4.1. Alba County: General Context

During the communist ruling, the economy of Alba County developed mainly in the industrial areas, largely depending on the chemical, wood processing, machine building, and food industries, but also mining, including gold mining, and quarrying industries. After the fall of communism, the county’s economy underwent major structural changes, some of its areas being among Romania’s less favored destinations. During the last decade of the 20th Century, the transition process particularly affected most of the county’s towns: Alba Iulia (county residence), Blaj, Câmpeni, Cugir, Ocna Mureș, Zlatna, and their adjacent villages. While some of these towns have managed to redevelop their industry as well, attracting major international private investors (e.g., Bergenbier and afterwards Bosch Automotive in Blaj, Star Assembly, a subsidiary of Daimler, in Sebeș [

42] (pp. 328–335); [

43], or managing to attract and use EU funds (e.g., Alba Iulia, a city that has managed to become a champion of EU funds absorption, both for refurbishing and for development, becoming a tourist hotspot and today working on becoming a genuine smart city [

44,

45]). Two renowned winemakers are also among the top companies of Alba County: Jidvei (in fact, one of Romania’s most important wine producers, both in terms of quantity and quality) and Domeniile Boieru, revealing an attractive activity sector, with high potential of further development. Other major players at County level include, but are not limited to, enterprises such as: Transavia, Roua Florilor, Kronospan, Albalact, Apulum, Cupru Min etc. [

46]. The experts who developed the National Territory Arrangement Plan (NTAP) identified in the case of Alba County a total of 30 administrative territorial units (ATUs) with protected areas [

47,

48,

49]; moreover, the county hosts access points for two highly attractive and valuable natural parks (Apuseni Mountains and Hațeg Dinosaurs Geopark); furthermore, it also features the Transylvanian Canyon (Râpa Roșie). From the perspective of the human built tourist attractions and resources, Alba County enjoys a rich presence of historic monuments and ruins. Tourism has proven to be a successful alternative for many urban and rural areas from Alba County that have faced major economic challenges after 1990. Thus, mountain tourism has developed in areas such as The Apuseni National Park but also in Arieșeni and Șureanu ski resorts; rural tourism is practiced on Arieșului Valley and around Albac, particularly on Aiud Valley, in Rîmetea and Colțești heritage villages, two highly attractive sustainable destinations [

50] (pp. 1–13). Two of the Romanian UNESCO heritage sites are located in Alba County (namely the Saxon fortified church of Câlnic [

51] and the Dacian fortress of Căpâlna, Săsciori commune [

52]). Moreover, other destinations from the same county are included on the UNESCO Tentative List (Alba Iulia [

53], Rîmetea [

54], Roșia Montană Mining Cultural Lanscape [

55]). Various localities in Alba County also possess valuable and attractive castles and fortresses, some of which have already been renovated and included in the tourist circuit, while others still await valorization opportunities; some of its most notorious castles and fortresses are located in towns such as: Alba Iulia (ancient Roman ruins and Vauban medieval military fortress), Aiud (medieval fortress and royal palace), Sâncrai (Bánffy castle—recently renovated and reintroduced in the tourist circuit [

56] (pp. 1443–1451)), Uioara de Sus (Teleki Castle), Blaj (Metropolitan Castle—headquarters of the Greek-Catholic church), Obreja (Wsselényi castle), Sânmiclăuș, Șona commune (Bethlen castle), Cetatea de Baltă (Bethlen-Haller castle—bought, renovated, and operated by the wine producing company Jidvei as a restaurant and winetasting area, including accommodation units and office space, too), Galda de Jos (Kemény castle), Sebeș (medieval fortress), etc. [

57]. (p. 5). The county also hosts significant religious landmarks (the Roman-Catholic and the Orthodox cathedrals in Alba Iulia, the Greek-Catholic cathedral in Blaj, the monastery of Râmeț, etc.). Overall, the most developed forms of tourism in Alba County include: Urban and rural cultural and heritage tourism; religious tourism; rural and nature-based tourism; given the grape growing profile of the county, gastronomic, culinary, and wine tourism have developed significantly; winter sports; business tourism; and transit tourism are practiced as well. Event tourism is also practiced. Held at the beginning of fall in Blaj and Alba Iulia, the Golden Grape Folkloric Festival organized by Jidvei since 2000 is one of the most notorious events dedicated to folkloric music, grapes, and wine [

58]. Festival tourism has also developed in Alba County over the past few years, an example being the Blaj aLive festival, which has been held seven times [

59].

The main purpose of this paper is that of establishing if wine businesses in Alba County are attractive for the Romanian wine tourist and if they can develop sustainably. This section is dedicated to the discussion of the results obtained during the undertaken analyses. Based on the information found online related to the activity of the wine businesses located in Alba County, the supply side can be briefly described as it follows.

4.2. Wineries in Alba County: Facts and Figures

A previous study revealed that from the point of view of the available infrastructure: six (out of 13) of the communes with vineyards present no accommodation, nor food services, while one more, destination does not have any food service providers; furthermore technical and/or tourism related infrastructure problems are faced by over 60% of the county’s ATUs [

47,

48,

49,

60], [

61] (pp. 727–737). The same study led to the conclusion that at the level of Alba County, only one wine cellar (two stars) and three classic restaurants named Taverna are officially ranked (three stars); no units named pivniță, Keller, pince, or cellar are registered [

60], [

61] (pp. 727–737).

Things have not changed much since the previous year. A brief analysis of the officially ranked accommodation facilities and food-serving units reveal the current situation at the level of the localities on the wine route [

2] from Alba County [

62,

63]. Of the 17 ATUs, adding up to 90 localities, on the Wine Road of Alba County, only 12 ATUs (of which five are municipalities and towns and seven communes, totaling 22 villages) have at least one accommodation unit; the remaining 5 ATUs have no officially ranked lodging facility; in fact, a total of 63 localities appear not to have any registered accommodation facility [

2,

62]. Of the 105 officially ranked lodging facilities, a fifth (21) are located in the rural environment; 15 of these units are boarding houses (only five are agritourist pensions, while the other 10 are rural tourist pensions). The rural environment also presents lodging facilities registered as: Tourist chalets (two), hotel, hostel, motel, and rooms-to-rent (one of each). Urban areas concentrate the majority of the lodging units (80%), specifically 84 of them, split by type as it follows: Boarding houses (35), rooms to let (15), hotels (13), villas and tourist villas (six), hostels (six), apartments to rent (four), motels (four), and camping site (one). Enjoying an increasing trend since 2005 [

64] (pp. 71–126), rural areas account in Alba County for 210 rooms and 440 beds, providing an average number of 10 beds per unit and an average of 2.1 beds per room. At the same time, urban destinations offer 3246 beds in 1596 rooms, having an accommodation capacity of nearly 39 beds per unit and 2.03 beds/room. Overall, Alba County has 364 accommodation units, with 3885 rooms and 8133 beds, presenting an average of 10.67 rooms per unit, with 2.09 beds per room. In terms of comfort level, the offer is a budget/economy–mid-scale one. Most of the urban facilities are ranked 3 stars and daisies (50 units), followed by four-star facilities (15), two-star (12 units), one star (5 lodgings), and only 2 facilities ranked at five stars. Rural destinations are also dominated by lodgings ranked at 3 daisies (12 units), followed by 2 and 4 daisies (3 facilities each), 1 daisy (2 units) and only one 5 daisy lodging. Food services are provided by 59 units on the wine route in Alba County [

2,

63], covering 10 localities that belong to eight ATUs (of which five are municipalities and towns). The offer is dominated by restaurants, with 45 units (mainly classic restaurants, one boarding house restaurant, one self-service restaurant, two cellars, eight bars, of which six were associated with restaurants, two buffet-bars, one bistro, and one gas station fast food). Again, the offer is an economy—mid-scale one, with 28 units ranking three stars, 24 facilities of two stars, four-star restaurants, two five-star facilities, and one one-star unit. Although one of the enterprises, Resort Company, runs in Alba Iulia a three star tourist boarding house, a two star classic restaurant, and a two star restaurant registered as a cellar, the website of the property reveals that this unit features, in fact, only a classic restaurant dedicated to hosting private events (weddings and baptisms) and does not provide any wine tasting services, specific to wine cellars [

65]. Similarly, the second registered cellar from Alba Iulia, operated by SC Narcis Cont SRL as four star boarding house, Select, and as three star cellar, is in fact another classic restaurant dedicated to hosting private and business events in two rooms (with capacities of 70 and 300 persons, respectively) [

66]. Some facilities seem to discretely link the services they provide to the wine businesses in Alba County:

The four boarding house La Vie (translated as In the Vineyard) operated by SC Man President SRL (from Izvoarele village, in the area of Blaj); the same enterprise also runs a three star rooms-to-let type of business in Blaj, offering 5 rooms and 10 beds, a two star classic restaurant with 100 seats, and a three star bar with 50 places; although there is no officially ranked restaurant, the owners promote it online; overall, except for its location, within the premises of No 8 Farm from Izvoarele, according to its website, the business does not have anything whatsoever to do with winegrowing, winemaking, and winetasting [

62,

63,

67];

The three daisy boarding house Casa dintre Vii (translated as The House between the Wines) from Jidvei is operated by SC Casa dintre Vii SRL, offers 23 beds in 11 rooms and does not provide any officially registered and ranked foodservices; despites its name, except for the fact that it provides accommodation services in Jidvei village, the unit does not provide any other wine-related services [

62,

63,

68].

