The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification

Abstract

:1. Introduction

2. The Development of the Green Bond Market

2.1. The Growth in Green Bond Emissions

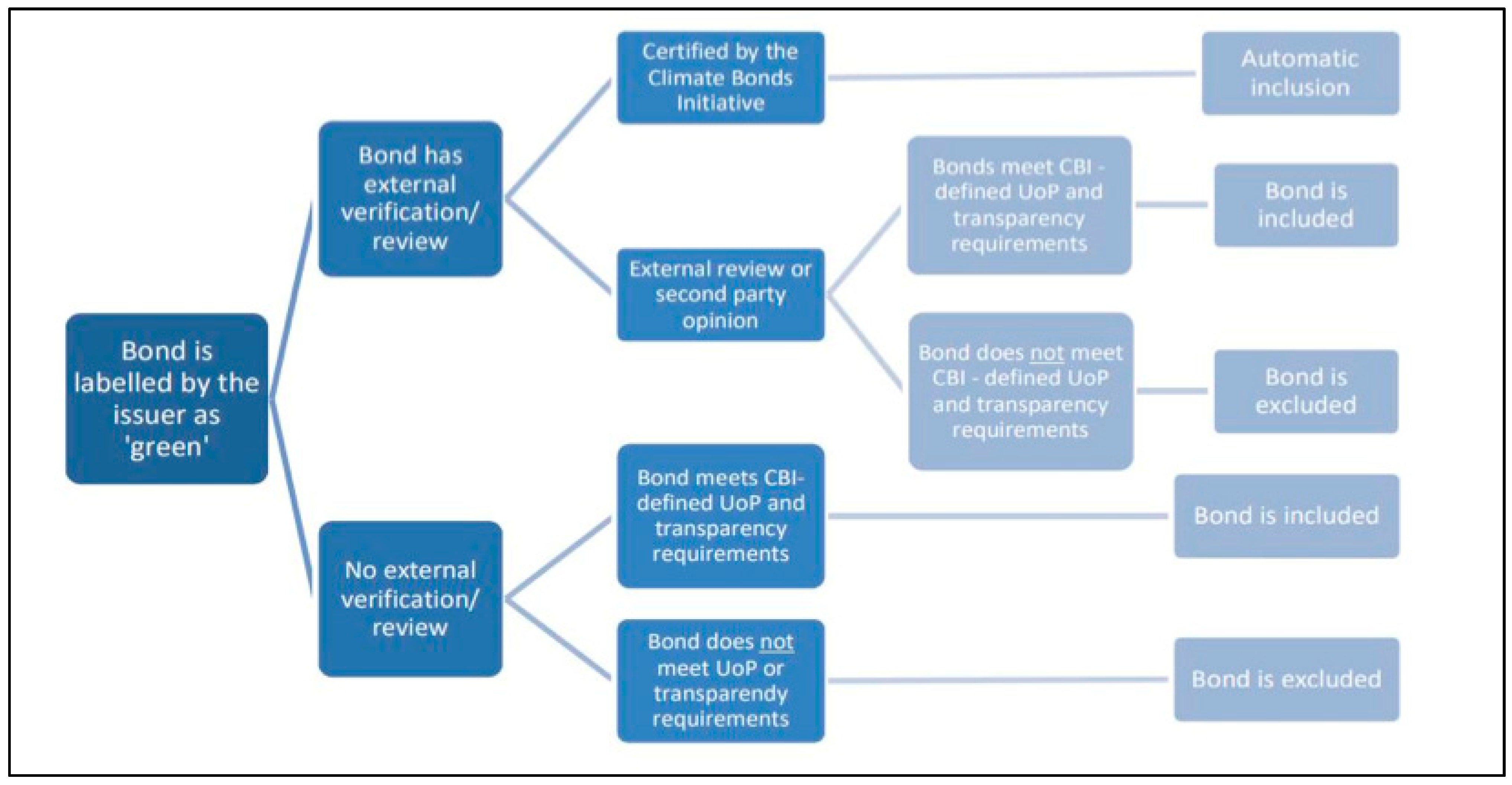

2.2. Standards and Regulation

3. Research Hypothesis

- The green adjective defining the bond issue may create, per se, a difference in terms of bond pricing, liquidity, and volatility on secondary markets;

- The effects of the issuer’s characteristics on asymmetric information and greenwashing risk perceived by investors, and, therefore, on the green bond premium.

