1. Introduction

This study aims to identify the key decision-making factors of foreign investors in investing in Korea Treasury Bonds (KTBs). This is important since foreign investment in the South Korean financial markets have increased substantially since the mid-2000s. In particular, we examine to what degree geopolitical risk plays a role in foreign investors’ decisions with regards to the KTB markets, given the geopolitical specificity of the Korean Peninsula. We also include the recently developed economic policy uncertainty index as a risk variable in the model to investigate the impact of economic policy uncertainties on KTB investments by foreign investors. The inclusion of geopolitical risk factors and economic policy uncertainty amongst the determinants of foreign investors’ decision to invest in South Korean financial markets is one of the contributions of this paper. The risk factors are especially important in the context of South Korea since geopolitical tensions and policy uncertainty could adversely affect all investment decisions by foreigners.

This research has important implications for both investors and issuers not only in terms of financial market investments but also in terms of the social aspects of sustainability in Korea.

(1) For domestic investors, following the expansion of the retirement pension scheme and the introduction of risk-based capital (RBC) requirements, non-bank financial institutions including pension funds and insurance companies are increasingly investing in KTBs. In fact, nearly 50% of total KTB issuance is held by Korea’s insurance company and pension fund as of the end of 2018. If foreign investors are very sensitive to risk factors, their actions could destabilize the KTB market and negatively affect the economic sustainability of Korea’s pension fund and insurance sector with social sustainability consequences.

