1. Introduction

The coal-mining industry in South Africa contributes much to the country’s economic welfare and offers lucrative investment opportunities, yet brings about a number of challenges, for example environmental impacts and compromising the health of workers. By far the most severe problem is the rise in the contamination of water, for instance, water in one of the South African Provinces, Mpumalanga, the Middelburg dam is estimated to be 40% unsuitable for human consumption. The critical challenge facing South Africa is to propose and provide policies and frameworks that are effective and integrated; and to implement resolute capital approaches to generate foreign capital inflows and platforms that ought to mitigate the problems that are indicated above. This should ensure that South Africa as a country is aligned to viable improvement, whilst taking full advantage of the prospective export profits through the export of coal [

1]. The coal deposits in South Africa are located in what is referred to as the Karoo Super group. This is a dense categorisation of alluvial rocks that have been deposited during a period ranging from 180 to 300 million years. These coal layers are found in the segment known as the Ecca subgroup, made up of mudstones including sandstones. These coal deposits that were placed in large river environments appropriate for the development of coal did not transpire in all places, and these coal deposits are fairly limited, mostly occurring in the basin of the Karoo. The stretch of the basin ranges from Welkom in the Free State province to Nongoma in Kwa Zulu Natal. It is also estimated that about 50% of the coalfields in areas such as Emalahleni, Ermelo, and Highveld encompass the deposits of coal that may be recovered [

2].

1.1. Corporate Social Responsibility

Corporate Social Responsibility (CSRx) (x = 1 or 2—see below) is a generic for two forms, namely Corporate Social Responsiveness (CSR1) and Corporate Social Responsibility (CSR2) [

3]. Modern companies, including coal-mining companies are run by CEOs, managers, etc. and understandably it is in the interest of management and the owners to maximise profits and create a long-term and sustainable competitive advantage. In this process, however, those in control often lose sight of environmental issues, and the effect their company has on the environment. Consequently company (mining) boards of control were formed. These boards usually represent the interests of other stakeholders, e.g., shareholders of the company, or in our case coal-mining companies, and guard against managerial opportunism. Since boards themselves may be compromised in their noble objectives, [

3] recommends that ordinary employees, but especially members from the local community ought to have membership on these boards. Presumably then, such community leaders would monitor company (mining) activities since it would affect them and their environment in which they live directly.

1.2. CSRx and the IT Information System

Plausibly because of the above CSRx aspects, modern companies, e.g., the coal-mining industry and their shareholders have become progressively concerned regarding matters relating to the environment. In the same context, the purpose of an information system (IS) and information technology (IT) in various companies concerning environmental sustainability has been transformed. Specific programmes and projects are considered to be reliable in striving towards a society that is sustainable. The fundamentals contained by an IS/IT assessment as well as expenses, profits and risks in companies linked to the appraisal of IS and the avoidance of the depletion of natural resources so as to maintain an ecological balance are being considered in relation to the major obstacles regarding sustainability processes. This compels companies to endeavour to lessen the influence of their IS/IT activities in a social and ethical manner towards the environment [

4].

An IS is a multifaceted communal item that emanates from embedding technological structures within a company wherein technical and matters of social nature are gradually entangled, combined with a wide range of moral decrees and actions. These are predisposed by societal ideals, welfare of political nature and the contestants’ specific delineations of their state of affairs paramount to the execution of such a system [

5]. To this effect, [

6] considers an IS as a community system entrenched in IT. Logically such entrenchment does not avert the complete unit from being a societal structure, and it might not be probable to develop a rigorous and efficient IS, integrating substantial technology without looking at it as a societal system.

There appears to be no simple solution to modern environmental problems and societal challenges facing humanity, hence there may never be scientific certainty or agreement [

7]. Key environmental problems that have been caused by coal-mining include amongst others: sterilised land; Acid Mine Drainage (AMD); underground fires and sink holes from abandoned mines. Human diseases include: pneumoconiosis, asthma, and hyperpigmentation (appearance that depicts patches or a flushed complexion). The coal-mining companies in South Africa also need to comply with good corporate governance as stipulated by King IV [

8], yet such compliance coupled with minimising environmental and health impacts may be costly. Subsequently, the researchers postulate the need for an information framework embedding Environmental Management Accounting (EMA) principles to facilitate cost saving of environmental impacts for the South African coal-mining industry and to guide companies to decrease their environmental footprint. King IV compliance may be largely absent, for instance, voluntary implementation of King IV by coal-mining companies is insufficient as these companies may focus on generating profits only, rather than saving the environment in which they operate. Furthermore, coal-mining companies should be accountable and responsible to ensure they mitigate negative impacts on conservation. Consequently, an information framework to facilitate cost savings of environmental impacts should be one of the essential tools for coal-mining companies in South Africa.

The above problem statement informs the following research questions.

- (1)

What challenges are generated by the South African coal-mining industry? (RQ1)

- (2)

Which frameworks exist to facilitate cost saving of environmental impacts for the coal-mining industry? (RQ2)

- (3)

What management accounting tools and techniques may be used to facilitate cost saving in coal-mining companies? (RQ3)

Our research objective is to:

Develop a conceptual information framework to facilitate cost saving of environmental impacts for the coal-mining industry in South Africa (RO).

2. Literature Review

Mining operations may have a harmful bearing on society and the physical environment in many different ways. Some of these effects and health impacts are discussed in

Section 2.1 and 2.2 thereby addressing the first research question (RQ1).

2.1. Effect of Coal-Mining Activities on the Environment

Numerous coal-mining undertakings may lead to the contamination of soil and water that flows beneath the earth’s surface thus filling the permeable spaces. These consist of: leakage from metropolitan and/or mine dumps that have chemical substances; mining sites that have been deserted; chemical leaks that occur by accident; indecorous subversive disposal of watery discharges; the strategic placing of tanks to collect liquid waste in hydrological and ecological sites; and inopportune application of manures and pesticides meant for agrarian and home procedures [

9]. All these undertakings impact on the confined societies wherein the mines are located.

In a study enquiring into the influence of the excavation of coal and how it impacts the populace assembly of plants in Jaintia Hills neighbourhood of Meghalaya, North East India, the authors of [

10] established that widespread mining of coal in this area caused contraction of the usage of land, and the cover of land; and caused a scenery that is deformed with mine plunders. The disruption due to mining activities has lessened the prospects of reviving of the plant types, resulting in plummeting of the quantity of species in the areas that have been excavated. The number of herbaceous species occurring in the excavated provinces remained established, greater as compared to the areas that were not mined. Thus, quarrying undertakings are considered to be detrimental to the plant diversity.

