Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach

,

,  , and

, and

Abstract

1. Introduction

- Provide a statistical data integration of previous research on the relationship between CSRD and organizational performance;

- Examine different variables that can moderate this relationship: organizational performance, type of disclosure, activity sector, region, type of organization, and measures of organization size.

2. Literature Review and Hypotheses

2.1. Debate about Relationship between Corporate Social Responsibility Disclosure (CSRD) and Performance

- Has evidence of any relationship between CSRD and performance been found?

- What sign does the link present: positive or negative?

2.2. Positive, Negative, and No Relationships between Variables Under Study

2.2.1. Positive Relationship

2.2.2. Negative Relationship

2.2.3. No Relationship

2.3. Moderators of Relationship between CSRD and Performance

3. Methods and Data

3.1. Study Selection Criteria and Literature Search

3.2. Data Extraction Process

3.3. Statistical Analysis

- Estimates with and without large samples to verify the impact of large samples on research results

- Subgroup analyses of the following moderating variables: performance dimensions, CSRD dimensions, sector of activity, region, type of organization, and measures of organization size.

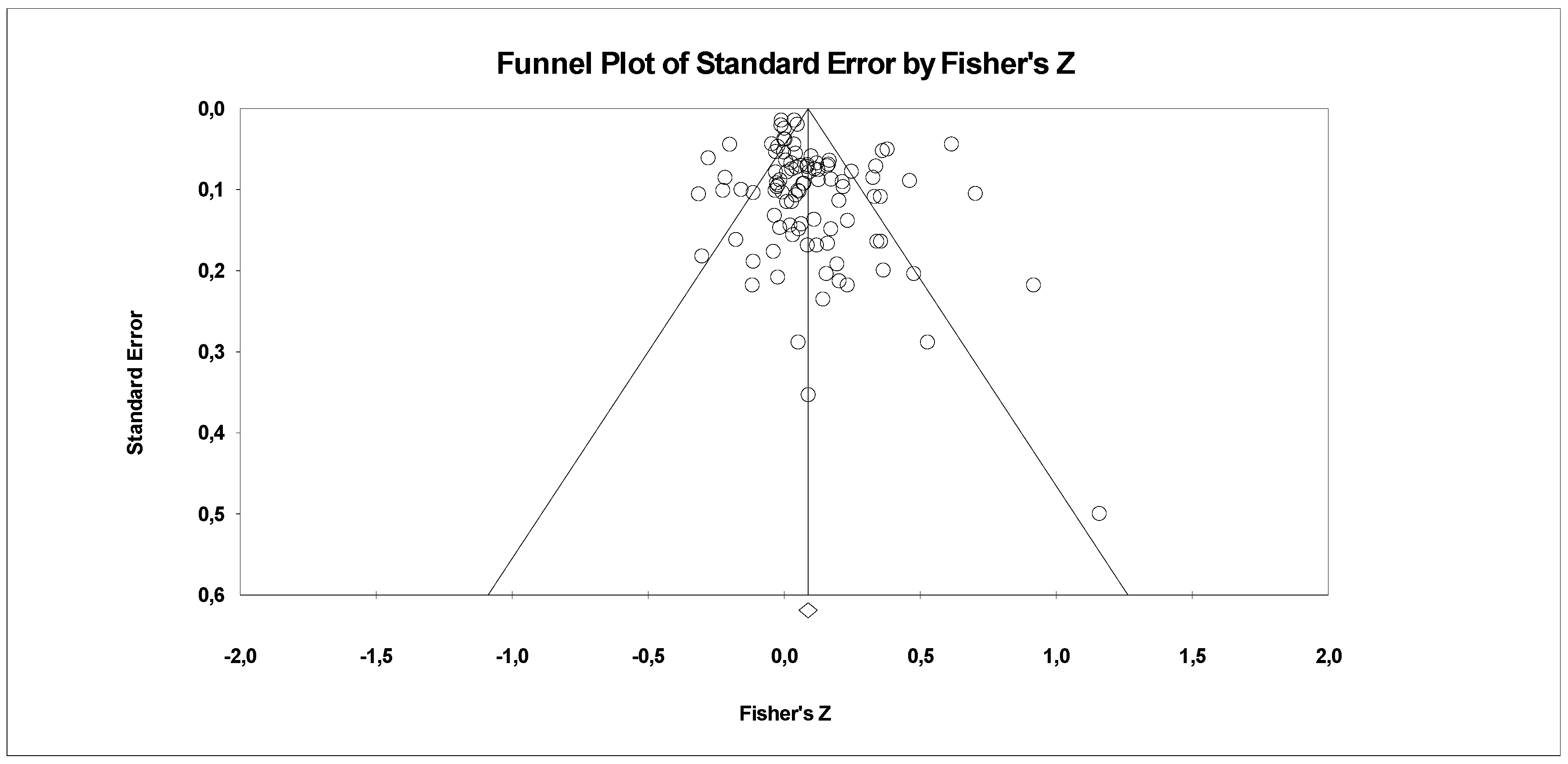

4. Results

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

Appendix A: Final List of Documents Used in Meta-analysis (Alphabetical Order)

References

- Chiu, T.K.; Wang, Y.H. Determinants of social disclosure quality in Taiwan: An application of stakeholder theory. J. Bus. Ethics 2015, 129, 379–398. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M.; Magnan, M. Corporate environmental disclosure: Contrasting management’s perceptions with reality. J. Bus. Ethics 2004, 49, 143–165. [Google Scholar] [CrossRef]

- Dong, S.; Burritt, R.; Qian, W. Salient stakeholders in corporate social responsibility reporting by Chinese mining and minerals companies. J. Clean. Prod. 2014, 84, 59–69. [Google Scholar] [CrossRef]

- Huang, C.L.; Kung, F.H. Drivers of environmental disclosure and stakeholder expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I. Stakeholders’ power, corporate characteristics, and social and environmental disclosure: Evidence from China. J. Clean. Prod. 2014, 64, 426–436. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Unerman, J.; Hession, E. User needs in sustainability reporting: Perspectives of stakeholders in Ireland. Eur. Account. Rev. 2005, 14, 759–787. [Google Scholar] [CrossRef]

- Rodrigue, M. Contrasting realities: Corporate environmental disclosure and stakeholder-released information. Account. Audit. Account. J. 2014, 27, 119–149. [Google Scholar] [CrossRef]

- Thijssens, T.; Bollen, L.; Hassink, H. Secondary stakeholder influence on CSR disclosure: An application of stakeholder salience theory. J. Bus. Ethics 2015, 132, 873–891. [Google Scholar] [CrossRef]

- Deegan, C.; Rankin, M.; Tobin, J. An examination of the corporate social and environmental disclosures of BHP from 1983–1997: A test of legitimacy theor. Account. Audit. Account. J. 2002, 15, 312–343. [Google Scholar] [CrossRef]

- Hahn, R.; Lülfs, R. Legitimizing negative aspects in GRI-oriented sustainability reporting: A qualitative analysis of corporate disclosure strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar] [CrossRef]

- Lai, A.; Melloni, G.; Stacchezzini, R. Corporate sustainable development: Is ‘integrated reporting’a legitimation strategy? Bus. Strat. Environ. 2016, 25, 165–177. [Google Scholar] [CrossRef]