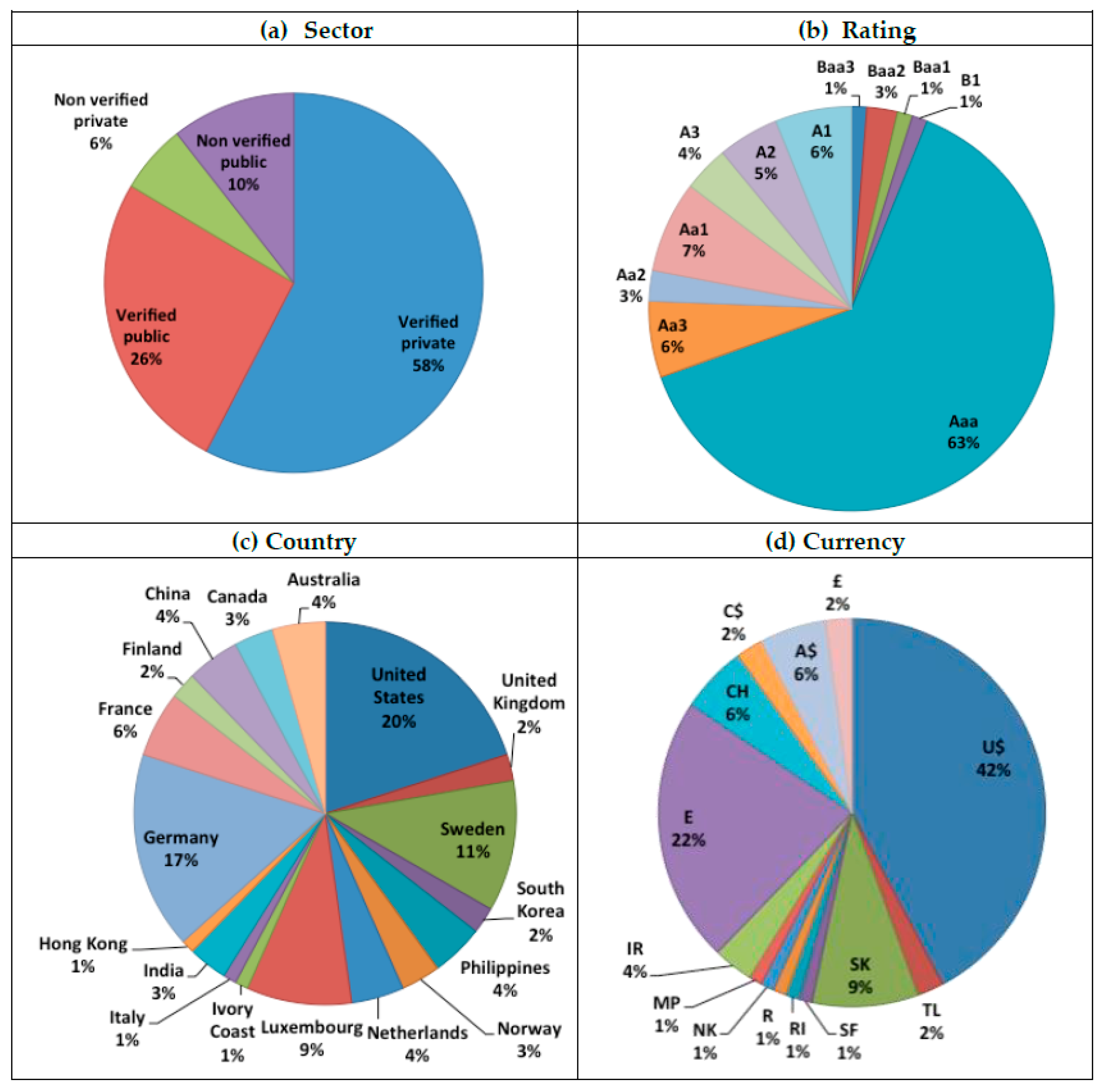

3.1. Matching Method and Dataset

3.2. Differences in Yields, Liquidity, and Volatility: The Green-Brown Bond Puzzle

3.3. The Institutional–Private Issuer Breakdown

4. Robustness Checks

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Couple | Green | Isin | Amount | Coupon | Issue Date | Maturity Date | Currency |