The phrase ‘origin of threat’ implies the derivation of the threats, for instance, polluted water emanating from the mined area; the alleyway as a way through which the danger stretches to a receptor for example, leakages and leaks of polluted water to ground and surface water; and a surge in other possibly unsafe biochemical spills. These chemical spills have the ability to damage aquatic flora and fauna, including other plant types at trophic intensities higher up in the food chain, particularly plant species that may not withstand the upsurge in high levels of metal content in waste water [

11]. Coal-mining companies should, therefore, operate within the relevant environmental policies to avoid environmental degradation, human diseases, and air pollution. The ‘source of risk’ model demonstrates clearly how coal-mining operations may affect the natural environment; human health; and flora, and fauna in terms of health hazards. Contamination due to mining activities from one mining project for instance, may disturb a wide range of square kilometres and AMD may sterilise the environment, making it unsuitable for plant growth for many years to come. Notwithstanding the undeniable proof of the conservational destruction triggered by excavating coal during the preceding years, the business holistically encouraged the corporate oxymoron of ecological quarrying of land [

12]. Therefore, coal-mining companies should control the discharge of AMD into the environment.

2.2. Health Impacts of Coal Mining Activities on Humans

In a study enquiring into nuisance dust, un-protective exposure to the levels of dust caused by mining activities in the in the USA, 1934–1969, the authors of [

13] established that dependence on this deceptive precaution, and the expansive perception of the nontoxicity of dust from the coal mines caused detrimental environmental challenges. An epidemic was caused by dust and, hence, led to the eminence of chronic respirational illness that affected many mine workers in America’s bituminous and anthracite coal-mining areas just before the 20th century. By 1969, the US Surgeon General predicted that about 100,000 miners including ex-mineworkers were affected and were sick from pneumoconiosis, anthracic-silicosis and illness that affects the lungs. Similarly, the author of [

14] maintains that more miners are suffering from the pneumoconiosis and other occupationally induced diseases. Therefore, regular health checks should be implemented by the coal mines so as to identify imminent diseases that may affect the miners.

Fire and eruptions are both serious hazards that occur in a mine when any of fuel (methane and coal dust) and oxygen mixtures, followed by an ignition such as electrical abrasion; smoking; or chemical reactions occur in mines. On 20 November 1968, 78 of 99 employees of the mine lost their lives due to a major blast at Consolidation Coals Farmington No.9 in Farmington, West Virginia. Due to the fact that coal is essentially carbon, it oxidises to produce heat, thereby creating a hazard. With the exception of anthracite, all grades of coal are subject to spontaneous heating and ignition. Since spontaneous heating is cumulative, coal is most dangerous 90 to 120 days after it has been mined [

15].

Other additional hazards such as machinery also account for many injuries and fatalities in the mines. Roof bolting equipment and power drills are often involved in mine accidents. There is also a danger associated with the use of explosives. Incorrect blasting may cause fires and explosions, and by-products of explosion, such as carbon monoxide and nitric oxide, may poison or kill workers. Miners who breathe dust could develop lung cancer or other respiratory diseases such as black lung disease. Since the majority of mining explosions occur underground, coal mining companies ought to continuously monitor underground working conditions [

15].

Imminent health hazards and challenges exist in the Balkans and these include health complications due to coal that is in the ground. Lignite for instance has been identified a contributing element of critical, devastating disease that affects the kidneys and also linked with urinary track cancers. The ailment recognised as Balkan endemic nephropathy (BEN) occurs in groups, such as the villages in the former Yugoslavia and Romania. [

16] Further argues that from the time records were retained in the 1950s, hundreds and thousands of individuals in the prevalent villages are assumed to have passed on due to kidney lapses and related complications. Burning coal seams that may not be managed around the world are dominant in China, India, and South Africa. Emissions emanating from these fires include high concentrations of chemicals such as benzene, toluene, xylene, and ethylbenzene [

16].

In South Africa for instance, the author of [

17] reports that the Blesboklaagte region which is located in the eastern part of the Ferrobank industrialised zone, in Emalahleni, Mpumalanga has been undermined as is demonstrated by board and pillar structures that have collapsed, as well as the existence of coal disposal dumps. When the mining operations ceased for instance, the original board and pillar, the shallow roof of the mine then curved in and warped, over a wide area. These subsidence landscapes may be noticed in suburban areas including the deserted parts south of the airfield and north of an informal settlement. Warning signs serve as a reminder that the area is not safe as depicted by the markings on the tar road. The major challenge and hazard is that dwellers from the informal settlement walk across this area daily unaware of the dangers they are faced with.

Figure 1 depicts a burning collapsed coal mining area (sink hole).

Over a period of time, crystalline silica (also known as silica) dust has since been renowned as a danger to human health as it affects the lungs and causes breathing problems. During subversive quarrying operations, the silica dust is formed from many sources for instance, cutting, drilling, or grinding of the rock structure. This rock material in normally found as an innate component of the coal, however, it is typically not a substantial foundation of silica [

18]. According to the authors of [

19] most major mining operations executed through the open cast mining method cause dust. Key activities that result in dust being produced include drilling, blasting, stacking, unstacking, and conveying of coal. Therefore, this dust impacts on the environment as it affects the quality of air within the vicinity of the mine and local communities thus creating health hazards.

In a similar study enquiring into the health effects of the use of coal in residential households in China, the authors of [

16] established that most types of coal experienced mineralisation, causing imminent affluences that are toxic, for example, fluorine, mercury, antimony, and thallium. The use of the mined coal with high content of carbon in domestic stoves that do not have air vents exacerbates the poisonous components in emissions. The condition is worsened by the exercise whereby crops are left to dry above the coal fires. People who are affected reveal characteristic signs of arsenic exterminating, as well as hyperpigmentation, hyperkeratosis (shows a skin that is peeling commonly mostly on the feet including hands), Bowen’s ailment (black, horny, precancerous skin scratches).

The authors of [

20] established that soil comprising substances such as arsenic, lead, and nickel are expressively associated with the prevalence of biological deficiencies. Thus, residents located in central Appalachia, where considerable and expansive coal mining activities occur, are subject to a higher level of risk in contracting main depression and major psychological anguish in relation to other regions of Appalachia [

21].

The discussions in

Section 2.1 and 2.2 above answered our first research question, namely: What challenges are generated by the coal-mining industry? (RQ1)

Next,

Section 2.3 and 2.4 address research question 2 (RQ2).

2.3. Environmental Management Accounting

Environmental Management Accounting (EMA) is considered as the procedure for managing conservation and performance aspects through developing and implementing relevant accounting systems and practices relating to the environment. This includes but not limited to some companies providing reports and conducting environmental audits. EMA encompasses the analysis of LCC, full cost accounting (FCA), complete assessing of related benefits, and strategic ecological management planning [

22].

On the outward evaluation of EMA, specifically in other contexts, it is also known as environmental financial accounting (EFA) that offers both financial information and ecological to external interested parties for instance stockholders, rating authorities, ecological governing authorities and statistical companies on the performances of business and level of risks. Green safeguarding projects, intending to minimise releases and wastes at origin (circumvention decision) by enhanced use of raw materials and calling for less (detrimental) operational materials are frequently not acknowledged and applied [

23]. As a result, the cost-effective and environmental benefits to be attained from these processes may not be applied by the coal mining companies.

