The Influence of Innovation on Corporate Sustainability in the International Banking Industry

Abstract

:1. Introduction

2. Innovation Performance That Fosters Corporate Sustainability in the Banking Industry

2.1. The Instrumental Value of Innovation Performance and Corporate Sustainability

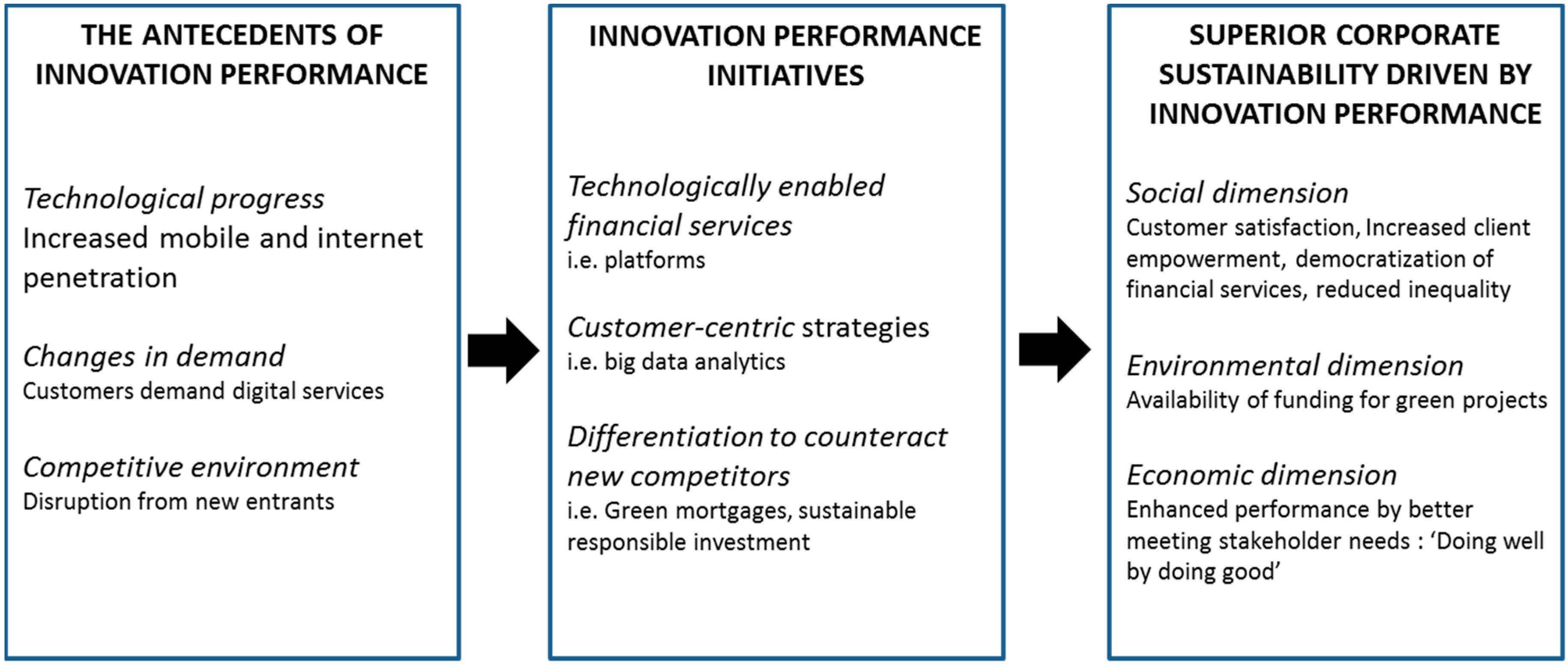

2.2. Antecedents of Innovation Performance in the Banking Industry

2.3. Innovation Performance Initiatives in the Banking Industry

2.4. The Influence of Innovation Performance on Corporate Sustainability in the Banking Industry

2.5. Operationalization of the Hypothesis

3. Methods

3.1. Sample and Variables

3.2. Model Specification

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

| Number of Banks | Observations | |

|---|---|---|

| Australia | 6 | 65 |

| Austria | 2 | 14 |

| Canada | 9 | 79 |

| Denmark | 3 | 15 |

| France | 4 | 26 |

| Germany | 2 | 12 |

| Greece | 4 | 17 |

| Italy | 9 | 78 |

| Norway | 1 | 12 |

| Portugal | 2 | 23 |

| Spain | 5 | 50 |

| Switzerland | 6 | 45 |

| United Kingdom | 6 | 71 |

| United States of America | 109 | 431 |

| Total | 168 | 938 |

References

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Montiel, I. Corporate Social Responsibility and Corporate Sustainability: Separate Pasts, Common Futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Forcadell, F.J.; Aracil, E. European banks’ reputation for corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 1–14. [Google Scholar] [CrossRef]

- Herzig, C.; Moon, J. Discourses on corporate social ir/responsibility in the financial sector. J. Bus. Res. 2013, 66, 1870–1880. [Google Scholar] [CrossRef]

- Ruiz, B.; Esteban, Á.; Gutiérrez, S. Determinants of reputation of leading Spanish financial institutions among their customers in a context of economic crisis. Bus. Res. Quar. 2014, 17, 259–278. [Google Scholar] [CrossRef] [Green Version]

- Edwards, K.L.; Gordon, T.J. Characterization of Innovations Introduced on the US Market in 1982; Futures Group and Ntis: Glastonbury, CT, USA, 1984. [Google Scholar]

- Cook, K.A.; Romi, A.M.; Sánchez, D.; Sánchez, J.M. The influence of corporate social responsibility on investment efficiency and innovation. J. Bus. Financ. Acc. 2016, 46, 494–537. [Google Scholar] [CrossRef]

