2.1. Defining SMEs in Africa

The definition of SMEs varies across Africa and a few African countries were randomly selected and discussed herein. Firstly, in Tanzania SMEs were found in three different categories. The definition utilises the two quantitative criteria, namely, the number of employees and capital invested in differentiating SMEs. The first category of SMEs in the Tanzanian context constitute of micro-enterprises which employ up to five employees. As for the capital invested, micro enterprises need to have 5 million Tanzanian shillings (TZS) invested in machinery. Secondly, small enterprises should have five to 50 employees and TZS 5 to 2000 million. Finally, medium-sized enterprises ought to have 50 to 100 employees and TZS of 200 to 800 million [

11].

In Ghana, various definitions have been propounded with regards to small-scale enterprises but the most prominently utilised method is the number of workers in a firm. One of the official sources, the Ghana Statistical Service (GSS) regards enterprises with less than 10 workers as small-scale firms and those with more than 10 workers as medium and large-sized firms [

12]. On the other hand, the National Board for Small Scale Industries (NBSSI) of Ghana utilises a two-pronged approach to define SMEs. The NBSSI utilises fixed assets and the number of workers in its definition. Accordingly, the NBSSI defines a small-scale firm as a business with less than nine employees, and has plant and machinery (disregarding land, buildings and vehicles) that are below 10 million Ghanaian cedes [

12].

However, the continuous depreciation of the local currency has been regarded as posing definitional challenges when the value of assets is utilised. As such, Asamoah [

5] argues that the most used definition is the one given by the EU which utilises the headcount of employees and turnover. In this regards, the US dollar (US

$) is used instead of the Ghanaian cedes. Based on this criterion, a small-scale firm is defined as employing more than five workers and not exceeding 50 workers. The value of assets, disregarding land, building and working capital-should be less than

$US 30,000 and the annual income turnover should be between

$US 6000 and

$US 30,000. On the other hand, a medium-sized firm is deemed to be a business employing between 50 and 100 employees.

In Nigeria, still, the definition of SMEs differs. According to Apulu, Latha and Moreton [

13], the Small and Medium Sized Development Agency of Nigeria (SMEDAN) categorises SMEs into micro, small and medium sized enterprises. SMEDAN states that a micro firm is an enterprise constituting fewer than ten employees with an annual turnover that is less than five million Naira. Furthermore, SMEDAN details that a small firm is a business employing 10–49 workers with an annual turnover ranging between five to 49 million Naira. Finally, the SMEDAN regards an enterprise as a medium firm if it employees between 50–199 workers whilst the annual turnover of 50–499 million Naira.

In South Africa, the Department of Trade and Industry [

14], defines small medium micro enterprise (SMMEs) in South Africa as any business that is having less than two hundred employees or no more than five hundred employees, and the annual turnover of less than five million rands, capital assets or equipment of less than two million rands and the owner is directly committed to management of the business. As such, in this study, both the quantitative and qualitative criteria are utilised from the South African perspective. This definition ignores the variances that apply in terms of the variances in industry as outlined in the definition contained in the National Small Business Act of South Africa 1996 as amended in 2003 [

14]. Many of the SMMEs in South Africa eventually take place in rural areas, whereby they operate on small premises and as time goes on they move to large premises that are sustainable for their business [

15].

2.2. Social Sustainability

Social sustainability transpires when prescribed and informal procedures, structures, associations and interactions vigorously enhance the capability of contemporary and upcoming generations to generate healthy and liveable societies. The social dimension or social equity principle under sustainable development relates to all societal members having equal access to the available resources and opportunities [

16]. Thus, social sustainability refers to activities that ensure that communities are impartial, varied, allied and self-governing and deliver a noble value of life. Acute to the delineation of sustainable development is the recognition that “needs” contemporaneous and impending ought to be achieved in an even-handed setting [

17]. Bogt [

18] argues that a firm may regard it socially sensible to imitate other firms, that is, to adopt socially rational behaviours in order to achieve this desired equilibrium.

Social activities focus on the community, sports, health and well-being, education, helping the low-income earners as well as participating in the community [

19]. These activities are regarded as interventions towards the enhancement of social and cultural causes in the societies as well as community development [

19]. SMEs have been considered crucial to the support of community activities in the European as well as Latin American economies. Accordingly, an empirical study by Polášek [

20] established that societal activities such as donations in the form of finance and kind, volunteering, education to the society, assistance towards the societal standards of living (i.e., sports, culture, etc.) as well as partnering with local schools, authorities and different community organisations are vital for SMEs.