EMA is considered to equally apply to financial and physical issues of conservational accounting. Physical EMA (PEMA) taking into account energy and the flow of water, whereas monetary EMA (MEMA) addresses expenditures relating to the business utilisation of natural resources and the expenses for averting conservational damages [

24]. Similarly, the author of [

25] argues that EMA is a means premeditated to manage fiscal and non-fiscal eco-friendly undertakings in businesses. It is turning out to be most imperative for inventiveness of an environmental nature and routine management activities such as the design of products; control of costs and apportionment; pricing of products; and performance appraisal. In the same line of thought, the author of [

26] contends that in addition to creating value for the consumers by bringing into being and delivering products that are ecologically friendly, companies must disclose their monetary enactment through the appropriate review of conservational costs in their cost accounting systems.

2.4. Analysing the Determinants of EMA Adoption

The development of EMA regarding waste management in local governments in Australia was influenced by social structural inspirations and company contextual encouragements. With reference to a case study in New South Wales (NSW) that was conducted on the twelve local municipalities, it was established that clement levels of EMA information is being utilised for the management of waste. It was further argued that initiatives such as recycling, physical and financial accounting for solid and liquid waste in these councils were much higher as compared to those of indirect and external cost; and effect on waste management accounting [

27].

In Malaysia, the authors of [

28] established that sociological alignment may directly impact the company systems thus bringing about backing for the new institutional sociology viewpoint of institutional theory, wherein tough pressure of normative and isomorphism were identified as having a positive influence on the embracing level of EMA. Most significantly, the research indicates the essential role played by academic institutions such as accounting associations, policymakers, the department of education (DOE), the Inland Revenue Board including EMA adoption by companies specialising in manufacturing in Malaysia.

In Germany, the authors of [

29] undertook a study on adopting corporate environmental systems and established that compliance of controlling nature and lawful certainties were major inspirations for the adoption of eco-friendly practices in the gas and energy businesses. Similarly, the authors of [

30] argue that in Zimbabwe, environmental compliance and pressures stem from regulatory institutions such as the Zimbabwean Revenue Authority (ZIMRA). Most administrations are regularly faced with key challenges of articulating policies and procedures that address manifold scale goals. Some major challenges include but are not limited to upholding high social and ecological values; and non-financial results that are challenging to put a price on for example a cleaner atmosphere or enhanced health of the community [

31]. The hazardous manufacturing and risky businesses for instance, companies dealing with the manufacturing of chemicals are expected to be proactive through legislative requirements to adhere to conservational managing undertakings [

32]. Therefore, regulatory authorities motivate coal-mining companies to comply with environmental policies.

Different societies worldwide are progressively expecting and needing a more substantial stake of reimbursements from the excavation projects based in their local communities, to be more included and involved in making of decisions, and guarantees that the processing of minerals will be carried out in a safe and responsible manner. These developments have been prompted by the upsurge evolution of the paradigm shift in ecological improvement (with its equivalent emphasis on the societal magnitudes of development taking into account the necessity for partaking in the taking of key decisions by the public) including expansive governance changes that have gradually conveyed principal authority towards non-state for instance, market and the public stakeholders in the mining industry [

33]. This may be elucidated by the reasoning that a lot of companies are still utilising fragile conservative management accounting systems.

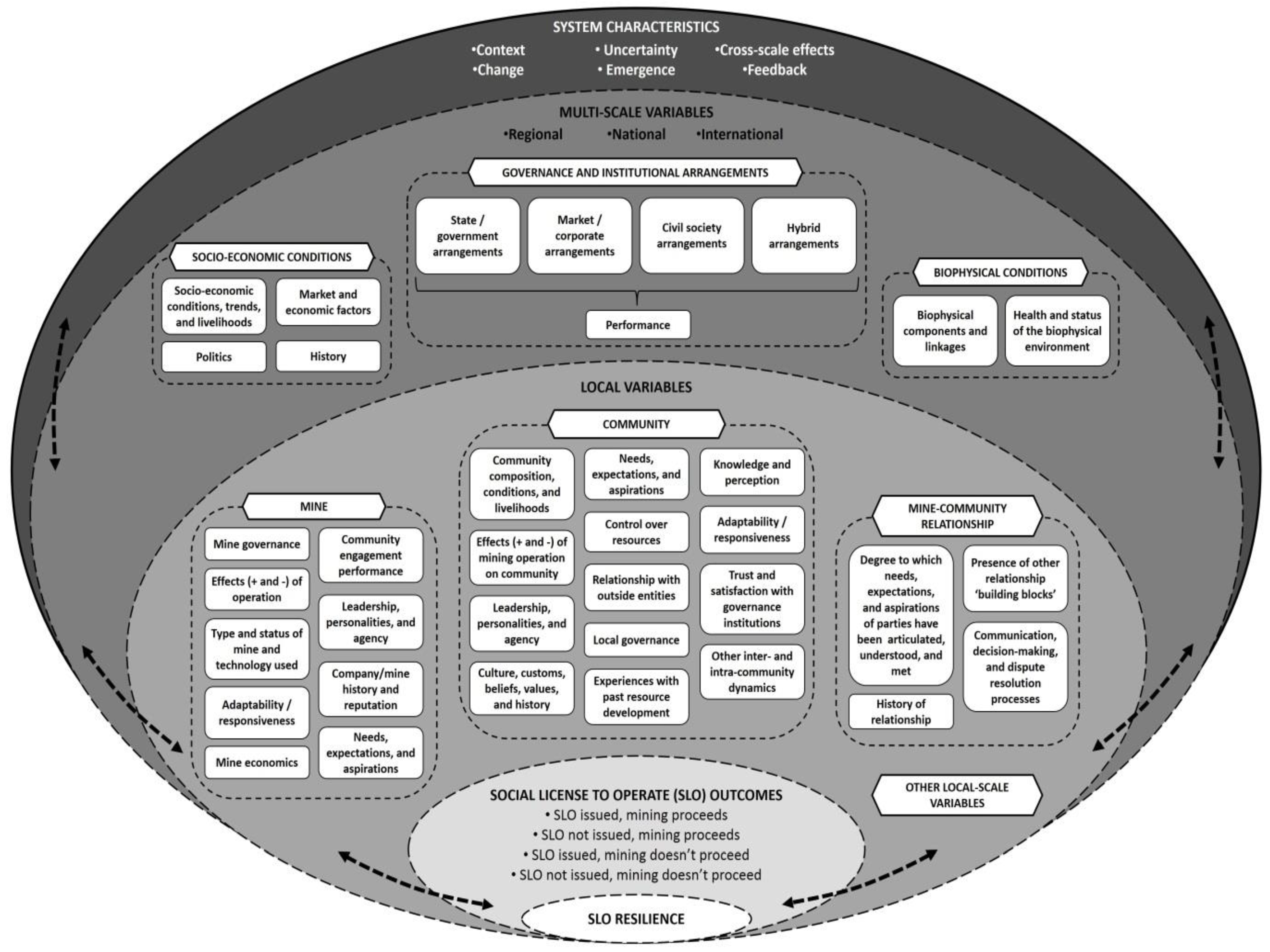

Figure 2 presents a theoretical framework for evaluating the Societal Licence to Operate (SLO) contributing factors and results in the mining industry.