|---|---|---|---|---|---|---|---|

| 1 | 0 | US45950KCH14 | 500,000 | 1.25 | 27/11/2015 | 27/11/2018 | U$ |

| 1 | 1 | US45950VHE92 | 500,000 | 1.25 | 27/11/2015 | 27/11/2018 | U$ |

| 2 | 0 | US61746BDX10 | 2,000,000 | 2.45 | 27/01/2016 | 01/02/2019 | U$ |

| 2 | 1 | US6174468B80 | 500,000 | 2.20 | 08/06/2015 | 07/12/2018 | U$ |

| 3 | 0 | XS1399311064 | 1,200,000 | 0.5 | 26/04/2016 | 26/04/2021 | SK |

| 3 | 1 | XS1494406074 | 3,000,000 | 0.5 | 22/09/2016 | 22/09/2023 | SK |

| 4 | 0 | US00850XAC20 | 500,000 | 2.75 | 21/05/2015 | 21/05/2020 | U$ |

| 4 | 1 | XS1303791336 | 500,000 | 2.75 | 20/10/2015 | 20/10/2020 | U$ |

| 5 | 0 | US459058CY72 | 750,000 | 2.125 | 13/02/2013 | 13/02/2023 | U$ |

| 5 | 1 | US45905URL07 | 600,000 | 2.125 | 03/03/2015 | 03/03/2025 | U$ |

| 6 | 0 | US500769HH04 | 4,000,000 | 1.75 | 07/03/2017 | 31/03/2020 | U$ |

| 6 | 1 | US500769GF56 | 1,500,000 | 1.75 | 15/10/2014 | 15/10/2019 | U$ |

| 7 | 0 | US45950KCE82 | 500,000 | 0.625 | 03/10/2014 | 03/10/2016 | U$ |

| 7 | 1 | US45950VCJ35 | 1,000,000 | 0.5 | 22/02/2013 | 16/05/2016 | U$ |

| 8 | 0 | US500769FH22 | 3,000,000 | 2 | 04/10/2012 | 04/10/2022 | U$ |

| 8 | 1 | US500769HP20 | 1,000,000 | 2 | 05/10/2017 | 29/09/2022 | U$ |

| 9 | 0 | US500769FH22 | 3,000,000 | 2 | 04/10/2012 | 04/10/2022 | U$ |

| 9 | 1 | US500769HD99 | 1,500,000 | 2 | 30/11/2016 | 30/11/2021 | U$ |

| 10 | 0 | DE000NWB17W8 | 500,000 | 0.5 | 07/06/2017 | 07/06/2027 | E |

| 10 | 1 | DE000NWB0AE6 | 500,000 | 0.5 | 13/09/2017 | 13/09/2027 | E |

| 11 | 0 | XS0965428799 | 350,000 | 4.17 | 11/09/2013 | 11/09/2018 | MP |

| 11 | 1 | XS1508504526 | 75,000 | 4.1 | 16/11/2016 | 16/11/2019 | MP |

| 12 | 0 | US045167CX94 | 2,250,000 | 1.875 | 18/02/2015 | 18/02/2022 | U$ |

| 12 | 1 | US045167EB56 | 750,000 | 1.875 | 10/08/2017 | 10/08/2022 | U$ |

| 13 | 0 | US30216BGN64 | 1,250,000 | 1.625 | 19/01/2017 | 17/01/2020 | U$ |

| 13 | 1 | US30216BGU08 | 500,000 | 1.625 | 01/06/2017 | 01/06/2020 | U$ |

| 14 | 0 | XS1043504452 | 4,924,000 | 2 | 11/03/2014 | 18/01/2017 | CH |

| 14 | 1 | XS1080036939 | 500,000 | 2 | 26/06/2014 | 26/06/2017 | CH |

| 15 | 0 | XS0993228534 | 1,000,000 | 0.375 | 13/11/2013 | 15/12/2016 | E |

| 15 | 1 | XS1047440448 | 550,000 | 0.25 | 20/03/2014 | 20/03/2017 | E |

| 16 | 0 | XS1371532117 | 600,000 | 1.875 | 01/03/2016 | 01/03/2019 | U$ |

| 16 | 1 | XS1437622548 | 500,000 | 1.875 | 12/07/2016 | 12/07/2019 | U$ |

| 17 | 0 | XS1346287748 | 1,000,000 | 1.5 | 22/01/2016 | 22/01/2019 | U$ |

| 17 | 1 | XS1383831648 | 600,000 | 1.5 | 22/03/2016 | 23/04/2019 | U$ |

| 18 | 0 | SE0005880143 | 200,000 | 2.45 | 15/04/2014 | 15/04/2019 | SK |

| 18 | 1 | SE0005798816 | 500,000 | 2.473 | 19/03/2014 | 19/03/2019 | SK |

| 19 | 0 | DE000NWB16P4 | 500,000 | 0.75 | 05/02/2014 | 05/02/2018 | E |

| 19 | 1 | DE000NWB0AA4 | 250,000 | 0.75 | 28/11/2013 | 28/11/2017 | E |

| 20 | 0 | US06051GES49 | 1,000,000 | 1.25 | 11/01/2013 | 11/01/2016 | U$ |

| 20 | 1 | US06051GEZ81 | 500,000 | 1.35 | 21/11/2013 | 21/11/2016 | U$ |

| 21 | 0 | XS1221967042 | 1,000,000 | 2.125 | 23/04/2015 | 23/04/2025 | U$ |

| 21 | 1 | XS1188118100 | 500,000 | 2.125 | 11/02/2015 | 11/02/2025 | U$ |

| 22 | 0 | US45950KCE82 | 500,000 | 0.625 | 03/10/2014 | 03/10/2016 | U$ |

| 22 | 1 | US45950VCP94 | 1,000,000 | 0.625 | 15/11/2013 | 15/11/2016 | U$ |

| 23 | 0 | XS1074055770 | 600,000 | 2.5 | 04/06/2014 | 04/06/2026 | E |

| 23 | 1 | XS1038708522 | 750,000 | 2.5 | 26/02/2014 | 26/02/2024 | E |

| 24 | 0 | DE000A168Y55 | 5,000,000 | 0.375 | 09/03/2016 | 09/03/2026 | E |

| 24 | 1 | XS1612940558 | 2,000,000 | 0.25 | 16/05/2017 | 30/06/2025 | E |

| 25 | 0 | XS1165130219 | 500,000 | 2.75 | 12/02/2015 | 12/08/2020 | U$ |

| 25 | 1 | XS1209864229 | 500,000 | 2.75 | 01/04/2015 | 01/04/2020 | U$ |

| 26 | 0 | US00254EMC39 | 1,000,000 | 1.875 | 17/06/2014 | 17/06/2019 | U$ |

| 26 | 1 | US00254EMD12 | 500,000 | 1.875 | 23/06/2015 | 23/06/2020 | U$ |

| 27 | 0 | XS1257176914 | 150,000 | 1.85 | 15/07/2015 | 15/07/2020 | U$ |

| 27 | 1 | XS1618289802 | 500,000 | 1.875 | 23/05/2017 | 01/06/2021 | U$ |

| 28 | 0 | XS1640903537 | 14,000,000 | 5.9 | 06/07/2017 | 20/12/2022 | IR |

| 28 | 1 | XS1618178567 | 3,000,000 | 6 | 24/05/2017 | 24/02/2021 | IR |

| 29 | 0 | XS1669155209 | 500,000 | 1.375 | 23/08/2017 | 23/11/2018 | U$ |

| 29 | 1 | XS1508672828 | 500,000 | 1.375 | 26/10/2016 | 26/10/2020 | U$ |

| 30 | 0 | XS1369614034 | 750,000 | 0.75 | 19/02/2016 | 19/02/2021 | E |

| 30 | 1 | XS1324923520 | 500,000 | 0.75 | 25/11/2015 | 25/11/2020 | E |

| 31 | 0 | US302154CJ68 | 500,000 | 2.125 | 25/01/2017 | 25/01/2020 | U$ |

| 31 | 1 | US302154BZ10 | 400,000 | 2.125 | 11/02/2016 | 11/02/2021 | U$ |

| 32 | 0 | XS0840673858 | 58,020 | 0.5 | 31/10/2012 | 24/10/2017 | TL |

| 32 | 1 | XS0536541005 | 65,000 | 0.5 | 29/09/2010 | 29/09/2017 | TL |

| 33 | 0 | SE0008963920 | 1,250,000 | 1.205 | 24/10/2017 | 24/04/2023 | SK |

| 33 | 1 | SE0010494351 | 1,250,000 | 1.205 | 24/10/2017 | 24/04/2023 | SK |

| 34 | 0 | SE0009345630 | 515,000 | 1.0075 | 29/08/2016 | 15/12/2021 | SK |