- Tidd, J.; Hull, F.M. Service innovation: Development, delivery and performance. In The Handbook of Innovation and Services: A Multi-Disciplinary Perspective; Gallouj, F., Djellal, F., Eds.; Edward Elgar Publishing: Heltenham, UK, 2011; pp. 250–278. [Google Scholar]

- Amore, M.D.; Schneider, C.; Žaldokas, A. Credit supply and corporate innovation. J. Financ. Econ. 2013, 109, 835–855. [Google Scholar] [CrossRef]

- Hsu, P.H.; Tian, X.; Xu, Y. Financial development and innovation: Cross-country evidence. J. Financ. Econ. 2014, 112, 116–135. [Google Scholar] [CrossRef] [Green Version]

- Lusch, R.F.; Nambisan, S. Service innovation: A service-dominant logic perspective. MIS Quar. 2015, 39, 155–175. [Google Scholar] [CrossRef]

- Adams, R.; Jeanrenaud, S.; Bessant, J.; Denyer, D.; Overy, P. Sustainability-oriented innovation: A systematic review. Int. J. Manag. Rev. 2016, 18, 180–205. [Google Scholar] [CrossRef]

- Hansen, E.G.; Grosse-Dunker, F.; Reichwald, R. Sustainability innovation cube—A framework to evaluate sustainability-oriented innovations. Int. J. Innov. Manag. 2009, 13, 683–713. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hansen, E.G.; Lüdeke-Freund, F. Business models for sustainability: Origins, present research, and future avenues. Organ. Environ. 2015, 29, 3–10. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business models for sustainability: A co-evolutionary analysis of sustainable entrepreneurship, innovation, and transformation. Organ. Environ. 2016, 29, 264–289. [Google Scholar] [CrossRef]

- Cai, W.G.; Zhou, X.L. On the drivers of eco-innovation: Empirical evidence from China. J. Clean. Prod. 2014, 79, 239–248. [Google Scholar] [CrossRef]

- Cainelli, G.; De Marchi, V.; Grandinetti, R. Does the development of environmental innovation require different resources? Evidence from Spanish manufacturing firms. J. Clean. Prod. 2015, 94, 211–220. [Google Scholar] [CrossRef]

- Del Río, P.; Morán, M.Á.T.; Albinana, F.C. Analysing the determinants of environmental technology investments. A panel-data study of Spanish industrial sectors. J. Clean. Prod. 2011, 19, 1170–1179. [Google Scholar] [CrossRef]

