All articles published by MDPI are made immediately available worldwide under an open access license. No special

permission is required to reuse all or part of the article published by MDPI, including figures and tables. For

articles published under an open access Creative Common CC BY license, any part of the article may be reused without

permission provided that the original article is clearly cited. For more information, please refer to

https://www.mdpi.com/openaccess.

Feature papers represent the most advanced research with significant potential for high impact in the field. A Feature

Paper should be a substantial original Article that involves several techniques or approaches, provides an outlook for

future research directions and describes possible research applications.

Feature papers are submitted upon individual invitation or recommendation by the scientific editors and must receive

positive feedback from the reviewers.

Editor’s Choice articles are based on recommendations by the scientific editors of MDPI journals from around the world.

Editors select a small number of articles recently published in the journal that they believe will be particularly

interesting to readers, or important in the respective research area. The aim is to provide a snapshot of some of the

most exciting work published in the various research areas of the journal.

Energy consumption is a crucial factor to promote industrial sector contribution in an economy for its economic progression. Indeed, Pakistan is an emerging country, but recently adjoining with a very severe deficit of electricity sources. Hence, the industry value added growth leading to economic progression is also fronting inevitable challenges to promote the industry growth. The main objective of the study is to investigate the linkages between industrial sector oil, gas and electricity consumption, and renewable energy consumption with economic development in Pakistan. The findings display evidence of cointegration and a long-run relationship between the consumption of industrial energy and economic growth in Pakistan. The results showed that industrial electricity consumption and industrial gas consumption have a positive and statistically significant impact on economic growth both in the long run and the short run in Pakistan. Industrial oil consumption negatively impacts economic growth in the long run, but positively and statistically significantly impacts economic growth in the short run in Pakistan. Moreover, indications through the vector error correction model (VECM) model confirmed bi-directional relationships of industrial sector oil consumption and economic growth in Pakistan. Furthermore, the uni-directional nexus instituted between economic growth to industrial electricity consumption, industrial gas consumption to industrial electricity consumption, and industrial oil consumption to industrial electricity consumption. The findings uncovered solid interconnections among the studied variables and suggested that the Pakistani government should build a robust policy to diminish the oil, gas, and fossil fuels consumption for electricity production, as a replacement to depend on solar, hydro, wind, and biomass energy sources in Pakistan. Consequently, the government should promote more gas concentrated projects, as these will alleviate the contests of gas dearth and provide it to the industry at cheap prices with ease.

Policy makers have been trying to tackle the issue of climate change in recent decades. The Paris Climate Conference (COP21) aims to confirm the goal of restraining the worldwide temperature to the minimum level. All parties also agreed to report on their progress in executing their objectives and pursuing advancement towards long-run goals through a strong, apparent, and responsible system. Conversely, the scheme of these energy reduction plans has a substantial effect on economic development. Following the pioneering effort of Kraft and Kraft [1], several studies have examined the causal association between energy use and fiscal development. At the general or state level, electricity use is closely linked to economic progress [2,3]. As earlier studies have shown, monetary progress depends to a great degree on energy inputs. Further, Pakistan is a developing country with a heavy dependence on energy consumption for its manufacturing industry.

Most existing studies used national or aggregated data to examine the linkage between electricity consumption and financial progress. However, backing for the energy-development association does not mean that the affiliation exists at the industrial level, although certain industries may show rigorous energy use. In Pakistan, the demand for energy is increasing every year, and the government of the country should take the crucial steps to fill demand and supply gaps by using alternative resources of energy such as wind energy and solar power [4].

In this contemporary stage of advancement and technological evolution, the energy source is not only a grounding column for economic progression, but also an indispensable strategic stockpile for a country like Pakistan, which is ruthlessly fronting to the energy dearth challenges. Similarly, sustainable financial and economic advancement categorically depends on energy ingesting in various sectors of an economy. Certainly, the leading font of energy production and utilization is fossil fuels (oil, gas, coal, and so on), and others are renewables (wind, solar, and nuclear energy sources), those licensed to achieve the energy necessities for running an economy. Hence, the dearth of these energy resources has an immense direct influence on industrial output and economic progression.

Several previous studies have demonstrated issues similar to energy, including energy crisis, energy security, future energy consumption, energy production from alternative resources, policy implications, power consumption, energy production and its association with economic development, clean and non-renewable energy sources, and the infrastructure of energy sectors in Pakistan for enhancing the energy and economic sectors [4,5,6,7,8,9,10]. Therefore, it is valuable to examine the relationship between energy consumption and financial progress at the industrial level. This analysis would illustrate the explicit energy preservation policies and carbon decrease technologies that we have identified for energy concentrated businesses.

Our investigation subsidizes to the prevailing literature as follows: (1) this study employed the autoregressive distributed lag (ARDL) cointegration modelling method to review the short-run and long-run impression of assorted energy consumption sources like industrial energy consumption, renewable energy consumption, industrial gas consumption for energy and their impact on economic performance of Pakistan; (2) it also provided a breakdown of the various energy production and consumption segments for an input of industrial output and gross domestic product over the period of 1983–2017; (3) this research enquiry utilized industrial energy consumption, industrial gas consumption, and industrial oil consumption for power generation purpose with add of renewable energy consumption for the economic growth of Pakistan. In accordance with the researcher’s best acquaintance, no investigation is deemed by utilizing these variables for industrial output as well as for economic performance. The crucial intent of the current study is to make certain how the advent of assorted energy consumption sources is serving to expand the scale of the Pakistani economy.

This work elaborates the linkages between energy consumption (electricity, oil, and gas), at the industry level, and economic growth in Pakistan in the time period 1983–2017. Augmented Dickey Fuller (ADF) and Phillips-Perron (P-P) unit root tests were applied for checking the stationarity of the variables, while ARDL-bounds testing methodology to co-integration was used to explore the causal link among the selected study variables, with the analysis of the long term and short run.