Relying on relevant online sources [

2,

31,

36,

37,

38,

39,

40,

41], 27 players in the winemaking sector were identified (see

Table 1 above); of these 15 are registered as enterprises (being operated by limited liability companies) and 12 as self-employed entrepreneurs. They are, in fact, the main providers of wine in Alba County [

31]. The local wine market is dominated by Jidvei, the largest player in the region. The much younger company, Domeniile Boieru, a medium-sized enterprise, is the second most important winemaker of Alba County. Most of the identified enterprises cultivate rather small surfaces (of 2 to 3 ha) and produce around 1000–3000 L of wine per year. Obviously, the exceptions must be noted:

Pivnița Takács Borpince/Takács Cellar (cultivates 17 ha and produces around 30,000 l of wine per year) [

41],

Domeniile Boieru (operates in an area with a tradition of winemaking that dates back to 1220, as mentioned by the Saxons; it exploits around 130 ha of wines and it has reached a wine production of about 50,000 l per year) [

37],

Crama Țelna (is established in Terra Vinorum [

69], a destination with a winegrowing tradition that goes back to the early centuries of the second millennium, being mentioned around 1173 and 1293; the local wine has enjoyed royal popularity, being served at the wedding of Matei Corvin, the Romanian King of Hungary in 1489; the wine cellar, one of the oldest in Romania, functions in a brick cellar built in 1784 and also capitalizes on the architectural heritage of an 18th century mansion, with wine crops spread on 43 ha) [

39], or

Jidvei (a key player at national level, cultivates more than 2,400 ha in an area first mentioned by Herodot (484–425 BC) and has reached a yearly production of more than 8,000,000 l) [

36].

Stațiunea de Cercetare și Dezvoltare pentru Viticultură și Vinificație Blaj/Stațiunea de Cercetare și Producție Vitivinicolă Blaj/Crama Blaj (SCDVV Blaj) is a scientific vinicultural state-owned and operated research center with significant contributions to the development of species and crops; SCDVV exploits today only nearly a quarter of the surfaces it used to crop before 1989 (some 1800 ha), operating on approximately 447 ha of vineyards; the wines produced and sold provide financial support for the station’s research and development activities, particularly as exported products (the main international target markets of wines, vine cuttings, vine graftings, and parent vine graftings of pomiculture products are: Germany, Italy, Austria, and Hungary, respectively); the cellars host collections of wines from the 1940’s; the center focuses on implementing ecological practices and the managers prefer to work with people instead of developing mechanized techniques; thus, the 30–40 regular employees are supported by up to 300 seasonal day-workers; a special attention and research interest is dedicated to the fight by natural means, and less with pesticides, against the Filoxera of the 21st Century [

38,

70].

The region is particularly renowned for its white wines. A great variety of breeds are cultivated in the area. By far, the breeds preferred by the owners are: Fetească Regală, Muscat Ottonel, Pinot Gris, Riesling Italian, and Sauvignon Blanc, closely followed by Traminer and Fetească Albă and Rhein Riesling. The list continues with: Amurg, Cabernet Sauvignon, Fetească Neagră, Gewürztraminer, Hercule, Iordană, Merlot, Neuburger, Syrah, and Traminer Roz. Wines are sold by most cellars either as plain or cuvée products; many of the wineries have developed renowned local brands: Pivnița Takács, Plebanos, Papp Peter, Vin de Ciumbrud—Domeniile Boieru (Vinul Boierului, Domeniile Boieru, Episcopal, Cardinal, Peratic-Orange Wine), Pivnița Savu, Pivnița Sallai, Jidvei (Tradițional, Premiat, Clasic, Grigorescu, Nec Plus Ultra, Tezaur, Castel, Mysterium, Owner Choice Ana, Owner Choice Maria, Vinars, and Spumant—Mărgăritar, Jidvei, and Romantine), Crama Țelna (Vinul Corvinilor and Vinul Baronului al Muzeului National Brukenthal). The area is also popular for gross distribution of wines.

4.2.1. The Economic Performance of the Analyzed Vineyards

The main conclusions of the economic analysis of the investigated wineries are presented by enterprise size. Thus, Jidvei Group and Domeniile Boieru Group are discussed separately, while all other enterprises are regarded comparatively. The first part of this analysis consists of a brief presentation of the main indicators reported publicly by the enterprises: Turnover, net profit, gross profit (where available), liabilities, assets (fixed, current, and total assets), equities, and average number of employees. Depending on the availability of financial data, only profitability indicators can be calculated. All indicators are discussed in terms of the entire analysis period, depending on the available data.

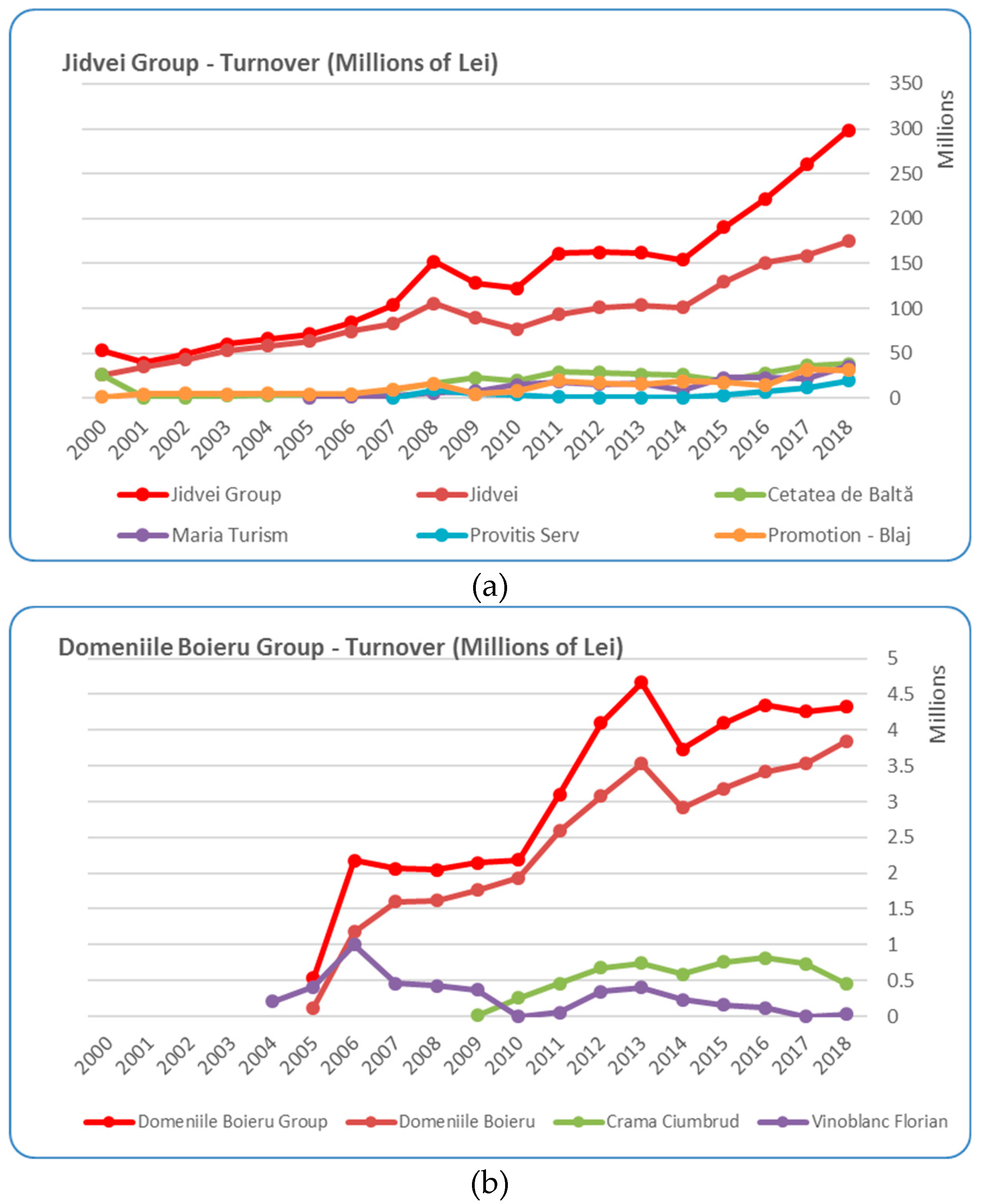

Turnover was the first analyzed indicator (

Figure 1a–c). Overall, except for Crama Plebanos, all other wineries registered an increasing trend of their business volumes. Jidvei is the leading business of the homonymous group, determining the trend of the turnover of the entire business group (