- Lioui, A.; Sharma, Z. Environmental corporate social responsibility and financial performance: Disentangling direct and indirect effects. Ecol. Econ. 2012, 78, 100–111. [Google Scholar] [CrossRef]

- Reif, C.; Rexhauser, S. Good enough! Are socially responsible companies the more successful environmental innovators? In New Developments in Eco-Innovation Research. Sustainability and Innovation; Horbach, J., Reif, C., Eds.; Springer: Augsburg, Germany, 2018; pp. 163–192. [Google Scholar]

- Shen, R.; Tang, Y.; Zhang, Y. Does Firm Innovation Affect Corporate Social Responsibility? Working Paper; Harvard Business School: Cambridge, MA, USA, 2016. [Google Scholar]

- Simpson, G.; Kohers, T. The link between corporate social and financial performance: Evidence from the banking industry. J. Bus. Ethics 2002, 35, 97–109. [Google Scholar] [CrossRef]

- Benfratello, L.; Schiantarelli, F.; Sembenelli, A. Banks and innovation: Microeconometric evidence on Italian firms. J. Financ. Econ. 2008, 90, 197–217. [Google Scholar] [CrossRef] [Green Version]

- Salmador, M.P.; Bueno, E. Strategy-Making as a complex, double-loop process of knowledge creation: Four cases of established banks reinventing the industry by means of the internet. In Strategy Process (Advances in Strategic Management, Volume 22); Gabriel Szulanski, J.P., Doz, Y., Eds.; Emerald: Yorkshire, UK, 2005; pp. 267–318. [Google Scholar]

- Yip, A.W.H.; Bocken, N.M.P. Sustainable business model Archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Baregheh, A.; Rowley, J.; Sambrook, S. Towards a multidisciplinary definition of innovation. Manag. Decis. 2009, 47, 1323–1339. [Google Scholar] [CrossRef]

- Dahlsrud, A. How corporate social responsibility is defined: An analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Park, E.; Kim, K.J.; Kwon, S.J. Corporate social responsibility as a determinant of consumer loyalty: An examination of ethical standard, satisfaction, and trust. J. Bus. Res. 2017, 76, 8–13. [Google Scholar] [CrossRef]

- Bansal, P.; Song, H. Similar but not the same: Differentiating corporate sustainability from corporate responsibility. Acad. Manag. Ann. 2017, 11, 105–149. [Google Scholar] [CrossRef]

- Forcadell, F.J.; Aracil, E. Can multinational companies foster institutional change and sustainable development in emerging countries? A case study. Business Strateg. Dev. 2019. [Google Scholar] [CrossRef]

- Frynas, J.G.; Yamahaki, C. Corporate social responsibility: Review and roadmap of theoretical perspectives. Bus. Ethics 2016, 25, 258–285. [Google Scholar] [CrossRef]

- Jackson, G.; Apostolakou, A. Corporate social responsibility in Western Europe: An institutional mirror or substitute? J. Bus. Ethics 2010, 94, 371–394. [Google Scholar] [CrossRef]

- Buckley, P.J.; Doh, J.P.; Benischke, M.H. Towards a reinassance in international business research? Big questions, grand challenges, and the future of IB scholarship. J. Int. Bus. Stud. 2017, 48, 1045–1064. [Google Scholar] [CrossRef]

- Ramos, T.B.; Caeiro, S.; Moreno Pires, S.; Videira, N. How are new sustainable development approaches responding to societal challenges? Sustain. Dev. 2018, 26, 117–121. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.; Rynes, S. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Raza, A.; Ilyas, M.I.; Rauf, R.; Qamar, R. Relationship between corporate social responsibility (CSR) and corporate financial performance (CFP): Literature review approach. Elixir Financ. Manag. 2012, 46, 8404–8409. [Google Scholar]

- Lii, Y.; Lee, M. Doing right leads to doing well: When the type of CSR and reputation interact to affect consumer evaluations of the firm. J. Bus. Ethics 2012, 105, 69–81. [Google Scholar] [CrossRef]

