Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies

Abstract

1. Introduction

2. Literature Review

2.1. The Growing Attention to Sustainability Reporting

2.2. Sustainability Reporting in Italy and Germany

2.3. Mandatory Disclosure of Nonfinancial Information in the EU

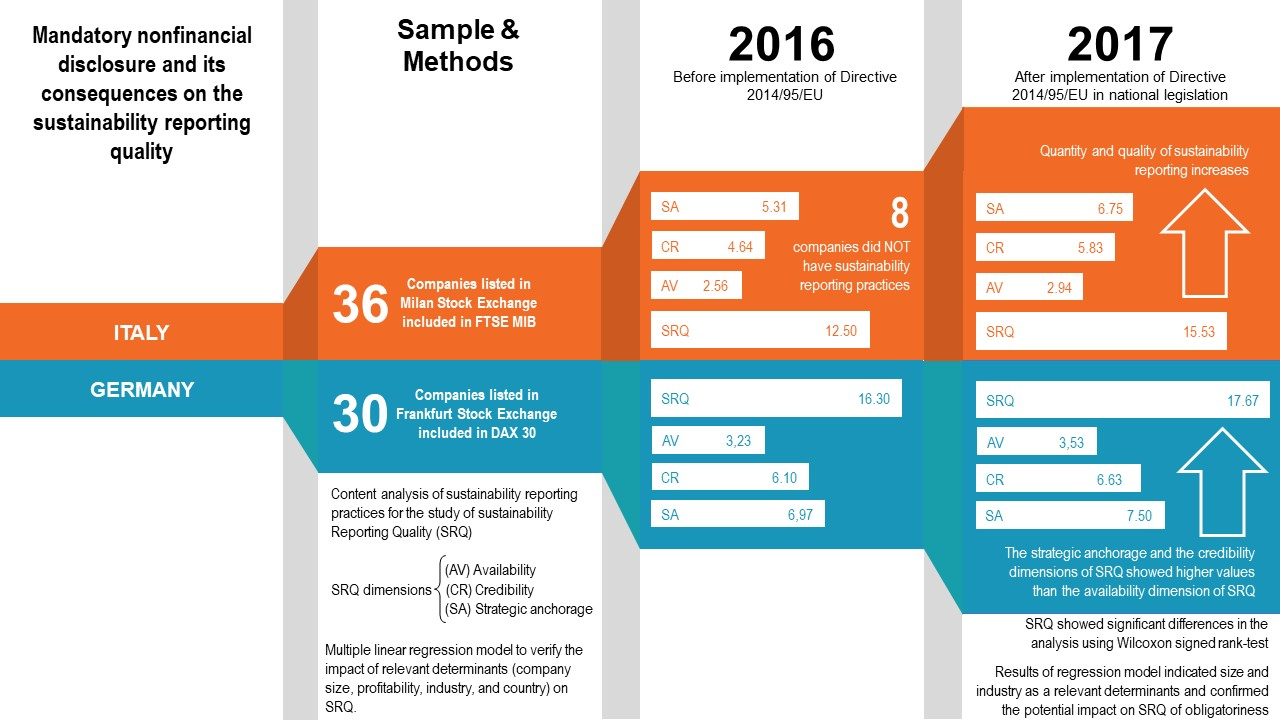

3. Materials and Methods

3.1. Research Design

- Has SRQ improved since the implementation of the new regulatory requirements for mandatory NFD?

- Does the SRQ of companies in Italy and Germany differ since the implementation of the new regulatory requirements for mandatory NFD?

- Is there evidence of harmonization between the NFD of companies in Italy and Germany since the implementation of new regulatory requirements?

3.2. Evaluation Scale

- Availability (indicators AV): the first dimension aims to understand whether sustainability reports are available to all possible stakeholders, including through nontechnical channels such as brochures or social media. The “universal” destination of sustainability reporting requires an effort to use different channels to reach different stakeholders, including those who do not have technical knowledge or free access to financial databases. Previous research has stated that this dimension of SRQ is crucial because of the natural tendency of sustainability reports to build good relationships with stakeholders.

- Credibility (indicators CR): the second dimension—largely recognized by previous research as fundamental in defining SRQ [22] and as being connected to the recognition of stakeholders’ concerns related to the reliability of sustainability reports [150]—concerns the content of sustainability reports and the possibility of immediately verifying the quality of the information included in the reports. This dimension is identified from the perspective of each reader of the report and concerns the methodology adopted by the corporation in constructing the report. This dimension could be related to some of the goals pursued by the legislative reform in relation to NFD, for example, the harmonization of nonfinancial information disclosed by companies and the comparability of performance related to environmental, social, and governance issues among large European corporations.

- Strategic anchorage (indicators SA): the third dimension is related to the nexus between reporting and strategic policies on sustainability and CSR. This third group of indicators aims to understand whether reporting is an autonomous and occasional process or part of a wider sustainable strategy that also considers global challenges (e.g., United Nations Sustainable Development Goals) and internationally acknowledged tools for sustainability.

3.3. Sample of Analysis

4. Results and Discussion

4.1. Descriptive Statistics

4.2. SRQ Differences before and after Implementing the EU Directive

4.3. Determinants of SRQ and Obligatoriness of NFD

5. Conclusions and Limitations

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Italian Companies | German Companies |

|---|---|

| A2A | Adidas AG |

| Atlanta | Allianz SE |

| Azimut Holding | BASF SE |

| Banca Generali | Bayer AG |

| Bper Banca | Beiersdorf AG |

| Brembo | Bayerische Motoren Werke AG |

| Buzzi Unicem | Commerzbank AG |

| Campari | Continental AG |

| Cnh Industrial | Covestro AG |

| Enel | Daimler AG |

| Eni | Deutsche Boerse AG |

| Exor | Deutsche Bank AG |

| Ferrari | Deutsche Post AG |

| Fiat Chrysler Automobiles | Deutsche Telekom AG |

| Generali | E.ON SE |

| Intesa Sanpaolo | Fresenius Medical Care AG & Co KGaA |

| Italgas | Fresenius SE & Co KGaA |

| Leonardo | HeidelbergCement AG |

| Luxottica | Henkel AG & Co KGaA |

| Mediaset | Infineon Technologies AG |

| Mediobanca | Deutsche Lufthansa AG |

| Moncler | Linde AG |

| Pirelli & C | Merck KGaA |

| Poste Italiane | Muenchener Rückversicherungs-Gesellschaft AG |

| Prysmian | RWE AG |

| Recordati | SAP SE |

| Saipem | Siemens AG |

| Salvatore Ferragamo | Thyssenkrupp AG |

| Snam | Vonovia SE |

| Stmicroelectronics | Volkswagen AG |

| Telecom Italia | |

| Tenaris | |

| Terna—Rete Elettrica Nazionale | |

| Ubi Banca | |

| Unicredit | |

| Unipolsai |

References

- Marston, C.L.; Shrives, P.J. The use of disclosure indices in accounting research: A review article. Br. Account. Rev. 1991, 23, 195–210. [Google Scholar] [CrossRef]

- Beretta, S.; Bozzolan, S. Quality versus Quantity: The Case of Forward-Looking Disclosure. J. Account. Audit. Financ. 2008, 23, 333–376. [Google Scholar] [CrossRef]

- Beattie, V.; McInnes, B.; Fearnley, S. A methodology for analysing and evaluating narratives in annual reports: A comprehensive descriptive profile and metrics for disclosure quality attributes. Account. Forum 2004, 28, 205–236. [Google Scholar] [CrossRef]