Figure 1a). The growth rate of the group’s turnover, calculated for the entire analysis period was +5.6, while that of Jidvei was +6.7. Maria Turism, the company that manages the Jidvei Castle from Cetatea de Baltă, and Promotion Blaj registered the most significant growth rates of their turnovers (+28.2 for Maria Turism and +30.9 for Promotion Blaj). The second business group, Domeniile Boieru, has also registered a significant growth rate between 2005 and 2018 (+8.2), the group’s trend setter being the homonymous business (

Figure 1b), while both of the other businesses, Crama Ciumbrud and Vinoblanc Florian, registered both ups and downs in terms of sales. While Jidvei seemed to have been somewhat affected by the economic crisis of 2008–2010, Domeniile Boieru enjoyed a continuous growth, even starting a new business in 2009 (Crama Ciumbrud). Among the small players, Crama Plebanos was the most visible business, with significant variations in terms of turnover over the first decade and with a somewhat more stable activity during the most recent period. Two wineries (Crama Riviera and Crama Țelna) seem to have had somewhat larger business volumes, while the other three players kept a lower profile (

Figure 1c).

The analyses continue with a brief discussion of the development of the wineries’ fixed, current, and total assets (

Figure 2a–c). As expected, the larger the enterprise and the larger its cultivated surfaces, the higher were the values of the fixed assets—which in the case of wineries are closely related to the viticulture areas and crops, respective to the processing machines and mechanisms. In the cases of the two business groups (Jidvei and Domeniile Boieru), similar to the development of their turnovers, fixed, current, and total assets registered an ascending trend over the entire investigated timespan. While in the case of Domeniile Boieru (

Figure 2b), fixed assets seemed to be higher than current ones in most years, in the case of Jidvei, the two indicators appeared in a relative balance (

Figure 2a). Overall, in both cases their rising trend was consistent with the continuous extension of the cultivated surfaces. In the case of Jidvei, the growth rates of the fixed assets by 2018 compared to the initial years were significant: +201.8 for the group’s fixed assets, +117.8 for Jidvei, and +250.3 for Maria Turism, while those of the current assets were +20.8 for the group’s current assets, +18.8 for Jidvei, of +40.6 for Maria Turism, and +38.4 for Provitis Serv. Consequently, the growth rate of the group’s total assets is +35.0, while that of Jidvei’s total assets is +27.5 and +92.9 in the case of Maria Turism. Domeniile Boieru registered similar situations. Since 2005 until 2018 the group’s fixed assets registered a growth rate of +337.3; Domeniile Boieru’s fixed assets increased by +117.6, while Vinoblanc Florian’s fixed assets grew by +426.2. The growth rates of Domeniile Boieru group’s current assets were much lower: +19.8 for the group, +23.4 for Domeniile Boieru, +31.5 for Crama Ciumbrud, and only +3.7 for Vinoblanc Florian. Overall, the group’s total assets have increased by +51.1, while Domeniile Boieru had a growth rate of +77.9 and Crama Ciumbrud of +28.7.

In the case of Pivnițele Logos—Crama Plebanos, by correlating the decrease of its turnover with the situation of its assets, one may conclude that the winery’s assets also contain significant stocks of unsold wines and not mainly the planted vines; moreover, their growth rates were +1.6 for total assets, +4.5 for current assets, and of +2.8 for fixed assets. In the cases of the other small players, the illustration of their assets was consistent with the developments of their turnovers (

Figure 1c and

Figure 2c).

A brief analysis of the dynamics of the wineries’ liabilities, entitles one to point out that their growth rates were consistent with the developments of their fixed assets and that they reflected the evolution of their turnovers (

Figure 3a–c). In the case of Jidvei Group, the growth index of its liabilities was +9.8, while Maria Turism increased by +53.3 as opposed to Jidvei which had a growth index of +13.2 (

Figure 3a). More visible growth indices appeared in the case of the second group, Domeniile Boieru, with +40.4 for the group’s overall liabilities, +45.3 for Domeniile Boieru, and +65.7 for Crama Ciumbrud. Obviously, these values were related to the investments made, both in new crops and in new facilities (

Figure 3b). The dynamics registered in the cases of the smaller players were like those of the previous indicators (

Figure 3c).

The evolution of the wineries’ equities was consistent with that of their assets and of their turnovers, assets, and liabilities (

Figure 4a–c). Logically, equities registered similar growth rates as the other indicators. Thus, the overall increase pace of Jidvei Group’s equities was of +6.3, while the equities of Jidvei increased by +10.4 (

Figure 4a). Further, in the case of Domeniile Boieru group, the equities’ growth rate was of +51.3, while that of Domeniile Boieru was of +29.6 (

Figure 4b). The equities of Crama Plebanos followed the same oscillating trend as all previous indices. The developments of the equities of the other small players were consistent with those of their previous indices. The situation observed in the case of Viticola Gârbova can be better understood in the context of its profitability. (

Figure 4c).

Consistent with the investments made in technology and mechanized viticulture, in the cases of the larger players who have started off via a privatization process, the number of employees has dropped significantly (

Figure 5a–c); it is particularly the situation of Jidvei Group, due to the developments of Jidvei company (

Figure 5a). Still, Jidvei was the most important employer in the area; practically each family from Jidvei commune has at least one member who is employed by the winemaking business; moreover, the Necșulescu family was highly appreciated by the locals, as this family also implemented many charity activities in the area [

71]. The second group, Domeniile Boieru, started off from grass roots with a higher number of agricultural workers, directly involved in viticulture, who were eventually replaced by the adoption of mechanization, as the development of assets, liabilities, and equities reveal for 2008–2010 (

Figure 2b,

Figure 3b,

Figure 4b and

Figure 5b), this idea was also supported by the increase in the overall business volume (

Figure 1b). The dramatic decrease of the overall business volume and its oscillations over the entire timespan was directly reflected in the developments of all the indicators of Pivnițele Logos—Crama Plebanos (

Figure 1c,

Figure 2c,

Figure 3c,

Figure 4c and

Figure 5c).

Jidvei Group was the only wine business in Alba County that registered profits over the entire analyzed period (

Figure 6a). Obviously, after the privatization process of 1999, the business group benefited from healthy management decisions, including personnel cut-offs doubled by technology renewal, and by crop renewal and expansions. The winemaker had the advantage of being the first state-owned enterprise to be privatized. The private entrepreneur and manager, Claudiu Necșulescu, carefully selected the company’s distributors and diminished the losses of the formerly state-owned company associated with the poor management of the distribution channels. Strict policies and control methods led to the development of a successful distribution system, where Jidvei cashes back [

72]. Perhaps the business had the chance to capitalize on the winemaker’s previous experience and reputation, thus managing to build a healthy, renowned brand, recognized and appreciated both nationally and internationally. Jidvei capitalized on all EU funding opportunities, managing to absorb considerable amounts of money and to direct them towards their strategic areas (from replantation, renewal, and extension of cultivated wines, to (re)technologization of their wineries, etc.) [

73]. The decision to penetrate international markets (e.g., from North America: The United States of America, Canada, and Mexico, to Europe: Spain, Italy, Germany, Belgium, The Netherlands, Poland, the United Kingdom, and France), was a smart one and proved to be a winning one [

74]. At the same time, the group’s management perfectly understood that Jidvei’s core market is the national one, thus, investments continued to be made in this sense [

72]. In fact, the owners of the business group consider a 10% quota of exports in the business portfolio to be reasonable [

75,

76]. Moreover, Jidvei also targets the Romanians established abroad, especially their communities in Italy and Spain [

