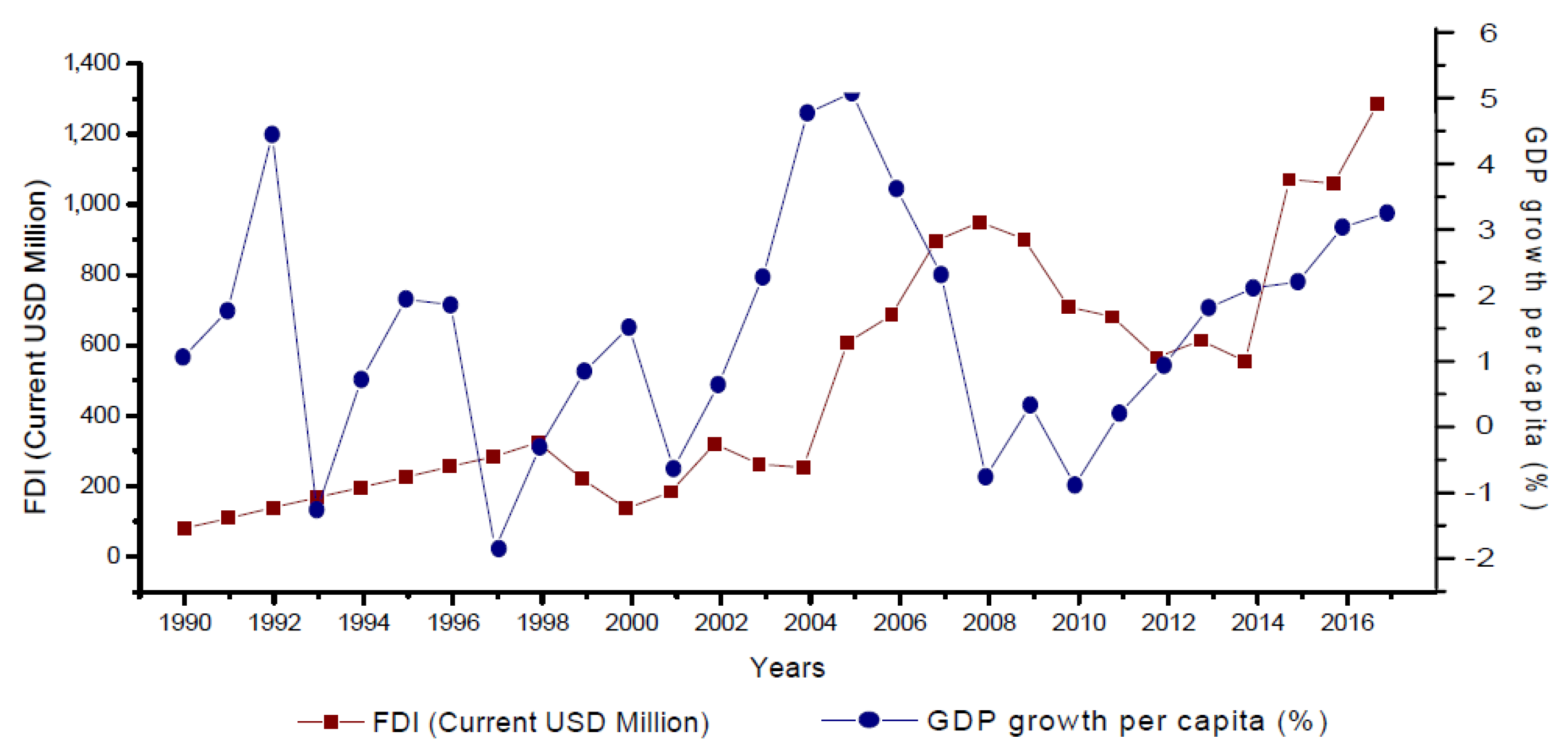

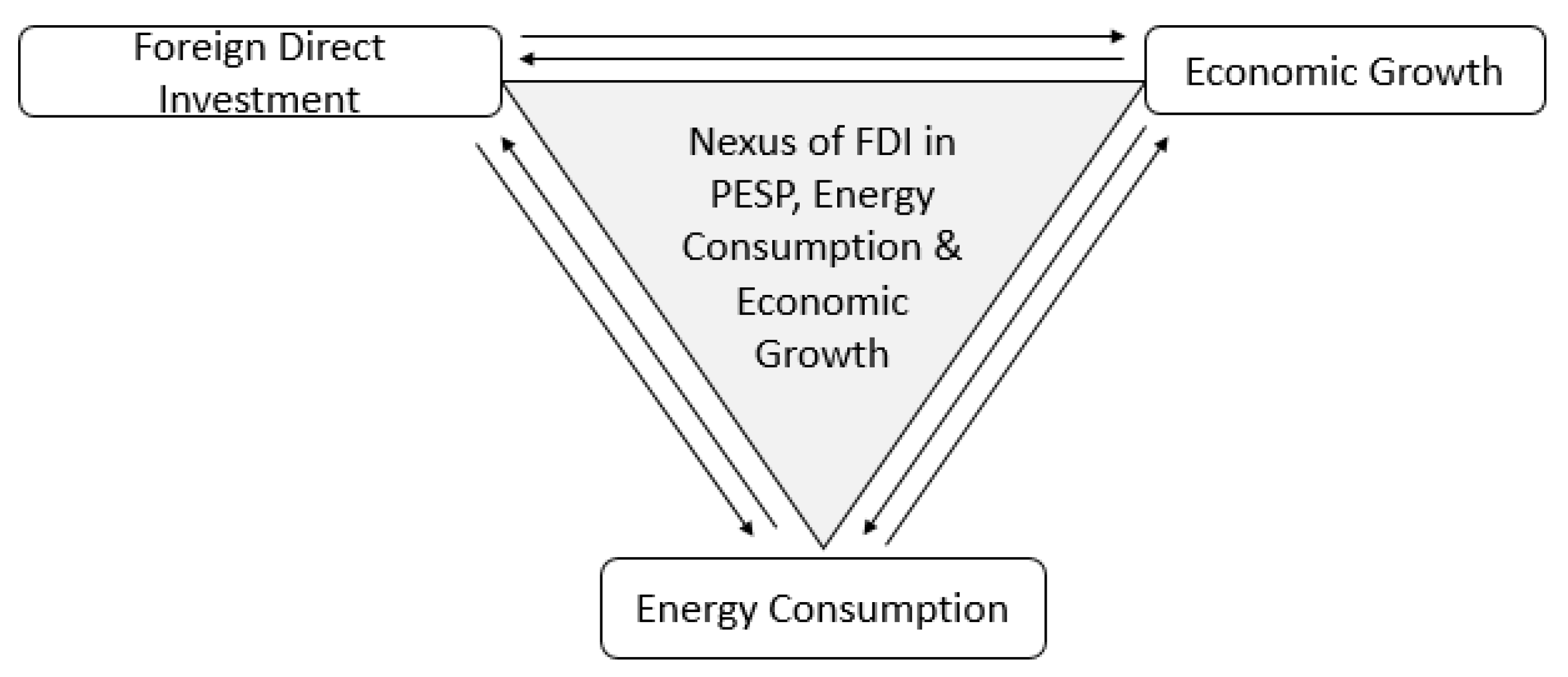

3.1. Foreign Direct Investment (FDI) and Economic Growth

The economic literature revolves around two main theories—modernization and dependency theories—to elaborate the linkage between FDI and economic growth [

12]. According to modernization theory, FDI helps to increase economic growth based on the significance of capital investment for achieving growth. FDI is the main source of technology transfer from developed countries to developing countries, which provides assistance to promote the domestic industry. Usually, developing countries suffer from less developed infrastructure, political and economic instability due to insufficient resources. It is generally claimed that FDI could be helpful for the transfer of knowledge, marketing expertise, managerial skills, and different opportunities to access the market [

13,

14].

On the other side, according to the dependency school theory advocated by D O’Hearn [

15], V Bornschier [

16], and C Stoneman [

17], FDI inflows can show a negative relationship with economic growth in the long-run. The basic reason was that the First World countries after World War II became wealthier by mining different resources from Third World countries. The developing countries were inadequately rewarded for their natural resources, which led to continuous poverty in those countries. The theorists found that capitalism is a basic cause for labor division at a global level. As a result, FDI can create hurdles for growth and increase the income inequality, which can negatively affect economic growth in the long-run.

There could also be some other reasons for the negative linkage between FDI and economic growth. The most important reason is that foreign investment can reduce the production level of domestic firms through competition in the market. Usually, foreign firms face lower marginal costs because of a firm-specific advantage, which provides them with the opportunity to captivate demand away from domestic firms. As a result, their cost is increased and production level decreased. There is also another reason that foreign firms may not be willing to spread firm-specific knowledge to domestic firms. As a result, the production of domestic firms could lead to an adverse situation due to backward technology and less-skilled workers [

18].

