Universal Basic Income and Inclusive Capitalism: Consequences for Sustainability

Abstract

:1. Introduction

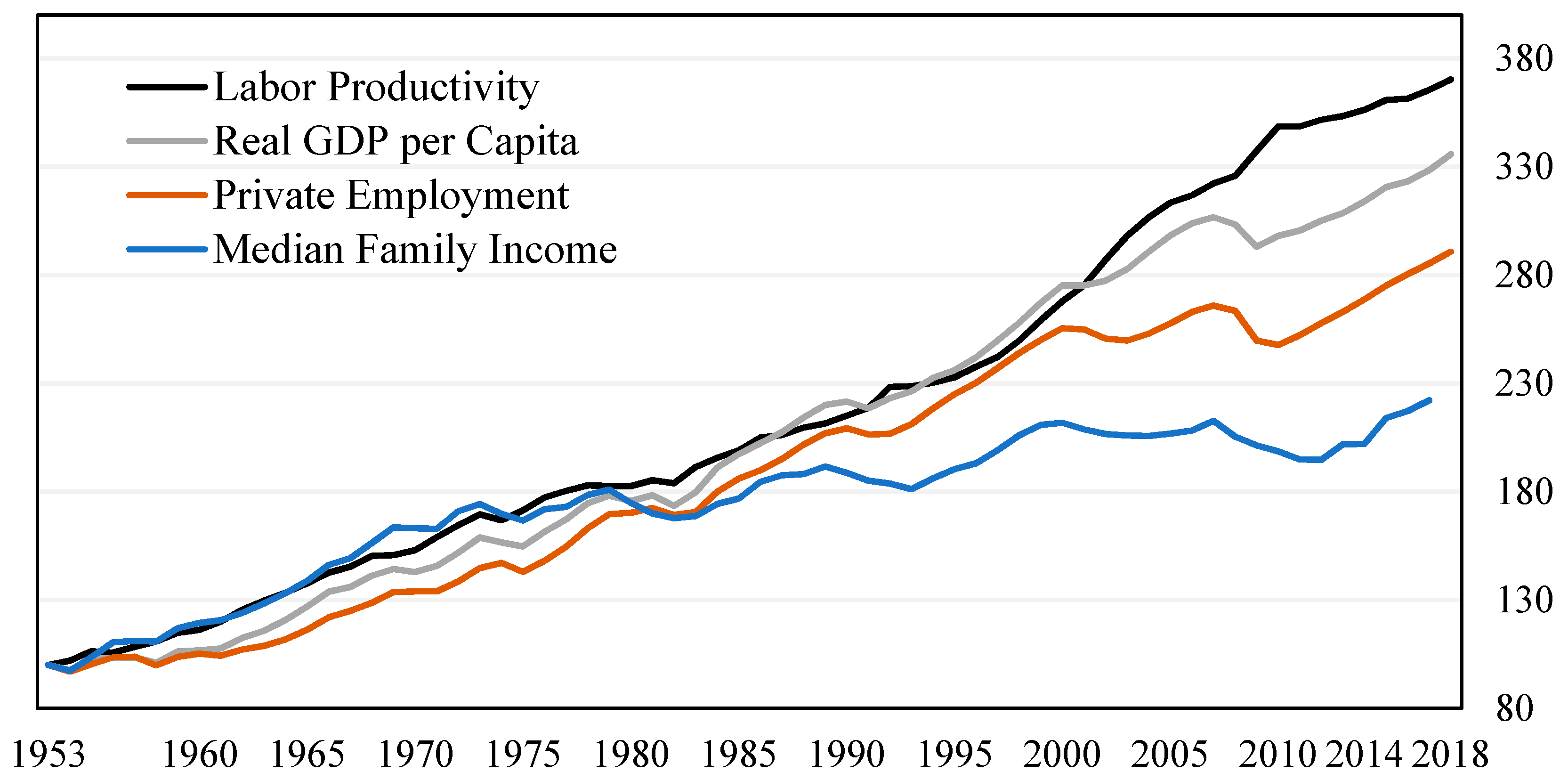

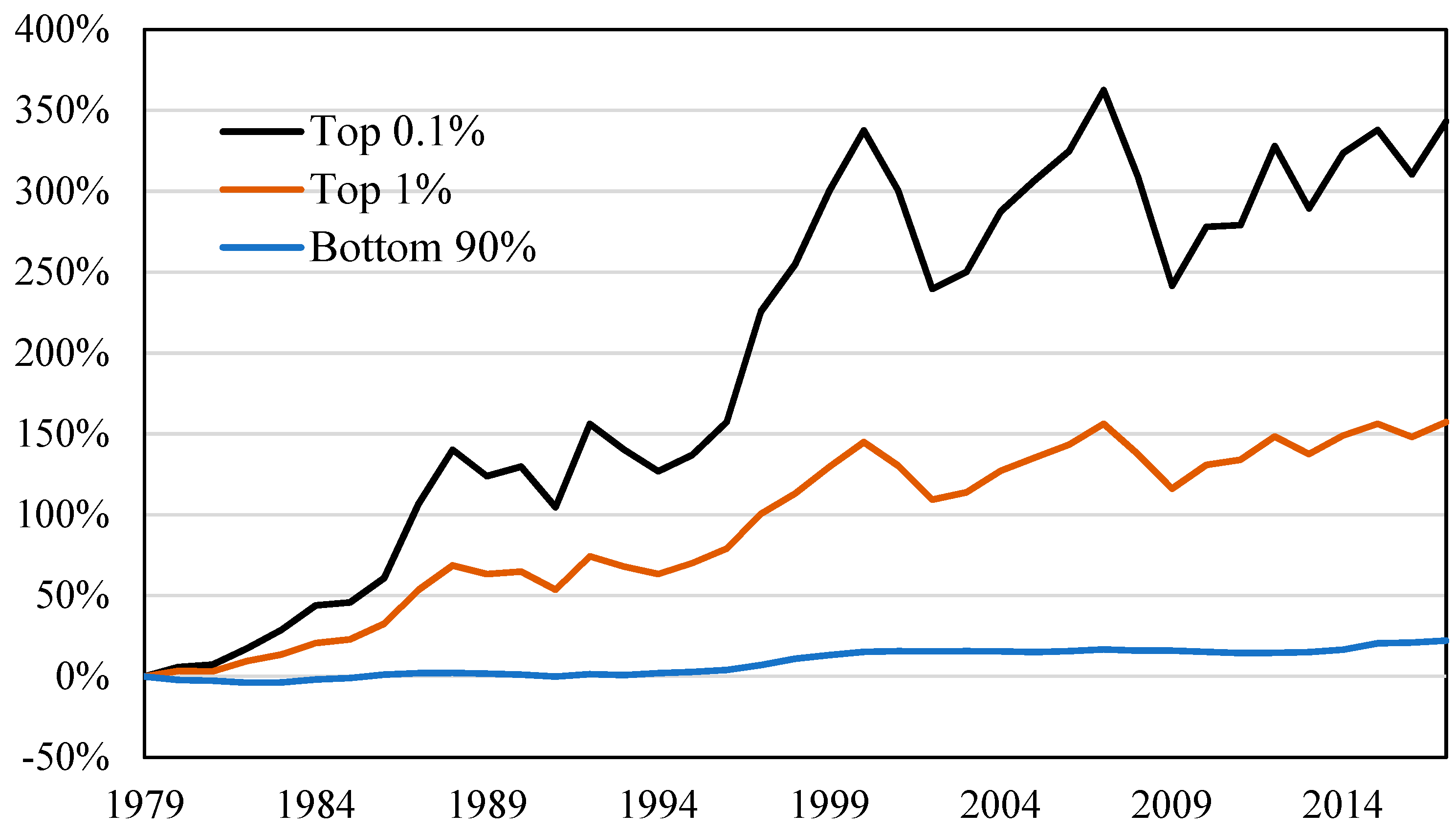

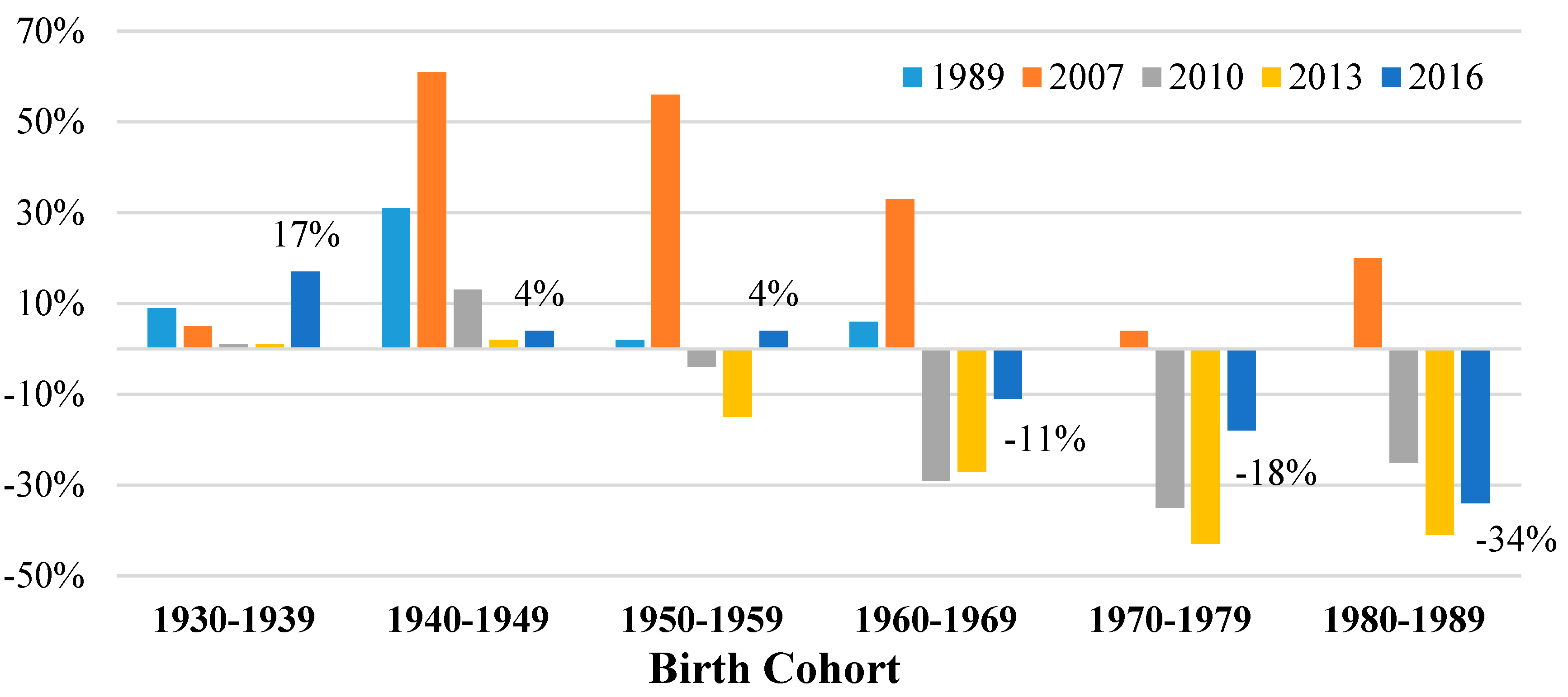

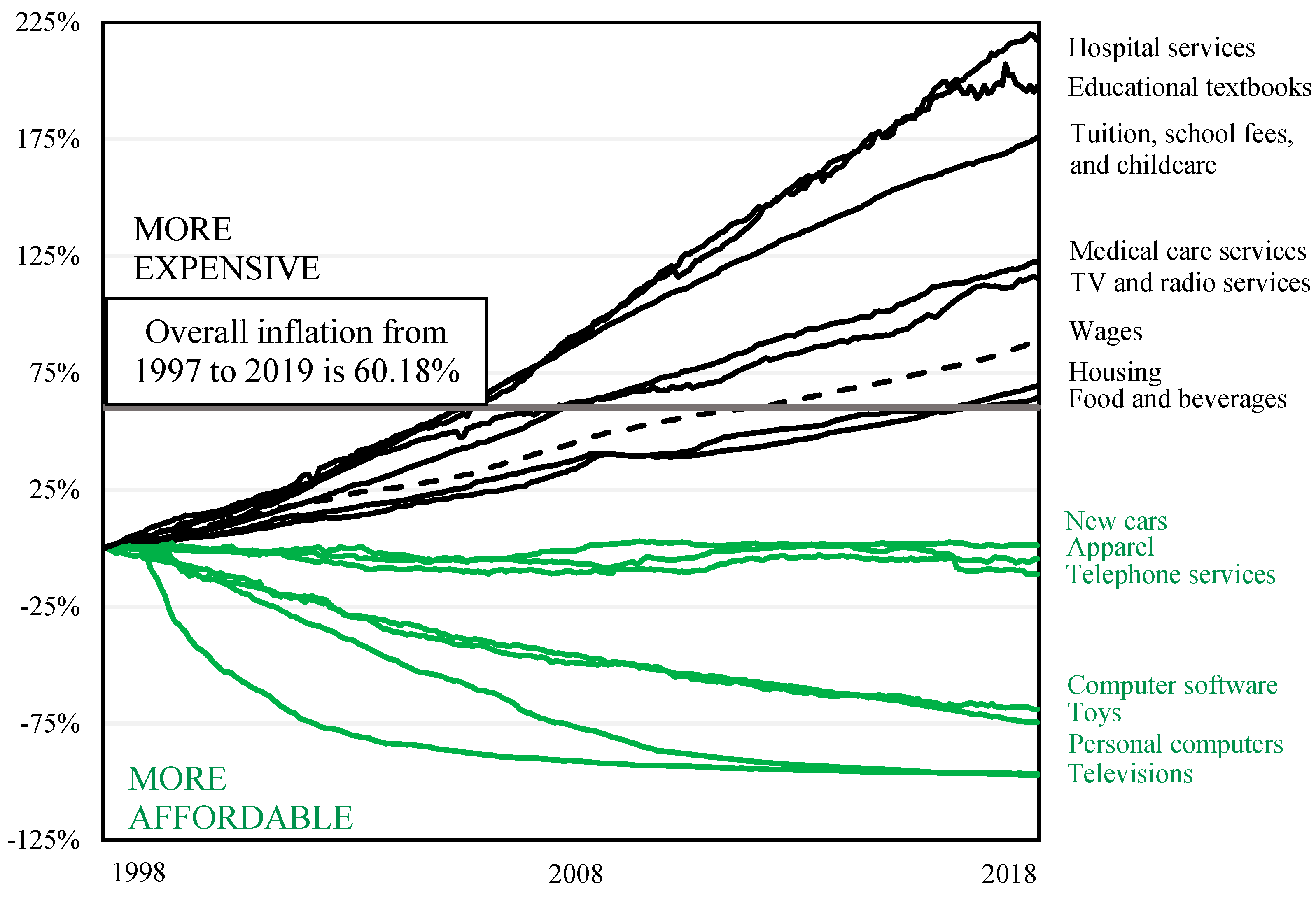

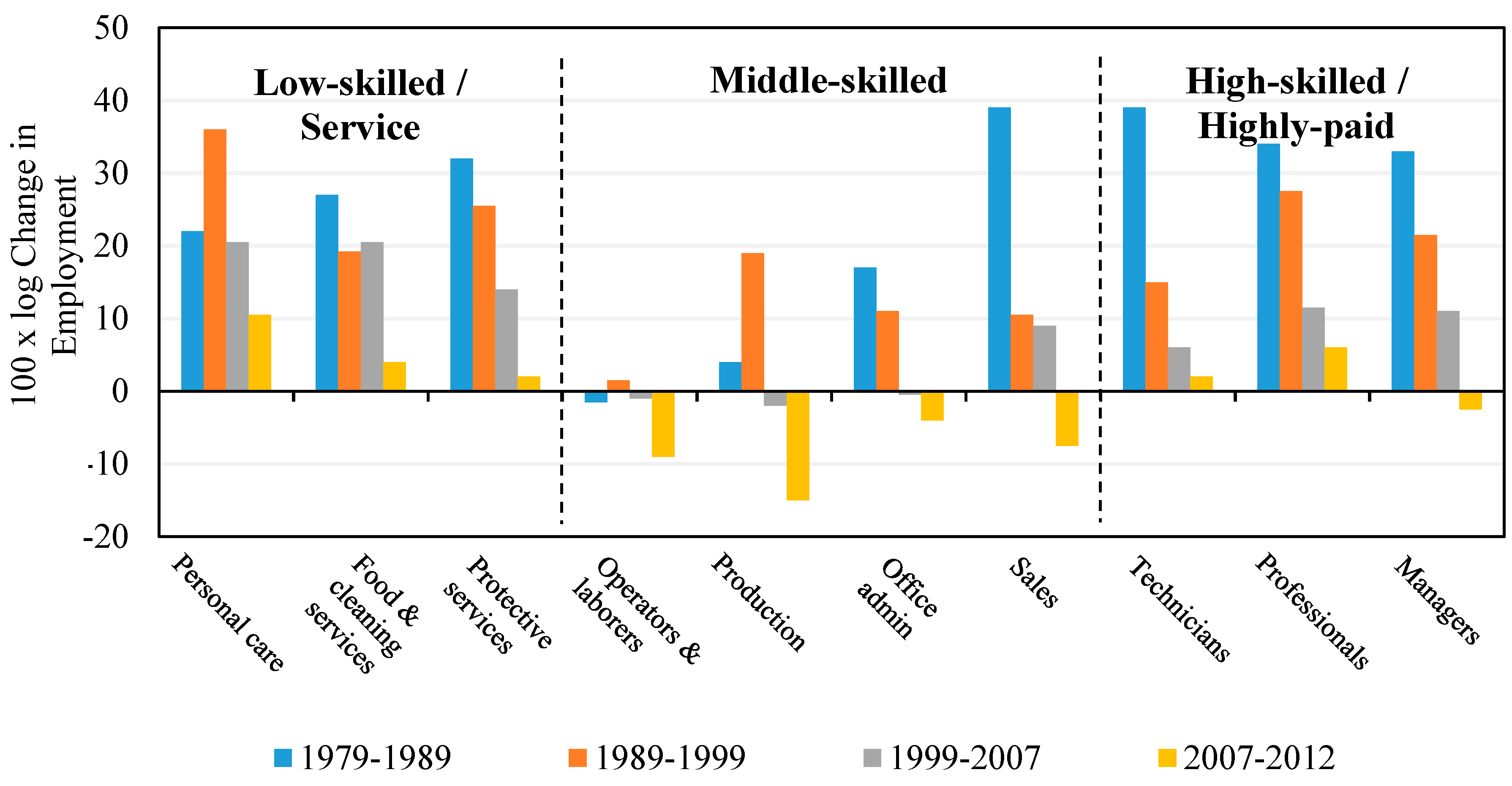

1.1. The Inequality Challenge

“Automation is imperceptibly but inexorably producing dislocations, skimming off unskilled labor from the industrial force. The displaced are flowing into proliferating service occupations. These enterprises are traditionally unorganized and provide low wage scales with longer hours”.[20] (p. 149)

1.2. The Environmental Challenge

1.3. Moving Beyond Green Growth

1.4. The EKC Hypothesis

2. Strategies to Provide a Universal Basic Income (UBI)

- an additional approach to fuller employment and per-capita growth;

- an additional approach to enhancing the earnings of poor and middle-class people in the age of automation/AI beyond minimum wage legislation, government jobs programs, and guaranteed minimum income (financed via redistribution mechanisms);

- a means to reduce the need for welfare distribution;

- an additional approach to environmental sustainability by (a) making greener technologies and regulations more affordable and politically achievable and (b) targeting ownership-broadening financing so as to promote the production of inherently sustainable goods and services;

- an additional approach to development and foreign assistance;

- an additional approach to globalization;

- an additional approach to privatization; and

- a means to reduce the need for economic immigration.

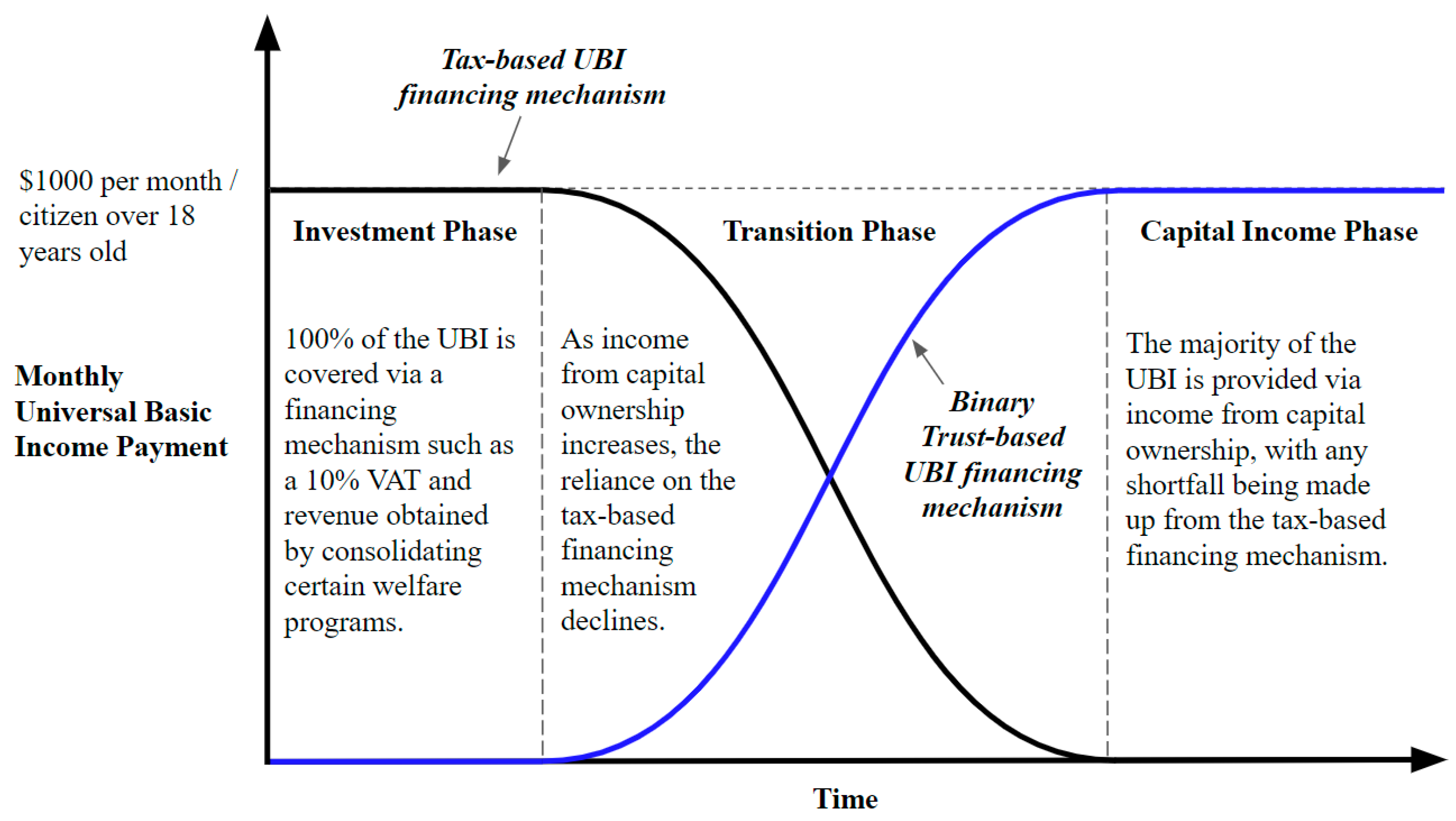

3. An Integrated and Environmentally Sustainable Approach to Providing a UBI

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Scheme/Program | Financing Mechanism | Income/Money Flow | Comments | Environmental Aspects |

|---|---|---|---|---|