74]. The success of Jidvei group is clearly linked to its healthy investment strategy, thus the managers regularly redirect significant chunks of the group’s profits towards technological development; for example the 6 million euros invested in 2018 generated over 21 million liters of wine, as more than 1000 workers and 13 machines were involved in the harvesting of the crops (300 million kg of grapes) spread on 2500 hectares [

77,

78]; the vineyards of Jidvei are the largest ones in Europe to be owned by a single entrepreneur, in this case the Necșulescu Family [

71]. The company’s plans do not include any further extension of the wine crops, as the management team considers the 2500 ha as optimal [

79]. Aiming at being even more environmentally friendly, the management of Jidvei invested 1.5 million euros in modern water-conditioning equipment for the vines’ direct treatment. Furthermore, for 2019 the company plans to invest significantly in communication, aiming at educating particularly native consumers towards the consumption of local wines and for a better acknowledgement of winemaking traditions and culture. In this respect, the company encourages people (both small cellar owners and private individuals) to produce craft wine by selling freshly squeezed grape juice and by providing advice in order to help people produce quality table wines. Furthermore, a competition for homemade wine is hosted each spring at the Bethlen-Haller castle from Cetatea de Baltă [

77,

80]. Current plans include international expansion and the development of new brands targeting younger consumers, as well as the revitalization of forgotten breeds, such as the Neuburger. After the modernization of Jidvei winery, the cellar from Bălcaciu is scheduled for renewal [

77]. Jidvei has managed to develop an offer that targets and addresses various customer segments; thus, the winemaker has a rich portfolio, from HoReCa wines (bag-in-box), to budget, mid-scale, premium and super-premium/exquisite, and collection wines, to sparkling wines and brandy [

81]. Furthermore, Jidvei has proven to be capable of staying in trend with the developments of the market—the winemaker has adapted and implemented new and modern solutions, such as the launching of an online store dedicated to its premium and super-premium brands (Owner’s Choice and Mysterium) [

82]. Claudiu Necșulescu, the representative of the owner family, explains how Jidvei has grown slowly but steadily, taking calculated risks, relying on the company’s winemaker, Ioan Buia, to nowadays become an empire [

83]. Strategic thinking has led to the development of the winemaker’s own vine nursery, the so-called “Școală de Viță” (translated “Wine-School”), where Jidvei produces yearly over 500,000 cuttings and seedlings of exclusively noble breeds (native: Fetească Regală and Fetească Albă, and international: Sauvignon Blanc, Pinot Grigio, Riesling, Syrah, etc.) [

81]; the nursery is, in fact, the first such private project in Romania [

36]. More than 80 million euro have been invested in Jidvei ever since the company’s privatization; hard work and strategic thinking have contributed to the transformation of the business into a super-brand, with more than 200 top-international awards as recognition for its quality wines. Highly adaptive and open towards innovation, Jidvei is the first Romanian producer with a gravitational winery, the largest in Europe. Also, the company uses the first GPS controlled seeding machine and it has also implemented the first fully computer-controlled winemaking technological line [

84]. An ambitious, though achievable, plan of the group’s management is that of transforming Jidvei into the first wine producer with zero energy consumption; this is, in fact, a very valuable sustainability target for the winemaker [

79].

The relatively young player on the wine market of Alba County, the Group Domeniile Boieru presents itself differently compared to Jidvei in terms of net profits (

Figure 6b). Obviously, with a business history of less than 15 years, the second analyzed business group registered oscillating results, with low profits and losses as well. These results are not surprising at all, as due to its investments, all other indicators are on a rising trend; equities, fixed, current and total assets, liabilities, and even employees registered growths similar to that of the turnover. One could assume that profits were carefully reinvested, providing the needed support for further development. This assumption was confirmed by the fact that the year 2017 brought the first associate, a friend of Dănoaie family, namely Mr Raul Ciurtin, the former owner of Albalact, who after the sale of his first business, decided to invest in his friend’s wine business. He bought 50% of the shares and he also announced his intention to credit the enterprise [

85]. The group Domeniile Boieru initiated significant changes in 2018, rebranding as Vin de Ciumbrud and focusing on extending is cultivated areas, with 220 ha of planted wines, of which 180 ha are already productive, with a processing capacity of 30,000 hl, the winemaker seems ready to move forward, putting a lot of effort in its steady growth [

86].

Regarding the small players, one could note that except for Pivnițele Logos—Crama Plebanos, all others seemed to have an even development, and a relatively constant one. As already mentioned, Crama Plebanos did not seem prepared enough to face the challenges of the business environment (

Figure 6c).

Due to the fact that the authors had limited access to the financial statements of the investigated enterprises, only three indicators were calculated for a six-year timespan: Financial profitability (%), sales’ economic profitability (%), and assets’ economic profitability (%), the three of them offering us an overview on the financial situation, but not the complete information. The values obtained are going to be briefly discussed.

The first indicator (

Table 2), financial profitability (%), generally measures a company’s efficiency. In the case of the selected wineries, it revealed a dynamic environment, typical for this industry, with each company having its own periods of growth and decline, some of them abruptly changing from one year to another, and others having a smoother transition. As one may notice, Jidvei Group presented the most visible stability when it comes to financial profitability, perhaps a reflection of its clear strategic thinking and planning, and an advantage of the company’s large size in an environment dominated by this business group.

The second indicator (

Table 3), sales’ economic profitability (%), revealed a less dramatic evolution of the companies’ financial situations compared to the previous situation, and still placed Jidvei Group in first place for its stability and efficiency. Logically following the trends revealed by the general financial profitability, the sales’ economic profitability shows that the customer-marketing relationship is not the one to blame for the unprofitable periods, but instead it may be the (poor) management strategies, or perhaps the lack thereof, and the (sometimes overenthusiastic) spending.

The values calculated under the third indicator (

Table 4), assets’ economic profitability (%), showed a modest efficiency. It should be no surprise by now that Jidvei Group was, once again, the leader when it came to the assets’ profitability, of course, due to its planning and implementing of carefully elaborated long-term strategies.

4.2.2. The Online Presence of the Analyzed Vineyards

Overall, the main conclusion regarding the wineries’ online is presence was that the small players were rather absent. Basically, the smaller the business size, the more discreet was their online presence. Thus, eight websites were identified for the investigated enterprises but three of them were not functional, while those that work belonged to: Jidvei (the biggest player), Domeniile Boieru (the largest member of the Alba Wine Association, a medium-sized SME), and Stațiunea de Cercetare și Dezvoltare pentru Viticultură și Vinificație Blaj/Stațiunea de Cercetare și Producție Vitivinicolă Blaj/Crama Blaj (the state-owned and operated research center from Blaj); while only two reflect the online presence of small players: Pivnița Takács Borpince and Crama Țelna. Some of the entrepreneurs opted for social media profiles, with Facebook being the preferred option. Still, while the same enterprises as above seemed to have more developed social media profiles and proved to be more skilled in terms of online communication (Jidvei, Domeniile Boieru, Stațiunea de Cercetare și Dezvoltare pentru Viticultură și Vinificație Blaj/Stațiunea de Cercetare și Producție Vitivinicolă Blaj/Crama Blaj, Pivnița Takács Borpince, and Crama Țelna), smaller players seemed less capable to capitalize on free online communication tools. Some cellars relied exclusively on Facebook as a new-media marketing communication tool: Crama Riviera–Dorel Popa and Crama Maier/Moșia Maier. Tamás András, the self-employed entrepreneur of Crama Tamás Pince, who is a winemaker and also a journalist put a lot of effort into properly promoting his family’s wine business, initially established in 1933; this cellar is promoted online via Facebook and LinkedIn business profiles, and via Foursquare. Youtube and Instagram were also used by Jidvei and Pivnița Takács Borpince; the owner–manager of the latter also had a blog.

The analyses of the vineyards’ online presence revealed interesting findings related to their activity. In this respect, one of the most significant results was that many of the small local producers had taken a step forward, moving from the gross sale of unbottled house wines at the door of the cellar or at the gate of the vineyard, to the development of their own labeled bottled wines [

87]. All local and regional associations supported and encouraged small producers in this direction. Yearly local, regional, and national wine tastings and wine competitions award and promote small producers. For example, the most important association of Alba County—Țara Vinului Alba, established in 2007, has reached the 7th edition of the Alba Wines’ Gala, dedicated to the small craft-wine producers [

2,

88]. The members of the association are granted access to scientific trainings and to specialized literature; moreover, they are helped to take part in international visiting trips and tours dedicated to know-how exchanges. Furthermore, a specialized research center has been opened for them in Aiud [

88]. Consumers, particularly wine tourism practitioners, seem to have become more educated and trust more those wines that are bottled and labeled by the local producers who have joined the association, and who also use the association’s logo on their labels [

88]. According to the information available, all vineyard-owners, and their winemakers are Romanian, in some cases of Hungarian ethnicity.