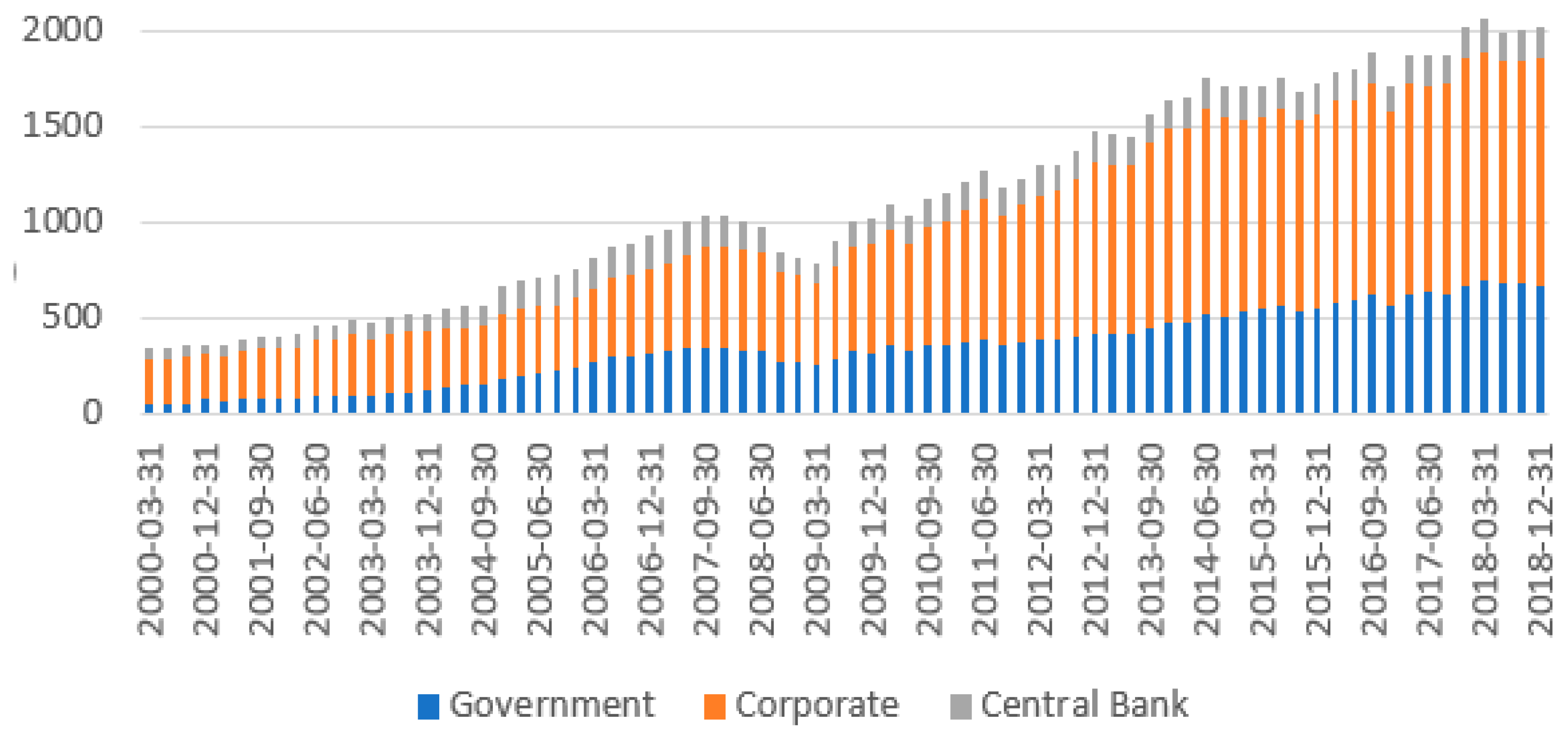

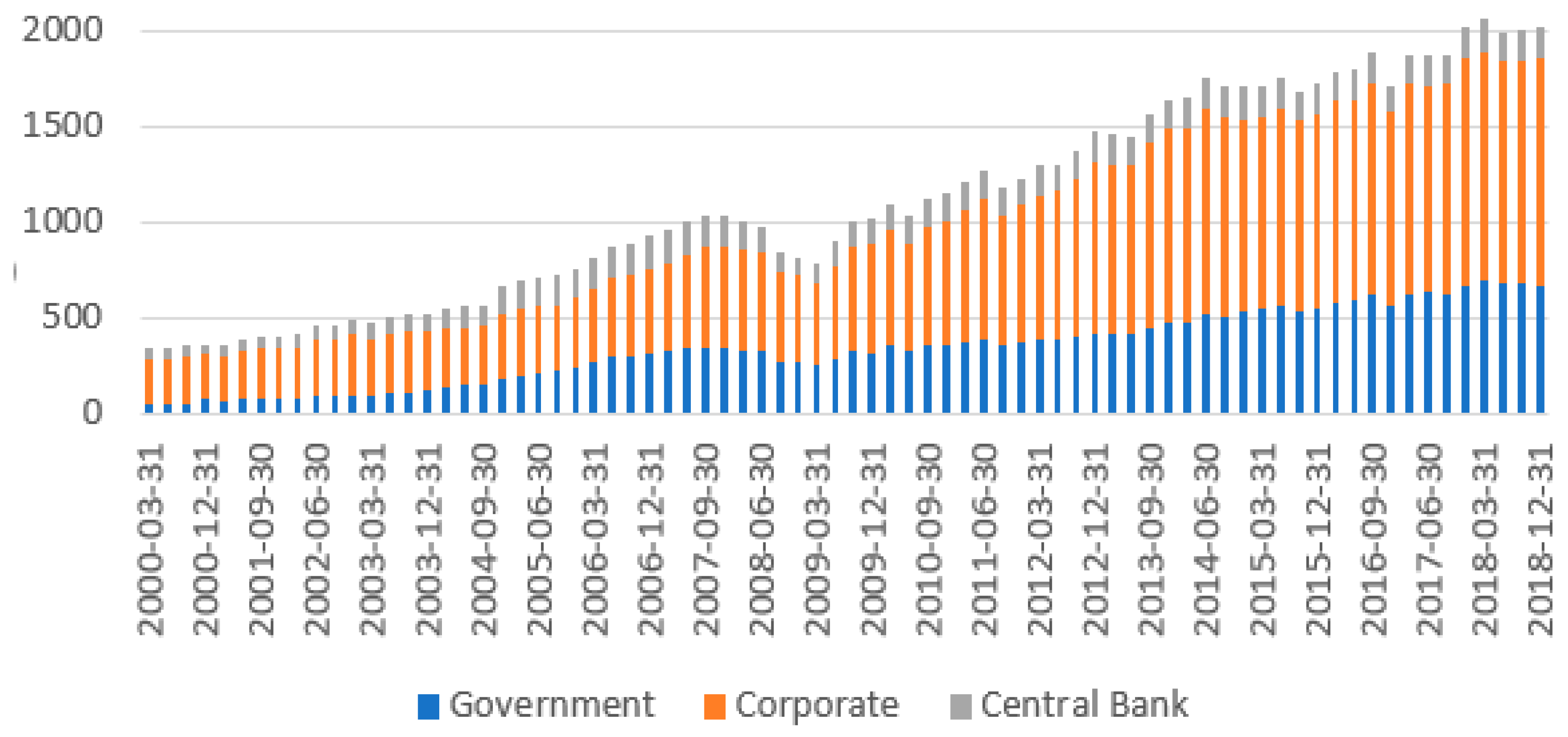

(2) In the case of the South Korean government, which is required to issue KTBs continuously, it is important to secure quality foreign investors to cover national revenue shortfalls and national budget financing. As shown in

Figure 1, the issuance of KTBs has increased significantly, and the increase is expected to continue in the future.

McKenzie [

2] states social sustainability occurs when formal and informal processes, systems, structures, and relationships actively support the ability of current and future generations to form a healthy and livable communities. Also, he argues that a socially sustainable community is equitable, diverse, connected, and democratic, and provide a good quality of life. The need for social sustainability began in developed countries and gradually expanded to emerging economies and developing countries [

3,

4].

