4.1. Descriptive Statistical Analysis of the Samples

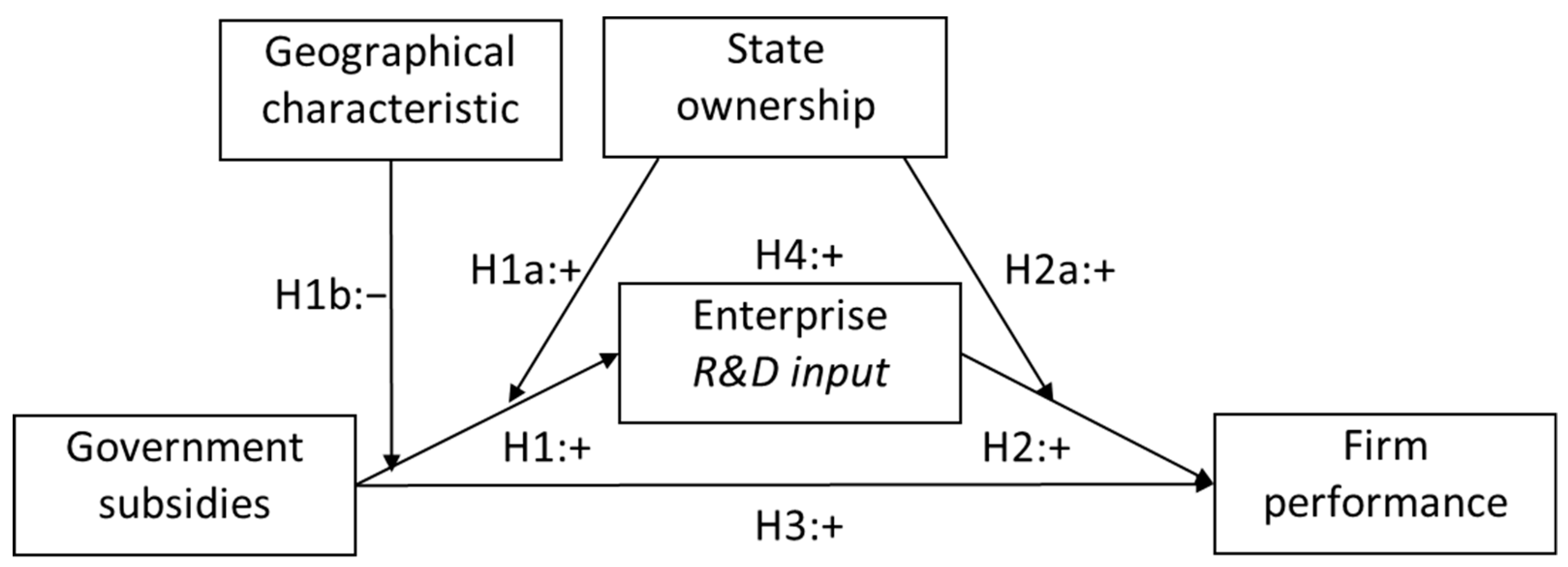

The 42 newly listed companies selected are classified according to state ownership type, geographical characteristics and industrial types. There are 12 state-owned enterprises and 30 non-state-owned enterprises. There are 22, 13, 3, and 4 companies in the home, photovoltaic, wind power, nuclear power, and biomass energy industries.

Stata software was used for the descriptive statistical analysis of the research variables of 42 A-share new energy enterprises listed in the Shanghai and Shenzhen stock exchanges from 2012 to 2016. The results are summarized in

Table 2.

From the analysis in

Table 2, the mean of return on equity (ROE), GS, RD, LEV, CF, SIZE, SO, and GC are −0.0030, 16.6157, 0.0430, 0.5228, 0.2805, 22.6474,0.7143, and 0.2619, respectively. The minimum and maximum values of ROE are GCL company integration in 2013 and 2015, respectively, which means that the firm performance has improved year by year. The minimum and maximum values of GS are solar energy company in 2012 and Shanghai electric company in 2013, respectively; the minimum and maximum values of

R&D are for Silver Star Energy in 2014 and Tianlong Optoelectronics in 2012, respectively. The mean of state ownership (SO) 0.7143 indicates the amount of non-state-owned enterprises is higher than that of state-owned enterprises in the sample. The mean of geographical characteristics (GC) 0.2619 shows the size of the eastern coastal area firms is more than that of non-eastern coastal area firms.