| A Negative Income Tax (NIT) (inspired by Milton Friedman [87]) | A Negative Income Tax (NIT) system would tax individuals earning an income above a specified income threshold and redistribute this income to individuals earning less than the threshold. The amount of taxes paid or received would depend on the tax rates and how far an individual’s income falls above or below the threshold, respectively. | An income would only be received by individuals whose income falls below a specified income threshold. The amounts received would vary by individual. | If implemented following Friedman’s approach, the NIT would be designed to replace all welfare and assistance programs, with the specified income threshold set at a level that would still encourage people to work. | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Cost of Living Refund [88] | Modernization of the Earned Income Tax Credit (EITC) (also known as the Working Families Tax Credit) | Single people earning less than $50,000 a year would receive $4000 per year. Married couples earning less than $90,000 a year would receive $8000 per year. The payments can also be received monthly. | Over the past several years, a broad range of legislation has been proposed to modernize the EITC [115]. The Cost of Living Refund approach builds on these proposals and targets low-income and middle-class families by broadening eligibility to all workers aged 18+, including “childless” workers, and expanding the definition of work to include family caregivers and low-income students. | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Federal Job Guarantee Program (H.R. 1000−Jobs for All Act−submitted to the 116th U.S. Congress) | A National Full Employment Trust Fund (NFETF) would be held in the U.S. Treasury and funds would be appropriated to the NFETF from three sources (Sec. 102(1–3)): (1) revenues generated from a financial transaction tax (FTT); (2) funds from the Federal Unemployment Trust Fund that would have been provided to an unemployed individual if they were not participating in the proposed guarantee