- Porter, M.; Kramer, M. Strategy and society: The link between competitive advantage and corporate social responsibility. Harvard. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Sen, S.; Bhattacharya, C.B. Does doing good always lead to doing better? Consumer reactions to corporate social responsibility. J. Market. Res. 2001, 38, 225–243. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation building and corporate strategy. Acad. Manag. J. 1990, 33, 233–258. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Lieberman, M.B.; Montgomery, D.B. First-mover (dis)advantages: Retrospective and link with the resource-based view. Strateg. Manag. J. 1998, 19, 1111–1125. [Google Scholar] [CrossRef]

- Hekkert, M.P.; Suurs, R.A.; Negro, S.O.; Kuhlmann, S.; Smits, R.E. Functions of innovation systems: A new approach for analysing technological change. Technol. Forecast Soc. 2007, 74, 413–432. [Google Scholar] [CrossRef] [Green Version]

- Den Hertog, P.; Van der Aa, W.; De Jong, M.W. Capabilities for managing service innovation: Towards a conceptual framework. J. Serv. Manag. 2010, 21, 490–514. [Google Scholar] [CrossRef]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Birindelli, G.; Ferretti, P.; Intonti, M.; Iannuzzi, A.P. On the drivers of corporate social responsibility in banks: Evidence from an ethical rating model. J. Manag. Gov. 2015, 19, 303–340. [Google Scholar] [CrossRef]

- Brammer, S.; Agarwal, V.; Taffler, R.; Brown, M. Corporate reputation and financial performance: The interaction between capability and character. In Proceedings of the European Financial Management Association 2015 Annual Meeting, Amsterdam, The Netherlands, 24–27 June 2015. [Google Scholar]

- Pérez, A.; Rodríguez del Bosque, I. How customer support for corporate social responsibility influences the image of companies: Evidence from the banking industry. Corp. Soc. Responsib. Environ. Manag. 2013, 22, 155–168. [Google Scholar] [CrossRef]

- O’Loughlin, D.; Szmigin, I. Customer perspectives on the role and importance of branding in Irish retail financial services. Int. J. Bank Market. 2005, 23, 8–27. [Google Scholar] [CrossRef]

- Wilkinson, A.; Balmer, J.M. Corporate and generic identities: Lessons from the Co-operative Bank. Int. J. Bank Market. 1996, 14, 22–35. [Google Scholar] [CrossRef]

- Pedersen, E.R.G.; Gwozdz, W.; Hvass, K.K. Exploring the relationship between business model innovation, corporate sustainability, and organisational values within the fashion industry. J. Bus. Ethics 2016, 149, 267–284. [Google Scholar] [CrossRef]

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable innovation, business models and economic performance: An overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- Jain, T.; Jamali, D. Strategic approaches to corporate social responsibility: A comparative study of India and the Arab World. In Development-Oriented Corporate Social Responsibility, Volume 2, Locally Led Initiatives in Developing Economies; Jamali, D., Karam, C., Blowfield, M., Eds.; Routledge: New York, NY, USA, 2015; pp. 71–90. [Google Scholar]

- DeYoung, R.; Lang, W.W.; Nolle, D.L. How the Internet affects output and performance at community banks. J. Bank. Financ. 2007, 31, 1033–1060. [Google Scholar] [CrossRef]

- Raymond, W.; Mohnen, P.; Palm, F.; Van Der Loeff, S.S. Persistence of innovation in Dutch manufacturing: Is it spurious? Rev. Econ. Stat. 2010, 92, 495–504. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Admin. Sci. Quart. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Hecker, A.; Ganter, A. Organizational and technological innovation and the moderating effect of open innovation strategies. Int. J. Innov. Manag. 2016, 20, 1650019. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Bleicher, J.; Stanley, H. Digitization as a catalyst for business model innovation a three-step approach to facilitating economic success. J. Bus. Manag. 2016, 12, 62–71. [Google Scholar]

- Steiber, A.; Alänge, S. Organizational innovation: Verifying a comprehensive model for catalyzing organizational development and change. Triple Helix 2015, 2, 1–28. [Google Scholar] [CrossRef]