- Core, J.E. A review of the empirical disclosure literature: Discussion. J. Account. Econ. 2001, 31, 441–456. [Google Scholar] [CrossRef]

- Grewal, J.; Riedl, E.J.; Serafeim, G. Market Reaction to Mandatory Nonfinancial Disclosure. Manag. Sci. 2019, 65, 3061–3084. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting; Harvard Business School: Boston, MA, USA, 2015. [Google Scholar]

- KPMG; Center for Corporate Governance in Africa; GRI; UNEP. Carrots and Sticks. Sustainability Reporting Policies Worldwide–Today’s Best Practice, Tomorrow’s Trends; KPMG: Amstelveen, The Netherlands; Center for Corporate Governance in Africa: Cape Town, South Africa; GRI: Amsterdam, The Netherlands; UNEP: Nairobi, Kenya, 2013. [Google Scholar]

- KPMG; GRI; UNEP; Center for Corporate Governance in Africa. Carrots Sticks. Global Trends in Sustainability Reporting Regulation and Policy; KPMG: Amstelveen, The Netherlands; Center for Corporate Governance in Africa: Cape Town, South Africa; GRI: Amsterdam, The Netherlands; UNEP: Nairobi, Kenya, 2016. [Google Scholar]

- Jackson, G.; Bartosch, J.; Avetisyan, E.; Kinderman, D.; Knudsen, J.S. Mandatory Non-Financial Disclosure and Its Influence on CSR: An International Comparison. J. Bus. Ethics 2019, 1–20. [Google Scholar] [CrossRef]

- Zeithaml, V.A.; Parasuraman, A.; Berry, L.L. Strategic Positioning on the Dimensions of Service Quality. In Advances in Services Marketing and Management; Swartz, T.A., Bowen, D.E., Brown, S.W., Eds.; JAI Press Inc.: Greenwich, UK, 1992; Volume 2, pp. 207–228. [Google Scholar]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management: A stakeholder perspective. Account. Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- Helfaya, A.; Whittington, M.; Alawattage, C. Exploring the quality of corporate environmental reporting. Account. Audit. Account. J. 2018, 32, 163–193. [Google Scholar] [CrossRef]

- Beck, A.C.; Campbell, D.; Shrives, P.J. Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British-German context. Br. Account. Rev. 2010, 42, 207–222. [Google Scholar] [CrossRef]

- Boesso, G.; Kumar, K. Drivers of corporate voluntary disclosure: A framework and empirical evidence from Italy and the United States. Account. Audit. Account. J. 2007, 20, 269–296. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Hammond, K.; Miles, S. Assessing quality assessment of corporate social reporting: UK perspectives. Account. Forum 2004, 28, 61–79. [Google Scholar] [CrossRef]

- Helfaya, A.; Kotb, A. Environmental Reporting Quality. In Handbook of Research on Green Economic Development Initiatives and Strategies; Erdoğdu, M.M., Arun, T., Ahmad, I.H., Eds.; IGI Global: Hershey, PA, USA, 2016; pp. 625–654. [Google Scholar]

- Whittington, M.; Ekara, A. Assesment of Corporate Reporting Quality: A Review of the Literature. In Proceedings of the European Accounting Association, 36th Annual Congress, Paris, France, 6–8 May 2013. [Google Scholar]

- Van Staden, C.J.; Hooks, J. A comprehensive comparison of corporate environmental reporting and responsiveness. Br. Account. Rev. 2007, 39, 197–210. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. Board gender diversity and sustainability reporting quality. J. Contemp. Account. Econ. 2016, 12, 210–222. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Comyns, B.; Figge, F. Greenhouse gas reporting quality in the oil and gas industry. Account. Audit. Account. J. 2015, 28, 403–433. [Google Scholar] [CrossRef]

- Matuszak, Ł.; Rózańska, E. CSR Disclosure in Polish-Listed Companies in the Light of Directive 2014/95/EU Requirements: Empirical Evidence. Sustainability 2017, 9, 2304. [Google Scholar] [CrossRef]

- Sierra-Garcia, L.; Garcia-Benau, M.A.; Bollas-Araya, H.M. Empirical Analysis of Non-Financial Reporting by Spanish Companies. Adm. Sci. 2018, 8, 29. [Google Scholar] [CrossRef]

- Helfaya, A.; Whittington, M. Does designing environmental sustainability disclosure quality measures make a difference? Bus. Strateg. Environ. 2019, 28, 525–541. [Google Scholar] [CrossRef]

- EU Commission. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014-amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Official J. Eur. Un. 2014, 330, 1–9. [Google Scholar]

- Braam, G.J.M.; Uit De Weerd, L.; Hauck, M.; Huijbregts, M.A.J. Determinants of corporate environmental reporting: The importance of environmental performance and assurance. J. Clean. Prod. 2016, 129, 724–734. [Google Scholar] [CrossRef]

- Fifka, M.S. Corporate Responsibility Reporting and its Determinants in Comparative Perspective a Review of the Empirical Literature and a Meta-analysis. Bus. Strateg. Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

- Kuzey, C.; Uyar, A. Determinants of sustainability reporting and its impact on firm value: Evidence from the emerging market of Turkey. J. Clean. Prod. 2017, 143, 27–39. [Google Scholar] [CrossRef]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting; KPMG: Amstelveen, The Netherlands, 2017. [Google Scholar]

- Ott, H.; Wang, R.; Bortree, D. Communicating Sustainability Online: An Examination of Corporate, Nonprofit, and University Websites. Mass Commun. Soc. 2016, 19, 671–687. [Google Scholar] [CrossRef]

- Adams, C.A.; Muir, S.; Hoque, Z. Measurement of sustainability performance in the public sector. Sustain. Account. Manag. Policy J. 2014, 5, 46–67. [Google Scholar] [CrossRef]

- Domingues, A.R.; Lozano, R.; Ceulemans, K.; Ramos, T.B. Sustainability reporting in public sector organisations: Exploring the relation between the reporting process and organisational change management for sustainability. J. Environ. Manag. 2017, 192, 292–301. [Google Scholar] [CrossRef]

- Adams, C.A.; Hill, W.Y.; Roberts, C. Corporate Social Reporting Practices in western Europe: Legitimating Corporate Behavior? Br. Acc. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Fekrat, M.A.; Inclan, C.; Petroni, D. Corporate Disclosures: Competitive Disclosure Hypothesis Using 1991 Annual Report Data. Int. J. Account. 1996, 31, 175–195. [Google Scholar] [CrossRef]

- Williams, S.M.; Ho Wern Pei, C.-A. Corporate social disclosures by listed companies on their web sites: An international comparison. Int. J. Account. 1998, 34, 389–419. [Google Scholar] [CrossRef]

- Beets, D.S.; Souther, C.C. Corporate environmental reports: The need for standards and an environmental assurance service. Account. Horiz. 1999, 13, 129–145. [Google Scholar] [CrossRef]

- Braam, G.J.M.; Peeters, R. Corporate Sustainability Performance and Assurance on Sustainability Reports: Diffusion of Accounting Practices in the Realm of Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 164–181. [Google Scholar] [CrossRef]

- Dando, N.; Swift, T. Transparency and Assurance: Minding the Credibility Gap. J. Bus. Ethics 2003, 44, 195–200. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation. Bus. Strateg. Environ. 2010, 19, 182–198. [Google Scholar] [CrossRef]