In South Korea, the stability of the KTB market is an important pillar supporting the current government’s goal of a ‘people-centered economy’ to overcome structural problems in the economy, such as economic inequality (negative polarization) and low growth. In fact, the South Korean government’s budget for fiscal 2019 reached a record high of KRW 469.6 trillion (US

$ 421.2 billion). This is an increase of 9.6 percent from 2018 and 32.1 percent from 2014 [

5]. Specifically, there have been a major increase in various areas, including health, welfare, employment, education, and the environment. Revenue raised by the government via KTBs are used to finance these projects. Indeed, foreign investors’ holdings of government bonds continue to increase, and their market influence grows, it is difficult to raise government funds through the successful issuance of KTBs without stable foreign investment. It is therefore important that government decision-makers have a deep understanding of the investment patterns and decisions of foreign investors. It is also important to actively understand and manage the government bond market in order to avoid foreigners’ deviation from the government bond market due to investment impediments in the context of a sustainable society. With these points in mind, this study examines the determinants of foreigners’ KTB holdings in a model of portfolio choice involving domestic and international factors and augmented by risk factors and economic policy uncertainty.

On the methodological side, we employ modern time series analysis techniques in this study. In particular, we use the lag-augmented vector autoregressive model with exogenous variables (LA-VARX). The LA-VAR allows us to use variables with possibly different orders of integration in a vector autoregressive (VAR) model and prevents the loss of information due to potential over-differencing. The geopolitical risk variable is included as an exogenous variable in the model since the geopolitical risk in the Korean Peninsula is assumed not to be affected by the models’ variables, while geopolitical risk might affect the variables included in the model.

Since the late 1990s, global financial market integration has rapidly increased [

6], and recently, low interest rates and quantitative easing policies in developed countries have provided the international financial markets with ample liquidity, allowing investors to act more aggressively and diversely [

7]. In fact, global portfolio funds have become more interested in emerging markets and have started investing not only in emerging market equities but also in emerging market bonds. After the financial crisis of the late 1990s, emerging economies, which previously lacked financial infrastructure, have recognized the importance of the local currency bond market to secure a stable inflow of funds, and made great efforts to secure quality investors [

8]. Raising more local currency funds from international investors also reduces the currency mismatch between assets and liabilities in emerging countries, which helps stabilize their financial markets by improving the maturity structure of their debt and increasing the efficiency of capital allocation by creating appropriate long-term interest rate markets [

9]. In 2008, local bond markets in emerging countries experienced a massive capital outflow as the global financial crisis heightened. However, investors quickly regained confidence in emerging economies due to their relatively strong growth performance, worldwide monetary easing, and fiscal stimulus.

As shown in

Table 1, South Korea’s bond market holds a significant edge over other major emerging economies in terms of market structural factors such as market size, liquidity, and stability of international credit ratings, and is more competitive than some advanced economies. South Korea is the world’s fourth-largest local currency bond market after Japan, China, and Canada with an outstanding balance of US

$ 2014 billion as of the end of 2018. Its liquidity is the highest in the world with an average of 0.5 basis points (bps) of the bid–ask spread for on-the-run [

10,

11], and its derivatives markets for risk-hedging are also well-developed compared to other emerging countries. The average time to maturity of Korean government bonds is 10.03 years, which is much longer than that of major countries—such as Japan, France, Canada and Germany—and South Korea’s sovereign credit rating is Aa2 (stable) by Moody’s and AA by S&P, which is higher than that of other emerging economies as of the end of 2018. In addition, South Korea ranked fifth in the world with the World Bank’s Doing Business 2019 score of 84.14, which is higher than the OECD high-income countries’ average of 77.81 [

12].

According to the Ministry of Economy and Finance (MoEF) and Financial Supervisory Service (FSS) in South Korea, the share of foreign investors’ holding of Korean domestic bonds have increased significantly from 0.6% (US

$ 4.9 billion) in 2006, to 6.6% (US

$ 101.8 billion) in 2018—see

Figure S1. As of the end of 2018, the ratio of foreign investment in the Korea Treasury Bonds including Monetary Stabilization Bonds was 15.2 % (US

$ 100.8 billion) of the total amount issued. Also, global investors’ investment in Korea’s bond market has improved greatly in terms of diversify. While foreign central banks and foreign public wealth management companies have increased their investment in long-term bonds, the proportion of global commercial banks and foreign assets management firms seeking short-term gains has decreased, and the number of investment countries increased and diversified from 19 countries in 2006 to 47 countries in 2018 [

13].

However, increased volatility in the financial markets and the growing impact of global investors in emerging financial markets have led to the need for more active risk management for both policymakers and investors. According to the IMF’s World Economic Outlook for 2019, global expansion has weakened. The global growth forecast for 2019 and 2020 was revised downward at 3.3 percent in 2019 and 3.6 percent in 2020, which is 0.4 and 0.1 percentage below last October’s projections, partly because of the negative effects of tariff increases enacted in the U.S. and China. Also, uncertainty over Brexit is a downside risk to the outlook for the European Union [

18,

19].