When it comes to the information presented online, in most cases, the content was limited. It was surprising to discover that despite the fact that the identified businesses are listed as wineries and cellars online, more than half of them do not provide any information concerning their cellar/cellars’ activity. Moreover, only five players (Cramele Jidvei—Cetatea de Baltă-Jidvei, Blaj, Bălcaciu, and Tăuni, Pivnița Takács Borpince, Crama Vin de Ciumbrud—Domeniile Boieru, Pivnițele Logos—Crama Plebanos—via the Association’s website, and SCDVV Blaj) provided details related to the winetasting packages/services they offer: Types of tasted wines, tariffs, included foodservices, etc. Furthermore, only three cellars also provide accommodation services (Jidvei, Domeniile Boieru and Crama Plebanos). In terms of quality of expression, all of the functioning websites, as well as the active Facebook and LinkedIn profiles use did not seem to have any problems. Two of the smaller players did not communicate in Romanian but only in Hungarian (pivnița Takács Borpince and Crama Tamás Pince). None of the wineries provided information in English, German, Italian, French, or any other foreign language. An interesting marketing approach could be noticed in the case of three wineries from Aiud: Crama Takács Borpince, Crama Papp Peter, and Crama Tamás Pince which were present in the most recent editions of a renowned travel guide, Rough Guides [

89,

90].

Two of the wineries were part of other businesses. The owners of Pivnița Takács Borpince also have a lavender crop and produce derivate products. PFA Popa Ioan Marius also produced sheep and goat’s milk and cheese, pork meat, and also sheep wool, sheep, lamb, goat, and beef; the winemaker also produce wine from the Gârbova de Sebeș vineyard. None of the investigated wineries seem to valorize any of the raw materials after the production of their wines, sparkling wines, or brandies.

An example of good practices came from the winemakers located in Ighiu, a commune of Terra Vinorum; the five villages of this commune, Bucerdea Vinoasă, Ighiel, Ighiu, Șard, and Țelna, were included in the wine route and provided an excellent example of successful association processes among local producers; thus, winemakers have managed to associate with produce and sell bottled wines. Moreover, in Bucerdea Vinoasă the local community managed to open a small but highly valuable and well documented ethnographic museum, established with the donations received from the local population. At the same time, the community opened a folk school where local traditions and crafts, namely weaving and knitting, are rediscovered by both children and tourists. Even the local school gets involved in similar activities, supporting and teaching religious glass painting techniques. Furthermore, Casa Apoulon was opened in Bucerdea Vinoasă as a center dedicated to wine and vine exhibits; the center functions in a renovated cellar, which was transformed into exhibition space and which also plays the role of wine-library. The old bottles and bilingual bottle tags prove the region’s multicultural features [

69].

4.3. Wineries in Alba County: The Perspective of the Entrepreneurs, of the Public Administration, and of the Local Population

In order to sketch a more complex picture of the wine businesses in Alba County, the next undertaken step was that of interviewing certain persons considered to be relevant for the current research study, as described in the methodological section. Some of the most relevant findings are going to be presented in the following paragraphs.

A first issue of concern was related to how the interviewed persons perceive the areas where they carry out their specific activities. Thus, the representative of Domeniile Boieru (DB) pointed out the importance of the land and terroir rather than that of the place itself; in their opinion the cellar can be moved to any destination, but it is essential to have good places for the wines and vineyards. A similar perspective was expressed by the representative of Jidvei (JV), too. In the view of ST (the representative of Stațiunea de Cercetare și Dezvoltare pentru Viticultură și Vinificație Blaj) the municipality of Blaj and its surrounding areas have a zero-unemployment rate due to the massive investments of Bosch, thus, workers are sought further away, in remote villages. Both local entrepreneurs (ND and VF) perceived the area to be on a developing trend from the perspective of their wine businesses. The representatives of the two larger players, JV and DB, both pointed out that the local public administrations have not done much to motivate them; in both cases the terroir is the triggering factor associated to the location of the business.

The interviews proceeded with the identification of the major weaknesses of the destinations from an administrative point of view. Given the reduced dimensions of Jidvei commune and of its villages, JV emphasized the challenge to find workers during the wine-picking season, when the company has to address people from remote localities. For DB, the main drawback was the fact that the enterprise was established in an urban area, Ciumbrud being subordinated to the municipality of Aiud and, consequently, being treated as an urban locality when it comes to European or other financing opportunities; in fact, although the nature of the activity is a rural one, the winemaker is not eligible for funding opportunities designated for rural areas. ST considered that SCDVV is less affected by the local administration and that its problems are related to the state ownership of the research center and the associated funding issues and challenges. Both local entrepreneurs (ND and FV) emphasized the lack of labor-force. In fact, the poor availability of the workers was the most important challenge for most winemakers, a fact pointed out in an interview by Claudiu Necșulescu, too: “To present the low unemployment rare as a virtue is highly dangerous for the business environment. It is perhaps the best moment to undertake the restructuring of the administrative apparatus. Given this deficit of labor-force, the restructured employees will be immediately integrated and absorbed by the private business environment. Both the Government and the entrepreneurial and employers’ associations must struggle to increase wages in order attract back Romanians who work abroad. [

79]”.

The research continued with the identification of the future perspectives of wine businesses. JV considered the business environment to be extremely dynamic and emphasized the importance of adaptiveness and quick adoption of new technologies. Thus, the Research and Development department of Jidvei works on creating a line of bio product; for example, due to the implementation of new concentration methods of the crop, the winemaker has eliminated added sugar and unnatural compounds. JV states: “On the long-run, development is useful for productivity as it diminishes the costs”. DB had a special point of view considering that the company’s success depends directly on its attractiveness among potential consumers. ST saw Blaj on a development trend from the perspective of its industry, “the city flourishes”. ND saw only limited development opportunities, while VF considered that in the area of Aiud, agriculture, viticulture, and pomiculture are attractive and promising business areas.

Further, the researchers aimed at identifying any social responsibility actions and to assess the involvement of entrepreneurs in this area. JV showed that Jidvei is a key employer in the area, the local population having access to workplaces; almost each family has at least one family member who is employed by the winemaker. Moreover, Jidvei supports the local community, as the company is actively involved in the community life, it finances schools, churches, it has contributed to the building of public kindergartens and schools, where the enterprise provides financial support for all other activities, except for teaching; the company supports renovations and refurbishments of public facilities. Together with the authorities, Jidvei contributes to the development of the infrastructure (e.g., the road from Jidvei to Valea Lungă) and of telecommunication services. The representative of Domeniile Boieru brought up the problem of the labor-force, as even the wine workers need certain skills (for planting, cutting, fixing, picking wines etc.). DB explained that in Aiud there used to exist an agriculture vocational school with classes for viticulture, but these ceased to function 20 years ago. The company has initiated a memorandum for the reestablishing of viticulture education, offering to host educational and practical activities, but the central authorities seem not to be capable of understanding their need. The enterprise faces the same challenge as Jidvei, working with locals but also having to seek employees all over the county. ST explained that the research center contributes less to the local community due to its financial weaknesses; it is, in fact, Jidvei who are involved directly in the life of the locals. Both small local entrepreneurs saw the local community only as a source of labor-force they can employ and use. Neither of the two mentioned anything in terms of social involvement but emphasized the opportunities generated by winegrowing and winemaking.

Another topic of interest was to establish what sort of products and derivates are offered by the winemakers. JV explained that Jidvei only produces and sells wine; relatively recently (in 2015), the company also began to sell freshly squeezed grape juice for small craft winemakers and for table winemakers (household users), which turned into a new, separate business of Jidvei without affecting the sales of their bottled wines. JV further explained that Jidvei sells both on the native and on foreign markets, working with specialized distributors, with specialized liquor-stores, with retailers, and with key super- and hypermarkets, and the company participates at fairs and competitions. For the international markets, Jidvei has a department dedicated to market testing and participation at fairs, exhibitions, and competitions. Similarly, DB revealed that Domeniile Boieru also focus on grape-processing for winemaking and being present both on the Romanian and international markets. ST explained that in order to raise money (for their employees’ wages!), the research center must sell wines and also various viticulture products, such as cuttings and seedlings from their viniculture farm; the center also operates a pomiculture farm where they develop and sell various fruit trees. They only carry out local trading activities. Both local entrepreneurs explained that they only sell grapes and make wine. Thus, in the case of ND part of the grapes are sold to other producers, while the produced wine is sold mainly locally (60–70%) and in other localities (~30%). Similarly, VF explained that the grapes are sold by breed and the remainder are used for winemaking; the wine is sold locally and in some neighboring counties. One may notice that none of the producers valorize any of the remainders of their grapes. It is peculiar to notice that the big players have not sensed the opportunities provided by the valorization of the left-over raw materials; for example, seeds can be further processed and transformed into grape oil, flour, and bread. Moreover, in other countries (e.g., France) the vinegar and mustard industries are commonly associated with that of wines.