- Kathuria, A.; Andrade Rojas, M.; Saldanha, T.; Khuntia, J. Extent Versus range of service digitization: Implications for firm performance. In Proceedings of the XXth America’s Conference on Information Systems, Savannah, GA, USA, 7–9 August 2014. [Google Scholar]

- López-Pérez, M.V.; Pérez-López, M.C.; Rodríguez-Ariza, L. Corporate social responsibility and innovation in European companies. An empirical research. Corp. Ownersh. Control 2009, 7, 274–284. [Google Scholar] [CrossRef]

- Halme, M.; Laurila, J. Philanthropy, integration or innovation? Exploring the financial and societal outcomes of different types of corporate responsibility. J. Bus. Ethics 2009, 84, 325–339. [Google Scholar] [CrossRef]

- Chang, S.J. Sustainable evolution for global business: A synthetic review of the literature. J. Mgmt. Sustain. 2016, 6, 1–23. [Google Scholar] [CrossRef]

- Dietrich, M.; Znotka, M.; Guthor, H.; Hilfinger, F. Instrumental and non-instrumental factors of social innovation adoption. Volunt. Int. J. Volunt. Nonprofit Organ. 2016, 27, 1950–1978. [Google Scholar] [CrossRef]

- Hall, J.K.; Martin, M.J. Disruptive technologies, stakeholders and the innovation value-added chain: A framework for evaluating radical technology development. RD Manag. 2005, 35, 273–284. [Google Scholar] [CrossRef]

- Brüggen, E.C.; Hogreve, J.; Holmlund, M.; Kabadayi, S.; Löfgren, M. Financial well-being: A conceptualization and research agenda. J. Bus. Res. 2017, 79, 228–237. [Google Scholar] [CrossRef]

- Zhao, Q.; Tsai, P.; Wang, J. Improving financial service innovation strategies for enhancing china’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef]

- Brenner, B. Transformative Sustainable Business Models in the Light of the Digital Imperative—A Global Business Economics Perspective. Sustainability 2018, 10, 4428. [Google Scholar] [CrossRef]

- Urban, M.A.; Wójcik, D. Dirty banking: Probing the gap in sustainable finance. Sustainability 2019, 11, 1745. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus Strateg. Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Leone, M.I.; Belingheri, P. The relevance of Innovation for Ethics, Responsibility and Sustainability. Ind. Innov. 2017, 24, 437–445. [Google Scholar] [CrossRef] [Green Version]

- Peeters, H. Sustainable development and the role of the financial world. In The World Summit on Sustainable Development; Hens, L., Nath, B., Eds.; Springer: Dordrecht, The Netherlands, 2005; pp. 241–274. [Google Scholar]

- Pomering, A.; Dolnicar, S. Assessing the prerequisite of successful CSR implementation: Are consumers aware of CSR initiatives? J. Bus. Ethics 2009, 85, 285–301. [Google Scholar] [CrossRef]

- Hong, T.L.; Cheong, C.B.; Rizal, H.S. Service innovation in Malaysian banking industry towards sustainable competitive advantage through environmentally and socially practices. Procedia Soc. Behav. 2016, 224, 52–59. [Google Scholar] [CrossRef]

- Ordanini, A.; Parasuraman, A. Service innovation viewed through a service-dominant logic lens: A conceptual framework and empirical analysis. J. Serv. Res.-US 2011, 14, 3–23. [Google Scholar] [CrossRef]

- Adams, M. Big data and individual privacy in the age of the Internet of Things. Technol. Innov. Manag. Rev. 2017, 7, 12–24. [Google Scholar] [CrossRef]

- Kim, G.; Shin, B.; Lee, H.G. Understanding dynamics between initial trust and usage intentions of mobile banking. Inf. Syst. J. 2009, 19, 283–311. [Google Scholar] [CrossRef]

- Möser, M.; Böhme, R.; Breuker, D. An inquiry into money laundering tools in the Bitcoin ecosystem. In Proceedings of the 2013 APWG eCrime Researchers Summit, San Francisco, CA, USA, 17–18 September 2013; pp. 1–14. [Google Scholar]