For emerging markets that are more sensitive to market volatility [

19], it is important to understand the trends and decision-making factors of global investors in order to proactively respond to these potential risks. Recent indicators regarding South Korea show that the economy grew at a slower pace in the first quarter of 2019 [

20]. Industrial output fell in January and February 2019, with growth in manufacturing and construction falling in contrast to the growth posted in the fourth quarter of 2018. Exports in the first quarter of 2019 also marked the first annual decline in more than two years, and trade surplus also shrank. In addition, volatility in the financial markets has increased significantly in recent months.

Most previous studies on foreign investors’ investment in the Korean financial market have attempted to identify patterns of foreign investment in South Korea by arbitrarily setting some financial and economic variables and associating investment returns with specific variables. This study aims to contribute to the literature by augmenting the conventional international portfolio investment decision models by utilizing the recently developed economic policy uncertainty index and geopolitical risk index, considering that foreign investment can be affected by risk factors. In particular, although Korea’s geopolitical instability is relatively large, the study contributes to providing new implications because it has never considered geopolitical risk factors in previous studies on Korean bond investment.

This analysis provides further insight and implications for government decision-makers who want to manage the financial market reliably and to investors seeking stable returns and links our research with social dimensions of sustainability.

The remainder of the paper is organized as follows:

Section 2 provides a review of the literature.

Section 3 presents the data,

Section 4 reports the analysis results, and

Section 5 concludes.

2. Literature Review

The continued development of information and communication technology and financial markets have created an environment that allows investors to invest not only in their home countries but also in various regions, including emerging markets. In terms of global portfolio investment behavior, research on portfolios that mix stocks and bonds is common, and more recently, studies on the diversification of investment portfolios are being actively conducted. Hansson et al. [

21] reported that diversified investment effects are more pronounced when emerging market bonds are incorporated into portfolios composed of developed government bonds and that this could help increase profitability. There are also papers that have studied global investors’ investment diversification from a risk perspective. Solnik and McLeavey [

22] classified the risks of foreign bond investments as credit risk, market risk, and foreign exchange risk. After this classification, many studies analyzing determinants of bond investment by global investors have found that arbitrage opportunities based on interest rate parity theory [

23,

24], as well as credit default swap (CDS) spreads [

25], global liquidity [

26], and foreign exchange rates [

27] are important variables.

In this section, we provide a detailed review of the existing literature in two parts. First, we examine previous studies on the determinant of Korean bond investments by foreign investors. Next, we focus our review particularly on the variables that will be employed in our empirical analyses.

With the expansion of the bond market and the changing patterns of foreign investors’ investment in KTBs, related research topics have also changed. Since global investors rarely invested in Korean bonds before 2007, most studies focused on finding reasons as to why global investors’ investments in Korean local bonds were sluggish. However, since 2007, foreign investors’ investments in Korean bonds have started to increase significantly, and the direction of the research has focused on identifying the main causes of global investors’ investment in Korean bonds. Specifically, Won and Cho [

28] argued that the foreign investors’ investment in Korean domestic bonds is highly dependent on the expected return on risk-free arbitrage transactions and to the country’s credit risk. Kim and Lee [

29] reported that swap spreads, credit risk, and global liquidity risks play an important role in foreign investors’ investment in Korean local bonds. Yoon and Kim [

30] found that market volatility and global liquidity have a significant impact on the inflow of investments into the Korean bond markets, but also that economic growth and interest rate does not have a significant effect. Park et al. [

31] analyzed that foreign investors’ decision to invest in bonds was strongly influenced by arbitrage trading opportunities before the global financial crisis but was more affected by the stock market movements after the global financial crisis. On the other hand, Kim et al. [

32] argued that the determinants of Korean bond investment were the effective interest rates in South Korea, in addition to industrial production, interest rates, and volatility in developed countries.

Various studies were conducted to analyze the impact of each element of the financial markets on cross-border investment. With regards to the exchange rate, most studies showed that an increase in exchange rate volatility has a negative effect on cross-border stocks and bond investment, and that the stock market, bond market, and foreign exchange markets have a close correlation with each other [

33,

34]. On the other hand, Kim [

35] argued that unstable exchange rates reduce investment in the stock market but does not affect the bond market significantly.

Credit default swap (CDS) is widely used as the index of credit risk [

36,

37]. Many researchers have developed CDS pricing models, including Duffie [

38]; Hull and White [

39]; Houweling and Vorst [

40]. Duffie argued that the CDS premium and corporate bond spread should be the same due to arbitrage trading called Duffie’s parity. Collin-Dufresne and Goldstein [

41] reported that the interdependence between the CDS and the stock market is relatively higher than the correlation between the bond market and the stock market.

With regards to studies that analyzed stocks and bonds, most studies on diversification of risks in government bond investments showed that there was a reverse correlation between the bond markets and the stock markets, suggesting that bonds could be a hedging instrument for capital risk [

42,

43,

44,

45].