- Hummel, K.; Schlick, C. The relationship between sustainability performance and sustainability disclosure–Reconciling voluntary disclosure theory and legitimacy theory. J. Account. Public Policy 2016, 35, 455–476. [Google Scholar] [CrossRef]

- Chauvey, J.N.; Giordano-Spring, S.; Cho, C.H.; Patten, D.M. The normativity and legitimacy of CSR disclosure: Evidence from France. J. Bus. Ethics 2015, 130, 789–803. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Bebbington, J.; Larrinaga, C.; Moneva, J.M. Corporate social reporting and reputation risk management. Account. Audit. Account. J. 2008, 21, 337–361. [Google Scholar] [CrossRef]

- Cho, C.H.; Guidry, R.P.; Hageman, A.M.; Patten, D.M. Do actions speak louder than words? An empirical investigation of corporate environmental reputation. Account. Organ. Soc. 2012, 37, 14–25. [Google Scholar] [CrossRef]

- Koch, C.; Schmidt, C. Disclosing conflicts of interest–Do experience and reputation matter? Account. Organ. Soc. 2010, 35, 95–107. [Google Scholar] [CrossRef]

- Michelon, G. Sustainability Disclosure and Reputation: A Comparative Study. Corp. Reput. Rev. 2011, 14, 79–96. [Google Scholar] [CrossRef]

- Odriozola, M.D.; Baraibar-Diez, E. Is corporate reputation associated with quality of CSR reporting? Evidence from Spain. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 121–132. [Google Scholar] [CrossRef]

- Cahan, S.F.; De Villiers, C.; Jeter, D.C.; Naiker, V.; Van Staden, C.J. Are CSR disclosures value relevant? Cross-country evidence. Eur. Account. Rev. 2016, 25, 579–611. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I.; Ortas, E. Corporate environmental sustainability reporting in the context of national cultures: A quantile regression approach. I. Bus. Rev. 2017, 26, 337–353. [Google Scholar] [CrossRef]

- Garcia-Sanchez, I.M.; Cuadrado-Ballesteros, B.; Frías-Aceituno, J.V. Impact of the institutional macro context on the voluntary disclosure of CSR information. Long Range Plan. 2016, 49, 15–35. [Google Scholar] [CrossRef]

- Llena, F.; Moneva, J.M.; Hernández, B. Environmental disclosures and compulsory accounting standards: The case of Spanish annual reports. Bus. Strat. Environ. J. 2007, 16, 50–63. [Google Scholar] [CrossRef]

- Luo, X.R.; Wang, D.; Zhang, J. Whose call to answer: Institutional complexity and firms’ CSR reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Tinker, T.; Neimark, M.; Lehman, C. Falling down the hole in the middle of the road: Political quietism in corporate social reporting. Account. Audit. Account. J. 1991, 4. [Google Scholar] [CrossRef]

- Luque-Vílchez, M.; Mesa-Pérez, E.; Husillos, J.; Larrinaga, C. The influence of pro-environmental managers’ personal values on environmental disclosure: The mediating role of the environmental organizational structure. Sustain. Account. Manag. Policy J. 2019, in press. [Google Scholar] [CrossRef]

- Fassin, Y. The reasons behind non-ethical behaviour in business and entrepreneurship. J. Bus. Ethics 2005, 60, 265–279. [Google Scholar] [CrossRef]

- Moneva, J.M.; Llena, F. Análisis de la Información Sobre Responsabilidad Social en las Empresas Industriales Que Cotizan en Bolsa. R. Esp. Financ. Contab. 1996, 25, 361–402. [Google Scholar]

- Gray, R.H.; Owen, D.L.; Maunders, K.T. Corporate Social Reporting: Accounting and Accountability; Prentice Hall International: Hemel Hempstead, UK, 1987; ISBN 9780131754645. [Google Scholar]

- Van Riel, C.B. Corporate Communication Orchestrated by a Sustainable Corporate Story. In The Expressive Organization; Schultz, M., Hatch, M.J., Larsen, M.H., Eds.; Oxford University Press: Oxford, UK, 2000; pp. 157–181. ISBN 978-0198297796. [Google Scholar]

- Cormier, D.; Magnan, M. The Revisited Contribution of Environmental Reporting to Investors’ Valuation of a Firm’s Earnings: An International Perspective. Ecol. Econ. 2007, 62, 613–626. [Google Scholar] [CrossRef]

- Dawkins, C.E.; Fraas, J.W. Coming Clean: The Impact of Environmental Performance and Visibility on Corporate Climate Change Disclosure. J. Bus. Ethics 2011, 100, 303–322. [Google Scholar] [CrossRef]

- Drobetz, W.; Merikas, A.; Merika, A.; Tsionas, M.G. Corporate Social Responsibility Disclosure: The Case of International Shipping. Transp. Res. Part. E. 2014, 71, 18–44. [Google Scholar] [CrossRef]

- Alexopoulos, I.; Kounetas, K.; Tzelepis, K. Environmental and financial performance. Is there a win or a win-loss situation? Evidence from the Greek manufacturing. J. Clean. Prod. 2018, 197, 1275–1283. [Google Scholar] [CrossRef]

- Wittmann, C.M.; Hunt, S.D.; Arnett, D.B. Explaining Alliance Success: Competences, Resources, Relational Factors, and Resource-advantage Theory. Ind. Mark. Manag. 2009, 38, 743–756. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. A Survey of Corporate Governance. J. Financ. 1997, 52, 737–783. [Google Scholar] [CrossRef]

- Gompers, P.A.; Ishii, J.L.; Metrick, A. Corporate Governance and Equity Prices. Quart. J. Econ. 2003, 118, 107–155. [Google Scholar] [CrossRef]

- Giroud, X.; Mueller, H.M. Corporate Governance, Product Market Competition, and Equity Prices. J. Financ. 2011, LXVI(2), 563–600. [Google Scholar] [CrossRef]

- Asensio-López, D.; Cabeza-García, L.; González-Álvarez, N. Corporate governance and innovation: A theoretical review. Eur. J. Manag. Bus. Econ. 2018. [Google Scholar] [CrossRef]

- Miroshnychenko, I.; Barontini, R.; Testa, F. Corporate governance and environmental performance: A systematic overview. In Ethics, ESG, and Sustainable Prosperity; World Scientific Publishing: Singapore, 2018. [Google Scholar]

- Bansal, S.; López-Pérez, M.V.; Rodríguez-Ariza, L. Board Independence and Corporate Social Responsibility Disclosure: The Mediating Role of Presence of Family Ownership. Adm. Sci. 2018, 8, 33. [Google Scholar] [CrossRef]

- Ong, T.; Djajadikerta, H.G. Corporate governance and sustainability reporting in the Australian resources industry: An empirical analysis. Soc. Responsib. J. 2018. [Google Scholar] [CrossRef]

- Giannarakis, G.; Konteos, G.; Sariannidis, N.; Chaitidis, G. The relation between voluntary carbon disclosure and environmental performance: The case of S&P 500. Int J. Law Manag. 2017, 59, 784–803. [Google Scholar] [CrossRef]

