrossRef]

- Phillips, N.; Tracey, P.; Karra, N. Rethinking institutional distance: Strengthening the tie between new institutional theory and international management. Strateg. Organ. 2009, 7, 339–348. [Google Scholar] [CrossRef]

- Lord, R.G.; Kernan, M.C. Scripts as Determinants of Purposeful Behavior in Organizations. Acad. Manag. Rev. 1987, 12, 265–277. [Google Scholar] [CrossRef]

- Zaheer, S. Overcoming the Liability of Foreignness. Acad. Manag. J. 1995, 38, 341–363. [Google Scholar] [CrossRef]

- Ang, S.H.; Benischke, M.H.; Doh, J.P. The interactions of institutions on foreign market entry mode. Strateg. Manag. J. 2015, 36, 1536–1553. [Google Scholar] [CrossRef]

- Hart, T.A.; Sharfman, M. Assessing the Concurrent Validity of the Revised Kinder, Lydenberg, and Domini Corporate Social Performance Indicators. Bus. Soc. 2012, 54, 575–598. [Google Scholar] [CrossRef]

- Malhotra, S.; Zhu, P.; Reus, T.H. Anchoring on The Acquisition Premium Decisions of Others. Strateg. Manag. J. 2015, 36, 1866–1876. [Google Scholar] [CrossRef]

- Guo, W.; Clougherty, J.A.; Duso, T. Why are Chinese MNES not Financially Competitive in Cross-border Acquisitions? The Role of State Ownership. Long. Range. Plann. 2016, 49, 614–631. [Google Scholar] [CrossRef]

- Reuer, J.J.; Tong, T.W.; Wu, C.-W. A Signaling Theory of Acquisition Premiums: Evidence from IPO Targets. Acad. Manag. J. 2012, 55, 667–683. [Google Scholar] [CrossRef]

- Moeller, S.B.; Schlingemann, F.P.; Stulz, R.M. Firm size and the gains from acquisitions. J. Financ. Econ. 2004, 73, 201–228. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does Corporate Social Responsibility Affect the Cost of Capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Jha, A.; Cox, J. Corporate Social Responsibility and Social Capital. J. Bank. Financ. 2015, 60, 252–270. [Google Scholar] [CrossRef]

- Lim, M.-H.; Lee, J.-H. National economic disparity and cross-border acquisition resolution. Int. Bus. Rev. 2017, 26, 354–364. [Google Scholar] [CrossRef]

- Hofstede, G.; Minkov, M. Long-versus short-term orientation: New perspectives. Asia Pac. Bus. Rev. 2010, 16, 493–504. [Google Scholar] [CrossRef]

- Kogut, B.; Singh, H. The Effect of National Culture on the Choice of Entry Mode. J. Int. Bus. Stud. 1988, 19, 411–432. [Google Scholar] [CrossRef]

- Baum, J.A.C.; Li, S.X.; Usher, J.M. Making the Next Move: How Experiential and Vicarious Learning Shape the Locations of Chains’ Acquisitions. Adm. Sci. Q. 2000, 45, 766–801. [Google Scholar] [CrossRef]

- Raad, E. Why Do Acquiring Firms Pay High Premiums to Takeover Target Shareholders: An Empirical Study. J. Appl. Bus. Res. 2012, 28, 725. [Google Scholar] [CrossRef]

- Liu, H.; Luo, J.-h.; Cui, V. The Impact of Internationalization on Home Country Charitable Donation: Evidence from Chinese Firms. Manag. Int. Rev. 2018, 58, 313–335. [Google Scholar] [CrossRef]

- Lim, J.; Makhija, A.K.; Shenkar, O. The Asymmetric Relationship between National Cultural Distance and Target Premiums in Cross-Border M&A. J. Corp. Financ. 2016, 41, 542–571. [Google Scholar] [CrossRef]

- Hitt, M.A.; Pisano, V. The Cross-Border Merger and Acquisition Strategy: A Research Perspective. Manag. Res. 2003, 1, 14. [Google Scholar] [CrossRef]