The central bank’s interest rate adjustment, especially the Federal Reserve’s decision on policy interest rates, is a major variable that affects the global bond and stock markets. Several studies have shown that interest rate policy has a large impact on liquidity [

46,

47], and others have analyzed the transmission path and effect of interest rate policy [

48,

49]. Park and Kim [

50] argued that the policy rate adjustment of the Fed after the financial crisis had a significant impact on the price of Korean government bonds, and Lee [

51] reported a negative relationship between changes in the Fed policy rate and the return of Korean stocks.

Many previous studies have shown that oil prices have a significant impact on macroeconomic and financial markets. Most studies have shown that rising oil prices have a negative impact on the economy, but Hooker [

52] concluded that oil prices have not had a statistically significant impact on the U.S. economy since 1973, and that previous literature on oil prices is exaggerated. Shigeki [

53] used the vector autoregression (VAR) model in Brazil, China, India, and Russia to investigate the relationship between oil prices and stock returns and found a positive relationship between oil prices and real stock returns in all but Brazil. In addition, Çevik et al. [

54] employed time-varying Granger-causality tests and detected Granger-causal relationships between oil prices and emerging market stock returns and volatility around the global financial crisis period.

The TED spread is the difference between the three-month U.S. Treasury bill and the three-month US

$ London Interbank Offer Rate (LIBOR). TED spread is used as an indicator of credit risk. This is because the U.S. Treasury bill is a risk-free asset and the US

$ LIBOR includes bank credit risk when borrowing money from international banks. Widening of the TED spreads is considered to be an increase in the default risk of interbank lending. For example, after the collapse of Lehman Brothers in 2008, the TED spread was the highest at 450 basis points. Coffey et al. [

55] defined the TED spread as the shadow price of capital and concluded that the TED spread is an important variable explaining the arbitrage margin. Kawaller [

56] argued that if the TED spread narrows, stocks and bond prices will rise and provide information that predicts future interest rates.

Changes in basis swap spread have a large impact on cross-border investment. This is the main reason that global investors have significantly increased investment in KTBs in the mid and late 2000s. Existing research has traditionally focused on deviations of cross-currency basis swaps from covered interest rate parity [

57,

58]. Miron and Swannell [

59] argued that basis can be temporarily out of range due to capital market uncertainties but will thereafter recover to some extent due to risk-free arbitrage trading in the market, and that basis is the phenomenon caused by an imbalance in supply and demand due to lack of liquidity in the market. Additionally, they explained that the reason that the theory of interest rate parity theory is not well-applied in the forward market is due to government regulations on international capital movements, foreign exchange control, taxes, and transaction costs

Many studies have found that sovereign bond spreads are determined by country specific factors and global risk factors [

60,

61]. In the case of emerging economies, there has been previous research showing that bond spreads increased excessively when the global economy becomes unstable [

62]. It was confirmed that the short-term and long-term interest rates reversed when the US recession occurred. At present, the slope of the yield curve has become one of the most important indicators of economic outlook [

63]. Estrella and Mishkin [

64] calculated the likelihood that the U.S. economy would enter a recession due to short- and long-term interest rate differentials. Mehl [

65] obtained positive results using short-term and long-term U.S. interest rate differentials to test economic forecasts for emerging economies.

An increase in volatility lowers the stability and efficiency of the financial markets and financial institutions, weakens the effectiveness of monetary policy, and shrinks real economic activity such as consumption, investment, and exports. Lee and Lee [

66] estimated that the volatility spillover effect from the CDS market to the asset market is evident and has a stronger spillover effect during and after the financial crisis. Antonakakis and Badinger [

67] found an important correlation between economic growth and volatility.

In addition, macroeconomic and fiscal soundness of the country also have an impact on cross-border investment, and several studies have been conducted. Early financial research was led by the arbitrage pricing theory [

68], and there have been many studies examining the impact of macroeconomic indicators on the bond and stock markets. Bjornland and Leitemo [

69] found that interdependence between interest rates and stock returns was high based on research using the CPI, the Industrial Production index, the US policy rate and the commodity price index. Mahmood and Dinniah [

70] looked at the relationship between the CPI, industrial production indexes, FX rates, and stock prices and found that there is a long-term relationship between macroeconomic factors and stock prices. Ang and Piazzesi [

71] and Diebold et al. [

72] argued that economic growth and inflation have a positive impact on bond risk premiums. Kim and Lee [

73] concluded that the monetary policy decision process is mainly affected by the CPI, short-term and long-term interest rates, the industrial production index, and the stock price index.

A country’s credit rating is an important determinant of cross border investment. A country’s credit rating has been shown to affect the cost that rated countries face when borrowing [

74], the amount of foreign direct investments and bank inflows [

75], and the amount of development in their financial sector and the domestic stock market [

76]. Reisen and Maltzan [

77] concluded that the ratings of international rating agencies had a significant impact on emerging bond markets.