| 34 | 1 | SE0009983810 | 830,000 | 1.083 | 24/05/2017 | 24/05/2022 | SK |

| 35 | 0 | US298785HP47 | 5,000,000 | 2.5 | 17/01/2018 | 15/03/2023 | U$ |

| 35 | 1 | US298785GQ39 | 1,000,000 | 2.5 | 15/10/2014 | 15/10/2024 | U$ |

| 36 | 0 | US302154CB33 | 1,000,000 | 1.75 | 26/05/2016 | 26/05/2019 | U$ |

| 36 | 1 | US302154BG39 | 500,000 | 1.75 | 27/02/2013 | 27/02/2018 | U$ |

| 37 | 0 | DE000A1RET72 | 2,000,000 | 0.375 | 15/04/2013 | 18/04/2017 | E |

| 37 | 1 | XS1087815483 | 1,500,000 | 0.375 | 22/07/2014 | 22/07/2019 | E |

| 38 | 0 | US037833DK32 | 1,500,000 | 3 | 13/11/2017 | 13/11/2027 | U$ |

| 38 | 1 | US037833CX61 | 1,000,000 | 3 | 20/06/2017 | 20/06/2027 | U$ |

| 39 | 0 | AU3CB0223592 | 250,000 | 4 | 27/05/2014 | 27/11/2019 | A$ |

| 39 | 1 | AU3CB0226090 | 300,000 | 4 | 16/12/2014 | 16/12/2021 | A$ |

| 40 | 0 | XS1197351577 | 1,500,000 | 1.125 | 04/03/2015 | 04/03/2022 | E |

| 40 | 1 | XS1636000561 | 500,000 | 0.875 | 27/06/2017 | 27/06/2022 | E |

| 41 | 0 | US00828EBE86 | 1,100,000 | 1.375 | 12/02/2015 | 12/02/2020 | U$ |

| 41 | 1 | US00828EBJ73 | 500,000 | 1.375 | 17/12/2015 | 17/12/2018 | U$ |

| 42 | 0 | CA298785GT79 | 1,400,000 | 1.125 | 18/02/2015 | 18/02/2020 | C$ |

| 42 | 1 | XS1490971634 | 500,000 | 1.125 | 16/09/2016 | 16/09/2021 | C$ |

| 43 | 0 | US459058FF56 | 1,000,000 | 1.75 | 19/04/2016 | 19/04/2023 | U$ |

| 43 | 1 | US45905UZT41 | 500,000 | 1.75 | 22/11/2016 | 22/11/2021 | U$ |

| 44 | 0 | FR0013231743 | 1,000,000 | 1.125 | 18/01/2017 | 18/01/2023 | E |

| 44 | 1 | FR0013067170 | 300,000 | 1.125 | 14/12/2015 | 14/12/2022 | E |

| 45 | 0 | AU3CB0241891 | 400,000 | 3.25 | 17/01/2017 | 17/01/2022 | A$ |

| 45 | 1 | AU3CB0243657 | 450,000 | 3.25 | 31/03/2017 | 31/03/2022 | A$ |

| 46 | 0 | US45905UQ233 | 750,000 | 2 | 30/10/2017 | 30/10/2020 | U$ |

| 46 | 1 | US45905UG408 | 300,000 | 2 | 12/04/2017 | 12/04/2022 | U$ |

| 47 | 0 | XS1688390068 | 300,000 | 3 | 25/09/2017 | 25/05/2023 | U$ |

| 47 | 1 | XS1589873097 | 300,000 | 3 | 24/04/2017 | 21/10/2022 | U$ |

| 48 | 0 | XS0167422871 | 200,000 | 1 | 19/05/2003 | 17/05/2018 | U$ |

| 48 | 1 | US045167DQ35 | 800,000 | 1 | 16/08/2016 | 16/08/2019 | U$ |

| 49 | 0 | XS1481017520 | 500,000 | 0.875 | 25/08/2016 | 27/08/2018 | U$ |

| 49 | 1 | US30216BER96 | 300,000 | 0.875 | 30/01/2014 | 30/01/2017 | U$ |

| 50 | 0 | US459058ER04 | 4,000,000 | 1 | 07/10/2015 | 05/10/2018 | U$ |

| 50 | 1 | US45905UWE09 | 280,000 | 1.005 | 21/04/2016 | 01/10/2018 | U$ |

| 51 | 0 | CA298785GT79 | 1,400,000 | 1.125 | 18/02/2015 | 18/02/2020 | C$ |

| 51 | 1 | XS1314336204 | 500,000 | 1.25 | 05/11/2015 | 05/11/2020 | C$ |

| 52 | 0 | XS1346287748 | 1,000,000 | 1.5 | 22/01/2016 | 22/01/2019 | U$ |

| 52 | 1 | US50046PAU93 | 600,000 | 1.5 | 22/03/2016 | 23/04/2019 | U$ |

| 53 | 0 | XS1368576572 | 1,250,000 | 0.75 | 22/02/2016 | 22/02/2021 | E |

| 53 | 1 | XS1324217733 | 500,000 | 0.75 | 24/11/2015 | 24/11/2020 | E |

| 54 | 0 | US459058FQ12 | 300,000 | 1.2 | 30/09/2016 | 30/09/2019 | U$ |

| 54 | 1 | XS1517268105 | 100,000 | 1.181 | 14/11/2016 | 15/12/2019 | U$ |

| 55 | 0 | CH0180006113 | 305,000 | 1.625 | 02/04/2012 | 02/04/2026 | SF |

| 55 | 1 | CH0233004172 | 350,000 | 1.625 | 04/02/2014 | 04/02/2025 | SF |

| 56 | 0 | US44987DAE67 | 1,000,000 | 2.05 | 17/08/2015 | 17/08/2018 | U$ |

| 56 | 1 | US44987DAJ54 | 800,000 | 2 | 24/11/2015 | 26/11/2018 | U$ |

| 57 | 0 | SE0009580186 | 250,000 | 0.35 | 31/01/2017 | 31/07/2019 | SK |

| 57 | 1 | SE0009607013 | 490,000 | 0.38 | 14/02/2017 | 28/08/2019 | SK |

| 58 | 0 | US459058DY63 | 4,300,000 | 1.625 | 12/02/2015 | 10/02/2022 | U$ |

| 58 | 1 | US45905ULF92 | 5000 | 1.5 | 12/07/2012 | 12/07/2022 | U$ |

| 59 | 0 | DE000NWB12F4 | 75,000 | 4.32 | 24/08/2009 | 28/12/2017 | E |

| 59 | 1 | DE000NWB0AB2 | 500,000 | 4.25 | 04/11/2014 | 05/11/2018 | E |

| 60 | 0 | XS1405911576 | 1,350,000 | 0.83 | 10/05/2016 | 10/05/2021 | SK |

| 60 | 1 | XS1433082861 | 1,000,000 | 0.885 | 15/06/2016 | 15/06/2022 | SK |

| 61 | 0 | XS1399311064 | 1,200,000 | 0.5 | 26/04/2016 | 26/04/2021 | SK |

| 61 | 1 | XS1347786797 | 1,000,000 | 0.625 | 20/01/2016 | 20/01/2021 | SK |

| 62 | 0 | XS0858366098 | 3,550,000 | 1.375 | 27/11/2012 | 15/09/2020 | E |

| 62 | 1 | LU0953782009 | 3,000,000 | 1.375 | 18/07/2013 | 15/11/2019 | E |

| 63 | 0 | AU3CB0236727 | 175,000 | 3.25 | 07/04/2016 | 07/04/2021 | A$ |

| 63 | 1 | AU3CB0230100 | 6.000e+08 | 3.25 | 29/06/2015 | 03/06/2020 | A$ |

| 64 | 0 | CND100009HY3 | 5.000e+08 | 3.4 | NA | 14/03/2021 | CH |

| 64 | 1 | CND10000G4D6 | 1.000e+09 | 3.4 | NA | 24/09/2021 | CH |

| 65 | 0 | INE296A07LC6 | 2.000e+08 | 8.55 | NA | 28/04/2021 | IR |

| 65 | 1 | INE296A07LL7 | 2.000e+08 | 8.55 | NA | 14/07/2021 | IR |

| 66 | 0 | CND100005DQ6 | 2.500e+10 | 3.87 | NA | 28/06/2019 | CH |

| 66 | 1 | CND10000G602 | 1.000e+10 | 3.79 | NA | 23/12/2019 | CH |

| 67 | 0 | CND10000H8S4 | 2.000e+09 | 4.68 | NA | 10/05/2020 | CH |

| 67 | 1 | CND10000H6C2 | 2.000e+09 | 4.79 | NA | 11/04/2020 | CH |