Energy Crisis, Indigenous Energy Resources, and Power Consumption in Pakistan

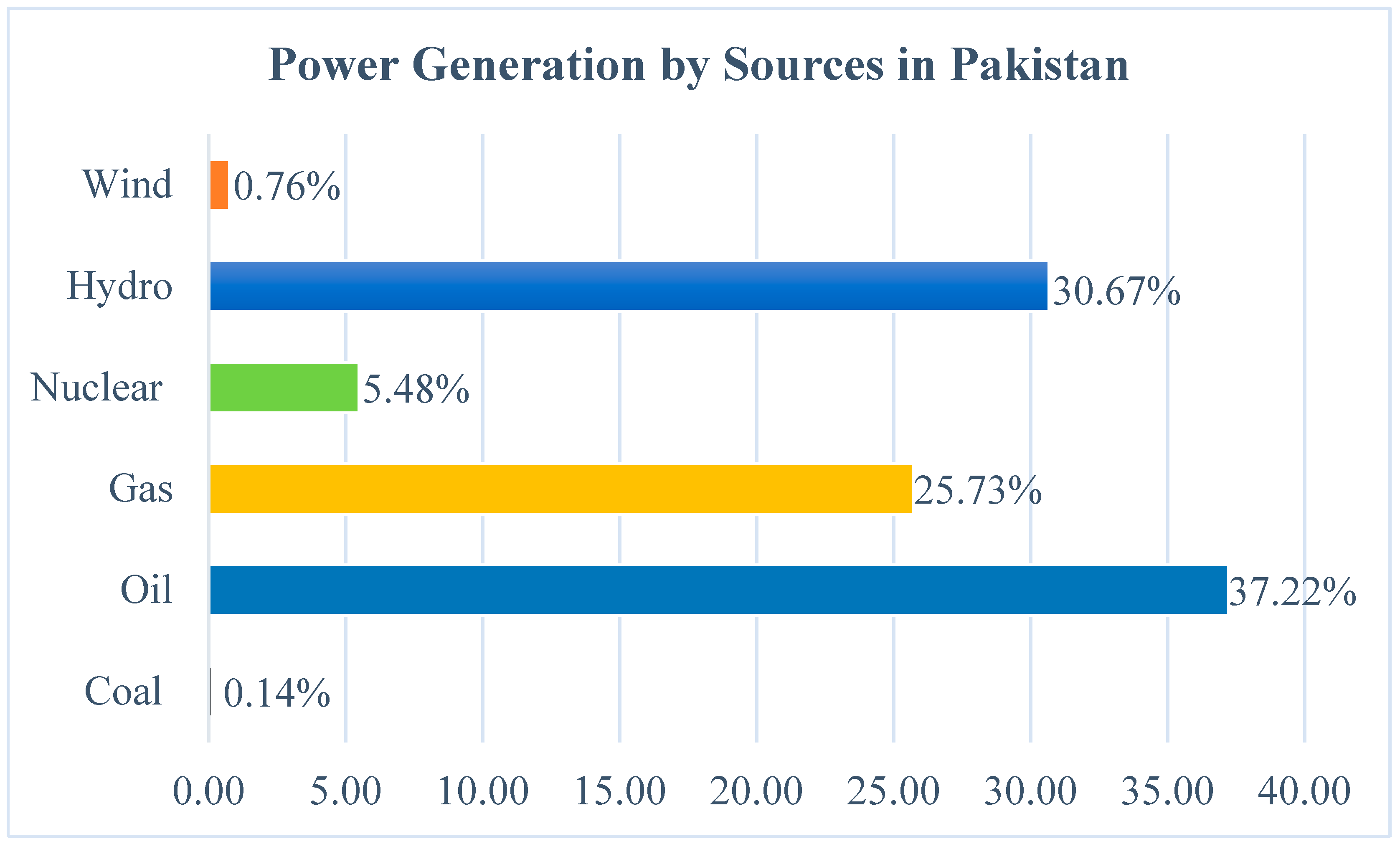

Pakistan’s energy crisis stems from different causes. Excessive energy consumption tends to increase the population’s energy demands, leading to a significant increase in power shortages. In municipal and rural parts of Pakistan, there is plain load shedding fluctuating from 8 to 12 h daily and almost 18 h, respectively. This is because of a lack of 5 to 7 GW stock of power [7,11]. For the power generation, the infrastructure is available; however, it is quite old, taking less competence as associated with the energy burdens in the country. In Pakistan, the renewable resources of energy are not suitably employed. Pakistan is very much enriching in coal reserves because of the 187 billion tonnes of coal that exist in the Makarwal, as well as in the Thar field. However, these reserves have not been properly used. They can be utilized in industry by properly purifying the carbon in evolutionary gases. This will boost the economy of Pakistan while reducing the energy crisis [10]. Pakistan’s energy mix scenario for electricity production in 2013–2014 is shown in Figure 1, which displays an estimation for wide-ranging power production sources such as wind, hydro, nuclear, gas, oil, and coal for the year of 2015. The hydropower means are likely to produce 60,000 MW; however, the development of energy invention is restricted to 11%. Meanwhile, the portion of hydropower in power production could be significantly enlarged to 40%, while the role of local energy to Pakistan’s energy production could reach 80.7% by the year 2030. Presently, oil and gas equity (> 64%) can be reduced to 11.8%, which is thus more conducive to the sustainable development of the country [12].

Figure 1 also illustrates a comprehensive segmental power production sources for the Pakistani economy, where the input of power of nuclear energy was restricted to 2% in 2013–2014, but increased significantly by 2015 to over 5%. As a result, by the 2021 financial year, 23,000 MW of nuclear power generation capacity will now increase to 9%. The Hydel’s share has also increased from 11% to 33% and should be added to the system by 2500 megawatts. More hydel plans are being pursued and will add 3000 megawatts to the state grid. Considering the energy mix of the year 2015, it is quite clear that for the electricity production Pakistan is setting extra exertions into renewable power means [13]. Thermal power is the country’s largest source of electricity generation, relying on fossil fuel sources such as natural gas, oil, high-speed diesel, and coal [14]. However, according to the 2015 statistics of the International Energy Agency (IEA), hydropower and oil are the main sources of power generation in Pakistan, at 37.2% and 30.6%, respectively, followed by natural gas, nuclear energy, wind energy, and coal at 25.7%, 5.4%, 0.76%, and 0.14%, respectively (see Figure 1). The power utilization in different segments accounts for 16% of total final energy consumption, relative to natural gas (44%), oil (29%), coal (10%), and liquefied petroleum gas (LPG) (1%) (GOP, 2013). The total electricity generation is estimated at 110,861 GWh, of which thermal power includes 152 GWh from coal generation, 41,268 GWh from oil, 28,519 GWh from natural gas, 6078 GWh from nuclear energy, 34,004 GWh from hydropower, and 840 GWh from wind energy. Though Pakistan’s total domestic power generation is 111,313 GWh, 17.1% is wasted on transmission and distribution losses (excluding statistical differences and the energy industry’s own use). As a result, the total final consumption decreased by 20.1% compared with the total domestic supply that caused the shortfall. Overall, thermal power accounts for 63% of total power generation, while renewable energy accounts for 31%.

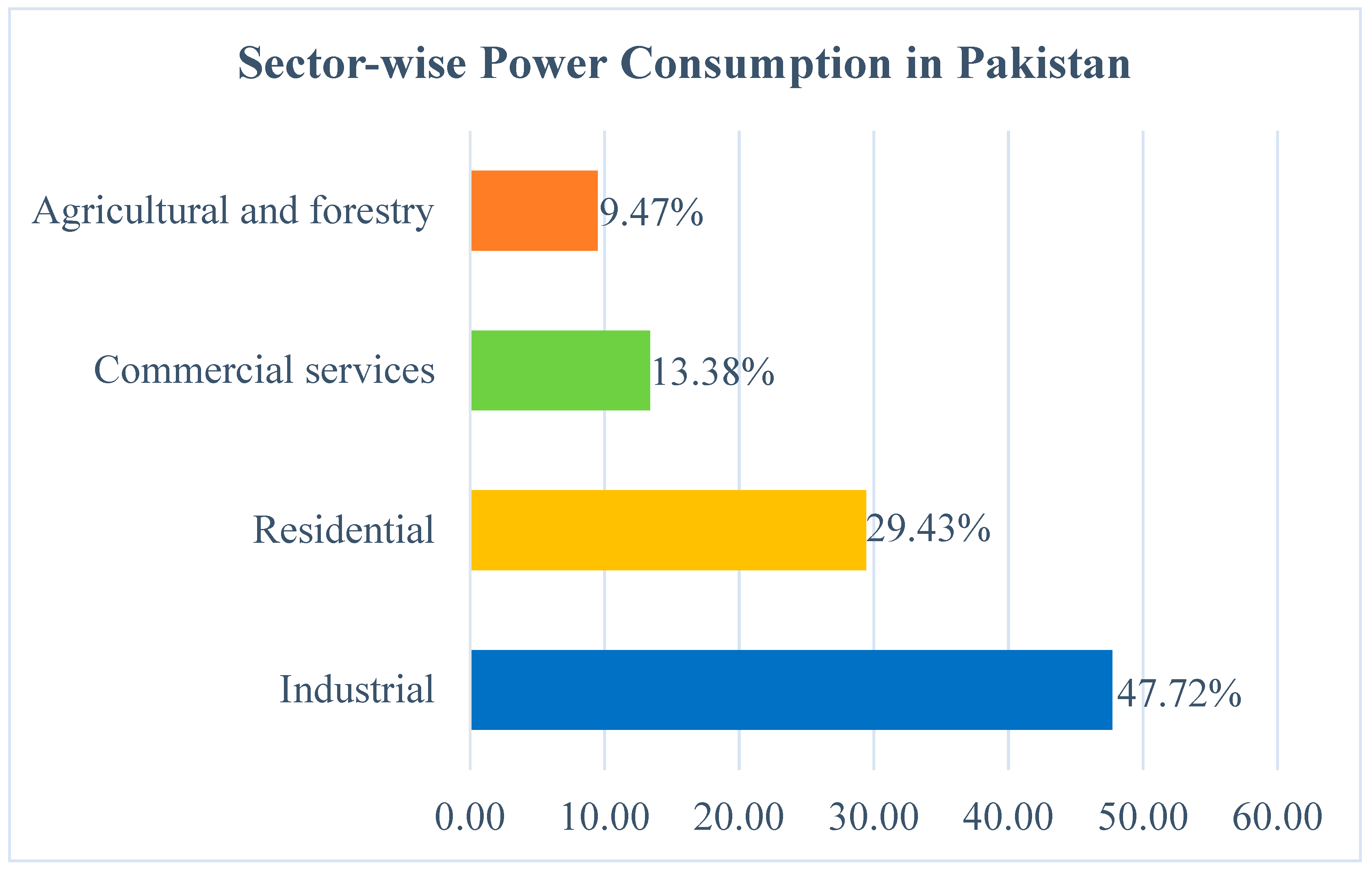

For the growth of industrial and services, good transport supply and movement of households for work and leisure have resulted in an increase in the demand for energy by more than 5% annually in recent years [14]. From 2000 to 2015, energy consumption in the power sector grew at a composite annual progress rate of 4.6%. As a result of rapid industrialization and growing energy demand, Pakistan’s gross domestic product (GDP) is anticipated to grow at a rate of more than 5% in the near future [15]. Currently, Pakistan’s energy production and consumption depend to a large extent on non-renewable sources, while the contribution of renewable energy to the overall percentage is small [16,17,18]. Power is mainly consumed in the residential, industrial, commercial, and agricultural sectors, and is expected to grow over the next 30 years [8,18,19]. Although power ingested in the housing segment accounts for almost half of the total fuel calculation (47.7%), followed by industry (29.4%) and commercial services (13.3%), the agricultural and forestry consumed 9.5% of the remaining power (see Figure 2).

The remaining investigative study is structured in the following manner. Section 2 sees to the brief literature reviews; Section 3 designates material and econometric methods. Furthermore, Section 4 offers wide-ranging results and a discussion for the long-run and short-run estimations. Lastly, Section 5 bundle up a comprehensive conclusion of the research investigation with some policy implications and future directions.

2. Literature Review

Energy use plays a pivotal part in financial progress. Kraft and Kraft [1] are the leading researchers to study the association between energy use and fiscal progress, by a variety of econometric approaches over diverse time eras. From the economist’s point of view, energy is the input to construction; however, practical indication proposes that the linkage between energy and growth is complex. The majority of experiential studies use the cointegration and Granger causality methods. The results of earlier tests are constructed using time series and dynamic panel data methods. The real GDP and electricity consumption are often found to be non-stationary, taking into account a number of cointegration tests. However, these two variables disclose contradictory outcomes on the current issue, as the approximation outcomes are very subtle to the time period measured and the method used. An additional factor complicating the relationship between energy and growth is the differences in the regions in which the study was directed (see, for instance, the works of [2,3]. These studies focused mainly on advanced and emergent nations; though, they did not come to an agreement on the contribution of energy in monetary growth. With regard to diverse datasets, it is quite imperative to take into account data attributes, as the results of approaches and experiences depend on the suitability of the data for empirical analysis.