A country’s fiscal soundness is an important metric for cross border investment, and there have been many debates between fiscal deficits, government debt, and economic growth. According to the traditional view, high deficit financing and public debt can increase long-term interest rates [

78], increase taxation and inflation [

79], and increase uncertainty in the economic outlook, eventually leading to a negative impact on economic growth [

80,

81]. In addition, these adverse effects can cause financial crises in extreme cases [

82]. On the other hand, it is widely accepted that higher capitalization can be achieved if capital constraints are placed on resource constraints, such as underdeveloped countries, if capital is used for productive investment. However, many theories point out that debt can have a negative impact on growth above a certain level [

83,

84]. Capital inflows from foreign countries may be positive for economic growth, but this can lead to macroeconomic imbalances such as excessive expansion of aggregate demand, overheating of the economy, inflation, real exchange rate overvaluation, and current account deterioration. Also, the rapid outflow of capital may lead to an economic crisis [

85]. Therefore, from the viewpoint of foreign investors, foreign exchange reserves can be an indicator of safety in the country that they are investing in. Foreign exchange reserves of emerging economies have been reported to significantly increase after the Asian financial crisis to prevent another crisis [

86]. Aizenman and Marion [

87] found that countries with a high level of foreign exchange reserves and stable exchange rates could reduce production losses in times of crisis.

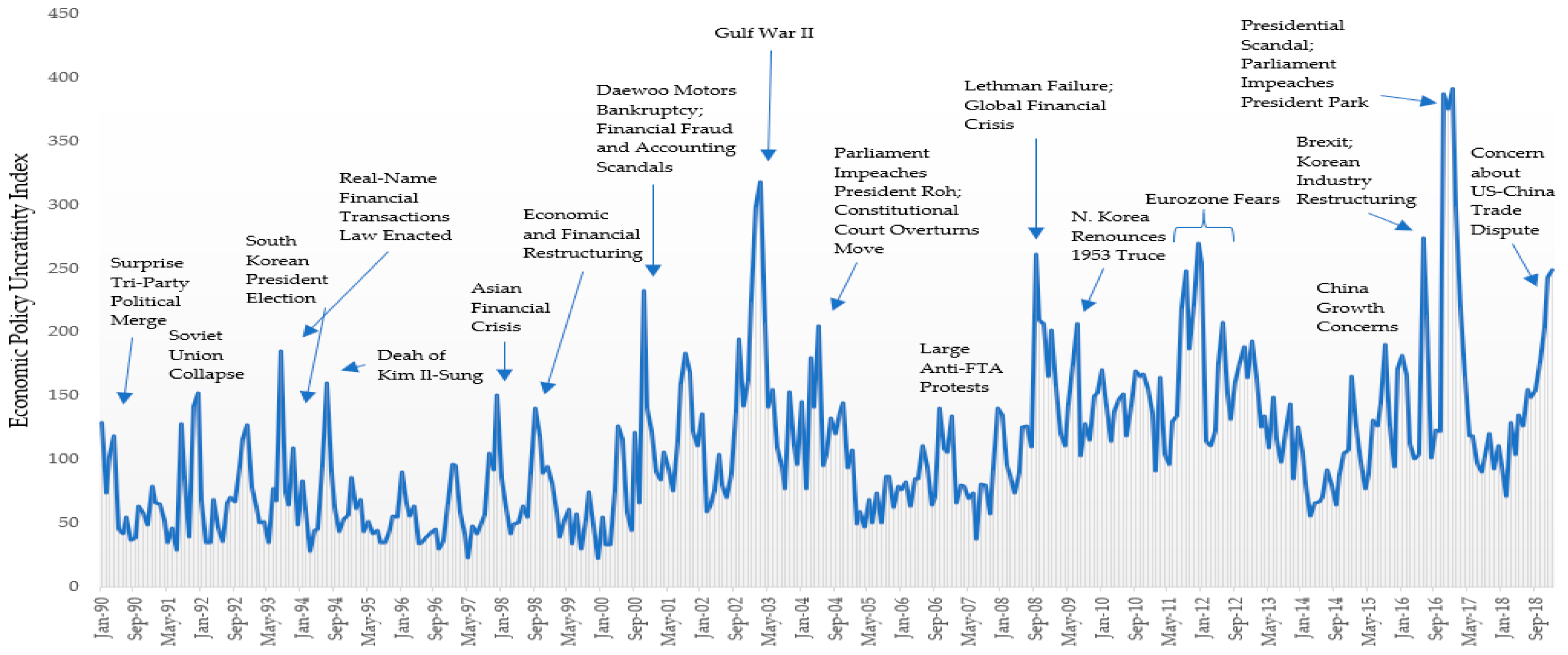

Political, geopolitical, and regulatory issues are also factor that influence investment. However, not many studies have been done in the past because these factors are difficult to quantify and analyze their effects. However, there have been attempts to measure the effect of political events through various phenomena observed in financial markets. The relationship between economic performance and the political business cycle was first analyzed by Nordhaus [

