The Impact of Green Lending on Credit Risk in China

Abstract

1. Introduction

2. Background

3. Literature Review

4. Theory

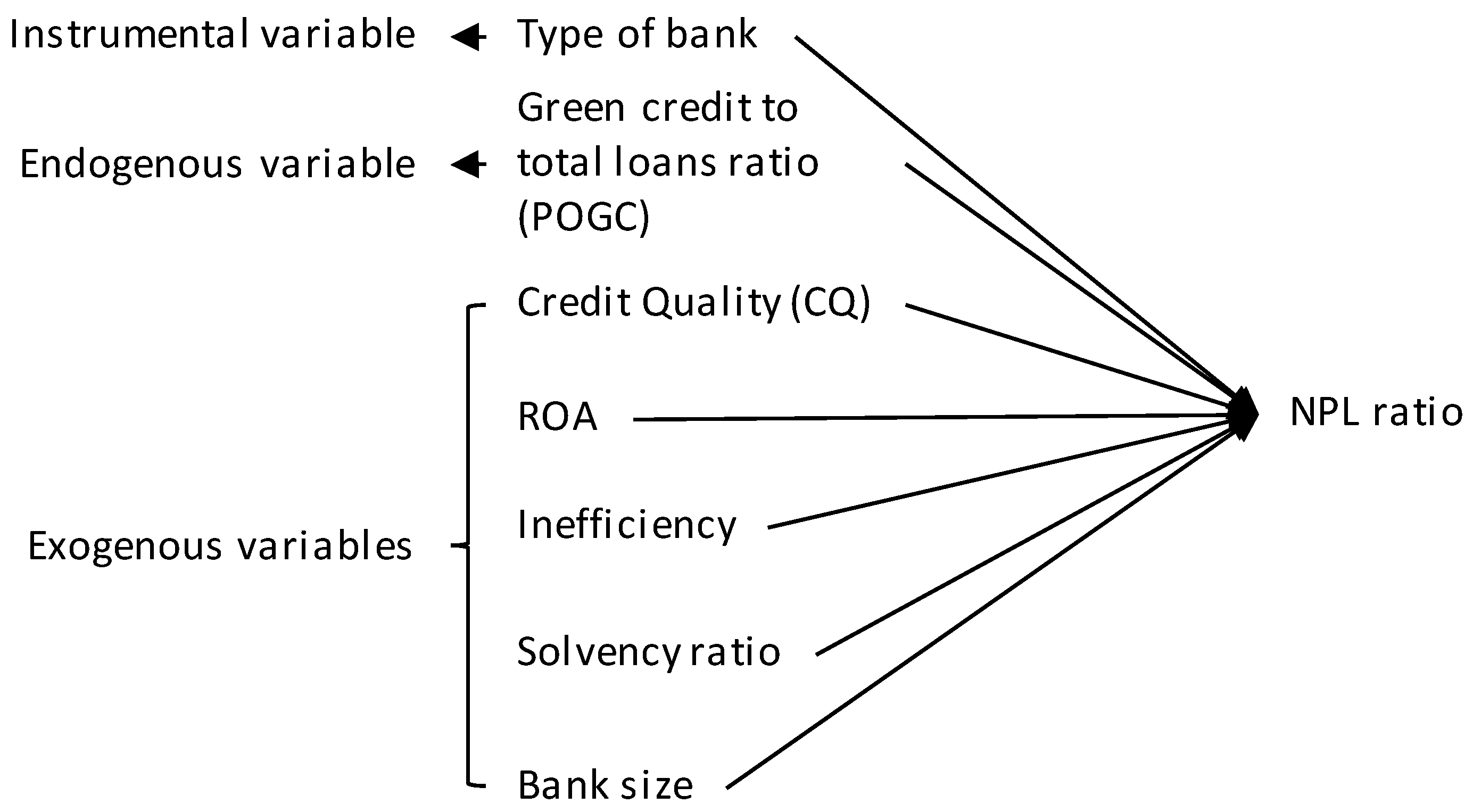

5. Methods

5.1. Regression Model

5.2. Dependent Variable

5.3. Instrumental Variable

5.4. Exogenous Variables

5.5. Efficiency

5.6. Solvency

5.7. Bank Size

6. Sample

7. Results

Regression Models

8. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Weber, O. The financial sector’s impact on sustainable development. J. Sustain. Financ. Investig. 2014, 4, 1–8. [Google Scholar] [CrossRef]