- Gatfaoui, H. Translating financial integration into correlation risk: A weekly reporting’s viewpoint for the volatility behavior of stock markets. Econ. Model. 2013, 30, 776–791. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Ortas, E.; Álvarez, I.; Jaussaud, J.; Garayar, A. The impact of institutional and social context on corporate environmental, social and governance performance of companies committed to voluntary corporate social responsibility initiatives. J. Clean. Prod. 2015, 108, 673–684. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Fernández-Izquierdo, M.Á.; Ferrero-Ferrero, I.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J. Rating the Raters: Evaluating how ESG Rating Agencies Integrate Sustainability Principles. Sustainability 2019, 11, 915. [Google Scholar] [CrossRef]

- Frame, W.S.; White, L.J. Empirical studies of financial innovation: Lots of talk, little action? J. Econ. Lit. 2004, 42, 116–144. [Google Scholar] [CrossRef]

- Altunbas, Y.; Goddard, J.; Molyneux, P. Technical change in banking. Econ. Lett. 1999, 64, 215–221. [Google Scholar] [CrossRef]

- Schumpeter, J.A. The Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest, and the Business Cycle; Harvard University Press: Cambridge, MA, USA, 1934. [Google Scholar]

- Foss, N.J.; Laursen, K.; Pedersen, T. Linking customer interaction and innovation: The mediating role of new organizational practices. Organ. Sci. 2011, 22, 980–999. [Google Scholar] [CrossRef]

- Bos, J.W.; Kolari, J.W.; Van Lamoen, R.C. Competition and innovation: Evidence from financial services. J. Bank. Financ. 2013, 37, 1590–1601. [Google Scholar] [CrossRef] [Green Version]

- Hess, K.; Francis, G. Cost income ratio benchmarking in banking: A case study. Benchmark. Int. J. 2004, 11, 303–319. [Google Scholar] [CrossRef]

- Clauss, T. Measuring business model innovation: Conceptualization, scale development, and proof of performance. RD Manag. 2017, 47, 385–403. [Google Scholar] [CrossRef]

- Organization for Economic Co-operation and Development (OECD). Oslo Manual: Guidelines for Interpreting and Collecting Innovation Data, 3rd ed.; OECD Publishing: Paris, France, 2005. [Google Scholar]

- Gallego-Álvarez, I.; Prado-Lorenzo, J.M.; García-Sánchez, I.M. Corporate social responsibility and innovation: A resource-based theory. Manag. Decis. 2011, 49, 1709–1727. [Google Scholar] [CrossRef]

- Mishra, D. Post-innovation CSR performance and firm value. J. Bus. Ethics 2017, 140, 285–306. [Google Scholar] [CrossRef]

- Chih, H.L.; Chih, H.H.; Chen, T. On the determinants of corporate social responsibility: International evidence on the financial industry. J. Bus. Ethics 2010, 93, 115–135. [Google Scholar] [CrossRef]

- Soana, M.G. The relationship between corporate social performance and corporate financial performance in the banking sector. J. Bus. Ethics 2011, 104, 133–148. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Detragiache, E.; Merrouche, O. Bank capital: Lessons from the financial crisis. J. Money Credit Bank. 2013, 45, 1147–1164. [Google Scholar] [CrossRef]

- Scholtens, B. Corporate social responsibility in the international banking industry. J. Bus. Ethics 2009, 86, 159–175. [Google Scholar] [CrossRef]

- European Central Bank (ECB). What Is Fit and Proper Supervision? 2016. Available online: http://www.ecb.europa.eu/ (accessed on 10 April 2018).