job program; and (3) an amount equal to the FICA (Federal Insurance Contributions Act), Medicare, and personal income taxes paid by participants in the proposed guarantee job program on their program earnings. Loans can also be made to the NFETF from the Federal Reserve to make up for any shortfall in the program, but these would need to be repaid (with interest equivalent to the return on 10-year Treasury bonds) over ten years unless the Federal Reserve decides that canceling the loans would have no negative effects on the economy. | The Federal Job Guarantee Program would prioritize the award of Employment Opportunity Grants to projects that provide affordable housing, childcare, transportation, and job training in areas with the greatest economic need. Participants enrolled in a work program would receive compensation that is comparable to public sector employees undertaking similar work (or work of comparable worth) in the geographic region of the program participant (Sec. 305(1)(D)). Participants enrolled in a job-training program would be eligible for a cost-of-living stipend set by standards established by the Secretary of Labor (Sec. 305(2)(A)). | The Jobs for all Act is based on the premise of the ‘right to work,’ whereas the other strategies included in this analysis primarily focus on ways to provide income support in the context of growing inequality. Of course, such support could help realize the human right to food, housing, healthcare, etc.In the context of this paper, a critical question is how resistant the jobs created by such a program would be to technological displacement? | The Federal Job Guarantee Program would require that all funded projects be carried out “in a manner that is as ecologically sustainable as is reasonably possible” (Sec. 304(10)). While a necessary requirement to limit the environment impacts of the program, the scale of the number of jobs created is unlikely to have a significant impact on the environmental performance of the U.S. economy. |