Figure 2 contextualises a practical scenario applicable to the coal-mining environment in South Africa in the sense that coal-mining companies operate within multi-scale variables (governance issues) such as regional. An example is regional (Mpumalanga), national (South African national government level) and international (e.g., global coal mining) requirements. This filters into governance and institutional arrangements. Socio-economic conditions indicate the livelihoods of the local communities in which these coal-mining companies operate and the political environment thereof, market, and history of such coal-mining activities. An example of a biophysical condition is the health status of the environment in which these coal-mining activities occur.

The LOCAL VARIABLES section in

Figure 2 specifies coal-mine relations in terms of how these coal mines are administered; how they interact with the local communities; their reputation; and community aspirations of expectations. For instance, a community in Lephalale or Emalahleni might expect the local coal mining companies to employ or give preference to local people instead of people from other provinces even if the local people are not sufficiently skilled, thereby creating role conflict. Furthermore, this might affect the reputation of the local coal mining companies. Similarly, community variables may include community needs, conditions, knowledge, perception, and local control. Mine-community relationships are significant in the sense that the degree to which needs and expectations are met may determine the level of trust and engagement (reputational image). This is consistent with the argument in [

34], claiming that factors influencing EMA success such as EMA adoption, EMA implementation, business corporate strategy, business plan, government legislation/policy, environmental sustainability, and financial resources may have an effect on business reputational image; net profit; business sustainability and trust by society; business growth; and EMA compliance.

The preceding factors lead to SLO outcomes such as the issuance or non-issuance of SLO proceeds for coal-mining companies. Lastly, these factors and other local scale variables (

Figure 2) could well lead to SLO resilience by the local communities. It should be noted that this process is iterative in nature [

33]. Although this framework has been developed for the South African coal-mining environment, it does not directly address the important aspect of an information framework to facilitate cost saving of environmental impacts specifically for the coal-mining industry in South Africa.

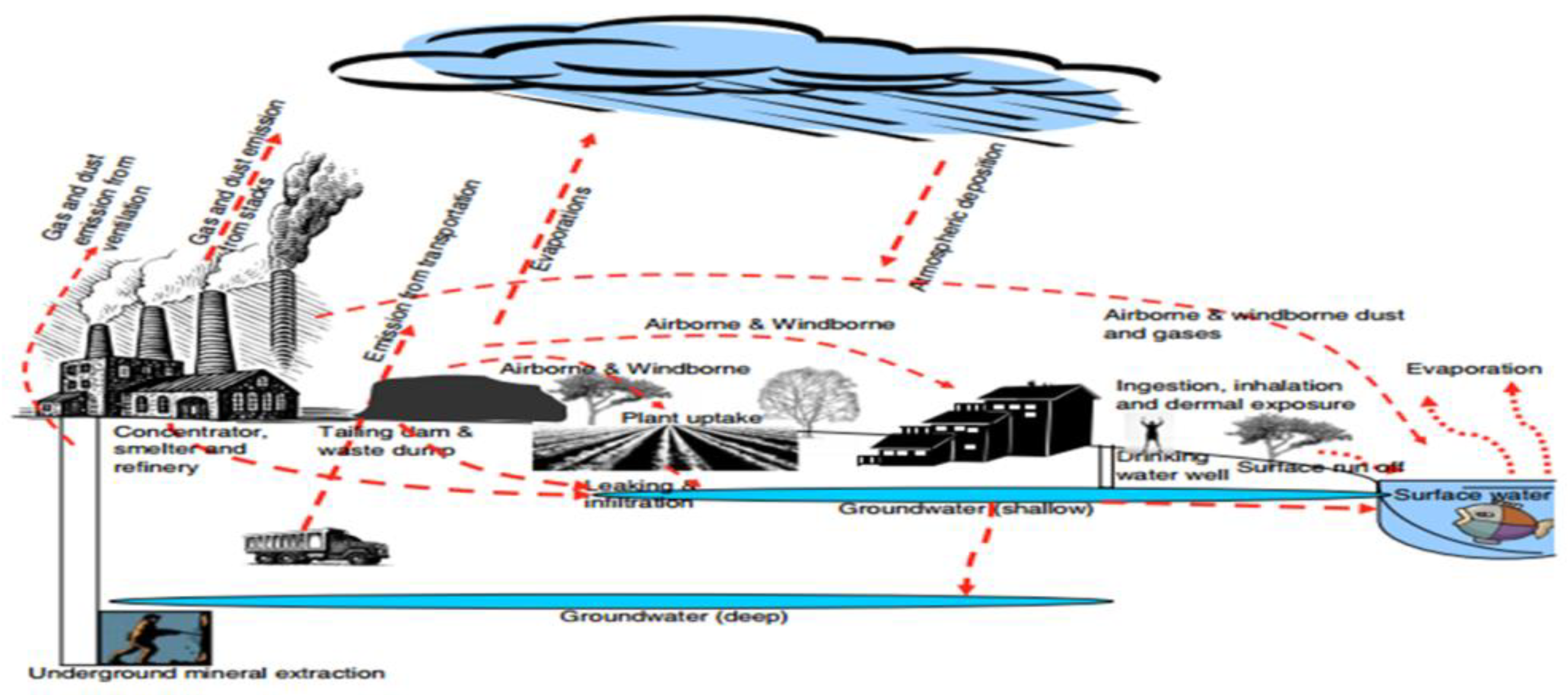

2.5. A conceptual Model for Coal Mining Operations and Its Environmental Impacts

Human and environmental receptors are highly sensitive to the discharge of chemical affluences due to the excavating activities. Repetitive counteractive verification and controlling of risk are fundamental for directing the focus and resources on the potentially utmost destructive risks, identified through stressful evaluation of risk [

11]. Since coal mining is a complex operation, proper risk management should be taken into account by coal-mining companies.

Figure 3 demonstrates the conceptual model of coal-mining operations.

The discussions in

Section 2.5 and 2.6 above answer the second research question, namely: Which frameworks exist to facilitate cost saving of environmental impacts for the coal mining industry? (RQ2)

Section 2.6–2.8 below address research question 3 (RQ3).