Most experimental studies use combined or country-level data to examine the problem. Soytas and Sari [20] believe that there is an overall deviation in many works. Campbell and Perron [21] described that a comparatively short time period could significantly deteriorate the ability of statistical testing, resulting in slanted and diverse outcomes. Data at the national level have failed to discourse the assorted impact of this problem. On the basis of industry-level data, few empirical studies have inspected the affiliation between energy use and financial progress [22,23,24]. Xu and Pan [23] found a long term linkage between the industrial evolution and the energy use of the six large industries. Likewise, Zhang and Jiao [24] applied panel approaches to test for unit roots, co-integration associations, and Granger causality. The findings exhibited that in China, financial progress bases more energy use not merely at the domestic level, but also at the provincial and sectorial level. Furthermore, the results exposed that in the eastern area of China, the industries vitrine a bidirectional causality association between energy use and financial development. Hamit-Haggar [25] examined the long term and the causal association between greenhouse gas emissions, energy consumption, and economic growth for Canadian industrial sectors over the period 1990–2007. The conclusions exposed that short-term Granger causality occurs, running from energy use to financial development, and that Environmental Kuznets Curve (EKC) holds.

Shahbaz et al. [26] applied several time series econometric approaches to check the linkages between gas consumption and fiscal growth in Pakistan over the period 1972–2010. The study concludes that natural gas use certainly affects the economic development in Pakistan. Meanwhile, Hassan et al. [27] examined the dynamic linkages between energy use and economic development in Pakistan over the period 1977–2013. The study found that natural gas consumption has a helpful and important influence in the long-run analysis. Additionally, the outcomes of the Granger causality test revealed that there exists an energy-led growth hypothesis in Pakistan, as causality test runs from energy to economic growth. A study conducted by Sari et al. [28] for United States inspected the association between disaggregate energy use and industrialized production. They used several approaches to analyze the data. The study found that energy effects the development expressively and the neutrality of postulation does not hold.

Hu et al. [22] investigated the causal association between power consumption and economic development for Chinese manufacturing sectors for 1980–2010. The results of this study showed that a 1% growth in energy use raises the industrial sectors value added by 0.871% and a 1% surge of industrial sectors value added raises energy use by 1.103%. Furthermore, they find out a unidirectional causality from financial progress to power consumption. However, energy use is established to influence economic development in the long term. Owing to wide variation in energy use detected across businesses, it is useful to check the affiliation between energy use (electricity, gas, and oil) at the industry level and financial progress in Pakistan for 1983–2017. Carrying out the study will help to develop more effective energy preservation and emanation decrease strategies and adjust the industrial structure.

3. Material and Econometric Methods

This research examines the linkage between energy use (electricity, gas, and oil) at the industry level and financial development in Pakistan for 1983–2017 using the following framework:

Supposing that a non-linear association exists between the dependent variable and independent variables, the model is specified as follows:

This study applied several estimation tests; the model is linearized by taking the double log of both sides, which is written in the following way:

where denotes the error term, is the logarithmic forms, represents per capita GDP, represents industrial electricity consumption, represents industrial gas consumption, represents industrial oil consumption, represents industrial value added, and REC specifies percentage of total energy consumption. All data are gathered from international and domestic sources such as World Bank Indicator and different issues of economic surveys of Pakistan (see Table 1). The logarithmic forms are used for all selected study variables.

3.1. Unit Root Tests

The ADF and P-P unit root tests were applied to investigate the stationary properties for long-run association of time series constructed study variables. The augmented Dickey Fuller (ADF) unit root test is based on the equation given below:

where denotes the first difference operator, is a time series, stands for the constant, represents the optimum numbers of lags of the dependent variable, and is the pure white noise error term. The ADF unit root test provides cumulative distribution of ADF statistics. The Phillip Perron (PP) unit root equation is given below:

The Phillip Perron (PP) unit root is also based on t-statistics that are linked with assessed coefficients of .

3.2. Autoregressive Distributed Lag (ARDL) Bound Testing Method

An autoregressive distributed lag (ARDL) cointegration method developed by Pesaran and Pesaran [29], Pesaran and Shin [30], Pesaran et al. [31], and Pesaran et al. [32] under the instructions of the unrestricted vector error correction model used to examine the linkages between energy consumption (electricity, gas, and oil) at the industry level and economic growth in a long-term relationship. Compared with other cointegration methods, the ARDL method has some advantages. Whether the selected study variables are pure I(0), I(1), or mutually co-integrated, the ARDL method [30] can be used. The ARDL method estimates the good small sample properties [33]. In ARDL programs, even if explanatory variables are endogenous variables, the results can be estimated [30,32]. An ARDL approach is developed for estimations as follows:

where is the white noise error term, is the constant, and the error correction dynamics are represented by the summation sign whereas the second part of the equation links to the long-run association. To identify the optimum lag of the model and each series, the Akaike information criteria (AIC) were used. In the ARDL-bounds testing to cointegration method, firstly we compute the F-test value by applying the fitting ARDL models. Secondly, the Wald (F-statistics) test is applied to examine the long-run association between the series. If the calculated value of the F-test exceeds the upper critical bound (UCB) value, the null hypothesis of no co-integration is rejected. If the computed value of F-test fall between the upper and lower critical bound, the results are said to be inconclusive. Lastly, if the calculated value of the F-test is below the lower critical bound, the null hypothesis of no co-integration is accepted. If the long-run relationship between industrial energy consumption and economic growth is found, then we estimate the long-run coefficients. The long run model to be estimated is given as follows:

Furthermore, if we find evidence of the long-run association between industrial energy consumption and economic growth, then we estimate the dynamics of the short run. The short-run model to be estimated is given as follows:

In Equation (8), is the coefficient of the error correction term in the estimated model that shows the speed of adjustment to reverse to its actual position.

3.3. The VECM Granger Causality Approach

The above examined estimates are only applicable in the attendance of the long-run and short-run relationship between the variables in ARDL bound testing method. However, it does not explicitly drift the causal connectedness among the variables. Thus, the instant of co-integrating closeness (if any) is surviving; the subsequent step is to inspect the Granger’s causality investigation among these variables. Resultantly, this test witnesses the causative influence from one variable to another by considering their probability based on their historic and present series values. To facilitate, the route of causativeness and assessing the Granger causality for the short-run analysis by means of vector error correction model (VECM) [34]. In this framework, if variables are mutually cointegrated for the long run in the VECM model, at that moment, the short-run causal scrutiny should hold the error correction term (ECT−1), where speed of adjustment is challenging in this model for attainting the actual long-run symmetric position. However, if co-integration under VECM model does not exist, then the short run causality examination may be engaged through the VAR technique. Hence, the VECM standard model is involved for probing the causality connectedness between the variables embodied as follows:

For the VECM models, the causality test is shown in Equation (9), where “Δ” is the sign of the difference operator, the error-based term is characterized with λ, ECT−1 (error correction term) represents the long-run linking evaluation, and “θ” is the coefficient of error correction term. If “θ” has a mathematically negative coefficient and probability significance < 0.05, then it entitled and declared the formation of long-run relationship between the variables. To investigate the short-run granger causative links, we argue for “F” statistics based on Wald statistical values. For example, α12, k ≠ 0∀k proposes that IEC is granger cause to GDPPC, and then similarly, causality would be tracked from IEC to GDPPC, if α21, k ≠ 0∀k.

4. Empirical Results and Discussions

4.1. Descriptive Statistics and Correlation Matrix

The outcomes of descriptive statistics of the series employed in this study are stated in Table 2. In Table 3, the results of correlation matrix display that industrial energy consumption (electricity, gas, and oil) has an affirmative and substantial association with economic growth. It suggests that energy is essential for boosting development. Financial growth is also positively linked with industrial value added.

4.2. Estimation of Unit Root Test

The estimations of ADF and PP are presented in Table 4. The findings of both tests show that the series are not stationary at their levels. The ADF and P-P unit root checks clearly display that all selected study variables are integrated of order one I(1), so the ARDL model can be used. The observations of this study are annual and the maximum order of lags selected in the ARDL regression approach is 2, as recommended by the authors of [30,35]. The information criterion (AIC) is used with a sample size of less than 60 as recommended by Liew [36].

4.3. ARDL-Bounds Testing

The ARDL-bounds testing method is used to inspect the presence of a cointegration association among industrial energy use (electricity, gas, and oil), and financial progress in Pakistan. For small and large sample sizes, the values of critical bounds are given by the authors of [32,35]. Table 5 reports the outcomes of ARDL-bounds testing; the values of FGDPPC (GDPPC/IEC, IGC, IOC, IVA), FIEC (IEC/GDPPC, IGC, IOC, IVA), FIGC (IGC/IEC, GDPPC, IOC, IVA), and FIOC (IOC/IGC, IEC, GDPPC, IVA) are 9.79, 5.66, 15.63, and 8.83, respectively, above the upper bound at the 1% and 5% significance level. These findings show the existence of a long-term equilibrium relationship among all variables. However, no cointegration association is found when industrial value added used the dependent variable, as the value of FIVA (IVA/IOC, IGC, IEC, GDPPC) is 2.35, showing below the lower bound at the 5% significance level. In addition, there is no cointegration relationship when renewable energy consumption is the dependent variable since 𝐹FREC (REC/IOC, IGC, IEC, GDPPC, IVA) is 2.10, below the lower bound at the 5% significance level.