- Simnett, R.; Vanstraelen, A.; Chua, W.F. Assurance on Sustainability Reports: An International Comparison. Account. Rev. 2009, 84, 937–967. [Google Scholar] [CrossRef]

- Smith, J.; Haniffa, R.; Fairbrass, J. A Conceptual Framework for Investigating “Capture” in Corporate Sustainability Reporting Assurance. J. Bus. Ethics 2011, 99, 425–439. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Deegan, C. Introduction The legitimising effect of social and environmental disclosures—A theoretical foundation. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Hess, D.; Dunfee, T.W. The Kasky-Nike Threat to Corporate Social Reporting: Implementing a Standard of Optimal Truthful Disclosure as a Solution. Bus. Ethics Q. 2007, 17, 5–32. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Corporate environmental disclosure, financial markets and the media: An international perspective. Ecol. Econ. 2008, 64, 643–659. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Res. 2001, 31, 405–440. [Google Scholar]

- Mills, D.L.; Gardner, M.J. Financial profiles and the disclosure of expenditures for socially responsible purposes. J. Bus. Res. 1984, 12, 407–424. [Google Scholar] [CrossRef]

- Plumlee, M.; Brown, D.; Hayes, R.M.; Marshall, R.S. Voluntary environmental disclosure quality and firm value: Further evidence. J. Account. Public Policy 2015, 34, 336–361. [Google Scholar] [CrossRef]

- Marin, L.; Ruiz, S.; Rubio, A. The role of identity salience in the effects of corporate social responsibility on consumer behavior. J. Bus. Ethics 2009, 84, 65–78. [Google Scholar] [CrossRef]

- Guidry, R.P.; Patten, D.M. Voluntary disclosure theory and financial control variables: An assessment of recent environmental disclosure research. Account. Forum 2012, 36, 81–90. [Google Scholar] [CrossRef]

- Boyer-Allirol, B. Faut-il mieux reglementer le reporting extra financier pour ameliorer sa prise en compte par les investisseurs? Comptab. Sans Front. Fr. Connect. 2013. [Google Scholar]

- Lewis, J.K. Corporate Social Responsibility/Sustainability Reporting Among the Fortune Global 250: Greenwashing or Green Supply Chain? Entrep. Bus. Econ. 2016, 1, 347–362. [Google Scholar]

- Mahoney, L.S.; Thorne, L.; Cecil, L.; LaGore, W. A research note on standalone corporate social responsibility reports: Signaling or greenwashing? Crit. Perspect. Account. 2013, 24, 350–359. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Thorne, L.; Mahoney, L.S.; Manetti, G. Motivations for issuing standalone CSR reports: A survey of Canadian firms. Account. Audit. Account. J. 2014, 27, 686–714. [Google Scholar] [CrossRef]

- Wilson, M. A Critical Review of Environmental Sustainability Reporting in the Consumer Goods Industry: Greenwashing or Good Business? J. Manag. Sustain. 2013, 3, 1–13. [Google Scholar] [CrossRef]

- Delmas, M.A.; Burbano, V.C. The Drivers of Greenwashing. Calif. Manag. Rev. 2011, 54, 64–87. [Google Scholar] [CrossRef]

- Laufer, W.S. Social Accountability and Corporate Greenwashing. J. Bus. Ethics 2003, 43, 253–261. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Greenwash: Corporate Environmental Disclosure under Threat of Audit. J. Econ. Manag. Strateg. 2011, 20, 3–41. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M.; Roberts, R.W. Corporate political strategy: An examination of the relation between political expenditures, environmental performance, and environmental disclosure. J. Bus. Ethics 2006, 67, 139–154. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental Reporting and its Relation to Corporate Environmental Performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- De Villiers, C.; van Staden, C.J. Can less environmental disclosure have a legitimising effect? Evidence from Africa. Account. Organ. Soc. 2006, 31, 763–781. [Google Scholar] [CrossRef]

- Hummel, K.; Schlick, C. The relationship between sustainability performance and sustainability disclosure—Reconciling voluntary disclosure theory and legitimacy theory. J. Account. Public Policy 2016, 35, 455–476. [Google Scholar] [CrossRef]

- Leuz, C.; Wysocki, P.D. Economic Consequences of Financial Reporting and Disclosure Regulation: A Review and Suggestions for Future Research. SSRN Electron. J. 2008, 79, 1–90. [Google Scholar] [CrossRef]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef]

- Lock, I.; Seele, P. The credibility of CSR (corporate social responsibility) reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef]

- Ferri, L.M. The influence of the institutional context on sustainability reporting. A cross-national analysis. Soc. Responsib. J. 2017, 13, 24–47. [Google Scholar] [CrossRef]

- Cantele, S. The trend of sustainability reporting in Italy: Some evidence from the last decade. Int. J. Sustain. Econ. 2014, 6, 381–405. [Google Scholar] [CrossRef]

- Patelli, L.; Prencipe, A. The relationship between voluntary disclosure and independent directors in the presence of a dominant shareholder. Eur. Account. Rev. 2007, 16, 5–33. [Google Scholar] [CrossRef]

- Prencipe, A. Proprietary Costs and Determinants of Voluntary Segment Disclosure: Evidence from Italian Listed Companies. Eur. Account. Rev. 2004, 13, 319–340. [Google Scholar] [CrossRef]

- Rossi, A.; Tarquinio, L. An analysis of sustainability report assurance statements Evidence from Italian listed companies. Manag. Audit. J. 2017, 32, 578–602. [Google Scholar] [CrossRef]

- Gavana, G.; Gottardo, P.; Moisello, A.M. Do customers value CSR disclosure? Evidence from Italian family and non-family firms. Sustainability 2018, 10, 1642. [Google Scholar] [CrossRef]

- Perrini, F. The Practitioner’s Perspective on Non-Financial Reporting. Calif. Manag. Rev. 2006, 48, 73–103. [Google Scholar] [CrossRef]

- Mio, C. Corporate social reporting in Italian multi-utility companies: An empirical analysis. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 247–271. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, F.; Cosma, S.; Leopizzi, R.; Pizzi, S. Directive 2014/95/EU: Are Italian Companies Already Compliant? Sustainability 2017, 9, 1385. [Google Scholar] [CrossRef]

- Costa, E.; Agostini, M. Mandatory Disclosure about Environmental and Employee Matters in the Reports of Italian-Listed Corporate Groups. Environ. Account. J. 2016, 36, 10–33. [Google Scholar] [CrossRef]

- Gulenko, M. Mandatory CSR reporting—literature review and future developments in Germany. In NachhaltigkeitsManagementForum| Sustainability Management Forum; Springer: Berlin/Heidelberg, Germany, 2018; Volume 26, pp. 3–17. [Google Scholar] [CrossRef]

- Saenger, I. Disclosure and Auditing of Corporate Social Responsibility Standards: The Impact of Directive 2014/95/EU on the German Companies Act and the German Corporate Governance Code. In Corporate Governance Codes for the 21st Century; Springer International Publishing: Cham, Germany, 2017; pp. 261–273. [Google Scholar]

- Scheuch, A. Soft Law Requirements with Hard Law Effects? The Influence of CSR on Corporate Law from a German Perspective. In Globalisation of Corporate Social Responsibility and Its Impact on Corporate Governance; Springer International Publishing: Cham, Germany, 2018; pp. 203–229. [Google Scholar]