- UNEP. Statement by Banks on the Environment and Sustainable Development; United Nations Environmental Program: Rio de Janeiro, Brazil, 1992. [Google Scholar]

- The Equator Principles. The Equator Principles; The Equator Principles: Geneva, Switzerland, 2013; p. 24. [Google Scholar]

- Bai, Y.; Faure, M.; Liu, J. The role of China’s banking sector in providing green finance. Duke Environ. Law Policy Forum 2013, 24, 89–279. [Google Scholar]

- EU High Level Expert Group in Sustainable Finance. Financing a Sustainable European Economy; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- European Banking Federation. Towards a Green Finance Framework; European Banking Federation: Brussels, Belgium, 2017. [Google Scholar]

- Aizawa, M.; Chaofei, Y. Green credit, green stimulus, green revolution? China’s mobilization of banks for environmental cleanup. J. Environ. Dev. 2010, 19, 119–144. [Google Scholar] [CrossRef]

- Zhao, N.; Xu, X.-J. Analysis on green credit in China. Adv. Appl. Econ. Financ. (AAEF) 2012, 3, 501–506. [Google Scholar]

- He, D.; Zhang, X. Thoughts about commercial banks under the green credit policy (translated). Chin. Acad. Soc. Sci. 2007, 12, 1006–1428. [Google Scholar]

- Hill, D. What Good Are China’s Green Policies If Its Banks Don’t Listen? Guardian. 16 May 2014. Available online: http://www.theguardian.com/environment/andes-to-the-amazon/2014/may/16/what-good-chinas-green-policies-banks-dont-listen (accessed on 13 June 2018).

- Jiguang, L.I.U.; Zhiqun, S. Low carbon finance: Present situation and future development in China. Energy Procedia 2011, 5, 214–218. [Google Scholar] [CrossRef]

- Zhang, B.; Yang, Y.; Bi, J. Tracking the implementation of green credit policy in China: Top-down perspective and bottom-up reform. J. Environ. Manag. 2011, 92, 1321–1327. [Google Scholar] [CrossRef] [PubMed]

- Weber, O. Corporate sustainability and financial performance of Chinese banks. Sustain. Account. Manag. Policy J. 2017, 8, 358–385. [Google Scholar] [CrossRef]

- Weber, O.; Scholz, R.W.; Michalik, G. Incorporating sustainability criteria into credit risk management. Bus. Strateg. Environ. 2010, 19, 39–50. [Google Scholar] [CrossRef]

- Zeidan, R.; Boechat, C.; Fleury, A. Developing a sustainability credit score system. J. Bus. Ethics 2015, 127, 283–296. [Google Scholar] [CrossRef]

- China Banking Regulatory Commission. Notice of the China Banking Regulatory Commission Cbrc on Issuing the Green Credit Guidelines; China Banking Regulatory Commission: Beijing, China, 2012; p. 6.

- Jin, D.; Mengqi, N. The paradox of green credit in China. Energy Procedia 2011, 5, 1979–1986. [Google Scholar] [CrossRef]

- Chan-Fishel, M. Time to Go Green Environmental Responsibility in the Chinese Banking Sector; Friends of the Earth and Banktrack: Amsterdam, The Netherlands, 2007; p. 107. [Google Scholar]

- International Institute for Sustainable Development. How to Issue a Green Bond in China; International Institute for Sustainable Development: Winnipeg, MA, USA, 2015. [Google Scholar]

- China Banking Regulatory Commission. Green Credit in Helping the Adjustment of Economic Structure and the Upgrade in Industry Transformation [Transl.]; China Banking Regulatory Commission: Beijing, China, 2016.

- Park, A.; Ren, C. Microfinance with Chinese characteristics. World Dev. 2001, 29, 39–62. [Google Scholar] [CrossRef]

- Song, W.; Xue, X.; Zhong, L. Microfinance performance in China’s rural areas: A perspective of regional differences. In Proceedings of the 2010 International Conference on Financial Theory and Engineering (ICFTE), Dubai, UAE, 18–20 June 2010; pp. 73–79. [Google Scholar]

- Wang, L.; Juslin, H. The impact of Chinese culture on corporate social responsibility: The harmony approach. J. Bus. Ethics 2009, 88, 433–451. [Google Scholar] [CrossRef]

- Scholtens, B.; Cerin, P.; Hassel, L. Sustainable development and socially responsible finance and investing. Sustain. Dev. 2008, 16, 137–140. [Google Scholar] [CrossRef]