The estimated outcomes of ARDL-bounds testing approve that four long term association occurs among industrial energy utilization (electricity, gas, and oil) and financial evolution in Pakistan. Additionally, to examine the strength of long-term co-integration relationships between industrial energy use (electricity, gas, and oil) and economic growth, the Johansen and Juselius co-integration approach with trace and maximum eigenvalue is used. The outcomes of Table 6 state the long-run relationships between energy consumption (electricity, gas, and oil) and monetary development in Pakistan.

4.4. Long-Run and Short-Run Analysis

Moving to investigate for long-term and short-term linkages between industrial energy consumption (electricity, gas, and oil) and financial progress in Pakistan with the ECM model. Table 7 shows that long-run coefficients of industrial electricity utilization and industrial gas consumption are 1.019 and 0.132, separately, stating a 1% escalation of industrial electricity consumption or industrial gas consumption causes a 1.019% or 0.132% increase in financial evolution of Pakistan, independently. Both industrial electricity consumption and industrial gas consumption have a positive influence on the fiscal evolution of Pakistan in the long run at 5%. Our findings are consistent with earlier studies [22,24,25,27,37,38]. However, industrial oil use has a negative influence on economic growth in the long term. This finding is similar to findings of [39]. Additionally, the long-run coefficient of industrial value added is 1.17, which implies that a 1% increase of industrial value added causes a 1.17% increase in fiscal development of Pakistan.

Our finding is similar to the results of previous findings of [40]. The outcomes of short-term vibrant coefficients are reported in Table 7. Industrial electricity utilization, gas use, oil consumption, and industrial value-added have an optimistic influence on the financial evolution of Pakistan in the short term. A 1% rise of industrial electricity consumption, industrial gas consumption, industrial oil consumption, and industrial value-added leads to a 0.27%, 0.08%, 0.15%, and 0.16% upsurge in financial progress, respectively, at the 1% and 5% impact levels. The short-term coefficients are lesser than the long-term coefficients for industrial power consumption (electricity, gas, and oil) and industrial value-added. Moreover, renewable energy consumption percentage of total energy consumption only influences the economic growth of Pakistan in the short run, but not for the long run. Thus, it infers that in long-term decisions, fossil fuels are a more significant contributor instead of renewable energy utilization for industrial output and economic progression of Pakistan. Consequently, the non-renewable energy consumption roots are a more indispensable input for industrial and economic progress compared with renewable energy utilization sources. The results of this work are consistent with previous findings in the literature [24,26,41,42,43,44,45,46,47].

4.5. Diagnostic Tests

Several diagnostics checks were operated to check good fit of the ARDL model. Table 8 reports that estimations are fine regarding normality, serial correlation, and heteroskedasticity, and the AR-root graph shows the stability of the model.

4.6. Granger Causality Analysis under VECM Context

The occurrence of co-integration provides us a chance to measure the directional casual connectedness among the variables. However, Table 9 illustrates the short-run causality ties in the VECM-based model. As the ARDL bound testing approach and Johansson cointegration were exercised, and demonstrated long-term cointegration equations existing among variables, in the meantime, granger causation in the short run through the VECM technique may yield necessary outcomes to express inferences for robust policy implications. Moreover, indications through the VECM model confirmed a bi-directional relationship of industrial sector oil use and financial progress in Pakistan. Similarly, industrial gas utilization and industry value added to (% of GDP) have one-way causality to economic growth in Pakistan.

Furthermore, the uni-directional nexus instituted between economic growth to industrial electricity use, manufacturing gas consumption to industrial electricity utilization, and industrial oil consumption to industrial electricity usage over 1983 to 2017 in the Pakistan. Additionally, a causal link runs from financial progress to industrial oil use and industrial gas consumption to industrial oil consumption. Finally, there is also one causativeness from industrial electricity utilization, industrial gas use, and industrial oil to industrial value added (% of GDP). Hence, the granger causality test under VECM uncovered solid interconnections among the studied variables and suggested that the Pakistani government should build a robust policy to diminish the oil, gas, and fossil fuels consumption for electricity production, as a replacement to depend on solar, hydro, wind, and biomass energy sources in Pakistan. Consequently, the government should inductee more gas concentrated projects, which will alleviate the contests of gas dearth and provide it to industry at cheap prices with ease.