- Stawinoga, M. Die Richtlinie 2014/95/EU und das CSR-Richtlinie-Umsetzungsgesetz–Eine normative Analyse des Transformationsprozesses sowie daraus resultierender Implikationen für die Rechnungslegungs-und Prüfungspraxis. Nachhalt. Sustain. Manag. Forum 2017, 25, 213–227. [Google Scholar]

- Fifka, M.S. Einführung-Nachhaltigkeitsberichterstattung: Eingrenzung Eines Heterogenes Phänomen; Springer: Berlin/Heidelberg, Germany, 2014; pp. 1–18. [Google Scholar]

- Kirchhoff. Nachhaltigkeitsberichterstattung im Wandel; Springer: Hamburg, Germany, 2017. [Google Scholar]

- Blankenagel, L. CSR-Berichte als Kommunikationsinstrument der DAX-Unternehmen: Eine Analyse der Ist-Situation und die daraus resultierenden Handlungsempfehlungen; VDM Verlag Dr. Müller: Saarbrücken, Germany, 2007. [Google Scholar]

- Cormier, D.; Magnan, M.; Van Velthoven, B. Environmental Disclosure Quality in Large German Companies: Economic Incentives, Public Pressures or Institutional Conditions? Eur. Account. Rev. 2005, 14, 3–39. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef]

- Verbeeten, F.H.M.; Gamerschlag, R.; Möller, K. Are CSR disclosures relevant for investors? Empirical evidence from Germany. Manag. Decis. 2016, 54, 1359–1382. [Google Scholar] [CrossRef]

- Quick, R.; Knocinski, M. Nachhaltigkeitsberichterstattung—Empirische Befunde zur Berichterstattungspraxis von HDAX-Unternehmen. J. Bus. Econ. 2006, 76, 615–650. [Google Scholar] [CrossRef]

- Gruner, M. Der Integrierte Nachhaltigkeitsbericht: Eine Studie zur Nachhaltigkeitsberichterstattung in Den Geschäftsberichten der DAX 30 Unternehmen; AV Akademikerverlag: Saarbrücken, Germany, 2011. [Google Scholar]

- Zimara, V.; Eidam, S. The benefits of social sustainability reporting for companies and Stakeholders-Evidence from the German chemical industry. J. Bus. Chem. 2015, 12, 85–103. [Google Scholar]

- Stibbe, R.; Voigtländer, M. Corporate sustainability in the German real estate sector. J. Corp. Real Estate 2014, 16, 239–251. [Google Scholar] [CrossRef]

- Hubbard, G. The Quality of the Sustainability Reports of Large International Companies: An Analysis. Int. J. Manag. 2011, 28, 824–848. [Google Scholar]

- Fifka, M.S. Corporate Citizenship in Deutschland und den USA Gemeinsamkeiten und Unterschiede im Gesellschaftlichen Engagement von Unternehmen und das Potential Eines Transatlantischen Transfers; Gabler Verlag: Wiesbaden, Germany, 2011. [Google Scholar]

- Blaesing, D. Nachhaltigkeitsberichterstattung in Deutschland und den USA: Berichtspraxis, Determinanten und Eigenkapitalkostenwirkungen; Peter Lang GmbH, Internationaler Verlag der Wissenschaften: Frankfurt, Germany, 2013. [Google Scholar]

- Fifka, M.S.; Drabble, M. Focus and Standardization of Sustainability Reporting—A Comparative Study of the United Kingdom and Finland. Bus. Strateg. Environ. 2012, 21, 455–474. [Google Scholar] [CrossRef]

- Chen, S.; Bouvain, P. Is Corporate Responsibility Converging? A Comparison of Corporate Responsibility Reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

- Freundlieb, M.; Teuteberg, F. Corporate social responsibility reporting—A transnational analysis of online corporate social responsibility reports by market-listed companies: Contents and their evolution. Int. J. Innov. Sustain. Dev. 2013, 7, 1–26. [Google Scholar] [CrossRef]

- Hetze, K.; Bögel, P.M.; Glock, Y.; Bekmeier-Feuerhahn, S. Online-CSR-Kommunikation: Gemeinsamkeiten und Unterschiede börsennotierter Unternehmen in der DACH-Region. Corp. Commun. An Int. J. 2016, 24, 223–236. [Google Scholar] [CrossRef]

- El-Bassiouny, D.; El-Bassiouny, N. Diversity, corporate governance and CSR reporting: A comparative analysis between top-listed firms in Egypt, Germany and the USA. Manag. Environ. Qual. An Int. J. 2018, 30, 116–136. [Google Scholar] [CrossRef]

- Institut für ökologische Wirtschaftsforschung (IÖW). Future E.V. Deutsche Unternehmen vor der CSR-Berichstspflicht: Monitoring zur Nichtfinaziellen Berichterstatung; Institut für ökologische Wirtschaftsforschung: Berlin, Germany, 2018. [Google Scholar]

- Folkens, L.; Schneider, P. Social Responsibility and Sustainability: How Companies and Organizations Understand Their Sustainability Reporting Obligations. In Social Responsibility and Sustainability; Springer: Cham, Germany, 2019; pp. 159–188. [Google Scholar]

- Herzig, C.; Kühn, A.-L. Corporate Responsibility reporting. In Corporate Social Responsibility: Strategy, Communication, Governance; Rasche, A., Morsing, M., Moon, J., Eds.; Cambdrige University Press: Cambridge, UK, 2017; pp. 187–219. [Google Scholar]

- Hess, D. Social Reporting and New Governance Regulation: The Prospects of Achieving Corporate Accountability Through Transparency. Bus. Ethics Q. 2007, 17, 453–476. [Google Scholar] [CrossRef]

- Archel, P.; Fernández, M.; Larrinaga, C. The organizational and operational boundaries of triple bottom line reporting: A survey. Environ. Manag. 2008, 41, 106–117. [Google Scholar] [CrossRef]

- Hahn, R.; Lülfs, R. Legitimizing Negative Aspects in GRI-Oriented Sustainability Reporting: A Qualitative Analysis of Corporate Disclosure Strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar] [CrossRef]

- La Torre, M.; Sabelfeld, S.; Blomkvist, M.; Tarquinio, L.; Dumay, J. Harmonising non-financial reporting regulation in Europe. Meditari Account. Res. 2018, 22, 598–621. [Google Scholar] [CrossRef]

- Hoffmann, E.; Dietsche, C.; Hobelsberger, C. Between mandatory and voluntary: Non-financial reporting by German companies. Nachhalt. Sustain. Manag. Forum 2018, 26, 47–63. [Google Scholar] [CrossRef]

- Kluge, N.; Sick, S. Geheimwirtschaft bei Transparenz zum gesellschaftlichen Engagement? In Zum Kreis der vom CSR Directive Implementation Act potentiell betroffenen Unternehmen; MBF-Report Nr. 27; Hans-Böckler-Stiftung: Düsseldorf, Germany, 2016. [Google Scholar]

- Global Reporting Initiative; CSR Europe. Member State Implementation of Directive 2014/95/EU. A Comprehensive Overview of How Member States Are Implementing the EU Directive on Non-Financial and Diversity Information; Global Reporting Initiative: Amsterdam, The Netherlands; CSR Europe: Bruxelles, Belgium, 2017. [Google Scholar]

- Abbott, W.F.; Monsen, R.J. On the Measurement of Corporate Social Responsibility: Self-Reported Disclosures as a Method of Measuring Corporate Social Involvement. Acad. Manag. J. 1979, 22, 501–515. [Google Scholar]