- Ortas, E.; Álvarez, I.; Zubeltzu, E. Firms’ Board Independence and Corporate Social Performance: A Meta-Analysis. Sustainability 2017, 9, 1006. [Google Scholar] [CrossRef]

- Azutoru, I.H.C.; Obinne, U.G.; Chinelo, O.O. Effect of Corporate Governance Mechanisms on Financial Performance of Insurance Companies in Nigeria. J. Finan. Account. 2017, 5, 93–103. [Google Scholar] [CrossRef]

- Albitar, K. Firm characteristics, governance attributes and corporate voluntary disclosure: A study of Jordanian listed companies. Int. Bus. Res. 2015, 8, 1. [Google Scholar] [CrossRef]

- Giannarakis, G. Corporate governance and financial characteristic effects on the extent of corporate social responsibility disclosure. Soc. Responsib. J. 2014, 10, 569–590. [Google Scholar] [CrossRef]

- Kamal, M.; Saadi, S. Corporate Governance, Economic Turbulence and Financial Performance of UAE Listed Firms. Stud. Econ. Financ. 2013, 30, 118–138. [Google Scholar] [CrossRef]

- Arayssi, M.; Dah, M.; Jizi, M. Women on boards, sustainability reporting and firm performance. Sustain. Account. Manag. Policy J. 2016, 7, 376–401. [Google Scholar] [CrossRef]

- Saidat, Z.; Silva, M.; Seaman, C. The relationship between corporate governance and financial performance: Evidence from Jordanian family and nonfamily firms. J. Fam. Bus. Manag. 2018. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Allouche, J.; Laroche, P. A Meta-analytical Investigation of the Relationship Between Corporate Social and Financial Performance. Rev. Gest. Resourc. Hum. Eska. 2005, 18, 1–29. [Google Scholar]

- Wu, M.L. Corporate Social Performance, Corporate Financial Performance and Firm Size. J. American Acad. Bus. 2006, 8, 163–171. [Google Scholar]

- Miras-Rodríguez, M.M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Responsabilidad Social Corporativa y Rendimiento Financiero: Un Meta-análisis. R. Esp. Financ. Contab. 2014, 43, 193–215. [Google Scholar] [CrossRef]

- Dang, C.; Li, Z.; Yang, C. Measuring Firm Size in Empirical Corporate Finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Patten, D.M. The Relation Between Environmental Performance and Environmental Disclosure: A Research Note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E. The Relations Among Environmental Disclosures, Environmental Performance, and Economic Performance: A Simultaneous Equations Approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Amran, A. Corporate Social Reporting in Malaysia: An Institutional Perspective. Unpublished doctoral thesis, University of Malaya, Kuala Lumpur, Malaysia, 2006. [Google Scholar]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The Determinants of Corporate Sustainability Performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The Impact of Culture and Governance on Corporate Social Reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the Relation Between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Fang, X.; Li, Y.; Richardson, G. The Relevance of Environmental Disclosures: Are Such Disclosures Incrementally Informative? J. Account. Public Policy 2013, 32, 410–431. [Google Scholar] [CrossRef]

- Buhr, N. Histories of and Rationales for Sustainability Reporting. In Sustainability Accounting and Accountability; Unerman, J., Bebbington, J., O’Dwyer, B., Eds.; Routledge: London, UK, 2007; ISBN 0415384885. [Google Scholar]

- Cormier, D.; Gordon, I.M. An Examination of Social and Environmental Reporting Strategies. Account. Audit. Account. J. 2001, 14, 587–616. [Google Scholar] [CrossRef]

- Ieng, C.; Chatterjee, B.; Brown, A. The Current Status of Greenhouse Gas Reporting by Chinese Companies. A Test of Legitimacy Theory. Manag. Audit. J. 2013, 28, 114–139. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The Role of Environmental Disclosures as Tools of Legitimacy: A Research Note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Hughes, S.B.; Anderson, A.; Golden, S. Corporate Environmental Disclosures: Are They Useful in Determining Environmental Performance? J. Account. Public Pol. 2001, 20, 217–240. [Google Scholar] [CrossRef]

- Mallin, C.; Farag, H.; Ow-Yong, K. Corporate Social Responsibility and Financial Performance in Islamic Banks. J. Econ. Behav. Organ. 2014, 103, S21–S38. [Google Scholar] [CrossRef]

- Leuz, C. Proprietary Versus Non-proprietary Disclosures: Voluntary Cash Flow Statements and Business Segment Reports in Germany; Working Paper; Department of Business and Economics, Johann Wolfgang Goethe-Universitat: Frankfurt, Germany, 1999. [Google Scholar]

- Stocken, P.C. Credibility of Voluntary Disclosure. Rand J. Econ. 2000, 31, 359–374. [Google Scholar] [CrossRef]

- Skinner, D.J. Earnings Disclosures and Stockholder Lawsuits. J. Account. Econ. 1997, 23, 249–282. [Google Scholar] [CrossRef]

- Freedman, M.; Jaggi, B. An Analysis of the Association Between Pollution Disclosure and Economic Performance. Account. Audit. Account. J. 1988, 1, 43–45. [Google Scholar] [CrossRef]

- Aupperle, K.; Carroll, A.; Hatfield, J. An Empirical Examination of the Relationship Between Corporate Social Responsibility and Profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Dumontier, P.; Raffournier, B. Why Firms Comply Voluntarily with IAS: An Empirical Analysis with Swiss Data. J. Int. Financ. Manag. Account. 1998, 9, 216–245. [Google Scholar] [CrossRef]

- Meek, G.K.; Roberts, C.B.; Gray, S.J. Factors Influencing Voluntary Annual Report Disclosures by US, UK and Continental European Multinational Corporations. J. Int. Bus. Stud. 1995, 26, 555–572. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate Social Responsibility and Financial Performance: Correlation or Misspecification? Strat. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Ball, R.; Robin, A.; Wu, J.S. Incentives Versus Standards: Properties of Accounting Income in Four East Asian Countries. J. Account. Econ. 2003, 36, 235–270. [Google Scholar] [CrossRef]

- Connelly, J.T.; Limpaphayom, P. Environmental Reporting and Firm Performance: Evidence from Thailand. J. Corp. Citizensh. 2004, 13, 137–149. [Google Scholar] [CrossRef]

- Forte, L.M.; Neto, J.B.; Nobre, F.C.; Nobre, L.H.; Queiroz, D.B. Determinants of Voluntary Disclosure: A Study in the Brazilian Baking Sector. Rev. Gest. Financ. Contab. 2015, 5, 23–37. [Google Scholar] [CrossRef]

- Pajuelo, M.L. Assessment of the Impact of Business Activity in Sustainability Terms. Empirical Confirmation of Its Determination in Spanish Companies. Sustain. 2013, 5, 2389–2420. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm Performance: The Interactions of Corporate Social Performance With the Innovation and Industry Differentiation. Strat. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Surroca, J.; Tribo, J.; Waddock, S. Corporate Responsibility and Financial Performance: The Role of Intangible Resources. Strat. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Van der Laan, G.; Van Ees, H.; Van, A. Corporate Social and Financial Performance: An Extended Stakeholder Theory, and Empirical Test With Accounting Measures. J. Bus. Ethics 2008, 79, 299–310. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. Culture, Corporate Governance and Disclosure in Malaysian Corporations. Abacus 2002, 38, 317–349. [Google Scholar] [CrossRef]