88]. Since then, Huang [

89] found a correlation between presidential elections and economic cycles. Le Vu and Zak [

90] argued that economic risk, political instability, and policy volatility are positively correlated with capital outflows, and that the most important variable is political instability. Bilson et al. [

91] found that the average returns in countries with reduced political risks in emerging markets are about 11% higher than those in risky countries. Geopolitical uncertainty in the Korean peninsula is higher than in any other region due to division and confrontation between the two Koreas. However, there are relatively few studies on the effects of inter-Korean relations on the financial markets. Some studies analyzed the effect of inter-Korean relations news on the stock index, focusing on the correlation between inter-Korean relations and stock market and concluded that foreign investors generally did not respond sensitively to inter-Korean news [

92,

93,

94].

Another important factor influencing economic and investment decisions is the uncertainty of the government’s economic policies [

95]. Pastor and Veronesi [

96,

97] argued that there is a strong correlation between US economic policy uncertainty and stock volatility. Bloom [

98] and Basu [

99] found that uncertainties in economic policies and regulations are considered major risk factors and can significantly affect future corporate profits. Barth et al. [

100] argued that the government should intervene in the market in order to improve the asymmetry among trading participants and to pursue financial market stability. However, they also stated that, if the regulation is too excessive, economic efficiency will be lowered due to the restriction of capital mobility. Jomini [

101] argued that the government should consider the benefits and costs of regulation in advance.

Cheng et al [

102] found that if investors question the fairness and frequent changes in tax laws, it could adversely affect investors’ investment decisions. In the past, investors have been confused by the Korean government’s repeated reform of the withholding tax system for foreign investors.

Inefficiency in the financial market are mainly caused by problems in the structure of the market, and market transparency and liquidity are considered to be representative measures in measuring the efficiency of market structure [

103]. The level of market transparency affects not only proper price discovery but also market reliability and investor protection. Market transparency is also known to be related to market liquidity. Market liquidity can be measured not only by transaction size, but also by transaction cost, price continuity, and market impact [

104]. Bloomfield and O’Hara [

105] argued that improving bond market transparency positively contributes to market liquidity.

Several studies have analyzed the protection of property rights as an important factor when foreign investors make investment decisions. Investing in a country with a lower level of protection of property rights would require an additional risk premium on the possibility of default, and foreign investors would avoid investing in the country’s bonds. La Porta et al. [

106] found a positive correlation between the degree of protection of property rights and the stock market. He used three indicators to measure this: the corruption index, the private property forfeiture index, and the contract denial index. Bae et al. [

107] used IMF’s Coordinated Portfolio Investment Survey (CPIS) results to analyze foreign bond investment determinants, and they found that the degree of protection of property rights was the most important factor in determining the retention of domestic bonds by foreigners, while macroeconomic variables such as inflation, interest rates, and gross domestic product did not have a significant impact on foreign bond investment.