2.6. Defining Material Flow Cost Accounting (MFCA) in the Perspective of EMA

In order to comprehend MFCA, its origin and background ought to be explored. MFCA as it later appeared in the International Organization for Standardization, the ISO 14051 standard emerged of national significance regarding projects of conservational nature in fabric companies in Kunert in Southern Germany during the late 1980s and the early 1990s [

35]. The author of [

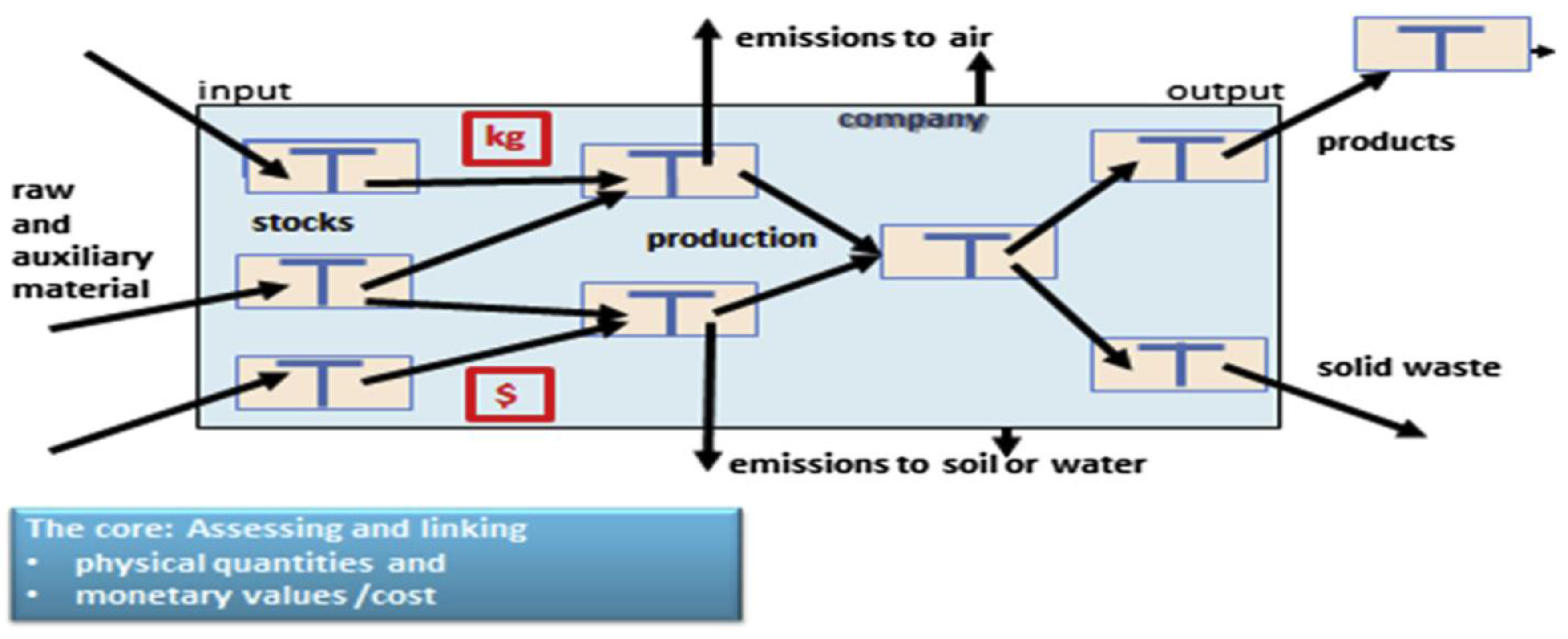

36] describes MFCA as a means for measuring the movements of materials inventories in the lines of production in both physical and financial units. MFCA as the main tool of EMA endorses an improved transparent materials usage based on the increase of a material flow that captures and calculates the input and output of material inventories amongst companies in both physical and monetary terms. MFCA identifies quantities of each material and its costs (including material, processing and waste treatment costs).

Figure 4 demonstrates that the physical quantities may be considered under PEMA and the monetary values as MEMA. This is due to the fact that purchased physical units or inventories are needed as inputs to the production process, leading to products that may be converted into cash to generate revenue (profit). The framework presented in

Figure 4 is applicable to the coal-mining companies; subsequently, they should be prudent in dealing with emissions to air; soil and water; and solid- and liquid waste. This framework demonstrates the operational process, making a start at addressing the need for a cost saving information framework for coal-mining companies in South Africa.

According to the author of [

37], MFCA as a tool of EMA provides a positive prospect for the accountants to collect information relating to the amount of waste generated through the production processes over and above those made available by conservative accounting structures. Waste produced by companies affects both overheads and the atmosphere in many ways for instance lost earnings through an amalgamation of lost resources and expenses associated with the disposal of such materials. Furthermore, the author of [

38] suggests MFCA may be observed as a methodology that has been directly and ultimately predisposed from numerous standpoints. The flows of material and the environmental bearing of dematerialisation have acknowledged consideration from conservational economics and cleaner production (CP) in addition to the field of managerial accounting.

With the ecological management issues of the 1990s, the matter of decreasing operative resources and input of energy was well thought-out as a mutual objective of monetary and ecological benefits. Initially, methods based on flow cost accounting were applied. This approach sought to compute and assess the flow of energy and material of a certain definite production line, firstly as a mass (in kilograms) and linking these to current cost accounting. Furthermore, this led to the development of residual material cost accounting that embraced the same method meant to compute the costs accrued in the remaining materials emanating from the manufacturing process. This also functioned based on the measures stated in kilograms. Further to the disposal expenses, the material residual expenses consist of the value of material resultant from the acquisition of unprocessed supplies, storing charges, outlays associated with the management of residual materials and overheads incurred in the protection of the environment [

39].

According to [

23] materials flows are recorded in kilograms through an input-output inquiry which is the foundation of conservational performance developments and for measuring the quantities and expenses relating to non-product output (NPO). The confines of the system may be at strategic level and may be subdivided into different sites, cost centres, procedures, and commodity lines in case of manufacturing companies. The balance in the flow of material is a calculation based on the assumption that whatever enters should also exit, or must be put away. In terms of the balance regarding the flow of materials, statistics for the utilised resources and the subsequent quantities of product, discarded material and emissions should be indicated. All substances are assessed in physical units in form of mass (Kg, tonnes) or energy (MJ, kWh). The procured input is validated with the manufactured quantities including the resultant unwanted materials and discharges. The objective is to financially and ecologically advance the productivity of managing material.

Contrary to conventional cost accounting methods, flow cost accounting and the remaining resource costs are grounded on the mass system that is expressed (Kgs) and the outcomes are articulated in financial terms (e.g., US

$ or ZAR). These two methodologies assign a cost element to the outstanding supplies of a manufacturing line hence recognising the remaining resources as a further charge per item [

39].

2.7. Benefits of MFCA

MFCA was assessed at Canon, a Japanese company on the production of their lens with special emphasis on the efficiency of their production lines regarding the crushing procedure. Conventional accounting indicated a 1% loss on faulty products. Almost 32% of the process expenses might be assigned to overheads of material. As a result, having successfully implemented MFCA, the methodology was embraced at the 17 Canon production locations in Japan and overseas bringing about in an overall saving of US

$51 million in the period 2004 and 2012. These savings were attributed to the competent use of resources leading to enhanced economic and conservational performance. The study further revealed that amid 20% and 30% of costs were essentially non-product output costs. MFCA facilitated the businesses to detect loss of materials that were up to that time concealed in their production practices [

40].

Eco-efficiency can be regarded as an extent that combines information relating to both financial and physical aspects about the green performance of companies [

41]. A provisional standard and guidelines in Japan articulate that eco-friendly data is an indispensable pointer and have a duty to be developed by an EMA system and integrated into company financial statements for reporting purposes regarding conservational matters.