- AbdRahman, N.H.W.; Zain, M.M.; YaakopYahaya Al-Haj, N.H. CSR Disclosure and Its Determinants: Evidence from Malaysian Government Link Companies. Soc. Responsib. J. 2011, 7, 181–201. [Google Scholar] [CrossRef]

- Ho, S.S.M.; Wong, K.S. A Study of the Relationship Between Corporate Governance Structures and the Extent of Voluntary Disclosure. J. Int. Account. Audit. Tax. 2001, 10, 139–156. [Google Scholar] [CrossRef]

- Hamrouni, A.; Miloudi, A.; Benkraiem, R. Signaling Firm Performance Through Corporate Voluntary Disclosure. J. Appl. Bus. Res. 2015, 31, 609–620. [Google Scholar] [CrossRef]

- Francis, J.; Nanda, D.; Olsson, P. Voluntary Disclosure, Earnings Quality, and Cost of Capital. J. Account. Res. 2008, 46, 53–99. [Google Scholar] [CrossRef]

- Dragomir, V.D. Environmentally Sensitive Disclosures and Financial Performance in a European Setting. J. Account. Organ. Change. 2010, 6, 359–388. [Google Scholar] [CrossRef]

- Gao, L.S.; Connors, E. Corporate Environmental Performance, Disclosure and Leverage: An Integrated Approach. Accounting and Finance Faculty Publications Series Paper 6; Scholar Works: Boston, MA, USA, 2011. [Google Scholar]

- Cochran, P.L.; Wood, R.A. Corporate Social Responsibility and Financial Performance. Acad. Manag. J. 1984, 27, 42–56. [Google Scholar] [CrossRef]

- Freedman, M.; Jaggi, B. Pollution Disclosures, Pollution Performance and Economic Performance. OMEGA, Int. J. Manag. Sci. 1982, 10, 167–176. [Google Scholar] [CrossRef]

- Hasseldine, J.; Salama, A.I.; Toms, J.S. Quantity Versus Quality: The Impact of Environmental Disclosures on the Reputations of UK PLCs. Brit. Account. Rev. 2005, 37, 231–248. [Google Scholar] [CrossRef]

- Guidry, R.P.; Patten, D.M. Voluntary Disclosure Theory and Financial Control Variables: An Assessment of Recent Environmental Disclosure Research. Account. Forum 2012, 36, 81–90. [Google Scholar] [CrossRef]

- Dawkins, C.E.; Fraas, J.W. Erratum to Beyond Acclamations and Excuses: Environmental Performance, Voluntary Environmental Disclosure and the Role of Visibility. J. Bus. Ethics 99, 383–397. [CrossRef]

- Delmas, M.; Blass, V.D. Measuring Corporate Environmental Performance: The Trade-Offs of Sustainability Ratings. Bus. Strat. Environ. 2010, 19, 245–260. [Google Scholar] [CrossRef]

- Salem, N.; Kavanagh, M.; Slaughter, G. An Empirical Study of the Relationship Between Corporate Social Responsibility Disclosure and Organizational Performance: Evidence from Libya. Int. J. Manag. Mark. Res. 2012, 5, 69–82. [Google Scholar]

- Contrafatto, M. The Institutionalization of Social and Environmental Reporting: An Italian Narrative. Account. Organ. Soc. 2014, 39, 414–432. [Google Scholar] [CrossRef]

- Adams, C. Internal Organizational Factors Influencing Corporate Social and Ethical Reporting: Beyond Current Theorizing. Account. Audit. Account. J. 2002, 15, 223–250. [Google Scholar] [CrossRef]

- Contrafatto, M. Il Social Environmental Reporting eleSue Motivazioni: Teoria, AnalisiEmpirica e Prospecttive; Guiffré: Milan, Italy, 2009; ISBN 978-8814144769. [Google Scholar]

- Adams, C.; McNicholas, P. Making a Difference: Sustainability Reporting, Accountability and Organizational Change. Account. Audit. Account. J. 2007, 20, 382–402. [Google Scholar] [CrossRef]

- Line, M.; Hawley, H.; Krut, R. The Development of Global Environmental and Social Reporting. Corp. Environ. Strat. 2002, 9, 69–78. [Google Scholar] [CrossRef]

- Gray, R.; Javad, M.; Porter, D.M.; Sinclair, C.D. Social and Environmental Disclosure and Corporate Characteristics: A Research Note and Extension. J. Bus. Fin. Account. 2001, 28, 327–356. [Google Scholar] [CrossRef]

- Hossain, M.; Hammami, H. Voluntary Disclosure in the Annual Reports of an Emerging Country: The Case of Qatar. Adv. Account. 2009, 25, 255–265. [Google Scholar] [CrossRef]

- James-Overheu, C.; Cotter, J. Corporate Governance, Sustainability and the Assessment of Default Risk. Asian J. Financ. Account. 2010, 1, 34–53. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of Corporate Social Responsibility Disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Ionel-Alin, I. Analyze of Environmental Disclosure Within European Union Countries. J. Knowl. Manag. Econ. Inf. Technol. 2012, 4, 1–23. [Google Scholar]

- Campbell, D. Intra and Intersectoral Effects in Environmental Disclosures: Evidence for Legitimacy Theory? Bus. Strat. Environ. J. 2003, 42, 207–252. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A Study of Environmental Disclosure Practices of Australian Corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Commitment to Corporate Social Responsibility Measured Through Global Reporting Initiative Reporting: Factors Affecting the Behaviour of Companies. J. Clean. Prod. 2014, 81, 244–254. [Google Scholar] [CrossRef]

- Patten, D.M. Exposure, Legitimacy and Social Disclosure. J. Account. Public Policy 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Roberts, R.W. Determinants of Corporate Social Disclosure: An Application of Stakeholder Theory. Account. Organ. Soc. 1992, 17, 595–612. [Google Scholar] [CrossRef]

- Luethge, D.; Guohong Han, H. Assessing Corporate Social and Financial Performance in China. Soc. Responsib. J. 2012, 8, 389–403. [Google Scholar] [CrossRef]

- Magness, V. Strategic Posture, Financial Performance and Environmental Disclosure. An Empirical Test of Legitimacy Theory. Account. Audit. Account. 2006, 19, 540–563. [Google Scholar] [CrossRef]

- Menassa, E. Corporate Social Responsibility. An Exploratory Study of the Quality and Extent of Social Disclosures by Lebanese Commercial Banks. J. Appl. Account. Res. 2010, 11, 4–23. [Google Scholar] [CrossRef]

- Miras-Rodríguez, M.M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Are Socially Responsible Behaviors Paid Off Equally? A Cross-cultural Analysis. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 237–256. [Google Scholar] [CrossRef]

- Fernández, J.L.; Luna, L. The Creation of Value Through Corporate Reputation. J. Bus. Ethics 2007, 76, 335–346. [Google Scholar] [CrossRef]

- Singh, J.; de los Salmones Sanchez, M.M.G.; Del Bosque, I.R. Understanding Corporate Social Responsibility and Product Perceptions in Consumer Markets: A Cross-cultural Evaluation. J. Bus. Ethics 2008, 80, 597–611. [Google Scholar] [CrossRef]