- Stephens, C.; Skinner, C. Banks for a better planet? The challenge of sustainable social and environmental development and the emerging response of the banking sector. Environ. Dev. 2013, 5, 175–179. [Google Scholar] [CrossRef]

- Weber, O.; Hoque, A.; Islam, A.M. Incorporating environmental criteria into credit risk management in Bangladeshi banks. J. Sustain. Financ. Investig. 2015, 5, 1–15. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Bae, S.C.; Chang, K.; Yi, H.-C. Corporate social responsibility, credit rating, and private debt contracting: New evidence from syndicated loan market. Rev. Quant. Financ. Account. 2017, 50, 261–299. [Google Scholar] [CrossRef]

- Bauer, R.; Hann, D. Corporate environmental management and credit risk. SSRN eLibrary 2010. [Google Scholar] [CrossRef]

- Erragragui, E. Do creditors price firms’ environmental, social and governance risks? Res. Int. Bus. Financ. 2017. [Google Scholar] [CrossRef]

- Mengze, H.; Wei, L. A comparative study on environment credit risk management of commercial banks in the Asia-Pacific region. Bus. Strateg. Environ. 2015, 24, 159–174. [Google Scholar] [CrossRef]

- Weber, O.; Diaz, M.; Schwegler, R. Corporate social responsibility of the financial sector–strengths, weaknesses and the impact on sustainable development. Sustain. Dev. 2014, 22, 321–335. [Google Scholar] [CrossRef]

- Ye, Y.; Li, X. Building the regulatory system for the green credit policy in China (trans.). China Bank. 2014, Z1, 70–74. [Google Scholar]

- Ma, J. On the construction of China’s green finance system. Financ. Forum 2015, 5, 18–27. [Google Scholar]

- Wang, Y.; Zhang, J. Evolution, impact, and development of the green credit policy (transl.). China Natl. Cond. Strengths 2014, 9, 45–47. [Google Scholar]

- Wei, G. Concern for the environmental risks and the construction of a green credit bank (transl.). Chin. Bank. 2010, 4, 27–31. [Google Scholar]

- Chang, M.; Wang, S.; Li, D. The Basis for the Implementation of Green Lending-Banking and Environmental Risk Management; Tsinghua University: Beijing, China, 2008; Volume 7. [Google Scholar]

- Hu, N.; Cao, D. Green credit policy and environmental risk management of commercial banks (transl.). Econ. Probl. 2011, 3, 103–107. [Google Scholar]

- Zhao, C. Commercial banks’ green credit practice as a support for the green economic transformation (transl.). Financ. Account. Mon. 2015, 32, 23. [Google Scholar]

- Zhang, X.; He, D. Financial and tax incentive policies for envionmental finance development: Global experience and revelation. Public Financ. Res. 2010, 5, 78–80. [Google Scholar]

- Cai, L.; Cui, J.; Jo, H. Corporate environmental responsibility and firm risk. J. Bus. Ethics 2015, 1–32. [Google Scholar] [CrossRef]

- Weber, O.; Fenchel, M.; Scholz, R.W. Empirical analysis of the integration of environmental risks into the credit risk management process of European banks. Bus. Strateg. Environ. 2008, 17, 149–159. [Google Scholar] [CrossRef]

- Chang, C.-H.; Sam, A.G. Corporate environmentalism and environmental innovation. J. Environ. Manag. 2015, 153, 84–92. [Google Scholar] [CrossRef] [PubMed]

- Saurina, J.; Jimenez, G. Credit cycles, credit risk, and prudential regulation. Int. J. Cent. Bank. 2006, 2, 65–98. [Google Scholar]

- Ghosh, A. Banking-industry specific and regional economic determinants of non-performing loans: Evidence from US States. J. Financ. Stab. 2015, 20, 93–104. [Google Scholar] [CrossRef]

- Messai, A.S.; Jouini, F. Micro and macro determinants of non-performing loans. Int. J. Econ. Financ. Issues 2013, 3, 852. [Google Scholar]

- Indira, R.; Garima, V. Non-performing loans of PSU banks: Some panel results. Econ. Political Wkly. 2002, 37, 429–435. [Google Scholar]

- Rajan, R.; Dhal, S.C. Non-performing loans and terms of credit of public sector banks in India: An empirical assessment. Occas. Pap. 2003, 24, 81–121. [Google Scholar]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Altman, E.I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Kong, D.; Liu, S.; Dai, Y. Environmental policy, company environment protection, and stock market performance: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2012. [Google Scholar] [CrossRef]