| UK Labour−Inclusive Ownership Fund (IOF) [89] | Companies with 250 or more employees would create an “inclusive ownership fund” (IOF) and transfer at least 1% of their ownership to this fund each year, up to a maximum of 10%. Smaller firms could set-up an IOF on a voluntary basis. The IOFs would be held and managed collectively, and shares would be non-tradeable. Fund representatives would have voting rights in a companies’ decision-making processes. | Workers in a firm with an IOF could receive up to £500 per month, after which any remaining dividends would be paid into a national fund to support public services and welfare programs. | The IOF scheme was proposed by the UK Labour Party in 2018. If implemented, the scheme could benefit 10.7 million people (40% of the private sector workforce). | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Lansley and Reed’s [90] Partial Basic Income (PBI) Proposal in the UK | The Partial Basic Income (PBI) program is estimated to cost about £300.2 billion per year, of which £118.2 billion would be covered by eliminating child benefit payments and state pensions and reducing means-tested benefits. The remaining £182 billion would come from eliminating personal allowance payments and increased national insurance and income tax rates. | Every British citizen would receive a weekly tax-free payment of £40 for those younger than 17 (£2080 annually), £60 for those aged 18–64 (£3120 annually), and £175 for people older than 65 (£9100 annually). Couples under 65 would receive £120 per week (£6240 annually), couples with one child would receive £160 (£8320 annually), and couples with two children would receive £200 (£10,400 annually). | The PBI program is designed to be revenue neutral, making it an implementable first step towards a Fuller Basic Income (FBI) program (see below). It is also designed to make the tax system more progressive. | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Lansley and Reed’s [90] Fuller Basic Income (FBI) Proposal in the UK | The Fuller Basic Income (FBI) program would build on the PBI (discussed above) and increase the weekly payments. The additional £26 billion a year needed to provide the higher weekly payments would come from a Citizen’s Wealth Fund created at the start of the PBI program, which would take some 20 years to reach maturity and start payments. The fund could be developed by transferring a range of existing commercial and public assets and profitable state-owned enterprises into the fund, one-off taxes on windfall profits, payments from corporations for the use of personal data, and increased taxation on wealth. In addition, large corporations could issue 0.5% of new shares annually that would pay directly into the fund, up to a maximum of 10% over 20 years (an approach that is similar to the IOF discussed above). It is estimated that the fund would need to reach £650 billion to provide the £26 billion needed for the higher basic income payments. The fund would be managed with a long-term investment horizon and kept in trust in perpetuity. All British citizens would have a direct ownership stake in the fund. | The FBI program would increase the PBI weekly payments. Every British citizen would receive a weekly tax-free payment of £50 for those younger than 17 (£2600 annually), £80 for those aged 18-64 (£4160 annually), and £180 for people older than 65 (£9360 annually). Couples under 65 would receive £160 per week (£8320 annually), couples with one child would receive £210 (£10,920 annually), and couple of two children would receive £260 (£13,520 annually). | The FBI program’s focus on capital ownership is intended to provide all British citizens with a stake in the future of the economy. The independence of the Citizen’s Wealth Fund from the state is considered as necessary to protect the fund from government interference and provide greater income security, independent of government, to future generations. Interestingly, the fund’s ownership of corporate shares is considered as one way for citizens to financially gain from job-displacing productivity growth from AI/automation (see the discussion below on binary economics). | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Andy Stern’s [91] Universal Basic Income (UBI) Proposal | The Universal Basic Income (UBI) would be funded using a broad range of options, including: (1) eliminating many of the existing 126 welfare programs; (2) eliminating/reducing the government’s tax expenditures (e.g., removing tax deductions); (3) implementing a 5%–10% value added tax (VAT) on goods and services; (4) implementing a financial transaction tax (FTT); (5) creating a “common wealth” fund based on Peter Barnes’ idea for a Common Wealth Trusts (see below); (6) establishing a 1.5 percent wealth (or net worth) tax on personal assets over $1 million; and (7) considering ways to reduce government expenditure related to military spending, farm subsidies, subsidies to oil and gas companies, etc. | Every U.S. Citizen between 18 and 64 would receive $1000 a month, regardless of income or employment status. All senior citizens who do not receive at least $1000 per month in Social Security payments would also receive $1000 per month. | Stern’s [91] proposal is based on the premise that efficiency and labor productivity will continue to undermine/replace jobs, forcing people into more contingent forms of employment. | The proposal has the potential to consider the environmental impacts related to a UBI, but only if a common wealth fund is created based on the principles discussed by Common Wealth Trusts (CWTs)—see below. There is also the critical questions of the relative scale of the critical ecosystems that would be put into trust and the contribution of the common wealth fund to the UBI when compared to the other funding options—i.e., the greater the contribution, the greater the potential for consumer education and environmental protection. |

| Andrew Yang’s [11] Universal Basic Income (UBI) Proposal | A 10% value added tax (VAT) on the production of goods or services a business produces. Certain welfare programs (unspecified) would be consolidated. | Every U.S. citizen over the age of 18 would receive $1000 a month, regardless of income or employment status. If Andrew Yang is elected as U.S. President in 2020, the scheme would start in January 2021. | Like Stern’s [91] proposal, Yang’s [11] plan is based firmly on the idea that automation and AI are displacing jobs and that a UBI is necessary given the continued impact of this displacement. Yang also argues that the UBI would result in job growth from the increased effective demand among consumers and the need for industry to increase production to meet this demand. | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Assured Income [9] | Revenue streams from a range of potential sources would be deposited in a trust fund managed by the Social Security Administration (SSA). These sources include a value added tax (VAT), taxes on unearned income, a carbon dioxide tax, and transaction fees on the trading of securities and derivates. | Children (0–17) would receive $100–$200 per month; working age adults (18–64) would receive $200–$400 per month; older individuals (64+) would receive $100–$200 per month | The proposed program would benefit 326 million people. At the lower-benefit level, the cost of the program would be $632.4 billion. At the higher-benefit level the cost would be $1.265 trillion. An interesting aspect of the proposal is that the SSA could be authorized to invest in securities other than Treasury bonds, enabling the trust to act like a pension fund or Sovereign Wealth Fund (SWF). | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Chris Hughes’ [92] Guaranteed Income for Working People | A tax on annual incomes of $250,000 or more would be used to underwrite the program. | A guaranteed income of $500 a month would be provided to every working adult who lives in a household with an annual income of less than $50,000. | It is estimated that 60 million adults would receive the guaranteed income at an annual cost of $290 billion. The program is designed to encourage work. | The program has no direct components that could improve the environmental performance of firms or shape consumer spending. |

| Iran’s Cash Transfer Program [93,94] | In 2010, Iran enacted a cash transfer program (via the Targeted Subsidy Reform law) to provide its citizens with a universal and unconditional income. The program is funded from revenues generated from removing price subsidies on fuel and food that accounted for around 80% of all subsidies. The program did not require new claims from the national budget, nor did it use oil export revenues. | In 2012, the program was providing monthly payments of 455,000 rials (worth USD $40 in 2012 and around $11 today) for approximately 70 million citizens (95 percent of Iran’s population). The transfers do not eliminate existing benefits. | In 2012, the program costs exceeded the available tax revenues by one third, forcing the government to print money that caused significant inflation (up to 40% in 2013), undermining the early gains made by the program. In 2016, the Iranian Parliament approved a bill to cut the cash payments to 24 million Iranians who already receive social welfare and who work in the public sector. | The removal of price subsidies on fuel can be viewed as a tax on the present consumption of oil. All countries (not only resource-rich ones) could use this scheme to ensure consumers pay the full market price for fuel. |

| The Alaska Permanent Fund (APF) [95] | At least 25% of all mineral lease rentals, royalties, royalty sale proceeds, federal mineral revenue sharing payments, and bonuses received by the State are placed in the Alaska Permanent Fund (APF)—valued at $64.9 billion (2018). The fund’s principal should be used for income-producing investments and cannot be spent without a constitutional amendment approved by Alaskan voters. | Each year, the Permanent Fund Dividend program provides Alaska residents with an annual dividend payout that typically falls between $1000–$2000. | The residents of Alaska have consistently voted to protect the Alaska Permanent Fund against efforts to use the fund’s principal to cover government deficits/spending. | While the APF is invested globally across seven asset classes—(1) Public Equities, (2) Fixed-Income Plus, (3) Private Equity and Special Opportunities, (4) Real Estate, (5) Infrastructure, (6) Absolute Return Strategies, and (7) Allocation Strategies—there is no explicit strategy to target sustainable investment opportunities. |

