The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials?

Abstract

:1. Introduction

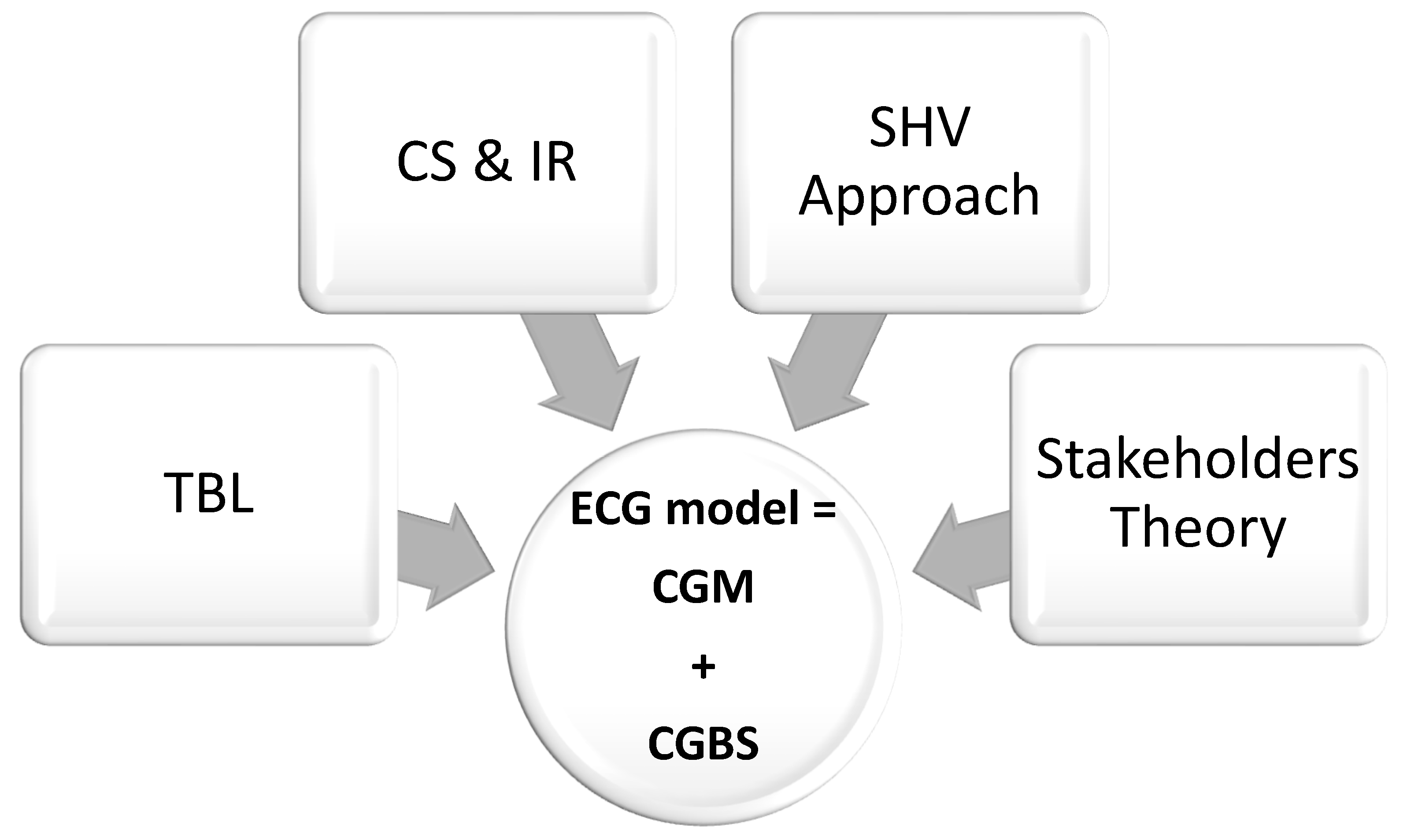

2. Theoretical Framework

2.1. Stakeholders Theory and ECG Model

2.2. Shared Value Approach and ECG Model

2.3. Triple Bottom Line and ECG Model

2.4. Corporate Sustainability, Integrated Reporting, and ECG Model

3. Methodology

3.1. Data-Gathering and Sample Profile

3.2. Measures

3.3. Analysis Technique

4. Findings

5. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Factor | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | Communality | |

