1. Introduction

As the backbone of economic activities, it is widely recognized that the transport sector has a key role in countries’ economic development; in 2015, the transport sector accounted for 33.1% of the total European Union-28 (EU-28) primary energy consumption, being equivalent to 359 Mtoe [

1]. The European Commission (EC) has recently issued its “long-term vision for a prosperous, modern, competitive, and climate neutral economy”, aiming at confirming the commitment to lead in global climate action towards net-zero greenhouse gas emissions by 2050 [

2]. The above-mentioned document contains interesting information regarding the current and the expected relative importance of each mode of transport, with respect to primary energy consumption (

Table 1).

In spite of the dominant role of the road sector, rail and aviation account for a significant share of the activities both for passenger as well as for freight. In 2015, rail accounted for 7.6% of the total EU passenger transport activity and for 12% of freight transport activity (

Table 2), while aviation had a share of 10% on passengers with a negligible share of freight. Since 2014, the aviation sector has been showing a stable growth, after the 2009 contraction corresponding to the economic crisis [

3]. The total number of passengers that were travelling by air in the EU in 2016 has been estimated in 973 million, with 17% of them moving within domestic airports (

Table 3). The European Aviation Environmental Report (EAER) [

4] presented an increase in passenger number of about 40% in 2017, as compared with 2005. In the same report, a base case future scenario forecasts that the total flights using EU and European Free Trade Area (EFTA) airports will increase from 9.5 million in 2017 to 13.6 million in 2040. The rail sector has been facing different trends when compared to aviation; passenger share in 2012 was 7.6% of the total passenger-km and, as previously shown, it remained stable in 2015 [

5]. The High Speed Rail (HSR) segment shows a remarkable growth, accounting for 84% of the increment in passenger activity between 2005 and 2015, and for 29% of total passenger rail activity in 2015 [

6].

Air and rail transport compete on EU domestic medium-haul trips (around 500 km) [

8,

9,

10], but their specific energy consumption and, consequently, their emission profiles, strongly differ. Aviation specific passenger kilometer emissions are still typically higher than rails‘, even if rapid technological advances in the sector have been helping in mitigating the existing gap. In order to see the effects of these technological advances, all the sector players—from manufacturers to operators—must be early adopters of Best Available Technologies (BAT): the average age of the fleet is a key point. Despite the availability of new aircraft models, such as the A320neo and B737 MAX families, the European fleet—albeit young—is getting slightly older: the mean aircraft age has increased from 10.3 years old in 2014 to 10.8 years old in 2017 [

4].

With no attempt to single out the contribution of EU domestic air traffic due to reporting systems, EU aviation has more than doubled its emissions since 1990 [

4], totaling 13.3% of the EU28 greenhouse gas (GHG) transport emissions in 2017 [

11]: this is the second most important source of transport GHG emissions after road. This happens despite the already occurred reduction in fuel burnt per passenger kilometer.

Two factors have contributed in the same period in lowering the environmental impact of the rail sector: enhanced energy efficiency in the rolling stock and a significant reduction in the use of oil products as energy source. According to International Energy Agency (IEA) and International Union of railways (UIC), the energy consumption per pkm decreased by 18.2% in the decade 2005 to 2015, and energy freight tkm decreased by 19.2% in the same period [

5,

6]. Due to the greening of the electrical production system, the corresponding GHG emissions per decreased by 38.1% (per passenger-km) and the freight by the 31.2% (per tonne-km).

The paper estimates the emission profiles for aviation and HSR on two intra-EU selected routes; these case studies are proposed for comparing the GHG emissions of the two modes of transport. The value of measuring this differential impact deals with the growing concern regarding the forecast for aviation deployment in the near-medium term, which is being expected to worsen the current sector impact. As Biomass Derived Fuels (BDF) use is claimed to be able to mitigate aviation GHG emissions, consequently filling the existing gap with other modes of transport, this paper presents the current EU production state of play, with the proposal of estimating the actual mitigation potential. In the last section, the results of a cost/benefit analysis are presented, aiming to identify alternative strategies to BDF, for achieving the goal of mitigating aviation environmental impact.

2. Materials and Methods

In this section, the methodology that is used to define the specific GHG emissions for HSR and aviation, on two selected medium-haul routes, is presented. This analysis is a follow-up of a previous work [

12].