The interviews continued with the topic of internationalization. Of course, JV pointed out that Jidvei has internationalized successfully due to the quality and development of its wines. Likewise, Domeniile Boieru has also penetrated some international markets, having distribution contracts in the Czech Republic and in Hungary. DB pointed out that if small players chose to exist in the grey economy and test their wines’ quality periodically, they could also capitalize on the potential of the international markets. Given the lack of financial support, ST explained that the research center lost its international contracts; before 1989, SCDVV Blaj used to export in Germany, France, Japan, and in the USA, while nowadays the center is present only on the local market (more at county level than regionally and nationally). ND considered that given the (very) small size of the business, the effort of internationalizing is nonsense. On the other hand, VF believed that having access to the international markets would be beneficial even for small players and that it would eventually lead to the further development of the market.

Communication and promotion are key factors of success in the case of almost all businesses. Thus, the interview continued in this direction, discussing the importance of the online presence of winemakers. JV considered that being present online is compulsory today, thus, Jidvei sells premium and super-premium wines online via a dedicated online shop. Still, most of the winemakers’ products are sold physically, as not all breeds are listed. DB illustrated the situation at Domeniile Boieru: “It is compulsory to be present online. We sell online via our own online shop. The oeno-tourism component of our business, the wine, the tourist destination and the winemaking activity are promoted online”. ST explained that the research center is present online without online sales; SCDVV Blaj only uses the website for marketing activities. Neither of the two entrepreneurs has invested in a website for their business. ND considered a website and an associated online shop would be good but for the moment, the website of the association ensures the winemaker’s online presence, while sales are made only at the wine cellar. Similarly, VF stated: “I’m not online but I sell based on personal advertising and word-of-mouth. For the time-being this method works well enough”.

When asked about the potential of the Road of Wine in Alba County and its ancillary services, the interviewed persons provided interesting responses. JV explained that the development of the Road of Wine would be beneficial for the winemaker and for the area. Further JV described the offer of Jidvei in this respect: “we have a restaurant and accommodation spaces (but only for protocol/internal use). In order to attend wine tastings at Jidvei, reservations need to be made in advance. The cellar provides wine tasting services with snack but also with meals. Currently [at the time of the interview], joint efforts are made with the local public administration of Alba Iulia, aiming at retaining and keeping tourists busy, for longer stays”. DB pointed out that: “The Route of Wine only shows the cellars, not mentioning tourist landmarks. It would be useful to develop the Wine Road because oeno-tourism is on a great rising trend and people are curious to find out what wine-tourism is about. Thus, it would be useful to develop ancillary services. By opening more locations in the county, the Road of Wine would eventually develop, providing clients with both wine tasting locations and accommodation services. I don’t see any near future developments in this respect. We have some development ideas that we only implement within our own business.” ST agreed that developing the Road of Wine would be a good idea and that it would be possible but also explains again the drawbacks of being state-owned and operated: “We had [this] in plan, we have rooms, but being a public institution it is less viable to implement this”. ND showed that the development of the Road of Wine would be necessary for wine businesses and that the infrastructure needs to be developed but as a business-owner, ND does not have development plans related to investments in ancillary services. VF also considered that the development of the Road of Wine would be a positive aspect. Moreover, VF explained: “For the moment, I don’t have any expansion plans, but in the future, I wish to extend my business with accommodation and foodservices”.

The final discussion topic of the interviews was dedicated to the estimated impact of the development of the Road of Wine in Alba County upon the interviewees’ businesses. JV considered that small producers have a limited capacity, thus, the organization of regular guided wine tasting tours would leave them without wine. Another challenge of small players is related to their capacity of ensuring proper winemaking and wine-keeping conditions. Furthermore, small cellars also have limited possibilities of providing accommodation and foodservices. In the view of DB, the positive impact of the development of the wine road upon a business does not really depend on a single factor; “Perhaps, being integrated in a project that also involves potential investors who would be interested to develop attractions and sites, further promoted by the local authorities and by the Wine Road Association and linked to the wineries. Otherwise, in theory, the Road of Wine exists but there is nothing to promote along it”. ST simply agreed once again with the opportunity of such a development. ND was a bit skeptical: “For sure, it would be very important. I am curious to find out when this is going to eventually happen.” VF concluded in a positive tone: “Yes, it would be beneficial to develop the Road of Wine. All wine-cellars and other businesses would have something to gain”.

The perspective of the representatives of the public administration and that of the local population were reflected by the interviews taken in Aiud and in Blaj with a total of five subjects. The two municipalities were selected because they are gravitational centers for the wineries in Alba County, concentrating the most significant players. The following acronyms are used for the five interviewees: MR—the Mayor‘s representative from Aiud; IT—an employee of an IT department; CA—a representative of the local chamber of agriculture; CT—an employee of an accounting office, and a local inhabitant—GP.

Both respondents from Aiud (MR and IT) considered that the municipality is on a positive development trend but that at the same time important industry is lack nowadays. Likewise, the three respondents from Blaj (CA, CT and GP) all agreed that Blaj is one of the most developed small towns of Romania, enjoying a good economic but also social evolution generated by the industrial players. Similarly, Alba Iulia and Sebeș also enjoy a fast growth due to the presence of important industrial investors, respectively of tourism development in the county’s residency city, too. Further, the respondents explained the key economic areas of the towns. Thus, MR pointed out that agriculture and services are the two development areas of this small town. IT completed the idea, further explaining that agriculture develops due to the viticulture and pomiculture farms that also produce vines and wines, seedlings and cuttings, and planting material—fruit trees and roses; some corn and granary crops are also exploited in the area. The three respondents considered that Blaj develops primarily in the industrial area. According to MR and IT, Aiud faces two problems related to the population; firstly, due to the lack of industry, the town cannot provide enough workplaces, thus, except for those employed by the public administration, by the prison, or as educators and craftsmen, many other locals end up commuting to nearby towns. In the view of all respondents (CA, CT, and GB)), Blaj enjoys a very high employment rate, which on the other hand raises the problem of skilled labor force availability. Both towns face the issue of an ageing population and of the migration of youngsters towards larger cities. Related to the economic development and to employees’ availability, the same challenges were also mentioned by the players in the winemaking sector.

Regarding the contribution of the wine sector to the development of the towns, opinions were somewhat different. Thus, while for Aiud, viticulture and viniculture are key activity sectors (MR), contributing to the town’s development (IT), in the case of Blaj some consider the sector marginal but on an ascending trend due to the small entrepreneurs (CA and GP), while CT considered that SCDVV Blaj is a major player. Overall, the three respondents from Blaj (CA, CT, and GP) tended to agree that the further development of the wine road will contribute to the development of their community. There already are 20 small winemakers who have a loyal clientele and who can positively contribute to the increase of this activity sector in Blaj. In both towns, there are important winemakers, some with a national or even international reputation, while others only of local or regional interest, and some who produce only for their households. Further, the respondents confirmed the information already provided by the entrepreneurs regarding the fact that no derivate products are made of the grape-leftovers. Basically, to their knowledge vineyards either make wine or sell the grapes. IT explained that every somewhat important public event or festival organized in Aiud also involves a wine tasting and vineyard and cellar visiting activities. By size, the producers from Aiud are medium and small (MR), while in Blaj, SCDVV is considered a large player; small ones are also involved (CA, CT and GP). Given the importance of the involvement of the public administration in the development of tourism and wine tourism in any destination, this was the next discussed topic. Aiud is on an ascending trend, as the municipality encourages this type of tourism (MR), the opening of new cellars is also encouraged (IT). At the same time, lodging facilities are necessary, with the town not having the possibility of accommodating all of its guests who seek such services in the nearby areas. Interviewees agree that tourism and wine tourism could contribute to the development of Blaj, too. Furthermore, CA, mentioning Casa dintre Vii, believed that opening new accommodation units in vineyards or other places can be beneficial for Blaj. Unlike Aiud, Blaj has many accommodation facilities, which provide diverse services, thus, opening new lodgings would not be compulsory, as GB and CT considered, but the municipality of Blaj salutes the opening of new cellars. All respondents agreed that the Road of Wine has contributed positively to the development of the two towns. A more visible connection between the two types of businesses appears in Aiud, where winemakers have also opened accommodation facilities in the vineyards, but basically only existing businesses have developed, no new entries have been registered (IT). In Blaj, the administration senses a certain causality effect between wine tourism and tourism development but not exclusively. The development of wine tourism, and of tourism in general, is encouraged by the town hall of Aiud, as many landmarks (e.g., the Citadel and the monument dedicated to the victims of political imprisonment) underwent renovations and the road infrastructure has been modernized, providing access to the natural Gorges of Aiud. The town does not yet have a tourist information center, but initial steps have been taken in this respect. While accommodation services and food services seem to be good, still developing but insufficient (MR and IT), leisure services are missing (IT). The recently rehabilitated Bánffy Castle from Sâncraiu and a mansion are popular facilities among locals and visitors from Transylvania (IT). The respondents form Blaj agreed that the municipality plans to further develop tourism, but they are not aware if wine tourism is considered a priority sector. Blaj has a functional tourist information center but accommodation services should improve, food services can also continue their development, while the municipality works on the development of leisure facilities (sports’ hall, swimming pool, sport-grounds, etc.) (CA, CT and GP).