| 68 | 0 | DE000BHY0BA8 | 500,000 | 0.125 | 22/10/2015 | 22/10/2020 | E |

| 68 | 1 | DE000BHY0GP5 | 500,000 | 0.125 | 05/05/2015 | 05/05/2022 | E |

| 69 | 0 | DE000BHY0MT5 | 500,000 | 0.125 | 05/09/2017 | 05/01/2024 | E |

| 69 | 1 | DE000BHY0GH2 | 500,000 | 0.125 | 14/06/2017 | 23/10/2023 | E |

| 70 | 0 | XS0849420905 | 2,000,000 | 2.5 | 31/10/2012 | 3/11/02022 | £ |

| 70 | 1 | XS1051861851 | 1,800,000 | 2.25 | 08/04/2014 | 07/03/2020 | £ |

| 71 | 0 | XS1351517260 | 1.800e+08 | 8.46 | 18/02/2016 | 19/02/2019 | RI |

| 71 | 1 | XS1324201497 | 1.700e+08 | 8.66 | 14/12/2015 | 17/12/2018 | RI |

| 72 | 0 | XS1417412506 | 142,800 | 2.5 | 29/11/2016 | 29/11/2021 | A$ |

| 72 | 1 | XS1367226385 | 49,100 | 2.3 | 24/06/2016 | 18/06/2020 | A$ |

| 73 | 0 | XS1014678053 | 2,500,000 | 3.45 | 16/01/2014 | 16/01/2017 | CH |

| 73 | 1 | XS1437844100 | 1,500,000 | 3.6 | 12/07/2016 | 12/07/2018 | CH |

| 74 | 0 | XS1254823682 | 412,000 | 5.71 | 30/07/2015 | 05/08/2020 | IR |

| 74 | 1 | XS1241051967 | 260,000 | 5.6 | 25/06/2015 | 25/06/2020 | IR |

| 75 | 0 | DE000NWB18E4 | 500,000 | 0.25 | 04/07/2017 | 04/07/2025 | E |

| 75 | 1 | DE000NWB0AD8 | 500,000 | 0.375 | 17/11/2016 | 17/11/2026 | E |

| 76 | 0 | XS1138501918 | 400,000 | 1.34 | 18/11/2014 | 18/11/2019 | SK |

| 76 | 0 | XS1697577556 | 1,000,000 | 0.98 | 11/10/2017 | 11/10/2022 | SK |

| 76 | 1 | XS1436518606 | 1,000,000 | 1.048 | 23/06/2016 | 23/06/2021 | SK |

| 77 | 0 | XS1401196958 | 500,000 | 1.125 | 28/04/2016 | 28/04/2027 | E |

| 77 | 0 | XS1523192588 | 500,000 | 0.875 | 22/11/2016 | 21/02/2025 | E |

| 77 | 1 | XS1218319702 | 500,000 | 1 | 15/04/2015 | 14/03/2025 | E |

| 78 | 0 | US30216BFZ04 | 1,000,000 | 1.25 | 02/02/2016 | 04/02/2019 | U$ |

| 78 | 1 | US30216BFY39 | 300,000 | 1.25 | 08/12/2015 | 10/12/2018 | U$ |

| 79 | 0 | DE000A168Y06 | 5,000,000 | 0.125 | 03/09/2015 | 01/06/2020 | E |

| 79 | 1 | XS1311459694 | 1,500,000 | 0.125 | 27/10/2015 | 27/10/2020 | E |

| 80 | 0 | XS0995130712 | 2,250,000 | 8.5 | 22/11/2013 | 25/07/2019 | TL |

| 80 | 1 | XS1198278175 | 275,000 | 8.5 | 12/03/2015 | 27/03/2019 | TL |

| 81 | 0 | AU3CB0204402 | 1,200,000 | 3.5 | 24/01/2013 | 24/01/2018 | A$ |

| 81 | 1 | AU3CB0220424 | 300,000 | 3.5 | 29/04/2014 | 29/04/2019 | A$ |

| 82 | 0 | XS1346200055 | 1,450,000 | 1.375 | 18/01/2016 | 01/02/2021 | £ |

| 82 | 1 | XS1268337844 | 1,000,000 | 1.625 | 30/07/2015 | 05/06/2020 | £ |

| 83 | 0 | XS0544798167 | 1,250,000 | 7 | 06/10/2010 | 06/10/2015 | R |

| 83 | 1 | XS0994434487 | 2,300,000 | 6.75 | 19/11/2013 | 15/09/2017 | R |

| 84 | 0 | XS1040151315 | 750,000 | 0.75 | 05/03/2014 | 05/03/2018 | E |

| 84 | 1 | XS1083955911 | 500,000 | 0.625 | 03/07/2014 | 03/07/2019 | E |

| 85 | 0 | DE000NWB17G1 | 1,000,000 | 0.625 | 11/02/2016 | 11/02/2026 | E |

| 85 | 1 | DE000NWB0AC0 | 500,000 | 0.875 | 10/11/2015 | 10/11/2025 | E |

| 86 | 0 | NO0010724743 | 1,500,000 | 2.45 | 24/11/2014 | 24/05/2023 | NK |

| 86 | 1 | NO0010752702 | 1,500,000 | 2.35 | 04/12/2015 | 04/09/2024 | NK |

| 87 | 0 | US06050TME90 | 1,250,000 | 2.05 | 07/12/2015 | 07/12/2018 | U$ |

| 87 | 0 | US06050TMC35 | 1,750,000 | 1.75 | 05/06/2015 | 05/06/2018 | U$ |

| 87 | 1 | US06051GFR56 | 600,000 | 1.95 | 12/05/2015 | 12/05/2018 | U$ |

| 88 | 0 | XS1128264758 | 350,000 | 4.125 | 23/10/2014 | 23/04/2020 | U$ |

| 88 | 1 | XS1325600994 | 350,000 | 4.25 | 30/11/2015 | 30/11/2020 | U$ |

| 89 | 0 | XS1422841202 | 500,000 | 0.625 | 31/05/2016 | 31/05/2022 | E |

| 89 | 1 | XS1244060486 | 500,000 | 0.75 | 09/06/2015 | 09/06/2020 | E |

References

- Zerbib, O.D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. J. Bank. Finance 2019, 98, 39–60. [Google Scholar] [CrossRef]

- Wulandari, F.; Schäfer, D.; Andreas, S.; Sun, C. Liquidity Risk and Yield Spreads of Green Bonds. DIW Berlin Discussion Paper No. 1728. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3161323 (accessed on 16 February 2019).

- Reboredo, J.C. Green Bond and Financial Markets: Co-Movement, Diversification and Price Spillover Effects. Energy Econ. 2018, 74, 38–50. [Google Scholar] [CrossRef]

- Karpf, A.; Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nat. Clim. Chang. 2018, 8, 161. [Google Scholar] [CrossRef]

- Hachenberg, B.; Schiereck, D. Are green bonds priced differently from conventional bonds? J. Asset Manag. 2018, 19, 371–383. [Google Scholar] [CrossRef]

- Glavas, D.; Bancel, F. Are Agency Problems a Determinant of Green Bond Issuance? Univ. Libr. MunichGer. 2018. MPRA Paper No. 88377. Available online: https://mpra.ub.uni-muenchen.de/88377/ (accessed on 16 February 2019).

- Reichelt, H. Green bonds: A model to mobilise private capital to fund climate change mitigation and adaptation projects. In The EuroMoney Environmental Finance Handbook; World Bank Group: Washington, DC, USA, 2010; pp. 1–7. [Google Scholar]

- World Bank. What Are Green Bonds? (English); World Bank Group: Washington, DC, USA, 2015; Available online: http://documents.worldbank.org/curated/en/400251468187810398/What-are-green-bonds (accessed on 16 February 2019).