2.1. Cities-Pairs Definition and Distances

In order to measure the potential for BDF to mitigate aviation emissions, a comparison with HSR is proposed by means of two case studies. Two intra-EU cities pairs have been selected as representative examples for the comparison of the two transport modes. Four specific airports have been chosen in order to connect the cities-pairs, mainly for their relative proximity, both in terms of distance and for flight duration: no more than one and a half hour:

LHE: London Heathrow (UK): the busiest airport in the EU, with a total of 78.0 million passengers carried in 2017;

CDG: Paris-Charles de Gaulle (France): the second busiest airport in Europe, with 69.5 million passengers moved in 2017;

FRA: Frankfurt Main (Germany): 64.5 million passengers in 2017; and,

AMS: Amsterdam Schiphol (The Netherlands): 68.5 million passengers in 2017 [

12].

These two routes were already analyzed, among others, in a previous [

13], but in this paper time for commuting has also been added to the comparison.

Table 4 shows the results of the HSR versus aviation comparison in terms of trip duration. The time that is required for reaching the airport from downtown, plus the time from the arrival airport to the city center have been added for aviation to refine the quality of the comparison with HSR, for which stations are often in the very center of the cities. Data have been obtained by comparing the various tools [

13,

14,

15,

16,

17,

18].

2.2. Emissions for Rail Transport

High Speed Rail is powered by electrical energy and the GHG emissions have been calculated on the basis of the carbon intensity of the electric power generation, which is a direct function of the primary energy mix of the country that is crossed by the train during its trip. The carbon intensity of each country has been estimated using Moro et al. [

19], in terms of gCO

2e/kWh for Medium Voltage infrastructure (

Table 5). The specific energy consumption for HSR services can be calculated by defining an average occupancy rate for the specific journey. When considering the European case [

20,

21,

22], a typical occupancy rate of 65% is deemed to be appropriate. According to available studies [

23,

24], a final specific energy consumption of HSR can be set in 0.057 kWh/pkm. With these assumptions as input, it is possible to calculate the specific emissions factor for the routes selected.

The lower specific carbon intensity of the Paris–London route, with respect to the AmsterdamFrankfurt, is due to the lower carbon intensity of France, where nuclear power is still a relevant source in the current mix.

2.3. Emissions for Aviation

In order to estimate the air transport emissions on the identified routes, the aircraft type doing the service has to be taken into account. On the defined distance bands, all below 1000 km, regional Small Jet (SJ)—mostly turboprops—and Narrow Body (NB) aircrafts constitute the typical vectors; today, there is a general trend of reducing the small jets in favor of aircrafts with a higher load capability [

25,

26].

Based on the analyses that were reported in the previous study [

12], in the present work flights among the reference airports have been segmented for the two aircraft types (SJ and NB), and fuel consumption has been calculated using the Corinair database [

27]. The fuel consumption per aircraft type has been estimated for the standard LTO cycle (Take-Off, climb, approach, and taxi-in) adding the cruise phase. Two reference weeks of the yearly traffic have been analyzed: week 24 and week 37, which are typically recognized by airline operators as representative of the overall year [

28,

29]. The CO

2e emissions can be obtained by the fuel consumption—as expressed in kg of Jet A1—using a coefficient of 3.15 for the conversion (according to the EU Emission Trading System (EU ETS) Directive [

30]).

2.4. Comparison over the Emissions Profiles

The comparison of the emission profiles from

Table 6 and

Table 7 clearly highlights the higher impact of aviation as compared with HSR. The sector is fully aware of its impact, thus it has set an aspirational target for its international activities to achieve carbon neutral growth from 2020 onward and cut its overall carbon emissions by 50% by 2050 (as compared to 2005 levels [

31]); no specific target is currently defined for EU. Among the tools that are available today for greening the sector, BDF are a technically available solution, and are here analyzed.

2.5. Biomass Derived Fuel Carbon Intensity

Alternative fuels for aviation, independently from the feedstock that are utilized for their production, have to meet specific quality characteristics in order to be used in commercial flights. The American Society for Testing and Materials (ASTM) is the body that is in charge of issuing the technical norms regulating this aspect; today, the two reference norms are the ASTM D4054 and ASTM D7566 [

32,

33]. The procedures that are contained in the norms do not take into account only the final fuel quality, but the pathway that is used for its production. Currently, six production pathways are certified (see

Table 8). These bio-derived jet fuels are drop-in: they can be directly blended with fossil derived Jet A1. For the time being, there are other pathways in the pipeline for ASTM certification.

Defining the maturity level of the available production pathways, either from a technological or from a commercial point of view, is challenging and, despite the great dynamism of the sector, hardly any significant ASTM certified alternative fuels batches are today supplied at the commercial scale [

41]. Among the already certified pathways, HEFA shows the highest maturity level [

42], as a relevant amount of production capacity is already installed, being currently capable of supplying fuel for commercial flights. the maturity level for the Fischer–Tropsch conversion process is less clear, despite having been the first to get ASTM certification, today this technology has not yet reached a truly commercial scale. Alcohol to Jet pilot plants are today supplying, even at a very small scale, fuel for commercial flights [

41], demonstrating an interesting maturity level. The production of alternative aviation fuels from sugars appears today as a promising technology and pilot plants are supporting pilot commercial initiatives [

43].