| American Solidarity Fund (ASF) [96] | The American Solidarity Fund (ASF) would be made up from a combination of voluntary contributions, ring-fencing existing state assets, levies (taxes and fees), leveraged purchases, and monetary seigniorage. The ASF would be managed by a public entity (a new state-owned enterprise—e.g., the America Solidarity Fund Corporation) to generate investment returns that would fund a universal basic dividend for U.S. citizens. | Every U.S. citizen over the age of 17 would be given one nontransferable share of ownership in the ASF, which would entitle them to receive a Universal Basic Dividend (UBD). The UBD would be equal to a five-year moving average of a percentage of the ASF’s market value. The amount received each year would depend on the size of the ASF and its five-year performance. | In contrast to the Alaska Permanent Fund, the ASF would provide citizens with a formal ownership share that cannot be sold and would return to the ASF upon death. | The allocation of the ASF’s assets would be determined by Congress or Treasury mandates. Companies could be excluded from the fund if they violate established guidelines—e.g., engage in human rights violations or environmental destruction. (The ASF could model their list of excluded companies following Norway’s sovereign wealth fund exclusion list [111].) |

| Peter Barnes [97] Common Wealth Trusts | Common Wealth Trusts (CWTs) would manage the rights to critical ecosystems for which asset preservation is the paramount mission. The CWTs would be organized as “legal shells” (not-for-profit corporations with state charters, self-governance, perpetual life, and legal personhood) and have fiduciary responsibility to future generations (the managers of these not-for-profit corporations would be required to protect their assets for future generations and to share current income—if any—equally). Corporations wishing to use (or pollute) a critical ecosystem would need to pay for this right. The actual design, structure, and management of the CWTs would require research, discussion, and experimentation. Thus, additional work is needed to fully develop the concept. | The CWTs would belong to all citizens who would receive dividend payments from the CWTs. The amount of these payments is not specified. | The CWTs would provide a counter-weight to profit-maximizing companies within a market economy; in this context, the state would need to ensure a proper balance between business and organized common wealth. The creation of trust-administered property rights to protect ecosystems is considered to be more effective than a redistributive taxation approach on the grounds that property rights tend to endure. | The CWTs would be legally accountable to future generations and would have the authority to limit the use of threatened ecosystems and charge for the use of public resources. Thus, rather than providing citizens with a corporate ownership stake, they would have an ownership stake in the natural/environmental common wealth. |

| Robert Ashford’s [98,99] Inclusive Capitalism (based on binary economics) | Inclusive capitalism is based on the principle of “binary growth.” According to this principle, a broader distribution of capital acquisition with the earnings of capital distributes capital income more broadly in future years (thereby producing more effective future consumer demand) and therefore more demand for investment in capital and labor in earlier years. Thus, if capital can competitively pay for its acquisition costs out of its future earnings primarily for existing owners, the same institutions and practices that work profitably for well-capitalized people and corporations can do so even more profitably if all people are included in the acquisition process (a process called ownership-broadening binary financing). The institutions that can be used most effectively to competitively acquire capital with the earnings of capital for poor and middle-class people are the largest three thousand or so credit-worthy corporations (roughly comprising the Russell Index) working cooperatively with professional investment trust (“Binary Trust”) fiduciaries (such as Fidelity, T. Rowe Price, TIAA-CREF, and Vanguard). If implemented at a national scale, a Binary Trust could borrow money from banks and other lenders and use it to acquire dividend-paying common shares issued to the trust fiduciaries by participating companies. The share acquisition loans would be collateralized by private and/or public capital credit insurance and would be repaid with the earnings of the capital acquired, after which the capital earnings would be broadly distributed to its beneficiaries (who could be citizens, employees, consumers, and/or welfare recipients). | The beneficial owners would be selected by the participating companies in conformity with legislated eligibility and nondiscrimination rules. No income would be distributed to the binary beneficiaries unless their capital has repaid all current acquisition debt obligations. Thereafter, beneficiaries would receive net income only after all expenses of production are paid and all necessary reserves for depreciation and research and development are set aside to maintain the capital in a competitive condition.Unlike income enhancement via a UBI, this inclusive capitalism approach does not guarantee or prescribe any absolute amount of income; the amount paid in dividends to beneficiaries according to this approach depends on the earning capacity of the capital acquired. However, this binary approach could be employed along with other approaches that do provide for an absolute payment and the dividends paid can be used to reduce, eliminate, or supplement reliance on such approaches (see Section 3 of this paper). | Enabling all people to increase their earning capacity by acquiring capital with the earnings of capital requires no redistribution of prior accumulated income/wealth and reduces no competitive claim on future wealth. Ownership-broadening binary financing offers the prospect of a competitive alternate distribution of the ownership of, and income from, rationally expected future growth. The approach is based on an analysis recognizing that a broader distribution of capital acquisition in future years provides greater incentive to employ labor and capital in earlier years. | With bank loans secured by private capital credit insurers, ownership-broadening trusts could invest (on behalf of designated beneficiaries) in common stock voluntarily issued by companies that are advancing inherently sustainable forms of development. The trust could go beyond Norway’s list of excluded companies and review investments using lifecycle assessment and other accepted forms of sustainability analysis. In addition, the trust could finance the growth of employee-owned B Corporations that frequently outperform investor-controlled corporations from an environmental and social perspective [112]. |

References

- Bernstein, A.; Raman, A. The great decoupling: An interview with erik brynjolfsson and andrew mcafee. Harv. Bus. Rev. 2015, 93, 66–74. [Google Scholar]

- The Urban Institute. Nine Charts about Wealth Inequality in America (Updated). Available online: http://apps.urban.org/features/wealth-inequality-charts/ (accessed on 19 June 2019).

- Federal Reserve Bank of St. Louis. Louis. Essay no. 2. A Lost Generation? Long-Lasting Wealth Impacts of the Great Recession on Young Families; Federal Reserve Bank of St. Louis: St. Louis, MO, USA, 2018; pp. 6–21. [Google Scholar]

- Economic Policy Institute (EPI). Annual Wages by Wage Group; State of Working America Data Library. Available online: https://www.epi.org/data/#?subject=wagegroup (accessed on 18 August 2019).

- Akers, B.; Chingos, M.M. Game of Loan: The Rhetoric and Reality of Student Debt; Princeton University Press: Princeton, NJ, USA, 2016. [Google Scholar]

- Auerbach, D.I.; Kellermann, A.L. How does Growth in Health Care Costs Affect the American Family? Rand Corporation: Santa Monica, CA, USA, 2011. [Google Scholar]

- Dieleman, J.L.; Squires, E.; Bui, A.L.; Campbell, M.; Chapin, A.; Hamavid, H.; Horst, C.; Li, Z.; Matyasz, T.; Reynolds, A.; et al. Factors associated with increases in us health care spending, 1996–2013. JAMA 2017, 318, 1668–1678. [Google Scholar] [CrossRef] [PubMed]

- Ashford, N.A.; Hall, R.P. Technology, Globalization, and Sustainable Development: Transforming the Industrial State; Routledge: New York, NY, USA, 2018; p. 772. [Google Scholar]

- Arnone, W.J.; Barnes, P.; Landers, R.M. Assured Income; National Academy of Social Insurance: Washington, DC, USA, 2019. [Google Scholar]

- Brynjolfsson, E.; McAfee, A. The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies; W. W. Norton & Company: New York, NY, USA, 2014. [Google Scholar]

- Yang, A. The War on Normal People: The Truth about America’s Disappearing Jobs and Why Universal Basic Income Is Our Future; Hachette Books: New York, NY, USA, 2018. [Google Scholar]

- McKinsey Global Institute. A Future that Works: Automation, Employment, and Productivity; McKinsey & Company: New York, NY, USA, 2017. [Google Scholar]

- Perry, M.J. Chart of the Day (Century?): Price Changes 1997 to 2017. Available online: http://www.aei.org/publication/chart-of-the-day-century-price-changes-1997-to-2017/ (accessed on 18 June 2019).