- Svensson, G.; Wood, G.; Singh, J.; Carasco, E.; Callaghan, M. Ethical Structures and Processes of Corporations Operating in Australia, Canada, and Sweden: A Longitudinal and Cross-cultural Study. J. Bus. Ethics 2009, 86, 485–506. [Google Scholar] [CrossRef]

- Kolk, A. Sustainability, Accountability andCorporate Governance: Exploring Multinationals’ Reporting Practices. Bus. Strat. Environ. J. 2008, 17, 1–15. [Google Scholar] [CrossRef]

- Hartman, L.; Rubin, R.; Dhanda, K. Communications and Corporate Social Responsibility: United States and European Union Multinational Corporations. J. Bus. Ethics 2007, 74, 373–389. [Google Scholar] [CrossRef]

- Van der Laan Smith, J.; Adhikari, A.; Tondkar, R.H. Exploring Differences in Social Disclosures Internationally: A Stakeholder Perspective. J. Account. Public Policy 2005, 24, 123–151. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the Adoption of Sustainability Assurance Statements: An International Investigation. Bus. Strat. Environ. J. 2010, 19, 182–198. [Google Scholar] [CrossRef]

- Adelopo, I. Voluntary Disclosure Practices Amongst Listed Companies in Nigeria. Adv. Account. 2011, 27, 338–345. [Google Scholar] [CrossRef]

- Siregar, S.V.; Bachtiar, Y. Corporate Social Reporting: Empirical Evidence From Indonesia Stock Exchange. Int. J. Islamic Middle East. Financ. Manag. 2010, 3, 241–252. [Google Scholar] [CrossRef]

- Hope, O.K. Firm-level disclosures and the relative roles of culture and legal origin. J. Int. Financ. Manag. Account. 2003, 14, 218–248. [Google Scholar] [CrossRef]

- Vurro, C.; Perrini, F. Making the Most of Corporate Social Responsibility Reporting: Disclosure Structure and Its Impact on Performance. Corp. Gov. 2011, 11, 459–474. [Google Scholar] [CrossRef]

- Al-Ajmi, M.; Al-Mutairi, A.; Al-Duwaila, N. Corporate Social Disclosure Practices in Kuwait. Int. J. Econ. Financ. 2015, 7, 244–254. [Google Scholar] [CrossRef]

- Bens, D.A.; Monahan, S.J. Disclosure Quality and the Excess Value of Diversification. J. Account. Res. 2004, 42, 691–730. [Google Scholar] [CrossRef]

- Chan, M.C.; Watson, J.; Woodliff, D. Corporate Governance Quality and CSR Disclosures. J. Bus. Ethics 2014, 125, 59–73. [Google Scholar] [CrossRef]

- Castelo Branco, M.; Lima Rodriguez, L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Cho, C.H.; Freedman, M.; Patten, D.M. Corporate Disclosure of Environmental Capital Expenditures. A Test of Alternative Theories. Account. Audit. Account. J. 2012, 25, 486–507. [Google Scholar] [CrossRef]

- Sánchez-Meca, J. Meta-análisis Para la Investigación Científica. In Metodología Para la Investigación en Marketing y Dirección de Empresas; Sarabia-Sánchez, F.J., Ed.; Pirámide: Madrid, Spain, 1999; pp. 173–201. ISBN 9788436813425. [Google Scholar]

- Eisend, M. Morality effects and consumer responses to counterfeit and pirated products: A meta-analysis. J. Bus. Ethics 2019, 154, 301–323. [Google Scholar] [CrossRef]

- Ismagilova, E.; Slade, E.; Rana, N.P.; Dwivedi, Y.K. The effect of characteristics of source credibility on consumer behaviour: A meta-analysis. J. Retail. Consum. Serv 2019, in press. [Google Scholar] [CrossRef]

- Zhang, Y.; Weng, Q.; Zhu, N. The relationships between electronic banking adoption and its antecedents: A meta-analytic study of the role of national culture. Int. J. Inf. Manag. 2018, 40, 76–87. [Google Scholar] [CrossRef]

- Guerrero-Villegas, J.; Pérez-Calero, L.; Hurtado-González, J.; Giráldez-Puig, P. Board Attributes and Corporate Social Responsibility Disclosure: A Meta-Analysis. Sustainability 2018, 10, 4808. [Google Scholar] [CrossRef]

- Hamari, J.; Keronen, L. Why do people play games? A meta-analysis. Int. J. Inf. Manag. 2017, 37, 125–141. [Google Scholar] [CrossRef]

- Geyskens, I.; Krishnan, R.; Steenkamp, J.B.E.; Cunha, P.V. A Review and Evaluation of Meta-analysis Practices in Management Research. J. Manag. 2009, 35, 393–419. [Google Scholar] [CrossRef]

- Hunter, J.E.; Schmidt, F.L. Meta-analysis: Correcting Error and Bias in Research Findings, 2nd ed.; Sage: Thousand Oaks, CA, USA, 2004; ISBN 1452286892. [Google Scholar]

- Hawcroft, J.L.; Milfont, L.T. The Use (and Abuse) of the New Environmental Paradigm Scale Over the Last 30 Years: A Meta-analysis. J. Environ. Psychol. 2010, 30, 143–158. [Google Scholar] [CrossRef]

- Marcus, B.; Taylor, O.A.; Hastings, S.E.; Sturm, A.; Weigelt, O. The Structure of Counterproductive Work Behavior. A Review, a Structural Meta-analysis, and a Primary Study. J. Manag. 2013, 42, 203–233. [Google Scholar] [CrossRef]

- Sánchez-Meca, J. Meta-análisis de la Investigación. In Metodología en la Investigación Sobre Discapacidad. Introducción al Uso de las Ecuaciones Estructurales; Verdugo Manuela Crespo, M.Á., Badía, M., Arias, B., Eds.; VI Seminario Científico SAID, Publicaciones del INICO, Colección Actas: Salamanca, Spain, 2008; pp. 121–140. [Google Scholar]

- Sánchez-Meca, J.; Marín-Martínez, F.; López-López, J.A. Metodología del Meta-análisis. In Métodos de Investigación Social y de la Empresa; Sarabia Sánchez, F., Ed.; Pirámide: Madrid, Spain, 2013; pp. 447–470. [Google Scholar]

- Wallace, J.C.; Edwards, B.D.; Paul, J.; Burke, M.; Christian, M.S.; Eissa, G. Change the Referent? A Meta-analytic Investigation of Direct and Referent-shift Consensus Models for Organizational Climate. J. Manag. 2016, 42, 838–861. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G. The PRISMA Group. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef]

- David, R.J.; Han, S.K. A Systematic Assessment of the Empirical Support for Transaction Cost Economics. Strat. Manag. J. 2004, 25, 39–58. [Google Scholar] [CrossRef]

- Newbert, S.L. Empirical Research on the Resource-based View of the Firm: An Assessment and Suggestions for Future Research. Strat. Manag. J. 2007, 28, 121–146. [Google Scholar] [CrossRef]

- Palmatier, R.W.; Dant, R.; Grewal, D.; Evans, K. Factors Influencing the Effectiveness of Relationship Marketing: A Meta-analysis. J. Mark. 2006, 70, 136–153. [Google Scholar] [CrossRef]