- Clarkson, P.M.; Fang, X.; Li, Y.; Richardson, G. The relevance of environmental disclosures: Are such disclosures incrementally informative? J. Account. Public Policy 2013, 32, 410–431. [Google Scholar] [CrossRef]

- Da Silva Monteiro, S.M.; Aibar-Guzmán, B. Determinants of environmental disclosure in the annual reports of large companies operating in Portugal. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 185–204. [Google Scholar] [CrossRef]

- Kuo, L.; Yi-Ju Chen, V. Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Manag. Decis. 2013, 51, 1462–1487. [Google Scholar] [CrossRef]

- Sutantoputra, A.W. Social disclosure rating system for assessing firms’ CSR reports. Corp. Commun. 2009, 14, 34–48. [Google Scholar] [CrossRef]

- Adler, R.W.; Milne, M.J. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar]

- Krippendorff, K. Reliability in Content Analysis. Hum. Commun. Res. 2004, 30, 411–433. [Google Scholar] [CrossRef]

- Marascuilo, L.A.; Serlin, R.C. Statistical Methods for the Social and Behavioral Sciences; W.H. Freeman: New York, NY, USA, 1988. [Google Scholar]

- Rey, D.; Neuhäuser, M. Wilcoxon-Signed-Rank Test. In International Encyclopedia of Statistical Science; Springer: Berlin/Heidelberg, Germany, 2011; pp. 1658–1659. [Google Scholar]

- Siegel, S.; Castellan, N.J. Nonparametric Statistics for the Behavioral Sciences, 2nd ed.; McGraw-Hill: New York, NY, USA, 1988. [Google Scholar]

- Wiseman, J. An evaluation of environmental disclosures made in corporate annual reports. Account. Organ. Soc. 1982, 7, 53–63. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The Influence of Governance Structure and Strategic Corporate Social Responsibility Toward Sustainability Reporting Quality. Bus. Strateg. Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Bachoo, K.; Tan, R.; Wilson, M. Firm Value and the Quality of Sustainability Reporting in Australia. Aust. Account. Rev. 2013, 23, 67–87. [Google Scholar] [CrossRef]

- Choi, J.-S. An investigation of the initial voluntary environmental disclosures made in Korean semi-annual reports. Pac. Account. Rev. 1999, 11, 73–102. [Google Scholar]

- Huang, C.L.; Kung, F.H. Drivers of Environmental Disclosure and Stakeholder Expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Lanis, R.; Richardson, G. Corporate social responsibility and tax aggressiveness: An empirical analysis. J. Account. Public Policy 2012, 31, 86–108. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Post, C.; Rahman, N.; Rubow, E. Green governance: Boards of directors’ composition and environmental corporate social responsibility. Bus. Soc. 2011, 50, 189–223. [Google Scholar] [CrossRef]

- Stanny, E.; Ely, K. Corporate environmental disclosures about the effects of climate change. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 338–348. [Google Scholar] [CrossRef]

- Seele, P.; Lock, I. Instrumental and/or Deliberative? A Typology of CSR Communication Tools. J. Bus. Ethics 2015, 131, 401–414. [Google Scholar] [CrossRef]

- Chapple, W.; Moon, J. Corporate social responsibility (CSR) in Asia a seven-country study of CSR Web site reporting. Bus. Soc. 2005, 44, 415–441. [Google Scholar] [CrossRef]

- Kühn, A.-L.; Stiglbauer, M.; Fifka, M.S. Contents and Determinants of Corporate Social Responsibility Website Reporting in Sub-Saharan Africa: A Seven-Country Study. Bus. Soc. 2018, 57, 437–480. [Google Scholar] [CrossRef]

- Manetti, G.; Bellucci, M. The use of social media for engaging stakeholders in sustainability reporting. Account. Audit. Account. J. 2016, 29, 985–1011. [Google Scholar] [CrossRef]

- Nikolaeva, R.; Bicho, M. The role of institutional and reputational factors in the voluntary adoption of corporate social responsibility reporting standards. J. Acad. Mark. Sci. 2011, 39, 136–157. [Google Scholar] [CrossRef]

- Habisch, A.; Patelli, L.; Pedrini, M.; Schwartz, C. Different Talks with Different Folks: A Comparative Survey of Stakeholder Dialog in Germany, Italy, and the US. J. Bus. Ethics 2011, 100, 381–404. [Google Scholar] [CrossRef]

- Manetti, G. The quality of stakeholder engagement in sustainability reporting: Empirical evidence and critical points. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 110–122. [Google Scholar] [CrossRef]

- Bellantuono, N.; Pontrandolfo, P.; Scozzi, B. Capturing the stakeholders’ view in sustainability reporting: A novel approach. Sustainability 2016, 8, 379. [Google Scholar] [CrossRef]

- Font, X.; Guix, M.; Bonilla-Priego, M.J. Corporate social responsibility in cruising: Using materiality analysis to create shared value. Tour. Manag. 2016, 53, 175–186. [Google Scholar] [CrossRef]

- Khan, M.; Serafeim, G.; Yoon, A. Corporate Sustainability: First Evidence on Materiality. Account. Rev. 2016, 91, 1697–1724. [Google Scholar] [CrossRef]

- Barkemeyer, R.; Comyns, B.; Figge, F.; Napolitano, G. CEO statements in sustainability reports: Substantive information or background noise? Account. Forum 2014, 38, 241–257. [Google Scholar] [CrossRef]

- Adams, C.A. The Sustainable Development Goals, Integrated Thinking and the Integrated Report; International Integrated Reporting Council (IIRC): London, UK, 2017. [Google Scholar]

- Busco, C.; Izzo, M.F.; Granà, F. Sustainable Development Goals and Integrated Reporting; Routledge: London, UK, 2018. [Google Scholar]

- Orzes, G.; Moretto, A.M.; Ebrahimpour, M.; Sartor, M.; Moro, M.; Rossi, M. United Nations Global Compact: Literature review and theory-based research agenda. J. Clean. Prod. 2018, 177, 633–654. [Google Scholar] [CrossRef]

- Stubbs, W.; Higgins, C. Stakeholders’ Perspectives on the Role of Regulatory Reform in Integrated Reporting. J. Bus. Ethics 2018, 147, 489–508. [Google Scholar] [CrossRef]

- Peters, G.F.; Romi, A.M. The Association between Sustainability Governance Characteristics and the Assurance of Corporate Sustainability Reports. Audit. A J. Pract. Theory 2015, 34, 163–198. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. CEO Compensation and Sustainability Reporting Assurance: Evidence from the UK. J. Bus. Ethics 2017, 158, 1–20. [Google Scholar] [CrossRef]

- Erwin, P.M. Corporate Codes of Conduct: The Effects of Code Content and Quality on Ethical Performance. J. Bus. Ethics 2011, 99, 535–548. [Google Scholar] [CrossRef]

- Painter-Morland, M. Triple bottom-line reporting as social grammar: Integrating corporate social responsibility and corporate codes of conduct. Bus. Ethics A Eur. Rev. 2006, 15, 352–364. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. Credibility of sustainability reports: The contribution of audit committees. Bus. Strateg. Environ. 2018, 27, 973–986. [Google Scholar] [CrossRef]

- Bland, J.M.; Altman, D.G. Cronbach’s alpha. Br. Med J. (Clin. Res. Ed.) 1997, 314, 572. [Google Scholar] [CrossRef]