In order to define an average GHG saving potential, from the use of BDF in aviation, the technologies and the production pathways that are used in EU-28 need to be assessed. Europe today relies on a significant number of commercial plants, which are currently in operation; the most common technology, in terms of installed nominal capacity, is the HEFA process. HEFA is obtained from Hydrogenated Vegetable Oils (HVO)—which is used in road transport as an alternative to biodiesel—with an additional isomerization step. According to a recent work from Prussi et al. [

44], the maximum aviation fuel technical potential ranges from 350 to 830 kt/yr, depending on the assumptions that are used for plants setting and market demand. A significant increase can be expected for the medium term, as co-processing and other new pathways may unlock larger potential.

In order to define a potential GHG saving by using BDF from EU production, a 2020 scenario has been defined. Based on the current status of the technological deployment—as shown in

Table 9—it can be assumed that, in 2020, EU production will be mainly constituted by HEFA, with a minor share of ATJ and FT: we set a relative share of 80% for HEFA, 15% for ATJ and 5% for FT. This scenario results in an ideal EU average BDF blend. An average GHG saving can be associated to such a theoretical blend, on the basis of the technologies that are used for production but also as a function of the feedstocks that are used to supply the processes. When considering the current market values as well as the indications from RED-II,

Table 9 reports the proposed shares of feedstocks considered per production pathway—based on the defined scenario, the average EU BDF GHG saving can be calculated.

In spite of the high expectation for FT from lignocellulosic residues to significantly contribute in medium-term to EU production, HEFA is currently dominating the market. In the near term, the feedstocks for HEFA are expected to originate from waste or residual streams, namely UCO and tallow. While palm oil has gained a bad environmental reputation on the EU market, the Palm Fatty Acid Distillate (PFAD) could be widely used for biofuels production. PFAD is already widely used by industry, such as for feed production—an extensive use in aviation may lead to indirect effects, due to the displacement of this feedstock forcing, for instance, the feeding industry to use more vegetable oil to meet its demand. The real displacement effect is hard to be estimated and models that are proposed appear today unable to supply reliable results. For the time being, PFAD is still a suitable feedstock for companies producing biofuels, as Member States are able to classify this material as a waste.

3. Results

Based on the scenario and assumptions described, the theoretical EU production BDF—in 2020—would allow for a saving of 59 gCO

2e/MJ (

Table 10): 66% as compared to the reference 89 gCO

2e/MJ of the fossil Jet A1.

In order to calculate the potential for GHG saving per trip, a BDF blending rate with fossil kerosene has to be defined. All the pathways considered for the production of this EU typical BDF can be theoretically blended up to 50%; this is the maximum share allowed by ASTM certification and can be considered as a really high share, that is unlikely to be reached in real-world operations particularly with respect to its management at existing airport infrastructures.

At the airport level, a lower blending rate can be more easily and realistically managed. In spite of this practical consideration (mainly cost related), a blend of at least several perceptual points needs to be considered to have a measurable impact. For the purposes of this paper, and when considering the plans that were outlined by specific EU airport initiatives, a blending rate of 3% has been analyzed.

The 3% blend could be a viable solution for an airport willing to introduce BDF in its infrastructure; nevertheless, despite this ease of implementation, the environmental measurable benefits would be really limited. Conversely, for both the analyzed routes, when a 50% blend rate is used, the emissions drop significantly, to 94 and 77 gCO

2e per pkm, respectively. Despite this relevant reduction, as shown in

Table 11, even a 50% blend of BDF does not allow to fill the gap between the emission profiles of flights on selected routes, as compared to the HSR emission profile.

4. Discussion

Cost-benefit Comparison for Mitigating GHG from Aviation

BDF has the potential to mitigate the GHG emissions of the aviation sector; however, the costs of this option constitute a barrier to real-market deployment [

45]. To estimate the cost of saving CO

2e by using BDF, it is first necessary to define the differential cost with respect to commercial fossil derived Jet-A1; according to the International Air Transport Association [

46], Jet-A1 fuel price today costs around 650 €/t. The variability of the costs for BDF, instead, is less certain, not only because most of the pathways are not fully commercial, but also because feedstocks are often subject to high price volatility. The SGAB group [

47] reports HEFA production costs that range from 80–90 €/MWh (22–25 €/GJ), and aviation alternative fuel via FT in 110–140 €/MWh (31–39 €/GJ). A recent JRC study [

48] presents the total production costs for conventional and advanced biofuel pathways for the road sector. The JRC values, which are in line with SGAB figures, can be used to calculate the cost of the average BDF for our scenario: according to the limited data available in literature [

49], a 10% cost for upgrading to jet fuel has been added.