| A1 | 0.923 | 0.965 | ||||

| A2 | 0.925 | 0.965 | ||||

| A3 | 0.916 | 0.945 | ||||

| A4 | 0.929 | 0.953 | ||||

| B1 | 0.916 | 0.921 | ||||

| B2 | 0.937 | 0.952 | ||||

| B3 | 0.889 | 0.854 | ||||

| B4 | 0.934 | 0.932 | ||||

| C1 | 0.668 | 0.498 | ||||

| C2 | 0.817 | 0.773 | ||||

| C3 | 0.463 | 0.461 | 0.484 | |||

| C4 | 0.774 | 0.627 | ||||

| D1 | 0.724 | 0.615 | ||||

| D2 | 0.732 | 0.682 | ||||

| D3 | 0.787 | 0.789 | ||||

| D4 | 0.430 | 0.353 | ||||

| E1 | 0.843 | 0.785 | ||||

| E2 | 0.839 | 0.712 | ||||

| E3 | 0.441 | 0.609 | 0.613 | |||

| E4 | 0.481 | 0.396 | ||||

| Squared Multiple Correlation | Cronbach’s Alpha if Item Deleted | |

|---|---|---|

| A1 | 0.989 | 0.788 |

| A2 | 0.989 | 0.791 |

| A3 | 0.959 | 0.799 |

| A4 | 0.963 | 0.799 |

| B1 | 0.919 | 0.800 |

| B2 | 0.955 | 0.799 |

| B3 | 0.851 | 0.801 |

| B4 | 0.940 | 0.800 |

| C1 | 0.330 | 0.792 |

| C2 | 0.588 | 0.782 |

| C3 | 0.519 | 0.796 |

| C4 | 0.463 | 0.789 |

| D1 | 0.381 | 0.792 |

| D2 | 0.486 | 0.782 |

| D3 | 0.591 | 0.784 |

| D4 | 0.367 | 0.791 |

| E1 | 0.474 | 0.789 |

| E2 | 0.489 | 0.795 |

| E3 | 0.512 | 0.788 |

| E4 | 0.379 | 0.790 |

| Chronbach’s Alpha (full set of items): 0.801 ANOVA test (full set of items): 473.787 (df.: 19; Significance: 0.000) | ||

| Factor | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | Communality | |

| A1 | 0.945 | 0.984 | ||||

| A2 | 0.948 | 0.982 | ||||

| A3 | 0.937 | 0.964 | ||||

| A4 | 0.947 | 0.971 | ||||

| B1 | 0.914 | 0.915 | ||||

| B2 | 0.938 | 0.953 | ||||

| B3 | 0.900 | 0.872 | ||||

| B4 | 0.942 | 0.949 | ||||

| C1 | 0.761 | 0.638 | ||||

| C2 | 0.831 | 0.776 | ||||

| C4 | 0.765 | 0.614 | ||||

| D1 | 0.745 | 0.644 | ||||

| D2 | 0.657 | 0.654 | ||||

| D3 | 0.417 | 0.770 | 0.790 | |||

| D4 | 0.270 | |||||

| E1 | 0.879 | 0.838 | ||||

| E2 | 0.841 | 0.716 | ||||

| E4 | 0.489 | 0.383 | ||||

| Total | ||||||

| Eigenvalue | 6.830 | 2.435 | 2.269 | 1.308 | 1.050 | 13.892 |

| % of Variance | 37.946 | 13.629 | 12.608 | 7.266 | 5.831 | 77.280 |

| A1 | A2 | A3 | A4 | B1 | B2 | B3 | B4 | C1 | C2 | C4 | D1 | D2 | D4 | E1 | E2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A2 | 915.97 (0.000) | |||||||||||||||

| A3 | 305.52 (0.000) | 347.46 (0.000) | ||||||||||||||

| A4 | 417.26 (0.000) | 463.39 (0.000) | 361.35 (0.000) | |||||||||||||

| B1 | 4.531 (0.000) | 3.961 (0.000) | 5.052 (0.000) | 5.045 (0.000) | ||||||||||||

| B2 | 4.945 (0.000) | 4.619 (0.000) | 4.593 (0.000) | 4.863 (0.000) | 239.09 (0.000) | |||||||||||

| B3 | 8.808 (0.000) | 7.766 (0.000) | 7.159 (0.000) | 7.774 (0.000) | 73.763 (0.000) | 101.15 (0.000) | ||||||||||

| B4 | 5.559 (0.000) | 5.015 (0.000) | 5.228 (0.000) | 5.464 (0.000) | 94.132 (0.000) | 243.10 (0.000) | 180.60 (0.000) | |||||||||

| C1 | 1.590 (0.011) | 1.502 (0.017) | 1.791 (0.004) | 1.878 (0.002) | 2.302 (0.000) | 2.429 (0.000) | 1.832 (0.002) | 1.726 (0.003) | ||||||||

| C2 | 1.657 (0.006) | 1.521 (0.016) | 1.544 (0.011) | 1.654 (0.006) | 1.724 (0.003) | 1.870 (0.001) | 1.643 (0.007) | 1.704 (0.004) | 1.888 (0.001) | |||||||

| C4 | 1.710 (0.004) | 1.609 (0.007) | 1.948 (0.001) | 2.046 (0.001) | 3.555 (0.000) | 3.293 (0.000) | 2.626 (0.000) | 2.562 (0.000) | 2.119 (0.000) | 5.965 (0.000) | ||||||