In Indonesia, the authors of [

42] established that for the country’s cement industry, they could comprehend the significance of encouraging industrial symbiosis at the far-reaching level through utilising the process of material flow analysis (MFA), life cycle analysis (LCA), and MFCA in a cement factory. In a case study exploring the application of MFCA in the JBC food company in the Philippines [

43] ascertained that the MFCA approach revealed that about 10% of total production costs were caused by material losses. Peanut skin (6.3%) and rotten peanuts (2.4%) in boiling and peeling contributed most to these avoidable costs, followed by broken peanuts (0.8%) in cooling and selecting processes.

Taking into account comparative benefits over current practices and reliability with prevailing objectives of the company, it was established that ISO 14051 as a regulation standard, by combining financial as well as statistics of a physical nature as a basis for proficient actions, was possibly to encourage acceptance by executives and to fast-track the dispersal of MFCA in a profitable way. Companies conversant with similar ISO excellence, ecological management principles, and related technology may decrease the level of complication and also affluence administrators into implementing MFCA with its prospective for progressive development in eco-friendly and financial enactment [

44].

Furthermore, the author of [

45] ascertained that when companies are confronted by diminishing natural resources, they ought to considerably advance their material innovativeness. In order to achieve a proficient use of natural resources, MFCA is an aiding tool. Nevertheless, in order to attain resource efficiency as one of the major objectives, businesses should bind themselves from corporate level. This commitment should filter down to all operational levels through the implementation of management control systems (MCS). As a result, businesses must consider applying MFCA as a tool to cut cost and to eliminate unnecessary waste.

2.8. Life Cycle Cost (LCC) Analysis

LCC being a set of systematic tools that belongs to a group of the life cycle methodologies is defined as a technique of computing all costs relating to the merchandise (consisting both goods and services) generated through its life span. Life cycle processes are the tools, programmes and procedures that facilitate decision-making with regard to the life cycle of products. LCC is sometimes utilised for decision-making regarding product design, development, and procurement of these products as well as any processes, activities, and public policies related to them [

46]. Furthermore, the author of [

47] posits that the LCC method could incorporate prevailing monetary data such as cost information that indicates the metrics of life cycle methodologies. LCC involves the benefits and costs that someone has invested, for example, the amount that the manufacturer, transporter, customer, or any other directly or indirectly involved shareholder invested.

Several outdated cost-accounting structures lead to inappropriate investment judgements regarding environmentally friendly overheads. The key challenge is that destruction and costs associated with reconditioning fall outside the periphery of the outdated accounting system. Therefore, LCC has been advocated to resolve this challenge. On the other hand, this might not be a suitable solution since LCC was traditionally not created in a conservational perspective. In a traditional point of view, LCC was considered as a form of investment calculus utilised as a means to classify various investment options. Another objection relates to the boundaries of the LCC system in that the major variance between traditional investment calculus and LCC is that the LCC method has a broader life cycle standpoint. This is due to the fact that it does not only contemplate investment costs, but also considers operational costs during the expected life span of a product. It is imperative to highlight that an outdated LCC does not turn into an eco-friendly accounting instrument due to the fact that it encompasses the words ‘life cycle’ [

48].

In a study enquiring into integrating LCC and LCA using extended MFA, the author of [

49] argues that the scope of LCC entails specific financial issues directly or indirectly triggered by the product process. This includes the input of raw materials based on the procedures from upstream that are vital in comprehending the product. All the expenses associated in each stage of the life cycle of the product should be included in the final pricing of the services or products as part of the procurement costs for the next buyer. This implies that expenses and risks incurred on the upstream processes are then passed from one actor to another. In the same context, all the downstream effects of financial nature must be indicated by remaining (residual) amounts.

LCC is furthermore, considered as a means for assessing short-term decisions on whether to invest and for aiding long-term decision-making at corporate level [

50]. Specifically, LCC prides itself for reasonable valuations investments that are complicated, for instance, investment decisions regarding construction projects or procurement of capital equipment. In assessing similar projects, LCC can thus be recognised as the total of actual investment and the current value of recovery (salvage) which can in some way be the transactions price at the end of the actual period. In a study enquiring into the application of an LCC methodology in assessing the quality of food produced in Italy, [

51] established that LCC may be a convenient logical tool of expediency in creating and controlling investments. The use of the LCC model has largely been restrained to the scrutiny of the utilisation of costs during the life cycle of a product.

There may be hidden costs incurred by coal-mining companies as discussed next.

2.9. Hidden Costs That May Be Incurred by Coal-Mining Companies

In classifying conservational costs, EA vocabulary utilises phrases such as ‘full’, ‘total’, ‘true’ and ‘life cycle’ to accentuate that the scope of the traditional methods was not complete as it disregarded essential environmental costs (and possible cost savings and profits). Most of the environmental costs are listed and accordingly classified in this section.

The United States (US) environmental protection agency [

52] argues that exposing and distinguishing ecological outlays relating to the merchandise, procedure, and structure are crucial for taking effective decisions. Accomplishing these objectives as decreasing green costs, increasing profits, and improving conservational performance necessitates paying consideration to recent, forthcoming, and probable environmentally friendly overheads. How a business delineates ecological expenses is subject to how it anticipates utilising the information for example, allocation of expenses; capital planning; design of a product; or other relevant decisions that may be considered by management. It is sometimes difficult to classify costs for instance, determining of the cost is conservational or partly environmental (grey zone). Whether the expense is eco-friendly may not be important, however, the aim is to make certain that appropriate overheads receive fitting consideration.

Some researchers, e.g., the authors of [

53], argue that ‘environmental cost’ is sometimes defined very narrowly as being expenditures on pollution control equipment that are installed only for environmental reasons. In other cases, it has a broader definition which incorporates expenditure on areas such as energy efficiency which might well have been undertaken more for commercial than for environmental reasons. This is because of increasing difficulty of separating business costs from environmental costs as environmental considerations are built into mainstream investment decisions. Sometimes the usage also includes the notion of opportunity costs, that is, forgone income and other benefits that might have resulted from alternative courses of action to those that are actually pursued. Calculations of environmental benefits often turn to be primarily composed of avoided costs, based on future projections of regulatory or other trends.

Table 1 depicts the examples of environmental costs from the literature that may be incurred by coal-mining companies.

2.10. Guidelines of Global Reporting Initiative (GRI)

The global GRI (Global Reporting Initiative) promotes sustainability reporting on company activities, aimed at sustaining company operations as well as the global economy. The authors of [

54,

55] recommend standard reporting templates, layouts and formats to adhere to the GRI initiative. Their guidelines promote a scenario whereby (amongst other) coal-mining companies report their sustainability issues so as to add value in a worldwide viable economy. GRI permits businesses such as coal-mining companies to account for their financial- in addition to ecological responsibility. Similarly, mining companies should divulge their conservational effects in deliberation of the South African NEMA Act, 1998 as allied to the GRI sustainability criterions.