Table 12 shows the costs for specific pathways and technologies; while considering the relative share of each pathway, as already presented in

Table 9; the final production costs for an ideal EU BDF for aviation equals 1124 €/t.

The emissions from Jet-A1 are equal to 3.8 tCO2e/tJetA1, while BDF value 1.3 tCO2e/tBDF (66% saving). Each tonne of Jet-A1 replaced by BDF allows for saving 2.5 tCO2e and the cost of this saving is equal to the difference in fuels prices: the difference between Jet-A1 and BDF is around 470 €/t—and consequently, the cost saved results in 186 €/tCO2e.

As alternatives to BDF, other options can be considered to mitigate the emissions from the aviation sector: for example, market-based measures, such as emission trading and carbon offsetting. Because of the above-mentioned enhanced cost of the use of BDF, market based measures are explored below as an economical way to reduce the emissions of aviation.

In 2005, the European Union launched the EU Emissions Trading System (EU-ETS) as a pilot of its strategy for cutting emissions of carbon dioxide (CO

2) and other greenhouse gases at least cost [

50]. Emission allowances are ‘currencies’ in the EU ETS and the limit on their total number available should define their value. Companies have to balance part of their emissions (tonnes of CO

2e or the equivalent amount for nitrous oxide, N

2O, or perfluorocarbon emissions, PFCs), by acquiring allowances that are auctioned within the EU ETS [