- International Energy Agency. Global Energy & CO2 Status Report 2017. Available online: https://www.iea.org/publications/freepublications/publication/GECO2017 (accessed on 16 February 2019).

- Climate Bonds Initiative. Green Bond Policy: Highlights from 2017. Available online: https://www.climatebonds.net/files/reports/cbi-policyroundup_2017_final_3. (accessed on 16 February 2019).

- OECD. Mapping Channels to Mobilise Institutional Investment in Sustainable Energy. In Green Finance and Investment; OECD Publishing: Paris, France, 2015. [Google Scholar]

- ICMA—International Capital Market Association. Green Bond Principles. Voluntary Process Guidelines for Issuing Green Bonds; ICMA: Washington, DC, USA, 2015. [Google Scholar]

- Technical Expert Group on Sustainable Finance: Report on Climate-Related Disclosures. Available online: https://ec.europa.eu/info/publications/190110-sustainable-finance-teg-report-climate-related-disclosures_en (accessed on 16 February 2019).

- Roe, B.; Teisl, M.F.; Levy, A.; Russell, M. US consumers’ willingness to pay for green electricity. Energy Policy 2001, 29, 917–925. [Google Scholar] [CrossRef]

- Kaenzig, J.; Heinzle, S.L.; Wüstenhagen, R. Whatever the customer wants, the customer gets? Exploring the gap between consumer preferences and default electricity products in Germany. Energy Policy 2013, 53, 311–322. [Google Scholar] [CrossRef]

- Rommel, J.; Sagebiel, J.; Müller, J.R. Quality uncertainty and the market for renewable energy: Evidence from German consumers. Renew. Energy 2016, 94, 106–113. [Google Scholar] [CrossRef]

- Amiraslani, H.; Lins, K.V.; Servaes, H.; Tamayo, A. A matter of Trust? The Bond Market Benefits of Corporate Social Capital during the Financial Crisis. CEPR Discussion Paper No. DP12321. 2017. Available online: https://ssrn.com/abstract=3042634 (accessed on 16 February 2019).

- Bauer, R.; Hann, D. Corporate Environmental Management and Credit Risk. Available online: https://ssrn.com/abstract=1660470 (accessed on 16 February 2019).

- Graham, A.; Maher, J.J.; Northcut, W.D. Environmental liability information and bond ratings. J. Account. Audit. Finance 2001, 16, 93–116. [Google Scholar] [CrossRef]

- Oikonomou, I.; Brooks, C.; Pavelin, S. The effects of corporate social performance on the cost of corporate debt and credit ratings. Financial Rev. 2014, 49, 49–75. [Google Scholar] [CrossRef]

- Becchetti, L.; Ciciretti, R.; Dalo, A. Fishing the Corporate Social Responsibility Risk Factors. J. Financial Stabil. 2018, 37, 25–48. [Google Scholar] [CrossRef]

- Becchetti, L.; Ciciretti, R.; Hasan, I.; La Licata, G. Environmental Reputational Risk, Negative Media Attention and Financial Performance. Mimeo 2019. [Google Scholar]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Finance 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Kreander, N.; Gray, R.H.; Power, D.M.; Sinclair, C.D. Evaluating the performance of ethical and non-ethical funds: A matched pair analysis. J. Bus. Finance Account. 2005, 32, 1465–1493. [Google Scholar] [CrossRef]

- Gregory, A.; Matatko, J.; Luther, R. Ethical unit trust financial performance: Small company effects and fund size effects. J. Bus. Finance Account. 1997, 24, 705–725. [Google Scholar] [CrossRef]

- Crabbe, L.E.; Turner, C.M. Does the liquidity of a debt issue increase with its size? Evidence from the corporate bond and medium-term note markets. J. Finance 1995, 50, 1719–1734. [Google Scholar] [CrossRef]

- Helwege, J.; Turner, C.M. The slope of the credit yield curve for speculative-grade issuers. J. Finance 1999, 54, 1869–1884. [Google Scholar] [CrossRef]

- Huang, W.J.; Zhang, Y.B. Assessment of power customer credit risk based on extension method. Power Syst. Prot. Control 2008, 19. [Google Scholar]

- Helwege, J.; Huang, J.Z.; Wang, Y. Liquidity effects in corporate bond spreads. J. Bank. Finance 2014, 45, 105–116. [Google Scholar] [CrossRef]

- Dick-Nielsen, J.; Feldhütter, P.; Lando, D. Corporate bond liquidity before and after the onset of the subprime crisis. J. Financial Econ. 2012, 103, 471–492. [Google Scholar] [CrossRef]

- Green Bonds Market Summary—Q1 2018. Climate Bond Initiative. Available online: https://www.climatebonds.net/resources/reports/green-bonds-market-summary-q1-2018 (accessed on 16 February 2019).

- Chen, L.; Lesmond, D.A.; Wei, J. Corporate yield spreads and bond liquidity. J. Finance 2007, 62, 119–149. [Google Scholar] [CrossRef]

| Bond Characteristic | Matching Criterion |

|---|---|

| Amount issued | ±400% |

| Coupon rate | ±0.25% |

| Maturity date | ±2 years |

| Currency | Same |

| Issuer | Same |

| Rating | Same |

| Coupon type | Same (fixed rate) |

| Variable Name | Variable Description |

|---|---|

| Agency | Rating agency |

| Amount | Amount issued (national currency) |

| amount dollar | Amount issued (USD) |

| Bond type | Bond type |

| Borrower | Name of the issuer of the bond |

| C_type | Coupon type (fixed or floating) |

| Country | Country of risk |

| Coupon | Coupon rate |

| Currency | Currency of amount issued |

| Date | Date |

| Green | Dummy variable equal to 1 if the bond is green and 0 otherwise |

| I_year | Issue year |

| Id_pair | Number identifying the green-brown pair |

| Isin | International Securities Identification Number for the bond |

| Issue Date | Issue date of the bond |

| Verified | Dummy variable equal to 1 if the green bond is third-party verified and 0 otherwise |

| Pask | Ask price (Datastream) |

| Pbid | Bid price (Datastream) |

| Institutional | Dummy variable equal to 1 if the bond is issued by national governments, municipalities or supranational institutions such as World Bank and 0 if private institution |

| Rating | Rating of the bond by Moody’s (from C to AAA) |

| Sector | Industry sub-sector description |

| Time | Number that identifies the trading day |

| Time to Maturity | Number of days to reach maturity date |

| Zero Trading Day (ZTD) Liquidity Yield Standard Deviation (SD) | Dummy variable equal to 1 if the bond has not been traded during the whole day and 0 otherwise Difference between the bid and the ask price Bond yield standard deviation computed ex post |