- Capron, L. The Long-Term Performance of Horizontal Acquisitions. Strateg. Manag. J. 1999, 20, 987–1018. [Google Scholar] [CrossRef]

- Lim, M.-H.; Lee, J.-H. The effects of industry relatedness and takeover motives on cross-border acquisition completion. J. Bus. Res. 2016, 69, 4787–4792. [Google Scholar] [CrossRef]

- Sharma, S.; Durand, R.M.; Gur-Arie, O. Identification and Analysis of Moderator Variables. J. Market. Res. 1981, 18, 291–300. [Google Scholar] [CrossRef]

- Echols, A.; Tsai, W. Niche and Performance: The Moderating Role of Network Embeddedness. Strateg. Manag. J. 2005, 26, 219–238. [Google Scholar] [CrossRef]

- Ghoul, S.E.; Guedhami, O.; Kim, Y. Country-level institutions, firm value, and the role of corporate social responsibility initiatives. J. Int. Bus. Stud. 2017, 48, 26. [Google Scholar] [CrossRef]

- Caputo, F.; Pizzi, S. Ethical Firms and Web Reporting: Empirical Evidence about the Voluntary Adoption of the Italian “Legality Rating”. Int. J. Bus. Manag. 2019, 14, 36–45. [Google Scholar] [CrossRef]

- Bosetti, L. Web-Based Integrated CSR Reporting: An Empirical Analysis. Symph. Emerg. Issues Manag. 2018, 1, 18–38. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel A: Distribution of the Sample by Acquirer Nation (/Region) | ||