| D1 | 1.595 (0.011) | 1.503 (0.017) | 1.898 (0.005) | 2.089 (0.001) | 3.059 (0.000) | 2.349 (0.000) | 1.669 (0.006) | 2.169 (0.001) | 2.188 (0.001) | 5.885 (0.000) | 2.956 (0.000) | |||||

| D2 | 1.431 (0.040) | 1.457 (0.041) | 1.561 (0.015) | 1.568 (0.015) | 1.606 (0.007) | 1.691 (0.006) | 1.710 (0.004) | 1.761 (0.004) | 1.803 (0.002) | 2.325 (0.000) | 4.503 (0.000) | 1.981 (0.001) | ||||

| D4 | 2.653 (0.000) | 2.425 (0.000) | 2.788 (0.000) | 3.024 (0.000) | 2.742 (0.000) | 2.446 (0.000) | 1.743 (0.003) | 2.371 (0.000) | 2.522 (0.000) | 3.701 (0.000) | 2.947 (0.000) | 3.016 (0.000) | 3.173 (0.000) | |||

| E1 | 2.241 (0.000) | 2.037 (0.001) | 2.237 (0.000) | 2.608 (0.000) | 2.032 (0.001) | 2.079 (0.000) | 1.910 (0.001) | 2.058 (0.000) | 8.099 (0.000) | 3.200 (0.000) | 2.191 (0.001) | 1.914 (0.002) | 3.778 (0.000) | 4.009 (0.000) | ||

| E2 | 1.528 (0.016) | 1.612 (0.007) | 1.633 (0.005) | 1.442 (0.044) | 1.532 (0.011) | 1.734 (0.003) | 1.741 (0.003) | 1.546 (0.017) | 1.806 (0.002) | 4.022 (0.000) | 2.646 (0.000) | 1.502 (0.017) | 1.950 (0.001) | 2.906 (0.000) | 1.523 (0.021) | |

| E4 | 1.603 (0.007) | 1.726 (0.005) | 1.734 (0.005) | 1.804 (0.003) | 3.316 (0.000) | 2.457 (0.000) | 1.895 (0.002) | 1.852 (0.002) | 5.159 (0.000) | 2.251 (0.001) | 4.953 (0.000) | 2.319 (0.000) | 2.529 (0.000) | 2.787 (0.000) | 1.842 (0.002) | 1.647 (0.006) |

References

- Brundtland, G.; Khalid, M.; Agnelli, S.; Al-Athel, S.; Chidzero, B.; Fadika, L.; Singh, M. Our Common Future; Brundtland report; United Nations World Commission on Environment and Development: New York, NY, USA, 1987. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strateg. Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R.L. Corporate sustainability accounting: A nightmare or a dream coming true? Bus. Strateg. Environ. 2006, 15, 293–295. [Google Scholar] [CrossRef]

- Johnson, M.P.; Schaltegger, S. Two decades of sustainability & management tools for SMEs: How far have we come? J. Small Bus. Manag. 2016, 54, 481–505. [Google Scholar]

- La Torre, M.; Trotta, A.; Chiappini, H.; Rizzello, A. Business models for sustainable finance: The case study of social impact bonds. Sustainability 2019, 11, 1887. [Google Scholar] [CrossRef]

- Flower, J. The international integrated reporting council: A story of failure. Crit. Perspec. Acc. 2015, 27, 1–17. [Google Scholar] [CrossRef]

- Dumay, J.; Bernardi, C.; Guthrie, J.; Demartini, P. Integrated reporting: A structured literature review. Acc. Forum 2016, 40, 166–185. [Google Scholar] [CrossRef]

- Klaus, F.; Kroczak, A.; Facchinetti, G.; Egloff, S. Economy for the Common Good. DAS in Sustainable Business; Business School Lausanne: Lausanne, Switzerland, 2013; Available online: https://balance.ecogood.org/ecg-reports/bsl-economy-of-the-common-good.pdf (accessed on 15 April 2019).

- Frémeaux, S.; Michelson, G. The common good of the firm and humanistic management: Conscious capitalism and economy of communion. J. Bus. Ethics 2017, 145, 701–709. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of the 21st-Century Business; Capstone Publishing: Oxford, UK, 1997. [Google Scholar]

- Felber, C. Neue Werte für die Wirtschaft—eine Alternative zu Kapitalismus und Kommunismus; Deuticke: Vienna, Àustria, 2008. [Google Scholar]

- Felber, C. Gemeinwohl-Ökonomie; Piper: Munich, Germany, 2018. [Google Scholar]

- Felber, C. Change Everything: Creating an Economy for the Common Good; Zed Books: London, UK, 2015. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman Publishing: Boston, MA, USA, 1984. [Google Scholar]

- European Economic and Social Committee. The Economy for the Common Good: A Sustainable Economic Model Geared Towards Social Cohesion, EUR-Lex. 2016. Available online: lex.europa.eu/legal-content/EN/TXT/ (accessed on 15 April 2019).