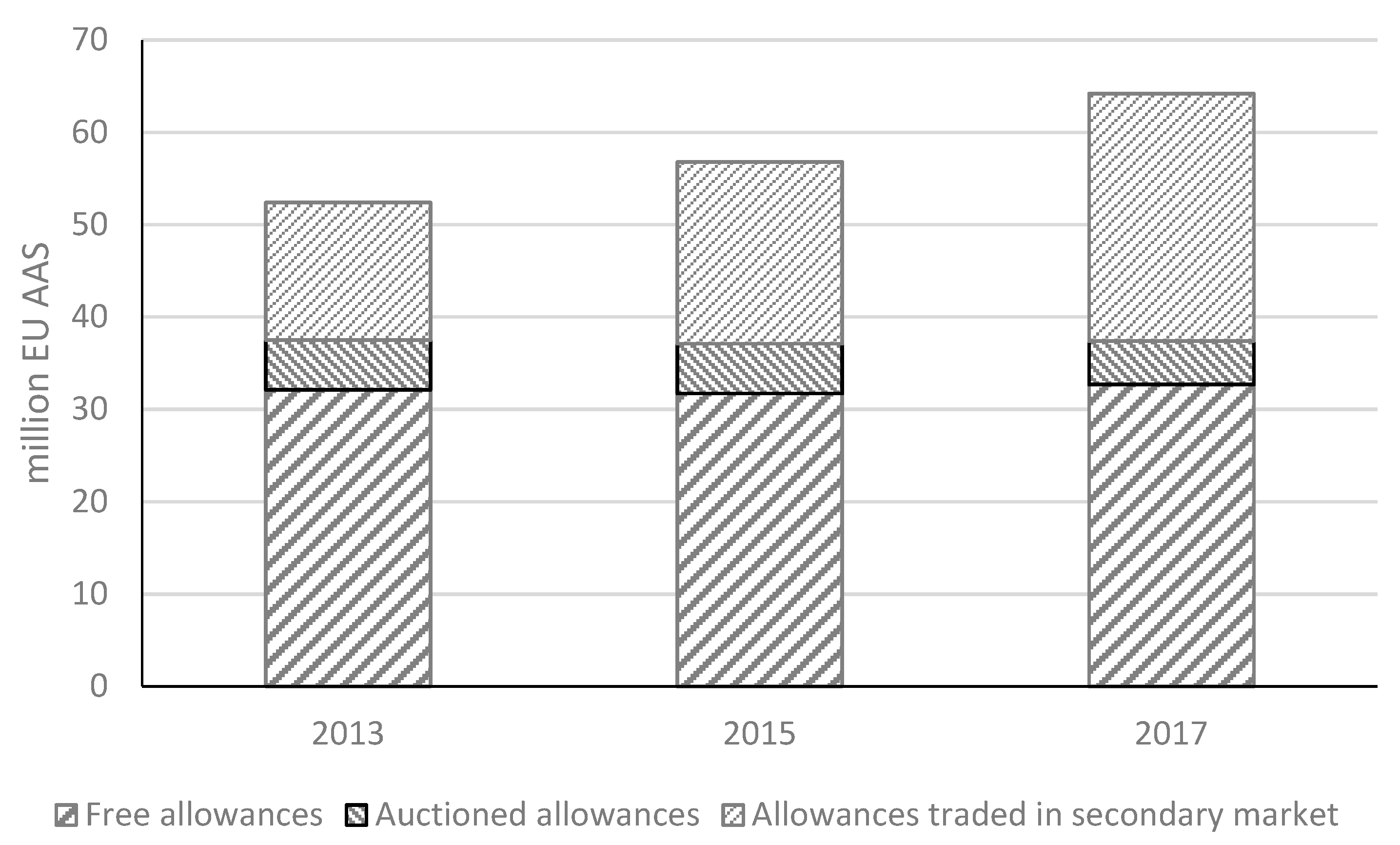

50]. Aviation activities have been included in the EU ETS since 2012 but until 31 December 2023 the EU ETS will only apply to flights between airports that are located in the European Economic Area (EEA) with a cap for the total allowances. The cap for the whole 2013–2020 period has been set at 210 million aviation allowances per year [

4]; this is equivalent to 95% of the aviation emissions for the reference period 2004–2006. For the time being, 82% of the aviation allowances are granted for free to aircraft operators, 15% of aviation allowances are auctioned, while the remaining 3% of aviation allowances are held in a special reserve for later attribution to new market entrants and fast-growing operators. Firms are incentivized to become more energy efficient because they can then sell their emissions permits on the secondary market.

Figure 1 summarizes the aviation CO

2e emissions under EU ETS. The EU ETS allowances price varied between 4–6 €/tCO

2e during the 2013–2017 period, while in the course of 2018, their value rose above 20 €/tCO

2e [

51].

In addition to the EU ETS, the EU Member States can participate, on voluntary basis, in the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA): an attempt to address international aviation emissions. CORSIA was launched in 2016, with the aim of offsetting international aviation CO2e emissions—above the 2020 levels, by means of credits acknowledged at global level. CORSIA operates on a route-based approach: a route is covered by CORSIA offsetting obligations if the state of departure and the state of destination are participating in the scheme. Offsetting credits represent the certification that a tonne of CO2e has been reduced, in comparison with a scenario without CORSIA.

In order to give EU Member States the possibility to participate in ETS and CORSIA, in December 2017, the Parliament and the Council agreed to prolong the derogation at ETS for extra-EEA flights—until 31 December 2023. Emissions trading systems (ETS) and offsetting schemes (CORSIA) aim to address the need of reducing aviation emissions but they differ in the way that they operate. CORSIA has a larger geographical scope when compared to EU ETS. Concerns and criticisms have been moved for this kind of tools, as they may tend to divert the focus from reducing emissions to trading on emissions. On the other hand, BDF are a direct way to try to reduce emissions, but their costs—per tonne of saved CO2e—are today still significantly higher than the ETS allowances.

5. Conclusions

In this paper, the emission profiles of aviation and HSR on two intra-EU selected routes (London–Paris and Frankfurt–Amsterdam) have been compared. The aviation mode of transport shows higher GHG emissions when compared with rail. For the route London-Paris the GHG emissions resulted in 18.0 and 143 gCO2e/pkm for HRS and aviation, respectively. The corresponding figures for the route Frankfurt-Amsterdam were 33.6 and 116 gCO2e/pkm.

Biomass Derived Fuels could be considered as a direct way to reduce aviation GHG emissions, and the potential impact of their use has been analyzed. A theoretical EU BDF blend has been defined on the basis of EU production capacity in 2020. For both of the routes analyzed, when a 50% BDF and fossil jet-A1 blend is used, the emissions drop significantly, to 94 and 77 gCO2e/pkm, respectively. Despite this relevant reduction, even a 50% blend of BDF does not allow for fill the aviation gap, as compared to the HSR emission profile.

Moreover, the final production cost for an ideal EU BDF for aviation is expected to be higher than 1100 €/t, making this option unattractive in economic terms. The cost per tonne of saved CO2e has been estimated at 186 €/tCO2e.

In near future, the limitation of the number of the allowances, with the consequent expected rise in their price will act as an incentive for the aviation companies to consider BDF as an alternative means to reduce emissions. Nevertheless, for the time being, while taking into account the current price per tonne of CO2e in the EU-ETS (around 20 €/tCO2e), it could be concluded that EU ETS is still a more viable option for the sector.

{kind=link}