On the other hand, Thiel [

21] indicates that there are four themes that define the social domain in a sustainability context, namely, social-economics, stakeholders, societal-wellbeing and social sustainability. Consistently, social sustainability includes definitions of society, community and culture and is measured in the firm’s performance in donations, safety, strategic philanthropy and corporate citizenship [

22]. Thus, social sustainability places a demand upon firms to play an active role and acknowledge more responsibilities toward stakeholders and the social environment they operate in [

23]. Human needs include basic needs such as food, shelter, clothing as well as good quality of life, with quality of life including things like healthcare, education and political freedom [

21]. Overall, social sustainability is measured through principles, actions and measures implemented [

9].

The firm’s appearance in the locality of its operations, the way in which it is regarded as an employer, service provider and accomplice in the local confinements categorically influence its competitive locus [

20]. Moreover, businesses that are held as a socially dynamic stand to experience an enhancement in their repute from the community and business guild. In this instance, this heightens the prospects for businesses to draw capital together with improving their competitive situation [

19]. SMEs are conspicuous in availing social sustenance in the areas of sporting activities in nearly all the nations in Europe. Coherently, in Latin America, SMEs appear to be vastly dynamic in the fields of sporting, healthiness and cultural happenings [

19]. In Africa, among others, SMEs contribute towards social sustainability through employing people with inadequate education and skills levels, women in the lower spectrums of the society. According to Apulu et al. [

13], SMEs support in enhancing the living standards of people through bringing about extensive local capital formation and attaining great levels of productivity and capacity.

2.3. Firm Performance

Firm performance constitutes the second construct in this study. Firm performance is not a new concept in the field of business research [

24]. However, despite its prominence in latent literature, the construct of firm performance is challenged by incongruences pertaining to indicators being selected based on the researcher’s convenience [

25]. Another incongruence noted by Santos and Brito [

25] is that of inadequate consideration of the dimensionality of firm performance. Thus, firm performance means different things to different people. According to Ha-Brookshire [

26] firm performance is a complex concept to define and the complexity of the definition is even more entrenched within the context of SMEs operations. Consistently, Rodríguez-Gutiérrez et al. [

24] argue that a vast difference found in firms is the main reason why the definition of business performance is challenging. Thus, there is a need to consider how firm performance can be assessed within the context of SMEs which have substantive differences contrasted with large businesses [

8].

This study utilises both financial and non-financial measures of ascertaining the impact of social sustainability on SMEs. Financial measures have long proven to be reliable when it comes to ascertaining the outcomes of strategies and decisions by businesses [

27]. However, universal application of financial measures in ascertaining business performance has since been subject to debate with assertions promulgated that financial measures alone are not sufficient to measure the intangible aspects of business such as social sustainability [

28]. For adequacy of measurement, there is a need to augment financial measures with non-financial measures so as to properly depict the outcome of business activities that are undertaken by firms. To this end, the stakeholder approach has been utilised in an endeavour to encapsulate the effects of business activities on different contracts it has with various interested parties. Whilst, financial performance is primarily concerned with the shareholders or owners of the business, there is a need to also ascertain the performance of firms with regards to other interested parties such as customers, employees, society and suppliers [

28,

29]. In this regards, this study focuses on the three primary stakeholder groups, namely, shareholders, customers and employees. As indicated in latent literature [

30], sustainability practices by businesses should be designed in a stakeholder-inclusive manner and respond to numerous demands by different stakeholders. In addition, firms (large and small) need to proactively communicate their sustainability strategies and outcomes so as to enhance their relationships with their respective stakeholder groups [

30].

Consistently, latent research indicators have utilised either economic (profitability and productivity measures) financial or growth indicators [

24]. Furthermore, within the sustainability spectrum, it is argued that there is a need to broaden the matrices utilised to measure firm performance [

8,

25]. On the other hand, Santos and Brito [

25] consider multidimensionality to consist of financial performance and non-financial performance, with the financial performance dimension comprising profitability, growth and market value. Selvarajan, Ramamoorthy, Flood, Guthrie, MacCurtain and Liu [

31] state that return on investment (ROI), earnings per share and net income after tax have often been employed as measures of financial performance. Profitability and growth indices are of high significance in characterising firms between more and less successful ones [

32]. However, the financial measurement of firm performance faces criticism because it is primarily backwards-looking and it also partially predicts the future pertaining to depreciation and amortization [

33]. In this regard, the following hypothesis was postulated:

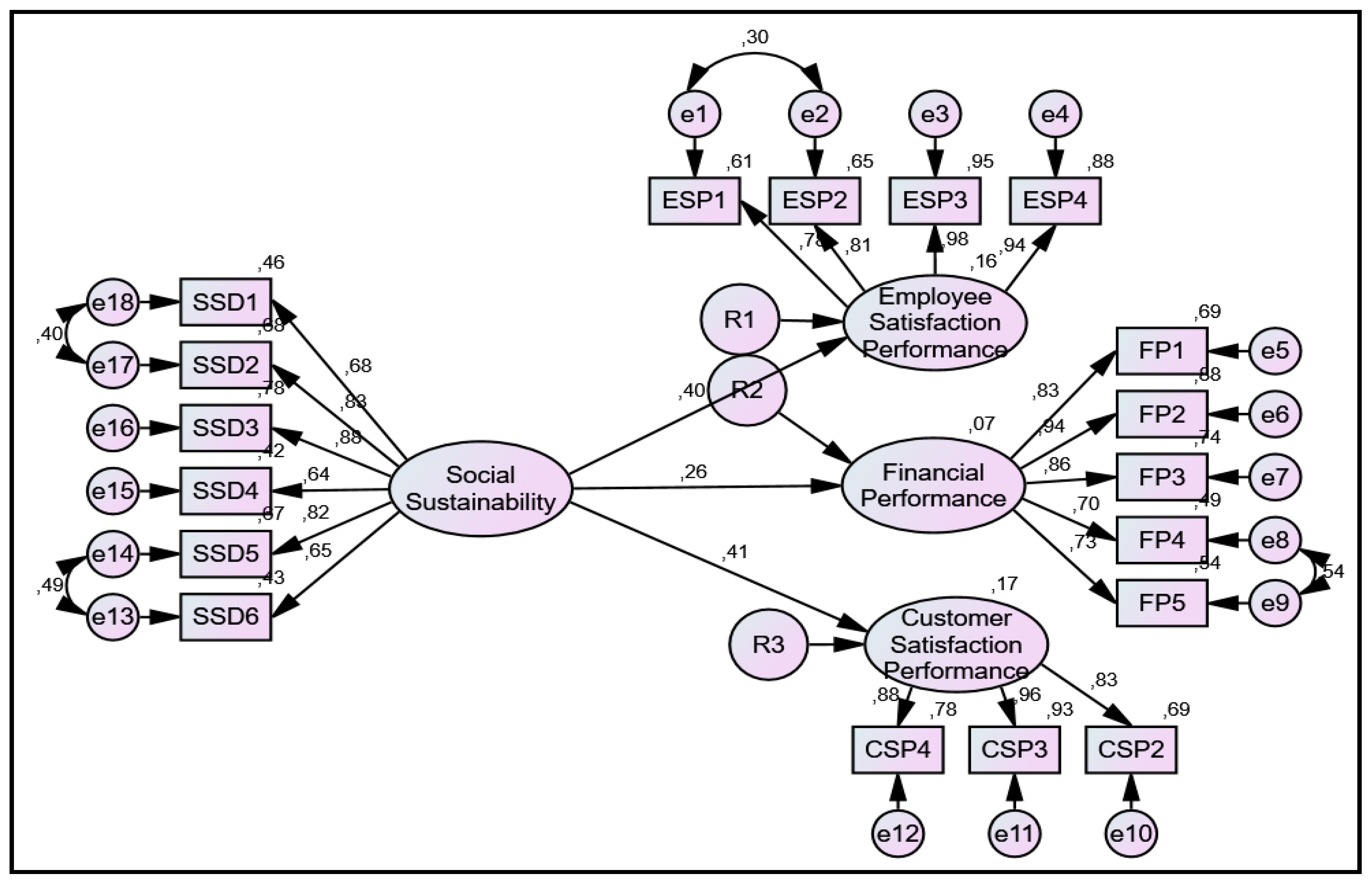

Hypothesis 1 (H1). There is a significant positive link between social sustainability practices (SSD) and financial performance (FFP) of SMEs in Limpopo Province.

Financial measures are ex-post and focus on recognised strategies whilst they disregard the future [

34]. Consistently, the phenomenon of definitional confusion with regards to firm performance emanates from authors utilising antecedents of performance as indicators of performance [

25]. Thus, Sambharya [

34] critiques that financial measures also tend to be internally oriented and assess management, whilst they disregard the stakeholders and external environments. Furthermore, Al-Matari et al. [

33] propound that financial performance is regarded to be insufficient as a firm performance measure because it is subject to the accounting profession standards. Thus, it is constrained by the accounting practice since it is determined by the accountant. Alternatively, non-financial performance dimensions that have been utilised by authors include innovativeness, employee satisfaction, customer satisfaction, entrepreneur satisfaction and competitiveness [

26,

35,

36]. Whereas, Santos and Brito [

25] note that the non-financial dimensions are measured at the hand of competitive issues such as customer satisfaction, quality, innovation, employee satisfaction and reputation. Furthermore, research on sustainable performance, in general, has been observed to be insufficient from the milieus of developing countries, especially from a subjective perspective [

37]. On this background, the following hypotheses were developed in this study.

Hypothesis 2 (H2). There is a significant positive link between social sustainability practices (SSD) and customer satisfaction performance (CFP) of SMEs in Limpopo Province.

Hypothesis 3 (H3). There is a significant and positive link between social sustainability practices (SSD) and employee satisfaction performance (EFP) of SMEs in Limpopo Province.

{kind=link}