- Foti, V.T.; Scuderi, A.; Timpanaro, G. The economy of the common good: The expression of a new sustainable economic model. Qual. Acc. Suc. 2017, 18, 16. [Google Scholar]

- Gómez-Calvo, V.; Gómez-Alvarez, R. The economy for the common good and the social and solidarity economies, are they complementary? CIRIEC J. Pub. Soc. Coop. Econ. 2017, 87, 257–294. [Google Scholar]

- Dierksmeier, C.; Pirson, M. Oikonomia versus chrematistiké, learning from aristotle about the future orientation of business management. J. Bus. Ethics 2009, 88, 417–430. [Google Scholar] [CrossRef]

- Freeman, R.E.; Reed, D.L. Stockholders and stakeholders: A new perspective on corporate governance. Calif. Manag. Rev. 1983, 25, 88–106. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Friedman, A.L.; Miles, S. Stakeholders: Theory and Practice; Oxford University Press: Oxford, UK, 2006. [Google Scholar]

- Adeneye, Y.B.; Ahmed, M. Corporate social responsibility and company performance. J. Bus. Stud. Quart. 2015, 7, 151–166. [Google Scholar]

- Jiang, C.; Fu, Q. A Win-win outcome between corporate environmental performance and corporate value: From the perspective of stakeholders. Sustainability 2019, 11, 921–939. [Google Scholar] [CrossRef]

- Lux, S.; Crook, R.; Woehr, D.J. Mixing business with politics: A meta-analysis of the antecedents and outcomes of corporate political activity. J. Manag. 2011, 37, 223–247. [Google Scholar] [CrossRef]

- Carroll, A.B.; Buchholtz, A. Business and Society: Ethics and Stakeholder Management, 6th ed.; Thompson Learning: Mason, OH, USA, 2006. [Google Scholar]

- Ackermann, F.; Eden, C. Strategic management of stakeholders: Theory and practice. Long Range Plan. 2011, 44, 179–196. [Google Scholar] [CrossRef]

- Bellantuono, N.; Pontrandolfo, P.; Scozzi, B. Capturing the stakeholders’ view in sustainability reporting: A novel approach. Sustainability 2016, 8, 379. [Google Scholar] [CrossRef]

- Miles, S. Stakeholder theory classification: A theoretical and empirical evaluation of definitions. J. Bus. Ethics 2017, 142, 437–459. [Google Scholar] [CrossRef]

- Smith, H.J. The Shareholders vs. Stakeholders debate. MIT Sloan Manag. Rev. 2003, 44, 85–91. [Google Scholar]

- Argandoña, A. The stakeholder theory and the common good. J. Bus. Ethics 1998, 17, 1093–1102. [Google Scholar] [CrossRef]

- Porter, M.; Kramer, M. Creating shared value. Harvard Bus. Rev. 2011, 89, 1–17. [Google Scholar]

- Barisan, L.; Lucchetta, M.; Bolzonella, C.; Boatto, V. How does carbon footprint create shared values in the wine industry? Empirical evidence from prosecco superiore PDO’s wine district. Sustainability 2019, 11, 3037. [Google Scholar] [CrossRef]

- Porter, M.; Kramer, M. Strategy and society: The link between competitive advantage and corporate social responsibility. Harvard Bus. Rev. 2006, 84, 1–13. [Google Scholar]

- Wójcik, P. How creating shared value differs from corporate social responsibility. J. Manag. Bus. Admin. 2016, 24, 32–55. [Google Scholar] [CrossRef]

- Florin, J.; Schmidt, E. Creating shared value in the hybrid venture arena: A business model innovation perspective. J. Soc. Entrepren. 2011, 2, 165–197. [Google Scholar] [CrossRef]

- Beschorner, T. Creating shared value: The one-trick pony approach. Bus. Ethics J. Rev. 2014, 1, 106–112. [Google Scholar] [CrossRef]

- Michelini, L.; Fiorentino, D. New business models for creating shared value. Soc. Responsib. J. 2012, 8, 561–577. [Google Scholar] [CrossRef]

- Pfitzer, M.; Bockstette, V.; Stamp, M. Innovating for shared value. Harvard Bus. Rev. 2013, 91, 100–107. [Google Scholar]

- De los Reyes, G., Jr.; Scholz, M.; Smith, N.C. Beyond the “Win-Win” creating shared value requires ethical frameworks. Calif. Manag. Rev. 2017, 59, 142–167. [Google Scholar] [CrossRef]

- Hartman, L.P.; Werhane, P.H. Proposition: Shared value as an incomplete mental model. Bus. Ethics J. Rev. 2013, 1, 36–43. [Google Scholar] [CrossRef]

- Crane, A.; Palazzo, G.; Spence, L.J.; Matten, D. Contesting the value of creating shared value. Calif. Manag. Rev. 2014, 56, 130–153. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horizons 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Ansaram, K.; Pariag-Maraye, N. Modelling the impact of responsibility levels on corporate financial performance: The. case of top 100 firms in mauritius Bus. Econ. Res. 2018, 8, 118–138. [Google Scholar]