4.2. The Relationship Test between Government Subsidies and Enterprise R&D Input

To analyze the relationship between government subsidies and

R&D input, a panel multiple linear regression model is constructed as follows:

where

is the intercept,

is the coefficient, and

is the residual. A multi-panel regression is used to analyze panel data on 42 new energy listed companies from 2012 to 2016. To select a panel model that is suitable for the data features, first, the F-test,

BP test, and

Hausman test are used to determine the choice of the fixed-effects model for regression analysis. Problems related to intergroup heteroscedasticity and cross-section caused by multi-panel regression will lead to a biased estimation. To improve the accuracy of the estimation result and to show that bias is not an issue to the greatest extent possible. White and Newey corrections are used for processing. Because the time span of the panel data used is small, the sequence-related problems are not considered here. The regression results of the government subsidies and enterprise R&D input are shown in

Table 3 below.

The results of the data analysis are shown in

Table 3 and show that government subsidies (

β = 0.0041,

p < 0.05) are significantly and positively correlated with the R&D input of enterprises, which is consistent with the research results of documents [

53,

54,

55], and so on. That is, government subsidies have a positive effect on the R&D input of new energy companies. This result shows that when the government increases the amount of subsidies for new energy companies, these enterprises will increase their R&D input; when the government reduces the amount of subsidies for new energy companies, these enterprises will reduce their R&D input accordingly. Therefore, it is assumed that H1 is supported. In addition, the asset-liability ratio (

β = −0.0502,

p < 0.05) is significantly and negatively correlated with the R&D input of the enterprises; that is, the higher the asset-liability ratio of the enterprise, the less R&D input of the enterprise. The impacts of the enterprise scale and cash flow on the R&D input of the enterprise are not obvious.

4.3. Inspection of the State Ownership and Geographical Characteristics of Firms

Among the moderation variables, enterprise nature (state-owned, non-state-owned) and regional characteristics (the eastern coastal region and other coastal regions) are categorical variables. Because the independent variable, government subsidy, is a continuous variable, grouping regression analysis is conducted. After the test and adjustment, the final regression results are shown in

Table 4.

The results of the analysis are shown in

Table 4 and indicate that among the 42 new energy companies, the government subsidies of state-owned new energy enterprises (

β = 0.0042,

p < 0.05), and the government subsidies of non-state-owned enterprises (

β = 0.0076,

p < 0.05) are significantly and positively related to R&D input, but the coefficient for government subsidies for non-state-owned enterprises is larger than that of state-owned enterprises; that is, government subsidies promote the R&D input of non-state-owned new energy enterprises more strongly than that of state-owned enterprises. Therefore, it is assumed that H1a is supported; that is, state ownership has a significant moderating effect on the relationship between government subsidies and R&D input.

The reason for this phenomenon may be that management and institutional problems existing in state-owned enterprises have caused government subsidies to not be fully invested in R&D activities. Therefore, government subsidies have a weaker effect on R&D input. Therefore, the government should establish a corresponding supervision system to strengthen the measurement of the supervision and the subsidy effect of enterprises in terms of the use of relevant subsidies and guide enterprises to effectively use government subsidies. State-owned new energy enterprises should focus on improving internal governance and creating a good external environment for R&D activities. The environment should also focus on improving enthusiasm for internal technological innovation and R&D. In addition, in the group of state-owned enterprises, the enterprise scale, the asset-liability ratio, and the cash flow have no significant impact on the R&D input of the enterprise. In the group of non-state-owned enterprises, the asset-liability ratio (β = −0.0541, p < 0.1) is significantly and negatively correlated with the R&D input of the enterprise, while cash flow (β = 0.0037, p < 0.05) is significantly and positively correlated with the R&D input of the enterprise. This result shows that state-owned enterprises have not yet realized the role of real market players.