| Green Bonds | Count | Mean | SD | 1st Perc. | 25th Perc. | 50th Perc. | 75th Perc. | 99th Perc. |

|---|---|---|---|---|---|---|---|---|

| Yield | 39,333 | 2.03 | 2.55 | −0.45 | 0.39 | 1.54 | 2.45 | 11.82 |

| Price ask | 38,435 | 100.87 | 4.71 | 79.68 | 99.55 | 100.62 | 102.40 | 115.53 |

| Price bid | 38,513 | 100.64 | 4.69 | 79.63 | 99.41 | 100.41 | 102.16 | 115.02 |

| Liquidity | 38,435 | −0.22 | 0.34 | −1.75 | −0.26 | −0.13 | −0.08 | −0.011 |

| ZTD | 39,333 | 0.053 | 0.225 | 0 | 0 | 0 | 0 | 1 |

| Yield SD | 39,329 | 0.06 | 0.074 | 0.01 | 0.033 | 0.049 | 0.075 | 0.42 |

| Coupon | 39,333 | 1.93 | 1.66 | 0.12 | 0.75 | 1.62 | 2.3 | 8.5 |

| Amount ($) | 39,333 | 0.169 | 1.32 | 0.0003 | 0.00032 | 0.005 | 0.006 | 4.45 |

| Time to Maturity | 39,333 | 3219.02 | 2833.80 | 77 | 862 | 2743 | 2745 | 9936 |

| Brown Bonds | Count | Mean | SD | 1st Perc. | 25th Perc. | 50th Perc. | 75th Perc. | 99th Perc. |

|---|---|---|---|---|---|---|---|---|

| Yield | 39,333 | 2.01 | 3.21 | −0.45 | 0.44 | 1.51 | 2.32 | 11.93 |

| Price ask | 38,869 | 101.14 | 4.71 | 80.94 | 99.67 | 100.70 | 102.16 | 116.08 |

| Price bid | 38,964 | 100.85 | 4.85 | 79.02 | 99.50 | 100.51 | 101.94 | 115.82 |

| Liquidity | 38,869 | −0.27 | 0.44 | −2.5 | −0.27 | −0.13 | −0.07 | −0.01 |

| ZTD | 39,333 | 0.056 | 0.23 | 0 | 0 | 0 | 0 | 1 |

| Yield SD | 39,329 | 0.11 | 1.80 | 0.01 | 0.032 | 0.049 | 0.08 | 0.49 |

| Coupon | 38,778 | 2.01 | 1.66 | 0.12 | 0.75 | 1.62 | 2.5 | 8.5 |

| Amount ($) | 39,333 | 0.26 | 3.07 | 0.00013 | 0.0031 | 0.0075 | 0.011 | 0.78 |

| Time to maturity | 39,333 | 3248.82 | 3102.90 | 45 | 700 | 2292 | 4322 | 11,360 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | OLS | OLS | OLS | FE | FE | FE |

| Δ Coupon | 0.184 *** | 0.178 *** | 0.123 *** | |||

| (0.00980) | (0.0109) | (0.00887) | ||||

| Δ Amount | −11.07 ** | −13.01 ** | −15.33 *** | |||

| (5.091) | (5.629) | (5.774) | ||||

| Δ Maturity | 0.134 *** | 0.136 *** | 0.124 *** | |||

| (0.00227) | (0.00262) | (0.00230) | ||||

| Δ σ | 0.499 * | 0.500 * | 0.501 *** | 0.502 *** | ||

| (0.255) | (0.255) | (0.00169) | (0.00169) | |||

| Δ Liquidity | −0.106 *** | −0.0153 | ||||

| (0.0118) | (0.0420) | |||||

| Δ ZTD | −0.136 * | −0.0897 | ||||

| (0.0700) | (0.0906) | |||||

| α0 | 0.0360 *** | 0.0590 *** | 0.0465 *** | 0.0206 ** | 0.0433 *** | 0.0305 *** |

| (green premium) | (0.0107) | (0.00369) | (0.00261) | (0.00991) | (7.64e-05) | (0.00251) |

| Observations | 37,802 | 37,798 | 36,673 | 39,333 | 39,329 | 38,204 |

| R-squared | 0.007 | 0.206 | 0.208 | 0.000 | 0.206 | 0.202 |

| Number of bond couples | 89 | 89 | 88 |

| (1) | (2) | |

|---|---|---|

| Variable | Liquidity FE | SD FE |

| α0 | 0.0549 *** | −0.0453 *** |

| (0.00138) | (0.00897) | |

| Observations | 38,207 | 39,329 |

| R2 | 0.000 | 0.000 |

| Number of bond couples | 88 | 89 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | OLS | OLS | OLS | FE | FE | FE |

| Δ Coupon | 0.0512 *** | 0.0488 *** | 0.0499 *** | |||

| (0.00568) | (0.00369) | (0.00378) | ||||

| Δ Amount | −9.615 ** | −11.07 ** | −10.68 ** | |||

| (4.437) | (5.008) | (4.992) | ||||

| Δ Maturity | 0.114 *** | 0.115 *** | 0.113 *** | |||

| (0.00189) | (0.00183) | (0.00174) | ||||

| Δ σ | 0.107 | 0.106 | 0.144 *** | 0.140 | ||

| (0.146) | (0.146) | (0.00881) | (0.0960) | |||

| Δ Liquidity | −0.118 *** | −0.113 *** | ||||

| (0.00755) | (0.0172) | |||||

| Δ ZTD | 0.00226 | 0.00722 | ||||

| (0.0201) | (0.0131) | |||||

| α0 | 0.0323 *** | 0.0328 *** | 0.0319 *** | 0.0237 *** | 0.0248 *** | 0.0246 *** |

| (green premium) | (0.00170) | (0.00166) | (0.00155) | (0.00131) | (0.00131) | (0.000961) |

| Observations | 22,347 | 22,345 | 22,094 | 22,902 | 22,900 | 22,649 |

| R2 | 0.161 | 0.164 | 0.193 | 0.000 | 0.012 | 0.026 |

| Number of bond couples | 58 | 58 | 57 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | OLS | OLS | OLS | FE | FE | FE |

| Δ Coupon | 2.867 *** | 2.800 *** | 2.744 *** | |||

| (0.0810) | (0.0685) | (0.0719) | ||||

| Δ Amount | −965.3 *** | −1128 *** | −1074 *** | |||

| (74.16) | (67.89) | (68.60) | ||||

| Δ Maturity | 0.415 *** | 0.358 *** | 0.359 *** | |||

| (0.0149) | (0.0136) | (0.0135) | ||||

| Δ σ | −0.281 *** | −0.264 *** | −0.154 *** | −0.122 ** | ||

| (0.0150) | (0.0120) | (0.0151) | (0.0338) | |||

| Δ Liquidity | −0.0104 | −0.0104 | −5.45e-05 | 0.000137 | ||

| (0.0104) | (0.00814) | (0.00181) | (0.00394) | |||

| Δ ZTD | 0.992 *** | 1.258 * | ||||

| (0.125) | (0.595) | |||||

| α0 | 0.0370 *** | 0.0340 *** | 0.0321 *** | 0.124 *** | 0.112 *** | 0.111 *** |