4.7. Stability Tests

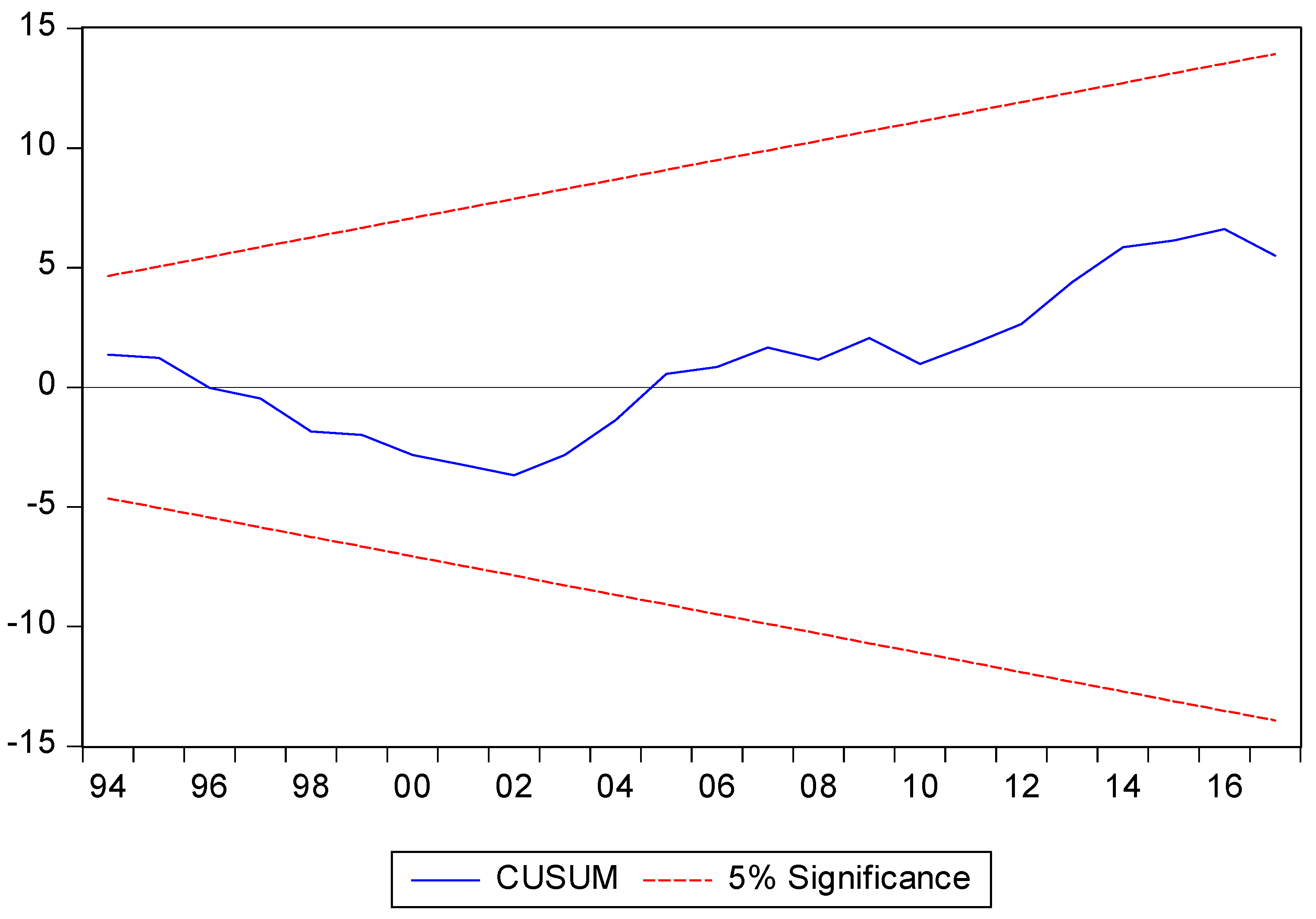

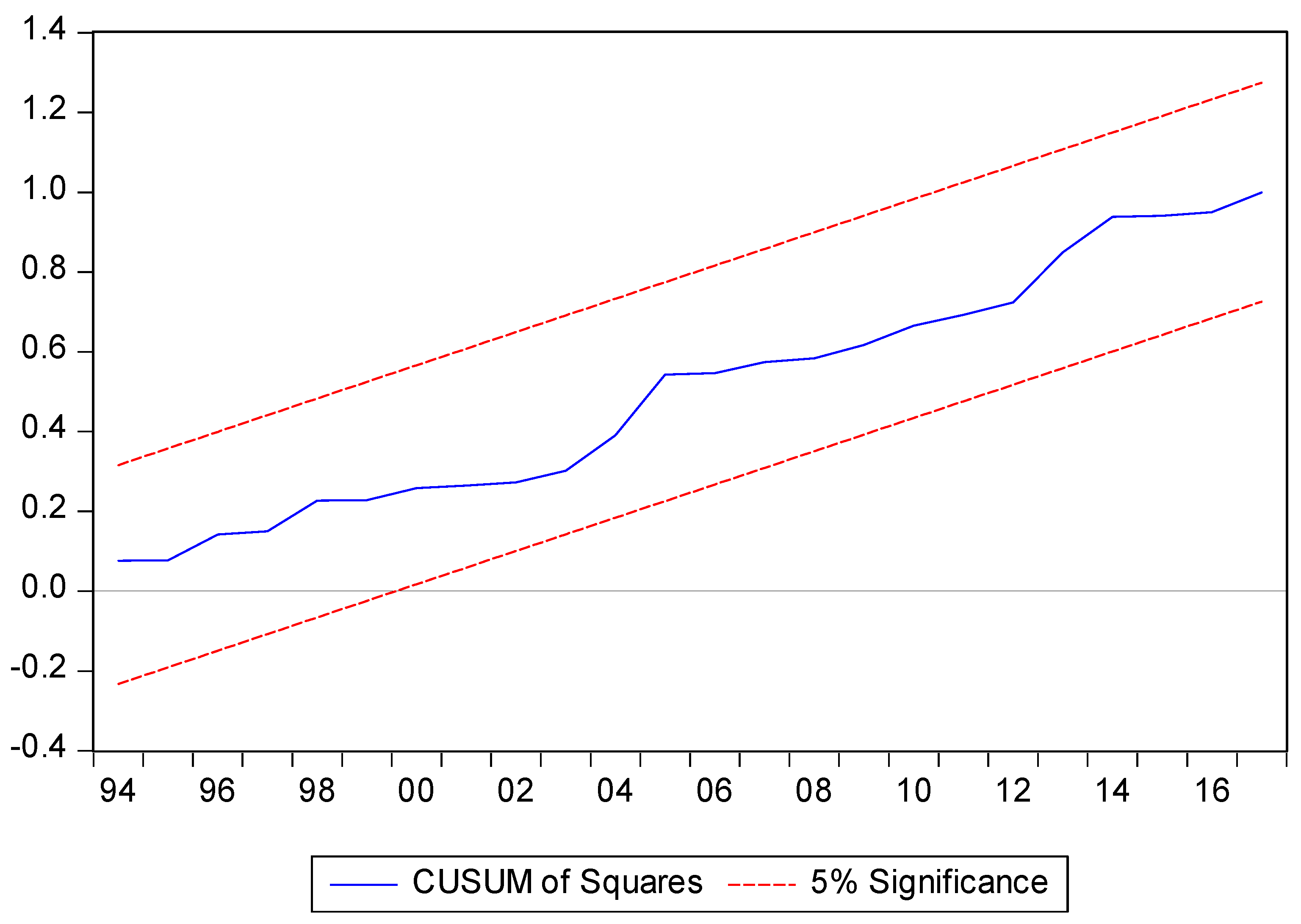

This empirical study also applied the CUSUM and CUSUMSQ tests to confirm the stability of strictures in ARDL regression model. As displayed in Figure 3 and Figure 4, both plots of the CUSUM and CUSUMSQ tests fall within limits, which approves the constancy of parameters. Therefore, the ARDL regression model and parallel limits for industrial energy usage (electricity, gas, and oil), industrial value added, renewable energy consumption, and economic growth in Pakistan are very much reliable.

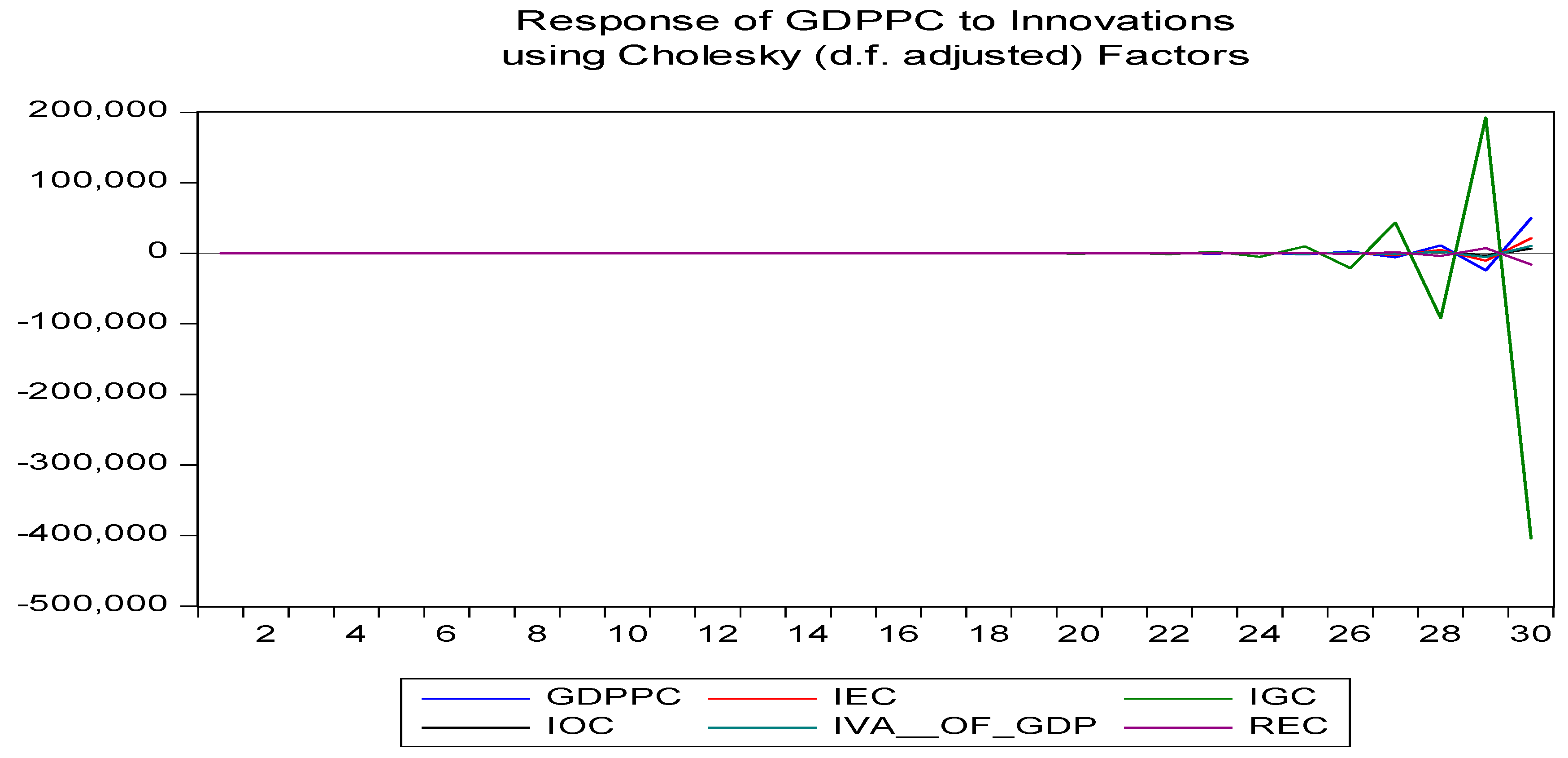

4.8. Impulse Response Fundtion

The impulse response function (IRF) under the VECM model postulated in Figure 5, at preliminary, the response of GDPPC for himself till 26 periods, is flat. The first 24 periods would have a flat trend near to zero for predicted and regressors, after reaching the 25th and afterwards, periods have a mixed trend prevail till the next 30th period. Similarly, other variables will also have the same behaviors till the end of the 30th period.