| Nation | Number of Deal | Percentage of Sample |

| Argentina | 2 | 0.79% |

| Australia | 4 | 1.59% |

| Belgium | 2 | 0.79% |

| Brazil | 4 | 1.59% |

| Canada | 44 | 17.46% |

| Chile | 1 | 0.40% |

| China | 7 | 2.78% |

| Denmark | 4 | 1.59% |

| Finland | 2 | 0.79% |

| France | 22 | 8.73% |

| Germany | 13 | 5.16% |

| India | 2 | 0.79% |

| Italy | 5 | 1.98% |

| Japan | 20 | 7.94% |

| Mexico | 5 | 1.98% |

| Netherlands | 17 | 6.75% |

| Norway | 2 | 0.79% |

| Puerto Rico | 2 | 0.79% |

| Singapore | 2 | 0.79% |

| South Korea | 8 | 3.17% |

| Spain | 8 | 3.17% |

| Sweden | 8 | 3.17% |

| Switzerland | 20 | 7.94% |

| United Kingdom | 47 | 18.65% |

| United States | 1 | 0.40% |

| Total | 252 | 100.00% |

| Panel B: Distribution of the Sample by Target Nation (/Region) | ||

| Nation | Number of Deal | Percentage of Sample |

| Belgium | 1 | 0.40% |

| Canada | 1 | 0.40% |

| Finland | 1 | 0.40% |

| France | 2 | 0.79% |

| Netherlands | 1 | 0.40% |

| South Africa | 1 | 0.40% |

| United Kingdom | 1 | 0.40% |

| United States | 244 | 96.83% |

| Total | 252 | 100.00% |

| Panel C: Distribution of the Sample by Year | ||

| Year | Number of Deal | Percentage of Sample |

| 1993 | 2 | 0.79% |

| 1994 | 1 | 0.40% |

| 1995 | 2 | 0.79% |

| 1996 | 3 | 1.19% |

| 1997 | 1 | 0.40% |

| 1998 | 4 | 1.59% |

| 1999 | 5 | 1.98% |

| 2000 | 7 | 2.78% |

| 2001 | 2 | 0.79% |

| 2002 | 2 | 0.79% |

| 2003 | 7 | 2.78% |

| 2004 | 17 | 6.75% |

| 2005 | 18 | 7.14% |

| 2006 | 29 | 11.51% |

| 2007 | 30 | 11.90% |

| 2008 | 16 | 6.35% |

| 2009 | 7 | 2.78% |

| 2010 | 20 | 7.94% |

| 2011 | 11 | 4.37% |

| 2012 | 16 | 6.35% |

| 2013 | 10 | 3.97% |

| 2014 | 20 | 7.94% |

| 2015 | 22 | 8.73% |

| Total | 252 | 100.00% |

| Variable | Mean | S.D. | Min | Max | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Cross-border acquisition premium | 0.209 | 0.728 | −0.997 | 5.328 | 1.000 | |||||||||||||

| 2. Target firm’s CSR | 0.042 | 3.782 | −11.835 | 18.165 | 0.021 * | 1.000 | ||||||||||||

| 3. Institutional distance | 0.034 | 0.705 | −1.820 | 1.795 | −0.129 * | 0.023 | 1.000 | |||||||||||

| 4. Cultural distance | −0.163 | 1.285 | −1.562 | 3.347 | −0.165 * | −0.003 | −0.035 | 1.000 | ||||||||||

| 5. Number of fellow acquisitions | 0.105 | 1.488 | −5.314 | 1.896 | 0.133 * | 0.023 | 0.019 | −0.616 *** | 1.000 | |||||||||

| 6. Acquirer size | 9.838 | 1.681 | 4.443 | 13.212 | −0.041 | −0.019 | 0.015 | −0.041 | −0.029 | 1.000 | ||||||||

| 7. Target size | 7.772 | 1.754 | 3.714 | 12.049 | −0.161 * | 0.081 | 0.008 | 0.047 | −0.040 | 0.323 *** | 1.000 | |||||||

| 8. Acquirer performance | −0.013 | 0.054 | −0.484 | 0.142 | 0.059 | −0.074 | 0.022 | −0.033 | 0.017 | 0.114 * | −0.150 *** | 1.000 | ||||||

| 9. Target performance | −0.077 | 1.098 | −17.063 | 0.577 | 0.092 | 0.083 | 0.125 ** | −0.092 | −0.019 | 0.017 | 0.058 | −0.014 | 1.000 | |||||

| 10. Target firm’s leverage ratio | 5.466 | 11.506 | 0.032 | 151.205 | 0.156 * | −0.070 | −0.079 | −0.114 * | 0.029 | 0.091 | −0.120 *** | −0.025 | −0.003 | 1.000 | ||||

| 11. Number of bidders | 1.067 | 0.281 | 1.000 | 3.000 | 0.087 | −0.073 | 0.043 | −0.054 | 0.007 | −0.149 ** | 0.026 | −0.118 * | 0.020 | 0.043 | 1.000 | |||

| 12. Cash payment | 71.105 | 41.641 | 0.000 | 100.000 | 0.215 * | 0.021 | −0.018 | 0.017 | −0.009 | 0.106 * | −0.187 *** | −0.031 | 0.134 *** | 0.040 | −0.072 | 1.000 | ||

| 13. Target firm’s nation | 0.968 | 0.176 | 0.000 | 1.000 | 0.072 | −0.036 | −0.061 | −0.016 | 0.198 ** | −0.047 | −0.182 ** | 0.099 | −0.051 | 0.108 | 0.044 | 0.060 | 1.000 | |

| 14. Industry relatedness | 0.313 | 0.687 | 0.000 | 1.000 | 0.039 | −0.071 | −0.002 | −0.036 | 0.132 * | −0.161 * | 0.021 | −0.088 | 0.081 | 0.019 | 0.071 | −0.083 | −0.074 | 1.000 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| Constant | −0.112 | −0.104 | −0.078 | −0.088 | −0.132 | −0.167 |