- Jose, S.; Venkitachalam, K. A matrix model towards CSR—Moving from one size fit approach. J. Strat. Manag. 2019, 12, 243–255. [Google Scholar] [CrossRef]

- Savitz, A. The Triple Bottom Line: How Today’s Best-Run Companies are Achieving Economic, Social and Environmental Success-And How you can too; John Wiley & Sons: Hoboken, NJ, USA, 2013. [Google Scholar]

- Fauzi, H.; Svensson, G.; Rahman, A.A. “Triple bottom line” as “Sustainable corporate performance”: A proposition for the future. Sustainability 2010, 2, 1345–1360. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Norman, W.; MacDonald, C. Getting to the bottom of the triple bottom line. Bus. Ethics Quart. 2004, 14, 243–262. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A.; Appolloni, A. Sustainability value creation, survival, and growth of the company: A critical perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 2019, 11, 2119–2138. [Google Scholar] [CrossRef]

- Hubbard, G. Measuring organizational performance: Beyond the triple bottom line. Bus. Strat. Environ. 2009, 18, 177–191. [Google Scholar] [CrossRef]

- Elkington, J. The Holy Grail of Integrated Reporting. 2009. Available online: http://www.sustainability.com/blog/the-holy-grail-of-integrated-reporting (accessed on 8 April 2019).

- Elkington, J. 25 years ago i coined the phrase “Triple Bottom Line.” Here’s why it’s time to rethink it. Harvard Bus. Rev. 2018. Available online: https://hbr.org/2018/06/25-years-ago-i-coined-the-phrase-triple-bottom-line-heres-why-im-giving-up-on-it (accessed on 8 April 2019).

- Gray, R.; Milne, M. Sustainability reporting: Who’s kidding whom? Chart. Account. J. New Zeal. 2002, 81, 66–70. [Google Scholar]

- McDonough, W.; Braungart, M. Design for the triple top line: New tools for sustainable commerce. Corp. Environ. Strat. 2002, 9, 251–258. [Google Scholar] [CrossRef]

- Henderson, J.C. Corporate social responsibility and tourism: Hotel companies in Phuket, Thailand, after the Indian Ocean tsunami. Int. J. Hosp. Manag. 2007, 26, 228–239. [Google Scholar] [CrossRef]

- Salzmann, O.; Ionescu-Somers, A.; Steger, U. The business case for corporate sustainability: Literature review and research options. Eur. Manag. J. 2005, 23, 27–36. [Google Scholar] [CrossRef]

- Fechete, F.; Nedelcu, A. Performance management assessment model for sustainable development. Sustainability 2019, 11, 2779. [Google Scholar] [CrossRef]

- Van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: Separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Atkinson, G. Measuring corporate sustainability. J. Environ. Plan. Manag. 2000, 43, 235–252. [Google Scholar] [CrossRef]

- Perrini, F.; Tencati, A. Sustainability and stakeholder management: The need for new corporate performance evaluation and reporting systems. Bus. Strat. Environ. 2006, 15, 296–308. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business cases for sustainability: The role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119. [Google Scholar] [CrossRef]

- Raluca, C.; Costin, V. Performance evaluation of the implementation of the 2013/34/EU directive in Romania on the basis of corporate social responsibility reports. Sustainability 2019, 11, 2531–2547. [Google Scholar]

- Aras, G.; Crowther, D. Corporate sustainability reporting: A study in disingenuity? J. Bus. Ethics 2009, 87, 279. [Google Scholar] [CrossRef]

- Willis, A. The role of the global reporting initiative’s sustainability reporting guidelines in the social screening of investments. J. Bus. Ethics 2003, 43, 233–237. [Google Scholar] [CrossRef]

- Visser, W.; Tolhurst, N. The World Guide to CSR: A Country-by-Country Analysis of Corporate Sustainability and Responsibility; Routledge: London, UK, 2017. [Google Scholar]

- Levy, D.L.; Szejnwald Brown, H.; De Jong, M. The contested politics of corporate governance: The case of the global reporting initiative. Bus. Soc. 2010, 49, 88–115. [Google Scholar] [CrossRef]

- Ballou, B.; Heitger, D.L.; Landes, C.E.; Adams, M. The future of corporate sustainability reporting. J. Account. 2006, 202, 65–74. [Google Scholar]

- Milne, M.J.; Gray, R. W(h)ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- González, J.A.; Núñez, J. Socially responsible investment: A view from the social rating agencies of Vigeo-Eiris and MSCI ESG Stats. Financ. Mark. Valuat. 2018, 4, 39–55. [Google Scholar]

- Association for the promotion of the Economy for the Common Good. Common Good Matrix. 2015. Available online: https://www.ecogood.org/en/common-good-balance-sheet/common-good-matrix/ (accessed on 8 April 2019).