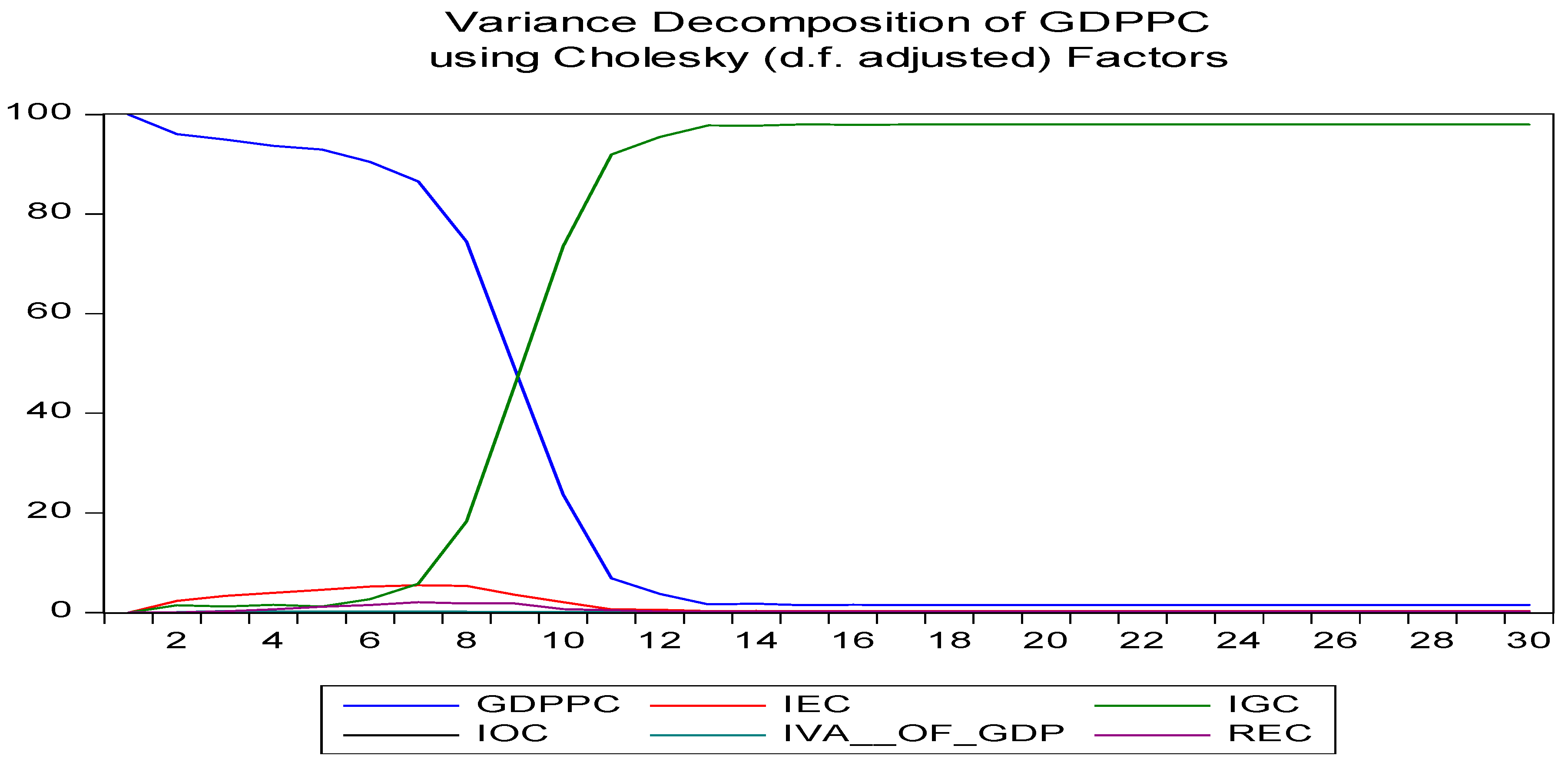

4.9. Variance Decomposition Analysis

In Figure 6, a falling trend for GDPPC in first seven periods can be noticed, and then flat at 5% at the end of the 30th period, while the other variables (IEC, IGC, IOC, REC, and IVA) would have an ascendant inclination and then will succeed to be flat till the 30th period. Henceforth, we may imply the inference that industrial oil, gas, and electricity consumption in Pakistan ought to be balanced in a vital landscape for its economic development and sustainability.

5. Conclusions and Policy Implications

This work explored the causal connection between industrial energy use and financial evolution in Pakistan using annual data from 1983 to 2017. The ARDL bounds testing method to cointegration was used to examine for the presence of long-term relationship between industrial energy usage through (oil, gas, and fossil fuels) and economic development. The findings display evidence of cointegration and the long-run connection between usage of industrial energy and monetary evolution in Pakistan. Moreover, indications through the VECM model confirmed a bi-directional relationship between industrial sector oil utilization and economic development in Pakistan. Similarly, industrial gas usage and industry value added (% of GDP) have one-way causality to economic growth in Pakistan. Furthermore, the uni-directional nexus instituted between economic growth to industrial electricity use, industrial gas utilization to industry electricity consumption, and industrial oil use to industrial electricity consumption for 1973–2017.

The outcomes showed that industrial electricity utilization and industrial gas consumption have a positive and statistically substantial influence on economic progress both in the long and short term. However, industrial oil consumption negatively impacts financial evolution in the long term, but for the short term, it has a positive and statistically substantial effect on financial progress in Pakistan. Hence, it confirms that oil-based energy utilization in long run has an adverse effect on economic output, so as to pay the overheads for fossil fuels energy production sources (IPP’s or other private energy producer companies) and cut the scale of gross domestic product (GDP). This becomes non-beneficial in the long run, but good in the short run for Pakistan’s economy.

The findings discovered solid interconnections among the studied variables and suggested that the Pakistani government should build a robust policy to diminish the oil, gas, and fossil fuel consumption for electricity production, as a replacement to depend on solar, hydro, wind, and biomass energy sources in Pakistan. Consequently, the government should promote more gas concentrated projects, which will alleviate the contests of gas dearth and provide it to industry at cheap prices with ease.

Our investigated results proposed that Pakistan’s government must supplement energy policies and focus on renewable energy production technologies instead of fossil fuels energy. Further energy resources, counting hydroelectric, nuclear-powered energy, wind energy, and solar power creators could be established in equivalence with natural gas utilization. It would be possible to sufficiently meet the energy demand of Pakistan. Thus, the sustainable energy plan is principally worthwhile to enlarge the usage of natural gas and oil in an effectual way, and complementary familiarize more and more of such initiatives with instantaneous investment for renewable energy sources.

As a final point, this current study extends the scope for investigation in an imminent period, as examiners may rehearse the presented methodological techniques to draw back more cognizance for oil and gas electricity utilization in industry links with financial progress in Pakistan. In addition, the current ARDL model technique may conversant with nonlinear asymmetric (NARDL) or may elevate by constructing an index of industrial progress instead of utilizing the single component as a substitute for industrial growth. The recent investigation hired the collective scale of CO2 emissions for the Pakistan; however, henceforward discovering the relationships among these variables with CO2 emissions at disaggregate scale (industry wise), and it may leap better-quality interpretations. Consequently, these might support to the policy designers for articulating environment friendly energy policies.

Author Contributions

All authors contributed to writing, editing, analysis, idea generation, and data collection. Conceptualization: A.A.C. and A.R.; Formal analysis, A.A.C. and A.R.; Funding acquisition, Y.J.; Investigation, A.A.C., F.A., and A.R.; Methodology, A.A.C. and A.R.; Software, A.A.C. and A.R.; Supervision, Y.J.; Writing—original draft, A.A.C. and A.R.; Writing—review and editing, A.A.C., A.R., and I.O.

Funding

This work was supported by Soft-science Program of Department of Sci-technology of Sichuan Province, Study on Theory, Mechanism and Policy for the Coupling of Modern Agri-Technology Innovation and Financial Innovation (Code: 18RKX0773).

Conflicts of Interest

The authors declare that there is no conflict of interest.

References

Kraft, J.; Kraft, A. On the relationship between energy and GNP. J. Energy Dev.1978, 3, 401–403. [Google Scholar]

Abdoli, G.; Farahani, Y.G.; Dastan, S. Electricity Consumption and Economic Growth in OPEC Countries: A Cointegrated Panel Analysis. Opec Energy Rev.2015, 39, 1–16. [Google Scholar] [CrossRef]

Zhang, X.P.; Cheng, X.M. Energy consumption, carbon emissions, and economic growth in China. Ecol. Econ.2009, 68, 2706–2712. [Google Scholar] [CrossRef]

Akhtar, S.; Hashmi, M.K.; Ahmad, I.; Raza, R. Advances and significance of solar reflectors in solar energy technology in Pakistan. Energy Environ.2018, 29, 435–455. [Google Scholar] [CrossRef]

Aized, T.; Shahid, M.; Bhatti, A.A.; Saleem, M.; Anandarajah, G. Energy security and renewable energy policy analysis of Pakistan. Renew. Sustain. Energy Rev.2018, 84, 155–169. [Google Scholar] [CrossRef]

Kamran, M. Current status and future success of renewable energy in Pakistan. Renew. Sustain. Energy Rev.2018, 82, 609–617. [Google Scholar] [CrossRef]

Mirjat, N.H.; Uqaili, M.A.; Harijan, K.; Valasai, G.D.; Shaikh, F.; Waris, M. A review of energy and power planning and policies of Pakistan. Renew. Sustain. Energy Rev.2017, 79, 110–127. [Google Scholar] [CrossRef]

Omer, A.M. Sustainable Energy Development, the Role of Renewables and Global Warming. J. Sustain. Dev. Stud.2012, 1, 1–67. [Google Scholar]

Rafique, M.M.; Rehman, S. National energy scenario of Pakistan – Current status, future alternatives, and institutional infrastructure: An overview. Renew. Sustain. Energy Rev.2017, 69, 156–167. [Google Scholar] [CrossRef]

Shakeel, S.R.; Takala, J.; Shakeel, W. Renewable energy sources in power generation in Pakistan. Renew. Sustain. Energy Rev.2016, 64, 421–434. [Google Scholar] [CrossRef]

Latif, A.; Ramzan, N. A review of renewable energy resources in Pakistan. J. Glob. Innov. Agric. Soc. Sci.2014, 2, 127–132. [Google Scholar]

Qureshi, F.; Akintuğ, B. Hydropower potential in Pakistan. In Proceedings of the 11th International Congress in Advances in Civil Engineering-ACE, Istanbul, Turkey, 21–25 October 2014. [Google Scholar]

Shaikh, F.; Ji, Q.; Fan, Y. The diagnosis of an electricity crisis and alternative energy development in Pakistan. Renew. Sustain. Energy Rev.2015, 52, 1172–1185. [Google Scholar] [CrossRef]

IRENA. Renewables Readiness Assessment: Pakistan; International Renewable Energy Agency (IRENA): Abu Dhabi, UAE, 2018. [Google Scholar]

Bank, W. Pakistan–World Bank Open Data–World Bank Group; The World Bank: Washington, DC, USA, 2018. [Google Scholar]

Aftab, S. Pakistan’s Energy Crisis: Causes, Consequences and Possible Remedies; Expert Analysis; The Norwegian Peacebuilding Resource Centre (NOREF): Oslo, Norway, 2014; p. 6. [Google Scholar]

Amber, K.P.; Ashraf, N. Energy outlook in Pakistan. In Proceedings of the 2014 International Conference on Energy Systems and Policies (ICESP), Islamabad, Pakistan, 24–26 November 2014; pp. 1–5. [Google Scholar]