The regression results grouped by geographical characteristics show that the government subsidies of new energy enterprises in the eastern coastal areas (

β = 0.0060,

p < 0.05) are significantly positively correlated with the R&D input of enterprises; that is, the government subsidies of new energy enterprises in the eastern coastal areas have significant promotion of R&D input. The government subsidies for new energy enterprises in the other coastal areas (

β = −0.0021,

p < 0.05) are significantly negatively correlated with the R&D input of enterprises; that is, the government subsidies for new energy enterprises in the other coastal areas have a significant extrusion effect, and the results of this study are consistent with the results of document [

14]. This may be because the location conditions and resource endowments in the other coastal areas are poor, the degree of marketization is low, and the level of enterprise management is poor. Therefore, enterprises are less motivated and less conscious of technology R&D. However, government subsidies increase the income of new energy enterprises, which has caused these enterprises to be less interesting in technological innovation and R&D. Therefore, the government subsidies have a crowding-out effect on R&D input.

The scale of new energy enterprises in the other coastal regions (β = 0.0120, p < 0.01) has a significant positive impact on R&D input; the asset-liability ratio (β = −0.0877, p < 0.01) has a significant negative impact. The impact of cash flow on R&D input is not significant. In the eastern coastal areas, cash flow (β = 0.0040, p < 0.05) has a significant positive impact on corporate R&D input, while the asset-liability ratio and firm size have no significant impact on R&D input. According to the above analysis, H1b is supported; that is, the geographical characteristics are different, and the influence of government subsidies on R&D input of new energy enterprises is different. This means that the regional characteristics have significant effects on the regulation of government subsidies and R&D input.

4.4. The Relationship between Enterprise R&D Input and Firm Performance

To analyze the relationship between R&D input and the firm performance of new energy companies, based on documents [

12,

38], the panel multiple linear regression model is constructed as follows to test hypothesis 2:

The performance of the dependent variable in Equation (2) is measured by

ROE, where

is the intercept,

is the coefficient and

is the residual.

Table 5 shows the results of the regression analysis when the independent variable is ROE. Model II, Model III, and Model IV are the regression results of the enterprise’s R&D input without a lag period, lag phase 1, and lag phase 2, respectively. According to the Hausman test, Model I, Model II, and Model III in

Table 5 are better when the random effect model is used, while Model IV is better when the fixed effect model is used.

The results of the data analysis are shown in

Table 5 and show that when using

ROE to measure firm performance, the R&D input of new energy companies (

β = −1.2181,

p < 0.05) has a significant negative impact on current firm performance without a lag period. That is, the more R&D input of the enterprise in the current period, the greater the negative impact on the performance of the company. In addition, the size of the enterprise (

β = 0.0738,

p < 0.01) has a significant positive impact on the current firm performance; that is, the larger the enterprise, the better the current firm performance. The asset-liability ratio (

β = −0.5026,

p < 0.01) has a significant negative impact on the current firm performance; that is, the higher the asset-liability ratio of the enterprise, the worse the firm performance. Cash flow has a positive impact on the current firm performance. However, the impact is not significant.

Model III shows that the enterprise’s R&D input of lag phase 1 (β = −0.9797, p < 0.01) has a significant negative impact on firm performance; that is, the enterprise’s R&D capital investment will still have a negative impact on firm performance after one year. Model IV shows that the enterprise’s R&D input of the 2nd-order lag (β = 1.3382, p < 0.05) has a significant positive impact on firm performance; that is, the enterprise’s R&D input has positively promoted firm performance after 2 years. This result is similar to previous research conclusions. R&D capital investment and personnel input are significantly positively correlated with firm performance. The lag period of R&D capital investment is 1 period, and the lag period of R&D personnel investment is 2 periods.

The reason for this phenomenon may be that after a certain amount of R&D funds and R&D personnel are invested in the company, it takes a period of time for technology R&D to result in innovation. During this time, the funds and manpower invested cannot be immediately converted into enterprise income. The funds originally used by the company to improve performance are no longer available for other uses. Therefore, in the same year and one year after the investment, the enterprise’s R&D input has a significant negative impact on the firm performance. However, after investing in R&D funds for 2 years, the company has completed the development and application of new technologies and pushed new products to the market, so the firm performance has been significantly improved. It can be seen that the R&D input of enterprises has a significant positive impact on the performance of new energy enterprises, but it has a lag, and the lag period is 2 years. Therefore, we assume that H2 is supported.