- Autor, D. Why are there still so many jobs? The history and future of workplace automation. J. Econ. Perspect. 2015, 29, 3–30. [Google Scholar] [CrossRef]

- Pew Research Institute. The State of American Jobs: How the Shifting Economic Landscape in Reshaping Work and Society and Affecting the Way People Think about the Skills and Training they Need to Get Ahead; Pew Research Institute: Washington, DC, USA, 2016. [Google Scholar]

- Organisation for Economic Co-operation and Development (OECD). Under Pressure: The Squeezed Middle Class; OECD Publishing: Paris, France, 2019. [Google Scholar]

- Brussevich, M.; Dabla-Norris, E.; Khalid, S. Is Technology Widening the Gender Gap? Automation and the Future of Female Employment; International Monetary Fund: Washington, DC, USA, 2019. [Google Scholar]

- Chang, J.H.; Huynh, P. Asean in Transformation, The Future of Jobs at Risk of Automation; International Labour Organization: Geneva, Switzerland, 2016. [Google Scholar]

- Katz, L.F.; Krueger, A.B. The rise and nature of alternative work arrangements in the united states, 1995–2015. ILR Rev. 2019, 72, 392–416. [Google Scholar] [CrossRef]

- King, J.M.L. Where Do We Go from Here: Chaos Or Community? Beacon Press: Boston, MA, USA, 2010. [Google Scholar]

- Marchant, G.E.; Stevens, Y.A.; Hennessy, J.M. Technology, unemployment & policy options: Navigating the transition to a better world. J. Evolut. Technol. 2014, 24, 26–44. [Google Scholar]

- Marston, G. Greening the australian welfare state: Can basic income play a role. In Basic Income in Australia and New Zealand: Perspectives from the Neoliberal Frontier; Mays, J., Marston, G., Tomilson, J., Eds.; Palgrave Macmillan: London, UK, 2016; pp. 157–177. [Google Scholar]

- Carson, R. Silent Spring; Houghton Mifflin Company: New York, NY, USA, 1962. [Google Scholar]

- Colborn, T.; Dumanoski, D.; Meyers, J.P. Our Stolen Future: Are We Threatening Our Own Fertility, Intelligence, and Survival? A Scientific Detective Story; Dutton Press: New York, NY, USA, 1996. [Google Scholar]

- Solomon, G.M.; Schettler, T. Environmental endocrine disruption. In Life Support: The Environment and Human Health; McCally, M., Ed.; The MIT Press: Cambridge, UK, 1999; pp. 147–162. [Google Scholar]

- Myers, S. Planetary health: Protecting human health on a rapidly changing planet. Lancet 2017, 390, 2860–2868. [Google Scholar] [CrossRef]

- Díaz, S.; Settele, J.; Brondízio, E. Summary for Policymakers of the Global Assessment Report on Biodiversity and Ecosystem Services of the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services. In Report for the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (Ipbes)-7 Plenary, 6 May 2019; The Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES): Bonn, Germany, 2019. [Google Scholar]

- Ayres, R.; Warr, B. The Economic Growth Engine: How Energy and Work Drive Material Prosperity; Edward Elgar Publishing: Williston, VT, USA, 2009. [Google Scholar]

- Ayres, R.U. Application of physical principles to economics. In Resources, Environment and Economics: Applications of the Materials/Energy Balance Principle; Ayres, R.U., Ed.; Wiley: New York, NY, USA, 1978; pp. 37–71. [Google Scholar]

- Georgescu-Roegen, N. The Entropy Law and the Economic Process; Harvard University Press: Cambridge, UK, 1971. [Google Scholar]

- Meadows, D.H.; Meadows, D.L.; Randers, J.; Behrens, W.W. The Limits to Growth; Potomac Associates: New York, NY, USA, 1972. [Google Scholar]

- Ashford, N.A.; Caldart, C.C. Environmental Law, Policy, and Economics: Reclaiming the Environmental Agenda; MIT Press: Cambridge, UK, 2008. [Google Scholar]

- Ashford, N.A.; Miller, C.S. Chemical Exposures: Low Levels and High Stakes; Van Nostrand Reinhold: New York, NY, USA, 1998. [Google Scholar]

- Chivian, E.; McCally, M.; Hu, H.; Haines, A. Critical Condition: Human Health and the Environment; The MIT Press: Cambridge, UK, 1993. [Google Scholar]

- Commoner, B.; Bartlett, P.W.; Eisl, H.; Couchot, K. Long-Range Air Transport of Dioxin from North American Sources to Ecologically Vulnerable Receptors in Nunavut, Arctic Canada; Center for the Biology of Natural Systems (CBNS), Queens College: New York, NY, USA, 2000. [Google Scholar]

- McCally, M. Life Support: The Environment and Human Health; The MIT Press: Cambridge, UK, 1999. [Google Scholar]

- Sunderland, E.; Hu, X.; Dassuncao, C.; Tokranov, A.; Wagner, C.; Allen, J. A review of the pathways of human exposure to poly and perfluoroalkyl substances (pfass) and present understanding of health effects. J. Expo. Sci. Environ. Epidemiol. 2019, 29, 131–147. [Google Scholar] [CrossRef]

- Ash, M.; Boyce, J.K. Racial disparities in pollution exposure and employment at us industrial facilities. Proc. Natl. Acad. Sci. USA 2018, 115, 10636–10641. [Google Scholar] [CrossRef]

- Attina, T.; Malits, J.; Naidu, M.; Trasande, L. Racial/ethnic disparities in disease burden and costs related to exposure to endocrine-disrupting chemicals in the united states: An exploratory analysis. J. Clin. Epidemiol. 2019, 108, 34–43. [Google Scholar] [CrossRef]

- Elliott, J.; Smiley, K. Place, space, and racially unequal exposures to pollution at home and work. Soc. Curr. 2019, 6, 32–50. [Google Scholar] [CrossRef]

- Tessum, C.W.; Apte, J.S.; Goodkind, A.L.; Muller, N.Z.; Mullins, K.A.; Paolella, D.A.; Polasky, S.; Springer, N.P.; Thakrar, S.K.; Marshall, J.D.; et al. Inequity in consumption of goods and services adds to racial-ethnic disparities in air pollution exposure. Proc. Natl. Acad. Sci. USA 2019, 116, 6001–6006. [Google Scholar] [CrossRef]

- Intergovernmental Panel on Climate Change (IPCC). Summary for policymakers. In Climate Change: Impacts, Adaptation, and Vulnerability. Part a: Global and Sectoral Aspects. Contribution of Working Group ii to the fifth Assessment Report of the Intergovernmental Panel on Climate Change; Field, C.B., Barros, V.R., Eds.; Cambridge University Press: Cambridge, UK, 2014; pp. 1–32. [Google Scholar]

- United Nations (UN). Paris Agreement; United Nations: New York, NY, USA, 2015. [Google Scholar]

- Intergovernmental Panel on Climate Change (IPCC). Global Warming of 1.5°C. An. Ipcc Special Report on the Impacts of Global Warming of 1.5°C Above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2018. [Google Scholar]

- World Bank Group. Turn Down the Heat: Confronting the New Climate Normal; World Bank: Washington, DC, USA, 2014. [Google Scholar]

- Wallace-Wells, D. The Uninhabitable Earth: Life after Warming; Tim Duggan Books: New York, NY, USA, 2019. [Google Scholar]

- Autor, D. Skills, education, and the rise of earnings inequality among the “other 99 percent”. Science 2014, 344, 843–851. [Google Scholar] [CrossRef]

- Hoffmann, U. Some Reflections on Climate Change, Green Growth Illusions, and Development Space. No. 205; United Nations Conference on Trade and Development (UNCTAD): New York, NY, USA, 2011. [Google Scholar]

- Hoffmann, U. Can. Green Growth Really Work? Can. Green Growth Really Work and what are the True (Socio)Economics of Climate Change? Heinrich-Böll-Stiftung: Berlin, Germany, 2015; p. 39. [Google Scholar]

- Organisation for Economic Cooperation and Development (OECD). Towards Green Growth; Organisation for Economic Cooperation and Development: Paris, France, 2011. [Google Scholar]

- Parrique, T.; Barth, J.; Briens, F.; Kerschner, C.; Kraus-Polk, A.; Kuokkanen, A.; Spangenberg, J.H. Decoupling Debunked: Evidence and Arguments Against Green Growth as a Sole Strategy for Sustainability; European Environmental Bureau: Brussels, Belgium, 2019. [Google Scholar]

- Barbier, E.B. Summaries: Introduction to the environmental kuznets curve special issue. Environ. Dev. Econ. 1997, 2, 357–367. [Google Scholar] [CrossRef]

- Barbier, E.B. Environmental kuznets curve special issue: Introduction to the environmental kuznets curve special issue. Environ. Dev. Econ. 1997, 2, 369–381. [Google Scholar] [CrossRef]

- Bhattarai, M.; Hammig, M. Governance, economic policy, and the environmental kuznets curve for natural tropical forests. Environ. Dev. Econ. 2004, 9, 367–382. [Google Scholar] [CrossRef]

- Spangenberg, J.H. The environmental kuznets curve: A methodological artifact? Popul. Environ. 2001, 23, 175–191. [Google Scholar] [CrossRef]

- Lawn, P. A theoretical investigation into the likely existence of the environmental kuznets curve. Int. J. Green Econ. 2006, 1, 121–138. [Google Scholar] [CrossRef]

- Harbaugh, W.T.; Levinson, A.; Wilson, D.M. Reexamining the empirical evidence for an environmental kuznets curve. Rev. Econ. Stat. 2002, 84, 541–551. [Google Scholar] [CrossRef]