- Hunter, J.E.; Schmidt, F.L. Methods of Meta-analysis: Correcting Error and Bias in Research Findings; Sage: Newbury Park, CA, USA, 1990; ISBN 141290479X. [Google Scholar]

- Barroso-Mendez, M.J.; Galera-Casquet, C.; Valero-Amaro, V. Proposal of a Social Alliance Success Model from a Relationship Marketing Perspective: A Meta-analytical Study of the Theoretical Foundations. Bus. Res. Quart. 2015, 18, 188–203. [Google Scholar] [CrossRef]

- Peterson, R.A.; Brown, S.P. On the Use of Beta Coefficients in Meta-analysis. J. Appl. Psychol. 2005, 90, 175–181. [Google Scholar] [CrossRef]

- Rothstein, H.R.; Sutton, A.J.; Borenstein, M. (Eds.) Publication Bias in Meta-analysis: Prevention, Assessment, and Adjustments; Wiley: Chichester, UK, 2005; ISBN 978-0470870143. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Erlbaum: Hillsdale, NJ, USA, 1988; ISBN 9780805802832. [Google Scholar]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good? A Meta-analysis and Redirection of Research on the Relationship Between Corporate Social and Financial Performance; Working Paper; Ross School of Business, University of Michigan: Ann Arbor, MI, USA, 2007. [Google Scholar]

- Waldman, D.A.; de Luque, M.S.; Washburn, N.; House, R.J. Cultural and Leadership Predictors of Corporate Social Responsibility Values of Top Management: A GLOBE Study of 15 Countries. J. Int. Bus. Stud. 2006, 37, 823–837. [Google Scholar] [CrossRef]

- Rosenthal, R.; Di Matteo, M.R. Meta-analysis: Recent Developments in Quantitative Methods for Literature Reviews. Annu. Rev. Psychol. 2001, 52, 59–82. [Google Scholar] [CrossRef] [PubMed]

- Li, F. Endogeneity in CEO Power: A Survey and Experiment. Invest. Anal. J. 2016, 45, 149–162. [Google Scholar] [CrossRef]

{kind=link}

| Filter Type 1 | Description | ABI/Inform Result | EconLit Result | Total |

|---|---|---|---|---|

| Substantive | All works selected for keywords related to our key variables | 1659 | 261 | 1920 |

| Methodological | At least 1 of 7 keywords required to indicate empirical data or analysis | 1313 | 194 | 1507 |

| Substantive and methodological | Remaining abstracts read for both substantive relevance and statistical analysis | 405 | 53 | 458 |

| Substantive and methodological | Remaining full works read for both substantive relevance and statistical analysis | 86 | 24 | 110 |

| Duplicated | Duplicate works found in both databases deleted | 95 |

| Authors | Year | Journal | Correlation | Sample | Sector of Activity |

|---|---|---|---|---|---|

| Adelopo | 2011 | Advances in Accounting | 0.064 | 52 | Banking and insurance |

| Aerts and Cormier | 2009 | Accounting, Organizations and Society | 0.074 | 119 | Goods and services, manufacturing, chemicals, telecommunications, and mining |

| Agca and Onder | 2007 | Problems and Perspectives in Management | 0.023 | 51 | Several sectors but not banking and insurance |

| Agyei-Mensah | 2012 | Journal of Applied Finance and Banking | 0.143 | 21 | Rural banking |

| Ahmad et al. | 2003 | International Journal of Business Studies | 0.159 | 39 | Eleven industries |

| Ahmadi and Bouri | 2017 | Management of Environmental Quality: An International Journal | 0.329 | 40 | Manufacturing, technology, health, basic, and construction and building materials |

| Al-Ajmi et al. | 2015 | International Journal of Economics and Finance | 0.163 | 211 | Services |

| Albitar | 2015 | International Business Research | 0.212 | 124 | Companies listed on stock exchanges |

| Al-Tuwaijri et al. | 2004 | Accounting, Organizations and Society | 0.326 | 198 | Unspecified |

| Amran and Devi | 2008 | Managerial Auditing Journal | 0.172 | 133 | Manufacturing, consumer products, construction, technology, hotels, finance, and mining |

| Arayssi et al. | 2016 | Sustainability Accounting, Management and Policy Journal | −0.03 | 350 | Firms included in the Financial Times Stock Exchange (350 index) |

| Axjonow et al. | 2018 | Journal of Business Ethics | −0.03 | 164 | Unspecified |

| Bens and Monahan | 2004 | Journal of Accounting Research | 0.050 | 2519 | Thirty-eight sectors |

| Bhatia and Dhamija | 2015 | South Asian Journal of Management | 0.011 | 78 | Automobiles, consumer goods, energy, infrastructure, metals, pharmaceuticals, and services |

| Boonnual et al. | 2017 | Journal of Business and Retail Management Research | 0.363 | 394 | Companies in the Stock Exchange of Thailand (2014) |

| Bowrin | 2013 | Social Responsibility Journal | 0.230 | 55 | Companies listed on stock exchanges |

| Brammer and Pavelin | 2008 | Business Strategy and the Environment | −0.022 | 447 | Unspecified |

| Castelo and Lima | 2008 | Journal of Business Ethics | −0.015 | 49 | Seventeen sectors |

| Chakroun et al. | 2017 | Social Responsibility Journal | 0.09 | 11 | Listed banks |

| Chan et al. | 2014 | Journal of Business Ethics | 0.027 | 222 | Publicly listed companies |

| Chen et al. | 2008 | Journal of Accounting Research | −0.009 | 4415 | Family firms in the Standard & Poor’s (S&P) 1500 index |

| Cheng et al. | 2016 | Journal of Management and Governance | 0.002 | 1618 | All of the non-financial firms traded on the Shanghai Stock Exchange |

| Chiu and Wang | 2015 | Journal of Business Ethics | 0.007 | 246 | Eighteen sectors |

| Cho, Freedman et al. | 2012 | Accounting, Auditing and Accountability Journal | 0.071 | 119 | Environmentally sensitive industries: chemicals, metals, paper, and petroleum |

| Cho, Guidry et al. | 2012 | Accounting, Organizations and Society | −0.303 | 92 | Environmentally sensitive industries: basic materials, oil and gas, and utility industries |

| Clarkson et al. | 2013 | Journal of Accounting and Public Policy | 0.085 | 195 | Five most polluting industries: paper, chemicals, oil and gas, metals and mining, and utilities |

| Clarkson et al. | 2008 | Accounting, Organizations and Society | 0.046 | 191 | Five most polluting industries: paper, chemicals, oil and gas, metals and mining, and utilities |

| Connelly and Limpaphayom | 2004 | The Journal of Corporate Citizenship | −0.026 | 120 | Companies listed on Thailand’s stock exchange |

| Connors and Gao | 2011 | Accounting and Finance | 0.043 | 324 | Electronics |

| Cormier and Magnan | 2007 | Ecological Economics | −0.270 0.548 | 267 510 | Consumer goods and services, light and industrial manufacturing, water, energy, food and beverages, high technology, heavy industry, metals, chemicals and pharmaceuticals, paper and forest products, and oil and gas |

| Dawkins and Fraas | 2011a | Journal of Business Ethics | −0.196 | 500 | Large capitalization companies |