Anwar, J. Analysis of energy security, environmental emission and fuel import costs under energy import reduction targets: A case of Pakistan. Renew. Sustain. Energy Rev.2016, 65, 1065–1078. [Google Scholar] [CrossRef]

Farooq, M.; Shakoor, A. Severe energy crises and solar thermal energy as a viable option for Pakistan. J. Renew. Sustain. Energy2013, 5, 501–514. [Google Scholar] [CrossRef]

Soytas, U.; Sari, R. The relationship between energy and production: Evidence from Turkish manufacturing industry. Energy Econ.2007, 29, 1151–1165. [Google Scholar] [CrossRef]

Campbell, J.; Perron, P. Pitfalls and Opportunities: What Macroeconomists NBER Macroeconomic Annual; Blanchard, O.J., Fischer, S., Eds.; MIT Press: Cambridge, MA, USA, 1991. [Google Scholar]

Hu, Y.; Guo, D.; Wang, M.; Zhang, X.; Wang, S. The relationship between energy consumption and economic growth: Evidence from China’s industrial sectors. Energies2015, 8, 9392–9406. [Google Scholar] [CrossRef]

Xu, G.; Pan, Q. The empirical study among energy consumption, economic growth and energy efficiency-based on 6 industries panel cointegration model and parsimonious vector error correction model. J. Cent. Univ. Financ. Econ.2009, 5, 63–68. [Google Scholar]

Zhang, C.; Jiao, X. Retesting the causality between energy consumption and GDP in China: Evidence from sectoral and regional analyses using dynamic panel data. Energy Econ.2012, 34, 1782–1789. [Google Scholar] [CrossRef]

Hamit–Haggar, M. Greenhouse gas emissions, energy consumption and economic growth: A panel cointegration analysis from Canadian industrial sector perspective. Energy Econ.2012, 34, 358–364. [Google Scholar] [CrossRef]

Shahbaz, M.; Lean, H.H.; Farooq, A. Natural gas consumption and economic growth in Pakistan. Renew. Sustain. Energy Rev.2013, 18, 87–94. [Google Scholar] [CrossRef]

Hassan, M.S.; Tahir, M.N.; Wajid, A.; Mahmood, H.; Farooq, A. Natural gas consumption and economic growth in Pakistan: Production function approach. Glob. Bus. Rev.2018, 19, 297–310. [Google Scholar] [CrossRef]

Sari, R.; Ewing, B.T.; Soytas, U. The relationship between disaggregate energy consumption and industrial production in the United States: An ARDL approach. Energy Econ.2008, 30, 2302–2313. [Google Scholar] [CrossRef]

Peseran, M.; Peseran, B. Working with Microfit 4: Interactive Econometric Analysis; Oxford University Press: Oxford, UK, 1997. [Google Scholar]

Pesaran, M.H.; Shin, Y. An autoregressive distributed-lag modelling approach to cointegration analysis. Econom. Soc. Monogr.1998, 31, 371–413. [Google Scholar]

Pesaran, M.H.; Shin, Y.; Smith, R.J. Structural analysis of vector error correction models with exogenous I (1) variables. J. Econom.2000, 97, 293–343. [Google Scholar] [CrossRef]

Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom.2001, 16, 289–326. [Google Scholar] [CrossRef]

Haug, A.A. Temporal Aggregation and the Power of Cointegration Tests: A Monte Carlo Study. Oxf. Bull. Econ. Stat.2002, 64, 399–412. [Google Scholar] [CrossRef]

Engle, R.F.; Granger, C.W. Co-integration and error correction: Representation, estimation, and testing. Econom. J. Econom. Soc.1987, 55, 251–276. [Google Scholar] [CrossRef]

Narayan, P.K. The saving and investment nexus for China: evidence from cointegration tests. Appl. Econ.2005, 37, 1979–1990. [Google Scholar] [CrossRef]

Liew, V.K. Which Lag Length Selection Criteria Should We Employ. Econ. Bull.2006, 3, 1–9. [Google Scholar]

Guan, X.; Min, Z.; Ming, Z. Using the ARDL-ECM Approach to Explore the Nexus Among Urbanization, Energy Consumption, and Economic Growth in Jiangsu Province, China. Emerg. Mark. Financ. Trade2015, 51, 391–399. [Google Scholar] [CrossRef]

Lu, W.C. Greenhouse Gas Emissions, Energy Consumption and Economic Growth: A Panel Cointegration Analysis for 16 Asian Countries. Int. J. Environ. Res. Public Health2017, 14, 1436. [Google Scholar] [CrossRef]

Chandio, A.A.; Jiang, Y.; Rehman, A. Energy consumption and agricultural economic growth in Pakistan: is there a nexus. Int. J. Energy Sect. Manag.2018. [Google Scholar] [CrossRef]

Hussin, F.; Yik, S.Y. The Contribution of Economic Sectors to Economic Growth: The Cases of China and India. Res. Appl. Econ.2012, 4, 38–53. [Google Scholar] [CrossRef]

Lu, W.C. Electricity consumption and economic growth: Evidence from 17 Taiwanese industries. Sustainability2016, 9, 50. [Google Scholar] [CrossRef]

Mohammadi, H.; Parvaresh, S. Energy consumption and output: Evidence from a panel of 14 oil-exporting countries. Energy Econ.2014, 41, 41–46. [Google Scholar] [CrossRef]

Siddique, H.M.A.; Majeed, M.T. Energy consumption, economic growth, trade and financial development nexus in South Asia. Pak. J. Commer. Soc. Sci. (PJCSS)2015, 9, 658–682. [Google Scholar]

Rauf, A.; Liu, X.; Amin, W.; Ozturk, I.; Rehman, O.; Hafeez, M. Testing EKC hypothesis with energy and sustainable development challenges: A fresh evidence from Belt and Road Initiative economies. Environ. Sci. Pollut. Res.2018, 25, 32066–32080. [Google Scholar] [CrossRef]

Chandio, A.A.; Jiang, Y.; Rauf, A.; Mirani, A.A.; Shar, R.U.; Ahmad, F.; Shehzad, K. Does Energy-Growth and Environment Quality Matter for Agriculture Sector in Pakistan or not? An Application of Cointegration Approach. Energies2019, 12, 1879. [Google Scholar] [CrossRef]

Rauf, A.; Liu, X.; Amin, W.; Ozturk, I.; Rehman, O.U.; Sarwar, S. Energy and Ecological Sustainability: Challenges and Panoramas in Belt and Road Initiative Countries. Sustainability2018, 10, 2743. [Google Scholar] [CrossRef]

Rauf, A.; Zhang, J.; Li, J.; Amin, W. Structural changes, energy consumption and Carbon emissions in China: Empirical evidence from ARDL bound testing model. Struct. Chang. Econ. Dyn.2018, 47, 194–206. [Google Scholar] [CrossRef]

Figure 1.

Power generation by sources in Pakistan. Source: International Energy Agency (IEA) estimation (2015).

Figure 1.

Power generation by sources in Pakistan. Source: International Energy Agency (IEA) estimation (2015).

Figure 2.

Sector-wise Power Consumption in Pakistan, Source: IEA estimation (2015).

Figure 2.

Sector-wise Power Consumption in Pakistan, Source: IEA estimation (2015).

Figure 3.

The graph of cumulative sum of residual (CUMSUM)

Figure 3.

The graph of cumulative sum of residual (CUMSUM)

Figure 4.

The graph of cumulative sum of square of residual (CUMSUMsq)

Figure 4.

The graph of cumulative sum of square of residual (CUMSUMsq)

Figure 5.

Impulse response function (IRF). Notes: the outcomes from impulse response function (IRF) for VECM model with regard to GDPPC in 30 future periods. GDPPC = gross domestic product; IEC = industrial electricity consumption; IGC = industrial gas consumption; IOC = industrial oil consumption; IVA = industrial value added (% of GDP); REC = renewable energy consumption.

Figure 5.

Impulse response function (IRF). Notes: the outcomes from impulse response function (IRF) for VECM model with regard to GDPPC in 30 future periods. GDPPC = gross domestic product; IEC = industrial electricity consumption; IGC = industrial gas consumption; IOC = industrial oil consumption; IVA = industrial value added (% of GDP); REC = renewable energy consumption.

Figure 6.

Variance decomposition analysis. Notes: the outcomes from variance decomposition analysis (VDA) for VECM model with regard to GDPPC in 30 future periods. GDPPC = gross domestic product; IEC = industrial electricity consumption; IGC = industrial gas consumption; IOC = industrial oil consumption; IVA = industrial value added (% of GDP); REC = renewable energy consumption.

Figure 6.

Variance decomposition analysis. Notes: the outcomes from variance decomposition analysis (VDA) for VECM model with regard to GDPPC in 30 future periods. GDPPC = gross domestic product; IEC = industrial electricity consumption; IGC = industrial gas consumption; IOC = industrial oil consumption; IVA = industrial value added (% of GDP); REC = renewable energy consumption.

Table 1.

Data description.

Table 1.

Data description.

Variables

Identifier

Data Source

Measurement

GDP per capita

GDPPC

World Bank (2017)

(Constant at US$ 2010)

Industrial Electricity Consumption

IEC

GOP (2017)

(Gwh)

Industrial Gas Consumption

IGC

GOP (2017)

(Mm cft)

Industrial Oil Consumption Renewable Energy Consumption

IOC REC

GOP (2017) World Bank (2017)

Tonnes (in % of total)

Industrial Value Added (% of GDP)

IVA

World Bank (2017)

(Percentage)

Table 2.