- Liu, X.; Liu, B.; Shishime, T.; Yu, Q.; Bi, J.; Fujitsuka, T. An empirical study on the driving mechanism of proactive corporate environmental management in China. J. Environ. Manag. 2010, 91, 1707–1717. [Google Scholar] [CrossRef] [PubMed]

- Saunders, A. Credit Risk Measurement: New Approaches to Value at Risk and Other Paradigms; John Wiley & Sons, Inc.: New York, NY, USA, 1999. [Google Scholar]

- Caouette, J.B.; Altman, E.I.; Narayanan, P. Managing Credit Risk: The Next Great Financial Challenge; Wiley: New York, NY, USA, 1998. [Google Scholar]

- Krugman, P. Balance sheets, the transfer problem, and financial crises. In International Finance and Financial Crises: Essays in Honor of Robert P. Flood, Jr.; Isard, P., Razin, A., Rose, A.K., Eds.; Springer: Dordrecht, The Netherlands, 1999; pp. 31–55. [Google Scholar]

- Ferri, G. Are new tigers supplanting old mammoths in China’s banking system? Evidence from a sample of city commercial banks. J. Bank. Financ. 2009, 33, 131–140. [Google Scholar] [CrossRef]

- Lin, X.; Zhang, Y. Bank ownership reform and bank performance in China. J. Bank. Financ. 2009, 33, 20–29. [Google Scholar] [CrossRef]

- Huaqiang, S. On the endogenous nature of the non-performing loans of the state-owned-bank of China: An analytical framework based on the dual soft-budget constraint theory. J. Financ. 2004, 6, 2. [Google Scholar]

- Wang, N.; Zhu, B. Efficiency and total factor productivity in listed commercial banks in China under the constraint of non-performing loans: An empirical analysis based on sbmdirectional distance function. J. Financ. Res. 2011, 1, 110–130. [Google Scholar]

- Chen, x.; Skully, M.; Brown, K. Banking efficiency in China: Application of dea to pre-and post-deregulation eras: 1993–2000. China Econ. Rev. 2005, 16, 229–245. [Google Scholar]

- Louzis, D.P.; Vouldis, A.T.; Metaxas, V.L. Macroeconomic and bank-specific determinants of non-performing loans in greece: A comparative study of mortgage, business and consumer loan portfolios. J. Bank. Financ. 2012, 36, 1012–1027. [Google Scholar] [CrossRef]

- Reinhart, C.M.; Rogoff, K.S. This Time Is Different: Eight Centuries of Financial Folly; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

- Peiser, R.; Wang, B. Non-performing loan resolution in China. J. Real Estate Portfolio Manag. 2002, 8, 115. [Google Scholar]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach; Nelson Education: Scarborough, ON, Canada, 2015. [Google Scholar]

- Hausman, J.A. Specification tests in econometrics. Econom. J. Econom. Soc. 1978, 1251–1271. [Google Scholar] [CrossRef]

- Lancaster, T. The incidental parameter problem since 1948. J. Econ. 2000, 95, 391–413. [Google Scholar] [CrossRef]

- Kahane, L.H. Regression Basics; SAGE Publications: Thousand Oaks, CA, USA, 2007. [Google Scholar]

- Allison, P.D. Fixed Effects Regression Models; SAGE Publications: Thousand Oaks, CA, USA, 2009; Volume 160. [Google Scholar]

- Greene, W.H. Econometric Analysis (International Edition); Pearson: Toronto, ON, Canada, 2000. [Google Scholar]

- Berger, A.N.; DeYoung, R. Problem loans and cost efficiency in commercial banks. J. Bank. Financ. 1997, 21, 849–870. [Google Scholar] [CrossRef]

- Hellmann, T.F.; Murdock, K.C.; Stiglitz, J.E. Liberalization, moral hazard in banking, and prudential regulation: Are capital requirements enough? Am. Econ. Rev. 2000, 90, 147–165. [Google Scholar] [CrossRef]

- Makri, V.; Tsagkanos, A.; Bellas, A. Determinants of non-performing loans: The case of Eurozone. Panoeconomicus 2014, 61, 193–206. [Google Scholar] [CrossRef]

- Stern, G.H.; Feldman, R.J. Too Big to Fail: The Hazards of Bank Bailouts; Brookings Institution Press: Washington, DC, USA, 2004. [Google Scholar]

- China Banking Regulatory Commission (Ed.) Notice of the China Banking Regulatory Commission on Key Performance Indicators of Green Credit Implementation; China Banking Regulatory Commission: Beijing, China, 2014; Volume 186.