- Bernanke, B.S.; Gertler, M.; Gilchrist, S. The financial accelerator in a quantitative business cycle framework. In Handbook of Macroeconomics; Taylor, J.B., Woodford, M., Eds.; North-Holland: Amsterdam, The Netherlands, 1999; Volume 1, Part C; pp. 1341–1393. [Google Scholar]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. Eur. Manag. J. 2013, 31, 642–654. [Google Scholar] [CrossRef] [Green Version]

- Kim, Y.; Brodhag, C.; Mebratu, D. Corporate social responsibility driven innovation. Innov. Eur. J. Soc. Sci. Res. 2014, 27, 175–196. [Google Scholar] [CrossRef]

- Luo, X.; Du, S. Exploring the relationship between corporate social responsibility and firm innovation. Market. Lett. 2015, 26, 703–714. [Google Scholar] [CrossRef]

- MacGregor, S.P.; Fontrodona, J. Exploring the Fit Between CSR and Innovation; Working Paper 758; IESE and University of Navarra: Navarra, Spain, 2008. [Google Scholar]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How corporate social responsibility engagement strategy moderates the CSR–financial performance relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Arellano, M.; Bover, O. Another look at the instrumental variable estimation of error-components models. J. Econ. 1995, 68, 29–51. [Google Scholar] [CrossRef] [Green Version]

- Hayakawa, K. First difference or forward orthogonal deviation-Which transformation should be used in dynamic panel data models? A simulation study. Econ. Bull. 2009, 29, 2008–2017. [Google Scholar]

- Roodman, D. How to do xtabond2: An introduction to difference and system GMM in Stata. Stata. J. 2006, 9, 86–136. [Google Scholar] [CrossRef]

- Ahlstrom, D. Innovation and growth: How business contributes to society. Acad. Manag. Perspect. 2010, 24, 11–24. [Google Scholar] [CrossRef]

- Owen, R.J.; Bessant, J.R.; Heintz, M. (Eds.) Responsible Innovation: Managing the Responsible Emergence of Science and Innovation in Society; Wiley: Chichester, UK, 2013; Volume 104, pp. 27–50. [Google Scholar]

- Kim, Y. Environmental, sustainable behaviors and innovation of firms during the financial crisis. Bus. Strateg. Environ. 2015, 24, 58–72. [Google Scholar] [CrossRef]

- Lai, W.H.; Lin, C.C.; Wang, T.C. Exploring the interoperability of innovation capability and corporate sustainability. J. Bus. Res. 2015, 68, 867–871. [Google Scholar] [CrossRef]

- Friedrich, R.; Koster, A.; Groene, F.; Maekelburger, B. The 2012 industry digitization index. Perspective 2013, 1–13. [Google Scholar]

- Katz, R.L.; Koutroumpis, P. Measuring digitization: A growth and welfare multiplier. Technovation 2013, 33, 314–319. [Google Scholar] [CrossRef]

- Kumbhakar, S.C.; Wang, H.; Horncastle, A.P. A Practitioner’s Guide to Stochastic Frontier Analysis Using Stata; Cambridge University Press: New York, NY, USA, 2015. [Google Scholar]

- Huang, C.J.; Huang, T.H.; Liu, N.H. A new approach to estimating the metafrontier production function based on a stochastic frontier framework. J. Prod. Anal. 2014, 42, 241–254. [Google Scholar] [CrossRef]

| Variables | Obs. | Mean | S.D. | Median | Min. | Max. | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|---|

| CS | 938 | 55.683 | 21.851 | 54.356 | 54356 | 94.894 | 0.029 | 1.591 |

| INN | 938 | 0.971 | 0.020 | 0.977 | 0.842 | 0.997 | −2.342 | 10.903 |

| ROA | 938 | 0.007 | 0.007 | 0.008 | −0.058 | 0.045 | −2.118 | 16.005 |

| TIER-1 | 938 | 0.116 | 0.035 | 0.113 | 0.051 | 0.379 | 2.228 | 14.070 |

| Loans | 938 | 24.686 | 1.824 | 24.776 | 19.644 | 27.831 | −0.383 | 2.401 |

| NPL | 938 | 0.046 | 0.113 | 0.016 | 0.000 | 1.047 | 6.175 | 46.010 |

| Internet | 938 | 0.835 | 0.089 | 0.850 | 0.441 | 0.973 | −1.672 | 8.614 |

| Mobile | 938 | 1.017 | 0.241 | 1.072 | 0.469 | 1.565 | −0.677 | 2.430 |

| CSt−1 | INNt−1 | ROAt−1 | NPLt−1 | Tier1t−1 | Loanst−1 | GDPt | Growtht | Internett | Mobilet | |