- Heidbrink, L.; Kny, J.; Köhne, R.; Sommer, B.; Stumpf, K.; Welzer, H.; Wiefek, J. Schlussbericht für das Verbundprojekt Gemeinwohl-Ökonomie im Vergleich Unternehmerischer Nachhaltigkeitsstrategien (GIVUN). Flensburg & Kiel, 2018. Available online: https://www.ecogood.org/media/filer_public/2a/b5/2ab5defc-c5a0-4164-9b05-6efbc3019ad4/givun-schlussbericht.pdf (accessed on 8 April 2019).

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 6th ed.; Pearson New International Edition: Harlow, UK, 2010. [Google Scholar]

- Rummel, R.J. Applied Factor Analysis; Northwestern University Press: Evanston, IL, USA, 1970. [Google Scholar]

- Gorsuch, R.L. Factor Analysis; Hillsdale, Lawrence Erlbaum Associates: Hoboken, NJ, USA, 1983. [Google Scholar]

- Muthen, B.; Kapplan, D. A comparison of some methodologies for the factor analysis of non-normal like variables. Br. J. Math. Stat. Psychol. 1985, 38, 171–189. [Google Scholar] [CrossRef]

- Kaiser, H.F. A second-generation little jiffi. Psychometrica 1970, 35, 401–415. [Google Scholar] [CrossRef]

- Kaiser, H.F. Little Jiffi, Mark IV. Educ. Psychol. Meas. 1974, 34, 111–117. [Google Scholar] [CrossRef]

- Borgatta, E.F.; Kercher, K.; Stull, D.E. A cautionary note on the use of principal component analysis. Sociol. Meth. Res. 1986, 15, 160–168. [Google Scholar] [CrossRef]

- Snook, S.C.; Gorsuch, R.L. Principal component analysis versus common factor analysis: A monte carlo study. Psychol. Bull. 1989, 106, 148–154. [Google Scholar] [CrossRef]

- Gorsuch, R.L. Common factor analysis versus component analysis: Some well and little-known facts. Multiv. Behav. Res. 1990, 25, 33–39. [Google Scholar] [CrossRef]

- Mulaik, S.A. Bluring the distinction between component analysis and common factor analysis. Multiv. Behav. Res. 1990, 25, 53–59. [Google Scholar] [CrossRef]

- Velicer, W.F.; Jackson, D.N. Component analysis versus common factor analysis: Some issues in selecting an appropriate procedure. Multiv. Behav. Res. 1990, 25, 1–28. [Google Scholar] [CrossRef]

- Anderson, J.C.; Gerbing, D.W.; Hunter, J.E. On the assessment of unidimensional measurement: Internal and external consistency and overall consistency criteria. J. Mark. Res. 1987, 24, 432–437. [Google Scholar] [CrossRef]

- Hattie, J. Methodology review: Assessing unidimensionality of test and items. Appl. Psychol. Measur. 1985, 9, 139–164. [Google Scholar] [CrossRef]

- McDonald, R.P. The dimensionality of tests and items. Br. J. Math. Soc. Psychol. 1981, 34, 100–117. [Google Scholar] [CrossRef]

- Nunnally, J.L. Psychometric Theory, 2nd ed.; McGraw-Hill: New York, NY, USA, 1979. [Google Scholar]

| Dimension | Items | Measurement Scales |

|---|---|---|

| Suppliers A | A1. Human dignity in the supply chain. A2. Solidarity and social justice in the supply chain. A3. Environmental sustainability in the supply chain. A4. Transparency and co-determination in the supply chain. | Absolute values (scores) |

| Owners, equity and financial service providers B | B1. Ethical position in relation to financial resources. B2. Social position in relation to financial resources. B3. Use of funds in relation to the environment. B4. Ownership and co-determination. | Absolute values (scores) |

| Employees C | C1. Human dignity in the workplace and the working environment. C2. Self-determined working arrangements. C3. Environmentally friendly behavior of staff. C4. Co-determination and transparency within the organization. | Absolute values (scores) |

| Customers and business partners D | D1. Ethical customer relations. D2. Cooperation and solidarity with other companies. D3. Impact on the environment of the use and disposal of products and services. D4. Customer participation and product transparency. | Absolute values (scores) |

| Social environment E | E1. Purpose of products and services and their effects on society. E2. Contribution to the community. E3. Reduction of environmental impact. E4. Social co-determination and transparency. | Absolute values (scores) |