| (0.563) | (0.566) | (0.568) | (0.563) | (0.568) | (0.560) | |

| Acquirer size | −0.043 | −0.043 | −0.044 | −0.038 | −0.044 | −0.037 |

| (0.035) | (0.035) | (0.035) | (0.035) | (0.035) | (0.035) | |

| Target size | −0.027 | −0.026 | −0.028 | −0.031 | −0.026 | −0.040 |

| (0.037) | (0.037) | (0.037) | (0.037) | (0.037) | (0.036) | |

| Acquirer performance | 1.592 * | 1.589 * | 1.604 * | 1.519 * | 1.589 * | 1.474 * |

| (0.832) | (0.834) | (0.836) | (0.832) | (0.836) | (0.824) | |

| Target performance | 0.032 | 0.032 | 0.026 | 0.044 | 0.033 | 0.047 |

| (0.042) | (0.042) | (0.043) | (0.042) | (0.042) | (0.043) | |

| Target firm’s leverage ratio | 0.071 *** | 0.070 *** | 0.069 *** | 0.075 *** | 0.069 *** | 0.067 ** |

| (0.020) | (0.020) | (0.020) | (0.020) | (0.021) | (0.020) | |

| Number of bidders | 0.222 | 0.218 | 0.219 | 0.202 | 0.232 | 0.266 * |

| (0.163) | (0.164) | (0.164) | (0.164) | (0.166) | (0.164) | |

| Cash payment | 0.004 *** | 0.004 *** | 0.004 *** | 0.004 *** | 0.004 *** | 0.004 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | |

| Target firm’s Nation | −0.006 | −0.003 | −0.004 | −0.034 | 0.022 | 0.075 |

| (0.274) | (0.275) | (0.276) | (0.275) | (0.279) | (0.281) | |

| Industry relatedness | 0.055 | 0.056 | 0.060 | 0.069 | 0.054 | 0.060 |

| (0.100) | (0.100) | (0.101) | (0.100) | (0.101) | (0.275) | |

| Institutional distance | −0.151 ** | −0.151 ** | −0.145 ** | −0.146 ** | −0.152 ** | −0.139 * |

| (0.063) | (0.063) | (0.064) | (0.063) | (0.064) | (0.063) | |

| Cultural distance | −0.034 | −0.034 | −0.034 | −0.032 | −0.035 | −0.031 |

| (0.046) | (0.046) | (0.046) | (0.046) | (0.046) | (0.045) | |

| Number of fellow acquisitions | 0.027 | 0.026 | 0.025 | 0.025 | 0.026 | 0.022 |

| (0.041) | (0.042) | (0.041) | (0.041) | (0.041) | (0.040) | |

| Target firm’s CSR | 0.003 * | 0.001 * | 0.005 * | 0.002 * | 0.002 * | |

| (0.012) | (0.013) | (0.012) | (0.012) | (0.013) | ||

| Target firm’s CSR× Institutional distance | −0.012 | −0.023 ** | ||||

| (0.018) | (0.019) | |||||

| Target firms’ CSR× Cultural distance | −0.017 ** | −0.037 *** | ||||

| (0.010) | (0.013) | |||||

| Target firm’s CSR× Number of fellow acquisitions | −0.006 | −0.029 ** | ||||

| (0.009) | (0.012) | |||||

| Year | fixed | fixed | fixed | fixed | fixed | fixed |

| F-value | 2.57 | 2.64 | 2.67 | 2.72 | 2.69 | 2.74 |

| R2 | 0.287 | 0.295 | 0.295 | 0.297 | 0.296 | 0.317 |

| Adjusted R2 | 0.175 | 0.177 | 0.177 | 0.179 | 0.179 | 0.195 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| Constant | –0.112 | –0.121 | –0.112 | –0.070 | –0.118 | –0.062 |

| (0.563) | (0.566) | (0.569) | (0.564) | (0.567) | (0.566) | |

| Acquirer size | –0.043 | –0.043 | –0.044 | –0.046 | –0.043 | –0.043 |

| (0.035) | (0.035) | (0.035) | (0.035) | (0.036) | (0.035) | |

| Target size | –0.027 | –0.026 | –0.026 | –0.027 | –0.024 | –0.031 |

| (0.037) | (0.037) | (0.036) | (0.037) | (0.037) | (0.037) | |

| Acquirer performance | 1.592 * | 1.573 * | 1.572 * | 1.595 * | 1.575 * | 1.576 * |