Descriptive statistics results.

Table 2.

Descriptive statistics results.

Variables

GDPPC

IEC

IGC

IOC

IVA

REC

Mean

7.477819

9.544628

11.90988

14.14587

3.071011

3.904881

Median

7.389545

9.488124

11.70710

14.16555

3.076900

3.906209

Maximum

7.964270

10.12803

13.47612

14.69774

3.239800

4.062016

Minimum

7.230333

8.625509

11.16368

12.87813

2.978500

3.765787

Std. Dev.

0.211073

0.430225

0.603618

0.366687

0.057475

0.080605

Skewness

0.864102

−0.493268

0.569714

−1.249650

0.852089

0.207743

Kurtosis

2.568201

2.362946

2.341809

5.438340

4.510785

2.033979

Jarque-Bera

4.627500

2.011175

2.525125

17.78000

7.563926

1.612662

Probability

0.098890

0.365830

0.282928

0.000138

0.022778

0.446493

Observations

35

35

35

35

35

35

Source: Authors’ computation.

Table 3.

Correlation matrix.

Table 3.

Correlation matrix.

Correlation

GDPPC

IEC

IGC

IOC

IVA

REC

GDPPC

1.00000

-----

IEC

0.81575 ***

1.00000

0.00000

-----

IGC

0.76761 ***

0.83248 ***

1.00000

0.00000

0.00000

-----

IOC

0.10181

0.47261 ***

0.19938

1.00000

0.56060

0.00410

0.25090

-----

IVA

0.71070 ***

0.63454 ***

0.52406 ***

0.23769

1.00000

0.00000

0.00000

0.00120

0.16920

-----

REC

−0.78614 ***

−0.53051 ***

−0.66701 ***

0.14620

−0.48330

1.00000

0.00000

0.00100

0.00000

0.40200

0.00330

-----

Source: Authors’ computation. Notes: *** Significant at the 1%; t-statistics are in [] and p-values are in ().

Table 4.

Augmented Dickey Fuller (ADF) and Phillip-Perron (PP) unit root test results.

Table 4.

Augmented Dickey Fuller (ADF) and Phillip-Perron (PP) unit root test results.

Variables

Statistics (Level)

Statistics (First Difference)

Conclusion

LnGDPPC

2.486532

−3.087439

−4.031597 ***

−4.419128 ***

I(1)

LnIEC

−2.329907

−2.822866

−2.870999 **

−3.327254 *

I(1)

LnIGC

−2.570594

−3.031467

−4.234173 ***

−10.71059 ***

I(1)

LnIOC

−2.411553

−2.309894

−5.299490 ***

−5.180570 ***

I(1)

LnIVA

−1.118967

−2.543110

−6.112228 ***

−6.068763 ***

I(1)

LnREC

−0.518581

−3.630334 **

−4.030535 ***

−4.391772 ***

I(1)

P-P unit root test

LnGDPPC

1.837307

−3.087439

−4.127932 ***

−6.135400 ***

I(1)

LnIEC

−2.329907

−2.822873

−2.870984 **

−3.327239 *

I(1)

LnIGC

−2.570594

−3.031467

−4.234173 ***

−10.74666 ***

I(1)

LnIOC

−2.263896

−2.309894

−5.180570 ***

−5.299490 ***

I(1)

LnIVA

−1.118967

−2.543110

−6.112228 ***

−6.068763 ***

I(1)

LnREC

−1.157980

−3.543668 ***

−3.976567 ***

−4.392851 ***

I(1)

Source: Authors’ computation. Notes: τμ represents intercept and τT represents the intercept and trend model. *, **, and *** denote rejection of the null hypothesis at the 1%, 5%, and 10% levels, respectively.

Table 5.

Results of bounds testing.

Table 5.

Results of bounds testing.

Dependent Variable

F-Statistic

K = 5

FGDPPC(GDPPC/IEC, IGC, IOC, IVA, REC)

9.79

FIEC(IEC/GDPPC, IGC, IOC, IVA, REC)

5.66

FIGC(IGC/IEC, GDPPC, IOC, IVA, REC)

15.63

FIOC(IOC/IGC, IEC, GDPPC, IVA, REC)

8.83

FIVA(IVA/IOC, IGC, IEC, GDPPC, REC)

2.35

FREC(REC/IOC, IGC, IEC, GDPPC, IVA)

2.10

Critical Value

Lower Bound

Upper Bound

10%

2.08

3.00

5%

2.39

3.38

2.5%

2.7

3.73

1%

3.06

4.15

Source: Authors’ computation.

Table 6.

Multivariate co-integration approach.

Table 6.

Multivariate co-integration approach.

Trace Test

Hypothesized No. of CE(s)

Eigenvalue

Trace Test

Critical Value at 5% Significance Level

Critical Value at 1% Significance Level

None *

0.769202

115.1202

95.75366

0.0012

At most 1

0.575991

66.73522

69.81889

0.0859

At most 2

0.476206

38.42123

47.85613

0.2840

At most 3

0.276481

17.08156

29.79707

0.6341

At most 4

0.127332

6.401812

15.49471

0.6480

At most 5

0.056156

1.907209

3.841466

0.1673

Maximum Eigenvalue Test

Hypothesized No. of CE(s)

Eigenvalue

Trace Test

Critical Value at 5% Significance Level

Critical Value at 1% Significance Level

None *

0.769202

48.38500

40.07757

0.0047

At most 1

0.575991

28.31399

33.87687

0.1994

At most 2

0.476206

21.33967

27.58434

0.2562

At most 3

0.276481

10.67975

21.13162

0.6792

At most 4

0.127332

4.494603

14.26460

0.8038

At most 5

0.056156

1.907209

3.841466

0.1673

Source: Authors’ computation. Notes: Trace test indicates 1 cointegrating equation(s) at the 10% level; trace test indicates 1 cointegrating equation(s) at the 1% level; max-eigenvalue test indicates 0 cointegrating equation(s) at the 5% level; max-eigenvalue test indicates 1 cointegrating equation(s) at the 1% level; *(**) denotes rejection of the hypothesis at the 5% (1%) level.

Table 7.

Long-run and short-run results.

Table 7.

Long-run and short-run results.

Variables

Coefficient

Std. Error

t-Statistic

Prob

Long-run estimation

LnIEC

1.019799 **

0.417555

2.442309

0.0217

LnIGC

0.132658 **

0.140996

−0.940862

0.0355

LnIOC

0.280343

0.240607

1.165149

0.2545

LnIVA

1.177475

0.879271

1.339149

0.1921

LnREC

−0.474488

0.812232

−0.584178

0.5641

C

−6.315801

8.909962

−0.708847

0.4847

Short-run dynamics

DLnIEC

0.275746 ***

0.078647

3.506142

0.0016

DLnIGC

0.083642 ***

0.032625

2.563776

0.0160

DLnIOC

0.150200 **

0.070754

2.122851

0.0427

DLnIVA

0.159913

0.210568

0.759435

0.4539

DLnREC

0.476239 ***

0.184023

2.587932

0.0156

CointEq(-1)

−0.118180 ***

0.014461

−8.172409

0.0000

R-squared

0.995438

Adjusted R-squared

0.993728

F-statistic

581.9346 ***

Prob(F-statistic)

0.000000

Source: Authors’ computation. Note: *** and ** indicate the levels of significance at 1% and 5%.

Chandio, A.A.; Rauf, A.; Jiang, Y.; Ozturk, I.; Ahmad, F.

Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability2019, 11, 4546.

https://doi.org/10.3390/su11174546

AMA Style

Chandio AA, Rauf A, Jiang Y, Ozturk I, Ahmad F.

Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability. 2019; 11(17):4546.

https://doi.org/10.3390/su11174546

Chicago/Turabian Style

Chandio, Abbas Ali, Abdul Rauf, Yuansheng Jiang, Ilhan Ozturk, and Fayyaz Ahmad.

2019. "Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan" Sustainability 11, no. 17: 4546.

https://doi.org/10.3390/su11174546

APA Style

Chandio, A. A., Rauf, A., Jiang, Y., Ozturk, I., & Ahmad, F.

(2019). Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability, 11(17), 4546.

https://doi.org/10.3390/su11174546

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.

Article Metrics

No

No

Article Access Statistics

For more information on the journal statistics, click here.

Multiple requests from the same IP address are counted as one view.

Chandio, A.A.; Rauf, A.; Jiang, Y.; Ozturk, I.; Ahmad, F.

Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability2019, 11, 4546.

https://doi.org/10.3390/su11174546

AMA Style

Chandio AA, Rauf A, Jiang Y, Ozturk I, Ahmad F.

Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability. 2019; 11(17):4546.

https://doi.org/10.3390/su11174546

Chicago/Turabian Style

Chandio, Abbas Ali, Abdul Rauf, Yuansheng Jiang, Ilhan Ozturk, and Fayyaz Ahmad.

2019. "Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan" Sustainability 11, no. 17: 4546.

https://doi.org/10.3390/su11174546

APA Style

Chandio, A. A., Rauf, A., Jiang, Y., Ozturk, I., & Ahmad, F.

(2019). Cointegration and Causality Analysis of Dynamic Linkage between Industrial Energy Consumption and Economic Growth in Pakistan. Sustainability, 11(17), 4546.

https://doi.org/10.3390/su11174546

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}