| M | SD | Z Skewness | Z Kurtosis | Shapiro-Wilk | ||

|---|---|---|---|---|---|---|

| Statistic | Significance | |||||

| A1 | 19.50 | 8.695 | 0.180 | −0.584 | 0.984 | 0.322 |

| A2 | 15.32 | 6.681 | 0.041 | −0.748 | 0.981 | 0.610 |

| A3 | 4.46 | 1.914 | 0.320 | 0.111 | 0.962 | 0.850 |

| A4 | 4.45 | 1.865 | 0.347 | 0.425 | 0.954 | 0.197 |

| B1 | 3.23 | 2.123 | 0.911 | 0.763 | 0.925 | 0.373 |

| B2 | 4.27 | 2.808 | 0.874 | 0.499 | 0.971 | 0.524 |

| B3 | 1.73 | 1.263 | 0.643 | 0.043 | 0.919 | 0.931 |

| B4 | 3.19 | 1.985 | 0.740 | −0.065 | 0.956 | 0.226 |

| C1 | 51.60 | 18.968 | 0.022 | −0.571 | 0.991 | 0.243 |

| C2 | 65.13 | 27.603 | −0.213 | −0.292 | 0.996 | 0.929 |

| C3 | 15.07 | 9.372 | 2.204 | 9.113 | 0.938 | 0.104 |

| C4 | 29.70 | 25.959 | 0.643 | −0.577 | 0.943 | 0.701 |

| D1 | 29.47 | 10.004 | 0.213 | 1.590 | 0.980 | 0.506 |

| D2 | 47.35 | 19.569 | 0.493 | 0.521 | 0.996 | 0.306 |

| D3 | 40.48 | 22.023 | 0.252 | −0.987 | 0.942 | 0.267 |

| D4 | 14.37 | 12.490 | 1.935 | 1.841 | 0.984 | 0.421 |

| E1 | 52.16 | 19.630 | −0.127 | −0.320 | 0.987 | 0.167 |

| E2 | 59.33 | 26.145 | −0.253 | −0.699 | 0.995 | 0.736 |

| E3 | 26.42 | 16.889 | 0.634 | 0.068 | 0.914 | 0.059 |

| E4 | 9.78 | 9.167 | 1.427 | 2.013 | 0.959 | 0.297 |

| A1 | A2 | A3 | A4 | B1 | B2 | B3 | B4 | C1 | C2 | C3 | C4 | D1 | D2 | D3 | D4 | E1 | E2 | E3 | E4 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A1 | 1.000 | 0.993 * | 0.964 * | 0.969 * | 0.390 * | 0.397 * | 0.421 * | 0.403 * | 0.265 * | 0.180 | 0.442 * | 0.203 * | 0.287 * | 0.195 | 0.518 * | 0.359 * | 0.328 * | 0.067 | 0.527 * | 0.295 * |

| A2 | 1.000 | 0.964 * | 0.967 * | 0.372 * | 0.387 * | 0.405 * | 0.388 * | 0.264 * | 0.184 | 0.439 * | 0.209 * | 0.266 * | 0.190 | 0.523 * | 0.351 * | 0.337 * | 0.063 | 0.529 * | 0.286 * | |

| A3 | 1.000 | 0.972 * | 0.394 * | 0.393 * | 0.385 * | 0.383 * | 0.281 * | 0.197 | 0.449 * | 0.189 | 0.315 * | 0.220 * | 0.495 * | 0.337 * | 0.318 * | 0.065 | 0.500 * | 0.283 * | ||

| A4 | 1.000 | 0.383 * | 0.379 * | 0.392 * | 0.384 * | 0.274 * | 0.188 | 0.447 * | 0.192 | 0.297 * | 0.208 * | 0.472 * | 0.368 * | 0.292 * | 0.073 | 0.485 * | 0.273 * | |||

| B1 | 1.000 | 0.949 * | 0.826 * | 0.895 * | 0.272 * | 0.128 | 0.543 * | 0.211 * | 0.371 * | 0.302 * | 0.114 | 0.244 * | 0.206 * | 0.154 | 0.240 * | 0.366 * | ||||

| B2 | 1.000 | 0.859 * | 0.947 * | 0.286 * | 0.127 | 0.510 * | 0.212 * | 0.357 * | 0.293 * | 0.133 | 0.226 * | 0.229 * | 0.136 | 0.265 * | 0.364 * | |||||

| B3 | 1.000 | 0.912 * | 0.241 * | 0.075 | 0.407 * | 0.204 | 0.275 * | 0.280 * | 0.156 | 0.207 * | 0.241 * | 0.079 | 0.273 * | 0.288 * | ||||||

| B4 | 1.000 | 0.276 * | 0.078 | 0.440 * | 0.175 | 0.327 * | 0.281 * | 0.131 | 0.227 * | 0.237 * | 0.109 | 0.247 * | 0.299 * | |||||||

| C1 | 1.000 | 0.296 * | 0.253 * | 0.212 * | 0.424 * | 0.376 * | 0.147 | 0.108 * | 0.189 | 0.074 | 0.185 | 0.178 | ||||||||