- Cui, Y. Analyzing Green Finance Incentives: An Empirical Study of the Chinese Banking Sector. Master’s Thesis, University of Waterloo, Waterloo, ON, Canada, 2017. [Google Scholar]

- China Banking Regulatory Commission. Annual Report 2015; China Banking Regulatory Commission: Beijing, China, 2015.

- Tukey, J.W. Exploratory Data Analysis; Addison-Wesley Publishing Company: Reading, MA, USA, 1977. [Google Scholar]

- Allison, P.D. Multiple Regression: A Primer; Pine Forge Press: Newbury Park, CA, USA, 1999. [Google Scholar]

- Nerlove, M. Essays in Panel Data Econometrics; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Altman, E.I.; Saunders, A. Credit risk measurement: Developments over the last 20 years. J. Bank. Financ. 1998, 21, 1721–1742. [Google Scholar] [CrossRef]

- Liu, X.; Anbumozhi, V. Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Zhao, N.; Patten, D.M. An exploratory analysis of managerial perceptions of social and environmental reporting in China: Evidence from state-owned enterprises in Beijing. Sustain. Account. Manag. Policy J. 2016, 7, 80–98. [Google Scholar] [CrossRef]

- Weber, O. Environmental, social and governance reporting in China. Bus. Strateg. Environ. 2014, 23, 303–317. [Google Scholar] [CrossRef]

- Zhang, B.; Bi, J.; Yuan, Z.; Ge, J.; Liu, B.; Bu, M. Why do firms engage in environmental management? An empirical study in China. J. Clean. Prod. 2008, 16, 1036–1045. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between operational practices and performance among early adopters of green supply chain management practices in Chinese manufacturing enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Lardy, N. Financial Repression in China; Peterson Institute for International Economics: Washington, DC, USA, 2008. [Google Scholar]

{kind=link}

| Bank | Type of Bank |

|---|---|

| China Development Bank (CDB) | Policy bank |

| Industrial and Commercial Bank of China (ICBC) | State-owned commercial bank |

| China Construction Bank (CCB) | State-owned commercial bank |

| Agricultural Bank of China (ABC) | Policy bank |

| Bank of China Limited (BOC) | State-owned commercial bank |

| Bank of Communications (BOCOM) | State-owned commercial bank |

| China Merchants Bank (CMB) | Joint-stock commercial bank |

| Shanghai Pudong Development Bank (SPD) | Joint-stock commercial bank |

| China Minsheng Banking (CMBC) | Joint-stock commercial bank |

| Industrial Bank (CIB) | Joint-stock commercial bank |

| China Citic Bank (CNCB) | Joint-stock commercial bank |

| China Everbright Bank (CEB) | Joint-stock commercial bank |

| Ping An Bank | Joint-stock commercial bank |

| Hua Xia Bank (HXB) | Joint-stock commercial bank |

| China Guangfa Bank (CGB) | Joint-stock commercial bank |

| China Bohai Bank (CBHB) | Joint-stock commercial bank |

| Bank of Beijing (BOB) | City commercial bank |

| Bank of Nanjing | City commercial bank |

| Bank of Shanghai (BOS) | City commercial bank |

| Bank of Jiangsu | City commercial bank |

| Bank of Ningbo | City commercial bank |

| Bank of Chongqing | City commercial bank |

| Harbin Bank | City commercial bank |

| Bank of Zhengzhou | City commercial bank |

| Year | Indicator | POGC | NPL Ratio | Return on Assets | Inefficiency | Solvency | Size | Credit Quality |