The nature of the firm (state-owned, non-state-owned) has a significant moderating effect on the relationship between corporate R&D input and firm performance (

Table 6). The non-state-owned new energy enterprises’ R&D input (

β = −0.2754,

p < 0.05) has a significant negative correlation with the current firm performance and the state-owned new energy enterprise R&D input (

β = −0.4024,

p < 0.1) and the enterprise The current performance also has a significant negative correlation, but the negative impact of increased R&D input on state-owned new energy companies is greater than that of non-state-owned new energy companies. Therefore, if H2a is supported, then state ownership has different effects on the R&D input of enterprises. The impact of performance is different; that is, state ownership has a significant moderating effect on the relationship between R&D input and firm performance.

In the group of state-owned enterprises and the group of non-state-owned enterprises, the independent R&D input as measured by the independent variable are delayed by one period and delayed by two periods. According to the regression results, in the group of non-state-owned enterprises, the R&D input of the first phase (β = −0.1925, p < the R&D input of 0.05) and the lag phase 2 (β = 1.8851, p < 0.05) are significantly positively correlated with the firm performance. In the group of state-owned enterprises, the R&D input of the lagged phase 1 and lagged phase 2 were not related to firm performance.

In addition, in the group of non-state-owned enterprises, the enterprise scale (β = 0.1538, p < 0.1) has a significant positive correlation with the performance of new energy enterprises; that is, the larger the enterprise scale, the better the firm performance. The impact of asset-liability ratio and cash flow on firm performance is not significant. In the group of state-owned firms, the enterprise scale (β = 0.1080, p < 0.05) is significantly positively correlated with the performance of new energy companies and the asset-liability ratio (β = −1.1288, p < 0.1) Cash flow is significantly negatively correlated with firm performance, and the impact of cash flow on the performance of new energy companies is not significant.

4.5. The Mediation Effect of R&D Input on the Relationship between Government Subsidies and Firm Performance

First, based on documents [

12,

38], we conduct a regression analysis of the relationship between government subsidies and firm performance to test hypothesis 3 (Equation (3)).

The regression results of the independent government subsidy without a lag period and with lagged period 1 and lagged period 2 show that government subsidies for new energy enterprises (β = 0.0106, p > 0.1) have a positive impact on the current firm performance, but the impact is not significant. The government subsidy of the first phase (β = 0.0340, p > 0.1) still has a positive impact on the performance of new energy companies, but the impact is still not significant. The government subsidies of the second phase (β = 0.0356, p < 0.1) have a significant positive impact on the performance of new energy businesses. We assume that H3 is supported.

Second, we conduct a regression analysis of the relationships among government subsidies, R&D input and firm performance. The regression analysis of government subsidies and firm performance shows that government subsidies in the second phase are significantly and negatively correlated with firm performance. The R&D input in the 2 lagged phase is significantly and positively correlated with firm performance [

35]. Therefore, the mediating effect of R&D input with 2 lags on the relationship between government subsidies with 2 lags and firm performance (hypothesis 4) is tested by constructing models (4), (5), and (6) based on [

38].

The regression results are shown in

Table 7. In Model II, the dependent variable is firm performance (ROE) and the independent variable is government subsidy with the lag phase 2. In Model III, the dependent variable is the lag phase 2 R&D input and the independent variable is the lag phase 2 government subsidy. In Model IV, the dependent variable is firm performance (

ROE). According to the results of the Hausman test, Model II and Model IV are better when using the fixed effect model, and Model III is better when using the random effect model.

Table 7 shows that the regression coefficients for the independent variables in Model II and Model III are significant, and the coefficients for GS (−2) and RD (−2) in Model IV are significant when using the mediation effect test method. The partial mediation effect of R&D input is significant; that is, the relationship between the two-stage government subsidy and firm performance is transmitted through the partial mediation effect of the late stages of R&D input. Therefore, we assume that H4 is supported.

{kind=link}