| C2 | 1.000 | 0.114 | 0.591 * | 0.204 | 0.406 * | 0.184 | 0.246 | 0.119 | 0.616 * | 0.110 | 0.330 * | |||||||||

| C3 | 1.000 | 0.005 | 0.293 | 0.147 | 0.212 | 0.316 * | 0.064 | -0.010 | 0.355 | 0.345 * | ||||||||||

| C4 | 1.000 | 0.118 | 0.258 * | 0.191 | 0.122 | 0.169 | 0.473 * | 0.089 | 0.321 * | |||||||||||

| D1 | 1.000 | 0.426 * | 0.260 * | 0.210 * | 0.261 * | 0.077 | 0.164 | 0.266 * | ||||||||||||

| D2 | 1.000 | 0.256 * | 0.434 * | 0.321 * | 0.271 * | 0.097 | 0.313 * | |||||||||||||

| D3 | 1.000 | 0.213 * | 0.613 * | 0.131 | 0.570 | 0.209 * | ||||||||||||||

| D4 | 1.000 | 0.200 | 0.232 * | 0.151 | 0.192 | |||||||||||||||

| E1 | 1.000 | 0.102 | 0.406 * | 0.132 | ||||||||||||||||

| E2 | 1.000 | 0.136 | 0.329 | |||||||||||||||||

| E3 | 1.000 | 0.374 * | ||||||||||||||||||

| E4 | 1.000 | |||||||||||||||||||

| Overall Measure of Sample Adequacy (KMO): 0.846; Barlett Test of Sphericity: 4396.46 (Significance: 0.000). | ||||||||||||||||||||

| Factor | Initial Eigenvalues | Extraction Sums of Squared Loadings | ||||

|---|---|---|---|---|---|---|

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

| 1 | 7.451 | 37.255 | 37.255 | 7.451 | 37.255 | 37.255 |

| 2 | 2.548 | 12.741 | 49.996 | 2.548 | 12.741 | 49.996 |

| 3 | 2.315 | 11.574 | 61.569 | 2.15 | 11.574 | 61.569 |

| 4 | 1.315 | 6.573 | 68.142 | 1.315 | 6.573 | 68.142 |

| 5 | 1.186 | 5.931 | 74.073 | 1.186 | 5.931 | 7.073 |

| 6 | 0.969 | 4.847 | 78.921 | |||

| 7 | 0.945 | 4.724 | 83.644 | |||

| 8 | 0.607 | 3.033 | 86.677 | |||

| 9 | 0.540 | 2.702 | 89.379 | |||

| 10 | 0.497 | 2.486 | 91.865 | |||

| 11 | 0.396 | 1.982 | 93.847 | |||

| 12 | 0.351 | 1.753 | 95.601 | |||

| 13 | 0.286 | 1.431 | 97.032 | |||

| 14 | 0.259 | 1.295 | 98.327 | |||

| 15 | 0.163 | 0.813 | 99.140 | |||

| 16 | 0.070 | 0.351 | 99.491 | |||

| 17 | 0.042 | 0.211 | 99.702 | |||

| 18 | 0.031 | 0.153 | 99.855 | |||

| 19 | 0.023 | 0.115 | 99.970 | |||

| 20 | 0.006 | 0.030 | 100.000 | |||

| Factor | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | Communality | |

| A1 | 0.951 | 0.984 | ||||

| A2 | 0.956 | 0.984 | ||||

| A3 | 0.941 | 0.966 | ||||

| A4 | 0.946 | 0.970 | ||||

| B1 | 0.915 | 0.914 | ||||

| B2 | 0.939 | 0.954 | ||||

| B3 | 0.898 | 0.870 | ||||

| B4 | 0.942 | 0.948 | ||||

| C1 | 0.817 | 0.737 | ||||

| C2 | 0.839 | 0.777 | ||||

| C4 | 0.792 | 0.672 | ||||

| D1 | 0.713 | 0.641 | ||||

| D2 | 0.642 | 0.736 | ||||

| D4 | 0.821 | 0.775 | ||||

| E1 | 0.440 | 0.544 | ||||

| E2 | 0.814 | 0.721 | ||||

| E4 | 0.494 | 0.585 | ||||

| Total | ||||||

| Eigenvalue | 6.595 | 2.328 | 2.231 | 1.261 | 0.964 | 13.379 |

| % of Variance | 38.793 | 13.695 | 13.126 | 7.418 | 5.669 | 78.701 |

| Chronbach’s Alpha (17 items): 0.767 ANOVA test (17 items): 560.241 (df.: 16; Significance: 0.000) | ||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Felber, C.; Campos, V.; Sanchis, J.R. The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials? Sustainability 2019, 11, 3791. https://doi.org/10.3390/su11143791

Felber C, Campos V, Sanchis JR. The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials? Sustainability. 2019; 11(14):3791. https://doi.org/10.3390/su11143791

Chicago/Turabian StyleFelber, Christian, Vanessa Campos, and Joan R. Sanchis. 2019. "The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials?" Sustainability 11, no. 14: 3791. https://doi.org/10.3390/su11143791

APA StyleFelber, C., Campos, V., & Sanchis, J. R. (2019). The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials? Sustainability, 11(14), 3791. https://doi.org/10.3390/su11143791