| Dawkins and Fraas | 2011b | Journal of Business Ethics | 0 | 344 | S&P 500 and industrial firms |

| Delmas and Blass | 2010 | Business Strategy and the Environment | 0.484 | 15 | Chemicals |

| Dragomir | 2010 | Journal of Accounting and Organizational Change | −0.034 | 60 | Largest industrial business groups in the European Union (EU) |

| Forte et al. | 2015 | Gestao, Finanças, e Contabilidade | −0.031 | 100 | Banking |

| Francis et al. | 2008 | Journal of Accounting Research | 0.005 | 677 | Unspecified |

| Freedman and Jaggi | 1982 | OMEGA The International Journal of Management Science | −0.112 −0.024 | 31 109 | Banking |

| Giannarakis | 2014 | International Journal of Law and Management | 0.347 | 366 | Unspecified |

| Giannarakis et al. | 2017 | International Journal of Law and Management | −0.155 | 102 | Companies from a population of S&P´s 500 |

| Griffin and Youm | 2018 | Journal of Business Ethics | 0.038 | 507 | Unspecified |

| Haniffa and Cooke | 2002 | Abacus | 0.244 | 167 | Listed companies but not banks, insurance companies, or trust units |

| Haniffaand Cooke | 2005 | Journal of Accounting and Public Policy | 0.316 | 139 | Non-financial listed companies |

| Hassan and Guo | 2017 | Journal of Applied Accounting Research | 0.052 | 100 | Carbon and non-carbon-intensive industries |

| Hasseldine | 2005 | British Accounting Review | −0.212 | 139 | Companies with an environmental reputation from 26 sectors |

| Hettiarachchi and Gunawardana | 2012 | The Business and Management Review | 0.028 | 78 | Unspecified |

| Ho and Wong | 2001 | Journal of International Accounting Auditing and Taxation | 0.056 | 98 | Listed companies |

| Hossain and Hammami | 2009 | Advances in Accounting: Incorporating Advances in International Accounting | 0.201 | 25 | Four sectors: banking, insurance, manufacturing industry, and services |

| Hossain et al. | 2005 | Journal of Business Finance and Accounting | 0.166 | 243 | No financial sectors |

| Ieng et al. | 2013 | Managerial Auditing Journal | −0.220 | 100 | Unspecified |

| Ionel-Alin | 2012 | Journal of Knowledge Management, Economics and Information Technology | 0.445 | 27 | Unspecified |

| James-Overhu and Cotter | 2010 | Asian Journal of Finance and Accounting | 0.120 | 38 | No financial sectors |

| Jones et al. | 2007 | Australian Accounting Review | 0.112 | 181 | Unspecified |

| Kamal and Saadi | 2013 | Studies in Economics and Finance | −0.111 | 95 | Banking, insurance, investment, industry, and other non-financial services |

| Kansal et al. | 2014 | Advances in Accounting: Incorporating Advances in International Accounting | 0.200 | 80 | Unspecified |

| Khan | 2010 | International Journal of Law and Management | 0.193 | 30 | Commercial banks |

| Kuo and Chen | 2013 | Management Decision | 0.086 | 208 | Twenty-nine sectors |

| Lardon and Deloof | 2014 | Small Business Economics | 0.092 | 164 | Unspecified |

| Laskar and Maji | 2016 | Social Responsibility Journal | 0.350 | 28 | Listed non-financial firms |

| Liu and Anbumozhi | 2009 | Journal of Cleaner Production | 0.125 | 175 | Eleven sectors of activity |

| Luethge and Guohong Han | 2012 | Social Responsibility Journal | 0.030 | 181 | Transportation, energy, chemicals, industrial manufacturing, and other materials |

| Lundholm and Myers | 2002 | Journal of Accounting Research | 0.039 | 4478 | Thirty-three sectors |

| Lungu et al. | 2011 | The Amfiteatru Economic Journal | −0.291 | 33 | Unspecified |

| Luo et al. | 2006 | Pacific-Basin Finance Journal | −0.044 | 516 | Eight sectors |

| Magness | 2006 | Accounting, Auditing, and Accountability Journal | −0.174 | 41 | Mining sector |

| Mallin et al. | 2014 | Journal of Economic Behavior and Organization | 0.043 | 90 | Financial sector |

| Mallin et al. | 2013 | Journal of Business Ethics | 0.120 | 221 | Unspecified |

| Menassa | 2010 | Journal of Applied Accounting Research | 0.725 | 24 | Financial sector |

| Meng et al. | 2013 | Journal of Business Ethics | −0.010 | 2259 | Manufacturing sector |

| Mia and Al-Mamun | 2011 | International Journal of Economics and Finance | 0.054 | 48 | Utilities and industrial companies listed on the Australian stock exchange |

| Michelon | 2011 | Corporate Reputation Review | −0.021 | 114 | Fifty-seven companies listed on the Dow Jones Sustainability Index (DJSI) and 57 companies listed on the Dow Jones Global Index |

| MohdGhazali | 2007 | Corporate Governance | 0.320 | 87 | Non-financial companies listed on the Bursa Malaysia composite index: technology, consumer products, industrial products, trading and services, construction, infrastructure project companies, properties, and plantations |

| Ngwakwe | 2017 | Journal of Accounting and Management | 0.821 | 7 | Unspecified |

| Oeyono et al. | 2011 | Journal of Global Responsibility | 0.171 | 48 | Top corporations in Indonesia (i.e., Global Reporting Initiative) |

| Patten | 1991 | Journal of Accounting and Public Policy | 0.432 | 128 | Environmentally sensitive sectors: chemicals, metals, paper, and petroleum |

| Patten | 2002 | Accounting, Organizations and Society | 0.126 | 131 | Environmentally sensitive sectors: chemicals, metals, paper, and petroleum |

| Platonova et al. | 2018 | Journal of Business Ethics | 0.229 | 24 | Banking |

| Reverte | 2009 | Journal of Business Ethics | 0.110 | 56 | Companies listed on the Spanish stock exchange except financial services: consumer goods, oil and energy, basic materials, utilities and construction, consumer services, real estate, technology, and telecommunications |

| Roberts | 1992 | Accounting, Organizations and Society | −0.014 | 130 | Automobile, food, health and personal care, airline, oil, hotel, and appliance and household products |

| Rouf | 2011 | Business and Economic Research Journal | 0.607 | 93 | Publicly listed companies in Bangladesh |

| Salem et al. | 2012 | International Journal of Management and Marketing Research | 0.342 | 40 | Manufacturing, mining, banking and insurance, and services |

| Scaltrito | 2016 | EuroMed Journal of Business | 0.06 | 203 | Italian listed companies |

| Sharma and Davey | 2013 | International Journal of Economics and Accounting | 0.053 | 15 | Companies listed on the South Pacific Stock Exchange in Fiji: food and household, beverage, insurance, telecommunications, transportation, manufacturing, timber, and natural resources |

| Sierra et al. | 2013 | Corporate Social Responsibility and Environmental Management | −0.038 | 35 | Companies listed on the Spanish stock exchange: consumer goods, oil and energy, basic materials, utilities and construction, consumer services, financial services and real estate, technology, and telecommunications |