|---|---|---|---|---|---|---|---|---|---|---|

| CSt−1 | 1.000 | |||||||||

| INNt−1 | −0.040 | 1.000 | ||||||||

| ROAt−1 | −0.170 | −0.013 | 1.000 | |||||||

| NPLt−1 | 0.105 | 0.020 | −0.238 | 1.000 | ||||||

| Tier1t−1 | −0.095 | 0.073 | 0.010 | 0.041 | 1.000 | |||||

| Loanst−1 | 0.683 | −0.004 | −0.229 | 0.045 | −0.267 | 1.000 | ||||

| GDPt | −0.343 | 0.030 | 0.212 | −0.266 | −0.057 | −0.267 | 1.000 | |||

| Growtht | −0.031 | −0.100 | 0.392 | −0.216 | 0.028 | −0.100 | 0.119 | 1.000 | ||

| Internett | −0.083 | 0.082 | 0.164 | −0.207 | −0.158 | 0.156 | 0.343 | 0.153 | 1.000 | |

| Mobilet | −0.219 | 0.066 | 0.131 | −0.203 | −0.073 | 0.050 | 0.028 | 0.088 | 0.579 | 1.000 |

| Variables | (1) GMM FOD One-Step | (2) GMM FOD Two-Step |

|---|---|---|

| 0.677 **** | 0.684 **** | |

| (0.060) | (0.059) | |

| 39.390 ** | 35.805 ** | |

| (15.300) | (14.024) | |

| −7.512 | 6.710 | |

| (58.333) | (54.983) | |

| −4.686 | −4.245 | |

| (3.482) | (5.314) | |

| 0.598 | −14.886 | |

| (21.993) | (25.119) | |

| 2.807 *** | 2.646 *** | |

| (1.046) | (0.931) | |

| 6.782 * | 8.552 ** | |

| (3.447) | (3.397) | |

| −0.391 | −0.508 ** | |

| (0.250) | (0.234) | |

| Constant | −174.529 *** | −189.634 *** |

| (53.869) | (57.051) | |

| Number of instruments | 97 | 97 |

| Included time dummies | Yes | Yes |

| Included country dummies | Yes | Yes |

| Arellano-Bond test for AR(1) | −5.710 **** | −4.910 **** |

| Arellano-Bond test for AR(2) | 0.460 | 0.390 |

| Hansen J test of overidentification | 53.290 | 53.290 |

| Observations | 875 | 875 |

| Number of banks | 168 | 168 |

| GMM FOD Model | |

|---|---|

| Model 3: One step (collapse, instrumented) | 36.468 ** |

| Model 4: Two step (collapse, instrumented) | 40.153 ** |

| Model 5: One step (limited lags, collapse, no instrumented) | 38.054 ** |

| Model 6: Two step (limited lags, collapse, no instrumented) | 23.584 |

| Model 7: One-step (collapse, no instrumented) | 35.934 ** |

| Model 8: Two-step (collapse, no instrumented) | 28.512 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Forcadell, F.J.; Aracil, E.; Úbeda, F. The Influence of Innovation on Corporate Sustainability in the International Banking Industry. Sustainability 2019, 11, 3210. https://doi.org/10.3390/su11113210

Forcadell FJ, Aracil E, Úbeda F. The Influence of Innovation on Corporate Sustainability in the International Banking Industry. Sustainability. 2019; 11(11):3210. https://doi.org/10.3390/su11113210

Chicago/Turabian StyleForcadell, Francisco Javier, Elisa Aracil, and Fernando Úbeda. 2019. "The Influence of Innovation on Corporate Sustainability in the International Banking Industry" Sustainability 11, no. 11: 3210. https://doi.org/10.3390/su11113210

APA StyleForcadell, F. J., Aracil, E., & Úbeda, F. (2019). The Influence of Innovation on Corporate Sustainability in the International Banking Industry. Sustainability, 11(11), 3210. https://doi.org/10.3390/su11113210