The debate about the relationship of FDI to economic growth has been extensively studied in the literature. However, the empirical results are varied across countries based on domestic human capital, infrastructure, and domestic policies to promote foreign investment and trade. Some studies revealed the direct linkage of FDI with economic growth, while there are also many studies in the literature that have highlighted the inverse linkage of FDI with economic growth. Studies that have specifically focused on FDI in the power and energy sector and its effect on economic growth are rarely available in the empirical literature. Most of the prior studies have focused on the analysis of overall FDI and its relationship to economic growth along with different exogenous variables.

The studies that focused on a single country to explore the nexus of FDI–economic growth include MA Almfraji, MK Almsafir, and Y Liu [

19]; C Zhao and J Du [

20]; M Belloumi [

21]; F Khatun and M Ahamad [

12]; Y Hao, L Zhu and M Ye [

22]; JS Mah [

23]; MA Fadhil and MK Almsafir [

24]; C Chakraborty and P Nunnenkamp [

25]; S Anwar and S Sun [

26]; and CF Tang and BW Tan [

27]. The studies that selected multiple countries to analyze the nexus of FDI–economic growth include P Gupta and A Singh [

28]; S Iamsiraroj [

29]; A Omri and B Kahouli [

30]; G Agrawal [

31]; D Herzer [

18]; S Adams [

13]; P Srinivasan, M Kalaivani, and P Ibrahim [

32]; M Al-Iriani [

33]; and SL Gui-Diby [

34].

For example, in the case of a single country to examine the nexus of FDI–economic growth, MA Almfraji, MK Almsafir, and Y Liu [

19] used time-series data for the period 1990–2010 by focusing on Qatar as a sample. Using Vector Auto-Regression (VAR) and Granger causality tests, the results of the study showed a significant effect of FDI inflows on economic growth in the long-run. C Zhao and J Du [

20] used a unit root test, the vector error correction model (VECM), the Augmented-Dickey–Fuller (ADF) test, and a co-integration test, and found a non-significant causal relationship between FDI and economic growth in the context of China for the period 1985–2003.

Moreover, M Belloumi [

35] applied the ARDL bounds testing technique to study the relationship among trade openness, economic growth, and FDI by using data on Tunisia for the period 1970–2008. The findings of the study highlighted that there is no significant causality between economic growth and FDI. More specifically, F Khatun and M Ahamad [

12] could not find causality between FDI in the energy sector and economic growth in both the long-run and the short-run by using Granger causality tests in case of Bangladesh.

In the case of multiple countries to analyze the nexus of FDI–Economic growth, P Gupta and A Singh [

28] used a panel of data on BRICS countries for the period from 1992 to 2013. Using the ordinary least square (OLS) technique, the Johansen co-integration technique, and VECM, the results showed a causal relationship between FDI and economic growth in the context of China, Brazil, and India. Furthermore, the results also showed a short-run causal relationship between FDI and economic growth in the case of China. S Iamsiraroj [

29] applied the fixed effect model and the Generalized Method of Moments (GMM) model to a sample of 124 countries for the time span 1971–2010. The findings established the direct linkage of FDI with economic growth, while economic freedom, trade openness, and labor force, as the major determinants of FDI, were found to directly increase the income growth.

Moreover, A Omri and B Kahouli [

30] observed the relationship between FDI, energy consumption, and economic growth by constructing a panel dataset of 65 countries for the period 1990–2011. They divided the panel dataset more into three sub-panel datasets based on various income levels. Using simultaneous equations with GMM, the results revealed bi-directional causality between FDI and economic growth in some countries. G Agrawal [

31] employed VEC Granger causality and panel co-integration, and confirmed causality between FDI and economic growth by using a panel dataset on BRICS countries for the period 1989–2012.

Table 1 shows a summary of the main empirical studies about the FDI–economic growth nexus.

3.2. Energy Consumption and Economic Growth

In the economics literature, the debate about the nexus of energy consumption and economic growth was initiated by J Kraft and A Kraft [

36], and found the strongest evidence of a relationship between these variables by using data on the United States for the period 1947–1974. Afterward, many researchers examined causal relationships by using Granger causality and tested four hypotheses: (a) the conservation hypothesis, (b) the neutrality hypothesis, (c) the feedback hypothesis, and (d) the growth hypothesis [

37].