| Siew et al. | 2013 | Smart and Sustainable Built Environment | 0.033 | 44 | Construction |

| Siregar and Bachtiar | 2010 | International Journal of Islamic and Middle Eastern Finance and Management | 0.341 | 87 | Firms listed on the Indonesia Stock Exchange |

| Stanwick and Stanwick | 1998 | International Journal of Commerce and Management; | −0.115 | 24 | Chemicals |

| Sulaiman et al. | 2014 | International Journal of Economics, Management and Accounting | 0.011 | 164 | Environmentally sensitive sectors: industrial products, consumer products, plantations, property, trading and services, construction, mining and infrastructure project companies |

| Uyar | 2011 | African Journal of Business Management | −0.006 | 96 | Corporations listed on the Istanbul Stock Exchange-100 Index |

| Vurro and Perrini | 2011 | Corporate Governance | 0.086 | 38 | Worldwide companies included in accountability ratings |

| Wang et al. | 2008 | Journal of International Accounting, Auditing, and Taxation | 0.215 | 109 | Agriculture, chemicals and allied products, conglomerates, construction, electronics, food and beverage, industrial and commercial machinery, information technologies, mining and metal productions, paper and printing, pharmaceuticals, real estate, social services, textiles and apparel, transportation, utilities, and wholesale and retail trade |

| Wiseman | 1982 | Accounting, Organizations, and Society | −0.022 | 26 | Environmentally sensitive sectors: steel, oil, and pulp and paper |

| Yekini and Jallow | 2012 | Sustainability Accounting, Management, and Policy Journal | 0.155 | 27 | Twenty-seven UK companies from top 100 firms in BITCH ranking for corporate responsibility |

| Yuan | 2011 | Management and Engineering | 0.099 | 291 | Companies listed on the Shanghai and Shenzhen stock exchanges |

| Yuen et al. | 2009 | Asian Journal of Finance and Accounting | 0.159 | 200 | Mining, manufacturing, utilities, transportation and warehousing, information technology, wholesale and retail trade, and real estate |

| Zorio et al. | 2013 | Business Strategy and the Environment | 0 | 690 | Companies listed on the Spanish stock exchange: consumer goods, oil and energy, basic materials, utilities and construction, consumer services, financial services and real estate, technology, and telecommunications |

| Link | Number of Effects | Sample | Effect Size 1 | Confidence Intervals | Observed Total Variance | Sampling Error Variance | Q-Statistic 2 | |

|---|---|---|---|---|---|---|---|---|

| Lower Bound | Upper Bound | |||||||

| Corporate social responsibility disclosure (CSRD)⟷Performance | 97 | 29,098 | 0.046 * | 0.03 | 0.05 | 0.017 | 0.003 | 499.21 *** |

| CSRD⟷Performance (without large samples) | 92 | 13,809 | 0.084 * | 0.06 | 0.10 | 0.033 | 0.006 | 471.93 *** |

| Measures of performance | ||||||||

| Financial performance | 76 | 10,425 | 0.082 * | 0.06 | 0.10 | 0.023 | 0.007 | 250.99 *** |

| • Accounting-based measures | 78 | 10,645 | 0.094 * | 0.07 | 0.11 | 0.021 | 0.007 | 235.94 *** |

| • Market-based measures | 16 | 2491 | −0.013 * | −0.012 | −0.014 | 0.018 | 0.006 | 46.06 *** |

| Environmental performance | 22 | 3272 | 0.061 * | 0.02 | 0.09 | 0.032 | 0.006 | 105.75 *** |

| Type of disclosure | ||||||||

| Social disclosure | 5 | 563 | 0.131 * | 0.04 | 0.21 | 0.039 | 0.008 | 23.04 *** |

| Environmental disclosure | 33 | 4728 | −0.0006 | −0.02 | 0.02 | 0.021 | 0.007 | 98.60 *** |

| Economic disclosure | 4 | 599 | 0.087 * | 0.007 | 0.16 | 0.006 | 0.006 | 3.69 |

| Type of organization | ||||||||

| Private | 70 | 9788 | 0.053 * | 0.03 | 0.07 | 0.025 | 0.007 | 254.06 *** |

| Public | 3 | 342 | 0.045 | −0.06 | 0.15 | 0.021 | 0.008 | 7.48 ** |

| Mixed | 5 | 540 | 0.034 | −0.04 | 0.11 | 0.017 | 0.009 | 9.56 ** |

| Sector | ||||||||

| Environmentally sensitive sector | 25 | 3196 | 0.045 * | 0.01 | 0.07 | 0.017 | 0.007 | 56.62 *** |

| Non-environmentally sensitive sector | 19 | 2404 | 0.072 * | 0.03 | 0.11 | 0.020 | 0.007 | 50.22 *** |

| Region | ||||||||

| The Americas | 20 | 3427 | 0.133 * | 0.10 | 0.16 | 0.065 | 0.005 | 232.50 *** |

| Asia | 31 | 4789 | 0.117 * | 0.08 | 0.14 | 0.022 | 0.006 | 111.22 *** |

| Europe | 19 | 3282 | −0.008 | −0.04 | 0.02 | 0.012 | 0.005 | 40.93 *** |

| Oceania | 7 | 656 | 0.152 * | 0.07 | 0.22 | 0.007 | 0.010 | 4.88 * |

| Measures of organization size | ||||||||

| Log of total assets | 27 | 4653 | 0.079 * | 0.051 | 0.108 | 0.037 | 0.005 | 175.48 *** |

| Total assets | 14 | 1728 | 0.159 * | 0.113 | 0.205 | 0.038 | 0.007 | 69.32 *** |

| Log of total sales | 4 | 685 | 0.042 | −0.032 | 0.117 | 0.020 | 0.005 | 13.83 *** |

| Total sales | 3 | 245 | −0.173 * | −0.051 | −0.295 | 0.014 | 0.011 | 3.72 |

| Log of market capitalization | 4 | 217 | 0.136 * | 0.004 | 0.267 | 0.013 | 0.018 | 3.08 |

| Market capitalization | 4 | 577 | 0.119 * | 0.038 | 0.200 | 0.019 | 0.006 | 11.41 *** |

| Log of revenues | 5 | 556 | 0.145 * | 0.064 | 0.227 | 0.026 | 0.008 | 15.43 *** |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gallardo-Vázquez, D.; Barroso-Méndez, M.J.; Pajuelo-Moreno, M.L.; Sánchez-Meca, J. Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach. Sustainability 2019, 11, 1115. https://doi.org/10.3390/su11041115

Gallardo-Vázquez D, Barroso-Méndez MJ, Pajuelo-Moreno ML, Sánchez-Meca J. Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach. Sustainability. 2019; 11(4):1115. https://doi.org/10.3390/su11041115

Chicago/Turabian StyleGallardo-Vázquez, Dolores, María J. Barroso-Méndez, María L. Pajuelo-Moreno, and Julio Sánchez-Meca. 2019. "Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach" Sustainability 11, no. 4: 1115. https://doi.org/10.3390/su11041115

APA StyleGallardo-Vázquez, D., Barroso-Méndez, M. J., Pajuelo-Moreno, M. L., & Sánchez-Meca, J. (2019). Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach. Sustainability, 11(4), 1115. https://doi.org/10.3390/su11041115