5. Conclusions

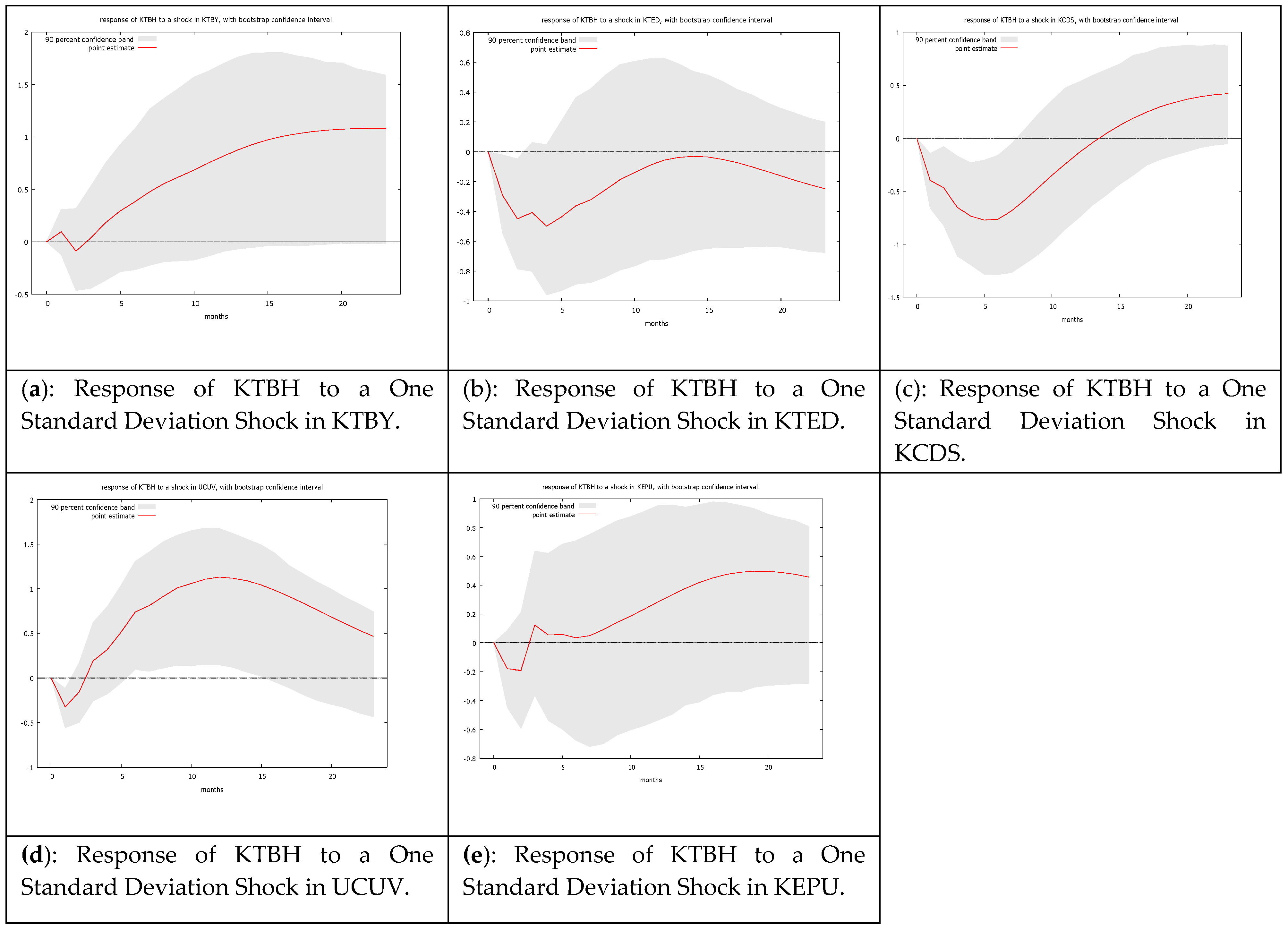

Using the lag-augmented vector autoregressive model with exogenous variables (LA-VARX), this study analyzes the determinants of foreign investors’ investment in Korea Treasury bonds (KTBs). The LA-VARX model consists of the KTB yields (return of KTB investment), KTB TED CCIRS (benchmark spread of risk-free arbitrage), and Korea’s sovereign CDS (benchmark spread for country risk). These three variables stand as proxies for the domestic factors affecting the KTB investment decisions of foreign investors. The slope of the U.S. Treasury bond short-term and long-term yield curves is taken as a proxy for international factor the portfolio allocation decisions for foreign investors. These domestic and international variables were chosen through literature review and are in line with international finance theory and practice. As a novelty in this paper, we included the Korean economic policy uncertainty index and the geopolitical risk index as risk factors into the model and examined the effects of these risk variables on the KTB market actions of foreign investors.

The main implications of this study are that foreign investors’ investments in KTBs are affected by government bond yields, as well as opportunities for arbitrage transactions, country’s default risk, and global economic conditions. Specifically, we found that foreigners’ decision to invest in government bonds are influenced more heavily by domestic factors than international or risk factors, and among domestic factors, foreign investors responded negatively in the short term to a reduction in arbitrage transaction opportunities and increased sovereign default risks.

With regards to geopolitical risks and economic uncertainties noted in this study, foreign investors’ KTB investments are affected by domestic geopolitical risks, but not by economic policy uncertainties. While foreign investors are generally expected to be more sensitive and responsive to geopolitical risks, this actually appears to have only a limited short-term effect on government bond investments. This study provides some evidence that the KTB market has its own dynamics and is somewhat resistant to economic policy uncertainty or geopolitical risks over the long term.

As discussed in the introduction, the KTB provides a sustainable source of funds by allowing the government to borrow local currency that can be used for social and infrastructure projects from the international market, rather than being subject to foreign exchange risks. In this study, we found that having more foreign investors with long-term investment tendencies is important in a sustainable social context. Because foreign investors with short-term investment tendencies are much more sensitive to short-term expected yields and hedge costs, which can destabilize the market, and this market instability can prevent the government from securing sustainable resources. The Korean government needs to keep the fundamentals of the economy stable and promote the advantages of the Korean bond market more actively to foreign investors who make long-term investments.

The limitations of this study are that data at the investor-level are needed since the actions of investors may vary depending on their investment goals and risk appetite and tolerance, but lack of data prevented an investor-specific analysis. Future research is expected to expand the scope of research to various types of bonds in developed and emerging economies and to provide a comparative analysis of investors’ investment decision factors that considers each financial market situation. In addition, a variety of methodological approaches to this topic are expected to yield more substantial research results and contribute to the literature more broadly. Based on this view, we plan to conduct further research using various methodologies with bond market experts who decide, oversee, and manage bond portfolio investments.

{kind=link}

{kind=link}

{kind=link}