|---|---|---|---|---|---|---|---|---|

| 2009 | Average | 2.3% | 1.2% | 0.9% | 48.2% | 5.0% | 4.2% | 2.1% |

| SD | 2.2% | 0.6% | 0.3% | 11.0% | 1.2% | 5.8% | 0.6% | |

| 2010 | Average | 2.4% | 0.9% | 1.0% | 45.3% | 5.4% | 4.2% | 2.1% |

| SD | 2.6% | 0.4% | 0.2% | 10.5% | 1.0% | 5.6% | 0.5% | |

| 2011 | Average | 2.7% | 0.7% | 1.2% | 43.8% | 6.0% | 4.2% | 2.3% |

| SD | 2.9% | 0.3% | 0.2% | 11.8% | 0.9% | 5.5% | 0.6% | |

| 2012 | Average | 3.5% | 0.8% | 1.2% | 42.8% | 5.9% | 4.2% | 2.4% |

| SD | 3.4% | 0.3% | 0.2% | 12.1% | 0.9% | 5.2% | 0.5% | |

| 2013 | Average | 3.8% | 0.8% | 1.2% | 42.0% | 6.1% | 4.2% | 2.4% |

| SD | 3.5% | 0.2% | 0.2% | 11.2% | 0.7% | 5.1% | 0.5% | |

| 2014 | Average | 4.5% | 1.1% | 1.1% | 40.1% | 6.4% | 4.2% | 2.6% |

| SD | 4.8% | 0.2% | 0.2% | 9.8% | 0.9% | 5.0% | 0.5% | |

| 2015 | Average | 4.8% | 1.4% | 1.0% | 38.2% | 6.7% | 4.2% | 2.8% |

| SD | 5.2% | 0.3% | 0.2% | 9.4% | 1.0% | 4.8% | 0.6% | |

| Total | Average | 3.4% | 1.0% | 1.1% | 42.9% | 5.9% | 4.2% | 2.4% |

| SD | 3.7% | 0.4% | 0.2% | 11.1% | 1.1% | 5.2% | 0.6% |

| NPL Ratio | ROA | Size | Credit Quality | Efficiency | Solvency | |

|---|---|---|---|---|---|---|

| Return on Assets | −0.15 | |||||

| Size | 0.35 ** | 0.29 ** | ||||

| Credit quality | 0.54 ** | −0.01 | 0.33 ** | |||

| Inefficiency | −0.01 | −0.43 ** | −0.15 * | −0.05 | ||

| Solvency | 0.07 | 0.53 ** | 0.29 ** | 0.15 | −0.31 ** | |

| Green credit proportion | −0.08 | −0.12 | 0.12 | −0.10 | −0.12 | −0.36 ** |

| Variable | Transformation |

|---|---|

| Proportion of green credit | Square root |

| NPL ratio | Square root |

| ROA | Square |

| Size | Log |

| Credit quality | Log |

| Inefficiency | 1/square |

| Solvency | identity |

| Model 1 (RE) | Model 2 (2SLS) | |||

|---|---|---|---|---|

| NPLR | First Stage (POGC) | Second Stage (NPLR) | Second Stage (NPRL), Standardized Coefficients | |

| POGC | −0.058 (p < 0.0001) | −0.231 (p = 0.001) | −0.759 | |

| Type of bank | 0.036 (p < 0.0001) | |||

| Credit quality | 0.038 (p < 0.0001) | 0.046 (p = 0.084) | 0.047 (p < 0.0001) | 0.464 |

| ROA | −236.43 (p < 0.0001) | −85.51 (p = 0.598) | −158.19 (p = 0.001) | −0.539 |

| Inefficiency | 0.003 (p = 0.001) | 0.012 (p = 0.001) | 0.002 (p = 0.012) | 0.479 |

| Solvency | 0.275 (p = 0.084) | −1.67 (p = 0.806) | 0.144 (p = 0.441) | 0.124 |

| Year | −0.001 (p = 0.467 | 0.004 (p = 0.221) | 0.001 (p = 0.386) | −0.007 |

| Size | 0.005 (p = 0.002) | 0.003 (p = 0.756) | 0.011 (p < 0.0001) | 0.588 |

| Constant | 1.44 (p = 0.375) | −8.59 (p = 0.223) | −1.45 (p = 0.483) | 14.033 |

| Model significance | p < 0.00001 | p < 0.00001 | p < 0.00001 | |

| R-sq | 0.4055 | 0.390 | ||

| Obs | 168 | 168 | 168 | |

| Root MSE | 0.031 | |||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cui, Y.; Geobey, S.; Weber, O.; Lin, H. The Impact of Green Lending on Credit Risk in China. Sustainability 2018, 10, 2008. https://doi.org/10.3390/su10062008

Cui Y, Geobey S, Weber O, Lin H. The Impact of Green Lending on Credit Risk in China. Sustainability. 2018; 10(6):2008. https://doi.org/10.3390/su10062008

Chicago/Turabian StyleCui, Yujun, Sean Geobey, Olaf Weber, and Haiying Lin. 2018. "The Impact of Green Lending on Credit Risk in China" Sustainability 10, no. 6: 2008. https://doi.org/10.3390/su10062008

APA StyleCui, Y., Geobey, S., Weber, O., & Lin, H. (2018). The Impact of Green Lending on Credit Risk in China. Sustainability, 10(6), 2008. https://doi.org/10.3390/su10062008