- Field, A. Discovering Statistics Using SPSS, 3rd ed.; Sage: London, UK, 2009. [Google Scholar]

- Tavakol, M.; Dennick, R. Making sense of Cronbach’s alpha. Int. J. Med. Ed. 2011, 2, 53–55. [Google Scholar] [CrossRef]

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring more sustainable reporting in Europe using non-financial disclosure-de facto and de jure evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, F.; Leopizzi, R.; Pizzi, S. The state of art of corporate social disclosure before the introduction of non-financial reporting directive: A cross country analysis. Soc. Responsib. J. 2019, 15, 409–423. [Google Scholar] [CrossRef]

- Bubna-Litic, K. Environmental Reporting as a Communications Tool: A Question of Enforcement? J. Environ. Law 2008, 20, 69–85. [Google Scholar] [CrossRef]

- Criado-Jiménez, I.; Fernández-Chulián, M.; Husillos-Carqués, F.J.; Larrinage-González, C. Compliance with mandatory environmental reporting in financial statements: The case of Spain (2001–2003). J. Bus. Ethics 2008, 79, 245–262. [Google Scholar] [CrossRef]

- Damak-Ayadi, S. Social and Environmental Reporting in the Annual Reports of Large Companies in France. Account. Manag. Inf. Syst. 2010, 9, 22–44. [Google Scholar]

- Dong, S.; Xu, L. The impact of explicit CSR regulation: Evidence from China’s mining firms. J. Appl. Account. Res. 2016, 17, 237–258. [Google Scholar] [CrossRef]

- Dumitru, M.; Dyduch, J.; Gușe, R.-G.; Krasodomska, J. Corporate Reporting Practices in Poland and Romania—An Ex-Ante Study to the New Non-Financial Reporting European Directive. Account. Eur. 2017, 14, 279–304. [Google Scholar] [CrossRef]

- Fatima, A.H.; Abdullah, N.; Sulaiman, M. Environmental disclosure quality: Examining the impact of the stock exchange of Malaysia’s listing requirements. Soc. Responsib. J. 2015, 11, 904–922. [Google Scholar] [CrossRef]

- Frost, G.R. The Introduction of Mandatory Environmental Reporting Guidelines: Australian Evidence. Abacus 2007, 43, 190–216. [Google Scholar] [CrossRef]

- Kerret, D.; Menahem, G.; Sagi, R. Effects of the Design of Environmental Disclosure Regulation on Information Provision: The Case of Israeli Securities Regulation. Environ. Sci. Technol. 2010, 44, 8022–8029. [Google Scholar] [CrossRef]

- Larrinaga, C.; Carrasco, F.; Correa, C.; Llena, F.; Moneva, J.; De Burgos, U. Accountability and accounting regulation: The case of the Spanish environmental disclosure standard. Eur. Account. Rev. 2010, 11, 723–740. [Google Scholar] [CrossRef]

- Li, Y.; Zhang, J.; Foo, C.-T. Towards a theory of social responsibility reporting: Empirical Analysis of 613 CSR Reports by Listed Corporations in China. Chin. Manag. Stud. 2013, 7, 519–534. [Google Scholar] [CrossRef]

- Llena, F.; Moneva, J.M.; Hernandez, B. Environmental disclosures and compulsory accounting standards: The case of spanish annual reports. Bus. Strateg. Environ. 2007, 16, 50–63. [Google Scholar] [CrossRef]

- Pedersen, E.R.G.; Neergaard, P.; Pedersen, J.T.; Gwozdz, W. Conformance and Deviance: Company Responses to Institutional Pressures for Corporate Social Responsibility Reporting. Bus. Strateg. Environ. 2013, 22, 357–373. [Google Scholar] [CrossRef]

- Albertini, E. A Descriptive Analysis of Environmental Disclosure: A Longitudinal Study of French Companies. J. Bus. Ethics 2014, 121, 233–254. [Google Scholar] [CrossRef]

- Fifka, M.S. CSR-Kommunikation und Nachhaltigkeitsreporting-Alles neu macht die Berichtspflicht? In CSR Und Kommunikation; Heinrich, P., Ed.; Springer: Berlin/Heidelberg, Germany, 2018; pp. 139–153. [Google Scholar]

- Fifka, M.S.; Loza Adaui, C.R. Corporate Social Responsibility (CSR) Reporting—Administrative Burden or Competitive Advantage? In New Perspectives on Corporate Social Responsibility; O’Riordan, L., Zmuda, P., Heinemann, S., Eds.; Springer: Wiesbaden, Germany, 2015; pp. 285–300. [Google Scholar]

- Brammer, S.; Pavelin, S. Factors influencing the quality of corporate environmental disclosure. Bus. Strateg. Environ. 2008, 17, 120–136. [Google Scholar] [CrossRef]

- Dyduch, J.; Krasodomska, J. Determinants of Corporate Social Responsibility Disclosure: An Empirical Study of Polish Listed Companies. Sustainability 2017, 9, 1934. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of Corporate Social Responsibility Disclosure Ratings by Spanish Listed Firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- D’Amico, E.; Coluccia, D.; Fontana, S.; Solimene, S. Factors Influencing Corporate Environmental Disclosure. Bus. Strateg. Environ. 2016, 25, 178–192. [Google Scholar] [CrossRef]

- Goodwin-Stewart, J.; Kent, P. Relation between external audit fees, audit committee characteristics and internal audit. Account. Financ. 2006, 46, 387–404. [Google Scholar] [CrossRef]

- Prawitt, D.F.; Sharp, N.Y.; Wood, D.A. Reconciling Archival and Experimental Research: Does Internal Audit Contribution Affect the External Audit Fee? Behav. Res. Account. 2011, 23, 187–206. [Google Scholar] [CrossRef]

- Baldini, M.; Maso, L.D.; Liberatore, G.; Mazzi, F.; Terzani, S. Role of Country- and Firm-Level Determinants in Environmental, Social, and Governance Disclosure. J. Bus. Ethics 2018, 150, 79–98. [Google Scholar] [CrossRef]

- Kutner, M.H.; Nachtsheim, C.J.; Neter, J.; Li, W. Applied Linear Statistical Models, 5th ed.; McGraw-Hill: New York, NY, USA, 2005. [Google Scholar]

- Frias-Aceituno, J.V.; Rodríguez-Ariza, L.; Garcia-Sánchez, I.M. Explanatory Factors of Integrated Sustainability and Financial Reporting. Bus. Strateg. Environ. 2014, 23, 56–72. [Google Scholar] [CrossRef]

- Lee, K.-H. Does Size Matter? Evaluating Corporate Environmental Disclosure in the Australian Mining and Metal Industry: A Combined Approach of Quantity and Quality Measurement. Bus. Strateg. Environ. 2017, 26, 209–223. [Google Scholar] [CrossRef]

- Bergmann, A.; Posch, P. Mandatory Sustainability Reporting in Germany: Does Size Matter? Sustainability 2018, 10, 3904. [Google Scholar] [CrossRef]

- Bushee, B.J.; Leuz, C. Economic consequences of SEC disclosure regulation: Evidence from the OTC bulletin board. J. Account. Econ. 2005, 39, 233–264. [Google Scholar] [CrossRef]

- Luque-Vílchez, M.; Larrinaga, C. Reporting Models do not Translate Well: Failing to Regulate CSR Reporting in Spain. Soc. Environ. Account. J. 2016, 36, 56–75. [Google Scholar] [CrossRef]