The picture of the supply side is completed with the opinions expressed by three residents: Two from Blaj (MI—local woman and MM—master student, employed at SCDVV Blaj) and one from Ighiu commune (ST—student). When asked about how they perceive their hometown, both MI and MM described Blaj as a small, calm town; MI further said that Blaj is: “developed, a community of hardworking people; it has a good financial situation since Bosch has begun investments; with many young people who have arrived to work for the local industry”. ST described the village of Țelna, in Ighiu commune as “a settlement from Alba County, renown for viticulture, because this area gave birth to the best wine, preferred even by Matei Corvin, who ordered it for his wedding”. When it came to negative aspects, Blaj lacks parking lots and has become a crowded town; moreover, existing private residences are not enough, due to the increasing number of people who establish in the town, working for the local industry (MI); there is a lack of tourism promotion (MM). Țelna faces other challenges: “the lack of financial resources and a poor public management” (ST). Both locals from Blaj (MI and MM) emphasized their intent to remain in Blaj. MI explained why the wine businesses of SCDVV Blaj have decreased: Due to the lawsuits related to the viticulture and agricultural pieces of land those who currently possess the land cannot work the vines because they do not own them, while the entitled owners have not yet received their properties back (after the nationalization process of 1948–1963. In the long run, wines are going to be exploited at their potential and wine tourism will recover; currently SCDVV Blaj only organizes wine tastings for Romanian and international visitors without meals (because of increased associated costs); three, five, or seven wines are served (MI). MM considered there are enough opportunities in Blaj. Ighiu enjoys both the advantages of viticulture and those of small industry (FS). All respondents described the above-mentioned vinicultural activities, mentioning that currently none of the winemakers use the grape leftovers to produce derivate products. MI mentions that a few years ago, in Blaj, used to function a producer of grapeseed oil who moved away. Nowadays, local winemakers focus on making wine or on selling the grapes and only use grape leftovers as natural fertilizers (MI). Wine businesses are considered to have positive contributions upon the localities’ wellbeing; moreover, the respondents considered the further development of a wine road to be an opportunity for their places, where tourism is supported by local authorities in both cases (MI, MM and FS).

4.4. Wineries in Alba County: A Profile of the Consumer

Wine tourism is still relatively young in Romania. Although the Wine Route Program was initiated by the Romanian Government in 2001, this market has become more visible only during the more recent years. Consequently, its consumer is not yet very well understood. Aiming at getting a clearer image of the consumer side, the researchers carried out survey-based research in 2018 among the existing and potential wine tourism consumers. Some of the main findings regarding the expectations and requirements of this type of tourist were discussed in a previous research study [

61] and will be briefly reiterated here along with the conclusions of a study implemented last year and repeated this year by ReVino.ro [

91]. The ReVino.ro study emphasized that education, wine tourism, and the more recent developments have led to an improvement (perhaps a bit of sophistication, too) in the consumption of wine among Romanians [

91]. According to the studies of the National Authority for Tourism/Ministry of Tourism, wine tourism is among the top 10 preferred activities of both Romanian and foreign visitors (enjoying a higher interest among German, Italian, British, and American tourists) [

61,

92]. The respondents indicated their preferences in terms of destination choice for holidays (more than one answer was allowed): mountain (66%), seaside (58%), city-breaks (50%), cultural (both urban and rural) (32%), and rural (29%). Obviously, given Romania’s geography, most of them are compatible with wine tourism.

Some of the main findings of the research in 2018 enable the characterization of the 489 Romanian respondents. A very high percent of the respondents (close to 97%) consumed occasionally or regularly one or more types of alcoholic drinks; 16 respondents (3%) were eliminated from the study as non-consumers of any type of alcoholic drink. Most of the sample members turned out to be wine consumers (~88%), most of them (75%) being occasional/special occasion consumers, and relatively few, regular consumers: Weekly consumers (~23%) and daily consumers (~2%). Beer is the second preferred alcoholic drink (~55%), followed by cocktails (~36%), spirits (~31%), and short & long drinks (26%). The respondents were asked to mention their preferred wines. Only 60% of the respondents mentioned at least one Romanian or one foreign brand. The following Romanian brands appear to be among the top spontaneous preferences: Jidvei, Recaș, Ceptura, Domeniile Sâmburești, Murfatlar, Dealu Mare, Domeniile Boieru, Tohani, Beciul Domnesc, Miniș, Lacrima lui Ovidiu, Sânge de Taur, Petro Vaselo, Zarea, Casa Isărescu, Panciu, Liliac, and Zestrea. Few respondents tend to prefer international brands: Purcari, Cricova, Vila de Corlo, Porto, Tokaj, Lafage, Australian, French, Italian, and Spanish wines. Most of the respondents were rare and occasional consumers of local wines (47%), followed by frequent consumers (29%). Percentages changed for Romanian wines; thus, 26% are rare and occasional consumers, relatively frequent, and very frequent consumers (47%). International wines are seldomly preferred (71%), obviously these ones being less known and accessible. Respondents were further asked to be more specific regarding their preferences of Romanian wines and to mention three of their favorite vineyards. Transylvanian wines enjoyed a pretty high popularity (nearly 30% of the respondents mentioning them): Jidvei was the leader (13%), followed by the wines produced in the Târnave area and in Alba County (10%), Ciumbrud (4%), and Salina Turda (1%); other popular Romanian vineyards were: Banat (9%), Moldova (9%), and Murfatlar (7%). A significant quota of the sample (17%) indicated other smaller winemakers, while 63% did not mention any vineyard.

Regarding the consumption of certain types of wines, respondents confirm their occasional consumption habits, picking white, red, and rosé wines as well, without a specific preference for dry, demi-dry, demi-sweet, or sweet wines (

Table 5). In fact, demand seems to be balanced among the classic types of wine, with a somewhat lower preference for sweet wines. This is consistent with the Romanian cuisine, and with the habit of associating sweet and demi-sweet wines with desserts.

The very low interest towards brandy may be explained on behalf of the existence of other types of spirits, such as the national țuica, a strong alcoholic drink, commonly consumed as appetizer; it is commonly homemade with fruit, especially of plums but also of other fruits (apples, pears, apricots, etc.). Perhaps, craft producers of țuica are more frequently found than craft-winemakers. Romanians still seemed to be somewhat conservative in tastes, and for many brandies may be perceived as too sophisticated, while whiskey drinkers are still few, compared to those who consume țuica. Likewise, in Romania, sparkling wines are still commonly associated with sophisticated desserts and special events, hence the relatively low demand for it, too.

Two questions were formulated aimed at establishing whether Romanian consumers are familiarized with, and would be interested in buying, products made of grape derivates. It is highly interesting to note that 65% of the respondents were (somewhat) familiar with such products. Moreover, even some of those who were not aware of such products would be willing to buy one or more of them: Natural supplements (55%), vinegar (54%), cosmetics (37%), oil (29%), bread (27%), mustard (20%), and flour (16%).