The author of [

55] defines no fewer than thirty (30) environmental and performance indicators for the mining- and metals industry. Amongst these, indicators 8–10 regulate water usage while guidelines 16–25 address emissions, effluents and waste. Naturally, these are very (coal-) mining specific as discussed previously in our work. Linking to these are also social performance indicators, notably indicators for Societal aspects and Product Responsibility. Clearly all these apply to the coal-mining industry which consumes large quantities of water, and generates volumes of emissions and waste.

Even though official disclosure is supportive through the coal-mining company monetary statements, GRI suggests that mining companies should reveal lists of shareholders with whom they are involved; their methodologies to engaging with these investors; as well as the approaches of such interactions. All these are aimed at South African coal-mining companies aligning to international sustainable ingenuities and to monitor CSRx aspects as discussed in

Section 2.1.

3. Research Methodology

This article’s research methodology follows the Research Onion of [

56]. The outmost layer of the onion is the philosophy that has two major components, namely, ontology and epistemology. Ontology is a systematic philosophy, analysing the development of an information framework for facilitating cost saving of environmental impacts in the coal-mining industry in South Africa. Hence, an ontological philosophy was used in this study. Looking towards the inner layers, an

interpretivist philosophy was followed as the researchers interpreted the findings and recommendations in the literature, as well as existing frameworks. The research approach is

inductive starting at specifics in the literature and working towards a conceptual framework, hence our strategy is a comprehensive literature

survey. A

qualitative choice was followed through a rigorous analysis of the available literature, which included scholarly material and mining magazines. Looking ahead, a qualitative survey among stakeholders in industry to validate our framework developed will be done in a next, 2nd phase of the research. Our time horizon as per the onion may be classified as being

cross sectional since the research was undertaken over a shorter period of time as is normally associated with a longitudinal study (e.g., observing human development from the infant stage to senior citizen). At the innermost layer of the onion, our techniques and procedures of data collection and analysis were through scholarly literature followed by

conceptual analyses and framework building.

4. Discussion and Findings

The review of existing literature indicated there are no easy or simple solutions to the environmental problems and the challenges facing modern society, hence there may never be scientific certainty or consensus on how these challenges ought to be addressed. In particular the coal-mining industry brings about a number of challenges. Some of the key environmental challenges elicited include:

water pollution,

sterilised land that may never be used for agricultural purposes or building,

underground coal fires,

AMD,

human diseases (due to air pollution and polluted water),

effects on the flora and fauna.

Existing frameworks to govern parts of the (coal) mining industry have been presented, yet none of these comprehensively address the aspects elicited in this work. Subsequently, the researchers postulated above that an information framework to facilitate cost savings of environmental impacts should, therefore, be developed within the context of EMA. The discussion on EMA established that there are two branches of EMA namely MEMA (a monetary part) and PEMA (a physical part). The analysis of the determinants of EMA adoption indicated that in most instances, companies adopt EMA due to regulatory requirements, pressure from non-governmental companies, sociological obligations, and stakeholder concerns.

A discussion on the theoretical framework for evaluating determinants of SLO (refer sub-

Section 2.4) and outcomes within the context of the coal-mining industry demonstrated that key variables such as systematic characteristics; governance and institutional provisions; socio-economic settings; biophysical circumstances; local variables and SLOs are applicable to the South African coal-mining sector. The discussion on the conceptual model for coal-mining operations depicted that although coal-mining operations may generate profit for shareholders, these operations may also have side effects. In order to address these challenges, MFCA was suggested to be one of the major tools of EMA as it encourages and improves transparency of material usage through the expansion of the flow of materials that also traces and computes the flows and inventories of materials within the coal-mining industry in physical and financial terms. The benefits of MFCA showed that the effective use of input materials may reduce the volume of waste concealed in the production process therefore create revenue. Furthermore, LCC as a technique of computing the overall price of production (encompassing both merchandises and services) and being a systematic instrument belonging to a cluster of the life cycle methodologies, could be utilised in cost reduction.

Lastly, a discussion was conducted on the potentially hidden costs that may be incurred by coal-mining companies depicting a list of such relevant costs. However, the term ‘environmental’, is sometimes narrowly defined as expenditures on pollution control equipment that are installed only for environmental purposes. In other cases, it is broadly defined to include expenditure in areas such as energy efficiency that might have been undertaken mostly on commercial rather than environmental factors.

5. Findings and Discussion

The review of existing literature established that coal-mining operations add value to the GDP of the country, for instance in South Africa 80% of electricity is generated from coal which then powers the processing of other economic minerals such as gold mining which then adds value to the GDP due to revenue generated form exports. In contrast, reviewed literature showed that coal-mining operations have an effect on the environment such as leakage of chemical substances from mine dumps, contamination of water due to AMD, deformed landscapes, underground fires etc. In the same context, reviewed literature pointed out that coal-mining activities impact on humans by causing diseases such as pneumoconiosis, asthma, and hyperpigmentation (appearance that depicts patches or a flushed complexion).

Reviewed literature also demonstrated that the determinants of EMA adoption were similar in countries such as Australia wherein the adoption of EMA was motivated by social structural inspirations and company contextual encouragements. Similarly, the adoption of EMA in Malaysia was encouraged by sociological, institutional theory, normative as well as isomorphic. In contrast, the adoption of EMA in Zimbabwe was established to be as a result of environmental compliance and pressure from law enforcement agencies such as ZIMRA. However, in South Africa, reviewed literature indicates that the adoption of EMA is on a voluntary basis as per King III and IV Codes. The researchers postulate that when the employment EMA is adopted on a voluntary basis (as is the case in South Africa), ecological degradation will persist whilst coal-mining companies are improving their bottom line, hence focusing on profit and not saving the environment.

This is consistent with the assertion by [

34] who argued that factors influencing EMA success such as EMA adoption, EMA implementation, business corporate strategy, business plan, government legislation/policy, environmental sustainability, and financial resources may have an effect on business net profit; business growth; and EMA compliance.

The review of existing literature indicated that existing frameworks do not comprehensively address the mining challenges elicited in the literature. This is echoed by the author of [

1], suggesting that South Africa should develop an integrated policy and regulatory framework for its coal-mining industry. Subsequently, the researchers postulate the need for an information framework necessary for facilitating cost savings of environmental impacts for the coal-mining industry in South Africa, taking into account the aspects elicited in the literature survey.

Furthermore, the researchers postulate that the successful implementation of the proposed information framework will be dependent on whether it is integrated in the corporate strategy, vision and mission of the coal-mining companies. As much as the framework depicts clear and concise tolls such as ISO, MFCA, LCC and a green strategy, it will also be subject to whether the management of these coal-mining companies understand and have the know-how of successfully implementing and applying these tools.