| (0.832) | (0.838) | (0.840) | (0.835) | (0.840) | (0.835) | |

| Target performance | 0.032 | 0.038 | 0.032 | 0.042 | 0.033 | 0.047 |

| (0.042) | (0.042) | (0.042) | (0.042) | (0.040) | (0.043) | |

| Target firm’s leverage ratio | 0.071 *** | 0.071 *** | 0.073 *** | 0.078 *** | 0.072 ** | 0.079 ** |

| (0.020) | (0.027) | (0.021) | (0.021) | (0.020) | (0.021) | |

| Number of bidders | 0.222 | 0.222 | 0.224 | 0.177 | 0.220 | 0.189 * |

| (0.163) | (0.163) | (0.164) | (0.164) | (0.165) | (0.166) | |

| Cash payment | 0.004 *** | 0.004 *** | 0.005 *** | 0.004 *** | 0.003 *** | 0.005 *** |

| (0.001) | (0.001) | (0.003) | (0.001) | (0.001) | (0.001) | |

| Target firm’s Nation | –0.006 | –0.004 | –0.003 | –0.019 | –0.004 | –0.033 |

| (0.274) | (0.275) | (0.276) | (0.274) | (0.276) | (0.274) | |

| Industry relatedness | 0.055 | 0.057 | 0.054 | 0.074 | 0.056 | 0.076 |

| (0.100) | (0.100) | (0.101) | (0.101) | (0.101) | (0.101) | |

| Institutional distance | –0.151 ** | –0.150 ** | –0.153 ** | –0.147 ** | –0.150 ** | –0.156 ** |

| (0.063) | (0.063) | (0.064) | (0.063) | (0.064) | (0.064) | |

| Cultural distance | –0.034 | –0.033 | –0.033 | –0.024 | –0.029 | –0.026 |

| (0.046) | (0.046) | (0.042) | (0.046) | (0.047) | (0.046) | |

| Number of fellow acquisitions | 0.027 | 0.027 | 0.024 | 0.026 | 0.029 | 0.020 |

| (0.041) | (0.041) | (0.043) | (0.041) | (0.041) | (0.041) | |

| Target firm’s CSR | 0.030 * | 0.022 * | 0.035 ** | 0.029 * | 0.039 * | |

| (0.131) | (0.138) | (0.132) | (0.131) | (0.140) | ||

| Target firm’s CSR× Institutional distance | –0.038 * | –0.066 * | ||||

| (0.197) | (0.217) | |||||

| Target firms’ CSR× Cultural distance | –0.161 * | –0.280 ** | ||||

| (0.095) | (0.128) | |||||

| Target firm’s CSR× Number of fellow acquisitions | –0.010 | −0.196 * | ||||

| (0.098) | (0.140) | |||||

| Year | fixed | fixed | fixed | fixed | fixed | fixed |

| F-value | 2.57 | 2.60 | 2.63 | 2.64 | 2.62 | 2.74 |

| R2 | 0.287 | 0.292 | 0.295 | 0.296 | 0.294 | 0.303 |

| Adjusted R2 | 0.175 | 0.177 | 0.178 | 0.179 | 0.177 | 0.185 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qiao, L.; Wu, J. Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability 2019, 11, 1291. https://doi.org/10.3390/su11051291

Qiao L, Wu J. Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability. 2019; 11(5):1291. https://doi.org/10.3390/su11051291

Chicago/Turabian StyleQiao, Lu, and Jianfeng Wu. 2019. "Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums" Sustainability 11, no. 5: 1291. https://doi.org/10.3390/su11051291

APA StyleQiao, L., & Wu, J. (2019). Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability, 11(5), 1291. https://doi.org/10.3390/su11051291