Neoclassical economists, such as ER Berndt [

38] and EF Denison [

39], argued that energy is not the significant factor that causes economic growth based on the assumption that energy affects economic growth only in definite ways. On the contrary, ecological economists, such as RU Ayres and I Nair [

40], proposed a model in which they highlighted energy as the main factor of production based on the Laws of Thermodynamics. Afterward, other researchers, such as CJ Cleveland, R Costanza, CA Hall, and R Kaufmann [

41], also endorsed their model by finding significant evidence about the relationship between economic production and energy. Furthermore, DI Stern [

42] also considered energy to be a vital factor in production.

A fairly considerable number of studies have focused on the linkage of energy consumption with economic growth in many countries. The studies that focused on a single country to analyze the relationship between these variables include I Ozturk and A Acaravci [

43]; X-P Zhang and X-M Cheng [

44]; N Bowden and JE Payne [

45]; M Shahbaz, M Zeshan, and T Afza [

46]; AS Alshehry and M Belloumi [

47]; W Oh and K Lee [

48]; M Belloumi [

21]; G Erdal, H Erdal, and K Esengün [

49]; F Karanfil [

50]; W Lise and K Van Montfort [

51]; K Bakhsh, S Rose, MF Ali, N Ahmad, and M Shahbaz [

52]; and F Khatun and M Ahamad [

12]. The studies that concentrated on multiple countries to examine the energy consumption–economic growth nexus include VC Govindaraju and CF Tang [

53]; E Lau, X-H Chye, and C-K Choong [

54]; RPP Pradhan [

55]; N Apergis and JE Payne [

56]; J Asafu-Adjaye [

57]; AM Masih and R Masih [

58]; S Noor and M Siddiqi [

59]; C-C Lee, C-P Chang, and P-F Chen [

60]; and B-N Huang, MJ Hwang, and CW Yang [

61].

For example, in the case of a single country to analyze the nexus of energy consumption and economic growth, I Ozturk and A Acaravci [

43] used the ARDL technique and Granger causality tests, and revealed a relationship among economic growth, employment rate, and energy consumption; however, while carbon emissions and energy consumption did not show causality with economic growth, the employment rate showed a causal relationship with economic growth in Turkey for the sample period 1968–2005. In addition, X-P Zhang and X-M Cheng [

44] used a multivariate model to analyze the relationship among carbon emissions, urban population, economic growth, and energy usage by selecting China as a sample for the period 1960–2007. Using co-integration and Granger causality tests, the results highlighted the unidirectional causality between energy consumption and economic growth in the long-run.

With the same view, M Shahbaz, M Zeshan, and T Afza [

46] analyzed the relationship between renewable and non-renewable energies and economic growth by selecting Pakistan as a sample for the period 1972–2011. Using ARDL and Granger causality tests, the results established a long-run causal relationship between energy consumption and economic growth. AS Alshehry and M Belloumi [

47] examined the inter-relationship between economic activity, energy consumption, and energy price for Saudi Arabia by using data for the period 1971–2010. Using Johansen multivariate co-integration tests and VECM, the results indicated that there is unidirectional causality running from energy consumption to economic growth in the long-run.

In the case of multiple countries to examine the nexus of energy consumption and economic growth, VC Govindaraju and CF Tang [

53] employed the co-integration technique and VECM to analyze the relationship among CO

2 emissions, economic growth, and coal consumption in India and China. The results highlighted the causality among coal consumption, economic growth, and CO

2 emissions in the case of China, but not in India. The results confirmed a unidirectional causal relationship between CO

2 emissions and economic growth. E Lau, X-H Chye, and C-K Choong [

54] studied the causality between energy consumption and economic growth in the context of 17 Asian countries by using a panel of data for the time duration from 1980 to 2006. The results of the study revealed that there is a long-run equilibrium in the selected countries. Furthermore, energy consumption showed direct causality with economic growth both in the long-run and in the short-run.

In addition, RPP Pradhan [

55] explored the relationship of energy consumption, electricity consumption, and oil consumption with economic growth by selecting SAARC countries as a sample for the time duration 1970–2006. Using the Johansen co-integration technique and VECM, the results of the study highlighted unidirectional and bidirectional causality among the variables across the selected countries based on the type of energy consumption. N Apergis and JE Payne [

56] applied the Pedroni co-integration technique and VECM, and revealed unidirectional causality between economic growth and energy consumption by using data on six Central American states for the period 1980–2004. A summary of important empirical studies on the energy consumption–economic growth nexus is shown in

Table 2.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}