- Perman, R.; Stern, D.I. Evidence from panel unit root and cointegration tests that the environmental kuznets curve does not exist. Aust. J. Agric. Resour. 2003, 47, 325–347. [Google Scholar] [CrossRef]

- Huang, W.M.; Lee, G.W.M.; Wu, C.C. Ghg emissions, gdp growth and the kyoto protocol: A revisit of environmental kuznets curve hypothesis. Energy Policy 2008, 36, 239–247. [Google Scholar] [CrossRef]

- Dasgupta, S.; Laplante, B.; Wang, H.; Wheeler, D. Confronting the environmental kuznets curve. J. Econ. Perspect. 2002, 16, 147–168. [Google Scholar] [CrossRef]

- Rothman, D.S. Environmental kuznets curves—real progress or passing the buck? A case for consumption-based approaches. Ecol. Econ. 1998, 25, 177–194. [Google Scholar] [CrossRef]

- Holtz-Eakin, D.; Selden, T.M. Stoking the fires? Co2 emissions and economic growth. J. Public Econ. 1995, 57, 85–101. [Google Scholar] [CrossRef]

- Cole, M.A.; Rayner, A.J.; Bates, J.M. The environmental kuznets curve: An empirical analysis. Environ. Dev. Econ. 1997, 2, 401–416. [Google Scholar] [CrossRef]

- Kallis, G.; Kalush, M.; O’Flynn, H.; Rossiter, J.; Ashford, N.A. “Friday off”: Reducing working hours in europe. Sustainability 2016, 4, 1545–1567. [Google Scholar] [CrossRef]

- Ashford, N.A.; Kallis, G. A four-day workweek: A policy for improving employment and environmental conditions in europe. Eur. Financ. Rev. 2013, 53–58. Available online: https://www.europeanfinancialreview.com/a-four-day-workweek-a-policy-for-improving-employment-and-environmental-conditions-in-europe/ (accessed on 18 August 2019).

- Colson, T. The economist behind universal basic income: Give all citizens ubi to help combat a ‘neofascist wave of populism’. Bus. Insid. 2017. Available online: https://www.businessinsider.com/free-money-universal-basic-income-guy-standing-economist-neofascism-populism-brexit-2017-1 (accessed on 18 August 2019).

- Klein, E.; Mays, J.; Dunlop, T. Implementing a Basic Income in Australia, Pathways Forward; Palgrave Macmillan: Cham, Switzerland, 2019; p. 277. [Google Scholar]

- Hanauer, N. Beware, Fellow Plutocrats, the Pitchforks are Coming. TEDSalon NY 2014. Available online: https://www.ted.com/talks/nick_hanauer_beware_fellow_plutocrats_the_pitchforks_are_coming/discussion#t-37798 (accessed on 24 July 2019).

- Hanauer, N. Pitchfork Economics: A Podcasts with Nick Hanauer. Available online: http://www.pitchforkeconomics.com/lp/ (accessed on 24 July 2019).

- Ashford, R.; Shakespeare, R. Binary Economics: The New Paradigm; University Press of America: Lanham, MD, USA, 1999. [Google Scholar]

- Standing, G. Universal Basic Income is Becoming an Urgent Necessity; The Guardian: London, UK, 2017. [Google Scholar]

- Kela. Basic Income Experiment. Available online: https://www.kela.fi/web/en/basic-income-experiment (accessed on 18 June 2019).

- Give Directly. Basic Income. Available online: https://www.givedirectly.org/basic-income (accessed on 18 June 2019).

- Y Research. Our Plan. Available online: https://basicincome.ycr.org/our-plan (accessed on 18 June 2019).

- Stockton Economic Empowerment Demonstration. A Guaranteed Income Demonstration. Available online: https://www.stocktondemonstration.org/ (accessed on 18 June 2019).

- Prokopchuk, M. Ontario’s Basic Income Pilot to End March 2019; CBC News: Toronto, ON, Canada, 2019; Available online: https://www.cbc.ca/news/canada/toronto/ontario-basic-income-pilot-end-march-2019-1.4807254 (accessed on 18 June 2019).

- Basic Income Earth Network (BIEN). Available online: https://basicincome.org/news/2018/12/germany-the-first-basic-income-experiment-in-germany-will-start-in-2019/ (accessed on 18 June 2019).

- Masih, N. Tiny Indian State Proposes World’s Biggest Experiment with Guaranteed Income. Available online: https://www.washingtonpost.com/world/2019/01/17/tiny-indian-state-proposes-worlds-biggest-experiment-with-guaranteed-income/?utm_term=.7571e323fea4 (accessed on 18 June 2019).

- BIG Coalition Namibia. Pilot Project. Available online: http://bignam.org/BIG_pilot.html (accessed on 18 June 2019).

- Springboard to Opportunities. Introducing the Magnolia Mother’s Trust. Available online: http://springboardto.org/index.php/blog/story/introducing-the-magnolia-mothers-trust (accessed on 12 July 2019).

- Urban Innovative Actions. Barcelona. Urban Poverty. B-Mincome-Combining Guaranteed Minimum Income and Active Social Policies in Deprived Urban Areas. Available online: https://uia-initiative.eu/en/uia-cities/barcelona (accessed on 18 June 2019).

- Eight. If We Want to Eradicate Poverty by 2030 We Need Radical and Evidence Based Recipes. Available online: http://eight.world/ (accessed on 18 June 2019).

- Mudle, K.; Drew, S. Labour to Pilot Universal Basic Income Scheme for Everyone-Rich or Poor. Available online: https://www.mirror.co.uk/news/politics/labour-pilot-universal-basic-income-15258572 (accessed on 18 June 2019).

- Standing, G. Basic Income as Common Dividends: Piloting a Transformative Policy a Report for the Shadow Chancellor of the Exchequer; Progressive Economy Forum (PEF): London, UK, 2019; Available online: https://www.progressiveeconomyforum.com/wp-content/uploads/2019/05/PEF_Piloting_Basic_Income_Guy_Standing.pdf (accessed on 18 June 2019).

- Ake, R.K.Q.; Copeland, W.E.; Keeler, G.; Angold, A. Parents’incomes and children’s outcomes: A quasi-experiment using transfer payments from casino profits. Am. Econ. J. Appl. Econ. 2010, 2, 86–115. [Google Scholar] [CrossRef]

- Littledave, S. The Big Money. Available online: https://www.topic.com/the-big-money (accessed on 18 June 2019).

- Friedman, M. Capitalism and Freedom: Fortieth Anniversary Edition; University of Chicago Press: Chicago, IL, USA, 2002. [Google Scholar]

- Cost of Living Refund. A Federal Cost-of-Living Refund. Available online: https://costoflivingrefund.org/federal (accessed on 15 August 2019).

- Syal, R. Employees to be Handed Stake in Firms under Labour plan, Companies with 250 or more Employees will be Expected to Create Ownership Fund, John Mcdonnell to Say. Available online: https://www.theguardian.com/politics/2018/sep/23/labour-private-sector-employee-ownership-plan-john-mcdonnell (accessed on 18 June 2019).

- Lansley, S.; Reed, H. Basic Income for All: From Desirability to Feasibility; Compass: London, UK, 2019. [Google Scholar]

- Stern, A. Raising the Floor: How a Universal Basic Income can Renew our Economy and Rebuild the American Dream; PublicAffairs: New York, NY, USA, 2016. [Google Scholar]

- Hughes, C. Fair Shot: Rethinking Inequality and How We Earn; Bloomsburg Publishing: London, UK, 2018. [Google Scholar]

- Tabatabai, H. The basic income road to reforming iran’s price subsidies. Basic Income Stud. 2011, 6. [Google Scholar] [CrossRef]

- Nikou, S.N.; Glenn, C. The Subsidies Conundrum; United States Institute of Peace: Washington, DC, USA, 2010; Available online: https://iranprimer.usip.org/resource/subsidies-conundrum (accessed on 18 June 2019).

- Alaska Permanent Fund Corporation. Alaska Permanent Fund. Available online: https://apfc.org/ (accessed on 18 June 2019).

- Bruenig, M. Social Wealth Fund for America. Available online: https://www.peoplespolicyproject.org/projects/social-wealth-fund/ (accessed on 18 June 2019).

- Barnes, P. Common Wealth Trusts: Structures of Transition; Tellus Institute: Cambridge, MA, USA, 2015. [Google Scholar]

- Ashford, R. Why working but poor? The need of inclusive capitalism. Akron Law Rev. 2016, 45, 507–537. [Google Scholar]

- Ashford, R. Binary Economics and the Case for Broader Ownership. Available online: https://ssrn.com/abstract=877925 (accessed on 19 June 2019).