Respondents were asked to express their categorical or relative agreement, or disagreement with six statements which were formulated by the researchers with the purpose of better understanding when, why, and how the subjects consume wine. Thus, for most people wine is a beverage consumed at mealtimes, as it highlights certain dishes and flavors (52% fully agree and 28% expressed a relative agreement). Furthermore, wine is a refined drink (34% fully agree and 50% partially agree). For most respondents, wine is the most natural drink (categorical agreement for 31% and partial agreement of 44%). In the perception of Romanian consumers, wine is a drink that enables socialization (30% total agreement and 52% partial agreement). Thus, wine tasting is an activity that can and should be introduced in the program of various business meetings, travels, and events, including field trips, conferences, or incentive trips for employees and managers, etc. Even though initially most respondents associated wine with meals, they did not consider it to be an important part of mealtimes (16% fully disagree, 46% rather disagree, while only 29% partially agree and 9% totally agree). Furthermore, very many of the respondents did not consider that wine contributes to digestion (10% fully agree, 36%partially agree, while 44% rather disagree and 11% fully disagree). These two opinions may be explained due to the lack of education and culture related to the consumption of alcoholic drinks, in general, and of wine, in particular. At the opposed pole, in French people regularly drink a glass of wine at lunch and are allowed to drive afterwards.

When asked about their previous wine tourism experiences, less than 13% confirmed having practiced tourism on a wine road in Romania or abroad. Moreover, 90% of those who have never visited a cellar, would be attracted to visit one in Romania and 70% would like to travel abroad as well; the somewhat lower interest towards international wine tourism may be due to various factors, including budget limitations.

The research continued with measuring the respondents’ interest towards wine-tourism in Romania. Thus, nearly 48% of the respondents were familiarized and considered attractive the tourist offer associated to the Romanian Roads of Wine, while 17% of the interviewees were aware of this offer but did not consider it appropriate. Still, an important quota of the sample (35%) were not aware of the possibilities to practice wine tourism in Romania. A rather peculiar finding was that 63.4% of the interviewed persons declared they did not know exactly what wine tourism involves, while only 36.6% are truly familiar with this concept. Still, despite the low familiarization of the respondents with this type of tourism, most of them expressed their interest towards practicing it in Romania. Overall, most of them (83%) would find the development of wine tourism in Romania as very attractive. More than half of the respondents who would like to attend wine tastings would also seek accommodation services, opting for one or more types of public lodging facilities: Boarding houses (65%), lodging facilities at the wine cellar/in the vineyard (56%), hotels (34%), or villas (33%); nearly a quarter of the respondents would accommodate in the private homes of the locals (23%). More than a third of the interviewees (34%) mentioned they would be interested to participate in organized groups, while 12% would like to travel independently. If considering wine tourism, most of the respondents would opt for short trips involving two to three overnight stays (64%) or for two-day trips, with one overnight (28%); some 6% would spend more than three nights on such trips, while only 2% would not seek accommodation services. Obviously, most people seek solutions to avoid drinking and driving. This is a clear business opportunity for many providers of hospitality services either to provide lodging and food services for wine tourists, or, for travel agencies to organize wine tasting day trips or more than one day tours. Even locals may capitalize on the desire of the potential tourists to accommodate in private residencies. An excellent example of sustainable valorization of market opportunities is provided by the community of Sâncraiu, Cluj County, where Mr Vincze, a local entrepreneur, managed to organize for people to register their homes as agritourist boarding houses and to cooperate in accommodating tourists [

93] (pp. 7–23).

Perhaps influenced by the fact that vineyards are commonly associated with grape picking, nearly half of the respondents (48%) indicated autumn, followed by spring (21%) as preferred seasons for wine tasting trips, while the other split evenly between summer (16%) and winter (15%). This distribution reveals that respondents associate this type of activity with short breaks or even with business and corporate trips, and not necessarily with typical holidays. Wine cellar owners ought to consider this potential interest and capitalize on it. Of particular interest are several recreational activities that can be associated to wine tasting trips, some of them including the tourists’ direct involvement in specific activities: Traditional local dishes (74%), nature walks (in the vineyards) and hill hiking (67%), winemaking (58%), guided tours of historical sites and monuments (56%), mountaineering (45%), wine picking and harvesting (38%), chariot rides (37%), bicycle riding (33%), outdoors relaxation and recreation (28%), birdwatching (12%), working in the vineyard, e.g., wine digging (7%), etc. In terms of potential destinations for wine tourism, the interviewees provided the following preferences. On a scale from 1 (rather unattractive) to 5 (very attractive), vineyards from Alba County seem to be quite attractive, enjoying relatively good average scores (

Figure 7).

When asked to be more specific about how they would expect wine tastings to take place, the respondents provided the following preferences:

3–4 types of wine plus snacks (29%),

3–4 types of wine plus starters (28%),

3–4 types of wine plus lunch (12%),

4–5 types of wine plus snacks (14%),

4–5 types of wine plus starters (8%),

4–5 types of wine plus lunch (9%).

Furthermore, in terms of spending, most of the respondents (65%) would be willing to spend at most 30 euro per person for a wine tasting session with meal included, while 31% would allot between 30 and 50 euro per person, and only 4% would spend more than 50 euro. On one hand, the budget is consistent with the rather low income levels of Romanian citizens (and also of a consistent part of the sample members) and can be further explained in correlation with the respondents’ lack of knowledge related to wine tourism, while, on the other hand, the allocated amounts match most of the wineries’ offers for one wine tasting session with snacks or starters. Given the relatively high demand for 3–4 types of wine plus snacks and starters, it does not seem too difficult for winemakers to come up with an offer that can match the tourists’ expectations and budgets.

The investigated sample presented the following structure. It was dominated by young respondents, mainly due to the massive online distribution of the survey: 18–25 years old (54%), 26–35 years old (23%), 35–55 years old (22%), and over 55 years old (1%). The gender distribution was almost relatively even: Female (58%) and male (42%). By occupation, most of the respondents (34%) were continuing their graduate studies, 22% were employed in the private environment, 17% worked for state institutions, 17% were entrepreneurs, 8% were still students but also work, 1% were retired and 1% were unemployed. In terms of income levels, given the age structure of the sample: 34% earn less than 300 euro (1500 Lei), 29% have incomes between 300 and 500 euro (1500–2500 Lei), while the remaining 37% earn more than 500 euro (2500 Lei). Most respondents had earned or will earn shortly graduate and/or post-graduate degrees, while 16% have only undergraduate studies. Most respondents resided in Transylvania (36% in region center and another 36% in the north-west region of development), all other regions were represented by relatively few respondents.

Various statistical bi-variate tests were run in order to verify the existence of significant relations among respondents’ features and behaviors. Several conclusions may be drawn regarding the profile of the sample members as consumers:

- •

The average income level of the respondents:

- ⚬

Does not influence their habitual alcohol consumption (p = 0.373 and r = –0.041); in fact, most of them are occasional consumers;

- ⚬

Does not influence the attractiveness of wine tasting (p = 0.139 and r = 0.067);

- ⚬

determines a weak influence upon the wine tasting budget (p = 0.023 and r = 0.31), thus, an income increase may determine a higher spending;

- ⚬

Does not influence the consumption of beer (p = 0.671 and r = 0.019), nor that of spirits (p = 0.068 and r = −0.083), implying that the consumption of somewhat unsophisticated and cheaper drinks is not dependent on the level of the consumers’ revenues;

- ⚬

Does not determine a significant influence on the demand for long and short drinks (p = 0.007 and r = −0.123), nor on that for cocktails (p = 0.068 and r = –0.083);

- ⚬

Determines a significant weak influence upon the consumption of wine (p = 0.000 and r = 0.270), meaning that higher revenues may contribute to the demand increase of wine;

- ⚬

Does not influence the respondents’ destination choice; obviously, that may be determined by other triggering factors such as seasonality, trends, etc.; moreover, the income level does not seem to influence the wine tasting trips of the questioned subject (wine tasting trips in Romania (p = 0.552 and r = 0.27) and wine tasting trips abroad (p = 0.808 and r = –0.011)), as the decision of practicing this type of tourism may be influenced by the awareness of the tourists regarding such opportunities, respectively of the notoriety of such destinations.

- •

The respondents’ gender seems:

- ⚬

To slightly determine the consumption of alcoholic drinks: in the case of beer (p = 0.000 and r = −0.338), spirits (p = 0.000 and r = 0.332), but not in that of wine (p = 0.133 and r = –0.068), cocktails (p = 0.000 and r = 0.190) or long and/or short drinks (p = 0.792 and r = –0.012);

- ⚬