| (green premium) | (0.00445) | (0.00362) | (0.00371) | (0.00182) | (0.00102) | (0.00110) |

| Observations | 3097 | 3071 | 3070 | 3097 | 3071 | 3070 |

| R2 | 0.521 | 0.591 | 0.625 | 0.000 | 0.062 | 0.239 |

| Number of bond couples | 7 | 7 | 7 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | OLS | OLS | OLS | FE | FE | FE |

| Δ Coupon | 1.196 *** | 0.945 *** | 0.960 *** | |||

| (0.0263) | (0.0135) | (0.0105) | ||||

| Δ Amount | −123,659 *** | −121,066 *** | −122,438 *** | |||

| (3956) | (2938) | (2670) | ||||

| Δ Maturity | 0.165 *** | 0.155 *** | 0.145 *** | |||

| (0.00579) | (0.00669) | (0.00351) | ||||

| Δ σ | −0.106 ** | −0.189 *** | 0.0447 ** | 0.0387 * | ||

| (0.0501) | (0.0152) | (0.0195) | (0.0210) | |||

| Δ Liquidity | −0.0755 | −0.282 ** | −0.191 | −0.192 | ||

| (0.127) | (0.138) | (0.183) | (0.176) | |||

| Δ ZTD | 0.502 * | 0.504 *** | ||||

| (0.256) | (0.00144) | |||||

| α0 | −0.0960 *** | −0.0947 *** | −0.0355 *** | 0.0163 | −0.0187 *** | 0.0324 *** |

| (green premium) | (0.0250) | (0.0320) | (0.00514) | (0.0236) | (0.00425) | (0.00335) |

| Observations | 15,455 | 14,580 | 14,579 | 16,431 | 15,556 | 15,555 |

| R-squared | 0.019 | 0.010 | 0.216 | 0.000 | 0.000 | 0.204 |

| Number of bond couples | 31 | 31 | 31 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | Institutional Issuers | Private Issuers | Private Issuers Non-Certified | Private Issuers Green Certified |

| α0 | 0.108 *** | 0.0186 *** | −0.0657 *** | 0.0319 *** |

| (0.00271) | (0.00141) | (0.00291) | (0.00157) | |

| Observations | 15,556 | 22,651 | 3071 | 19,580 |

| Number of bond couples | 31 | 57 | 7 | 50 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | Institutional Issuers | Private Issuers | Private Issuers Non-Certified | Private Issuers GREEN Certified |

| α0 | −0.0976 *** | −0.00774 *** | 0.000755 | −0.00907 *** |

| (0.0214) | (0.000980) | (0.000659) | (0.00113) | |

| Observations | 16,429 | 22,900 | 3096 | 19,804 |

| Number of bond couples | 31 | 58 | 7 | 51 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | OLS All Sample | OLS Institutional Issuers | OLS Private Issuers | OLS Private Issuers No Verification |

| Δ Coupon | 0.123 *** | 0.960 *** | 0.0499 *** | 2.744 *** |

| (0.00888) | (0.0106) | (0.00396) | (0.0737) | |

| Δ Amount | −15.33 *** | −122,438 *** | −10.68 ** | −1074 *** |

| (5.899) | (2684) | (4.768) | (70.99) | |

| Δ Maturity | 0.124 *** | 0.145 *** | 0.113 *** | 0.359 *** |

| (0.00243) | (0.00348) | (0.00176) | (0.0139) | |

| Δ σ | −0.106 *** | −0.189 *** | −0.118 *** | −0.264 *** |

| (0.0126) | (0.0156) | (0.00775) | (0.0122) | |

| Δ Liquidity | −0.136 * | −0.282 * | 0.00226 | −0.0104 |

| (0.0710) | (0.148) | (0.0205) | (0.00769) | |

| Δ ZTD | 0.500 * | 0.502 ** | 0.106 | 0.992 *** |

| (0.256) | (0.250) | (0.156) | (0.121) | |

| α0 | 0.0465 *** | −0.0355 *** | 0.0319 *** | 0.0321 *** |

| (green premium) | (0.00279) | (0.00509) | (0.00145) | (0.00375) |

| Observations | 36,673 | 14,579 | 22,094 | 3070 |

| R-squared | 0.208 | 0.216 | 0.193 | 0.625 |

| (1) | (3) | (5) | |

|---|---|---|---|

| Variable | TOBIT Public Issuers Sample | TOBIT Private Issuers Sample | TOBIT Private Issuers and Non-Verified Bonds |

| Δ Coupon | −122.430 *** | −10.79 ** | −1.082 *** |

| (2570) | (4.425) | (68.73) | |

| Δ Amount | 0.979 *** | 0.0481 *** | 2.746 *** |

| (0.0116) | (0.00156) | (0.0716) | |

| Δ Maturity | 0.149 *** | 0.115 *** | 0.363 *** |

| (0.00312) | (0.00124) | (0.0136) | |

| Δ σ | −0.188 *** | −0.112 *** | −0.252 *** |

| (0.0148) | (0.00454) | (0.0115) | |

| Δ Liquidity | −0.0900 *** | 0.000692 | −0.0102 |

| (0.0232) | (0.00861) | (0.00793) | |

| Δ ZTD | 0.194 *** | 0.122 *** | 0.764 *** |

| (0.0456) | (0.0267) | (0.0987) | |

| α0 | −0.0310 *** | 0.0317 *** | 0.0332 *** |

| (green premium) | (0.00383) | (0.00122) | (0.00372) |

| Observations | 14,579 | 22,094 | 3070 |

| Sigma | 0.471 *** | 0.181 *** | 0.107 *** |

| (0.00803) | (0.00216) | (0.00177) |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bachelet, M.J.; Becchetti, L.; Manfredonia, S. The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability 2019, 11, 1098. https://doi.org/10.3390/su11041098

Bachelet MJ, Becchetti L, Manfredonia S. The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability. 2019; 11(4):1098. https://doi.org/10.3390/su11041098

Chicago/Turabian StyleBachelet, Maria Jua, Leonardo Becchetti, and Stefano Manfredonia. 2019. "The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification" Sustainability 11, no. 4: 1098. https://doi.org/10.3390/su11041098

APA StyleBachelet, M. J., Becchetti, L., & Manfredonia, S. (2019). The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability, 11(4), 1098. https://doi.org/10.3390/su11041098