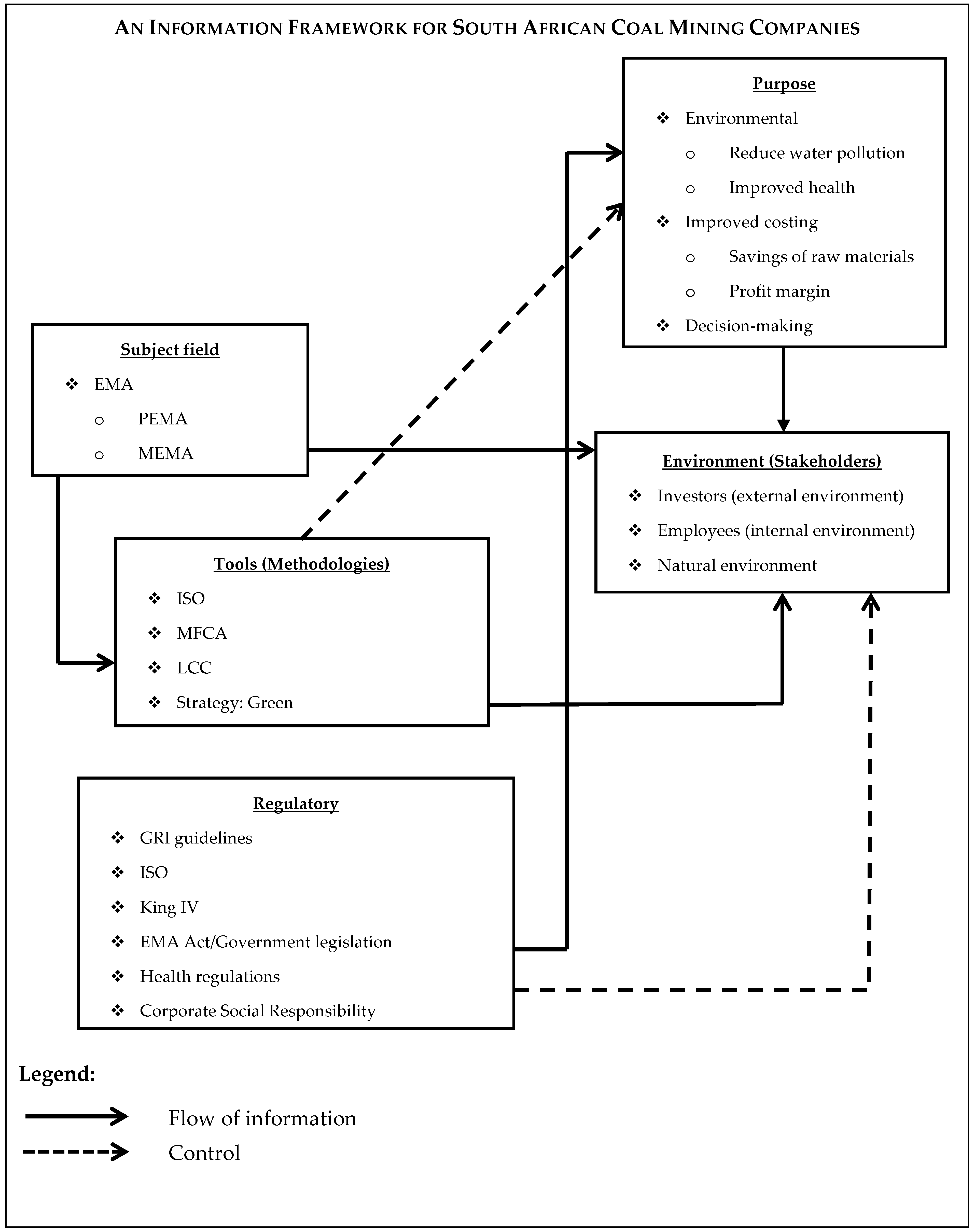

Such a conceptual information framework is presented in

Figure 5. It includes many of the environmental aspects mentioned before as well as the management accounting tools and techniques to facilitate cost savings for the industry. Regulatory aspects are acknowledged, notably [

36] which calls for the use of MFCA as part of EMA to promote increased transparency. Likewise the use of LCC as a decision-making tool [

46] has been included in the preliminary framework presented in

Figure 5. The conceptual information framework is in response to our objective (RO).

An Information Framework for South African Coal Mining Companies

Discussion

Our framework in

Figure 5 acknowledges PEMA (Physical Environmental Management Accounting) and MEMA (Monetary Environmental Management Accounting) as the main role players in the EMA arena. These two sub disciplines provide the information for various tools and techniques used in these, e.g., ISO, MFCA, etc. One of the drivers in this area is an adherence to green environmental aspects, a key objective of EMA. Naturally these tools and techniques control (determine) the purpose of this research, amongst other an improved environment and lower costing (higher profit) for the mining company. These involve decision-making aspects which is a rich source for further research. Various regulatory considerations provide information to guide the aforementioned purpose of the work. In this regard CSR (Corporate Social Responsibility) and GRI (Global Reporting Initiatives) are prominent role players in this group.

Ultimately the environment is the important variable which is what a large part of this research is about. Other variables as far as the mining company is concerned are the stakeholders (e.g., investors) and employees.

6. Conclusions and Future Work

The coal-mining industry offers lucrative business opportunities (profit), but challenges (environmental, health, etc.) as well. Opportunities include, amongst others the value added to a country’s GDP. For instance, South Africa generates about 240,300 gigawatt-hours of electricity on an annual basis. A greater portion of the produced electricity is for local consumption whilst about 12,000 gigawatt-hours are sold to neighbouring countries in the Southern African Development Community (SADC) which takes part in the Southern African power pool hence a contribution to the country’s GDP due to revenue generated form export [

57,

58]. Challenges include environmental impacts such as leakage of chemical substances from mine dumps, contamination of water due to AMD, deformed landscapes and underground fires that are evident in the Blesboklaagte region (

Figure 1). Furthermore, it was established that coal-mining activities impact on humans by causing diseases such as pneumoconiosis, asthma and hyperpigmentation.

PEMA and MEMA were established as the two branches of EMA. Key variables such as systematic characteristics, governance and institutional engagements, socio-economic conditions, biophysical settings, local variables and SLOs were major issues applicable to the South African coal mining sector and were noted as determinants to the SLO. MFCA and LCC within EMA were established as key tools to enhance efficiency in the production process and to reduce material waste in order to realise profit.

Key determinants of EMA adoption are different across countries, yet similar in some, and these include social structural inspirations and company contextual encouragements; institutional theory, normative- as well as isomorphic; environmental compliance and pressure from law enforcement agencies; whilst the adoption of EMA principles was established as being voluntary in South Africa. It was argued that in a voluntary scenario, ecological degradation may suffer whilst coal-mining companies are generating profits and not attending to the resultant environmental consequences.

The literature indicated a gap and a need to develop an information framework necessary for facilitating cost savings of environmental impacts for the coal-mining industry in South Africa. A preliminary and conceptual information framework incorporating these aspects was constructed.

Future work in this area may be carried out in a variety issues such as: The conceptual framework has to be enhanced in conjunction with the findings from a qualitative industry survey which the researchers intend to undertake in the near future. Knowledge management principles [

59] to strengthen the decision-making component of LCC in the framework have to be embedded. The final framework will be evaluated through a focus group as a follow-up survey.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}