- Perrault Crawford, E.; Clark Williams, C. Should corporate social reporting be voluntary or mandatory? Evidence from the banking sector in France and the United States. Corp. Gov. Int. J. Bus. Soc. 2010, 10, 512–526. [Google Scholar] [CrossRef]

- Rodrigue, M.; Magnan, M.; Cho, C.H. Is Environmental Governance Substantive or Symbolic? An Empirical Investigation. J. Bus. Ethics 2013, 114, 107–129. [Google Scholar] [CrossRef]

- Carini, C.; Rocca, L.; Veneziani, M.; Teodori, C. Ex-Ante Impact Assessment of Sustainability Information—The Directive 2014/95. Sustainability 2018, 10, 560. [Google Scholar] [CrossRef]

| Year | Initiative | Character | Reporting Focus | Nonfinancial Themes Mainly Addressed | Scope | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Management process | Principles | Themes | Indicators | Policies and/or processes | Environment | Social | Employee and labor | Human rights | Anti-corruption | Diversity | ||||

| July 1993 | Eco-Management and Audit Scheme (EMAS) | V | Yes | No | Yes | Partially | • | • | EU | |||||

| 1996 | ISO 14001 | V | Yes | No | Yes | Partially | • | • | GL | |||||

| 1999 | AA1000 Framework Standard | V | Yes | Yes | Yes | No | • | • | • | • | GL | |||

| June 2000 | GRI Sustainability Reporting Guidelines | V | Yes | Yes | Yes | Yes | • | • | • | • | GL | |||

| June 2000 | EU Financial Reporting Strategy: the way forward COM(2000)359 | M | No | Yes | No | No | • | GL | ||||||

| 2000 | United Nations Global Compact (UNGC) foundation | V | No | No | Yes | No | • | • | • | • | • | GL | ||

| 2000 | Carbon Disclosure project (CDP) foundation | V | No | No | No | Yes | • | GL | ||||||

| 2001 | GHG Protocol Standards | V | Yes | Yes | Yes | Yes | • | • | GL | |||||

| May 2001 | Commission Recommendation on the recognition, measurement and disclosure of environmental issues in the annual accounts and annual reports of companies (2001/453/EC) | M | No | No | Yes | Yes | • | EU | ||||||

| 2001 | Standard GBS 2001—Principi di redazione del bilancio social | V | No | Yes | Yes | Yes | • | • | • | • | IT | |||

| 2001 | SA8000 | V | No | Yes | Yes | No | • | • | • | • | • | • | GL | |

| 2001 | EMAS revision (EC No 761/2001) | V | Yes | No | Yes | Partially | • | • | EU | |||||

| 2002 | GRI G2 Guidelines (update) | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| June 2003 | Accounts Modernization Directive (2003/51/EC) | M | Yes | No | No | Mentioned | • | • | • | • | EU | |||

| 2003 | AA1000 Assurance Standard | V | Yes | Yes | Yes | No | • | |||||||

| 2004 | GHG Protocol Standards (update) | V | Yes | Yes | Yes | Yes | • | • | GL | |||||

| 2004 | ISO 14001 (update) | V | Yes | No | Yes | Partially | • | • | GL | |||||

| December 2004 | Gesetz zur Einführung internationaler Rechnungslegungsstandards und zur Sicherung der Qualität der Abschlussprüfung (Bilanzrechtregotmgesetz -BilReG) | M | Yes | No | No | Mentioned | • | • | • | • | GE | |||

| 2005 | GBS—La rendicontazione social nel settore pubblico | V | No | Yes | Yes | Yes | • | • | • | • | IT | |||

| 2005 | AA1000 Stakeholder Engagement Standard | V | Yes | Yes | Yes | No | • | GL | ||||||

| 2006 | GRI G3 Guidelines (update) | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| March 2007 | Decreto Legislativo 32/2007 (Italian implementation of Directive 2003/51/EC) | M | Yes | No | No | Mentioned | • | • | • | • | IT | |||

| 2008 | AA1000 Assurance Standard (update) | V | Yes | Yes | Yes | No | • | GL | ||||||

| 2008 | AA1000 AccountAbility Principles separate standard | V | No | Yes | No | No | • | GL | ||||||

| 2008 | SA8000: 2008 (update) | V | Yes | No | Yes | No | • | • | • | • | GL | |||

| 2009 | EMAS revision (EC No 1221/2009) | V | Yes | No | Yes | Mentioned | • | • | EU | |||||

| 2010 | ISO 26000 | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| 2011 | GRI G3.1 Guidelines (update) | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| June 2011 | Guiding Principles on Business and Human Rights | V | No | Yes | Yes | No | • | • | • | • | • | GL | ||

| 2012 | Rio+20 Declaration explicit references to nonfinancial reporting paragraph 47 | V | No | No | Yes | No | • | • | • | • | • | • | GL | |

| 2013 | GRI G4 Guidelines (update) | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| 2013 | Directive 2013/34/EU | M | Yes | No | Yes | No | • | EU | ||||||

| 2013 | Standard GBS 2013—Principi di redazione del bilancio sociale | V | No | Yes | Yes | Yes | • | • | • | • | IT | |||

| December 2013 | International Integrated Reporting Framework Framework | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| 2014 | Directive 2014/95/EU | M | Yes | Yes | Yes | No | • | • | • | • | • | • | • | EU |

| 2014 | SA8000: 2014 (update) | V | Yes | Yes | Yes | No | • | • | • | • | • | • | GL | |

| 2015 | ISO 14001 (update) | V | Yes | No | Yes | Partially | • | • | GL | |||||

| 2015 | AA1000 Stakeholder Engagement Standard (update) | V | Yes | Yes | Yes | No | • | GL | ||||||

| 2015 | GHG Protocol Standards (update) | V | Yes | Yes | Yes | Yes | • | • | GL | |||||

| 2016 | Decreto Legislativo 243/2016 (Italian implementation of Directive 2014/95/EU) | M | Yes | Yes | Yes | No | • | • | • | • | • | • | • | IT |

| 2016 | GRI Standards (update) | V | Yes | Yes | Yes | Yes | • | • | • | • | • | • | • | GL |

| April 2017 | CSR Richtlinie-Umsetzungsgesetz (German implementation of Directive 2014/95/EU) | M | Yes | Yes | Yes | No | • | • | • | • | • | • | • | GE |

| 2017 | Guidelines on non-financial reporting (2017/C 215/01) | V | Yes | Yes | Yes | Examples | • | • | • | • | • | • | • | EU |

| SRQ Indicator | Data-Collection Process | |

|---|---|---|

| AV1 | Availability of a stand-alone sustainability report (SR) or availability of an integrated report (IR) [58] | Analysis of corporate website (detailed analysis of ‘investor relations’ and ‘sustainability/Corporate Social Responsibility (CSR)’ sections) |

| AV2 | Availability of brochures or other autonomous documents about sustainability [131] | Analysis of corporate website in all its sections |

| AV3 | Availability of a webpage addressing sustainability/CSR issues [132,133] | Analysis of corporate website |

| AV4 | Availability of sustainability information via social media [134] | Analysis of social media (Facebook, Twitter, Youtube, and Linkedin) |

| CR1 | Explicit adoption of sustainability reporting guidelines (Global Reporting Initiative, Deutsche Nachhaltigkeits Kodex, Gruppo di Studio Bilancio Sociale) [22,116,123,135] | Content analysis of method section of SR/IR |