- Harvey, P. The right to work and basic income guarantees: Competing or complementary goals? Rutgers J. Law Urban Policy 2005, 2, 8–59. [Google Scholar]

- Harvey, P. Securing the right to work and income security. In Activation Policies for the Unemployed: The Right to Work and the Duty to Work; Dumont, D., Dermine, E., Eds.; P.I.E. Peter Lang: Brussels, Belgium, 2014; pp. 223–254. [Google Scholar]

- Standing, G. Why basic income is needed for a right to work. Rutgers J. Law Urban Policy 2005, 2, 91–102. [Google Scholar]

- Standing, G. Why a basic income is necessary for a right to work. Basic Income Stud. 2013, 7, 19–40. [Google Scholar] [CrossRef]

- Cox, E. Feminist perspectives on basic income. In Implementing a Basic Income in Australia, Exploring the Basic Income Guarantee; Klein, E., Mays, J., Dunlop, T., Eds.; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 69–85. [Google Scholar]

- Lawrence, M. John Mcdonnell’s Worker Ownership Funds Could be the Left’s Right to Buy, Labour’s Plan to Give Employees a Meaningful Stake in the Economy could Build a New Political Constituency for the Party. Available online: https://www.newstatesman.com/politics/economy/2018/09/john-mcdonnells-worker-ownership-funds-could-be-lefts-right-buy (accessed on 18 June 2019).

- Matthews, D. Bernie Sanders’s most Socialist Idea Yet, Explained, He Wants to Mandate Employee Ownership of Big Companies. Available online: https://www.vox.com/2019/5/29/18643032/bernie-sanders-communist-manifesto-employee-ownership-jobs (accessed on 12 July 2019).

- Ashford, R. A new market paradigm for sustainable growth: Financing broader capital ownership with louis kelso’s binary economics. Prax. Fletcher J. Dev. Stud. 1998, 14, 25–59. [Google Scholar]

- Daly, H.E. Elements of environmental macroeconomics. In Ecological Economics: The Science and Management of Sustainability; Costanza, R., Wainger, L., Eds.; Columbia University Press: New York, NY, USA, 1991; pp. 32–46. [Google Scholar]

- Costanza, R.; Daly, H.E. Natural capital and sustainable development. Conserv. Biol. 1992, 6, 37–45. [Google Scholar] [CrossRef]

- McDonough, W.; Braungart, M. The next industrial revolution. Atl. Mon. 1998, 282, 82–92. [Google Scholar]

- Norges Bank. Observation and Exclusion of Companies. Available online: https://www.nbim.no/en/responsibility/exclusion-of-companies/ (accessed on 18 June 2019).

- Stranahan, S.; Kelly, M. Mission-Led Employee-Owned Firms: The Best of the Best; The Democracy Collaborative: Washington, DC, USA, 2019. [Google Scholar]

- Ashford, R. Beyond austerity and stimulus: Democratizing capital acquisition with the earnings of capital as a means to sustainable growth. J. Post Keynes. Econ. 2013, 36, 179–206. [Google Scholar] [CrossRef]

- Ashford, R. Unutilized productive capacity, binary economics and the case for broadening capital ownership. Econ. Manag. Financ. Mark. 2015, 10, 11–53. [Google Scholar]

- Cost of Living Refund. Side by Side Analysis of Cost-of-Living Refund Policies. Available online: https://static1.squarespace.com/static/5acbc4bd0dbda3fb2fce2ab3/t/5d164bfa5fff8200019907b4/1561742331267/side-by-side_fed_legis.pdf (accessed on 15 July 2019).

| Scheme/Program | Principal Financing Mechanism(s) | Work Req.? | Amount Received? | By Whom? | Environmental/Sustainability Aspects? |

|---|---|---|---|---|---|

| A Negative Income Tax (NIT) (inspired by Milton Friedman [87]) | Taxation combined with the removal of welfare assistance programs | Yes | Varies based on income | Citizens/residents who file a tax return | None |

| Cost of Living Refund [88] | Modernization of the Earned Income Tax Credit (EITC) (also known as the Working Families Tax Credit) | Yes | Single people earning less than $50,000 a year would receive $4000 annually; married couples earning less than $90,000 a year would receive $8000 annually | All workers age 18+, including “childless” workers | None |

| Federal Job Guarantee Program (H.R. 1000—Jobs for All Act—submitted to the 116th U.S. Congress) | A National Full Employment Trust Fund (NFETF) | Yes | Compensation from the work program would be comparable to public sector employees undertaking similar work; job-training program participants would be eligible for a cost-of-living stipend | Participants enrolled in a work or training program | Funded projects should be carried out “in a manner that is as ecologically sustainable as is reasonably possible” (Sec. 304(10)) |

| UK Labour—Inclusive Ownership Fund (IOF) [89] | Inclusive Ownership Fund (IOF) | Yes | Up to £500 per month | Workers in a firm with an IOF | None |

| Lansley and Reed’s [90] Partial Basic Income (PBI) Proposal in the UK | The elimination of child benefit payments and state pensions, and reductions in means-tested benefits | No | Varies based on age and marital status; ranges from £2080 to £10,400 annually | Every British citizen | None |

| Lansley and Reed’s [90] Fuller Basic Income (FBI) Proposal in the UK | Same as PBI (above) with the addition of a Citizen’s Wealth Fund | No | Varies based on age and marital status; ranges from £2600 to £13,520 annually | Every British citizen | None |

| Andy Stern’s [91] Universal Basic Income (UBI) Proposal | Elimination of 126 welfare programs; reduction in government tax expenditures/spending; a 5%–10% value added tax (VAT) on goods and services; a financial transaction tax (FTT); a “common wealth” fund; a 1.5 percent wealth (or net worth) tax on personal assets over $1 million | No | $1000 a month | Every U.S. citizen between 18 and 64 | Potentially—if a common wealth fund is created based on the principles underlying Common Wealth Trusts (CWTs) (see below) |

| Andrew Yang’s [11] Universal Basic Income (UBI) Proposal | A 10% value added tax (VAT) on the production of goods or services a business produces; certain welfare programs (unspecified) would be consolidated | No | $1000 a month | Every U.S. citizen over the age of 18 | None |

| Assured Income [9] | A trust fund managed by the Social Security Administration (SSA), with revenue from a range of potential options including a value added tax (VAT), taxes on unearned income, a carbon dioxide tax, and small transaction fees on the trading of securities and derivatives | No | Children (0–17) would receive $100–$200 per month; working age adults (18–64) would receive $200–$400 per month; older individuals (64+) would receive $100–$200 per month | Every U.S. citizen | If designed well, the carbon dioxide tax could incentivize low-carbon investments |

| Chris Hughes’ [92] Guaranteed Income for Working People | A tax on annual incomes of $250,000 or more | Yes | $500 a month | Every working adult in a household with an annual income of less than $50,000 | None |

| Iran’s Cash Transfer Program [93,94] | Removal of price subsidies on fuel and food | No | In 2012, the program was providing monthly payments of 455,000 rials (worth USD $40 in 2012 and around $11 today) | Iranian citizens | None |

| The Alaska Permanent Fund (APF) [95] | The Alaska Permanent Fund (APF) | No | Annual dividend payments typically range between $1000–$2000. | Alaska residents | None |

| American Solidarity Fund (ASF) [96] | The American Solidarity Fund (ASF) | No | Not specified; The Universal Basic Dividend (UBD) payment would depend on the size of the ASF and its five-year performance | U.S. citizens | ASF’s assets could exclude companies if they violate human rights or cause environmental destruction |

| Peter Barnes’ [97] Common Wealth Trusts | Common Wealth Trusts (CWTs) | No | Not specified | Citizens | The CWTs would be legally accountable to future generations and would have the authority to limit the use of threatened ecosystems and charge for the use of public resources |

| Robert Ashford’s [98,99] Inclusive Capitalism (based on binary economics) | Inclusive capitalism based on the principle of “binary growth” | No | Unlike income enhancement via a UBI, no absolute amount of income is prescribed; the amounts paid in dividends to beneficiaries according to this approach depends on the earning capacity of the capital acquired | Citizens, employees, consumers, and/or welfare recipients | Ownership-broadening trusts could invest in common stock voluntarily issued by companies that are advancing inherently sustainable forms of growth |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hall, R.P.; Ashford, R.; Ashford, N.A.; Arango-Quiroga, J. Universal Basic Income and Inclusive Capitalism: Consequences for Sustainability. Sustainability 2019, 11, 4481. https://doi.org/10.3390/su11164481

Hall RP, Ashford R, Ashford NA, Arango-Quiroga J. Universal Basic Income and Inclusive Capitalism: Consequences for Sustainability. Sustainability. 2019; 11(16):4481. https://doi.org/10.3390/su11164481

Chicago/Turabian StyleHall, Ralph P., Robert Ashford, Nicholas A. Ashford, and Johan Arango-Quiroga. 2019. "Universal Basic Income and Inclusive Capitalism: Consequences for Sustainability" Sustainability 11, no. 16: 4481. https://doi.org/10.3390/su11164481

APA StyleHall, R. P., Ashford, R., Ashford, N. A., & Arango-Quiroga, J. (2019). Universal Basic Income and Inclusive Capitalism: Consequences for Sustainability. Sustainability, 11(16), 4481. https://doi.org/10.3390/su11164481