| CR2 | Independent verification or assurance of NFD [22,40,41,42,116,123] | Research into SR/IR for independent assessment letter |

| CR3 | Evidence of stakeholder engagement in sustainability reporting process [22,76,116,123] | Content analysis of method section of SR/IR and possibly other sections (‘stakeholder’ section if one exists) |

| CR4 | Description of instruments used for stakeholder engagement in sustainability reporting process [136,137] | Content analysis of method section of SR/IR and possibly other section (‘stakeholder’ section if one exists) |

| CR5 | Availability of quantitative data about sustainability-related expenditure [114,124,128] | Content analysis of SR/IR (only explicit sustainability-related expenditures are considered, for example, expenditures for environmental sanctions are not considered) |

| CR6 | Availability of quantitative data about sustainability performance [108,114,124] | Content analysis of SR/IR |

| CR7 | Inclusion of a materiality analysis as part of the sustainability report [138,139,140] | Content analysis of method section of SR/IR and possibly other sections (‘materiality analysis’ section if one exists) |

| SA1 | Top-management statement about sustainability or reference to sustainability in top-management statement of integrated report [141] | Content analysis of CEO’s/president’s letter |

| SA2 | Description of a sustainability policy/strategy [114] | Content analysis of SR/IR |

| SA3 | Reference to the United Nations Sustainable Development Goals [142,143] | Content analysis of SR/IR |

| SA4 | Reference to the United Nations Global Compact [144] | Content analysis of SR/IR |

| SA5 | Integrated reporting [145] | Analysis of annual report (regardless of whether there is also a stand-alone SR) |

| SA6 | Existence of a sustainability/CSR governance entity in the organizational structure [146,147] | Content analysis of SR/IR and of corporate website |

| SA7 | Possession of certification by independent agencies for environmental issues (e.g., ISO 14000, EMAS) [22,123] | Content analysis of SR/IR and of corporate website |

| SA8 | Possession of certification by independent agencies for social issues (e.g., OSHAS, SA8000) [116] | Content analysis of SR/IR and of corporate website |

| SA9 | Possession of an ethical code or deontological code of behavior [148,149] | Content analysis of SR/IR and of corporate website |

| Sustainability Reporting Quality | ||||

|---|---|---|---|---|

| Italy (N = 36) | Germany (N = 30) | |||

| Period | Mean | Std dev. | Mean | Std dev. |

| Before implementation (2016) | 12.50 | 7.241 | 16.30 | 3.678 |

| After implementation (2017) | 15.53 | 3.828 | 17.67 | 2.155 |

| Period | Sustainability Reporting Quality | |||

|---|---|---|---|---|

| Italy (N = 36) | Germany (N = 30) | |||

| N | SRQ Mean | N | SRQ Mean | |

| Decrease of SRQ after implementation | 4 | 14.00 | – | – |

| Increase of SRQ after implementation | 20 | 14.40 | 16 | 17.06 |

| No change in SRQ after implementation | 12 | 17.92 | 14 | 18.36 |

| Sustainability Reporting Quality (SRQ) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Italy (N = 36) | Germany (N = 30) | |||||||

| AV | CR | SA | SRQ | AV | CR | SA | SRQ | |

| Mean before | 2.56 | 4.64 | 5.31 | 12.50 | 3.23 | 6.10 | 6.97 | 16.30 |

| Mean after | 2.94 | 5.83 | 6.75 | 15.53 | 3.53 | 6.63 | 7.50 | 17.67 |

| Δ | 0.38 | 1.19 | 1.44 | 3.03 | 0.30 | 0.53 | 0.53 | 1.37 |

| p | 0.046 * | <0.001 * | <0.001 * | <0.001 * | 0.014 * | 0.016 * | 0.002 * | <0.001 * |

| Z | −1.997 a | −3.234 a | −3.619 a | −3.502 a | −2.460 a | −2.410 a | −3.066 a | −3.573 a |

| Sustainability Reporting Quality | ||||

|---|---|---|---|---|

| Reporters with Experience (N = 58) | ||||

| AV | CR | SA | SRQ | |

| Mean before | 3.26 | 6.03 | 6.90 | 16.19 |

| Mean after | 3.40 | 6.45 | 7.38 | 17.23 |

| Δ | 0.14 | 0.42 | 0.48 | 1.04 |

| p | 0.083 | 0.002 * | <0.001 * | <0.001 * |

| Z | −1.734 a | −3.079 a | −3.781 a | −4.085 a |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

|---|---|---|---|---|---|---|---|---|

| 1 SRQ Index | 1 | |||||||

| 2 AV | - | 1 | ||||||

| 3 CR | - | - | 1 | |||||

| 4 SA | - | - | - | 1 | ||||

| 5 Size | 0.378 ** | 0.344 * | 0.440 ** | 0.188 | 1 | |||

| 6 Profitability | −0.281 * | −0.187 | −0.269 * | −0.215 | 0.454 ** | 1 | ||

| 7 Industry | 0.049 | −0.169 | −0.042 | 0.225 | −0.470 ** | −0.055 | 1 | |

| 8 Country | 0.200 | 0.167 | 0.230 | 0.096 | 0.429 ** | −0.368 ** | 0.701 | 1 |

| B | t | Collinearity statistics | ||

|---|---|---|---|---|

| Tolerance | VIF | |||

| (constant) | 9.352 | 3.397 *** | ||

| Size | 0.686 | 2.838 *** | 0.478 | 2.091 |

| Profitability | −0.016 | −0.284 | 0.686 | 1.459 |

| Industry | 1.448 | 1.957 * | 0.666 | 1.500 |

| Country | −0.148 | −0.225 | 0.754 | 1.326 |

| AV as Dependent Variable | CR as Dependent Variable | SA as Dependent Variable | Collinearity Statistics | |||||

|---|---|---|---|---|---|---|---|---|

| B | t | B | t | B | t | Tolerance | VIF | |

| (constant) | 1.961 | 1.778 * | 3.779 | 4.456 *** | 3.612 | 2.212 ** | ||

| Size | 0.122 | 1.257 | 0.239 | 3.204 *** | 0.326 | 2.272 ** | 0.478 | 2.091 |

| Profitability | −0.007 | −0.304 | −0.001 | −0.034 | −0.008 | −0.257 | 0.686 | 1.459 |

| Industry | −0.163 | −0.551 | 0.391 | 1.716 * | 1.221 | 2.781 *** | 0.666 | 1.500 |

| Country | 0.163 | 0.619 | −0.032 | −0.160 | −0.278 | −0.715 | 0.754 | 1.326 |

| N = 55 | N = 55 | N = 55 | ||||||

| R2 = 0.130 | R2 = 0.245 | R2 = 0.184 | ||||||

| Durbin-Watson = 1.693 | Durbin-Watson = 1.389 | Durbin-Watson = 1.171 | ||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mion, G.; Loza Adaui, C.R. Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability 2019, 11, 4612. https://doi.org/10.3390/su11174612

Mion G, Loza Adaui CR. Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability. 2019; 11(17):4612. https://doi.org/10.3390/su11174612

Chicago/Turabian StyleMion, Giorgio, and Cristian R. Loza Adaui. 2019. "Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies" Sustainability 11, no. 17: 4612. https://doi.org/10.3390/su11174612

APA StyleMion, G., & Loza Adaui, C. R. (2019). Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability, 11(17), 4612. https://doi.org/10.3390/su11174612